An Entrepreneurial Definition of the Blockchain Technology and a Stacked Layer Model of the ICO Marketplace Using the Text Mining Approach

Abstract

:1. Introduction

2. Literature Review

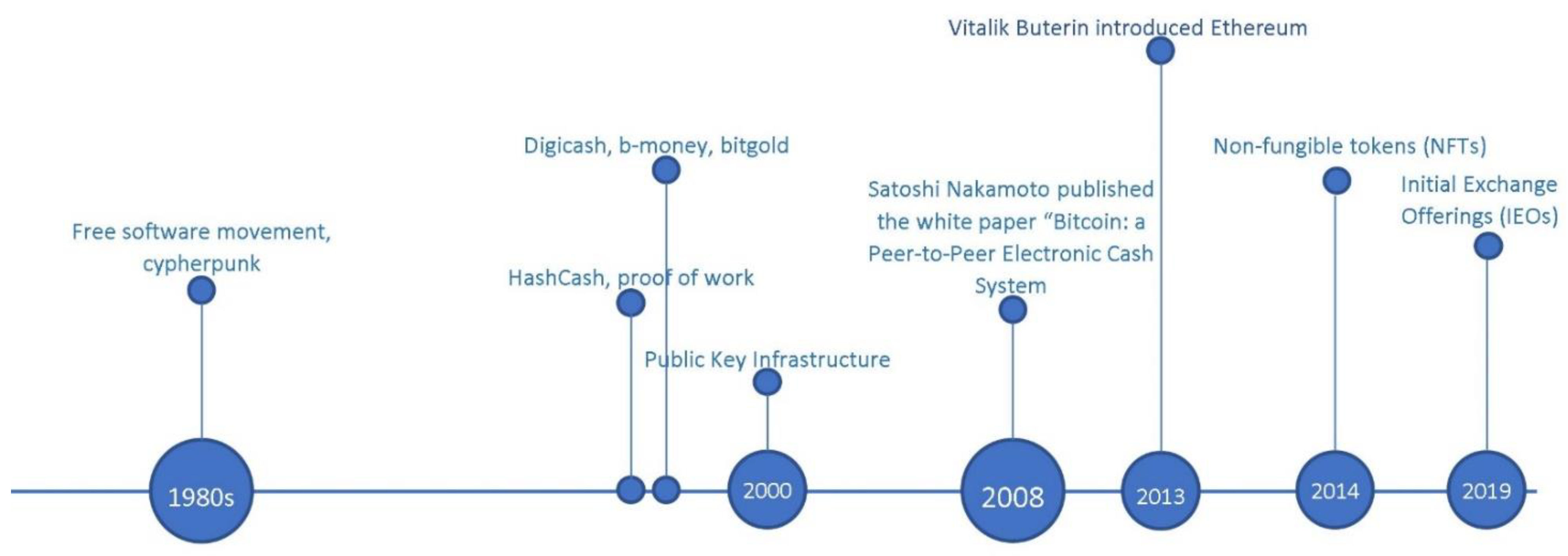

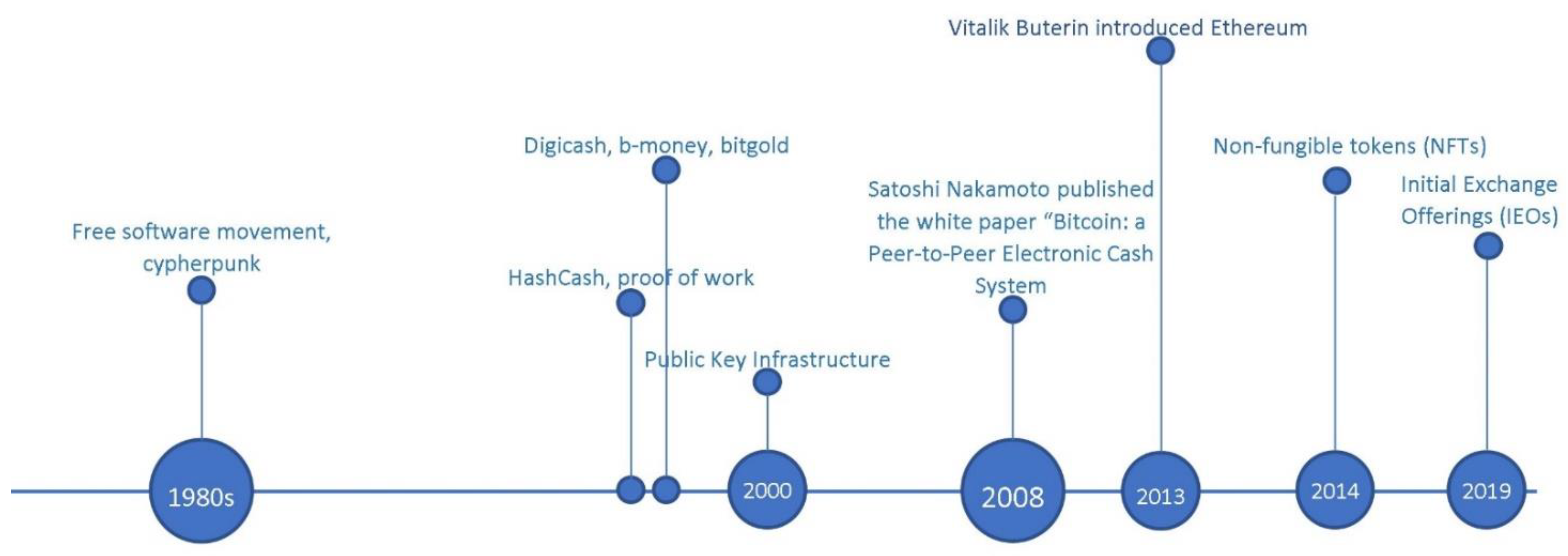

2.1. Blockchain History

2.2. Types of Cryptocurrencies

2.3. Using Data Mining with Blockchain

3. Research Objective

3.1. Data Sources, Collection, and Cleansing

3.2. Data Analysis

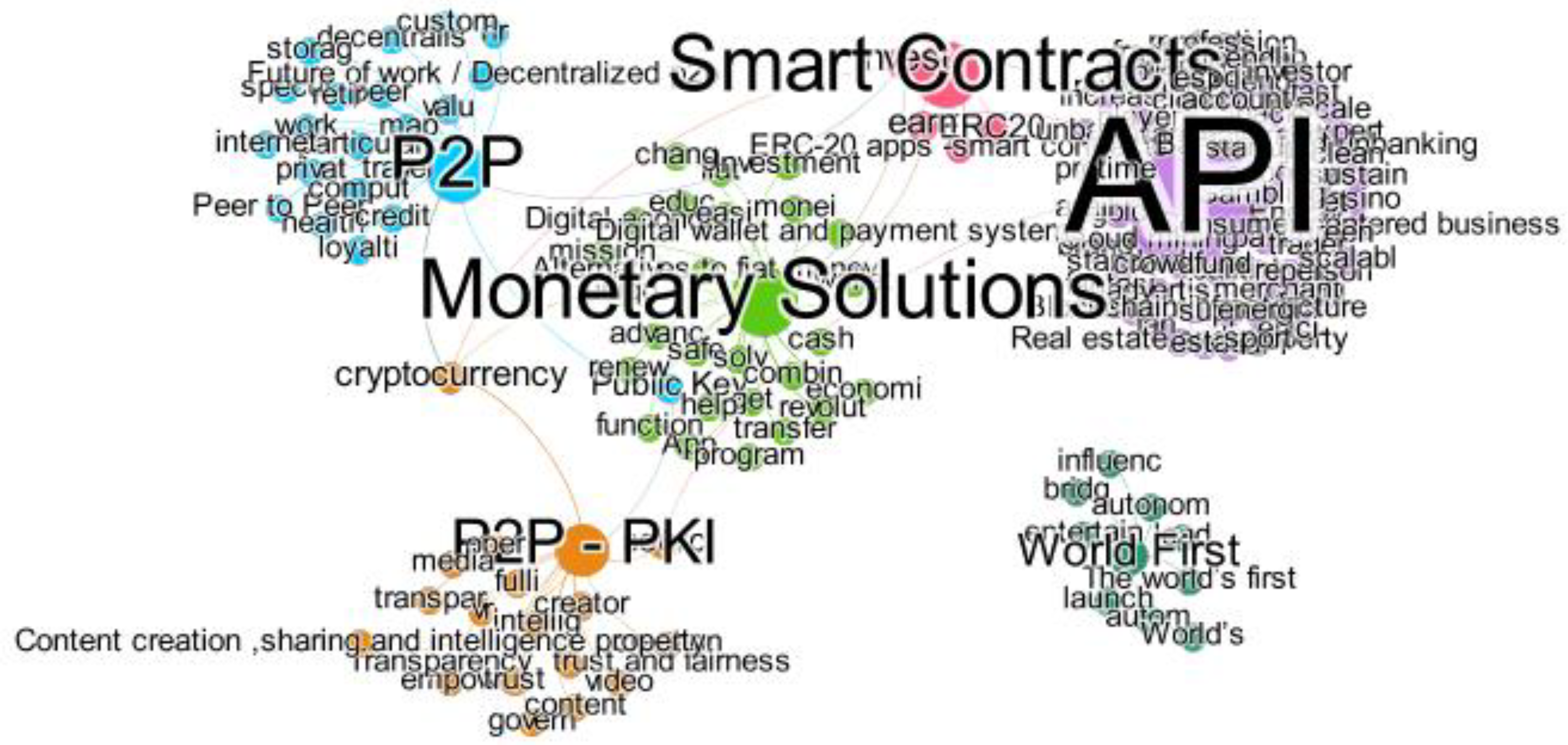

4. Results and Discussion

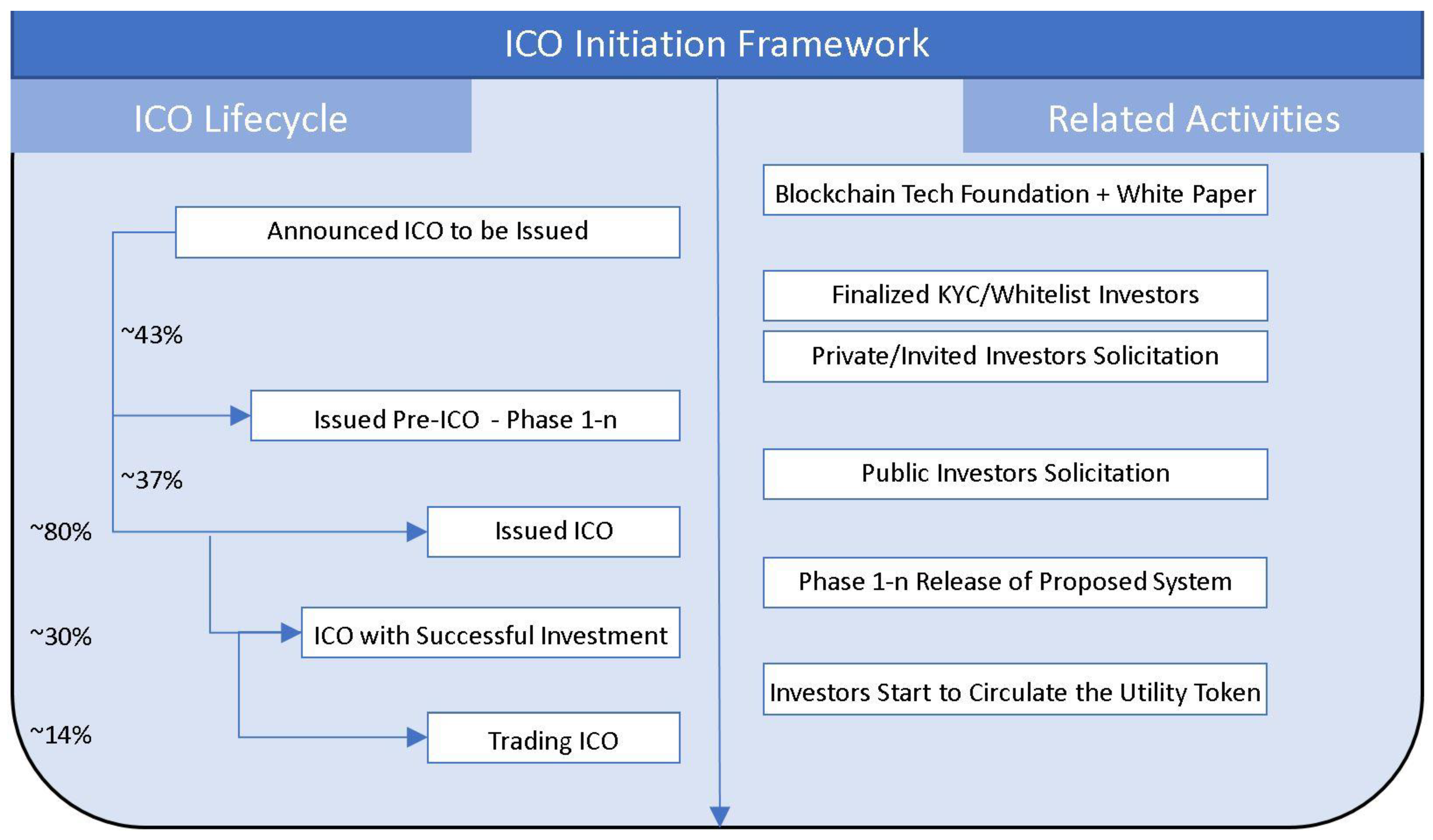

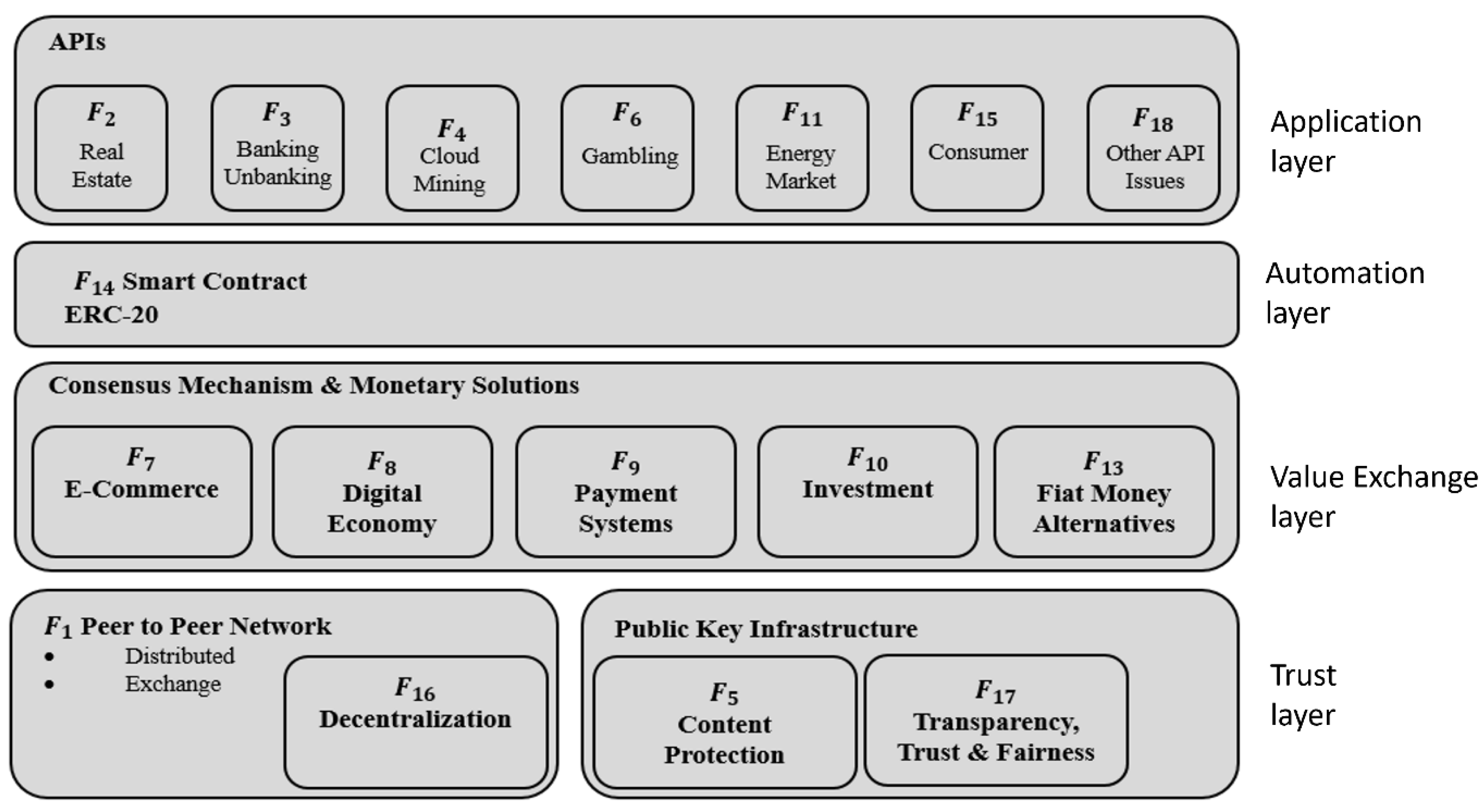

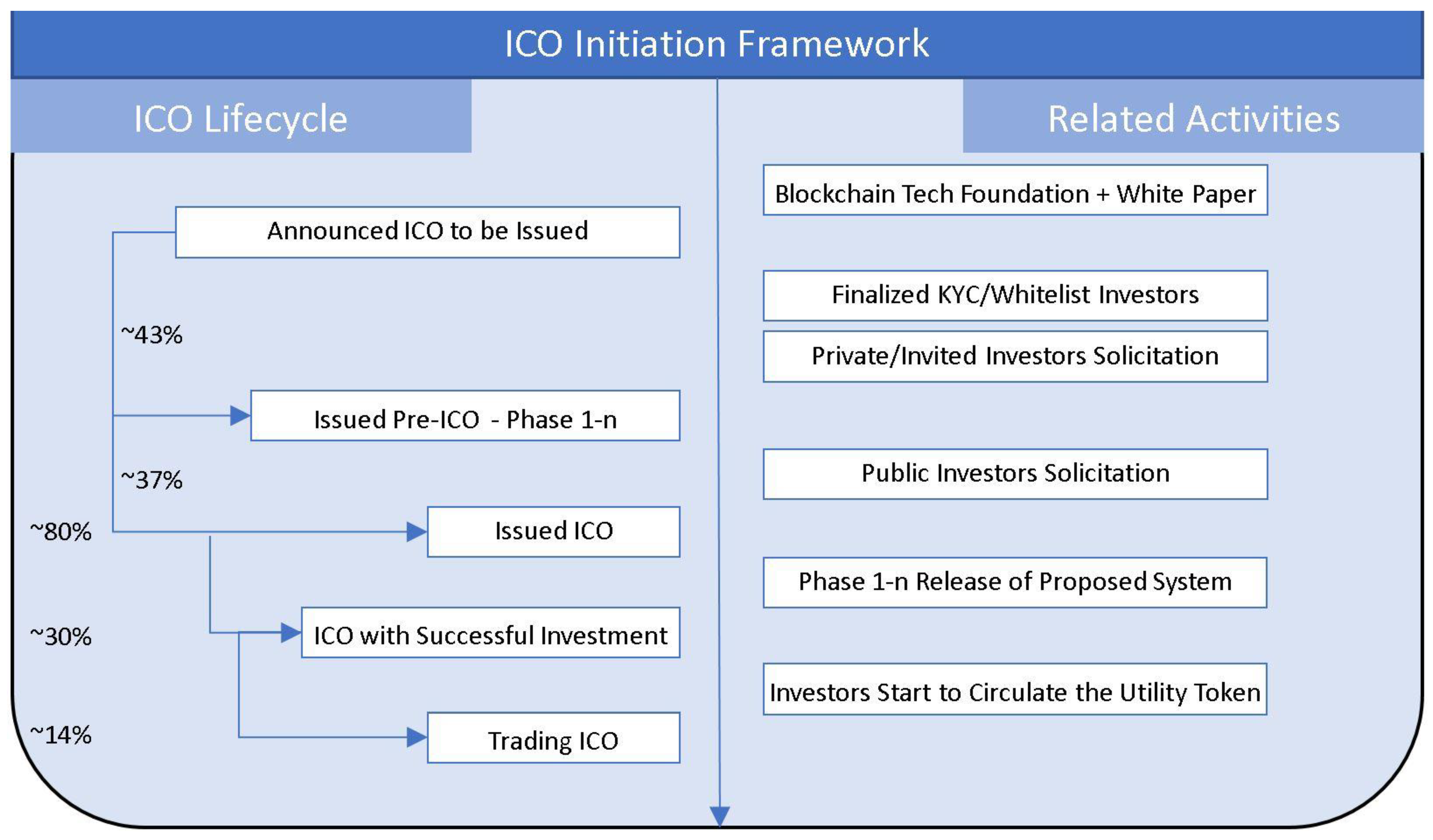

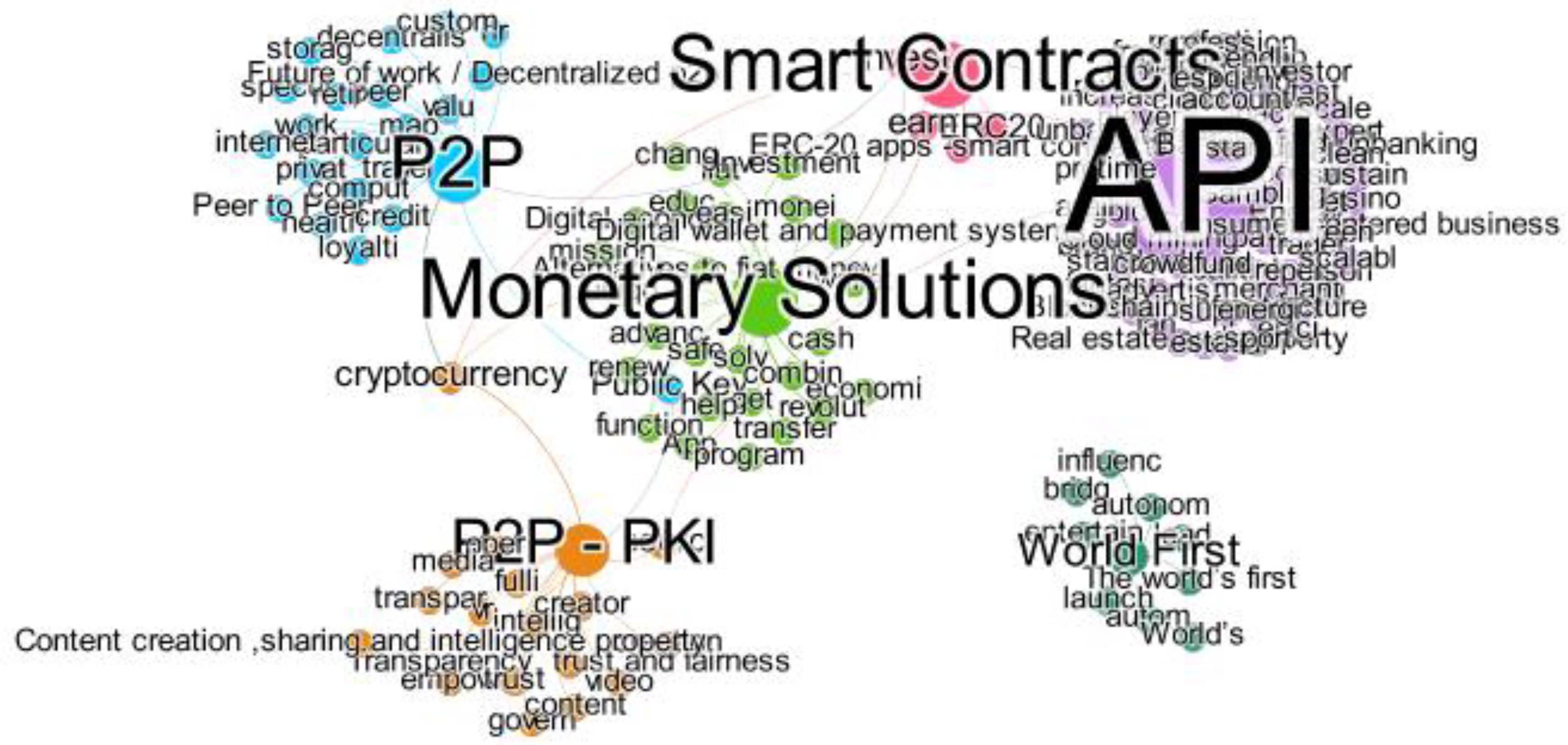

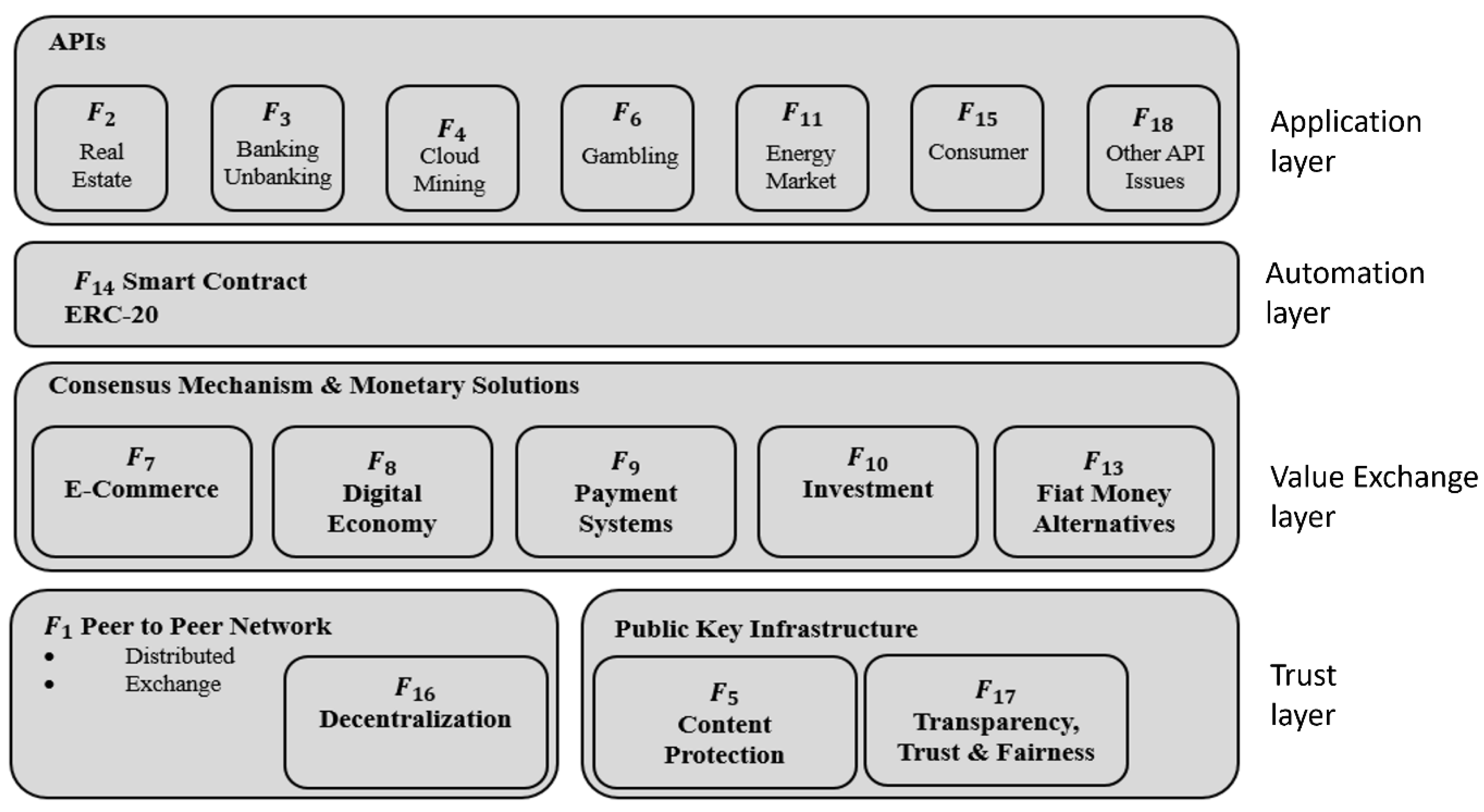

4.1. ICO Marketplace Stacked Layers Model

4.2. Blockchain Technology Definition

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Peer to Peer | peer endors map retir jet hr specul particular pow |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Real estate and property | estat advertis properti back rent rental fraction |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Banking and Unbanking | bank lend tradit unbank account card friendli |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Cloud Mining | mine profit gold crowdfund scale |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Digital Content Protection | content media creator video vr intellig monet artifici creation |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Gambling | bet sport event esport gambl fantasi standard casino revolutionari player fan |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

E-commerce | integr commerc sell bui suppli enterpris sector |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Digital Economy | economi uniqu get mission revolut |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Payment Systems | app wallet combin advanc function solv program |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Investment | investor trader opportun profession level avail expert time tool startup person |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Energy Market | util energi green sustain increas clean effici |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

The world’s first | world’s lead autonom autom bridg entertain influenc launch |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Fiat Money Alternatives | monei earn fiat help renew transfer easi educ chang safe cash |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Smart Contract | erc |

|

| Label | Top Loading Terms | Top Loading ICO Descriptions |

|---|---|---|

Consumer-centered Business | consum driven manufactur brand retail merchant |

|

| Label | Top Loading Terms | Top Loading ICOs Descriptions |

|---|---|---|

Decentralization | decentralis work privat custom loyalti internet travel credit store comput valu storag health |

|

| Label | Top Loading Terms | Top Loading ICOs Descriptions |

|---|---|---|

Transparency, Trust and Fairness | transpar oper sourc trust fulli fair empow govern |

|

| Label | Top Loading Terms | Top Loading ICOs Descriptions |

|---|---|---|

Blockchain Infrastructure Applications | infrastructur sourc support scalabl realiti virtual free multi softwar financ dapp cloud fast |

|

References

- Ahmad, Muhammad Farooq, Oskar Kowalewski, and Paweł Pisany. 2021. What determines initial coin offering success: A cross-country study. Economics of Innovation and New Technology, 1–24. [Google Scholar] [CrossRef]

- Altalhi, Abdulrahman H., José María Luna, M. A. Vallejo, and Sebastián Ventura. 2017. Evaluation and comparison of open source software suites for data mining and knowledge discovery. Wiley Interdisciplinary Reviews: Data Mining and Knowledge Discovery 7: e1204. [Google Scholar] [CrossRef]

- Ante, Lennart. 2022. Non-fungible token (NFT) markets on the Ethereum blockchain: Temporal development, cointegration and interrelations. Economics of Innovation and New Technology 1–19, 1–19. [Google Scholar] [CrossRef]

- Back, Adam. 2002. Hashcash—A Denial of Service Counter-Measure. Available online: http://www.hashcash.org/papers/hashcash.pdf (accessed on 22 November 2022).

- Bian, Shuqing, Zhenpeng Deng, Fei Li, Will Monroe, Peng Shi, Zijun Sun, Wei Wu, Sikuang Wang, William Yang Wang, Arianna Yuan, and et al. 2018. IcoRating: A Deep-Learning System for Scam ICO Identification. arXiv arXiv:1803.03670. [Google Scholar]

- Buterin, Vitalik. 2014. A Next-Generation Smart Contract and Decentralized Application Platform. Available online: https://cryptorating.eu/whitepapers/Ethereum/Ethereum_white_paper.pdf (accessed on 22 November 2022).

- Cai, Jinghan, and Ahmed Gomaa. 2019. Initial Coin Offering to Finance Venture Capital: A BehavioralPerspective. The Journal of Private Equity 22: 93–101. [Google Scholar] [CrossRef]

- Cao, Tianjie, Dongdai Lin, and Rui Xue. 2005. A randomized RSA-based partially blind signature scheme for electronic cash. Computers and Security 24: 44–49. [Google Scholar] [CrossRef]

- Catalini, Christian, and Joshua S. Gans. 2018. Initial Coin Offerings and the Value of Crypto Tokens. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Chitsazan, Hasti, Afsaneh Bagheri, and Mahdi Tajeddin. 2022. Initial coin offerings (ICOs) success: Conceptualization, theories and systematic analysis of empirical studies. Technological Forecasting and Social Change 180: 121729. [Google Scholar] [CrossRef]

- Chuanjie, Fu, Andrew Koh, and Paul Griffin. 2019. Automated theme search in ICO whitepapers. The Journal of Financial Data Science 1: 140–58. [Google Scholar] [CrossRef]

- Clark, David. 1988. The design philosophy of the DARPA Internet protocols. In Symposium Proceedings on Communications Architectures and Protocols. New York: Association for Computing Machinery, pp. 106–14. [Google Scholar]

- Cong, Lin William, and Zhiguo He. 2019. Blockchain disruption and smart contracts. The Review of Financial Studies 32: 1754–97. [Google Scholar] [CrossRef]

- Crain, Steven P., Ke Zhou, Shuang-Hong Yang, and Hongyuan Zha. 2012. Dimensionality reduction and topic modeling: From latent semantic indexing to latent dirichlet allocation and beyond. In Mining Text Data. Boston: Springer, pp. 129–61. [Google Scholar]

- Cunningham, William Michael, Bobby Henebry, and Hunter Horsley. 2019. BLOCKCHAIN: A Primer for Planners. Journal of Financial Planning 32: 23–25. [Google Scholar]

- Curran, Kevin, and John Honan. 2006. Eliminating the Volume of Spam E-Mails Using a Hashcash-Based Solution. Information Systems Security 15: 22–41. [Google Scholar] [CrossRef]

- De Andrés, Pablo, David Arroyo, Ricardo Correia, and Alvaro Rezola. 2022. Challenges of the market for initial coin offerings. International Review of Financial Analysis 79: 101966. [Google Scholar] [CrossRef]

- Dumais, Susan T., George W. Furnas, Thomas K. Landauer, Scott Deerwester, and Richard Harshman. 1988. Using latent semantic analysis to improve access to textual information. In Proceedings of the SIGCHI Conference on Human Factors in Computing Systems. New York: Association for Computing Machinery, pp. 281–85. [Google Scholar]

- Ellison, Carl, and Bruce Schneier. 2000. Ten risks of PKI: What you’re not being told about public key infrastructure. Computer Security Journal 16: 1–7. [Google Scholar]

- Evangelopoulos, Nicholas. 2011. Citing Taylor: Tracing Taylorism’s technical and sociotechnical duality through latent semantic analysis. Journal of Business and Management 17: 57–74. [Google Scholar]

- Evangelopoulos, Nicholas, Xiaoni Zhang, and Victor R. Prybutok. 2012. Latent semantic analysis: Five methodological recommendations. European Journal of Information Systems 21: 70–86. [Google Scholar] [CrossRef]

- Filipov, Nadezhda. 2018. Blockchain—An Opportunity For Developing New Business Models. Business Management 2018: 75–92. [Google Scholar]

- Fisch, Christian. 2019. Initial coin offerings (ICOs) to finance new ventures: An exploratory study. Journal of Business Venturing 34: 1–22. [Google Scholar] [CrossRef]

- Florysiak, David, and Alexander Schandlbauer. 2022. Experts or charlatans? ICO analysts and white paper informativeness. Journal of Banking & Finance 12: 106456. [Google Scholar]

- Golub, G. H., and C. Reinsch. 1970. Singular value decomposition and least squares solutions. Numerische Mathematik 14: 403–20. [Google Scholar] [CrossRef]

- Gomaa, Ahmed. 2018. The Creation of a Cryptocurrency to Support Disintermediation. Operatoins Management Education Review (OMER), 12. [Google Scholar] [CrossRef]

- Haber, Stuart, and W. Scott Stornetta. 1990. How to time-stamp a digital document. In Conference on the Theory and Application of Cryptography. Berlin: Springer, pp. 437–55. [Google Scholar]

- Halaburda, Hanna. 2018. Blockchain Revolution without the Blockchain? Communications of the ACM 61: 27–29. [Google Scholar] [CrossRef]

- Han, Jiawei, Jian Pei, and Micheline Kamber. 2011. Data Mining: Concepts and Techniques. Amsterdam: Elsevier. [Google Scholar]

- Hotho, Andreas, Andreas Nürnberger, and Gerhard Paaß. 2005. A brief survey of text mining. Ldv Forum 20: 19–62. [Google Scholar]

- Howell, Sabrina T., Marina Niessner, and David Yermack. 2018. Initial Coin Offerings: Financing Growth with Cryptocurrency Token Sales. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Hu, Yifan. 2005. Efficient, high-quality force-directed graph drawing. Mathematica Journal 10: 37–71. [Google Scholar]

- ICOBench.com. 2022. September 17. Available online: https://icobench.com/ (accessed on 22 November 2022).

- Jensen, Lars Juhl, Jasmin Saric, and Peer Bork. 2006. Literature mining for the biologist: From information retrieval to biological discovery. Nature Reviews Genetics 7: 119–29. [Google Scholar] [CrossRef] [PubMed]

- Jongsub, Lee, Tao Li, and Donghwa Shin. 2022. The Wisdom of Crowds in FinTech: Evidence from Initial Coin Offerings. The Review of Corporate Finance Studies 11: 1–46. [Google Scholar]

- Kaminska, Izabella. 2019. Blockchain officially confirmed as slower and more expensive. Financial Times. May 29. Available online: https://ftalphaville.ft.com/2019/05/29/1559146404000/Blockchain-officially-confirmed-as-slower-and-more-expensive/ (accessed on 22 November 2022).

- Karpenko, Oksana A., Tatiana K. Blokhina, and Lali V. Chebukhanova. 2021. The Initial Coin Offering (ICO) Process: Regulation and Risks. Journal of Risk and Financial Management 14: 599. [Google Scholar] [CrossRef]

- Keogh, Eamonn, and Abdullah Mueen. 2011. Curse of dimensionality. In Encyclopedia of Machine Learning. Boston: Springer, pp. 257–58. [Google Scholar]

- Kostovetsky, Leonard, and Hugo Benedetti. 2018. Digital Tulips? Returns to Investors in Initial Coin Offerings. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Lansky, Jan. 2018. Possible state approaches to cryptocurrencies. Journal of Systems Integration 9: 19–31. [Google Scholar] [CrossRef]

- Lansky, Jan. 2019. Cryptocurrency survival analysis. The Journal of Alternative Investments 22: 55–64. [Google Scholar] [CrossRef]

- Laskowski, M., and H. M. Kim. 2016. Rapid Prototyping of a Text Mining Application for Cryptocurrency Market Intelligence. Paper presented at IEEE 17th International Conference on Information Reuse and Integration (IRI), Pittsburgh, PA, USA, July 28–30. [Google Scholar]

- Lemchuk, Stephanie A. 2016. Virtual Whats: Defining Virtual Currencies in the Face of Conflicting Regulatory Guidances. Cardozo Public Law, Policy, and Ethics Journal 15: 319. [Google Scholar]

- Lin, Xiaolin, Yibai Li, and Xuequn Wang. 2017. Social commerce research: Definition, research themes and the trends. International Journal of Information Management 37: 190–201. [Google Scholar] [CrossRef]

- Lochbaum, Karen E., and Lynn A. Streeter. 1989. Comparing and combining the effectiveness of latent semantic indexing and the ordinary vector space model for information retrieval. Information Processing & Management 25: 665–76. [Google Scholar]

- Lockaby, C. Daniel. 2018. The Sec Rides into Town: Defining an Ico Securities Safe Harbor in the Cryptocurrency Wild West. Georgia Law Review 53: 335–66. [Google Scholar]

- Mai, Feng, Zhe Shan, Qing Bai, Xin (Shane) Wang, and Roger H. L. Chiang. 2018. How Does Social Media Impact Bitcoin Value? A Test of the Silent Majority Hypothesis. Journal of Management Information Systems 35: 19–52. [Google Scholar] [CrossRef]

- Masood, Saleha, Muhammad Alyas Shahid, Muhammad Sharif, and Mussarat Yasmin. 2018. Comparative Analysis of Peer to Peer Networks. International Journal of Advanced Networking and Applications 9: 3477–91. [Google Scholar]

- Morrison, Alan, and Subhankar Sinha. 2016. Blockchain and smart contract automation: Blockchains defined. In The Future of Law and Technologies. Edited by Tanel Kerikmae and Addi Rull. Berlin and Heidelberg: Springer. [Google Scholar]

- Nakamoto, Satoshi. 2008. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 22 November 2022).

- Pazaitis, Alex, Primavera De Filippi, and Vasilis Kostakis. 2017. Blockchain and value systems in the sharing economy: The illustrative case of Backfeed. Technological Forecasting and Social Change 125: 105–16. [Google Scholar] [CrossRef]

- Prentis, Mitchell. 2015. Digital Metal: Regulating Bitcoin as a Commodity. Case Western Reserve Law Review 66: 609–38. [Google Scholar]

- Qiang, Minqian, and Fei Lin. 2019. The Challenges of Existence, Status, and Value for Improving Blockchain. IEEE Access 7: 7747–58. [Google Scholar]

- Salton, Gerard, Anita Wong, and Chung-Shu Yang. 1975. A vector space model for automatic indexing. Communications of the ACM 18: 613–20. [Google Scholar] [CrossRef]

- Sapkota, Niranjan, and Klaus Grobys. 2021. Fear Sells: Determinants of Fund-Raising Success in the cross-section of Initial Coin Offerings. SSRN. [Google Scholar] [CrossRef]

- Senderowicz, Jeremy I., K. Susan Grafton, Timothy Spangler, Kristopher D. Brown, and Andrew J. Schaffer. 2018. SEC focuses on initial coin offerings: Tokens may be securities under federal securities laws. Journal of Investment Compliance 19: 10–14. [Google Scholar] [CrossRef]

- Sidorova, Anna, Nicholas Evangelopoulos, Joseph S. Valacich, and Thiagarajan Ramakrishnan. 2008. Uncovering the intellectual core of the information systems discipline. MIS Quarterly 32: 467–82. [Google Scholar] [CrossRef]

- Stenqvist, Evita, and Jacob Lönnö. 2017. Predicting Bitcoin Price Fluctuation with Twitter Sentiment Analysis. Stockholm: KHT. [Google Scholar]

- Sun, Yin Hao Hua, Klaus Langenheldt, Mikkel Harlev, Raghava Rao Mukkamala, and Ravi Vatrapu. 2019. Regulating Cryptocurrencies: A Supervised Machine Learning Approach to De-Anonymizing the Bitcoin Blockchain. Journal of Management Information Systems 36: 37–73. [Google Scholar] [CrossRef]

- Swartz, Lana. 2022. Theorizing the 2017 blockchain ICO bubble as a network scam. new media & society. New Media & Society 24: 1695–713. [Google Scholar]

- Takahashi, Koji. 2020. Prescriptive Jurisdiction in Securities Regulations: Transformation from the ICO (Initial Coin Offering) to the STO (Security Token Offering) and the IEO (Initial Exchange Offering). Ilkam Law Review 20: 31–50. [Google Scholar] [CrossRef]

- Thewissen, James, Prabal Shrestha, Wouter Torsin, and Anna M. Pastwa. 2022. Unpacking the black box of ICO white papers: A topic modeling approach. Journal of Corporate Finance 75: 102225. [Google Scholar] [CrossRef]

- Tirunillai, Seshadri, and Gerard J. Tellis. 2014. Mining marketing meaning from online chatter: Strategic brand analysis of big data using latent dirichlet allocation. Journal of Marketing Research 51: 463–79. [Google Scholar] [CrossRef]

- Varma, Jayanth Rama. 2019. Blockchain in Finance. The Journal for Decision Makers 44: 1–11. [Google Scholar] [CrossRef]

- Viriyasitavat, Wattana, and Danupol Hoonsoponb. 2019. Blockchain characteristics and consensus in modern business processes. Journal of Industrial Information Integration 13: 32–39. [Google Scholar] [CrossRef]

- Winotoatmojo, Hugo Prasetyo, Idris Gautama, Elidjen, and Meyliana. 2022. Initial Coin Offering (ICO) an Innovation Funding for Digitalpreneur. I T A L I E N I S C H 12: 1–9. [Google Scholar] [CrossRef]

- Yousif, Ahmed. 2022. Blockchain: The Protocol of Value. Makkah, Saudi Arabia. June 1. Available online: https://bsvblockchain.org/news/blockchain-the-protocol-of-value/ (accessed on 22 November 2022).

- Yu, Ju Hyun, Juyoung Kang, and Sangun Park. 2019. Information availability and return volatility in the bitcoin Market: Analyzing differences of user opinion and interest. Information Processing & Management 56: 721–31. [Google Scholar]

- Zetzsche, Dirk A., Ross P. Buckley, Douglas W. Arner, and Linus Föhr. 2017. The ICO Gold Rush: It’s a scam, it’s a bubble, it’s a super challenge for regulators. University of Luxembourg Law Working Paper 11: 17–83. [Google Scholar] [CrossRef]

- Zhang, Shuyu, Walter Aerts, Liping Lu, and Huifeng Pan. 2019. Readability of token whitepaper and ICO first-day return. Economics Letters 180: 58–61. [Google Scholar] [CrossRef]

- Zheng, Zibin, Shaoan Xie, Hong-Ning Dai, Xiangping Chen, and Huaimin Wang. 2018. Blockchain challenges and opportunities: A survey. International Journal of Web and Grid Services 14: 352–75. [Google Scholar] [CrossRef]

- Zhu, Dan, and Yuanfeng Cai. 2016. Fraud detections for online businesses: A perspective from blockchain technology. Financial Innovation 2: 20. [Google Scholar]

- Zutshi, Aneesh, Antonio Grilo, and Tahereh Nodehi. 2021. The value proposition of blockchain technologies and its impact on digital platforms. Computers & Industrial Engineering 155: 107187. [Google Scholar]

| Terms | Loadings | Top Loading ICO Descriptions |

|---|---|---|

| peer advertis bet economi estat content bank world’s internet freelanc bui decentralis monei integr sell investor energi fulli consum work | 0.882 0.096 0.094 0.086 0.071 0.067 0.066 0.061 0.061 0.06 0.058 0.057 0.056 0.054 0.054 0.053 0.053 0.052 0.05 0.05 |

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gomaa, A.; Li, Y. An Entrepreneurial Definition of the Blockchain Technology and a Stacked Layer Model of the ICO Marketplace Using the Text Mining Approach. J. Risk Financial Manag. 2022, 15, 557. https://doi.org/10.3390/jrfm15120557

Gomaa A, Li Y. An Entrepreneurial Definition of the Blockchain Technology and a Stacked Layer Model of the ICO Marketplace Using the Text Mining Approach. Journal of Risk and Financial Management. 2022; 15(12):557. https://doi.org/10.3390/jrfm15120557

Chicago/Turabian StyleGomaa, Ahmed, and Yibai Li. 2022. "An Entrepreneurial Definition of the Blockchain Technology and a Stacked Layer Model of the ICO Marketplace Using the Text Mining Approach" Journal of Risk and Financial Management 15, no. 12: 557. https://doi.org/10.3390/jrfm15120557

APA StyleGomaa, A., & Li, Y. (2022). An Entrepreneurial Definition of the Blockchain Technology and a Stacked Layer Model of the ICO Marketplace Using the Text Mining Approach. Journal of Risk and Financial Management, 15(12), 557. https://doi.org/10.3390/jrfm15120557