Electricity Generation in India: Present State, Future Outlook and Policy Implications

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Electricity Generation in India

3. Electricity Demand in India

4. Methodology: LEAP Modelling

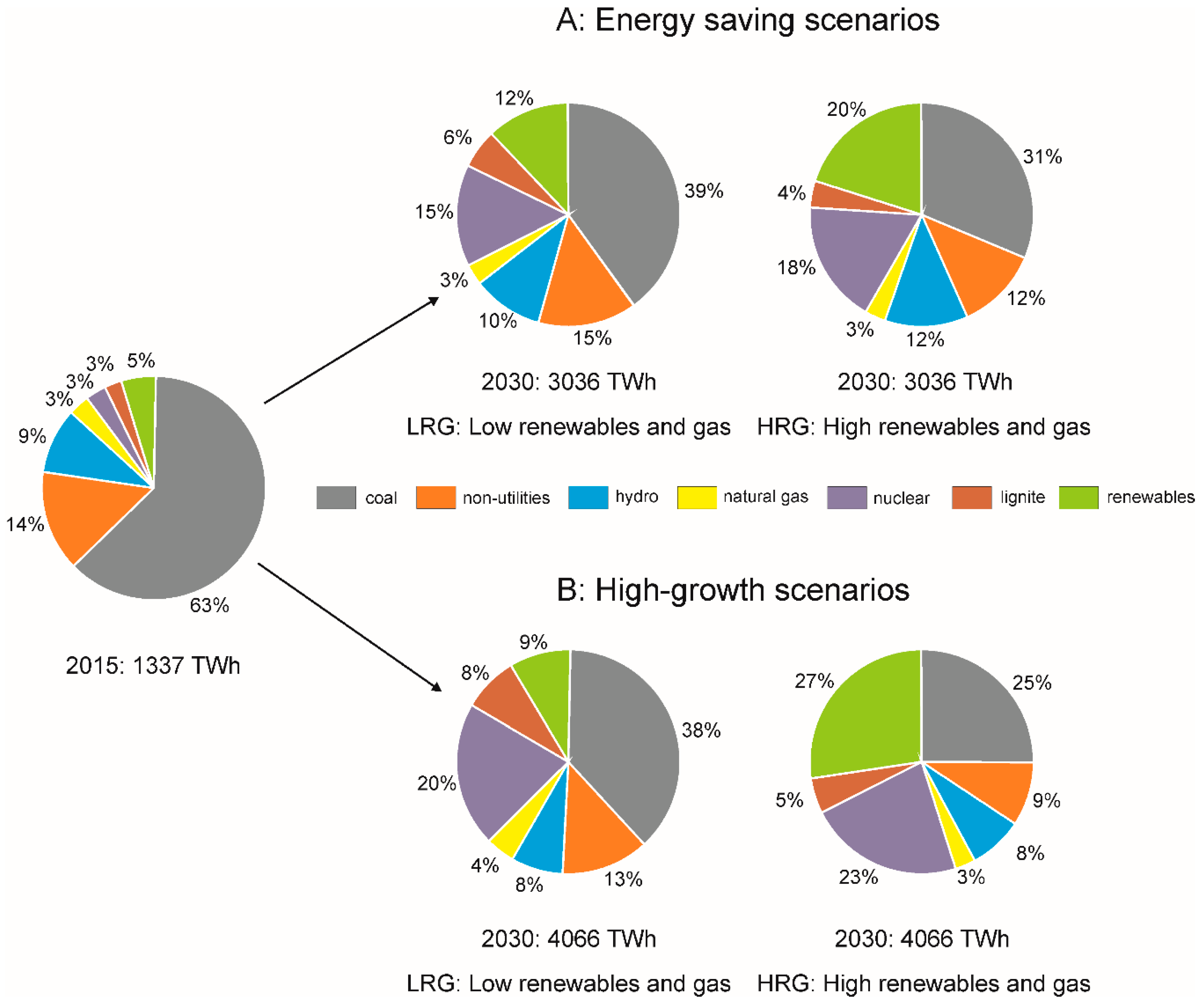

5. Results

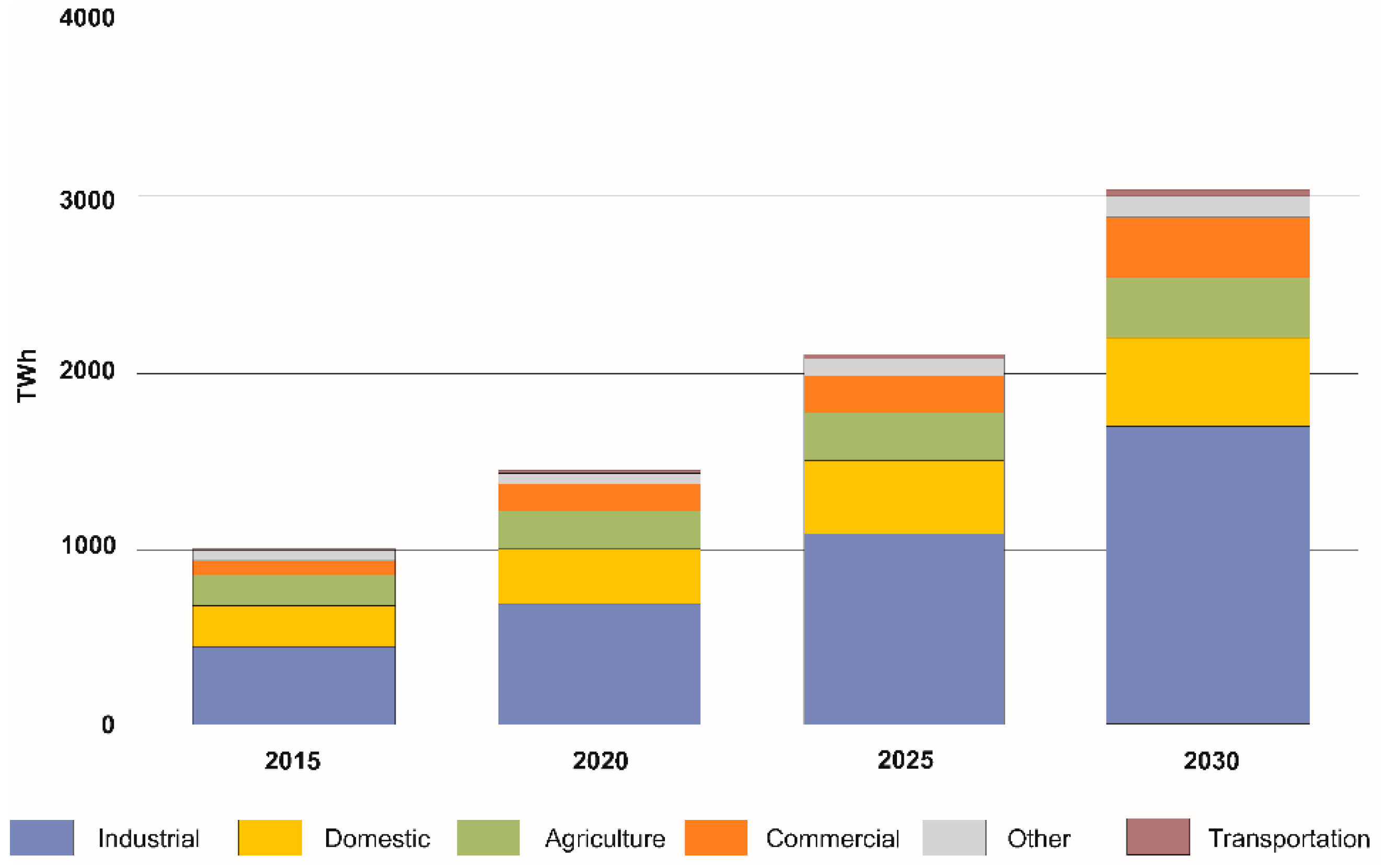

5.1. Electricity Demand

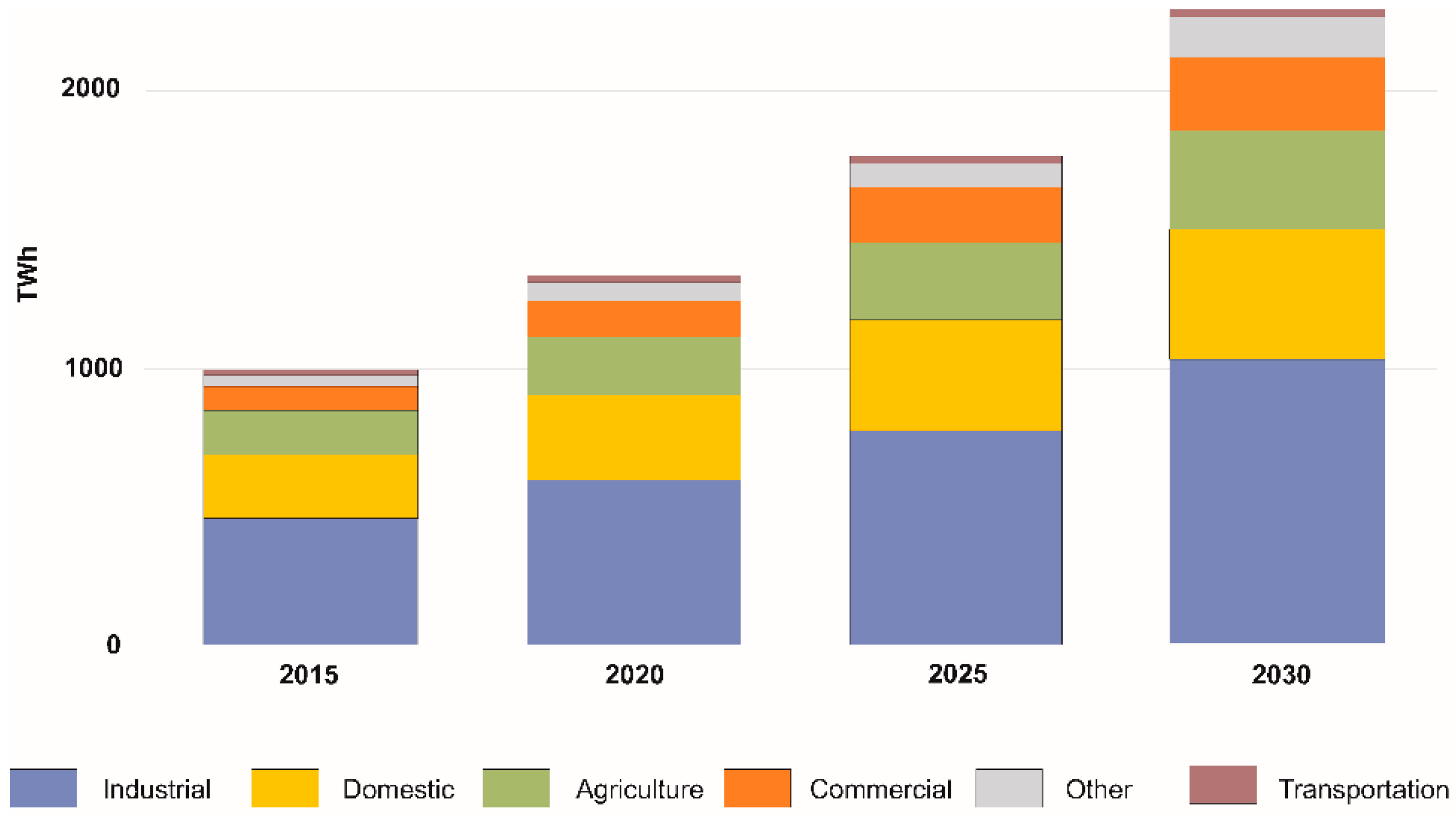

5.2. Electricity Generation

6. Discussion

7. Conclusions

- Realistic possibilities of nuclear energy including its social acceptance

- Evaluation of the potential of hydropower and renewable energy sources including their environmental impact

- Reduction of the present high carbon emission sources during electricity generation with future low-emission goals.

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

References

- International Monetary Fund. World Economic Outlook: Adjusting to Lower Commodity Prices; IMF: Washington, DC, USA, 2015. [Google Scholar]

- Central Electricity Authority. Annual Report 2014–2015; Government of India, Ministry of Power, Central Electricity Authority: New Delhi, India, 2015.

- Central Statistics Office. Energy Statistics; Ministry of Statistics and Pragramme Implementation: New Delhi, India, 2015.

- Ikegami, M.; Wang, Z.H. The long-time causal relation between electricity consumption and real GDP: Evidence from Japan and Germany. J. Policy Model. 2016, 38, 767–784. [Google Scholar] [CrossRef]

- Erdal, G.; Erdal, H.; Esengun, K. The causality between energy consumption and economic growth in Turkey. Energy Policy 2008, 36, 3838–3842. [Google Scholar] [CrossRef]

- Zamani, M. Energy consumption and economic activities in Iran. Energy Econ. 2007, 29, 1135–1140. [Google Scholar] [CrossRef]

- World Development Indicators: Electric Power Consumption (kWh Per Capita). The World Bank, 2016. Available online: http://data.worldbank.org/indicator/EG.USE.ELEC.KH.PC (accessed on 8 March 2017).

- World Development Indicators: GDP Per Capita. The World Bank, 2016. Available online: http://data.worldbank.org/indicator/NY.GDP.PCAP.CD (accessed on 8 March 2017).

- Hu, Z.; Hu, Z. Electricity Economics: Production Functions with Electricity; Springer: Berlin/Heidelberg, Germany, 2013. [Google Scholar]

- Heaps, C.G. Long-Range Energy Alternatives Planning (LEAP) System [Software Version 2012.0049]. Available online: http://www.energycommunity.org/ (accessed on 12 April 2017).

- Kale, R.V.; Pohekar, S.D. Electricity demand and supply scenarios for Maharashtra (India) for 2030: An application of long range energy alternatives planning. Energy Policy 2014, 72, 1–13. [Google Scholar] [CrossRef]

- McPherson, M.; Karney, B. Long-term scenario alternatives and their implications: LEAP model application of Panama’s electricity sector. Energy Policy 2014, 68, 146–157. [Google Scholar] [CrossRef]

- Yophy, H.; Jeffrey, B.Y.; Chieng-Yu, P. The long-term forecast of Taiwan’s energy supply and demand: LEAP model application. Energy Policy 2011, 39, 6790–6803. [Google Scholar]

- World Development Indicators: India. The World Bank, 2016. Available online: http://data.worldbank.org/country/india (accessed on 5 March 2017).

- Khare, V.; Nema, S.; Baredar, P. Status of solar wind renewable energy in India. Renew. Sustain. Energy Rev. 2013, 127, 1–10. [Google Scholar] [CrossRef]

- Gao, M.; Ding, Y.H.; Song, S.J.; Lu, X.; Chen, X.Y.; McElroy, M.B. Secular decrease of wind power potential in India associated with warming in the Indian Ocean. Sci. Adv. 2018, 4, 1–8. [Google Scholar] [CrossRef] [PubMed]

- Thapar, S.; Sharma, S.; Verma, A. Key determinants of wind energy growth in India: Analysis of policy and non-policy factors. Energy Policy 2018, 122, 622–638. [Google Scholar] [CrossRef]

- Deshmukh, R.; Wu, G.C.; Callaway, D.S.; Phadke, A. Geospatial and techno-economic analysis of wind and solar resources in India. Renew. Energy 2019, 134, 947–960. [Google Scholar] [CrossRef]

- Nautiyal, H.; Singal, S.K.; Varun, G.; Sharma, A. Small hydropower for sustainable energy development in India. Renew. Sustain. Energy Rev. 2011, 15, 2021–2027. [Google Scholar] [CrossRef]

- Khan, R. Small hydro power in India: Is it a sustainable business? Appl. Energy 2015, 152, 207–216. [Google Scholar] [CrossRef]

- Sharma, N.K.; Tiwari, P.K.; Sood, Y.R. Solar energy in India? Strategies, policies, perspectives and future potential. Renew. Sustain. Energy Rev. 2012, 16, 933–941. [Google Scholar] [CrossRef]

- Bijarniya, J.P.; Sudhakar, K.; Baredar, P. Concentrated solar power technology in India: A review. Renew. Sustain. Energy Rev. 2016, 63, 593–603. [Google Scholar] [CrossRef]

- Kumar, A.; Kumar, N.; Baredar, P.; Shukla, A. A review on biomass energy resources, potential, conversion and policy in India. Renew. Sustain. Energy Rev. 2015, 45, 530–539. [Google Scholar] [CrossRef]

- Ahmed, S.; Mahmood, A.; Hasan, A.; Sidhu, G.A.S.; Butt, M.F.U. A comparative review od China, India and Pakistan renewable energy sectors and sharing opportunities. Renew. Sust. Energy Rev. 2016, 57, 216–225. [Google Scholar] [CrossRef]

- Tripathi, L.; Mishra, A.K.; Dubey, A.K.; Tripathi, C.B.; Baredar, P. Renewable energy: An overview on its contribution in current energy scenario of India. Renew. Sustain. Energy Rev. 2016, 60, 226–233. [Google Scholar] [CrossRef]

- Kumar, A.; Patel, N.; Gupta, N.; Gupta, V. Photovoltaic power generation in Indian prospective considering off-grid and grid-connected systems. Int. J. Renew. Energy Res. 2018, 8, 1936–1950. [Google Scholar]

- Kumar, S.; Madlener, R. CO2 emission reduction potential assessment using renewable energy in India. Energy 2016, 97, 273–282. [Google Scholar] [CrossRef]

- Rajanna, S.; Saini, R.P. Development of optimal integrated renewable energy model with battery storage for a remote Indian area. Energy 2016, 111, 803–817. [Google Scholar] [CrossRef]

- Sen, S.; Ganguly, S.; Das, A.; Sen, J.; Dey, S. Renewable energy in India: Opportunities and challenges. J. Afr. Earth Sci. 2016, 122, 25–31. [Google Scholar] [CrossRef]

- Tiewsoh, L.S.; Sivek, M.; Jirásek, J. Traditional energy resources in India (coal, crude oil, natural gas): A review. Energy Sourc. Part. B 2017, 12, 110–118. [Google Scholar] [CrossRef]

- Planning Commission. Integrated Energy Policy: Report of the Expert Committee; Government of India: New Delhi, India, 2006.

- Directorate General of Hydrocarbons. Hydrocarbon Exploration & Production Activities, India 2014–2015; Ministry of Petroleum and Natural Gas: New Delhi, India, 2015.

- Communication Dated 10 September 2008, Received from the Permanent Mission of Germany to the Agency Regarding a “Statement on Civil Nuclear Cooperation with India”. IAEA, 2008. Available online: https://www.iaea.org/sites/default/files/publications/documents/infcircs/2008/infcirc734c.pdf (accessed on 20 March 2017).

- Grover, R.B. Policy initiative by the Government of India to accelerate the growth of installed nuclear capacity in the coming years. Energy Proced. 2011, 7, 74–78. [Google Scholar] [CrossRef]

- Grover, R.B. Green growth and role of nuclear power: A perspective from India. Energy Strateg. Rev. 2013, 1, 255–260. [Google Scholar] [CrossRef]

- National Action Plan on Climate Change; Prime Minister’s Council on Climate Change, Government of India: New Delhi, India, 2008.

- The Road from Paris: India’s Progress Towards Its Climate Pledge. NRDC, 2016. Available online: https://www.nrdc.org/sites/default/files/paris-climate-conference-India-IB.pdf (accessed on 17 February 2017).

- Fenton, M.D. Iron and steel. In Mineral Commodity Summaries 2017; U.S. Geological Survey: Reston, VA, USA, 2017; pp. 84–85. [Google Scholar]

- Krishnan, S.S.; Vunnan, V.; Sunder, P.S.; Sunil, J.V.; Ramakrishnan, A.M. A Study of Energy Efficiency in the Indian Iron and Steel Industry; Center for Study of Science, Technology and Policy: Bangalore, India, 2013. [Google Scholar]

- Bray, E.L. Aluminium. In Mineral Commodity Summaries 2017; U.S. Geological Survey: Reston, VA, USA, 2017; pp. 22–23. [Google Scholar]

- TERI. TERI Energy & Environment Data Directory and Yearbook (TEDDY) 2013/14; The Energy and Resources Institute: New Delhi, India, 2014. [Google Scholar]

- Van Oss, H.G. Cement. In Mineral Commodity Summaries 2017; U.S. Geological Survey: Reston, VA, USA, 2017; pp. 44–45. [Google Scholar]

- Ministry of Petroleum & Natural Gas. Indian Petroleum and Natural Gas. Statistics 2014–2015; Government of India: New Delhi, India, 2015.

- Ministry of Petroleum & Natural Gas. Energizing the Nation: Annual Report 2013–2014; Government of India: New Delhi, India, 2014.

- Ministry of Chemicals and Fertilizers. Indian Fertilizer Scenario; Government of India: New Delhi, India, 2014.

- Schumacher, K.; Sathaye, J. India’s Fertilizer Industry: Productivity and Energy Efficiency; Environmental Energy Technologies Division, University of California: Berkeley, CA, USA, 1999. [Google Scholar]

- Census of India. 2011. Available online: http://www.censusindia.gov.in/2011census/PCA/PCA_Highlights/pca_highlights_file/India/Chapter-1.pdf (accessed on 8 March 2017).

- Silk, J.I.; Joutz, F.L. Short and long-run elasticities in US residential electricity demand: A co-integration approach. Energy Econ. 1997, 19, 493–513. [Google Scholar] [CrossRef]

- Dergiades, T.; Tsoulfidis, L. Estimating residential demand for electricity in the United States, 1965–2006. Energy Econ. 2008, 30, 2722–2730. [Google Scholar] [CrossRef]

- Narayan, P.K.; Smyth, R.; Prasad, A. Electricity consumption in G7 countries: A panel cointegration analysis of residential demand elasticities. Energy Policy 2007, 35, 4485–4494. [Google Scholar] [CrossRef]

- Narayan, P.K.; Smyth, R. The residential demand for electricity in Australia: An application of the bounds testing approach to cointegration. Energy Policy 2005, 33, 467–474. [Google Scholar] [CrossRef]

- Ministry of Power. Deendayal Upadhyaya Gram Jyoti Yojana; Government of India: New Delhi, India, 2014.

- Filippini, M.; Pachauri, S. Elasticities of electricity demand in urban Indian households. Energy Policy 2004, 32, 429–436. [Google Scholar] [CrossRef]

- Holtedahl, P.; Joutz, F.L. Residential electricity demand in Taiwan. Energy Econ. 2004, 26, 201–224. [Google Scholar] [CrossRef]

- Halicioglu, F. Residential electricity demand dynamics in Turkey. Energy Econ. 2007, 29, 199–210. [Google Scholar] [CrossRef]

- Dergiades, T.; Tsoulfidis, L. Revisiting residential demand for electricity in Greece: New evidence from the ARDL approcach to cointegration analysis. Empir. Econ. 2011, 41, 511–531. [Google Scholar] [CrossRef]

- National Sample Office. Household consumption of Various Goods and Services in India 2011–2012, NSS 68th Round; Ministry of Statistics and Programme Implementation, Government of India: New Delhi, India, 2014.

- Rawal, R.; Shukla, Y.; Didwania, S.; Singh, M.; Maweda, V. Residential Buildings in India: Energy Use Projections and Savings Potential; Global Buildings Performance Network: Gujarat, India, 2014. [Google Scholar]

- Ministry of Agriculture. Agricultural Statistics at a Glance; Government of India: New Delhi, India, 2014.

- USAID ECO-III Project. Energy Assessment Guide for Commercial Building; International Resources Group: New Delhi, India, 2009. [Google Scholar]

- Statistical Summaries: Indian Railways. Tool Alfa, 2013. Available online: http://in.tool-alfa.com/LinkClick.aspx?fileticket=usxd2FyX02Y%3D&tabid=72&mid=486 (accessed on 8 March 2017).

- International Monetary Fund: World Economic Outlook Update. January 2019. Available online: https://www.imf.org/~/media/Files/Publications/WEO/2019/Update/January/WEOupdateJan2019.ashx?la=en (accessed on 27 March 2019).

- PricewaterhouseCoopers International Limited: The World in 2050. Available online: https://www.pwc.com/gx/en/issues/economy/the-world-in-2050.html (accessed on 27 March 2019).

- Sharma, R. The ever-emerging markets: Why economic forecasts fail. Foreign Aff. 2014, 93, 52–56. [Google Scholar]

- The World Bank: Population Growth (Annual %). 2019. Available online: https://data.worldbank.org/indicator/sp.pop.grow (accessed on 27 March 2019).

- The World Factbook 2016–2017; Government Printing Office: Washington, DC, USA, 2016.

- Kulkarni, P.M. Demographic Transition in India. 4 December 2014. Available online: http://censusindia.gov.in/DigitalLibrary/Demographic-Transition-in-India.pdf (accessed on 27 March 2019).

- Energy Efficient Solar/Green Buildings. Ministry of New and Renewable Energy, 2013. Available online: http://mnre.gov.in/file-manager/dec-green-buildings/MNRE-scheme-green-buildings.pdf (accessed on 12 March 2017).

- Fowler, K.; Rauch, E.; Henderson, J.; Kora, A. Re-Assessing Green Building Performance: A Post Occupancy Evaluation of 22 GSA Buildings; United States Department of Energy: Richland, WA, USA, 2011.

- A Diagnostic Study of the Energy Efficiency of IoT: A Technology and Energy Assessment Report. Pricewaterhouse Coppers, 2018. Available online: https://shaktifoundation.in/wp-content/uploads/2018/07/IOT.pdf (accessed on 20 November 2018).

- Ministry of Micro, Small and Medium Enterprises. Annual Report 2013–2014; Government of India: New Delhi, India, 2014.

- The Micro, Small and Medium Enterprises Development Act. 2006. Available online: http://www.wipo.int/edocs/lexdocs/laws/en/in/in114en.pdf (accessed on 8 March 2017).

- Buccirossi, P. (Ed.) Handbook of Antitrust Economics: Public Policy in Network Industries; The MIT Press: Cambridge, MA, USA, 2008. [Google Scholar]

- Singh, R.; Sood, Y.R. Current status and analysis of renewable promotional policies in Indian restructured power sector—A review. Renew. Sustain. Energy Rev. 2011, 15, 657–666. [Google Scholar] [CrossRef]

- Mahanty, M. Nuclear Energy in India: Debate and Public perception. In Proceedings of the International Conference on Gandhi, Disarmament and Development, Indore, India, 4–6 October 2013; pp. 1–6. [Google Scholar]

- Mishra, S. Socal acceptance of nuclear power in India. Air Power J. 2012, 7, 55–82. [Google Scholar]

- Lelieveld, J.; Evans, J.S.; Fnais, M.; Giannadaki, D.; Pozzer, A. The contribution of outdoor air pollution sources to premature mortality on a global scale. Nature 2015, 525, 367. [Google Scholar] [CrossRef]

- Lu, Z.; Zhang, Q.; Streets, D.G. Sulfur dioxide and primary carbonaceous aerosol emissions in China and India, 1996–2010. Atmos. Chem. Phys. 2011, 11, 9839–9864. [Google Scholar] [CrossRef]

- Anandarajah, G.; Gambhir, A. India’s CO2 emission pathways to 2050: What role can renewables play? Appl. Energy 2014, 131, 79–86. [Google Scholar]

- Kapoor, K.; Pandey, K.K.; Jain, A.K.; Nandan, A. Evolution of solar energy in India: A review. Renew. Sustain. Energy Rev. 2014, 40, 475–487. [Google Scholar] [CrossRef]

- Sahoo, S.K. Renewable and sustainable energy reviews solar photovoltavic energy progress in India: A review. Renew. Sustain. Energy Rev. 2016, 59, 927–939. [Google Scholar] [CrossRef]

- Kumar, A.; Prakash, O.; Dube, A. A review on progress of concentrated solar power in India. Renew. Sustain. Energy Rev. 2017, 79, 304–307. [Google Scholar] [CrossRef]

- Srikanth, R. India’s sustainable development goals—Glide path for India’s power sector. Energy Policy 2018, 123, 325–336. [Google Scholar] [CrossRef]

- Lawrentz, L.; Xiong, B.; Lorenz, L.; Krumm, A.; Hosenfeld, H.; Burands, T.; Loffler, K.; Oei, P.Y.; von Hirschhausen, C. Exploring energy pathways for the low-carbon transformation in India—A model-based approach. Energies 2018, 11, 3001. [Google Scholar] [CrossRef]

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tiewsoh, L.S.; Jirásek, J.; Sivek, M. Electricity Generation in India: Present State, Future Outlook and Policy Implications. Energies 2019, 12, 1361. https://doi.org/10.3390/en12071361

Tiewsoh LS, Jirásek J, Sivek M. Electricity Generation in India: Present State, Future Outlook and Policy Implications. Energies. 2019; 12(7):1361. https://doi.org/10.3390/en12071361

Chicago/Turabian StyleTiewsoh, Lari Shanlang, Jakub Jirásek, and Martin Sivek. 2019. "Electricity Generation in India: Present State, Future Outlook and Policy Implications" Energies 12, no. 7: 1361. https://doi.org/10.3390/en12071361

APA StyleTiewsoh, L. S., Jirásek, J., & Sivek, M. (2019). Electricity Generation in India: Present State, Future Outlook and Policy Implications. Energies, 12(7), 1361. https://doi.org/10.3390/en12071361