1. Introduction

Access to energy-providing resources has been of geopolitical relevance throughout many decades. Moreover, the impact of the transport sector on climate change and energy-related greenhouse gas (GHG) emissions has become a major aspect of political discussion throughout the past years [

1]. Vehicles run by fossil fuels such as petroleum products such as gasoline, diesel fuel or fuel oil are not only criticized for mentioned global GHG emissions but also for causing noise and local air pollution, hampering people’s health, particularly in urban environments. Moreover, governments of several EU-member states criticized the car-related petrol and diesel demand for having created a strong dependence on foreign energy sources, depending on providers from non-EU and non-NATO countries [

2].

Primarily based on these reasons, national and local governments in Europe, but also in other parts of the world, have adopted a wide range of measures to increase the use of alternative fuel vehicles (herein abbreviated by “AFVs”). Already, in 2010, a total of 16 EU member states had implemented a tax and/or purchase incentive related to vehicle engine fuel types. Particularly throughout the past decade, a thorough transition towards the usage and production of renewable energies was incentivized by public and multinational institutions [

3].

In the EU, the patchwork of initiatives, legislation and incentives on a local and national level has been changing significantly within the 21st century and is expected to continue doing so in the near future [

4]. Already, by 2012, countries such as Denmark, France, Germany, Ireland, the Netherlands, Portugal and the UK had implemented their own initiatives [

5]. Meanwhile, Norway, which was seen as the benchmark in regard to AFV incentives, offered a combination of purchase tax exemption and local user benefits [

6]. Thus, such public incentives and other public interventions related to the currently seen “green mobility transition” have caused important economic costs [

4].

Since the end of World War II, the European automotive industry has generally shown a stable growth rate, only significantly hampered by the effects of the so-called “1973 oil crisis”, the latest financial crisis (“subprime crisis”) in the period from 2007 to 2009 as well as by the effects of the COVID-19 disease spread and consequent “economic lockdowns” in 2020 and 2021. As a consequence of the economic bust in 2008 and to “stabilize the economy”, several monetary policies (such as “quantitative easing”) and fiscal policies (including scrappage campaigns and other public incentives) were implemented by central banks and governments, ultimately causing further market distortions and unsustainable economic effects such as prolonged periods of low interest rates, financial volatility and a misallocation of resources [

7]. The popular explanation among politicians and journalists is that laissez-faire—often also disrespectfully referred to as “neo-liberal”—politics had deregulated the financial markets, which ultimately led to the financial crash [

8,

9]. While also considering the opposite hypothesis, that national governments and other institutions are the actual originators of the mentioned crisis, the author “tries to

connect the dots”, arguing that such interventionist policies, implemented with the aim to “stimulate investments and consumption”, ultimately lead to further unsustainable distortions in the automotive industry [

7,

10,

11]. Accordingly, this paper evaluates whether the recent sales increase in alternative fuel vehicles (AFVs) was mainly caused by the corresponding public incentives. In the affirmative case, the author considers that such market distortion will likely lead to a harmful misallocation of resources with another unsustainable market bubble.

This paper only focuses on vehicles that use one or more electric motors or traction motors for propulsion, including hybrid vehicles (H-EV). Thus, vehicles run on alcohols (such as ethanol and methanol) or methane (including natural gas and biogas), as well as biodiesel and synthetic fuels, are herein not considered as AFVs. In the recent specialized literature, the term “alternative fuel vehicles” (AFVs) generally refers to “Plug-in electric vehicles”, abbreviated by “PEVs”. A “PEV” is any vehicle that can be recharged via an external source of electricity, e.g., wall sockets. Thus, the abbreviation “PEV” can currently be seen as an umbrella term for electrified vehicles, which includes all-electric, or battery electric vehicles (B-EVs), as well as plug-in hybrid vehicles (PH-EVs). In addition, hybrid vehicles (H-EVs) are also included in this analysis on AFVs, as this technology must be seen as the “stepping stone” for alternative fuel concepts, which has paved the way for plug-in hybrid electric (PH-EVs) vehicles and battery electric vehicles (B-EVs). Thus, whereas hybrid vehicles (“H-EVs”) are herein considered AFVs, they do not belong to the group of “PEVs”.

To limit our research to a crucial period of time, this paper focuses on analyzing the timeframe from 2010 to 2018. In this perspective, the year 2010 is seen as the beginning of the post-financial crisis era (which was shaped by the filing for bankruptcy of Lehman Brothers Holdings Inc, General Motors filing for government-backed Chapter 11 reorganization, as well as by the different automotive scrappage campaigns launched by various governments to “protect the automotive sector and its employees” [

12,

13]. The year 2018 can be seen as a crucial tipping-point in regard to the mass-market breakthrough of AFVs, as according to the Norwegian Road Traffic Information (OFV), more than 50% of all new passenger car sales in Norway, which occurred in the second half of 2018, were “plug-in electric vehicles” (B-EVs + PH-EVs). Thus, 2018 must be seen as the year in which alternative fuel vehicles became “mainstream” products in at least one country belonging to the European Free Trade Association (EFTA). Accordingly, the automotive sector has seen significant changes within the past decade, strongly influenced by public incentives for alternative fuel vehicles and other public interventions.

Several studies indicate that there are crucial environmental, consumer fuel-saving and macroeconomic benefits [

14] associated with alternative fuel vehicles, which are said to exceed the costs of electric vehicle incentives [

15]. Moreover, it is expected that throughout the next decades, public incentives for AFVs can be reduced due to the ongoing optimization of these vehicle technologies, not only in regard to their production costs but also regarding their driving range, which will naturally increase their competitiveness [

16]. In addition, the author argues that it is likely that the recent “positive” public interventions to support AFV sales (e.g., tax exemptions for AFVs) will simply be replaced by “negative interventions”, such as further regulations and taxes on ICE vehicles, or even their entire ban from European roads. By doing so, public entities could further steer the transition towards the “electric revolution” without needing significant public budgets for long-term public AFV incentives. Meanwhile, public subsidies and tax reductions implemented for electric vehicles in several European markets were substantial throughout recent years [

1,

17]. Governments have increased this market growth through a combination of financial incentives, other incentives such as parking and lane access, as well as by supporting charging infrastructure, training/education and outreach activities [

16]. Consequently, in particular, in Norway and the Netherlands, incentives have helped to significantly reduce the total vehicle costs of PEVs [

18]. However, PEVs still face relevant barriers to adoption; barriers that are common to most new technologies include the lack of knowledge by potential adopters, a low consumer risk tolerance [

19,

20] and high initial production costs [

21].

It is also key for this research to look at the importance of a free price system, crucial to properly allocate resources since, on the contrary, governmental interventions on pricing via taxes and subsidies lead to a hampering market distortion [

22,

23].

The “electric car revolution” was mainly initiated by the launch of models such as Opel Ampera /Chevrolet Volt, the Nissan Leaf and Tesla’s Model S [

24]. Previous research related to AFVs has thoroughly analyzed the impact of fiscal incentives for AFV users [

2,

5,

6,

15] as well as of regulations directly affecting manufacturers [

25]. Throughout the past years, public entities on the EU, national and municipal levels have tried to promote alternative fuel vehicle technologies with different forms of fiscal and legal support. Meanwhile, a wide range of incentives and promotion actions exist which different national and even regional governments have adopted to increase the attractiveness of AFVs. These incentives have clearly increased the awareness of AFVs. This paper focuses on the four most relevant alternative fuel technologies within the period from 2010 to 2018, which are hybrid (H-EV) and plug-in hybrid (PH-EV) as well as “full-electric”/battery electric (B-EV) and fuel cell (FC-EV) engines. As indicated, hybrid vehicles (H-EVs) are also included in this analysis on AFVs, as this technology must be seen as the “door-opener” for plug-in hybrid electric (PH-EVs) vehicles and battery electric vehicles (B-EVs).

In the early 2020′s, Europe is still in the adoption phase of AFVs with a relatively low market share in most markets [

1,

4]. From a different perspective, one can positively highlight that particularly in certain north-western European countries, such as the Netherlands and Norway, sales volumes of AFVs have constantly been growing to advanced levels [

5,

6]. Interest in alternative fuel technologies also increased due to the so-called “(Volkswagen) diesel emission scandal” and the continuous approach by governments to reduce fine particulate and nitrogen oxide (NOx) emissions [

6]. It should critically be evaluated if public incentives could, in any case, be justified from an economic perspective or whether any form of public incentives is unsustainable, leading to harmful market distortion. To detect the actual price competitiveness of PEVs with traditional internal combustion engine (ICEs) vehicles, independently from any public support, “total cost of ownership” comparisons (TCO comparisons) of ICEs versus PEVs are considered, including all costs related to the vehicle ownership and usages, such as fuel costs and insurance costs, as well as repair, maintenance and service costs (RMS costs) [

2,

5,

17]. The author argued that in order to assure the long-term stability of the market, sustainability needs to be assured, and product distribution must primarily be based on actual customer demand, not on public incentives. The hypothesis is raised that in case such sustainability is not provided, mentioned fiscal interventionism to artificially boost vehicle sales will further distort the market, causing a new form of “bubble” that could ultimately lead to another severe crisis in the automotive sector.

2. Literature Review

In his book “1984”, Orwell ironically stated: “

The best books… are those that tell you what you know already.” [

26]. Thus, to provide a holistic overview of the latest research on the analyzed topics, a broad and intense literature review is seen as crucial. In regard to alternative fuel vehicles, several empirical studies on the sales evolution of AFVs and on consumer preferences for AFVs were published over the last decades [

2,

5,

6,

15,

17,

18,

19]. Even detailed comparisons of the individual public incentive models can be found. In 2003, for example, Canes finalized a study comparing the total lifecycle costs of equivalent hybrid and gasoline models of that time and detected that lifecycle costs for hybrid vehicles clearly exceeded those for equivalent non-hybrid vehicles at the corresponding fuel prices at the time of analyses [

27]. On the one hand, the author focuses on the recognized academic secondary literature related to macroeconomics, monetary policies and fiscal policies. Thus, a wide variety of books from different schools of thought, such as the Austrian School of economics, Keynesianism, monetarism, public choice economics, new institutionalist economics and the economics of governance, including the Bloomington school, were studied. On the other hand, this research also used academic papers related to the automotive industry, with special emphasis on the so-called “scrappage campaigns” in the early 21st century [

11,

12,

13] and public incentives for alternative fuel vehicles [

5,

6,

18]. The mentioned literature helped to properly evaluate the main research objectives, which are to evaluate the impact and effectiveness of public incentives for AFVs on the vehicle sales evolution in Europe and to illustrate the sustainability and market competitiveness of AFVs without public incentives [

1,

4,

5,

18,

24,

27].

According to Axsen et al., the main constraint to the commercialization of “Plug-in electric vehicles” (PEVs) was the limited energy storage, while the evolution of battery technology was limited by the trade-off between power, energy, longevity, cost and safety [

28]. Several studies confirm that governments have incentivized this market growth through a combination of financial incentives, other incentives such as parking and lane access, as well as by supporting charging infrastructure [

29]. Previous research related to AFVs thoroughly analyzed the impact of fiscal incentives for AFVs users [

2,

18,

30,

31] and of regulations directly affecting manufacturers [

32,

33]. In particular, in Norway and the Netherlands, public incentives were sufficiently high to increase the cost competitiveness of PEVs, for which these markets were analyzed in particular [

18,

34,

35]. Several other academic papers on the competitiveness of AFV technologies were also reviewed, particularly focusing on the most challenging aspects for EVs, such as the limited maximum driving speed, relatively long recharging times, high initial purchase prices [

36], still relatively low driving ranges [

28] and a limited network of recharging stations [

37]. The vehicle’s driving range and the need to recharge PEVs are generally seen as crucial factors, but only a very few studies actually distinguished between “longer and shorter” recharging times. Reference is also made to authors who strongly question any economic benefits of the recent incentives for AFVs [

4,

38]. The author of this paper also considered aspects of customer behavior modeling, referring to corresponding models such as the “diffusion of innovations model”, the “theory of planned behaviour”, as well as the “willingness to consider concept” [

17,

39,

40,

41].

4. Analysis of the AFV Market Evolution

Throughout the first decade of the 21st century, Western automotive markets were mainly shaped by those European and US-American automotive manufacturing companies that had already been in the market for several decades. These so-called original equipment manufacturers (“OEMs”) focused on the production of traditional internal combustion engine vehicles (ICE vehicles), mostly operating in a low margin business, with complex supply chains while pushing sales volumes, trying to assure economies of scale. Automotive OEMs focused on constantly updating the vehicles’ design as well as improving engine powertrains in regard to performance and consumption, but fierce competition and the mentioned low margins have kept most OEMs from focusing on courageous long-term planning with truly revolutionary product developments [

43]. Then, in 2012, Tesla Motors, Inc. introduced its Model S. The US-American company Tesla, founded in 2003, focused on the production and distribution of electric vehicles (B-EVs) with the declared purpose to support the transition from a mine-and-burn hydrocarbon economy towards a solar electric economy. At that time, only a few automotive OEMs, such as Nissan, Renault, Mitsubishi and General Motors, had started the mass production and selling of battery electric vehicles.

As indicated, in recent years, the impact of the transport sector on climate change and energy-related greenhouse gas (GHG) emissions became a major aspect of political discussion [

1,

28,

43]. Accordingly, vehicles run by fossil fuels such as petroleum products, i.e., gasoline, diesel fuel or fuel oil, have increasingly been criticized, not only for global GHG emissions but also for causing noise and local air pollution, hampering people’s health, in particular in urban environments [

43,

44]. Moreover, in particular, EU-member states criticize the car-related petrol and diesel demand for having created a strong dependence on foreign energy sources, depending on providers from non-EU and non-NATO countries [

2].

Based on these reasons, national and local governments in Europe, and also in other parts of the world, adopted a wide range of measures to increase the use of alternative fuel vehicles [

45]. From a neoclassical perspective, market inefficiency is an indication of “market failure” for which government intervention appears to be necessary to “readjust” the market. Regarding externalities, the neoclassical notion of market externalities elaborates on the concept of costs and benefits to society as a whole as well as on the expanded concept of “social efficiency” [

23].

Alternative fuel vehicles (AFVs) are vehicles that can be fuelled either partially or entirely by alternatives to fossil gasoline and diesel. The market of alternative fuel vehicles is comprised of battery electric vehicles (B-EVs), plug-in hybrid electric vehicles (PH-EVs) and hybrid electric vehicles (HEVs), as well as fuel-cell electric vehicles (FC-EVs). Thus, the author takes a closer look at these four main alternative fuel technologies, which have been most successful in Europe throughout the past years. B-EVs do not require gasoline at any point during their operation, relying purely upon electric battery power. PH-EVs, just like B-EVs, use a lithium-ion battery and run on an electric engine [

28]. However, PH-EVs will switch to the gasoline engine each time their electric battery runs low. In this research, these technologies are mostly combined under the term “alternative fuel vehicles” (AFVs) in comparison to the traditional internal combustion engine vehicles (ICEs). As indicated in several statistics, PH-EVs and B-EV are often combined and shown as PEVs (plug-in electric vehicles). Thus, particularly when looking at recent developments, reference is often made to the mentioned term “plug-in electric vehicle” (“PEVs”).

Accordingly, at the beginning of the second decade of the 21st century, with the launches of a large variety of battery electric vehicles (B-EVs) and plug-in hybrid electric vehicles (PH-EVs), the situation has significantly changed throughout the past 10 years. While by now, all major Western automotive OEMs have launched models with the corresponding engine AFV technologies, and several new (mainly Chinese) automotive companies are also entering the European market with competitive PEV models [

46].

Several aspects, such as vehicle prices, fuel prices and maintenance costs, as well as circulation, registration and luxury taxes for petrol and diesel vehicles, or alternatively sales tax waivers and income tax credits for alternative fuel vehicles (AFVs), can have a crucial impact on the success or disappearance of entire fuel type technologies [

43,

47]. The desire to reduce one’s own carbon footprint by using low-emission vehicles, and the often-provided usage benefits of AFVs, e.g., preferential urban parking space or the permission to use the bus and taxi lanes during rush hours, were relevant AFV purchase reasons [

24]. However, one significant difficulty in analyzing the effectiveness of AFV adoption by using time series data is to truly define the proper correlation between the specific independent (“public incentives”) and the dependent variable (“customer demand”), as the status and impact of several intervening, moderating and control variables has changed throughout the evaluated period of time. For example, public incentives for AFVs might have developed in line with other crucial changes such as an optimization of the recharging network, the optimization of the vehicles’ driving range and a general consciousness for environmental issues [

48].

4.1. Environmental Protection and the Rise of Public Incentives for AFVs

By the year 2007, more than 88% of all analyzed Spanish companies within the automotive industry had already defined their own internal quantitative objectives related to “environmental protection” [

49]. In the case of larger analyzed corporates (with more than 250 employees), even 96.6% had already defined such objectives. By the end of 2007, 76% of these companies had already implemented an internal corporate strategy on environmental protection, and even 81.3% had implemented a related certified management system such as ISO 14001 [

49]. These interesting numbers indicate that, far before significant public incentives for AFVs were implemented, entrepreneurs and managers within the automotive sector had already recognized the need to consider environmental concerns in the definition of future corporate priorities and strategies. The author intends to evaluate whether, as soon as AFV technologies had become a serious competitive alternative to ICEs for consumers, the market would have embraced such new technologies without any public interventionism.

Historically, public support for OEMs by providing public incentives (such as the former public scrappage campaigns and bailout packages) have differed between the individual countries, but the main purpose of these public interventions has generally been to “stabilize the economy while protecting workers” [

12,

13]. The author argues that in order to assure the long-term stability of the market, sustainability needs to be assured, and product distribution must primarily be based on actual customer demand, not on public incentives. Accordingly, this analysis emphasized the long-term importance of free prices [

50], crucial to properly allocate resources, since on the contrary, (long-term) governmental interventions on pricing via taxes and subsidies lead to malinvestments and market distortions [

51], which could ultimately cause a new crisis of the automotive sector [

1,

4]. Throughout the past years, public entities on the EU, national and municipal levels have tried to promote alternative fuel vehicle (herein abbreviated by “AFVs”) technologies with different forms of fiscal and legal support. Whereas previous public incentives were often justified with the official aim to “protect workers from unemployment”, the recent incentives for AFVs are being justified with the aim to “reduce air pollution, CO

2 emissions and global warming”. These incentives have clearly increased the awareness of AFVs and have overall led to a notable growth of the AFVs’ sales evolution [

2,

4,

17]. By December 2019, all EFTA member states and the UK combined accounted for 25% of all PEVs globally in use. Whereas in 2016, PEVs only had a market share of 1.3% of all new car registrations in the EFTA+UK region, the share rose to 3.6% in 2019 [

52].

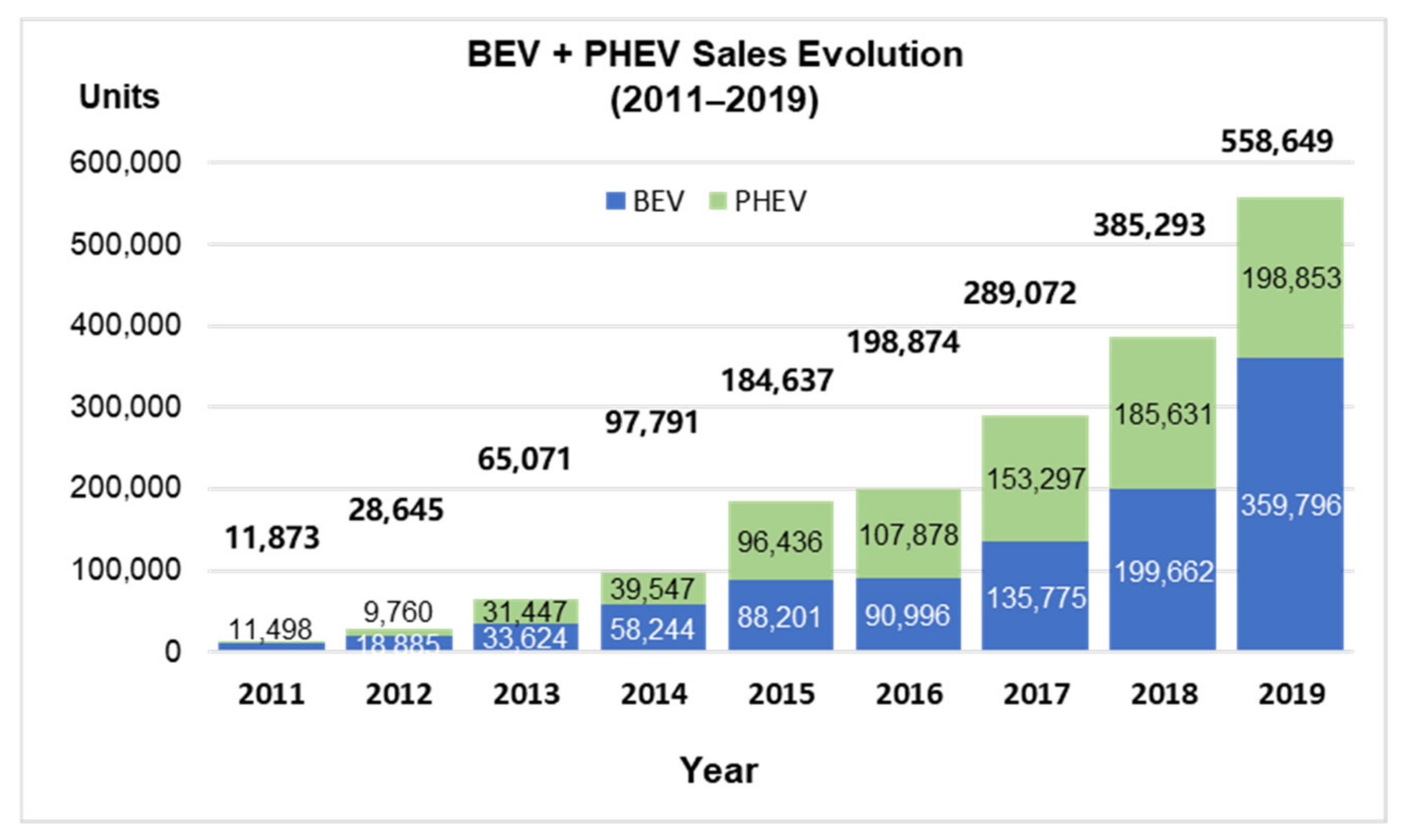

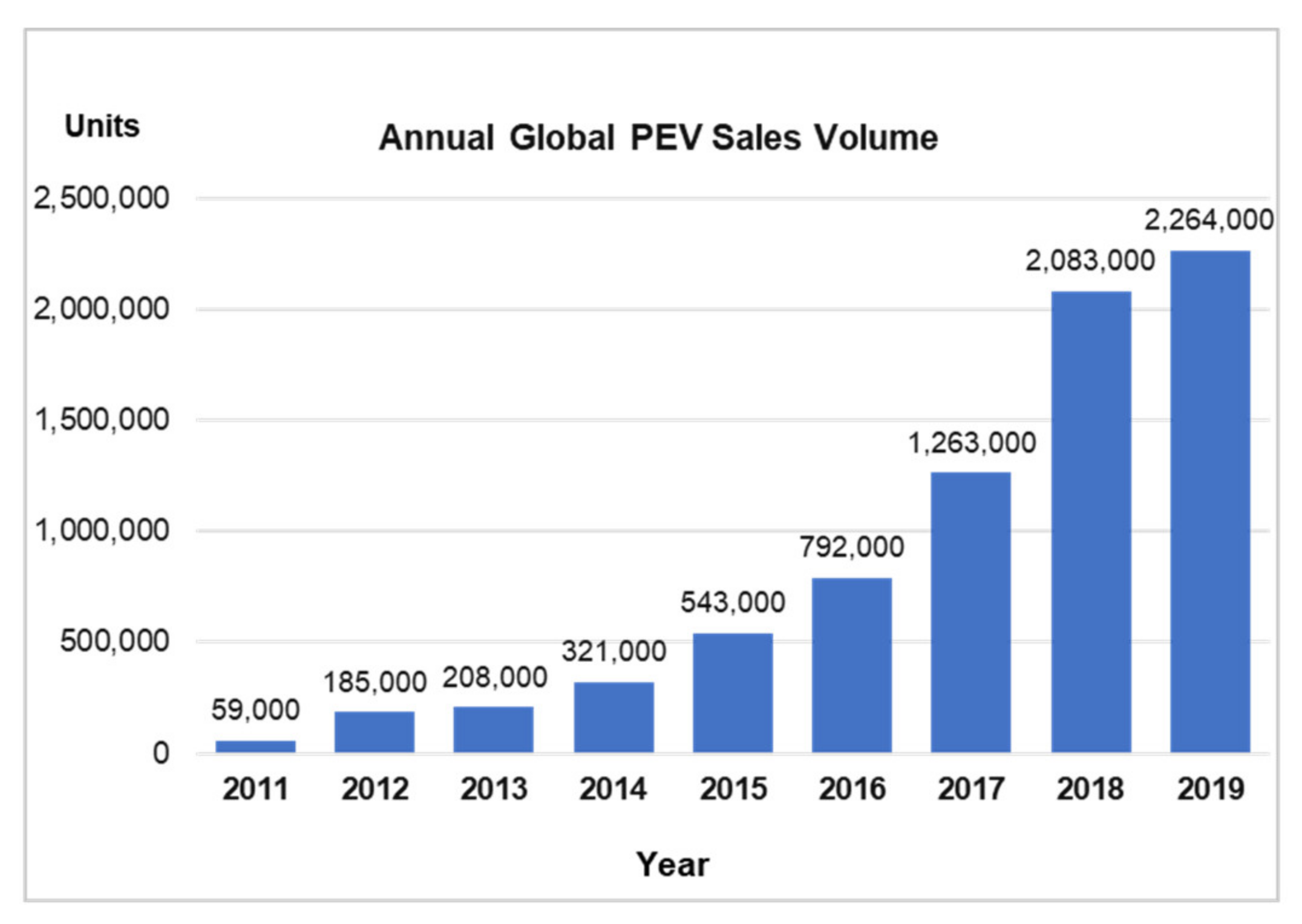

Figure 1 illustrates the notable increase in annual PEV sales in Europe (EFTA region and the UK) in the time period from 2011 to 2019.

The above chart shows the annual increase in vehicle registrations with a “full-electric” engine (B-EVs) or a plug-in hybrid technology (PH-EVs) within the EFTA region (including the UK). The public support for “AFVs” has differed between individual countries and often even between municipalities: meanwhile, the most common justifications for the increase in public incentives are to minimize the dependency on fossil fuels as well as to decrease greenhouse gas (GHG) emissions. Particularly in populated cities where mobility activities significantly contribute to generating negative externalities, the optimization of environmental sustainability in transport solutions requires new technologies, such as optimization of vehicle engines. Thus, the diffusion of AFVs (mainly PEVs) shall play a major role in reducing the environmental pollution. Around the world, policy-makers have intensified the implementation of new strategies in order to increase the market share of PEVs [

28,

53]. Several automotive experts define the currently available PEV technologies as superior to ICE from an environmental perspective and consider them as a key aspect towards the transition to a truly sustainable transportation system. Several frameworks and theoretical models were used to come to concrete conclusions. Up until the late 2010s, it was unclear whether PEVs would remain niche market products, only adopted by a small fraction of consumers, or whether they could truly become a mass product. Several papers written on AFV evaluated the influence of sociodemographic factors [

54] and the relevance of fuel consumption and tax incentives on the adoption decision [

55]. In addition, several researchers looked into attitudinal psychological factors such as moral values and environmental awareness [

24], while others primarily emphasized the required recharging infrastructure [

56]. Most of the mentioned literature shows that apart from the driving range and the actual vehicle costs, the public charging infrastructure has also been an important factor, although the detailed causalities cannot be precisely quantified. Thus, apart from the vehicle purchasing price, two main aspects considered by potential customers of B-EVs (and FC-EVs) were the status of the (public) recharging network as well as the actual recharging time for these vehicles [

28,

56]. Therefore, the continuous growth of B-EV sales will require further improvements in regard to battery technologies and a more extensive charging infrastructure. By the end of 2016, there were only 1403 public fast charging points in Germany, 523 fast chargers in Sweden, but already 1052 fast chargers in Norway [

17]. Most consumers were reluctant to switch to B-EVs as recharging infrastructures were limited in many regions, for which they have consequently preferred conventional ICE technologies (or PH-EVs, if heavily subsidized). The question of how much public charging infrastructure is needed cannot be precisely answered, as this will also strongly differ between countries and by region. First of all, a regular charging option, such as home or workplace charging, is considered crucial for the success of PEV in the early market phase [

56]. In this context, a significant difference can also be seen between most urban areas on the one hand and suburban and rural areas on the other hand. Consumers with their own garage or private parking space may rely on their personal charging infrastructure to ensure regular recharging, while most consumers living in inner-city areas may mostly rely on public charging infrastructure or privately-run recharging stations. Despite the high amount of academic research papers written on the AFV sales evolution, they mostly came to rather unprecise and often contradicting findings on the concrete effectiveness of corresponding government incentives [

28,

44]. On the one hand, in several markets, such as the Netherlands, Scandinavia and several metropolitan areas such as London and Paris, AFVs (including hybrid vehicles) gained notable market shares throughout the second decade of the 21st century. On the other hand, and in particular, in most southern and eastern EU countries, the total number of AFVs in usage is still relatively low and rather disappointing. Thus, despite the proliferation of such incentive programs, their efficacy in actually leading to significant adoption of AFVs is unclear. Particularly PEVs are still struggling due to their high initial purchase prices, still relatively low driving ranges and a limited network of recharging stations [

28,

36]. These disadvantages restrained many consumers from adopting the mentioned new technologies [

2].

To detect the actual price competitiveness of AFVs with traditional internal combustion engine vehicles, independently from any public support, one must consider “total cost of ownership” comparisons (TCO comparisons) of ICEs versus PEVs, including all costs related to the vehicle ownership and usage, such as fuel costs and insurance costs as well as repair, maintenance and service costs (RMS costs). Within this paper, the author raised the hypothesis that to assure a long-term and pan-European success of mentioned PEV technologies, sustainability needs to be assured, and product distribution must primarily be based on the actual customer demand, not on public incentives. Thus, it is argued that without strong public interventionism, the recently seen sales increase in AFVs/PEVs would not have been possible. A natural shift of the European mass market towards alternative fuel technologies could only occur if price competitiveness were given versus ICEs, which as of today is not the case. However, the seen significant public interventionism also led OEMs to tremendous investments into the optimization of AFV/PEV technologies [

44]. It is argued by several automotive experts that, if significant public interventions are held up until the year 2024/2025, PEVs technologies can reach price competitiveness with ICEs [

42], for which as of 2025, public interventions (and the corresponding public incentives for PEVs) could be reduced, whereas demand for PEVs could “naturally” continue growing. It is likely that the recent “positive” public interventions to support AFV sales (e.g., tax exemptions) will simply be replaced by “negative interventions”, such as further regulations and taxes on ICE vehicles. By doing so, public entities can further steer the transition towards the “electric revolution” without needing significant public budgets for long-term public AFV incentives.

4.2. Customer Behaviour and Its Impact on AFV Adaptation

The author argues that properly understanding consumer behavior is crucial to design policies that could notably increase the uptake of new products and technologies. Innovation can be seen as the process of transforming opportunities into new ideas, putting them into practice [

57]. The theory of planned behavior (TPB) by Ajzen links people’s individual beliefs and behavior. Ajzen argues that attitude towards behavior, subjective norms, as well as perceived behavioral control together, shape an individual’s behavior [

58]. Sovacool and Hirsh (2009) stated that the majority of Western consumers while making choices, stick to “notions of traditions and familiarity” rather than look for new technologies [

45].

One crucial aspect that has limited the success of AFVs is the uncertainty about the vehicles’ total cost of ownership (TCO) as residual values (RVs) for these new technology vehicles could hardly be predicted. Thus, from a financial perspective, one major challenge to the success of AFVs, in particular for B-EVs and FC-EVs, is the uncertainty about the vehicles’ actual total costs. Due to the significant progress in the AFV sector, including new engine technologies, new model launches and also a continuously high dependence on public interventionism, it was extremely challenging to forecast the residual value (“RV”) of B-EVs, PH-EVs and FC-EVs. The total cost of ownership is also a key aspect in any corporate fleet tender, as it is ultimately not the new-car transaction price but its TCO, which defines the cost competitiveness of a vehicle model versus its competitors [

59].

On the other hand, several analyses indicate that already by 2012, the development of social connotation of B-EV and PH-EV technologies had shown some impressive evolution: social connotative attributes, such as “environmental-friendly” and “high-tech”, ideally combining the reduction in CO

2 and NOx emissions with “connectivity & infotainment”, started to play a more significant role in the development of new vehicle models and engine technologies [

60].

As indicated, customers need to see an actual benefit in using the new technology, and manufacturers need to detect a benefit in producing the new good [

61]. However, other researchers state that the main constraint to the commercialization of PEVs was the limited energy storage, while the evolution of battery technology was limited by the trade-off between power, energy, longevity, cost and safety [

28,

62]. The durability of a battery depends on a number of factors such as the climate, the frequency of charging and the amount of energy involved in the charging process. Despite the general good intentions by most consumers to “help protecting the environment”, fiscal incentives—if sufficiently high to offset cost differences between AFVs and conventional vehicles—are still the most important reason to switch to green technologies, according to a survey among Norwegian battery electric-vehicle (B-EVs) drivers [

34].

4.3. Relevance of Fiscal Policies on the Competitiveness of AFVs

Thus, even if there are several psychologic/emotional as well as cultural/sociologic aspects that certainly influence customer decisions, the author concludes that ultimately, customers intend to take rather rational decisions when purchasing a vehicle, mainly based on a “value-for-money calculation”. Previous research has already evaluated the impact of fiscal incentives for AFV users as well as of regulations directly affecting manufacturers [

1,

5,

17,

18,

25,

27,

30]. A vast majority of corresponding studies concluded that financial, technical and public-infrastructure attributes are the key aspects in regard to AFV adoption. Thus, the sales evolution of AFVs must mainly be evaluated from the perspective of customers’ financial benefits/disadvantages. Additionally, this is mainly driven by the question of whether AFVs were able to compete with traditional ICE vehicles in regard to their total cost of ownership (TCOs). Apart from official EU fleet emission regulatory targets and member-state funded R&D projects, the “European Green Vehicle Initiative” was also launched in 2008 in the EU as a public–private partnership, which funded several activities under the EU framework program for research and innovation. In 2017, there were already more than 300 different R&D programs ongoing in the EU related to technological improvements such as energy storage and control devices, with a total budget of nearly EUR 3 billion, co-founded by the EU and the corresponding member states [

56]. Most of the mentioned automotive experts argue that, since the first decade of the 21st century, Europe can be found in the adoption phase of electric vehicles, with initially rather low but constantly growing sales rates. As indicated, this research focused on the four main technologies that have been the most relevant ones: hybrid electric and plug-in hybrid electric vehicles and battery electric vehicles and their “sub-category” of fuel cell electric vehicles. (fuel cell electric vehicles usually use a fuel cell, instead of a battery, to power their on-board electric motor, generally using oxygen from the air and compressed hydrogen. They only emit water and heat and might be seen as the most future-oriented technology if the needed recharging network can be developed.). Special attention needs to be paid to two European markets—Norway and the Netherlands—where significant public incentives were implemented at a very early stage to “‘ promote’ Alternative Fuel Vehicles (AFVs)”. Backed by different sorts of public interventions, a notable market change has taken place in these two countries, shifting the market from ICE to AFV engines [

5,

6,

18,

52].

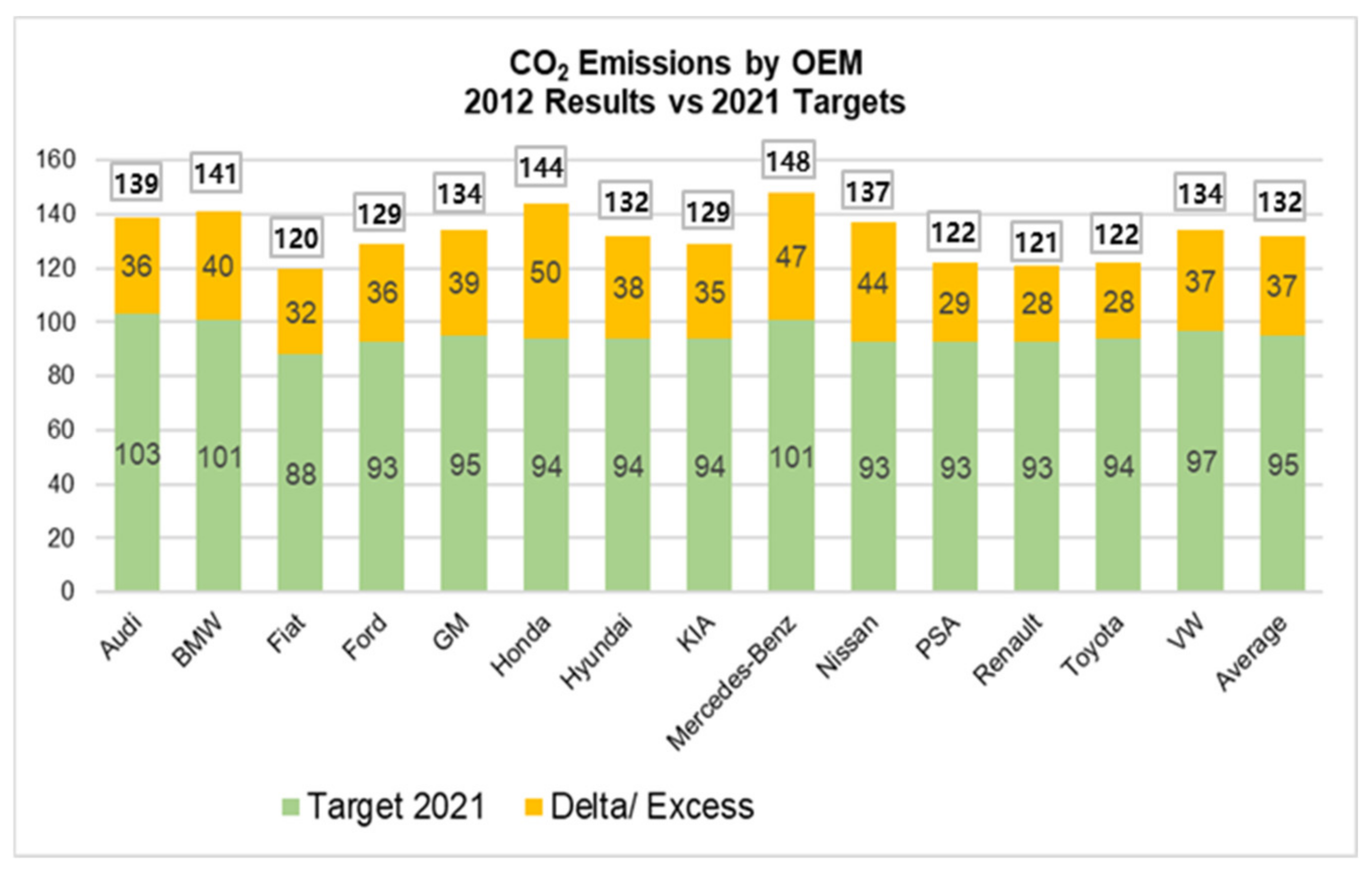

In 2014, European Union nations had agreed that carmakers should limit CO

2 emissions to 95 grams per kilometer across their entire model range within seven years. Consequently, AFVs were seen as a promising way to help OEMs in cutting CO

2 emissions to meet the corresponding EU targets. Based on data from the European Commission Amsterdam Roundtable Foundation, in 2012, the CO

2 emissions of all major OEMs clearly had exceeded these initially agreed targets for 2021 [

63].

Figure 2 illustrates the significant gap between the actual CO

2 emissions of major automotive OEMs in 2012 versus the official emission targets for 2021.

4.4. Net Customer Costs: Comparison of Gasoline vs. Electric Engines by Country

It is crucial to analyze the corresponding final total cost of ownership (TCO) of AFVs, and of B-EVs in particular, with and without public incentives. By comparing the examples of different European countries, one can evaluate if there was a significant causality between public incentives and the corresponding local AFV sales evolution. In this regard, one must critically evaluate the sustainability and market competitiveness of the AFV technology without public incentives [

64].

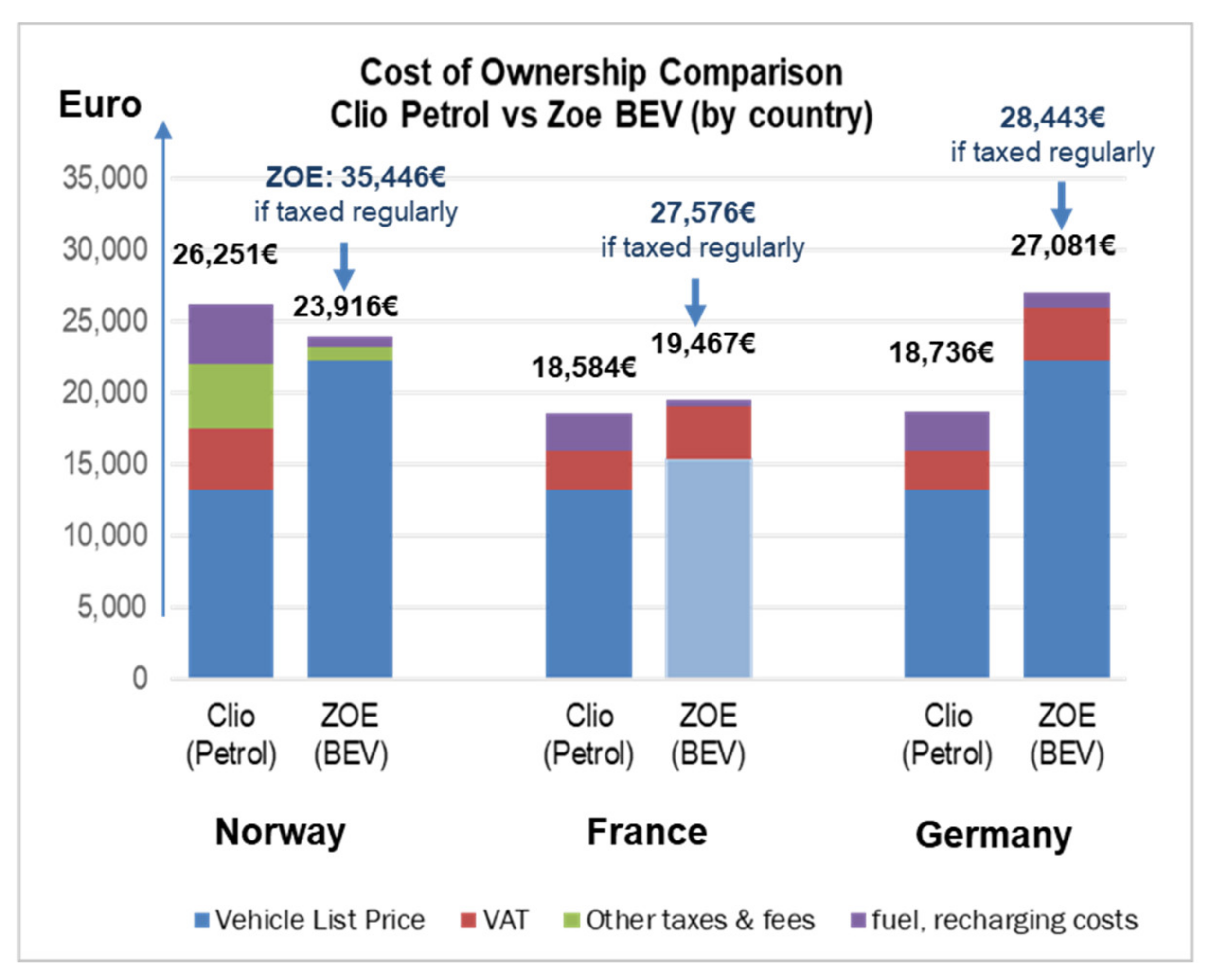

Figure 3 illustrates the notable difference in public incentives for BEVs across the European markets.

As shown in the chart, only because of heavy incentives could PEVs, such as the Zoe B-EV, compete with their ICE counterparts. In 2013, the B-EV model Renault ZOE had a lower market share in Germany than in France or Norway. A correlation can be found in the ICCT report from 2013, showing us the estimated total cost of ownership for a Renault Clio (with a gasoline engine) versus the mentioned Zoe (battery electric vehicle), including the corresponding local public incentives. Consequently, the higher the public incentives (for example, Norway), the more significant was Zoe B-EV’s market share [

64].

Hayek had already considered prices and profits to be knowledge-conveying devices. Prices, as well as profits, convey information regarding the supply of and demand for goods and services and the effectiveness of individuals in producing/providing them [

22,

51]. The development of the price system started to allow us to decide rationally about the allocation of scarce resources [

65]. Prices must be seen as signals of the relative scarcity of goods and resources, as prices also help to coordinate human activities [

22,

65]. As Carl Menger already stated, “

value is a judgement which economising men make about the importance of goods at their disposal for the maintenance of their lives and well-being” [

66]. In his early works, Hayek constantly emphasized the coordinating role of freely adjusting market prices [

22,

51]. As one can see in the above chart, a free market is clearly not provided in the European automotive market since the implemented high incentives and taxes have significantly distorted the market.

As indicated, different public incentive approaches with the aim to increase AFVs registrations were adopted by the individual European countries: before 2015, the use and/or purchase of fossil fuel vehicles causing negative externalities had already been penalized with significant taxes in several European countries, such as Norway, Netherlands and Italy, from which B-EVs and FC-EVs were partially or fully exempt [

5]. On the other hand, in the UK and France, direct subsidies had already been given to B-EV owners upon corresponding vehicle purchases. Simultaneously in 2015, in Poland, no public incentives at all were provided for AFVs [

34]. The Norwegian vehicle taxation system was heavily taxing fossil fuel vehicles based on curb weight and engine power, as well as on CO

2 and NO

x emissions. In addition, there was generally a high 25% VAT rate for vehicles, from which B-EVs were exempt [

5].

In addition, several other benefits and incentives were implemented, such as the mentioned access to bus lanes, free parking and road toll exemption, and the wide availability of public charging stations providing free electricity for EVs.

In the Dutch taxation system, the vehicle fuel type also played a significant role, as in 2014, a diesel surcharge of EUR 73 per gram of CO

2 emitted was imposed on emissions above 70 g/km. Moreover, the rate of the annual circulation tax has depended on the fuel type (petrol/diesel), while P-HEVs and B-EVs were exempt [

67].

It can be concluded that the Norwegian concept of providing tax exemptions, e.g., for the registration and circulation tax, mainly promoted big alternative fuel vehicles, whereas the lump-sum subsidies provided, e.g., France favored the purchase of small AFVs. Moreover, due to a lack of Budget transparency, it cannot be assured that taxes and fines related to “penalizing pollution” have mostly been “ring-fenced”, meaning that the corresponding government gains were truly allocated to projects protecting or enhancing the environment.

However, other important non-fiscal/non-purchase price-related factors can influence sales development. B-EV sales significantly increased from 2010 to 2015 in Norway, Netherlands, UK and France, even if simultaneously direct public incentives for B-EVs remained stable [

35]. Thus, it is crucial to note that from 2010 to 2014, the number of annual vehicle launches with an alternative fuel technology engine constantly increased. More diversity and more availability of PEV models on the market were considered of major importance to increase the PEV market share. A particular focus was on PH-EV model versions, as the PH-EV technology is often considered as the most appropriate transition technology from ICE to B-EV technologies [

67]. Consequently, Figenbaum et al. argued that the significant growth was mainly due to four aspects [

35]:

- (1)

A general customer awareness increase for AFVs;

- (2)

New B-EV model launches leading to a wider product variety;

- (3)

Optimization and densification of the recharging network;

- (4)

An optimized driving range due to improved technologies.

4.5. Fiscal Incentives and Their Impact on Price Competitiveness and Sales Evolution

In order to define the impact of fiscal incentives on the purchase decision of consumers, one needs to calculate all fiscal incentives and see them in comparison with the net price of the individual PEV. The total amount of all direct monetary incentives is the sum of all direct subsidies (e.g., upfront discounts) as well as the monetary differences in regard to dues and taxes such as the VAT, registration tax or circulation tax for PEVs versus their most similar ICE counterparts. With this relatively basic calculation in which other aspects such as local/municipal taxes or possible free parking spaces for PEVs are not yet included, we still obtain a helpful indication of how significant public interventions were on PEV market competitiveness [

64].

Apart from fiscal incentives to promote AFVs, there are also clear signs for European governments to generally ban petrol and diesel vehicles from the market. In 2018, the French government announced that France would end sales of diesel and petrol and vehicles by 2040. Prof David Bailey from Aston University said this French law would provide a clear signal to automotive manufacturers and consumers that the transition towards the increased importance of electric cars is significantly accelerated. The European Environment Agency had confirmed that the French car manufacturers Peugeot, Citroën and Renault ranked first, second and third on a 2016 list of large car manufacturers with the lowest carbon emissions [

68]. Consequently, one may speculate that the official aim of “environmental protection” was actually meant to camouflage a new form of national protectionism, as the laws passed by the French government were likely to benefit first and foremost the local French brands.

Even more radical are the targets of Norway, where already by 2025, only vehicles with a PEV technology should be sold [

69]. The Dutch government followed a very similar plan, and other countries have also floated the idea of banning cars powered by an internal combustion engine, but without having passed concrete laws yet. In this scenario, PEVs, which are currently already heavily state-subsidized, would no longer have to compete with petrol and diesel vehicles at all. Public interventionism would completely distort the market, not allowing any form of competition between PEVs and vehicles with an internal combustion engine.

4.5.1. AFV Sales Evolution

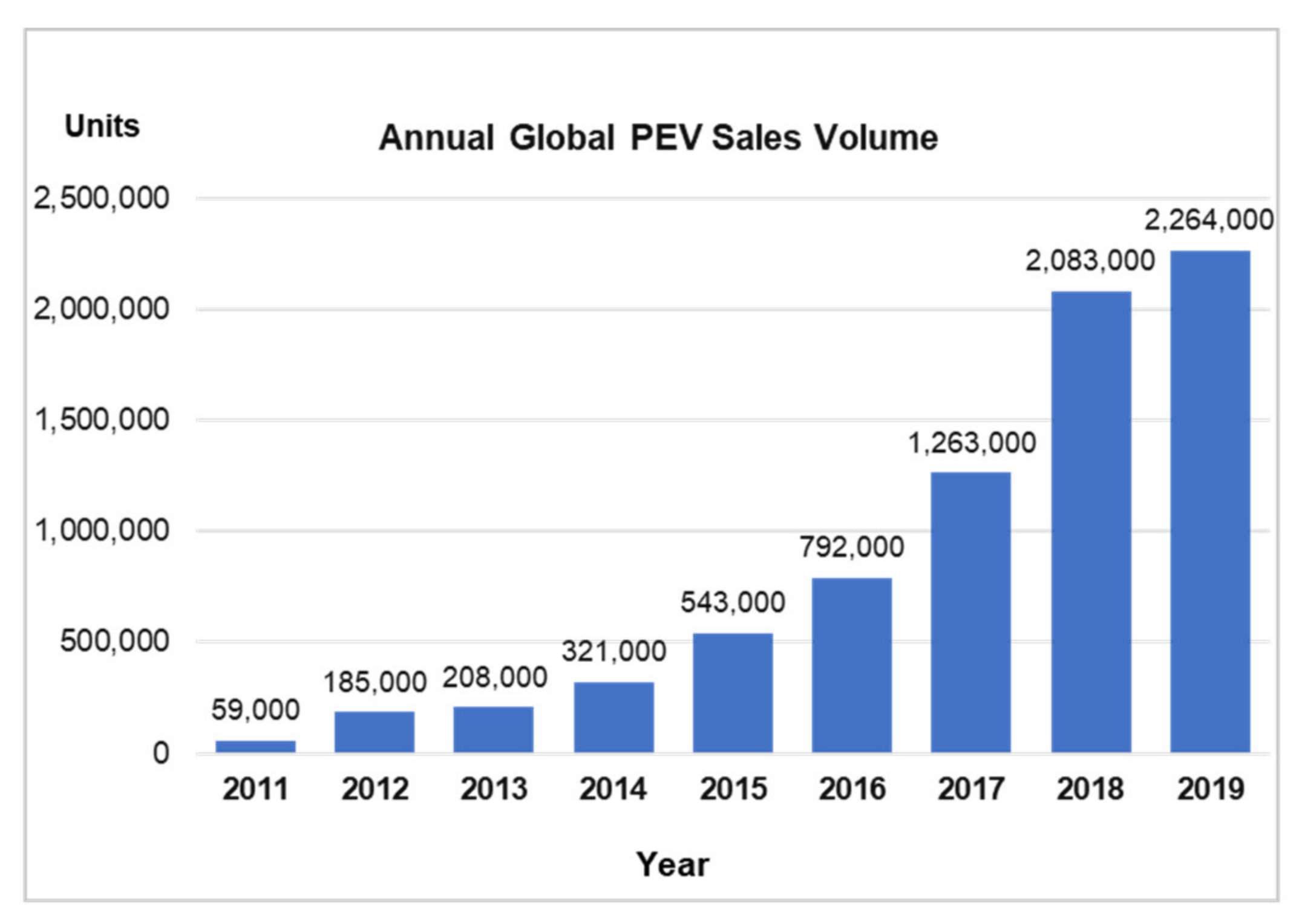

The following charts demonstrate the annual plug-in car sales’ evolution from 2011 to 2019. As indicated, the term plug-in electric vehicles (PEV) hereby refers to both battery electric vehicles (B-EV) and plug-in hybrid vehicles (PH-EV). In 2011, the global PEV sales had only reached a total of approximately 60,000 units, whereas six years later, in 2017, the annual PEV sales already reached 1.2 million units. However, in 2017 the PEV total market share was still relatively low, at approximately 1.3% of the total market [

70]. Thus, even if the uptake of PEVs was notable, most of the official PEV adoption targets set by public institutions at the beginning of the 21st century were not met by 2018.

Figure 4 is referring to the discussed increase in PEV sales across the globe in the period from 2011 to 2019.

In 2017, global sales of new electric vehicles (combining B-EVs and PH-EVs) passed 1 million units for the first time ever [

70]. In 2017, pure electric vehicles (B-EVs) made up 66% of all global PEV sales, while B-EVs sales grew faster than those of plug-in hybrid vehicles (PH-EVs) [

71].

However, this general global picture does not properly reflect that the specific individual markets have shown very different powertrain preferences and are also being influenced by public regulations and other public interventions [

43].

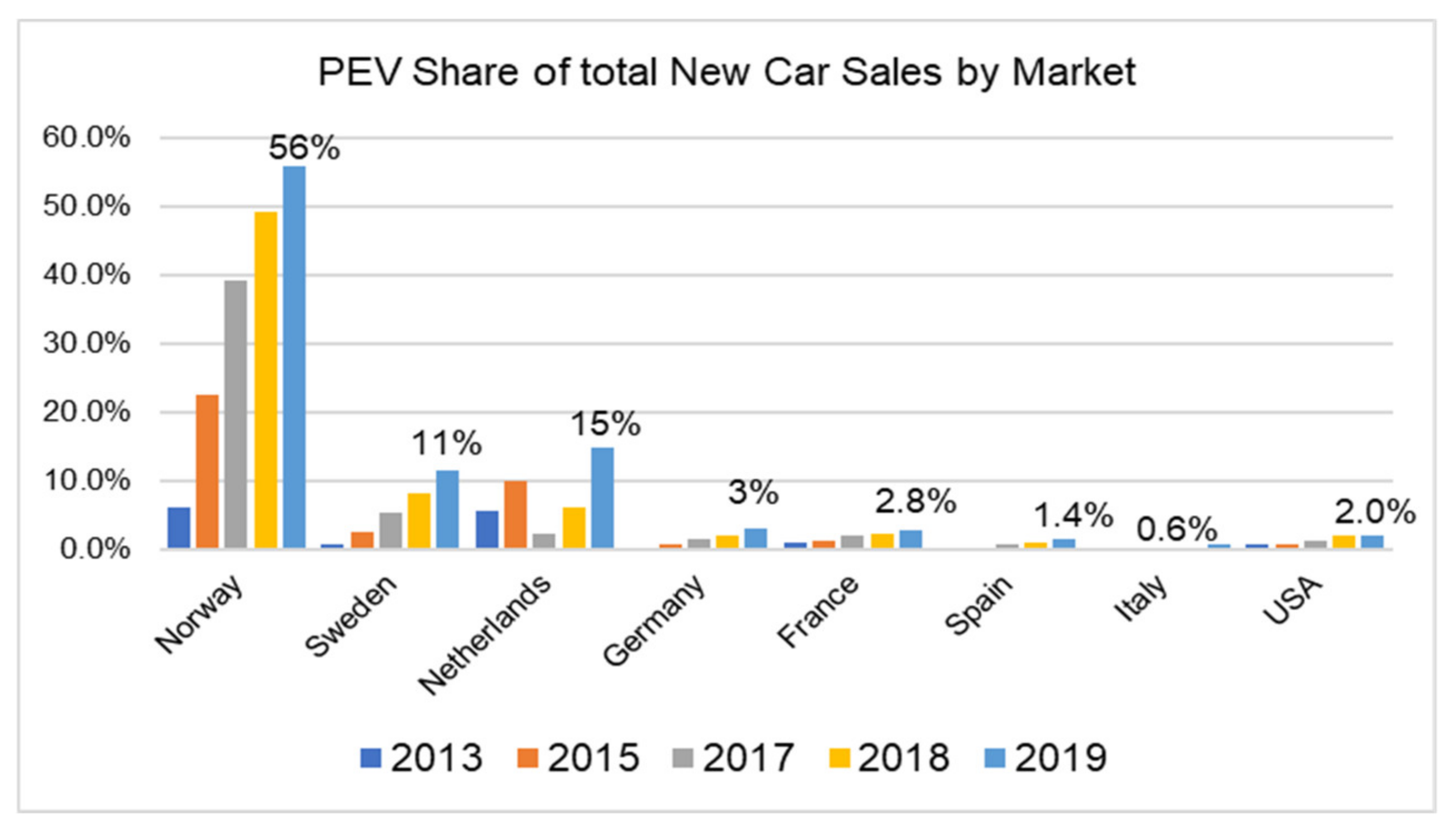

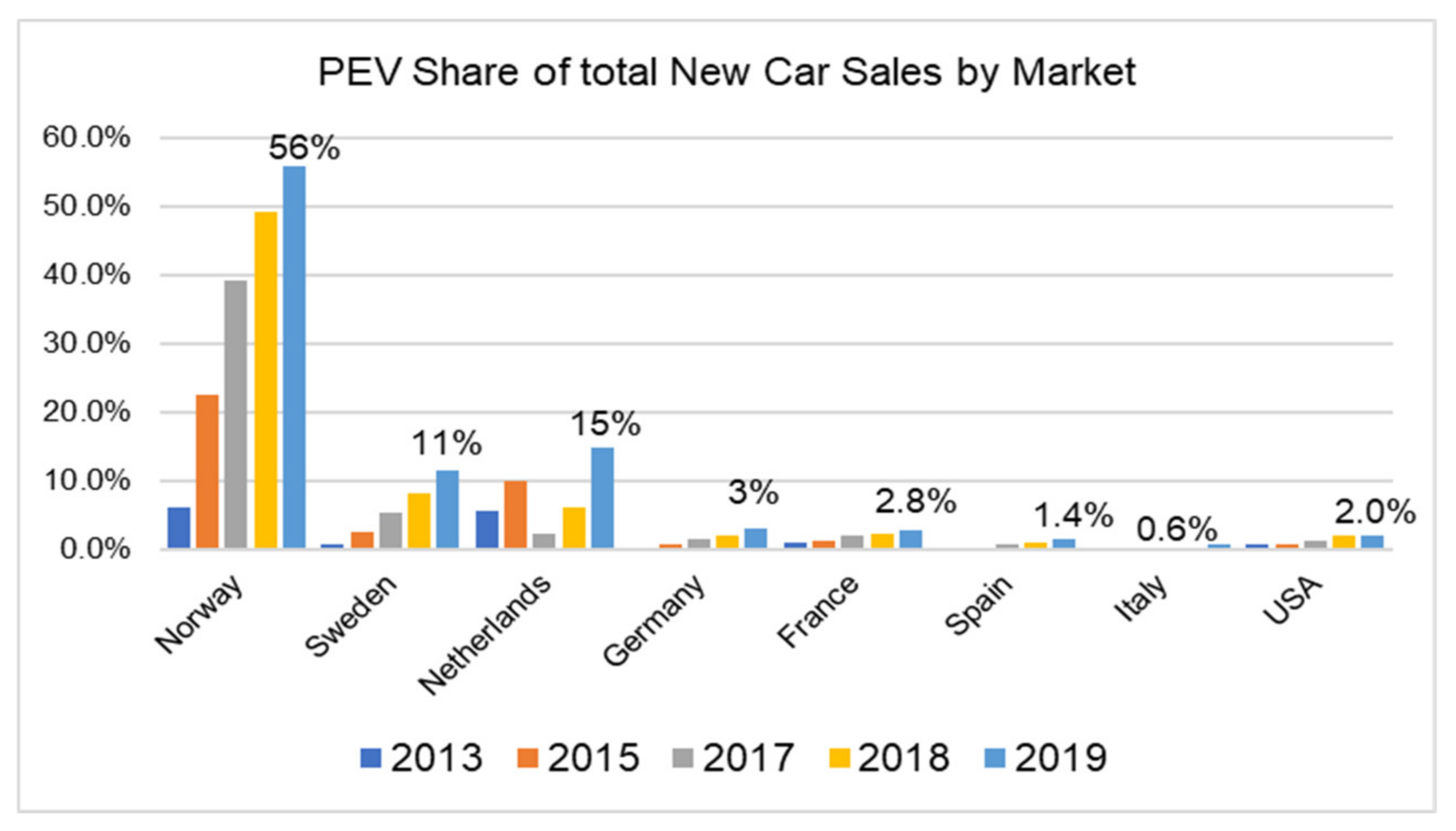

Figure 5 illustrates the significant differences between selected markets in regard to the individual local PEV sales share evolution.

In France, the registration of new B-EVs increased from only 184 units in 2010 to 32,203 units in 2018, which represented a market share of 1.4% of all new car registrations in 2018. The most sold plug-in electric vehicle from 2013 to 2019 was Renault’s Zoe. As previously stated, in 2008, the French government introduced a “bonus-malus system”, which was based on a purchase incentive for low emission vehicles and a penalty fee (malus) for the purchase of high-emission vehicles. Moreover, in 2015, the French government introduced an additional bonus for purchases of all-electric vehicles (B-EVs) connected to the simultaneous scrappage of diesel-powered cars if they were in circulation before 1 January 2001 [

52].

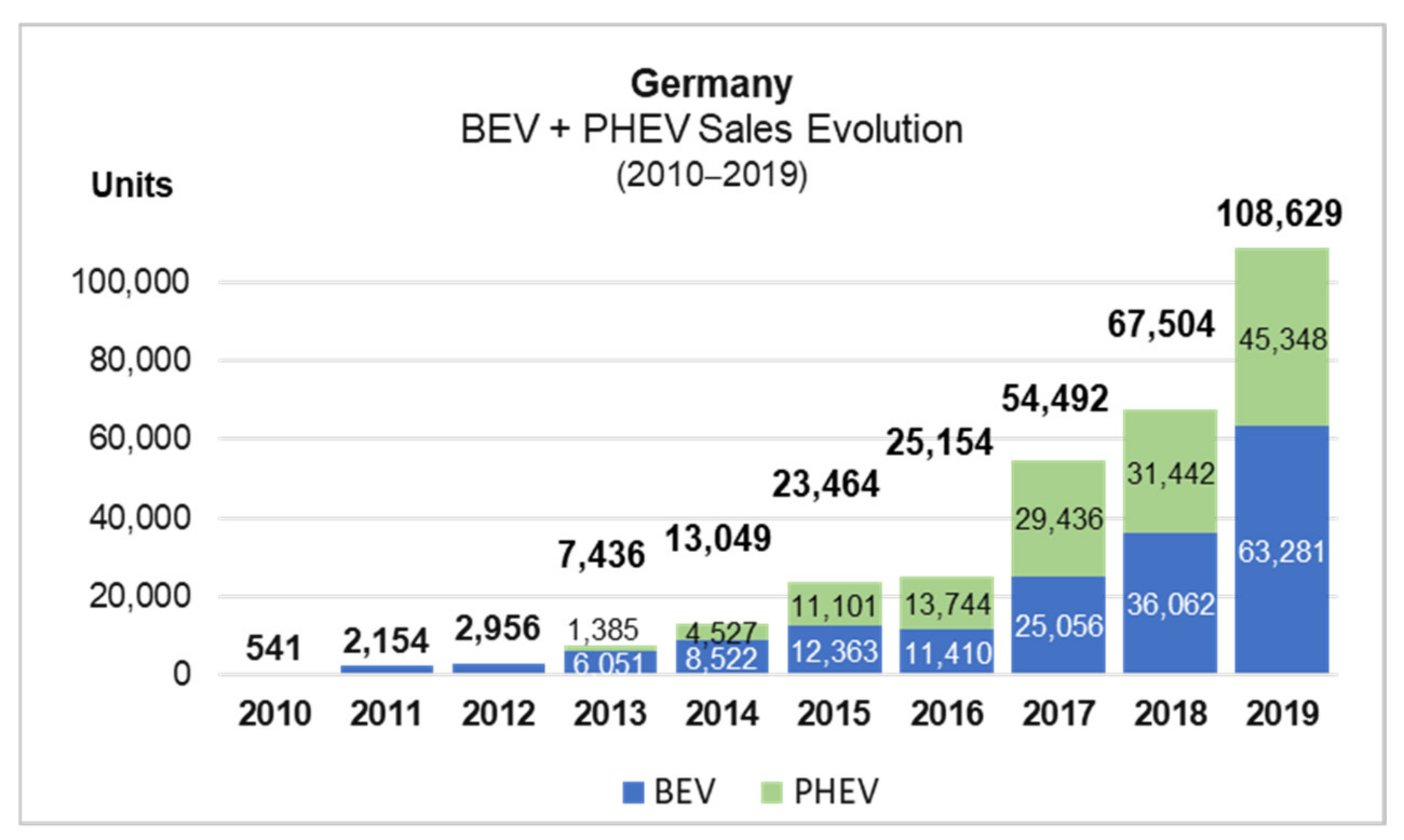

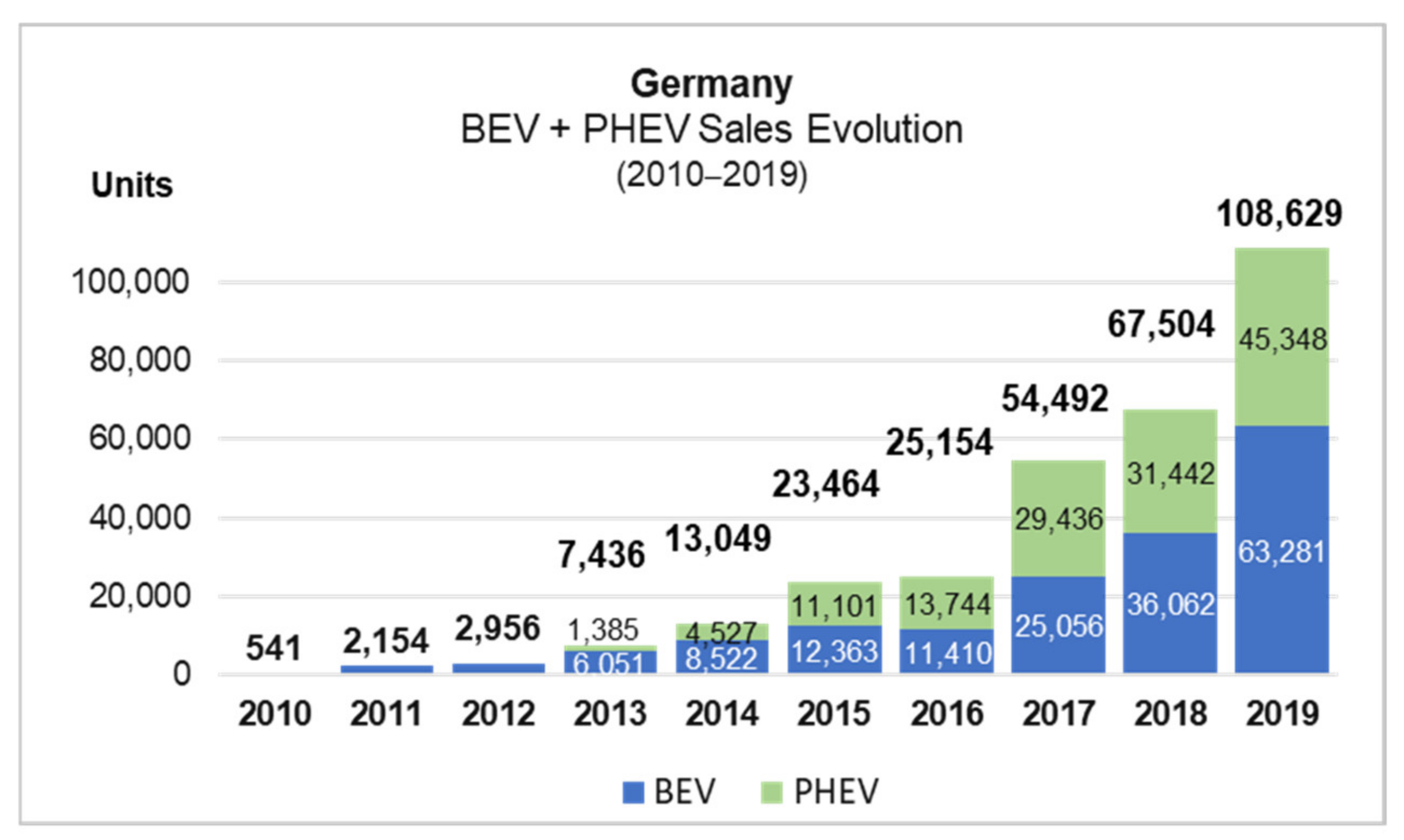

In Germany, cumulative registrations of all PEVs totaled 305,787 units between January 2010 and December 2019, consisting of 168,396 all-electric cars (B-EVs) as well as 137,391 PH-EVs. Although a constant volume growth could not be denied, the evolution was significantly less impressive than what had been foreseen by several politicians, journalists and consultancies [

52]. In 2010, and under its “National Platform for Electric Mobility”, German Chancellor Angela Merkel had set the target of putting one million electric vehicles on German roads by 2020. This far too optimistic target was not only a “German phenomenon”, but also most other European governments had defined similar, overly ambitious goals.

Figure 6 illustrates the corresponding gap between the indicated target and the actual sales evolution of PEVs in Germany.

In 2016, a national incentive scheme was approved for Germany, including purchase subsidies and public support for the expansion of the charging station network. Although Merkel’s mentioned PEV volume target was missed, corresponding vehicle sales significantly increased throughout the past years, thanks to optimized vehicle technologies with increased driving ranges, a (subsidized) growing recharging infrastructure as well as other public incentives and tax benefits. In particular, PH-EV sales had only seen a rather disappointing sales evolution up until the year 2019 [

4], but experienced a significant boost in 2020, mainly due to further optimized public incentives (including a new car purchase bonus as well as tax benefits, particularly for company car users) [

52].

In the Netherlands, new car sales of B-EVs significantly increased throughout the past years, whereas registrations of PH-EVs meanwhile even slightly decreased. Until 2016, the Dutch PEV market was dominated by plug-in hybrid electric vehicles (PH-EVs), when the Dutch government decided to reduce the relative tax advantages of PH-EVs. In 2016, as of January 1st, the registration fee for PH-EVs increased from 7% to 15% of its list price, whereas for all-electric vehicles (B-EVs) and vehicles with conventional internal combustion engines, the fees remained stable at 4% and 25%, respectively. Moreover, B-EVs have special access to parking spaces in Dutch cities such as Amsterdam, and free charging is provided in public parking spaces. The Netherlands can be seen as a good example of how public interventions helped to significantly boost PEVs, while then also moving customer demand from PH-EV models towards B-EVs [

52].

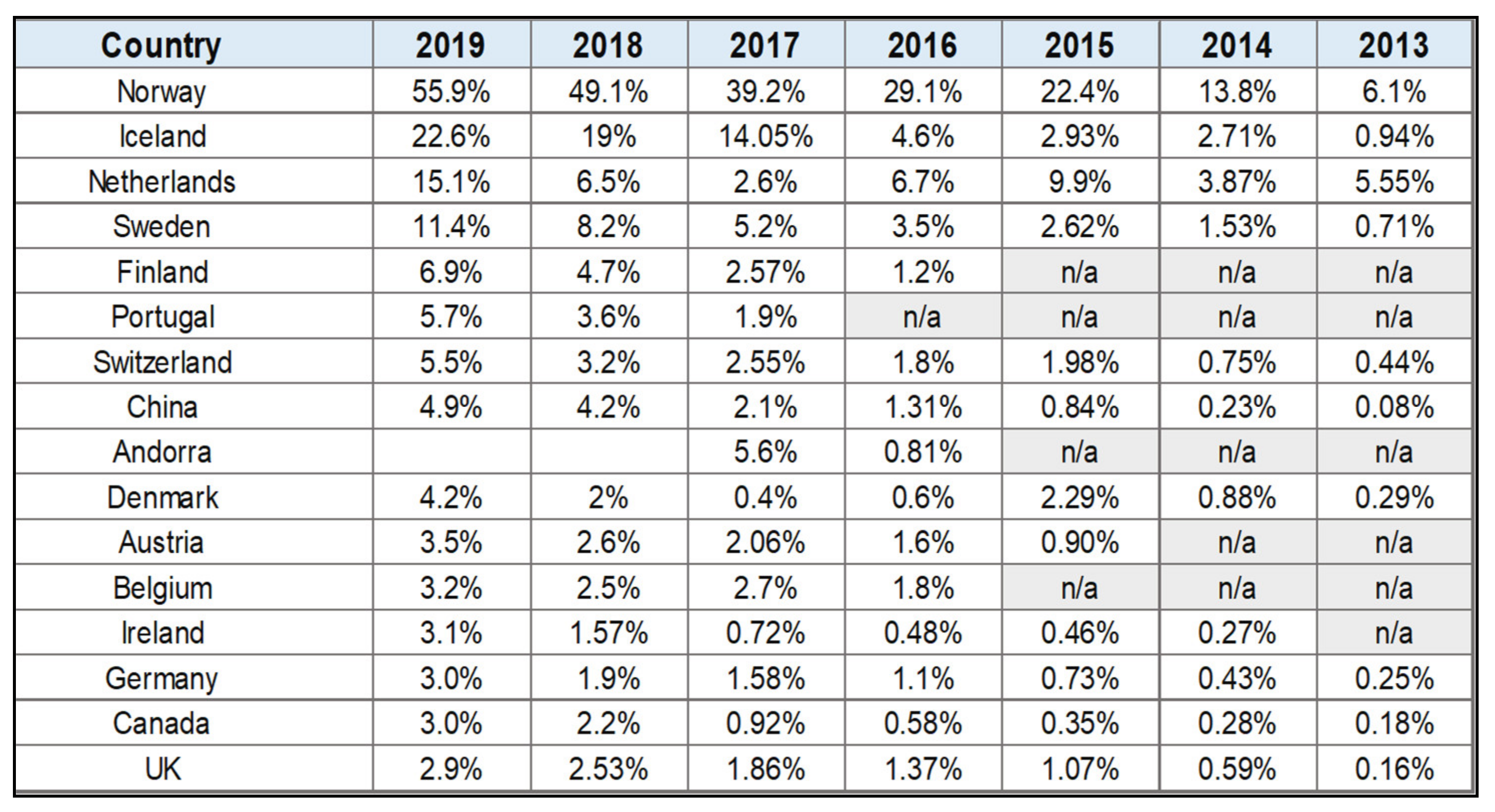

Figure 7 is illustrating the shift from PH-EVs to B-EVs in the Netherlands in the period from 2011 to 2019. Accordingly,

Table 1 shows the corresponding concrete figures, showing a clear tendency towards BEVs since 2016.

Meanwhile, in Norway, the market growth of PEV sales was even more stable and impressive than in the Netherlands. Norway has the world’s largest PEV ownership per capita. The Norwegian government implemented several incentives to promote the adoption of PEVs, such as an exemption of B-EVs from the annual road tax, public parking fees and toll payments. As of January 2018, at least 24 out of 58 major municipalities kept free parking for B-EVs. By 2016, PEVs had already captured a market share of 29.1% of the total Norwegian new car registrations, which rose to 39.2% in 2017 and then to 49.1% in 2018. In 2019, the PEV market share of new car registrations even rose to 55.9%, which meant that in 2019, more than every second new passenger car sold in Norway was a B-EV or PH-EV. In October 2018, Norway became the first country globally in which 1 in every 10 registered passenger cars was a PEV [

52,

71].

Table 2 illustrates the significant PEV sales increase (individually shown for PH-EVs and B-EVs) in Norway in the period from 2013 to 2018.

In Poland, public incentives were significantly lower than in the previously mentioned markets, such as Norway, Netherlands and Germany. In 2009, the Polish charging station infrastructure was developed in cities such as Gdańsk, Katowice, Kraków and Warsaw with EU funds, but public support by local governments was rather limited. Consequently, due to the lack of market-distorting public incentives and only relying on the actual customer demand, sales figures for PEVs were extremely low in Poland. Sales of new B-EVs rose from 70 units in 2015 to only 620 units in 2018, representing an insignificant 0.12% of the Polish automotive market in 2018 [

52,

71].

Moreover, in Italy, sales growth of PEVs was slower than in other European markets. By December 2015, the cumulative registrations of all PEVs only reached approximately 6100 units, consisting of 4580 B-EV units and 1550 PH-EVs. Even in 2018, the annual volume of PEV sales was relatively low, at approximately 10,000 units [

52,

71].

Overall, one can say that while manufacturers have shown progress in developing more competitive PEVs with a wider driving range, well-performing engines and superior styling, there are still several significant challenges to accelerate PEV sales in a sustainable way. Simultaneously, several new automotive brands and mobility providers were founded or restructured with a strong focus on PEVs. These interesting new start-ups include the Chinese companies NIO Inc. and Aiways Ltd., as well as the Chinese–US–American corporate Lucid Motors and Fisker Automotive Inc. While the Chinese brands NIO and Aiways focus on electric SUVs, such as NIO’s coupe SUV “EC6” and Aiways “U5”, Lucid Motors plans to initially target luxury customers with its sporty model “Air”. Other Asian OEMs entering the European market with PEV technologies are the Vietnamese Vingroup with its brand VinFast, as well as the Chinese OEMs Xiaopeng Motors (Xpeng), BYD Company Limited, Great Wall Motors (with its brands WEY and ORA) and “SAIC Motor Corporation Limited” (with the formerly British automotive brand MG), as well as the brands Polestar and Lynk and Co by Geely Auto Group [

46]. Whether these new brands, particularly the recently-founded start-ups, will succeed in Western markets cannot be defined at this stage. The author of this paper assumes that ultimately not more than two or three of the mentioned new players will be able to successfully establish themselves in the European market. For them, it will be crucial to establish an efficient supply chain and a manufacturing structure that successfully combines fast production processes and high-quality products with a reliable after-sales and service network. Even more so, a customer-friendly network of service points and a fast supply of spare parts must be assured.

Figure 8 illustrates the market share of PEVs among the annual new passenger car registrations in the period from 2013 to 2019. The analysis shows that PEV increase was particularly significant in countries located in the northwest of Europe. In smaller Nordic countries, such as Norway, the Netherlands, Iceland and Sweden, an impressive sales growth of PEVs occurred [

71,

72].

However, by 2019, in the larger European markets such as France, Germany and the United Kingdom, PEVs were still a niche product. Due to the increasingly strict CO

2-emission regulations, a growing range of PEV models and the mentioned economies of scale, the market share of PEVs is expected to notably increase across Europe [

52,

72].

4.5.2. Quantitative and Qualitative Status of the AFV Implementation

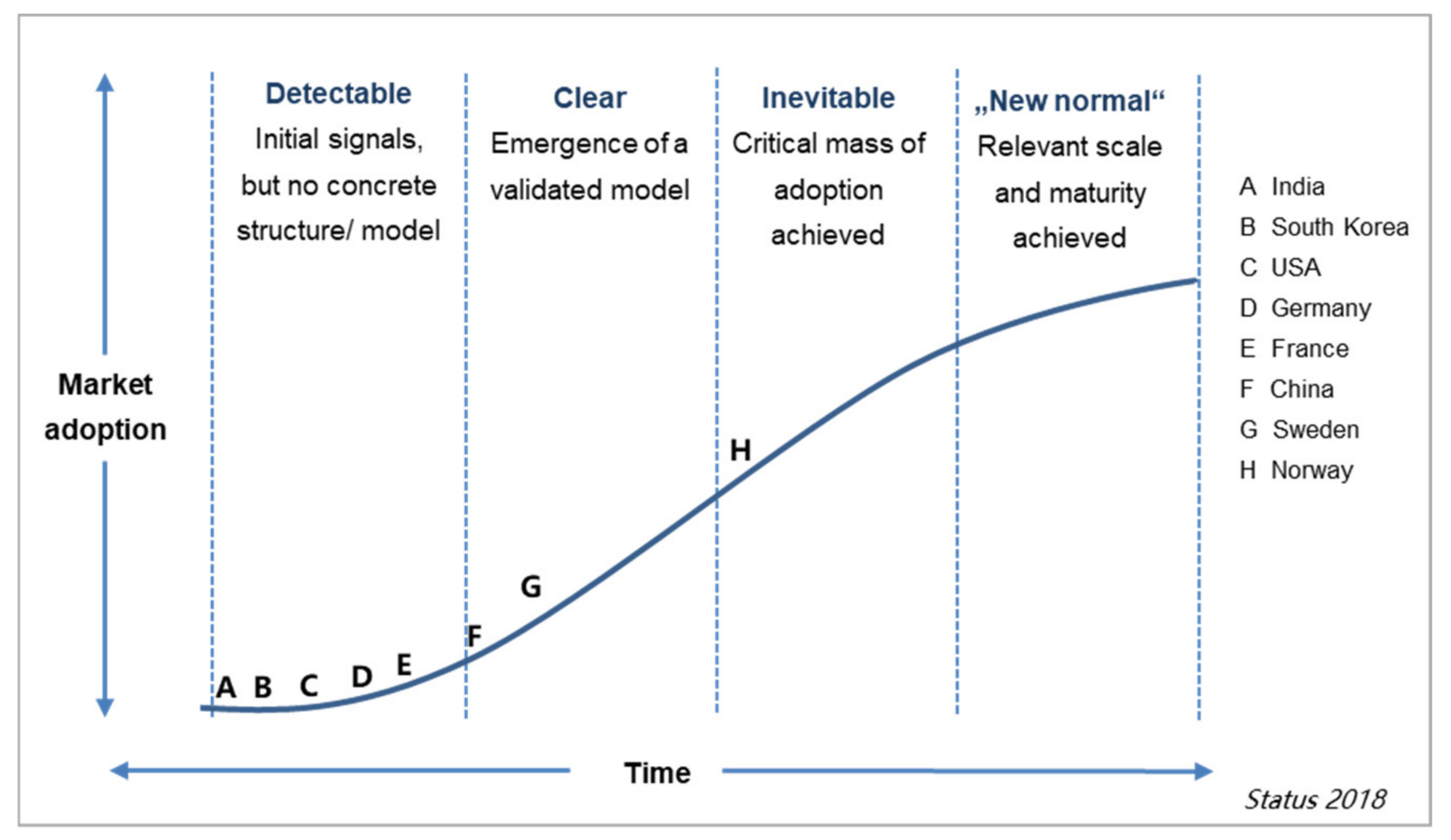

In the following section, the author intends to illustrate the evolution of PEV adaptation within the different markets throughout recent years. The author does not only refer to the pure quantitative evolution of PEV sales but also to how automotive experts at companies such as McKinsey and Bloomberg consider the individual competitiveness of automotive OEMs.

The following chart, based on an analysis by McKinsey in 2018, shows the four stages of a disruptive trend. It indicates that the so-called “electric vehicle disruption” is already inevitable in Norway, which has seen significant growth in PEV-sales. Apart from significant public incentives for PEVs, the rollout of more attractive, better-performing PEV models in key high-demand segments was also a major driver for a relevant sales uptake in several markets [

33,

70]. As noted, the increased investments by automotive OEMs into alternative fuel technologies are also driven by ambitious emissions targets (especially in China and Europe) and announcements by several national governments (or individual states and cities) around the world to set end-dates for the registration of diesel- and gasoline-powered vehicles [

68,

69]. Accordingly, the US-American State of California, as well as France and the United Kingdom, had announced that local sales of ICE vehicles should be terminated by the year 2040 [

71].

Figure 9 illustrates the status of selected markets regarding their maturity as a BEV market. It is based on mentioned McKinsey’s (2018) research, indicating that by 2018, markets such as India, the USA and Germany were still in the first phase of the PEV market adoption. Markets such as China and Sweden were already considered to be more “advanced”, being in the second phase, although a truly critical mass of market adoption was not achieved [

52,

71].

By 2018, only Norway achieved a PEV market adoption by a considerable critical mass [

71]. Thus, the mentioned considerable public supports to increase the competitiveness, and general customer acceptance of PEVs in Norway have apparently been effective.

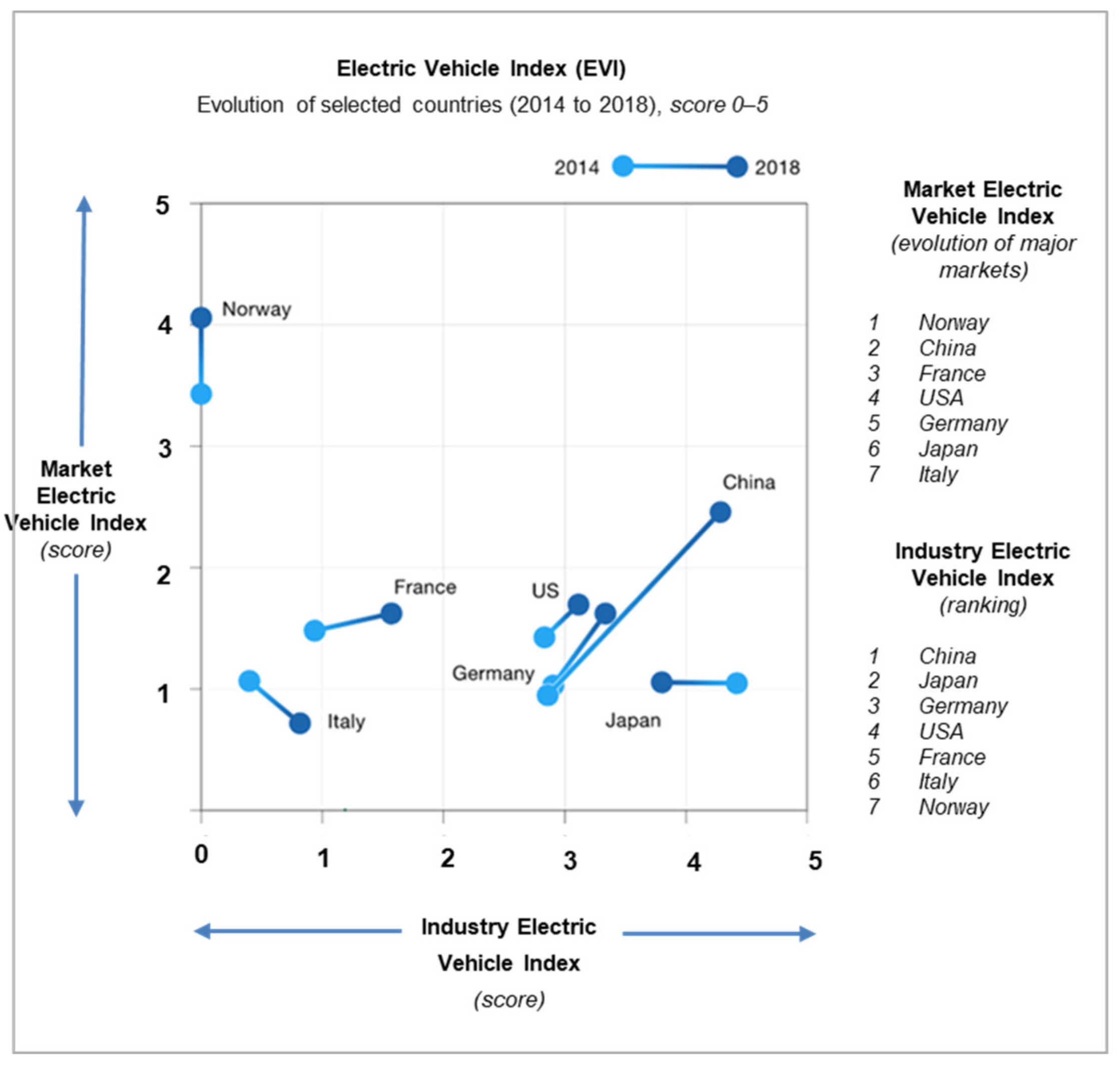

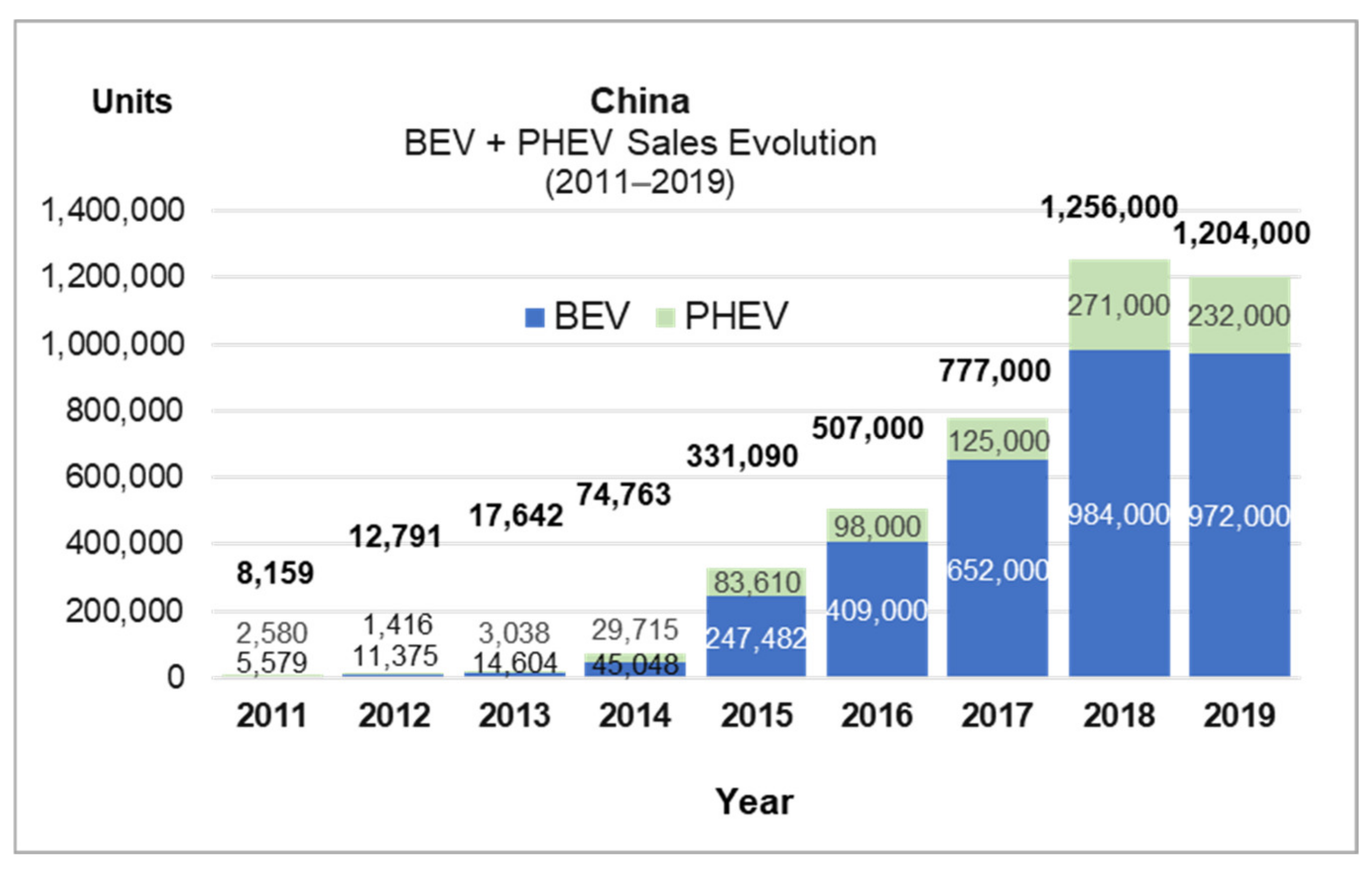

However, the author of this paper argues that due to its tremendous size, the evolution of the impressive Chinese automotive market is likely to have a significantly higher global impact than that of Norway. Correspondingly, the sales evolution of PEVs in China should herein be illustrated in more detail.

Figure 10 illustrates the annual sales volume evolution of B-EVs and PH-EVs in China within the period from 2011 to 2019. The stated numbers indicate the significant volume increase which had occurred, particularly from 2014 to 2018.

In 2019, China was by far the largest PEV (B-EV + PH-EV) market in the world, with a total of 3.4 million highway-legal PEV passenger cars in use, representing 47% of the global PEV fleet at that point in time. Since 2011, the combined sales of all classes of PEVs (passenger cars and commercial vehicles) totaled almost 4.2 million by the end of 2019 [

52,

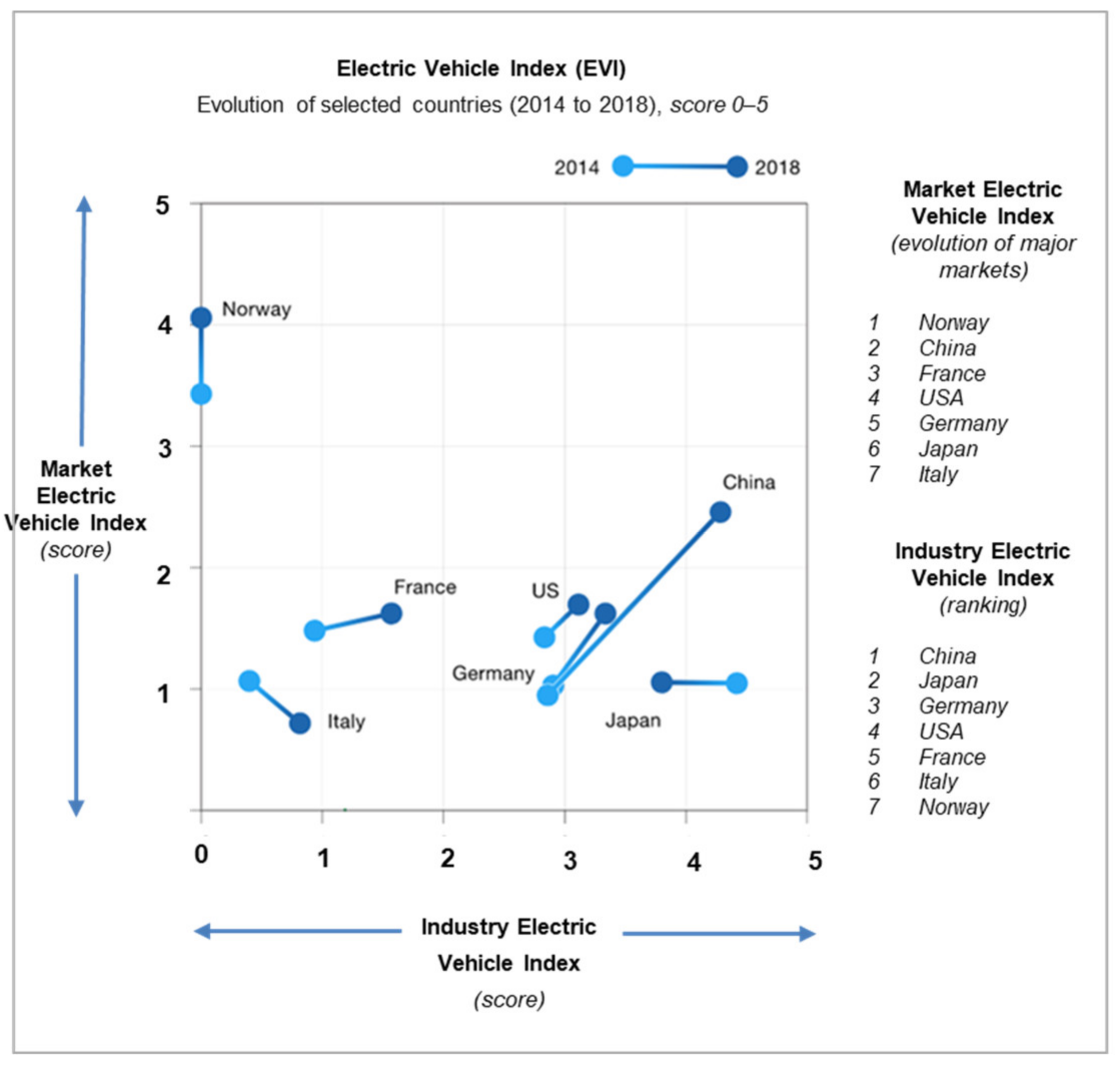

71]. In the following chart, the author intends to analyze how well individual economies are prepared for the transition towards an automotive market that is likely to be shaped by PEVs. This analysis shows the countries’ individuals from 2014 to 2018 and is conducted from two perspectives: from a consumer’s perspective as well as from an automotive producer’s point of view. A comparison of EVI performance over time indicates that China has already overtaken the United States and Germany when combining these two “EVI scores”. In McKinsey’s 2018 overall EVI rankings, China was only outperformed by Norway in the “EVI market score” (representing the consumer demand side) while reinforcing its leading position in the “industry EVI analysis” (which represents the “supply” side of the equation) [

71]. In other words, while Norway is considered the most advanced market (consumer-wise) in regard to the expected shift towards plug-in vehicles, China is seen as the economy in which local automotive producers are most prepared for this structural shift.

Figure 11 indicates that the index of several markets changed quite significantly from 2014 to 2018. China outperformed other countries in regard to the evolution of its market index as well as regarding its industry index. In regard to the “market EVI scoring”, China improved its position by providing significant monetary and non-monetary incentives, offering its consumers a wider range of models, as well as by increasing investments into the charging infrastructure. Moreover, China clearly optimized its “industry EVI scoring”, significantly increasing its EV production and component shares. Whereas France and Germany only slowly advanced in regard to increasing the local EV market share and the domestic production of EVs, Italy’s corresponding market-side performance had even decreased by 2018 [

71].

Thus, within the period from 2014 to 2018, some markets such as Italy did not show relevant progress in regard to a PEV adaptation. In the same period, the USA showed a slow adaptation, while the development in France and Germany was already slightly larger, but still at a relatively low level. The only market which significantly increased its EV development index, in regard to its market index as well as regarding its industry index, was China [

71].

However, one must consider that due to the limited price competitiveness of current EV batteries, China’s and Norway’s leadership in EVI scores has only been possible due to significant public interventionism [

1,

4,

43]. China and Norway have some of the world’s highest levels of spending on consumer and supply-side subsidies, which can only be financed at the citizen’s/taxpayers’ expense [

1,

43]. In 2009, the Chinese government adopted a thorough plan to turn China into the world leader in EV production, focusing on four main goals: creating a world-leading PEV industry, assuring energy security while also reducing urban air pollution, as well as to reduce local carbon emissions. In June 2012, the Chinese State Council published a plan to develop the domestic car industry, providing public incentives with the aim to achieve an annual target of 5 million new PEV sales by 2020 [

52].

Correspondingly, in a truly free market economy, it is highly unlikely that alternative fuel vehicles could have already gained a significant market share before the establishment of true price competitiveness versus ICE vehicles. Thus, the self-critical question all laissez-faire economists must ask themselves is: “Do the ends justify the means?” In other words, has public interventionism been necessary to create a world with less pollution, less global warming and less negative externalities? More importantly, can the seen public incentives and other forms of public interventionism be justified if ultimately automotive OEMs (due to their significant R&D investments and the expected economies of scale) are able to produce and sell PEVs at competitive prices without any public incentives? To go a step further, will those automotive OEMs, which are directly influenced (and protected) by their national government, be more competitive than traditional western OEMs that have been less controlled by public structures, such as BMW? Dudenhöffer agrees that it is very unlikely that Chinese automotive OEMs could have become so advanced in the development of plug-in electric vehicles without the significant interventionism and financial support by the Chinese state [

43,

44]. In other words, can China serve as an example that demonstrates that public interventionism is successful in preparing local OEMs to be more competitive in the future global automotive market? The author of this paper opposes this position, as in a truly free market, potentially other alternative fuel concepts could have been preferred by the market players for being economically more efficient and ecologically more sustainable than PH-EV and B-EV engines.

As initially stated, the implemented public incentives to increase the attractiveness of AFVs for consumers are often justified by the aim to protect the environment and to reduce negative externalities, such as air pollution and CO

2 emissions [

1]. It is not denied that battery electric vehicles (B-EV) can reduce greenhouse gas (GHG) emissions if powered with truly “clean” renewable energy. Accordingly, many consumers consider full electric vehicles to be more sustainable than hybrid vehicles, given that as of today, the latter still create some air-polluting emissions while driving. However, when referring to environmental protection and negative externalities, one must also consider that electric vehicles create a demand for additional electric power generation and, more importantly, that the current electric power generating industry has failed to properly switch to more sustainable energy sources [

1,

4]. Thus, in most countries, the power generation which is necessary to fuel “green” B-EVs ultimately also depends on the use of fossil fuels. Thus, current B-EVs still cause significant pollution for being are run on electricity that, in most European countries and the United States, is still mostly generated from the combustion of fossil fuels. Moreover, current PEVs are run by intricate lithium-based batteries, which are difficult to dispose of and which are harmful to the environment, containing toxic metals such as nickel, lead and copper, as well as toxic and flammable electrolytes [

1,

4,

17].

4.5.3. New Car Sales Evolution: Annual Global Light-Duty Vehicles—ICEs vs. EVs

Bloomberg New Energy Finance (2020) forecasts that by the year 2040, electric cars will dominate the global automotive market, stating that PEVs (with all its variances) will make up 28% of all passenger vehicle sales by 2030 and 58% by 2040. This significant increase is expected to be driven by a strongly increasing variety of PEV models, falling lithium-ion battery prices, reduced per-unit production costs, further public regulations and fiscal policies, as well as an increasing acceptance by consumers. Based on the same study, Bloomberg New Energy Finance considers production cost for certain PEVs to achieve price parity versus internal combustion engines (ICEs) by approximately 2025. This calculation is assuming that production costs can mainly be decreased due to economies of scale as well as due to possibly reduced per-unit research and development costs [

73,

74].

Concrete indications for increasing PEV sales volumes will reassure car manufacturers to invest in larger production facilities for PEVs, leading to reduced

per-unit costs. Correspondingly, in particular, regarding B-EVs, economies of scale will drive down battery costs, reducing total production costs of electric vehicles, enabling them to achieve much wider-scale adoption [

74]. The author agrees with Dudenhöffer that mentioned economies of scale could then occur, leading to cost advantages obtained by their scale of operation (typically measured by the amount of output produced) [

44,

75]. This scenario is illustrated in

Figure 12.

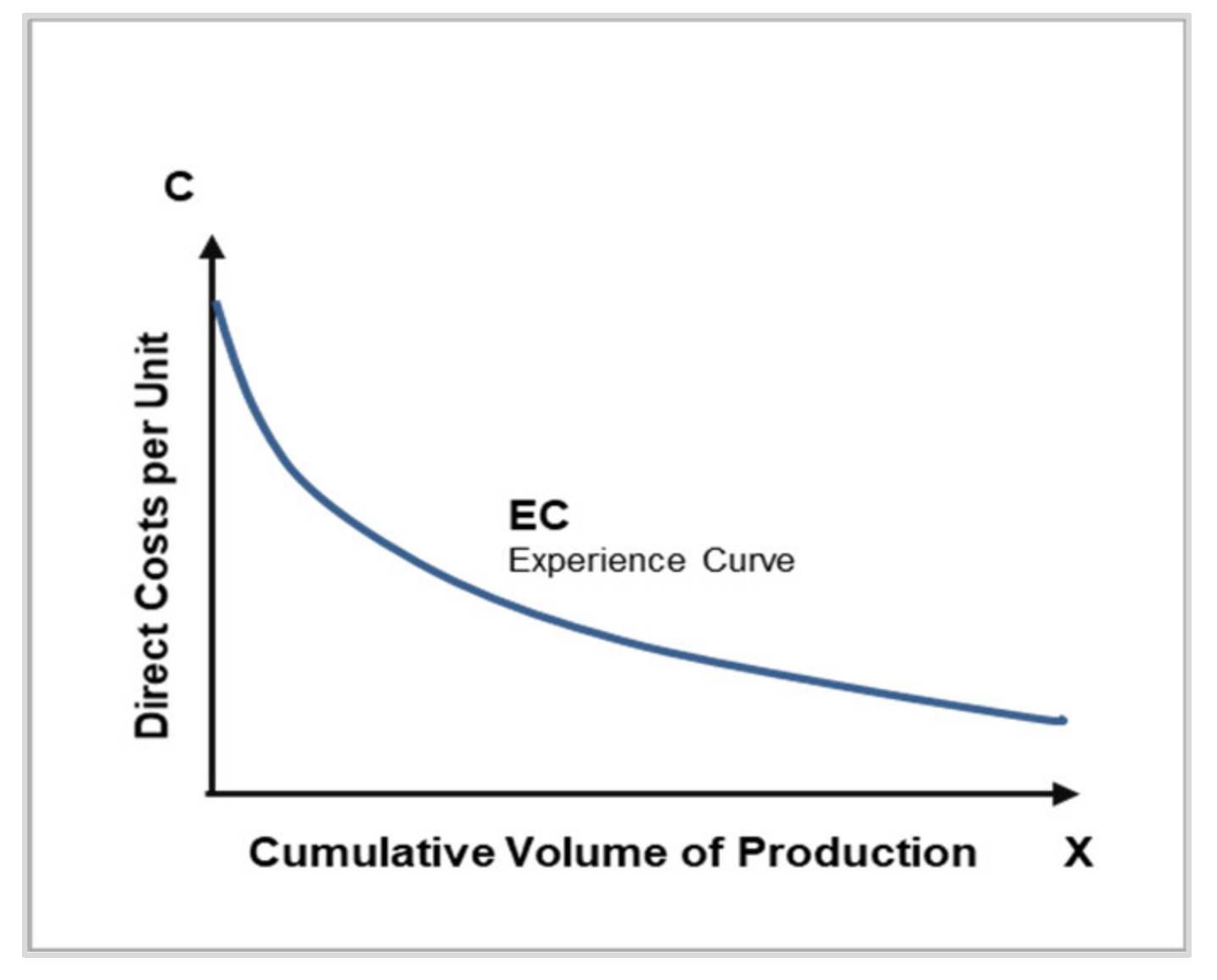

One must also consider what is called “the experience curve” which refers to the effect that the higher the cumulative volume of production (X), the lower the direct cost per new unit produced (C). As shown in

Figure 13, there shall generally be a reduction in the average cost of production of a particular product as a consequence of an increase in the company’s experience. As a consequence, the time and cost of producing

a unit of output will then be reduced. Thus, an experience curve is convex and has a downward slope, as shown in the following diagram [

74,

75].

Additional crucial aspects are the constantly increasing mileage/driving range of new, optimized PEV concepts, as well as the growing network of recharging stations [

37].

Moreover, it can be expected that plug-in hybrids (PH-EVs) will lose relevance within this period, being replaced by battery-only vehicles (B-EVs), for which competitiveness is constantly being increased due to optimized engines with longer driving ranges. Moreover, Bloomberg declared that while plug-in hybrid electric vehicle (PH-EV) sales would play a significant mid-term role in PEV adoption until the year 2025, pure battery-electric vehicles (B-EVs) would subsequently account for the vast majority of all PEV sales for the following years [

73]. The share of B-EVs is expected to grow particularly in the passenger car segments, whereas FC-EVs are rather expected to have an opportunity with commercial vehicles/medium and heavy-duty vehicles. Despite the growing general interest in hydrogen technologies in regard to energy production, sales results of FC-EVs in the European automotive market were rather disappointing, particularly for passenger cars. Moreover, the author argues that the narrowed focus of most European governments on promoting PH-EV and, even more so, B-EV technologies must be seen critically. However, throughout the second decade of the 21st century, FC-EVs are forecasted to become significantly cheaper from a TCO perspective, as vehicle development and production costs are expected to decline due to technological advancements and economies of scale [

73,

76]. Thus, apart from the “positive discrimination” (public incentives, free parking spaces, tax reductions, etc.) for PEVs by local governments and public institutions, it is expected that the “negative discrimination” of ICE vehicles (such as the introduction of additional fees and taxes, driving constraints in urban areas, etc.) will further intensify. Therefore, as indicated, ambassadors of the “electric revolution” argue that temporary public incentives were only needed for a limited period of time to “steer” the automotive industry into a more sustainable future. This perspective could present the latest developments on the automotive market as a success story, justifying public interventionism by arguing that in this case, “the result seems to justify the deeds”.

4.6. Summary on Fiscal Policies in the Automotive Industry

With the recent fiscal policies and legal settings, a proper definition of free-market prices is impossible due to massive public interventionism such as taxes, fees and other regulations [

1,

4]. It can be argued that the economic boom and real estate bubble seen in the early years of the 21st century showed similarities to the current “boom in eco-friendly car sales”. The ultra-lose monetary policies combined with artificial credit expansions that led to the financial crisis of 2007–2009, was caused by monetary policies which distorted the market, creating an artificial demand for credits, increasing unproductive investments into the early stages of production [

11,

77]. The author concludes that similarly, the recent growth of AFV sales would not have been possible without public interventionism and market-distorting fiscal policies. One may certainly argue that the development of the recharging infrastructure for PH-EVs and B-EVs would have been a challenge without any public support, as these engine technologies rely heavily on proper fuelling infrastructure. This interdependence between necessary, costly fuelling station investments and the competitiveness of AFVs in the market had caused a certain “chicken and egg” problem for which governments, automotive OEMs and gas station providers had blamed each other. Nevertheless, it is argued that if automotive OEMs (or gas station owners) had really seen a significant market demand, proper solutions certainly would have been found by the free markets, as truly free markets have always been able to adapt to changes [

78,

79]. Mises once stated that “

it is the speculative capitalists who create the data to which he has to adjust his business and which therefore gives direction to his trading operations.” [

78].

The recent increase in AFVs cannot be seen as sustainable development, as it is not occurring in a free market, not being based on actual customer demand [

80]. Friedman was right in saying that “

one of the great mistakes is to judge policies and programs by their intentions rather than their results.” [

81]. Consequently, the author of this paper argues that, as in the case of monetary policies by central banks, fiscal policies implemented by governments also directly lead to market distortions and

malinvestments, which have often led to negative long-term results, ending up in economic crisis [

82].

However, when looking at the reality in several corporations, it must also be remembered that in particular within the automotive industry, most OEMs are no more steered by “entrepreneurs”, but rather by “managers”. Consequently, whereas only a very few brands are still family-owned enterprises, the majority have become global corporations, often driven by short-term results necessary to optimize the company performance at the stock markets. Consequently, the traditional concept of entrepreneurs being alert and creative to discover new business opportunities [

23,

83] while personally investing time and money into their company’s long-term success does not fully match with several large corporations. The so-called “principal-agent problem” is an example of moral hazard, in which economic agents (such as managers/employees as well as stockholders of a company) are motivated to act in their own best interests, which are contrary to the long-term interests of the corresponding company.

Thus, from the author’s perspective, to fully appreciate the relevance of long-term entrepreneurial success and long-term competitiveness, an understanding of the concepts of “entrepreneurship and competition” developed by F.A. Hayek, Israel Kirzner and Huerta de Soto is seen as crucial [

22,

23,

65,

79]. Kirzner criticized the approach of many neo-classical economists who mainly concentrated on the concept of “economizing”, referring to their focus on the allocation of given means to achieve as fast as possible a set of given (competing) ends. He argued that this was not sufficient to guarantee entrepreneurial success in a dynamic market [

23].

From a dynamic perspective, it is much more relevant to be alert, discovering new opportunities than to purely focus on “preventing waste”. Thus, within the automotive industry, major decision-makers should also consider truly acting like creative, alert entrepreneurs, focusing on the long-term success of the company and maximizing its competitiveness.

Consequently, the author argues that the public incentives, which were provided to “promote” AFVs, were not only often exaggerated but actually harmful and inefficient from a long-term perspective. It is claimed that in a free market, once customer demand for AFVs had naturally increased, providers and consumers would have found truly adequate solutions by themselves, without public interventions [

80]. However, the automotive manufacturers have used these recent years of strong fiscal interventionism to optimize their AFV models in regard to crucial aspects such as product quality, reliability, driving range and needed recharging times. Consequently, due to the seen public subsidies and other public interventions as well as to the corresponding expected economies of scale, by the early 2030′s, several PEVs could likely be price competitive without any further governmental support.

5. Key Findings and Conclusions on Public Incentives for AFVs

Conflicts related to energy supply have often been the cause for political tensions between different states and confederations of states [

2,

29]. Accordingly, several nations intend to reduce their dependence on fossil fuels, and particularly a wide range of western countries intend to reduce their reliance on the crude oil-producing OPEC countries [

1,

19,

25]. Consequently, throughout the past decade, a notable transition towards renewable energies was incentivized by governments and multinational institutions [

2,

30,

84,

85]. Moreover, the impact of the transport sector on climate change and energy-related greenhouse gas (GHG) emissions has become a major aspect of political discussion throughout the past years [

1,

4,

84]. Vehicles run by fossil fuels such as petroleum products are not only criticized for global GHG emissions but also for causing noise and local air pollution [

2,

19]. Several studies indicate that there are crucial environmental, consumer fuel-saving and macroeconomic benefits associated with alternative fuel vehicles, which are said to exceed the costs of electric vehicle incentives [

86]. Moreover, in particular, EU-member states criticize the car-related petrol and diesel demand for having created a strong dependence on foreign energy sources. Thus, for geopolitical reasons, as well as due to the impact of the transport sector on climate change, several governments have started to provide significant public incentives to promote alternative fuel vehicles (AFVs). Throughout the past decade, several fiscal incentives were launched in Europe, Asia, North America and other regions to minimize the consumer’s total cost of ownership (TCO) of AFVs with the aim to increase their competitiveness and market share [

2,

28]. However, the currently seen transition has caused significant economic costs and an important distortion of the market [

1,

4,

85].

The author evaluated the four main alternative fuel technologies which were most successful in Europe throughout the past years: hybrid electric (H-EVs) and plug-in hybrid electric (PH-EVs) vehicles and battery electric vehicles (B-EVs) and their “sub-category” of fuel cell electric vehicles (FC-EVs).

Public entities on the EU, national and municipal levels have tried to promote AFV technologies via different fiscal and legal supports. Public incentives for PEVs have differed significantly between the individual EU countries. Governments have promoted this market growth through a combination of financial incentives such as tax exemptions and direct subsidies as well as other incentives including free parking, but also by supporting the setup of charging infrastructure [

16,

18,

84]. Public incentives for PEVs have differed significantly between the individual EU countries, while in several European markets, public subsidies and tax exemptions for PEVs have been quite substantial within recent years [

5,

6]. AFVs still face relevant barriers to adoption: barriers that are common to most new technologies, such as the lack of knowledge by potential adopters, a low consumer risk tolerance [

19,

20] and high initial production costs [

21]. By 2018, only comparably smaller Nordic countries such as Norway, Netherlands, Iceland and Sweden had a significant PEV sales growth occurred. In the Netherlands and Norway, sales volumes of AFVs have constantly been growing as simultaneously public incentives have compensated a significant portion of the AFVs’ total vehicle cost [

18]. It must be stated that in the absence of public incentives, PEVs have not been cost-competitive in any European market—despite the notable recent growth rate in PEVs sales.