1. Introduction

In the European Union (EU), the energy transition is largely shaped by the renewable energy targets set for 2020 in the 2009 Renewable Energy Directive (RED I) and for the period 2020–2030 in its recast (RED II) [

1]. In several EU countries, increased utilization of woody biomass for electricity and heat is a means to reaching renewable energy targets [

2]. In their long-term vision for a prosperous climate-neutral economy, the European Commission foresees an important role to be played by biomass, especially in sectors which are more difficult to decarbonize such as industry and (heavy) transport, by using biomass for the production of aviation fuel, industrial process heating and bio-based materials and chemicals [

3]. These different applications can all be covered by the utilization of sustainably sourced lignocellulosic biomass. A limiting factor in this is the availability of sustainable and affordable feedstock. Discrepancies between supply and demand in different countries have resulted in an emerging trade in fuel wood, wood chips and especially wood pellets between countries and world regions [

4,

5]. In 2018, the EU supplemented 17 Mt of wood pellet production with the importation of 8 Mt from the US and 2 Mt from other European countries [

6]. Increased demand for biobased energy and materials will likely result in further increases in the international wood pellet trade [

7].

With the introduction of RED II, binding sustainability criteria were established for all bioenergy sectors to ensure sustainable production. These criteria relate to aspects such as supply chain GHG emissions, the risk of indirect land use change and the protection of land with high biodiversity or carbon stock. In contrast to for example indirect land use change (ILUC) criteria, indicators for GHG savings criteria are relatively well defined and quantifiable. Minimum thresholds per end-use type have been defined. The calculation method is standardized including pre-defined fossil fuel comparators and calculation rules [

1]. For installations with a rated thermal input >20 MW, the standard is 70% savings after January 2021, compared to a predetermined fossil fuel comparator, increasing to 80% after 2026. Besides the imposed threshold on supply chain GHG emissions, there are market constraints for total supply chain costs. The fact that wood pellet utilization is in competition with fossil energy such as coal and natural gas as well as other renewable energy technologies limits maximum supply chain costs.

As shown in previous studies, the cost and GHG performance of solid biomass depends to a large extent on supply chain design such as the type of feedstock used and transport distances. The US currently is globally the largest exporter of wood pellets, mainly to western Europe [

6,

8]. With increasing demand, the question is whether new trade routes will emerge, utilizing unused fiber baskets in other world regions. Existing literature studies have concluded that an increase of wood pellet consumption in the EU may result in increased imports from, amongst others, Russia, Canada, Brazil and the US [

7,

9,

10]. What these studies however did not take into account is the detailed spatially explicit availability of feedstock and how this impacts supply chain costs and emissions. Emerging trade routes and import potentials can only be assessed by considering detailed mobilization and trade potentials at different cost and emission levels, and by comparing this to market and legislative constraints.

Supply chain costs and emissions could potentially be optimized by introducing additional pre-treatment technologies, such as thermochemical treatment to produce torrefied pellets (TOP). Combustion of pellets is more challenging than coal, introducing issues such as mechanical degradation during storage, efficiency loss resulting from lower energy density and increased ash deposition in boilers [

2]. Using TOP instead of white pellets (WP) could reduce some of these issues. TOP have increased grindability and hydrophobicity and a higher energy density, resulting in lower transport costs and emissions [

11]. On the other hand, the production of TOP increases processing costs and introduces an additional, energy consuming, processing step. Whether a transition towards using TOP instead of WP results in optimized costs and emissions of bioenergy production depends on the design of specific supply chains. This research will analyse and quantify the potential role for TOP in meeting current and future GHG and cost criteria. This analysis will show whether there are favourable conditions for TOP production and trade, as well as whether production of TOP unlocks increased production areas.

Policy making in the context of climate change can be based on integrated assessment modelling of the impact of different pathways or specific policies on carbon emissions or global warming. European energy system models, such as the Price-Induced Market Equilibrium System (PRIMES) [

12], the JRC-EU-TIMES model [

13] and global integrated assessment models such as IIASA’s Global Biosphere Management Model (GLOBIOM )[

14], the IMAGE model framework [

15] and the Global Forest Products Model (GFPM) [

16] are generally based on default biofuel supply chains, not accounting for supply shifts resulting from increased demand. Whereas these models do account for regional variation in costs of labour, land or capital, the impact of spatial feedstock availability and logistics on biomass costs is not included. The role of biobased energy and materials production in the energy transition can only be understood by incorporating a detailed characterization of logistics required to mobilize large quantities of biomass. The large impact of supply chain design on costs and emissions of bioenergy necessitates the inclusion of spatial impacts in global energy modelling. Sustainable import potential of pellets from different world regions to the Netherlands were amongst others analysed by Mai-Moulin et al. [

17]. Mai-Moulin et al., however, did not consider the spatial availability of feedstock and the impact of transport networks and distances in detail.

This article is based on the premise that a sharp worldwide reduction in GHG emissions will be pursued and realized, and that biobased energy and materials have an important role to play to achieve the required emission reductions. Within this article, the focus will be on solid biomass in the form of wood pellets, produced from forestry biomass in the US, Canada, Brazil, Russia and the Baltic States and imported to Western Europe. In this study, a spatially explicit assessment is made of import potentials, based on the growing stock of forestry biomass, limited by an exclusion of protected and high-biodiverse land as well as local use for energy and non-energy purposes. These potentials are combined with an explicit assessment of wood pellet supply chain costs and emissions, including the transport requirements from inland locations to export ports. Costs and GHG emission thresholds are applied to calculate potential import quantities to western Europe as well as maximum potential sourcing areas in the different countries for pellets and torrefied pellets.

2. Materials and Methods

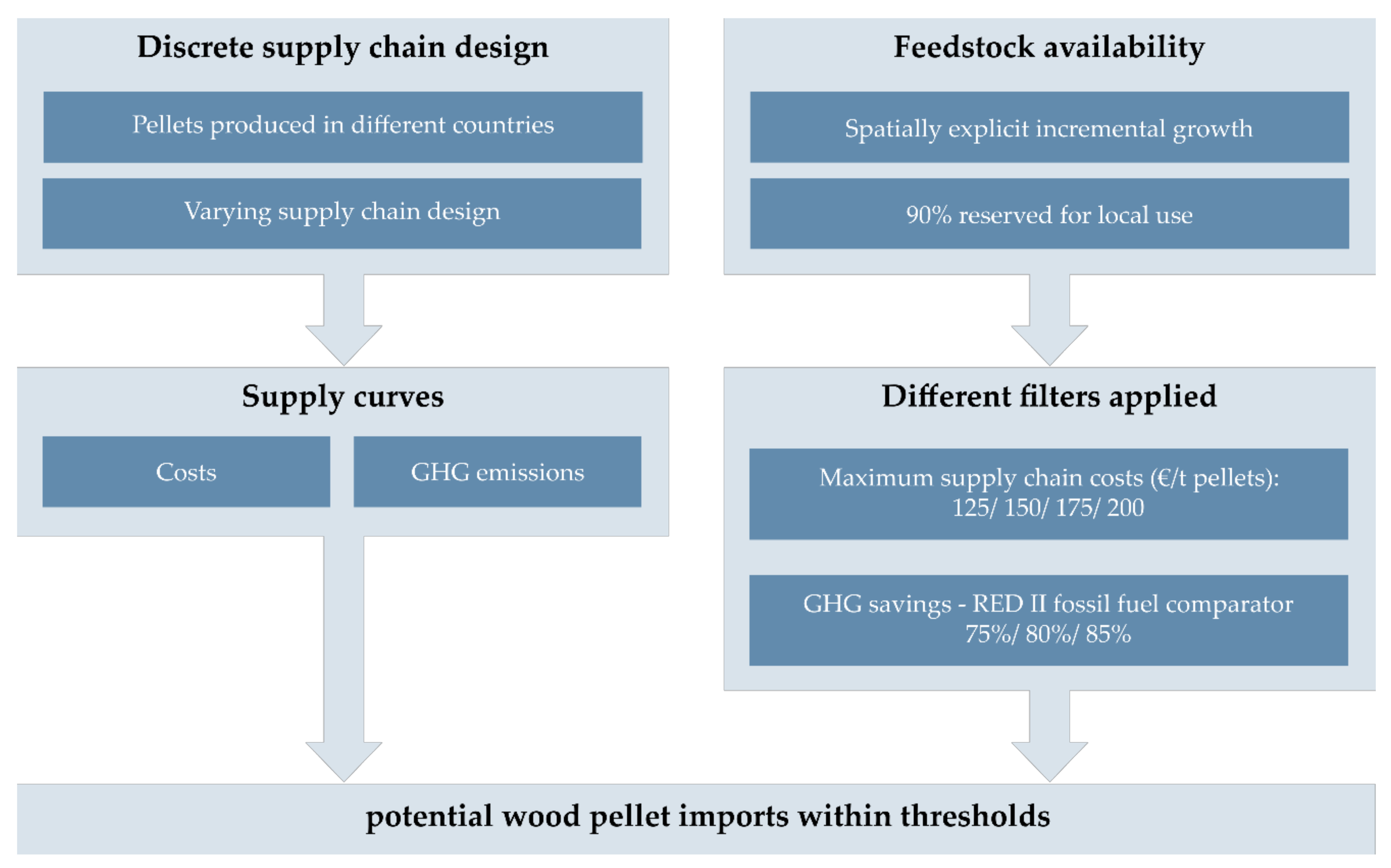

This work consists of a few different components, see

Figure 1. Firstly, supply chain design costs and emissions were calculated for discrete supply chains from selected sourcing countries (United States, Canada, Brazil, Estonia, Latvia, Lithuania, Russia). Certain supply chain design characteristics were varied to analyse the impact on total costs and emissions, specifically the choice between pulpwood and sawmill residues, and the distinction between wood pellets and torrefied pellets. The impact of inland transport distance was also calculated. See

Figure 2 for the impact of design variables on the included cost components. Secondly, pellet production potentials were calculated in the different countries based on feedstock availability in forests. These two parts were combined to generate costs and GHG supply curves, including the impact of inland transport. By applying different cost and emission criteria, the total potential availability of pellets under different circumstances was analysed.

When using “wood pellets” or “pellets” in the remainder of this article, this is always in reference to regular pellets from forestry biomass. The selection of sourcing countries was based on current pellet production and consumption and on the potential for future production increases [

5,

7,

18,

19]. Supply chain costs and GHG supply curves of potential pellet production and trade were constructed based on the locations of export ports suitable for pellet export, within the including sourcing countries. Results from costs and emission analyses were used in the calculation of maximum supply areas and the total potential pellet production that can be supplied from these areas. This potential was calculated based on incremental growth of forestry biomass in spatially explicit forestry areas. Areas assumed high in biodiversity were subtracted from the total area, including protected areas and areas previously untouched by human exploration, considered a good estimation of the extent of primary forests. Of the incremental growth, a share of 90% was assumed to be reserved for existing local energy and material use. The GHG emission thresholds used were the 70% and 80% included in the RED II standards, as well as 85% in reflection of further tightening of emission criteria. Calculations were based on the fossil fuel comparator for electricity and heat production as outlined by the Joint Research Centre (JRC) [

20]. These comparators represent typical or default GHG emissions of fossil electricity and heat production, and are based on a marginal mix of present and perspective power production and feedstocks [

20].

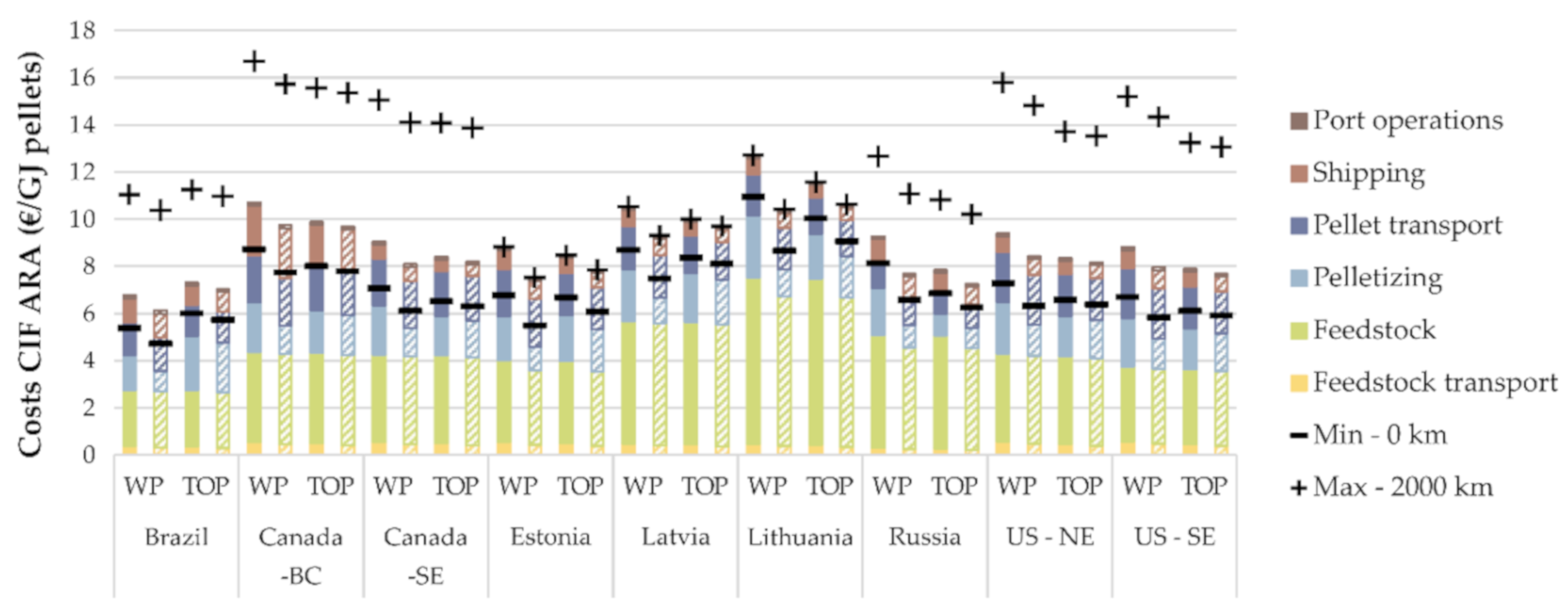

For the calculation within cost limits, a few criteria were included. A limit of 150 €/t pellets CIF ARA (costs, insurance and freight at the Amsterdam-Rotterdam-Antwerp ports), was used as reference, based on contract prices of pellets from Canada and the US fluctuating around this price level between 2012–2017 [

21]. As a lower limit, total costs of 125 €/t pellets were assumed, reflective of a situation in which there are fewer subsidy schemes supporting the use of wood pellets, and prices need to be more competitive. On the other end of the spectrum, cost limits of 175 and 200 €/t pellets were used. These higher costs represent scenarios in which the use of wood pellets is increasingly subsidized, or in which the use of fossil fuels has become considerably more expensive. The maximum costs for torrefied pellets were assumed to be equal to regular wood pellets on an energy basis, and therefore 114% higher per tonne of pellets. Shipping costs and emissions were calculated to the Port of Rotterdam and are considered representative for the entire Amsterdam–Rotterdam–Antwerp (ARA) region. The expected price difference between all ports in western Europe is very small based on the small difference in shipping distance. Therefore, these results can also be considered a very close representative for other import regions in for instance the UK, Belgium or Denmark.

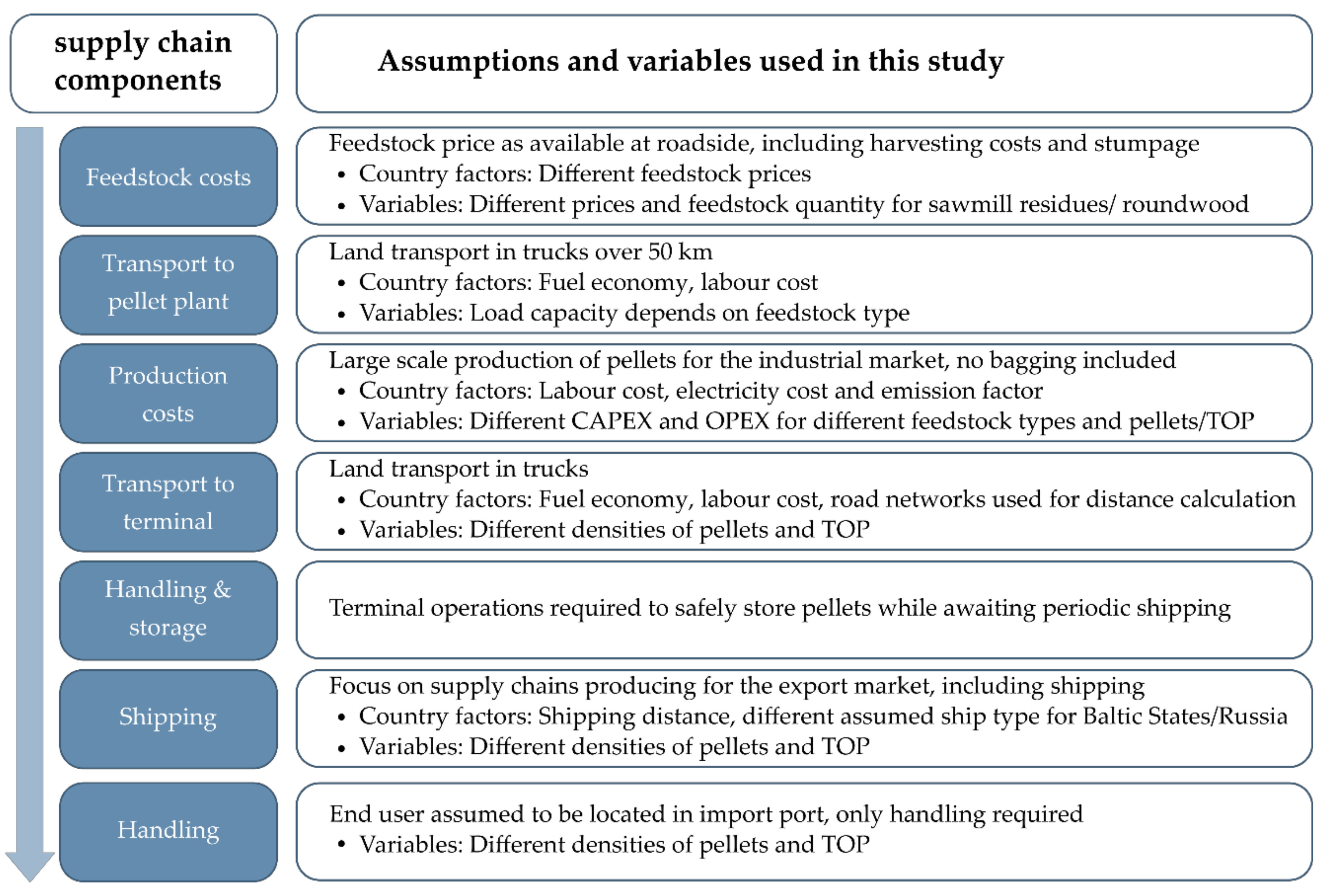

Supply chain components included in the cost and emission analyses can be seen in

Figure 2. For each component, assumptions were made on the specific supply chain design, as explained in

Section 2.1. These design choices impact the total costs and emissions and therefore have an impact on total calculated production potentials as well. For certain components, such as shipping, costs vary only with the type of ship used and the shipping distance. For other components, country differences were included, for instance in the form of differences in fuel, electricity and labour costs.

2.1. Supply Chain Costs and Emissions

The RED II GHG calculation methodology for biofuels prescribes that total emissions need to be calculated as the sum of emissions from raw material extraction/cultivation, emissions from processing, transport and distribution, emissions from fuel combustion and annualized emissions from carbon stock changes, minus emission savings from carbon storage through improved forest management and CO

2 capture and geological storage or replacement [

1]. This methodology was applied to the calculation of emissions in this research, with the exception of both positive and negative carbon stock changes caused by land-use change or improved management. Whereas changes in carbon stock can add significantly to total emission savings or losses, it could not be assessed within the limited scope of this paper. Production of energy from biofuels was not assumed to be combined with carbon storage or replacement, since this technology is currently not widely used and is not considered an available option for most bio-based power plants. This yields the following Equation (1) for total emissions (E), adapted from the RED II methodology [

1]:

where (e

ec) is the emissions from extraction or cultivation of raw materials, in this case forestry residues, (e

p) are the processing emissions from the production of pellets, emissions from transport and distribution (e

td) is a combination of the transport of raw material and transport of pellets in the production country and internationally, until delivery at energy companies located in the Port of Rotterdam. This category also includes loading and unloading at the various supply chain locations. Following RED II methodology, emissions from combustion of biomass to fuel processes (e

c) only includes non-CO

2 GHG. The emission factors for pellets of CH

4 and N

2O were taken from [

22], and were converted to CO

2-eq by using the global warming potential values for a 100-year time horizon from the Intergovernmental Panel on Climate Change (IPCC) Fifth Assessment Report [

23].

Savings (S) were calculated compared to RED II fossil fuel comparators for electricity (F

el) and heat (F

h) of respectively 183 and 80 gCO

2-eq/MJ

th. Efficiencies of energy production were assumed to be 40% for electricity and 89% for heat, based on pellet-based electricity or heat production, following Equation (2) [

1,

24].

2.1.1. Market Prices and Costs

There is a difference between supply chain costs and prices, depending on whether profit margins are included for the different components. In this research, wherever possible, calculations were based on costs, excluding profit margins for supply chain actors. This was considered to yield more robust results since profit margins can vary significantly between different supply chain actors and will vary over time as a response to market dynamics. An exception to this is the costs of feedstock. Calculating the biomass costs based on stumpage fees and harvesting and collection costs was not feasible for all countries since data on these components is lacking. Therefore, the choice was made to use biomass prices available at roadside instead of biomass costs to achieve homogeneous results across all regions. In the remainder of this article, the term cost will be used for all supply chain components, in the case of feedstock this refers to the biomass prices paid by pellet producers. The development of feedstock prices is uncertain and depends on many factors such as demand developments, competition for feedstock, improvements in infrastructure or technological innovations and productivity of forest areas. Especially in new markets, without large pellet sectors, the impact of increased feedstock demand for pellet production on feedstock prices is uncertain. Potential market developments and changes in feedstock prices lie beyond the scope of this article and could not be assessed. The assumption was made that current costs of feedstock are stable and will remain constant when demand increases.

2.1.2. Extraction and Cultivation

The different forestry feedstocks modelled are pulpwood, logging residues and sawmill residues, with assumed moisture contents of 50% for pulpwood, 55% for logging residues and 30% for sawmill residues [

25]. Pulpwood is defined, following the definitions used by the U.S. Forest Service, as wood that does not meet the quality standards for sawlogs, including a diameter at breast height over 23 cm for softwood and over 28 cm for hardwood, but does contain a minimum of 50% sound wood fiber by volume [

26,

27]. Definitions of pulplogs and sawlogs could be different in other countries. Country specific data on prices of pulplogs, as will be discussed in

Section 2.1.3, were used as such, without adjusting for differences in definitions. In case data was available for different diameter classes, the specific diameter class assumed will be specified. The volume of a tree meeting sawlog standards furthermore only includes the part of the trunk from a 1-foot stump to a 15 cm diameter top (softwood) or 20 cm diameter top (hardwood) [

27]. A felled tree can therefore yield sawlog as well as pulplog timber, with tops and branches being classified as logging residues. Pulplogs are too small and of too low quality to be used by sawmills but can be used by other forest product industries such as pulp and paper companies and pellet mills. Logging residues are generated during harvesting activities and consist of damaged or degraded trees that cannot be utilized by industries requiring premium timber, as well as tops and branches of harvested trees. Sawmill residues consist of residues generated during sawtimber production processes that are available for use by other industries. This consists of a mixture of sawdust, shavings and chips. Per RED II prescribed methodology, feedstock supply emissions are only allocated to pulpwood and not to residues. Allocation was done on mass basis for reasons of simplicity, instead of energy basis which would be more realistic [

28]. See

Table 1 for fuel input during forestry management. This data is based on medium productive forest plantations. Not all forestry production in the included countries will be based on cultivated forestry feedstock, and while this study excludes biomass from primary forests, other types of forests, such as natural or semi-natural forests are included in accordance with RED II methodology [

1]. Still this data is considered a good assumption since pellet production is facing relatively strict sustainability criteria, favouring the use of feedstocks from forestry plantations as opposed to feedstock from more natural forests. Furthermore, an increase in feedstock demand for pellet production is expected to result in increased management of forests [

29].

2.1.3. Feedstock Price

The costs of harvesting were not explicitly calculated, since prices for biomass were reported on the basis of roadside costs, including the costs for forestry management, harvesting and collection. This study relies largely on country specific prices of forestry fibers, thereby not considering regional differences. An exception is made for the US where a distinction was made between the Southeast (SE) and Northeast (NE), and Canada where a distinction was made between the Southeast and Southwest (SW). The United States Energy Information Agency (US EIA) publishes monthly data on the average feedstock prices paid by pellet producers [

32]. This is considered a good approximation to use for the Southeast, since pellet capacity in the US SE makes up 70% of the capacity in the entire country. The average price of 2018 was used, calculated from monthly data on average prices and production quantities. US EIA data is given for different feedstock types, among which roundwood/pulpwood and sawmill residuals. There is no significant difference in prices between the different feedstock types reported by the US EIA [

32]. Therefore, the assumption was made that prices for raw material are equal for all feedstock types in the US SE, at least on a wet basis.

Prices in Canada, US and Brazil were calculated relative to the US EIA data. Forest2Market reported on prices of hardwood and softwood in Brazil, the SE US and NE US and SE Canada and SW Canada in 2017 [

33]. From this data, an average value of softwood and hardwood prices was calculated for these regions. This value was converted to the level of US EIA feedstock prices using the ratio between the US EIA and Forest2Market prices for the SE US. Feedstock prices in the Baltic States and Russia were taken from a variety of sources. Data was available for pulplogs or sawlogs, sometimes of specific specified species and tree size categories. Feedstock prices in Estonia were based on pulpwood biomass from state forests and were first averaged for softwood and hardwood species using data on the distribution of fellings [

34]. Latvian data, for the second quarter of 2018, taken from the central statistics bureau, distinguished between different species and diameters. Softwood prices are 65–95% higher than hardwood prices and are reported in different size categories. Considering this large price difference, the assumption was made that in the case of Latvia pellet production would be based on the more affordable hardwood species. Pulplog prices were based on average costs of hardwood trees < 24 cm diameter. Lithuanian data was given as the average price of pulpwood sold from state forests in 2018, per cubic meter [

35]. Russian feedstock prices were based on price data for pulpwood, averaged for softwood and hardwood species [

36]. For the various countries, data on residue prices could not be found. Therefore, just as in the US case, prices of harvest and sawmill residues were assumed equal to the price of pulpwood, at roadside or the mill gate where residues are produced, on a wet basis.

2.1.4. Processing

In the case of pulpwood use, pelletization of forest biomass starts with debarking, and course grinding to obtain similar particle size. All feedstock types then require drying and fine grinding in a hammer mill, pelletization, cooling and storage [

37]. Cultivation and transport emissions of feedstock consumed for drying purposes were allocated to pelletizing emissions. Energy consumption for the different pelletizing components was taken from several literature studies, with the average of multiple values being used [

38,

39,

40,

41,

42,

43,

44]. During pelletization, a loss of 1% feedstock was assumed. The produced pellets were assumed to have an energy content of 17.5 GJ/t and bulk density of 0.65 m

3/t. For the generation of electricity and heat, pellet mills were assumed to generate heat in a boiler fuelled with biomass, assuming an efficiency of 85%, with the additional use of grid electricity [

20]. All assumptions on energy requirements and efficiencies are included in

Table A6 of

Appendix B.

Pelletizing costs are difficult to determine, as discussed in [

37]. Using the data laid out in this article, three different values were assumed for pelletizing costs, the median value of costs from literature was used as the baseline, medium cost value. The first and third quartile values were used as a low and high scenario for the calculation of pellet production potentials. Part of the variation of literature costs can be explained by supply chain design differences. In this study, a distinction was made between capital costs, maintenance costs, labour costs and costs for electricity and heat production. Capital costs are kept constant for all feedstock types, with the exception of costs for grinding equipment, which is not required when using sawmill residues. It must be noted that in practice many pellet mills will use a mixture of feedstock types and will therefore also require grinding equipment. The option of exclusively sawmill residues-based pellet production is however considered feasible in case of close proximity to and collaboration with lumber mills. For this reason, this study includes a cost analysis of pellet production based only on sawmill residues, using some adapted cost factors as explained in this section. Maintenance costs are assumed to be constant for all feedstock types and sizes, and were based on Pirraglia et al. [

44]. The base labour costs were based on the United States. Costs in other country were calculated by applying a cost factor based on hourly wages compared to the US, as given in

Appendix A. Labour requirements and costs were assumed to be equal for all feedstock types.

Emissions of torrefied pellets were calculated using the same assumptions and data as for wood pellets. During torrefaction, biomass is heated to 200–300 °C in the absence of oxygen, resulting in the devolatization of hemicellulose and cellulose [

45,

46]. Pellets from torrefied material have improved characteristics such as a higher energy and bulk density, 20 GJ/t and 0.75 m

3/t respectively, increased brittleness and improved hydrophobicity. During the torrefaction process, roughly 30% of the input mass is turned into several volatile components [

46]. The torrefaction gas emitted through this process can be combusted to provide the heat required for the torrefaction process as well as drying of the biomass prior to torrefaction. Total processing heat demand and the heat supply generated by the combustion of torrefaction gas was calculated based on Mobini et al. [

42]. The main cost and emission factors of pellet production used in this study can be found in

Table 2.

2.1.5. Transport and Distribution

Feedstock is assumed to be transported by truck to pellet plants. Weight limits vary for different feedstock types, as can be seen in

Table 3. Fuel consumption was based on a load of 26 tonne/truck, which was adapted to other weight limits, based on an assumed linear relation between weight and fuel consumption [

47]. Costs were calculated using different diesel prices, of May 2019, in the respective countries. Road transport includes costs for labour, against country specific labour prices. Fuel and labour costs for the different countries included in this study are given in

Appendix A. To any trip, 50% of the total duration was added for loading/unloading, driver breaks and delays. Trucks were assumed to work at 100% capacity for the trip from forests to pellet plants. Transported feedstock was assumed to contain some contaminants in the form of sand or metals, measuring up to 3% of the total mass.

For transport of pellets, both road and rail transport were considered viable theoretical options. Road transport is calculated in the same way as feedstock transport but based on an assumed load limit of 25 t/truck [

22], using heavy diesel trains. Since separate data on fuel consumption was available for the United States, Canada and the EU, the distinction was made between these geographical regions. For all other regions, the emissions of the United States were assumed. Costs of rail transport were based on a fixed price and a distance dependent price of the railway company CSX Transportation (CSXT) in the United States, as given in Gonzales et al. [

48]. Return trips on both road and rail are assumed to be empty, with emissions and costs being fully allocated to feedstock transport based on the empty weight of trucks and rail cars [

30]. Detailed information on transport cost calculations can be found in Visser et al. [

37]. General cost calculations to compare the different countries were based on a feedstock transport distance of 50 km and a transport distance from pellet plants to export ports of 500 km, via road transport.

2.1.6. Shipping and Port Operations

Shipping fuel consumption was calculated as in Visser et al. [

37], largely following the methodology as given in [

22]. Fuel consumption and emissions were calculated for four different ship types: short sea ship (SSS), Handysize, Handymax and Supramax. Fuel consumption was taken from the International Maritime Organisation and shipping distances between two ports were taken from online calculation tools [

53,

54]. Pellet transport from the Baltic countries and Russia was assumed to be done in an SSS vessel with a deadweight capacity of 10 kt. The other ports were assumed to be able to utilize the three larger ship types, which were varied in different scenarios, with a Handymax ship used as the reference case. Shipping costs were calculated using data on fuel costs and charter costs, both of which fluctuate over time and are therefore uncertain. Both fuel costs and charter costs were varied in a low, medium and high option, as can be seen in

Table A5.

Emissions from engine use during berth, anchorage and manoeuvring operations were included during the period of loading and unloading, and vary per ship size [

55]. The maximum unloading capacity was based on the Port of Rotterdam, and was set at 10,000 t/day [

54]. This unloading rate does not include potential delays caused by bad weather or scheduling difficulties. The assumption was made that loading emissions equal the unloading emissions. Additional terminal operations were also included, including the emissions from ship unloading and conveying of pellets [

56]. These operations are based on the Rotterdam terminal as well, assuming pneumatic ship unloading and conveying across 1500 m [

54]. Costs of port operations were based on the above methodology, calculated using country specific costs of electricity. Labour costs were left out of this equation since these depend largely on the degree of automation and form a small part of total costs compared to, for instance the daily charter costs.

2.2. Techno-Economic and GHG Supply Potential

2.2.1. Feedstock Availability

The impact of maximum supply areas was calculated by totalling the feedstock availability within supply areas in the different export countries. The availability of mill residues was excluded since this availability is inherently limited by the existence and proximity of other industries, and reliable spatial data on the extent of timber and paper industries in all included countries was not available. Logging residues were also excluded from total availability. Although this source of feedstock could be utilized for pellet production, mobilizing these residues requires significant effort and is usually not cost efficient compared to pulpwood [

57]. Increased use of logging residues instead of pulpwood presumably requires the existence of specific policies or support schemes. Furthermore, the extent of logging residue availability depends on the type and size of trees as well as the minimum merchantable diameters specified locally, and is therefore difficult to estimate spatially explicit [

58]. The total potentials calculated in this study can be considered indicative of the differences between various production regions but are not considered to represent accurate estimates of pellet production potential. The potential availability of forestry feedstock was analysed spatially explicit, based on raster maps of forested areas in the different countries. Detailed information on the data used for all different countries can be found in

Appendix C. All data given in volume was converted to weight based on a value of 990 kg/m

3 green wood, taken from [

59], calculated as the average between softwood and hardwood at 50% moisture content (MC) on a wet basis. Per tonne of pellets, 2.1 tonne of pulpwood feedstock is required. Calculated using the MC of 50% and a MC of dried feedstock of 8%, an efficiency of heat production of 85% and heat requirement for drying of 1200 kWh/t of evaporated water [

38,

40].

2.2.2. Sustainability Restrictions

To ensure that use of bioenergy results in carbon savings, the total forestry stock should not decrease, as required in the RED II. For this reason, total availability of forestry resources in this study was based on current annual incremental growth as opposed to total growing stock. Annual growth varies per tree and forest type, forest management intensity, climate and other factors. Whereas spatial data on annual growth was available for some countries, for other countries estimates had to be made on available data and additional literature.

Appendix C shows the method used in the different countries to calculate feedstock availability. This includes additional sustainability criteria such as the protection of land with high biodiversity value. Although it was not considered feasible to do a detailed analysis of biodiversity and species richness, this concern was included through the exclusion of untouched forest areas and areas marked as protected areas from total forest areas. In the case of Brazil also areas inhabited by indigenous people were excluded. In the case of the Baltic States, availability was taken from wood production maps, as analysed by the European Forest Institute. These maps already include several locational factors such as protected areas, and the resulting maps were used as such [

60,

61]. To avoid distortion of local markets and displacement of emissions, pellet production should not use feedstock already used locally for production of other forest products [

61]. The existing demand for forestry feedstock could not be assessed sufficiently detailed for the different countries. Instead a fixed percentage of incremental growth was assumed to be available for pellet production. In the US SE, in 2014, forest harvest removals for pellet production represented < 3% of removals in the entire region [

62]. Since then, pellet production in the SE US has doubled roughly, resulting undoubtedly in more removals. As upper limit in this study a value of 10% of the total annual increment was assumed. This forestry feedstock availability was assumed to be in the form of pulplogs, excluding harvest residues such as tops and branches. The collection and processing of residues requires several additional processing steps, necessitating the development of new procedures while the biomass is of relatively low energetic and monetary value. For this reason, the assumption was made that pellets will be produced from pulpwood and not from harvest residues. Other factors, such as the amount of biomass that needs to remain in forest areas to satisfy biodiversity and soil quality standards were not included [

17].

2.2.3. Mobilization

Pellets can only be produced and exported cost efficiently if feedstock can be transported across roads and is located close enough to export ports. To analyse this, the availability was calculated in relation to distance from the main export ports, in 100 km tranches based on the use of road networks, until a maximum of 2000 km. Distances from export ports that exceeded 100 km were assumed to be covered by transport of pellets and not feedstock. Transport distances were calculated based on Railroads maps and OpenStreetMap, as made available by Esri [

63] and Geofabrik [

64]. Assumed speed limits were varied for motorways (80 km/h), primary and secondary roads (60 km/h) and tertiary and residential roads (40 km/h). In the Baltic states even smaller, unpaved roads were included (20 km/h), unlocking additional forested areas. In the case of the US, where road networks are very extensive, all roads smaller than secondary roads were excluded. Transport across road with an assumed speed limit <80 km/h was factored according to the additional costs per distance, depending on the balance between fixed and variable costs. Service areas were calculated in ArcGIS using the Network Analyst Service Area tool (ArcGIS 10.7, Esri, Redlands, CA, USA). In calculating the availability within limits of maximum costs and GHG emissions, the maximum distance of each service area was used, e.g., the costs of pellets from a service area between 0–100 km were calculated using 100 km as transport distance value. In case of overlapping service areas, as is the case with several export ports in close proximity, the potentials were allocated based on lowest costs and emissions to a single export port.

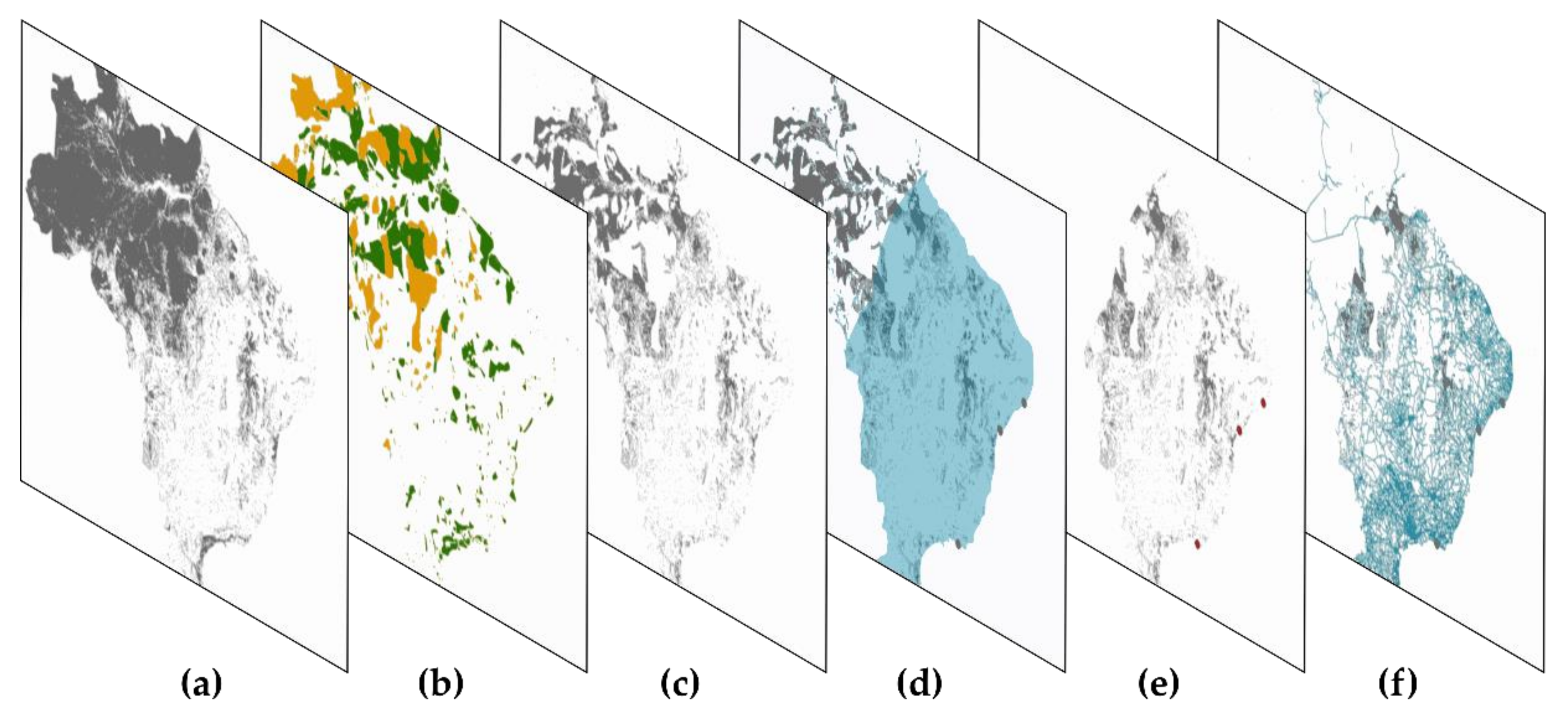

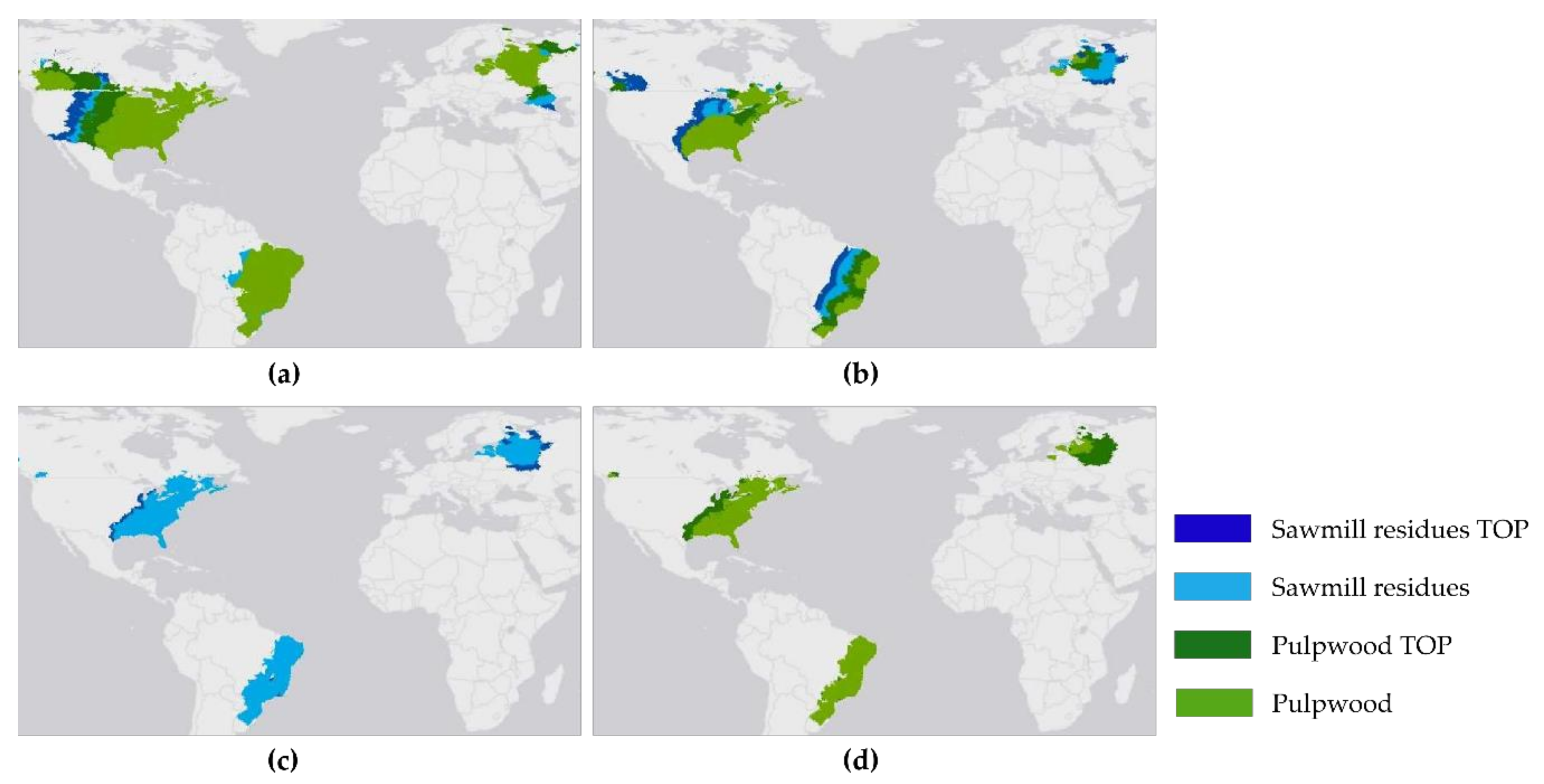

Figure 3 shows an example of the exclusion of forested areas based on biodiversity concerns or transport distance to export ports in Brazil.

5. Conclusions

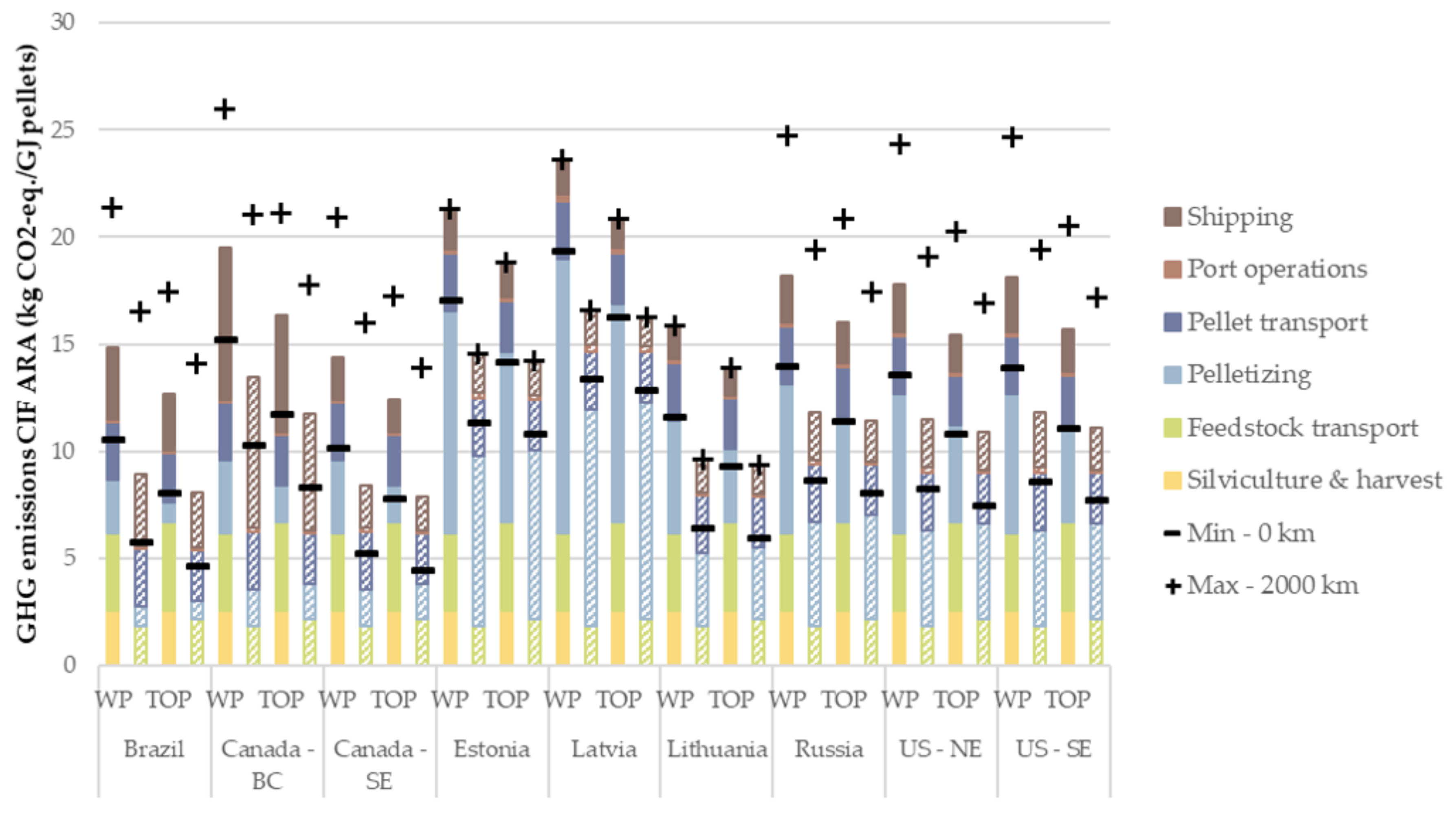

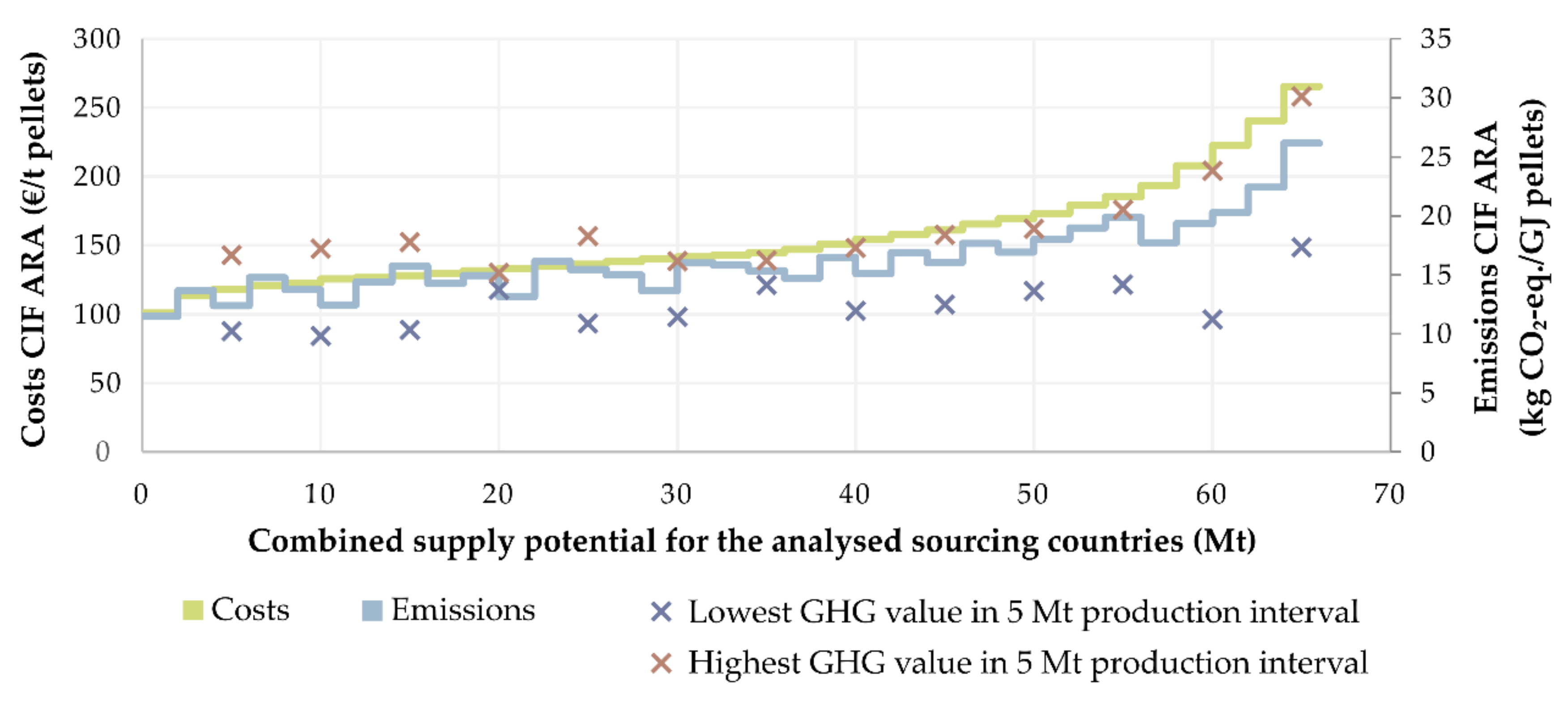

This study has shown large differences in supply chain costs and emissions of pellets imported from different countries to the CIF ARA region. Cost for procuring feedstock is the largest part of most supply chains and determines to a large extent the order of countries. The difference between the lowest and highest costs is a factor 3, ranging between 90 and 280 €/t pellets for the total production potential calculated. The impact of inland transport is large, adding up to almost 150 €/t pellets to the total supply chain costs. Pellets exported from the United States for instance range from 103 to 252 €/t pellets CIF ARA, when varying the transport distance from pellet mills between 0 and 2000 km for pellet mills that are located far inland. The costs and emissions calculated in this study are based on several assumptions and are therefore uncertain to some degree. What is however considered very robust, is the large relative impact of feedstock availability and transport distance on total costs and emissions. This work therefore shows the importance of considering spatial feedstock availability and competition in assessments on the potential contribution of bioenergy.

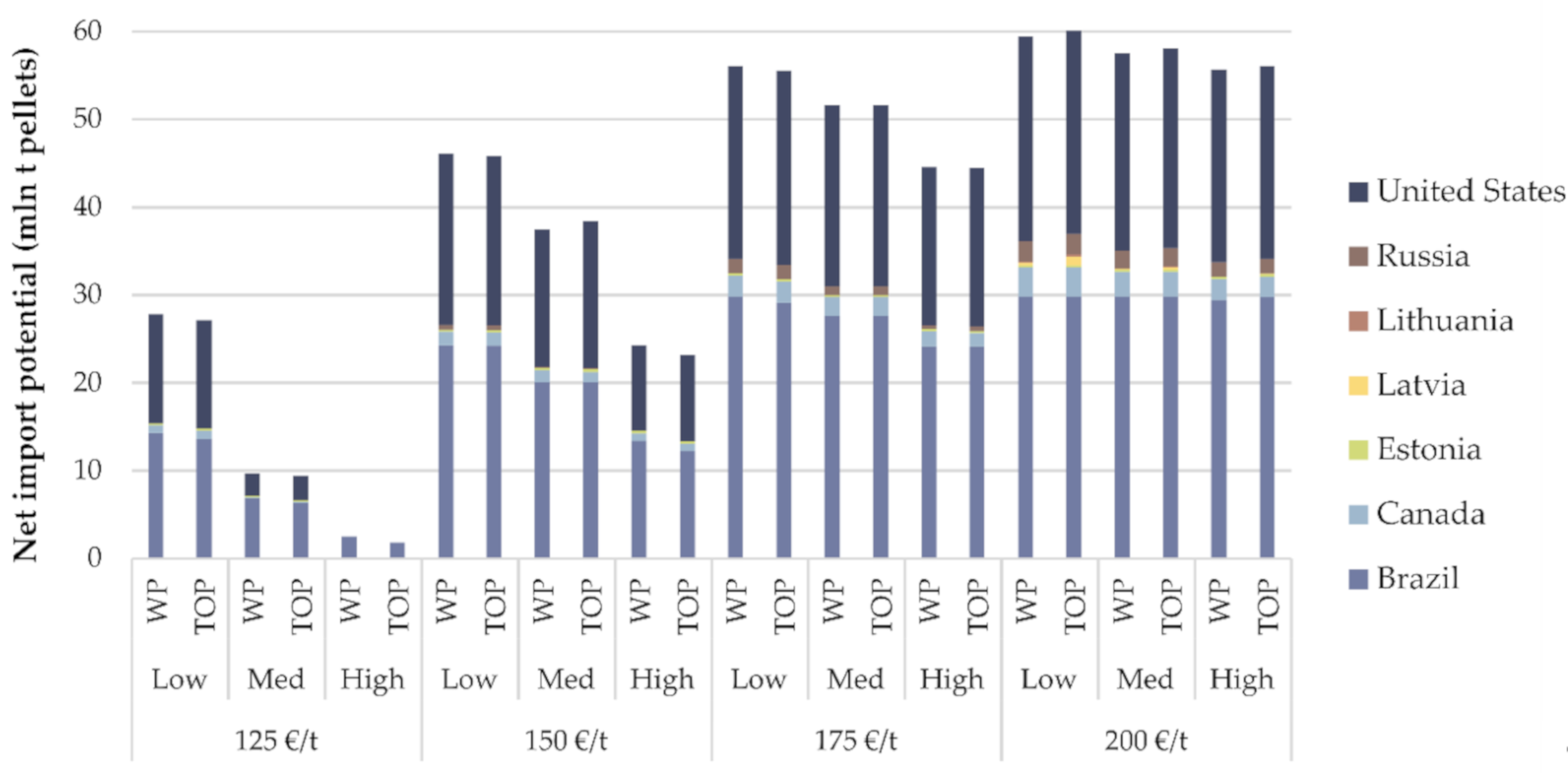

The cost limits analysed in this study clearly show diminished potentials for a cost limit of 150 €/t and especially 125 €/t. In the case of 125 €/t, production would be limited to only the coastal areas of Brazil and SE US. These costs are considered a good representation of spot and contract prices in previous years, even though no direct comparison can be made since pellet prices include profit margins for the different supply chain actors. Spot prices have varied between 110 and 160 €/t pellets between 2012 and 2017 and contract prices in the US and Canada have varied between 95 and 180 €/t pellets in the same years [

21]. Increasing demand for pellets could result in higher prices and more opportunities for supply chain optimizations, thereby increasing maximum supply chain costs. On the other hand, wood pellet consumption in previous years has been subsidized. If these subsidies were to be removed, the paying capacity and therefore maximum supply chain costs would reduce.

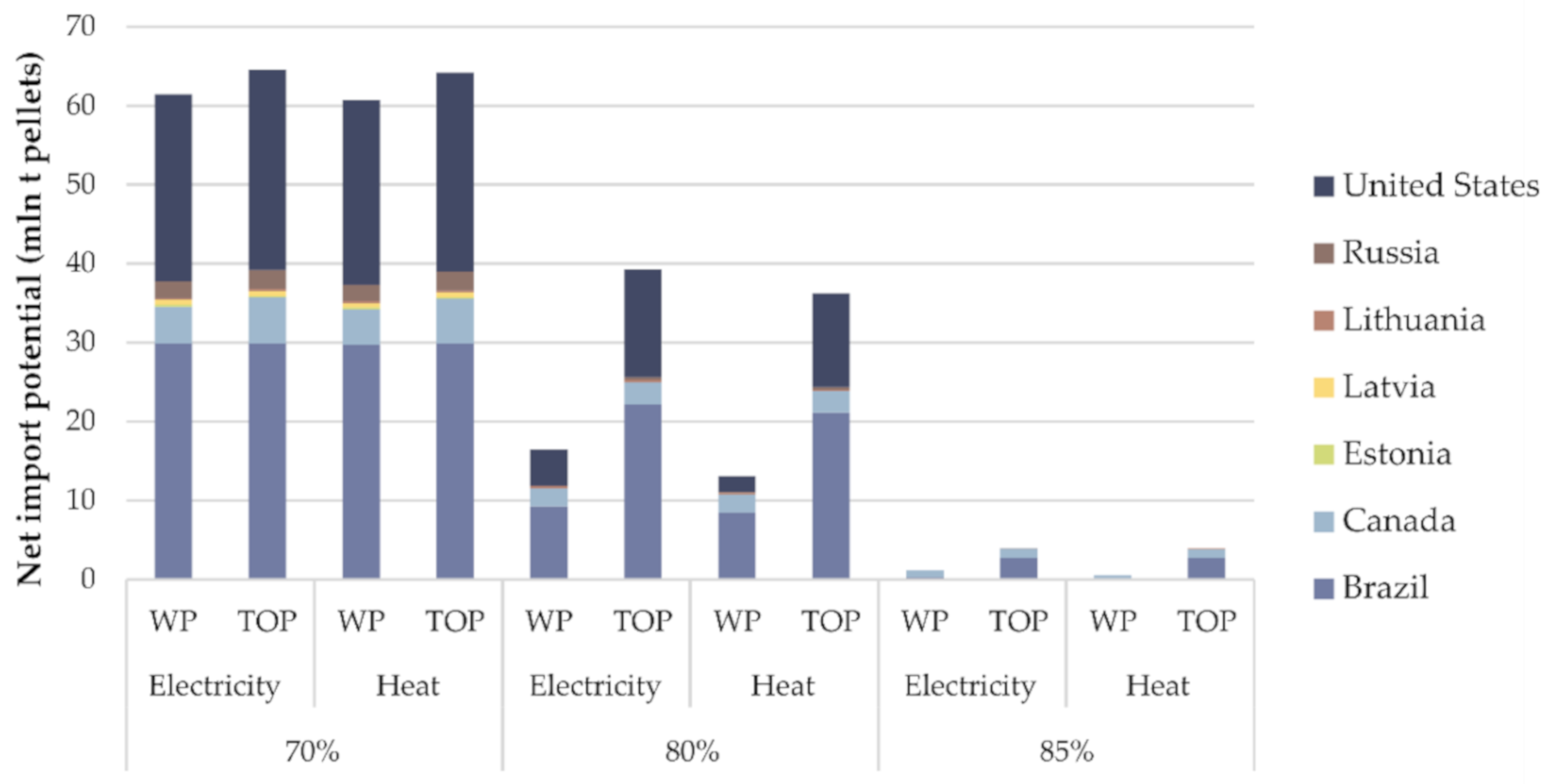

Stricter GHG thresholds have a significant impact on import potentials, especially in the case of electricity production. If the minimum GHG saving threshold is increased from 70% to 80%, the total potential will reduce from 61 to 16 Mt in the case of electricity production from pellets. With an 85% reduction threshold, only 1 Mt of the total export potential remains. For heat production, potentials decrease from 61 Mt under a 70% threshold, to 13 and 0.5 Mt using the stricter criteria. A shift to TOP would increase potentials to 39 Mt and 36 Mt for electricity and heat production respectively under the 80% criterium. The additional potential for TOP is however limited in the case of the 85% threshold, resulting in a total of 4 Mt. The sharp reductions of potentials towards the 85% threshold clearly indicates an upper limit for international trade of wood pellets and TOP. Increasing GHG thresholds will result in larger relative emission savings, but could also limit the amount of biomass use, and as such postpone the further decarbonisation of the European economy. Policy makers need to be aware of this trade-off between ambitious GHG thresholds and the potential contribution of biomass to renewable energy targets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}