A Coordination Mechanism For Reducing Price Spikes in Distribution Grids

, , and

, , and

Abstract

1. Introduction

2. Theoretical Background

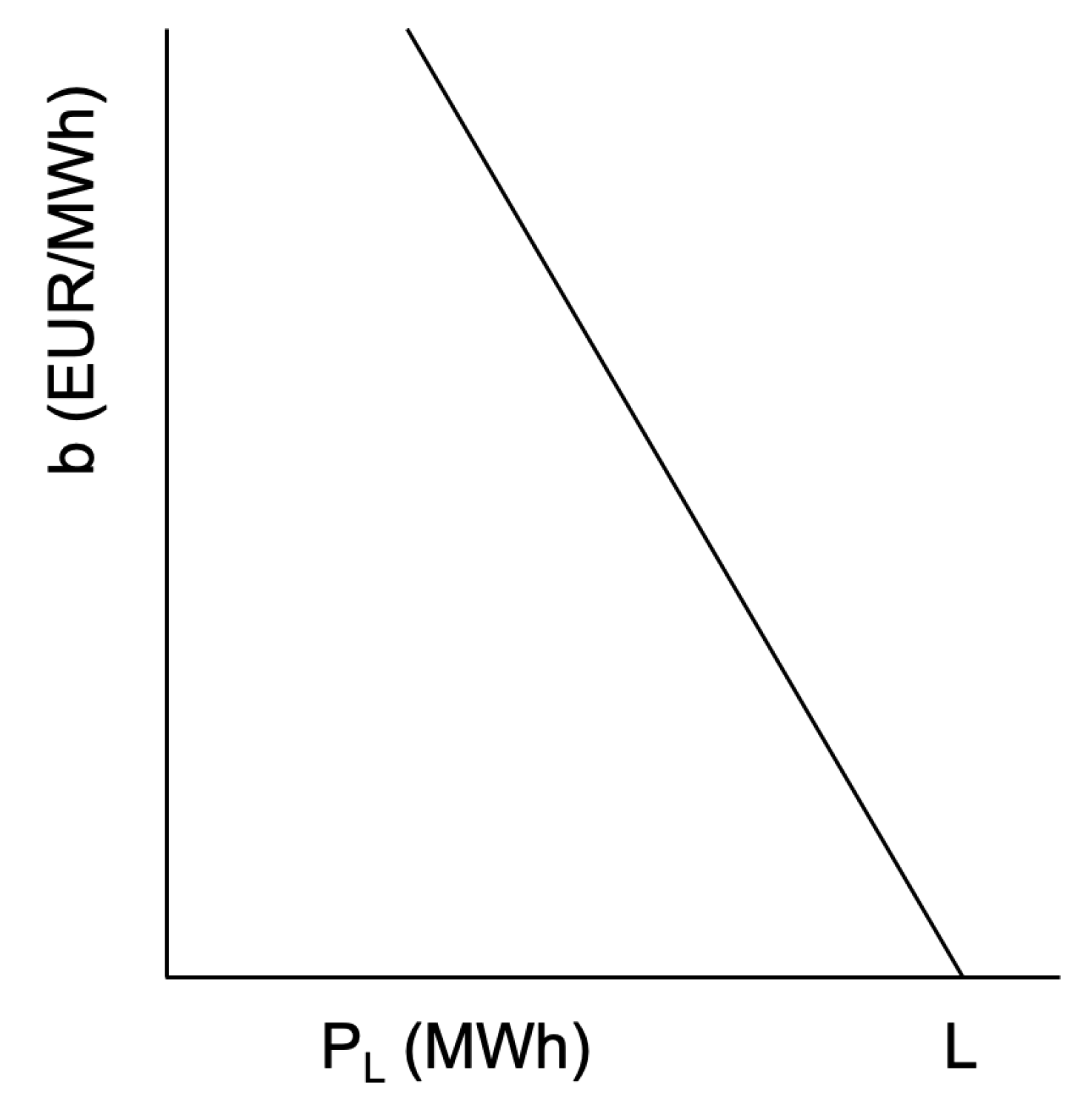

2.1. Capping Electricity Prices with Flexible Resources

2.2. Capping the Electricity Price in a More General Case

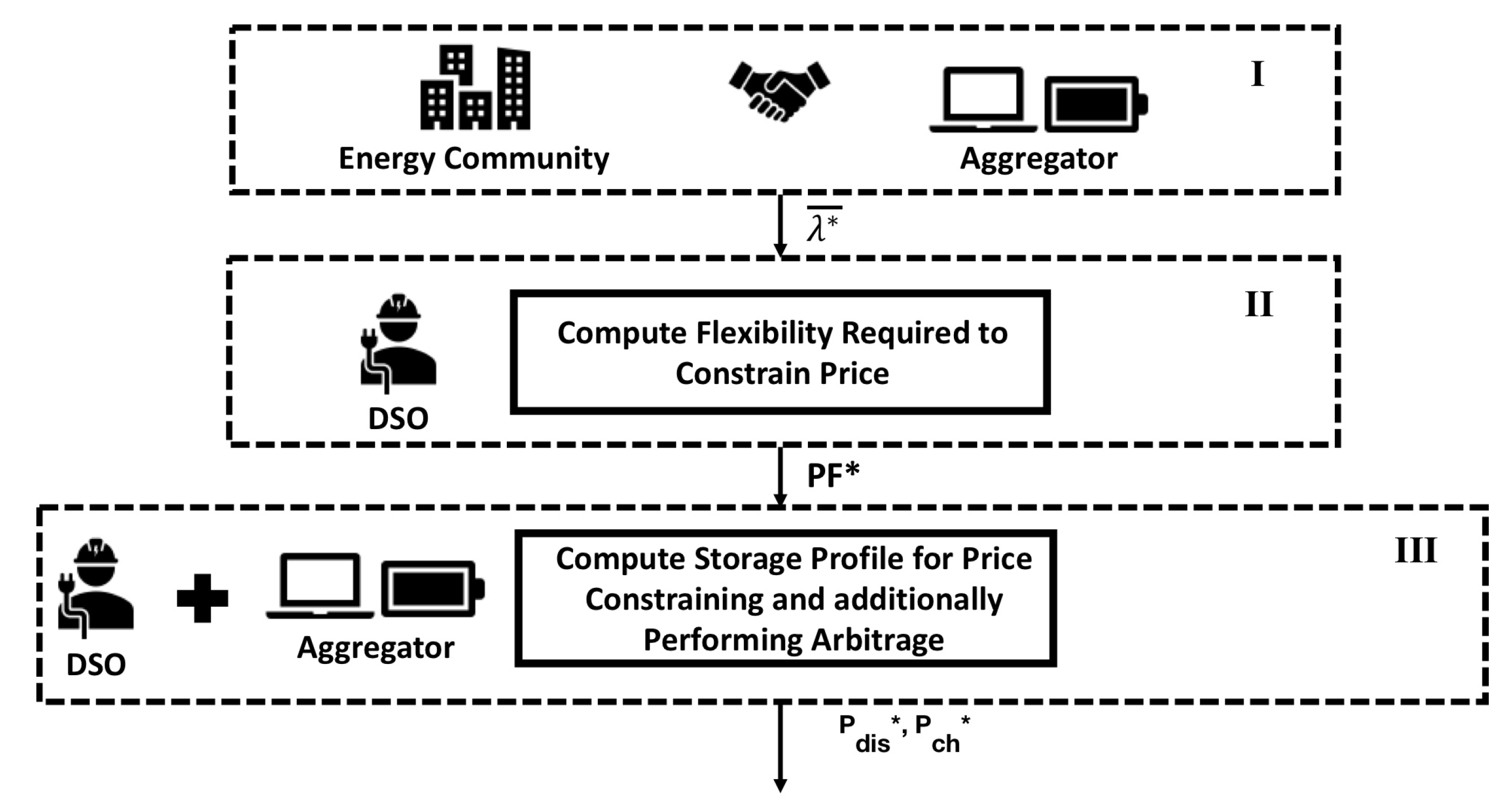

2.3. Organizational Structure for Flexibility Provision

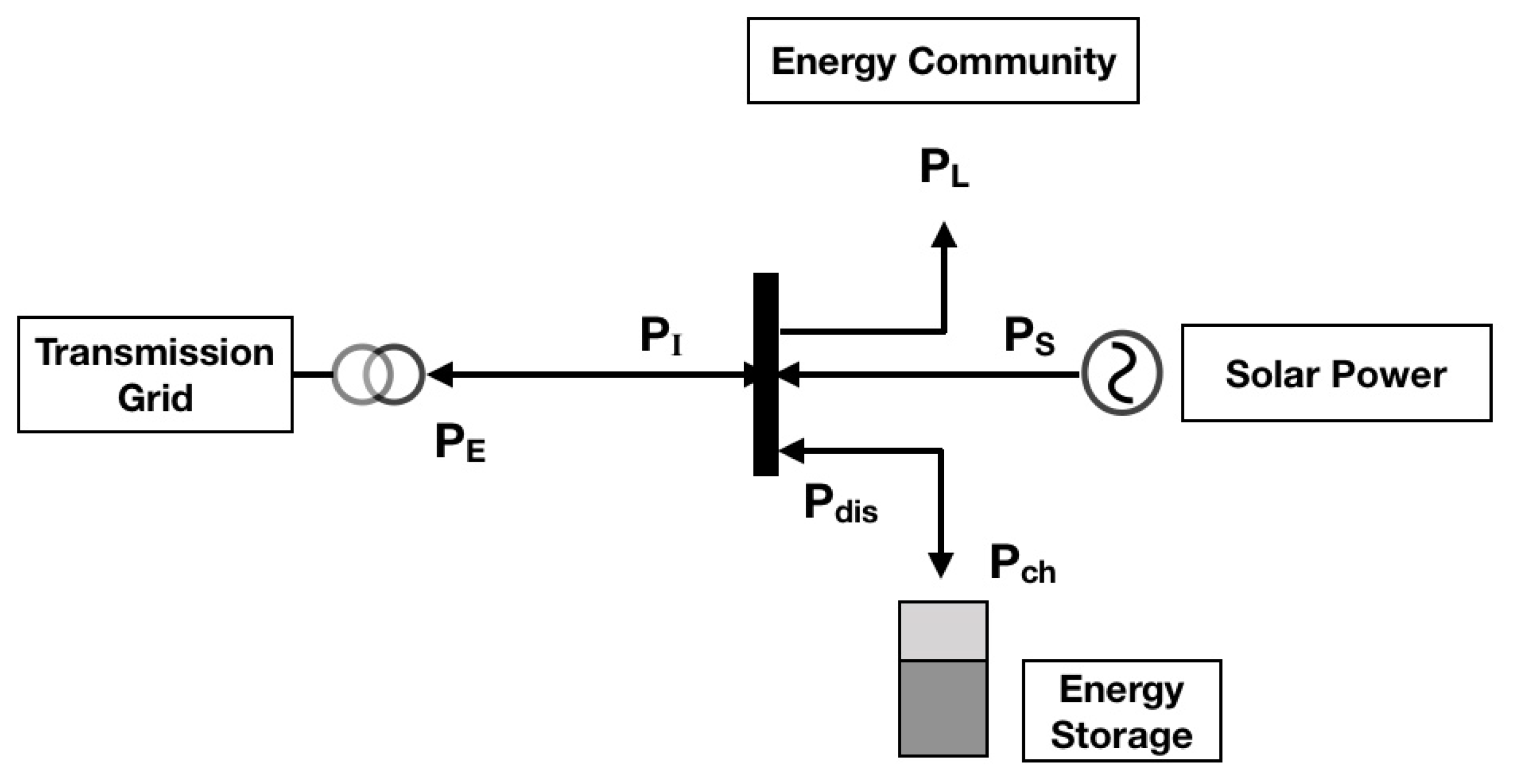

3. Case Study

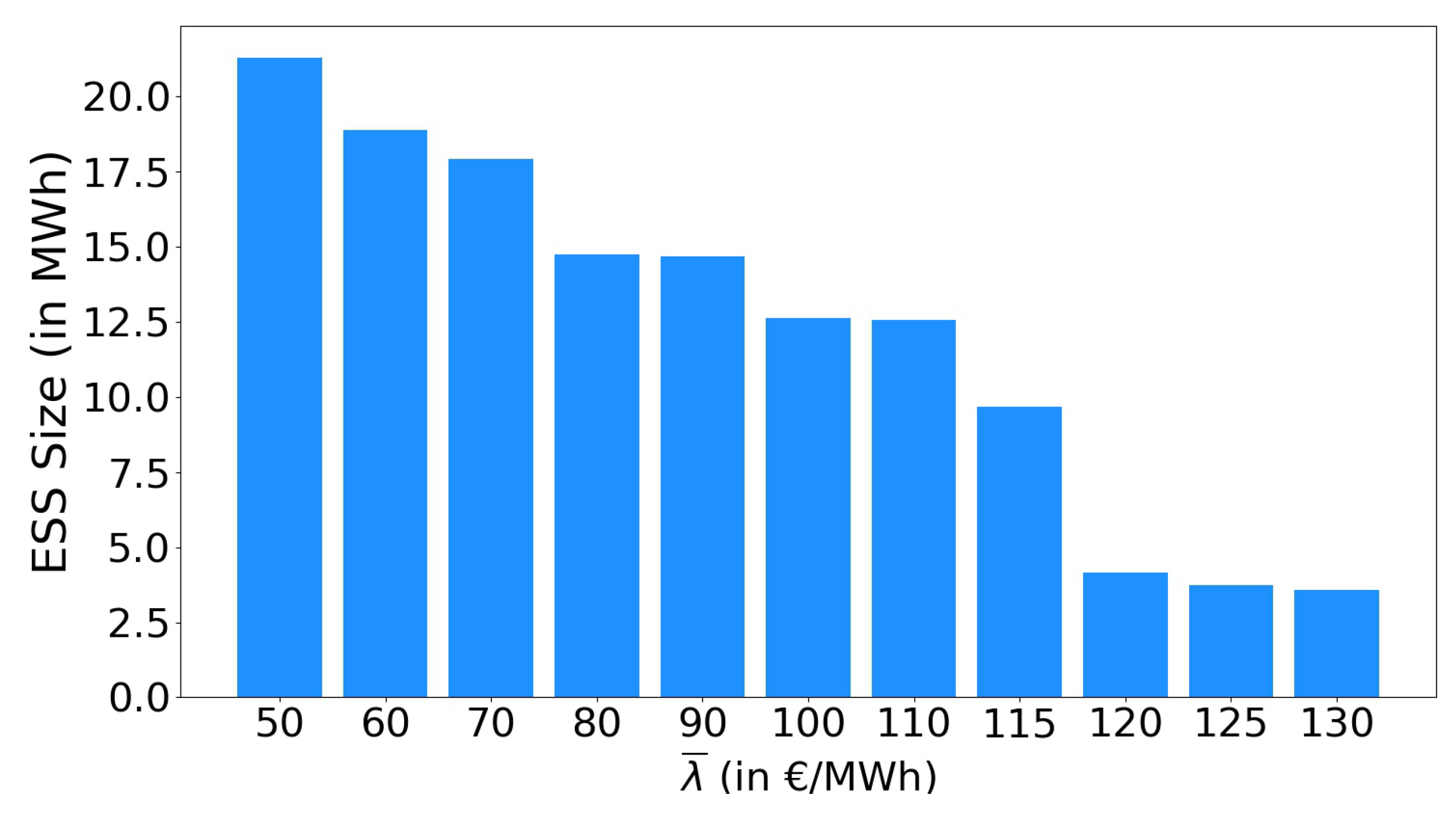

3.1. Determining the Volume of Required Flexibility

3.2. Battery Storage as a Flexible Generation Source

3.2.1. Optimal Storage Size

3.2.2. Providing Flexibility with an Energy Storage System

3.3. Flexibility and Arbitrage With an Energy Storage System

3.4. Arbitrage Only with an Energy Storage System

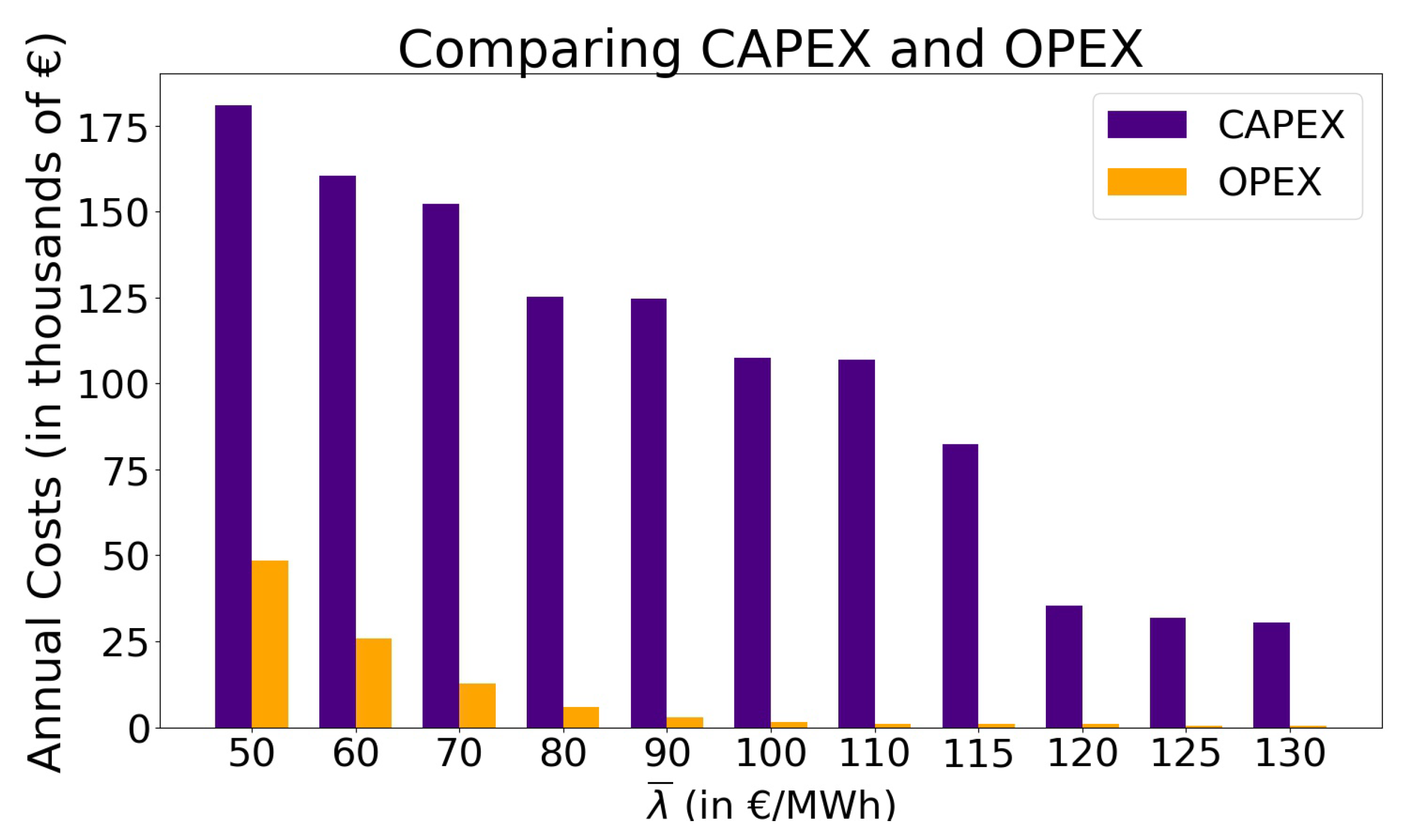

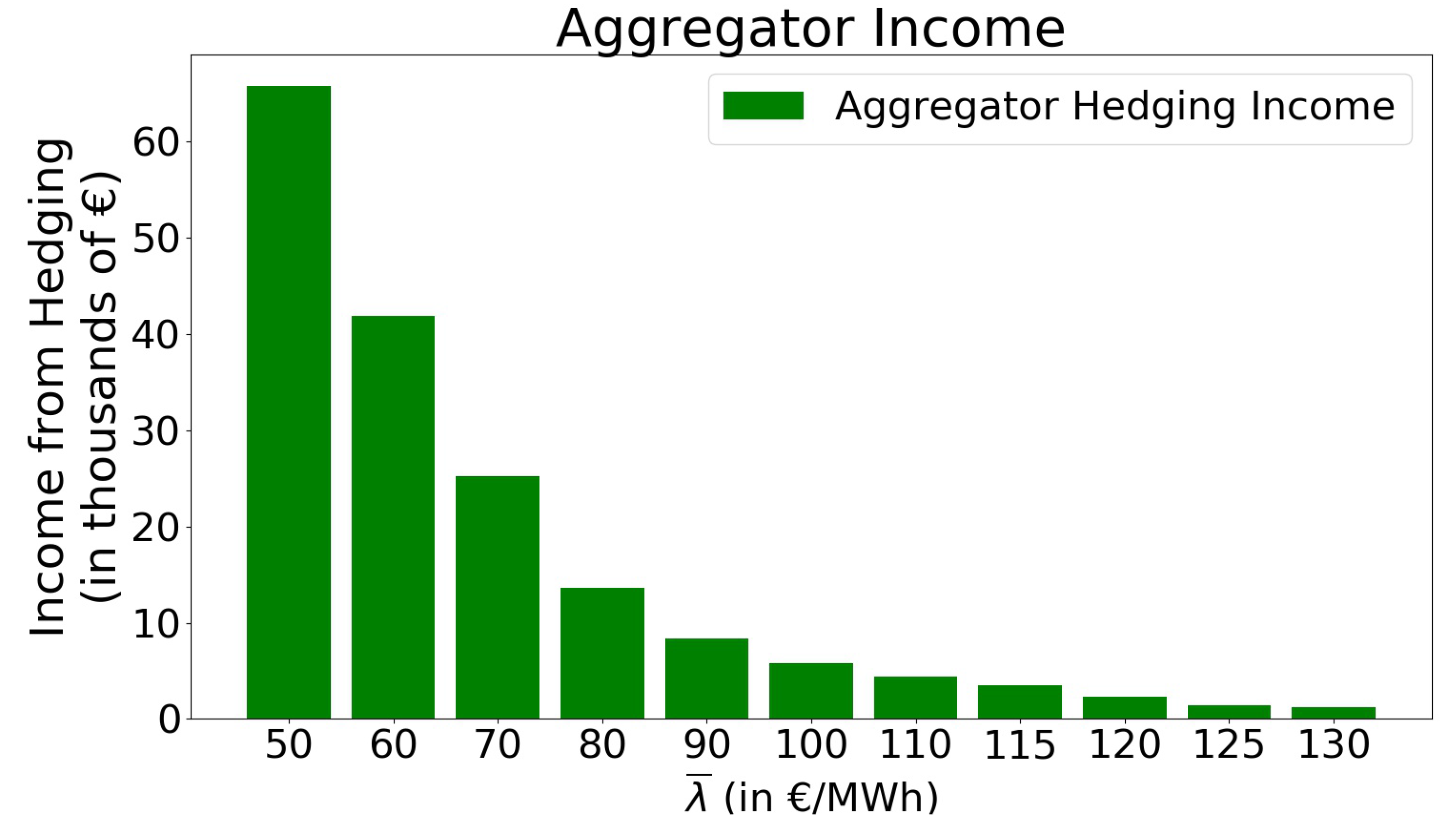

3.5. Economic Evaluation

4. Simulations and Results

4.1. Simulation Setup

4.2. Simulation Results

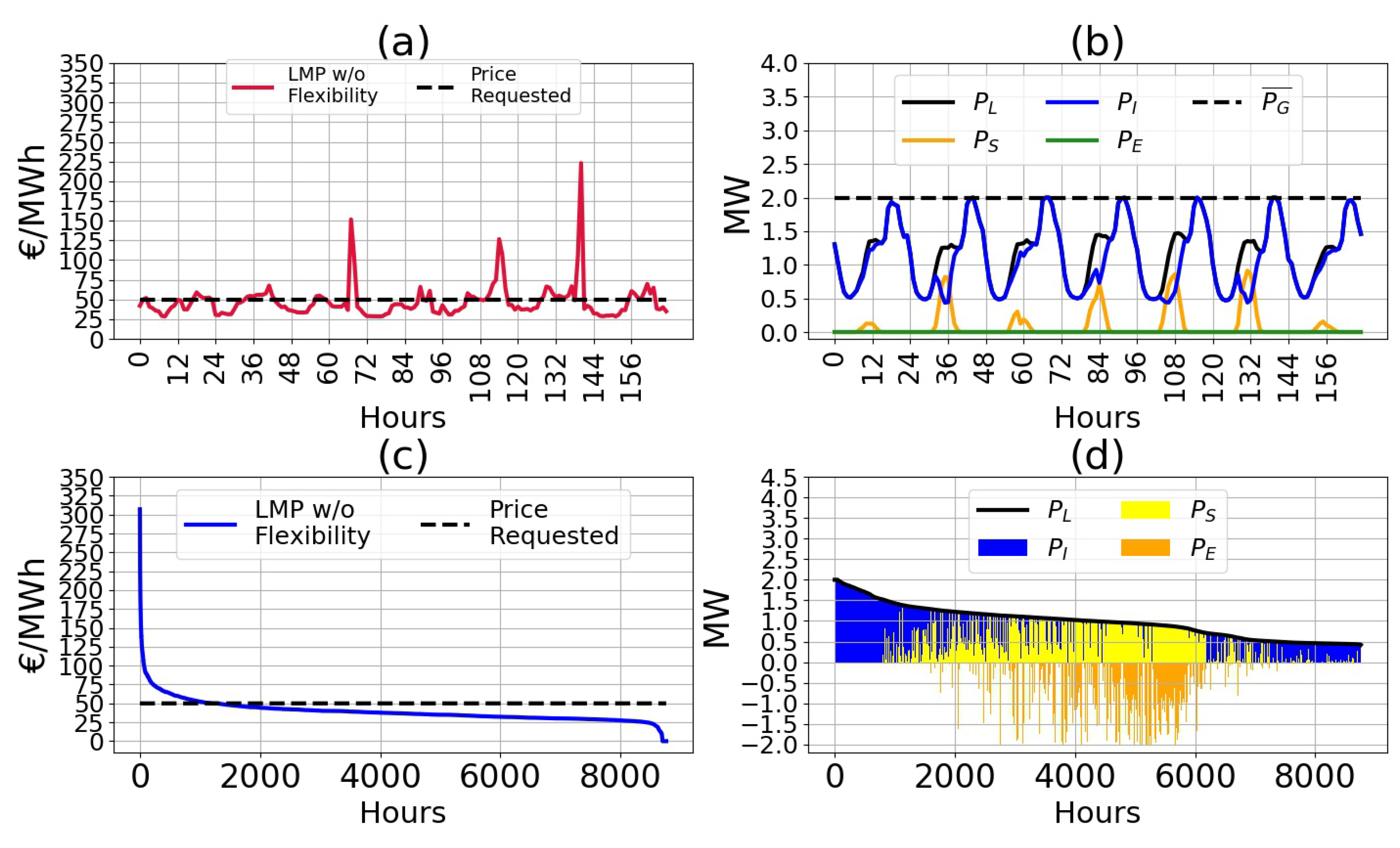

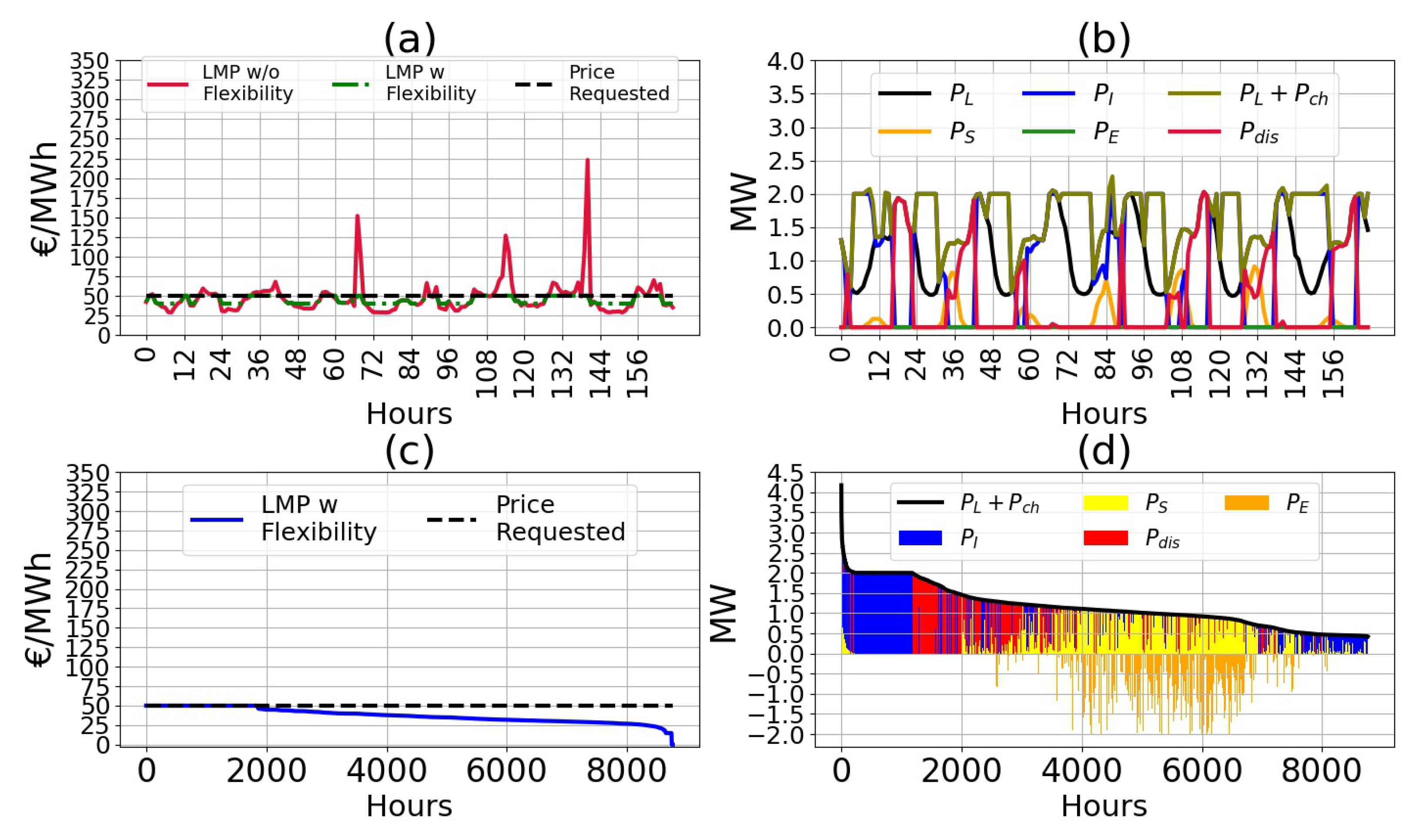

4.2.1. Reference Case

4.2.2. Constraining Price Using Energy Storage

4.2.3. Economic Analysis of Contractual Arrangements

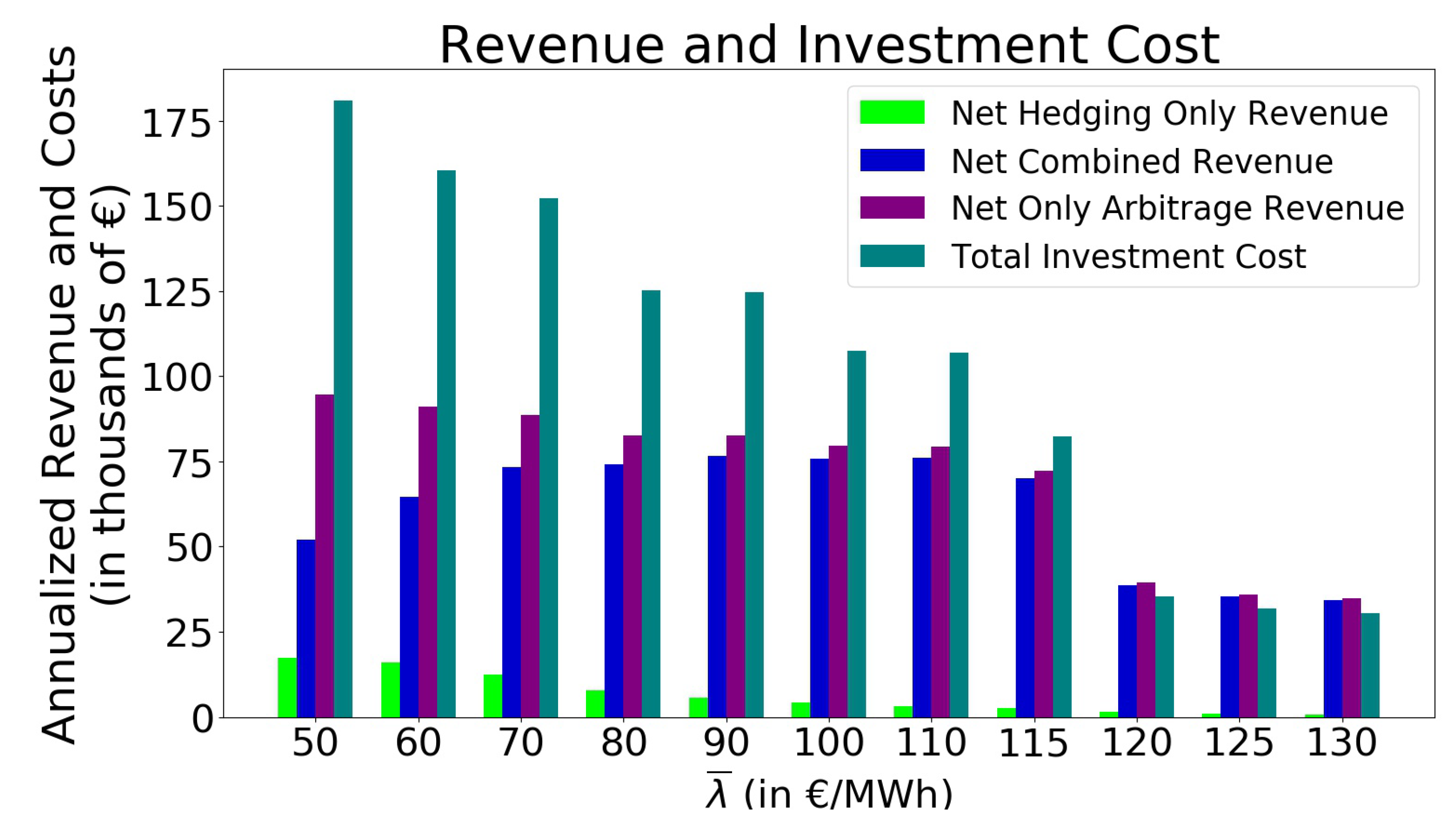

4.2.4. Comparative Analysis of Combined Hedging and Arbitrage and Arbitrage Alone

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Abbreviations

| T | length of simulation time period (hours) |

| t | discrete time interval (hours) |

| B | Load utility (€) |

| b | marginal load utility (€/MWh) |

| L | inflexible load (MW) |

| d | annualized per unit cost of energy (€/MWh-year) |

| C | annualized investment cost (/year) |

| D | total capital cost per unit of energy (€/MWh) |

| TCC | total capital cost |

| A | solar panel area (m) |

| r | solar panel efficiency |

| H | average hourly solar irradiance (MW/m) |

| DSO | distribution system operator |

| TSO | transmission system operator |

| ISO | independent system operator |

| ESS | energy storage system |

| LMP | locational marginal prices (€/MWh) |

| CAPEX | capital expenditure (€) |

| OPEX | operational expenditure (€) |

| power generation from generator i(MW) | |

| power demand (MW) | |

| maximum power demand (MW) | |

| minimum power demand (MW) | |

| marginal cost of generator i (€/MWh) | |

| marginal price of electricity (€/MWh) | |

| dual variable associated with upper bound generator i (€/MWh) | |

| maximum generation from generator i (MW) | |

| contractual price limit (€/MWh) | |

| flexibility provided at node i (MW) | |

| phase angle at bus i (degrees) | |

| reactance between nodes i and j () | |

| line flow limit from bus i to bus j (MW) | |

| contractual price limit at bus i (€/MWh) | |

| set of all nodes in the network | |

| set of all lines in the network | |

| flexibility required at node k to constrain prices (MW) | |

| coefficient of demand elasticity (/MWh) | |

| cost of importing to and exporting power from the energy community obtained from wholesale market price (€/MWh) | |

| power imported to the energy community from the main grid (MW) | |

| power exported from the energy community to the main grid (MW) | |

| solar power generation (MW) | |

| size of energy storage (MWh) | |

| coefficient of storage discharging | |

| coefficient of storage charging | |

| storage charging and discharging time constant | |

| penalty factor for preventing simultaneity (€/MWh) | |

| income from flexibility provision for constraining price (€) | |

| net revenue from hedging (€) | |

| constrained marginal price (€/MWh) | |

| cost of charging for providing flexibility to constrain price (€) | |

| time-steps in which the storage charges for being able to provide hedging functionality (hours) | |

| net operational revenue from arbitrage (€) | |

| net operational revenue from hedging and arbitrage (€) | |

| optimal storage size (MWh) |

References

- Koirala, B.P.; Koliou, E.; Friege, J.; Hakvoort, R.A.; Herder, P.M. Energetic communities for community energy: A review of key issues and trends shaping integrated community energy systems. Renew. Sust. Energ. Rev. 2016, 56, 722–744. [Google Scholar] [CrossRef]

- Parra, D.; Swierczynski, M.; Stroe, D.I.; Norman, S.A.; Abdon, A.; Worlitschek, J.; O’Doherty, T.; Rodrigues, L.; Gillott, M.; Zhang, X.; et al. An interdisciplinary review of energy storage for communities: Challenges and perspectives. Renew. Sust. Energ. Rev. 2017, 79, 730–749. [Google Scholar] [CrossRef]

- Holstenkamp, L.; Kahla, F. What are community energy companies trying to accomplish? An empirical investigation of investment motives in the German case. Energy Policy 2016, 97, 112–122. [Google Scholar] [CrossRef]

- Moret, F.; Pinson, P. Energy Collectives: A Community and Fairness Based Approach to Future Electricity Markets. IEEE Trans. Power Syst. 2019, 34, 3994–4004. [Google Scholar] [CrossRef]

- Tabors, R.; Caramanis, M.; Ntakou, E.; Parker, G.; Van Alstyne, M.; Centolella, P.; Hornby, R. Distributed Energy Resources: New Markets and New Products. In Proceedings of the 50th Hawaii International Conference on System Sciences, Hilton Waikoloa Village, HI, USA, 4–7 January 2017. [Google Scholar]

- Meng, F.; Chowdhury, B.H. Distribution LMP-based economic operation for future Smart Grid. In Proceedings of the IEEE Power and Energy Conference at Illinois, PECI, Urbana, IL, USA, 25–26 February 2011. [Google Scholar]

- Li, R.; Wu, Q.; Oren, S.S. Distribution locational marginal pricing for optimal electric vehicle charging management. IEEE Trans. Power Syst. 2014, 29, 203–211. [Google Scholar] [CrossRef]

- Liu, Z.; Wu, Q.; Oren, S.S.; Huang, S.; Li, R.; Cheng, L. Distribution locational marginal pricing for optimal electric vehicle charging through chance constrained mixed-integer programming. IEEE Trans. Smart Grid. 2018, 9, 644–654. [Google Scholar] [CrossRef]

- Faqiry, M.N.; Edmonds, L.; Wu, H. Distribution LMP-based Transactive Day-ahead Market with Variable Renewable Generation. unpublished.

- Astaneh, M.F.; Chen, Z. Price volatility in wind dominant electricity markets. In Proceedings of the IEEE EuroCon, Zagreb, Croatia, 1–4 July 2013. [Google Scholar]

- McConnell, D.; Forcey, T.; Sandiford, M. Estimating the value of electricity storage in an energy-only wholesale market. Appl. Energy 2015, 159, 422–432. [Google Scholar] [CrossRef]

- Yang, I.; Ozdaglar, A.E. Reducing electricity price volatility via stochastic storage control. In Proceedings of the American Control Conference, Boston, MA, USA, 6–8 July 2016. [Google Scholar]

- Pereira, J.P.; Pesquita, V.; Rodrigues, P.M. The effect of hydro and wind generation on the mean and volatility of electricity prices in Spain. In Proceedings of the 14th International Conference on the European Energy Market (EEM), Dresden, Germany, 6–9 June 2017. [Google Scholar]

- Higgs, H.; Lien, G.; Worthington, A.C. Australian evidence on the role of interregional flows, production capacity, and generation mix in wholesale electricity prices and price volatility. Econ. Anal. Policy 2015, 48, 172–181. [Google Scholar] [CrossRef]

- Rintamäki, T.; Siddiqui, A.S.; Salo, A. Does renewable energy generation decrease the volatility of electricity prices? An analysis of Denmark and Germany. Energy Econ. 2017, 62, 270–282. [Google Scholar] [CrossRef]

- Ketterer, J.C. The impact of wind power generation on the electricity price in Germany. Energy Econ. 2014, 44, 270–280. [Google Scholar] [CrossRef]

- Bradbury, K.; Pratson, L.; Patiño-Echeverri, D. Economic viability of energy storage systems based on price arbitrage potential in real-time U.S. electricity markets. Appl. Energy 2014, 114, 512–519. [Google Scholar] [CrossRef]

- Zakeri, B.; Syri, S. Value of energy storage in the Nordic Power market - Benefits from price arbitrage and ancillary services. In Proceedings of the 13th International Conference on the European Energy Market, EEM, Porto, Portugal, 6–9 June 2016. [Google Scholar]

- Ni, L.; Wen, F.; Liu, W.; Meng, J.; Lin, G.; Dang, S. Congestion management with demand response considering uncertainties of distributed generation outputs and market prices. J. Mod. Power Syst. Cle 2017, 5, 66–78. [Google Scholar] [CrossRef]

- Menniti, D.; Pinnarelli, A.; Sorrentino, N.; Burgio, A.; Belli, G. Management of storage systems in local electricity market to avoid renewable power curtailment in distribution network. In Proceedings of the 2014 Australasian Universities Power Engineering Conference, AUPEC, Perth, Australia, 28 Septembe–1 October 2014. [Google Scholar]

- Veldman, E.; Gibescu, M.; Slootweg, H.J.G.; Kling, W.L. Scenario-based modelling of future residential electricity demands and assessing their impact on distribution grids. Energy Policy 2013, 56, 233–247. [Google Scholar] [CrossRef]

- Karova, R. Regional electricity markets in Europe: Focus on the Energy Community. Util. Policy 2011, 19, 80–86. [Google Scholar] [CrossRef]

- Mamounakis, I.; Efthymiopoulos, N.; Makris, P.; Vergados, D.J.; Tsaousoglou, G.; Varvarigos, E.M. A novel pricing scheme for managing virtual energy communities and promoting behavioral change towards energy efficiency. Electr. Pow. Syst. Res. 2019, 167, 130–137. [Google Scholar] [CrossRef]

- Mohajeryami, S.; Doostan, M.; Moghadasi, S.; Schwarz, P. Towards the Interactive Effects of Demand Response Participation on Electricity Spot Market Price. Int. J. Emerg. Electr. Power Syst. 2017, 18. [Google Scholar] [CrossRef]

- Erdinc, O.; Paterakis, N.G.; Mendes, T.D.; Bakirtzis, A.G.; Catalão, J.P. Smart Household Operation Considering Bi-Directional EV and ESS Utilization by Real-Time Pricing-Based DR. IEEE Trans. Smart Grid 2015, 6, 1281–1291. [Google Scholar] [CrossRef]

- Barbour, E.; Parra, D.; Awwad, Z.; González, M.C. Community energy storage: A smart choice for the smart grid? Appl. Energy 2018, 212, 489–497. [Google Scholar] [CrossRef]

- Zenginis, I.; Vardakas, J.S.; Echave, C.; Morató, M.; Abadal, J.; Verikoukis, C.V. Cooperation in microgrids through power exchange: An optimal sizing and operation approach. Appl. Energy 2017, 203, 972–981. [Google Scholar] [CrossRef]

- Olivella-Rosell, P.; Lloret-Gallego, P.; Munné-Collado, Í.; Villafafila-Robles, R.; Sumper, A.; Ottessen, S.; Rajasekharan, J.; Bremdal, B.A. Local flexibility market design for aggregators providing multiple flexibility services at distribution network level. Energies 2018, 11, 822. [Google Scholar] [CrossRef]

- Esmat, A.; Usaola, J.; Moreno, M.Á. A decentralized local flexibility market considering the uncertainty of demand. Energies 2018, 11, 2078. [Google Scholar] [CrossRef]

- Esmat, A.; Usaola, J.; Moreno, M.Á. Distribution-level flexibility market for congestion management. Energies 2018, 11, 1056. [Google Scholar] [CrossRef]

- Kirschen, D.S.; Strbac, G. Fundamentals of Power System Economics, 2nd ed.; John Wiley & Sons: Hoboken, NJ, USA, 2004. [Google Scholar]

- Hanif, S.; Creutzburg, P.; Gooi, H.B.; Hamacher, T. Pricing Mechanism for Flexible Loads Using Distribution Grid Hedging Rights. IEEE Trans. Power Syst. 2019, 34, 4048–4059. [Google Scholar] [CrossRef]

- Zhou, D.P.; Dahleh, M.A.; Tomlin, C.J. Hedging Strategies for Load-Serving Entities in Wholesale Electricity Markets. In Proceedings of the 56th IEEE Conference on Decision and Control (CDC), Melbourne, Australia, 12–15 December 2017. [Google Scholar]

- Chakraborty, S.; Verzijlbergh, R.; Cvetkovic, M.; Baker, K.; Lukszo, Z. The Role of Demand-Side Flexibility in Hedging Electricity Price Volatility in Distribution Grids. In Proceedings of the IEEE Power and Energy Society Innovative Smart Grid Technologies Conference, (ISGT), Washington DC, USA, 17–20 February 2019. [Google Scholar]

- Chakraborty, S.; Baker, K.; Cvetkovic, M.; Verzijlbergh, R.; Lukszo, Z. Directly Constraining Marginal Prices in Distribution Grids Using Demand-Side Flexibility. In Proceedings of the IEEE Power and Energy Society General Meeting, Atlanta, GA, USA, 4–8 August 2019. [Google Scholar]

- Chakraborty, S.; Cvetkovic, M.; Baker, K.; Verzijlbergh, R.; Lukszo, Z. Consumer hedging against price volatility under uncertainty. In Proceedings of the IEEE Milan PowerTech, PowerTech, Milan, Italy, 23–27 June 2019. [Google Scholar]

- Zhang, Y.; Wang, J. K-nearest neighbors and a kernel density estimator for GEFCom2014 probabilistic wind power forecasting. Int. J. Forecast 2016, 32, 1074–1080. [Google Scholar] [CrossRef]

- Dowell, J.; Pinson, P. Very-Short-Term Probabilistic Wind Power Forecasts by Sparse Vector Autoregression. IEEE Trans. Smart Grid 2016, 7, 763–770. [Google Scholar] [CrossRef]

- Schweppe, F.C.; Caramanis, M.C.; Tabors, R.D.; Bohn, R.E. Spot Pricing of Electricity; Springer Economics: New York, NY, USA, 1988. [Google Scholar]

- Boyd, S.; Vandenberghe, L. Convex Optimization; Cambridge University Press: Cambridge, UK, 2004. [Google Scholar]

- Bernstein, A.; Dall’anese, E. Linear power-flow models in multiphase distribution networks. In Proceedings of the IEEE PES Innovative Smart Grid Technologies Conference Europe, Torino, Italy, 26–29 September 2017. [Google Scholar]

- Gerard, H.; Rivero Puente, E.I.; Six, D. Coordination between transmission and distribution system operators in the electricity sector: A conceptual framework. Util. Policy 2018, 50, 40–48. [Google Scholar] [CrossRef]

- Li, Z.; Guo, Q.; Sun, H.; Wang, J. Storage-like devices in load leveling: Complementarity constraints and a new and exact relaxation method. Appl. Energy 2015, 151, 13–22. [Google Scholar] [CrossRef]

- ENTSOE Transparency Platform. Available online: https://transparency.entsoe.eu/ (accessed on 26 January 2020).

- KNMI Weather Data. Available online: https://data.knmi.nl/datasets/ (accessed on 26 January 2020).

- Zakeri, B.; Syri, S. Electrical energy storage systems: A comparative life cycle cost analysis. Renew. Sust. Energ. Rev. 2015, 42, 569–596. [Google Scholar] [CrossRef]

- Voulis, N.; Warnier, M.; Brazier, F.M. Understanding spatio-temporal electricity demand at different urban scales: A data-driven approach. Appl. Energy 2018, 230, 1157–1171. [Google Scholar] [CrossRef]

- Hart, W.E.; Laird, C.D.; Watson, J.P.; Woodruff, D.L.; Hackebeil, G.A.; Nicholson, B.L.; Siirola, J.D. Pyomo–Optimization Modeling in Python, 2nd ed.; Springer Science & Business Media: New York, NY, USA, 2017; Volume 67. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Category | = €50/MWh | = €100/MWh | = €130/MWh | |||

|---|---|---|---|---|---|---|

| Max. Price and System Benefit | Combined Hedging and Arbitrage | Arbitrage Only | Combined Hedging and Arbitrage | Arbitrage Only | Combined Hedging and Arbitrage | Arbitrage Only |

| Max Price (in €/MWh) | 50.0 | 84.07 | 100.0 | 120.021 | 130 | 131.01 |

| System Benefit (in Millions of /year) | 9.897 | 9.911 | 9.898 | 9.904 | 9.8635 | 9.868 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chakraborty, S.; Verzijlbergh, R.; Baker, K.; Cvetkovic, M.; Vries, L.D.; Lukszo, Z. A Coordination Mechanism For Reducing Price Spikes in Distribution Grids. Energies 2020, 13, 2500. https://doi.org/10.3390/en13102500

Chakraborty S, Verzijlbergh R, Baker K, Cvetkovic M, Vries LD, Lukszo Z. A Coordination Mechanism For Reducing Price Spikes in Distribution Grids. Energies. 2020; 13(10):2500. https://doi.org/10.3390/en13102500

Chicago/Turabian StyleChakraborty, Shantanu, Remco Verzijlbergh, Kyri Baker, Milos Cvetkovic, Laurens De Vries, and Zofia Lukszo. 2020. "A Coordination Mechanism For Reducing Price Spikes in Distribution Grids" Energies 13, no. 10: 2500. https://doi.org/10.3390/en13102500

APA StyleChakraborty, S., Verzijlbergh, R., Baker, K., Cvetkovic, M., Vries, L. D., & Lukszo, Z. (2020). A Coordination Mechanism For Reducing Price Spikes in Distribution Grids. Energies, 13(10), 2500. https://doi.org/10.3390/en13102500