2. Literature Review

The definition of the term “insurance” given in the dictionary by S.I. Ozhegov and N.Yu. Shvedova is as follows: “Insurance is preventing material losses by payment to the institution, which undertakes to reimburse any damage incurred in specially stipulated cases”. To be able to cover losses and remain competitive, an insurance company must focus its efforts on those services that bring maximum profit. However, how can one determine what services (or in this case, insurance risks) are profitable? It is not possible to divide insurance risks into profitable and unprofitable ones by the method of determining the cost of services used for production companies.

The problem of organizing management accounting in insurance companies from the point of view of classifying insurance risks is particularly acute in countries where the purchasing power of the population is low. In Poland, some authors (

Tomczyk et al. 2016) note that the expectations related to the introduction of information systems of insurance management are often unjustified, and sales of insurance products often show completely surprising trends. The same problems are observed in the countries of eastern Europe by (

Bokšová 2015), who focus on the connection of these trends with the shortcomings of management accounting and the results of operations. The authors (

Lee and Lin 2016) come to a similar conclusion based on the study of 30 OECD countries, which, in recent years, have manifested the effects of globalization (among them is Poland due to the effects of its entry into the EEC, Russia after signing WTO agreements, the socialist countries of southeast Asia due to the liberalization of economic policy, and so on). In particular, in Turkey, there has been a significant structural change in the economic sector of insurance, indicated by (

Kalkavan et al. 2015) through the example of changes in a large insurance company. This work shows that successful changes in the accounting system with the purpose of management can lead to positive changes in the financial dynamics under the conditions of unwanted external influence. Turkey is a specific country in terms of the features of life and health insurance. Medical services provided in Turkey are highly appreciated by society; therefore, medical insurance, covering 85% of the population (

Now Health International 2017), should not be subject to changes, but the fact remains. From 2013 to 2016, profit after tax in the insurance industry has decreased from

$645 million to

$92 million due to the depreciation of lira and a reduction in the profitability of the market with a relatively stable number of companies in it (

Turkish Statistical Institute 2018).

As a result of such external influences, many insurance companies do not survive the competition and become unprofitable, including those in Russia. As of 1 January 2016, 326 insurance companies were registered in the Unified State Register of Insurance Entities, and as of 1 August 2017, that number was 305 (“Insurance Entities” 2018). The total number of insurers has decreased during this period by 21 companies and additionally, in 2015, by 65 companies compared with the data of 1 January 2016. Under these circumstances, the improvement of management accounting for insurance companies is of great practical interest. The views of scientists who believe that the purpose of management accounting is to provide information to managers responsible for achieving specific production goals (

Needles et al. 1992) are the most reasonable.

Among the most important problems in the sphere of management of an insurance business, there are the problems of financial stability and solvency of insurance companies (

Sanchis et al. 2007). The latter work considers their financial stability in both microeconomic and macroeconomic senses by the example of Spain, where a combination of changes in monetary policy and the growing insolvency of insurance companies has led to the need for more complicated accounting methods and management. The monitoring and evaluation of the financial condition are important for both individual insurance companies and the insurance market in general. The financial condition of the insurance market, as shown in (

Hainaut 2017) (for the part of the insurance market that does not include life insurance), is in bidirectional communication with the finance market. Mutual random and tendentious impacts of the financial and insurance markets, modeled by the authors, show the importance of improving the information support of decision-making in insurance companies worldwide.

Thus, the author will consider the solution of the problem of improving management accounting in insurance companies by improving the quality of information provision and decision support for risk management.

3. Materials and Methods

Let us decide the above assigned tasks based on data of Russian insurance companies, heavily influenced by external factors. Key performance indicators of insurance organizations in Russia are given in

Table 1.

As can be seen from

Table 1, the number of organizations by 2017 decreased by 4 percent; the concentration of assets has increased by more than 16 percent. The capital was increased by 6.46 percent, but liabilities have increased by a greater percentage of 22.71%, which resulted in reducing capital stock by 6.6 percent. As a result of the increase in profit by 60.31 percent in 2014, the profitability increased by 82 percent.

Table 2 presents the top 20 insurance companies (according to their cash flows from current activities) in Russia in 2017, engaged in voluntary and compulsory insurance (except compulsory medical insurance).

Table 2 shows that cash flows from current activities, including insurance premiums, for the top 20 insurance companies in Russia amounted to more than 79 percent of the total insurance market. Among them, SOGAZ has 41.41% of income and ranked second among all insurance companies. The top five were as follows: SOGAZ, Sberbank Life Insurance, Rosgosstrakh, RESO-Garantia, and Ingosstrakh. Overall, the share of income of the top five made up 46.66 percent, that is, almost half of all revenues across the insurance market.

Table 3 presents the best 20 insurance companies in Russia in 2017 according to amount of payments.

The five companies with the largest payments in Russia were as follows: Rosgosstrakh, Sogaz, Reso-Garantia, Ingosstrakh, and VSK. Overall, the share of income of the top five made up 46.66 percent, that is, almost half of all revenues across the insurance market. Among them, JSC “SOGAZ” has 13.49% of payments and ranked second among all insurance companies.

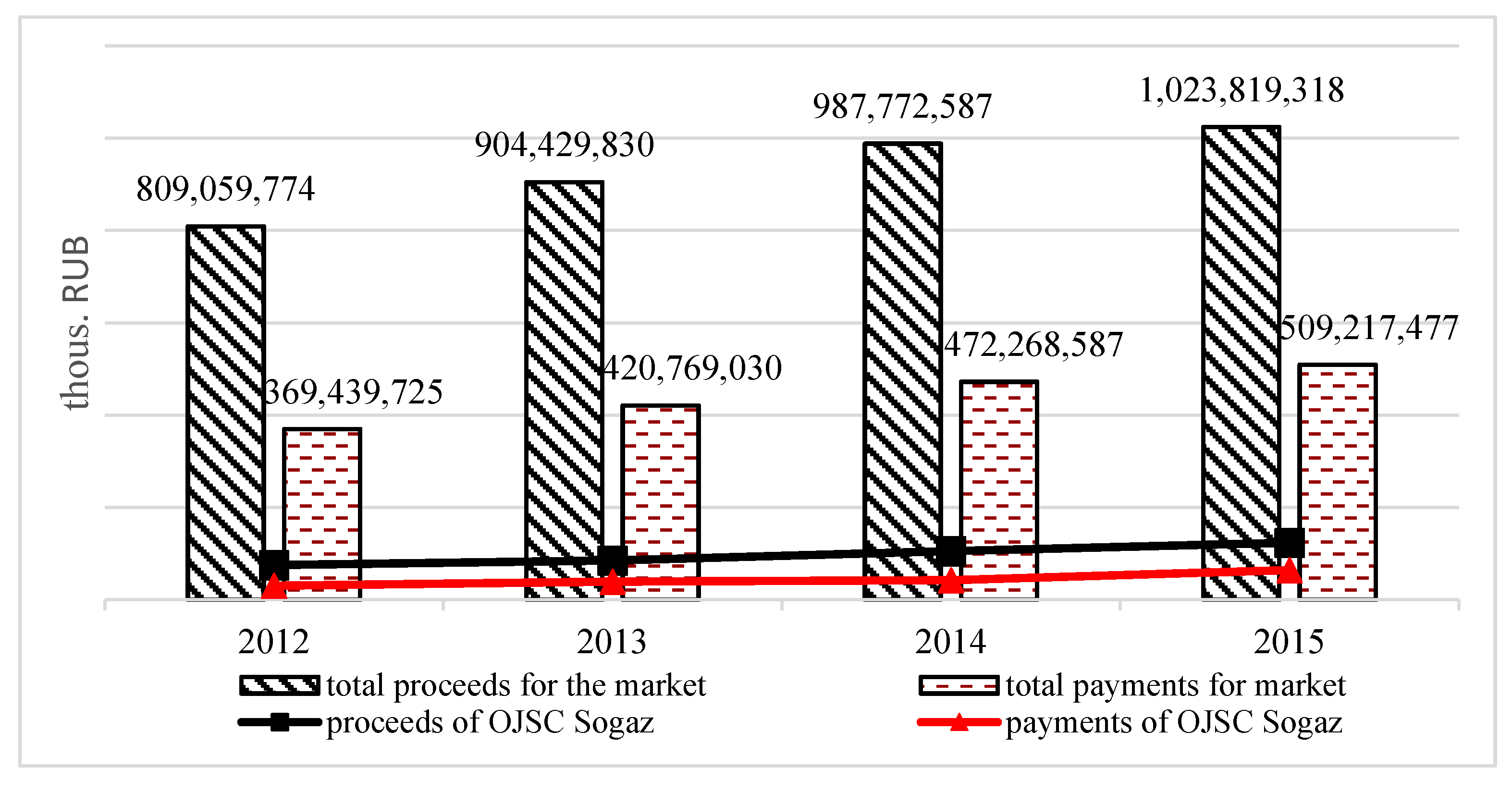

To illustrate the trends, continuing to the present,

Figure 1 shows a comparison of the level of proceeds and payments for voluntary and compulsory insurance (except compulsory medical insurance) in the insurance market of Russia and JSC “SOGAZ”.

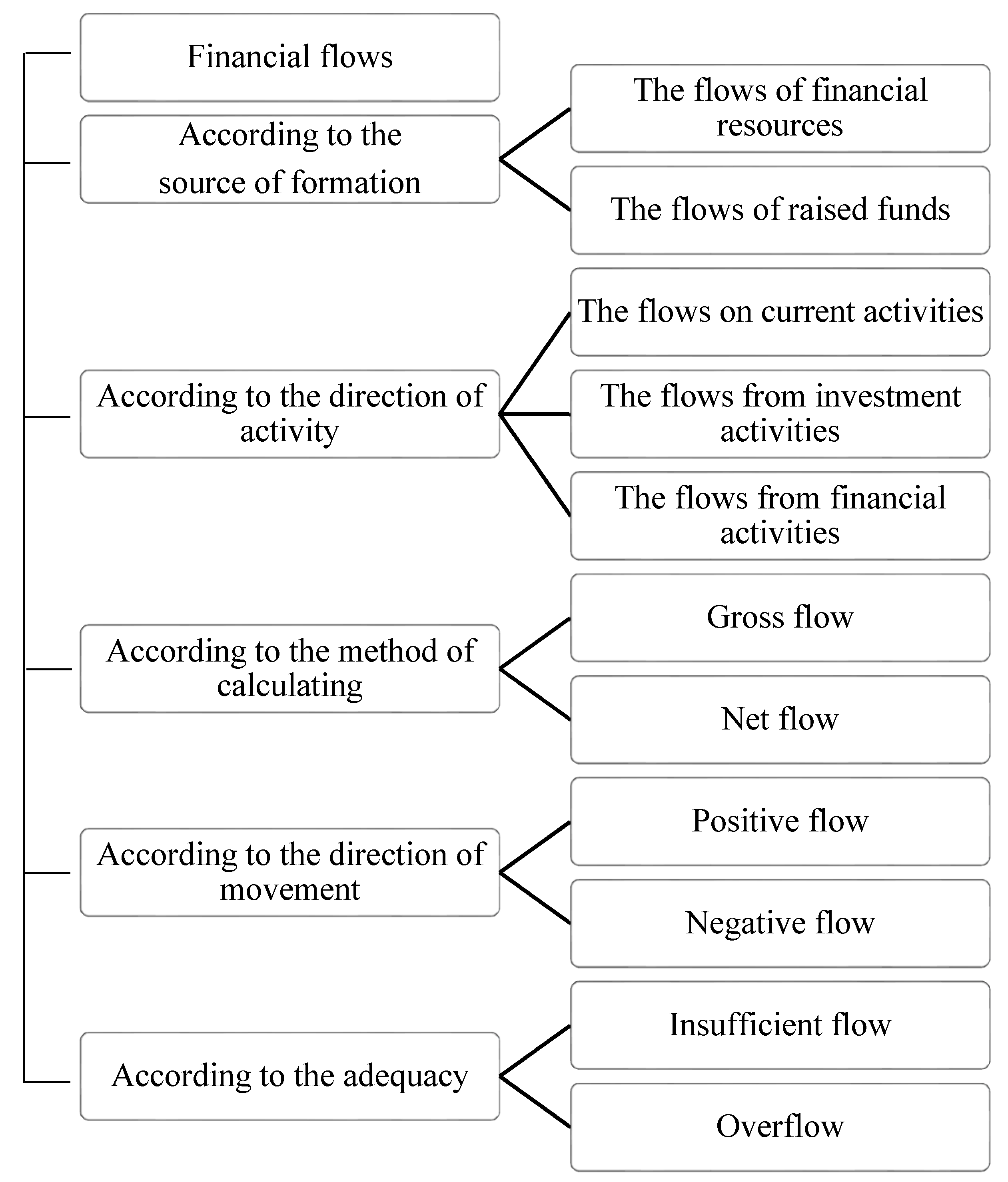

An insurance company, in order to meet its obligations to policyholders, must have certain financial capacity. The financial capacity of the insurer is the financial resources that are in financial turnover and are used for the implementation of the financial, investment, and insurance activities.

The activity of an insurance company involves accumulating monetary funds. The movement of the insurer’s funds represents the circulation of financial flows, that is, their receipt, expenditure, and conversion. The classification of financial flows is presented in

Figure 2.

The main sources of the inflow of insurers’ revenues remain the insurance premiums, and the outflow is business expenses and insurance payments. The cash inflow is a positive cash flow, and the cash outflow is a negative cash flow. These flows either increase or reduce the capital, transforming it from one form to another. The main challenge in the management of financial flows is to determine the degree of sufficiency of limited monetary resources and effective and optimal directions for their use.

The methodological basis of an accounting organization in Russia is the system of methods and specific techniques (inventory, use of certain documentation, a balance sheet, a system of synthetic and analytical accounts using the method of double entry, valuation of assets and liabilities, other balance sheet items, costing and reporting of the enterprise) (

Babchenko et al. 2003). Other countries have similar accounting systems that differ in details. It is stated (

Hellmann 2016) that accounting standards have a significant impact on the behavioral patterns of those who use the results of the accounting. This article deals with the relationship between accounting and managerial accounting in production enterprises. It seems that the impact of a particular accounting methodology in insurance, where much is based on vague and poorly justified desires and decisions of customers, is even bigger. This is particularly evident in Russia, where, because of the nature of the political system, there are high risks, for example, in life and health insurance. Even foreign researchers (

Jaspersen and Richter 2015;

Ramsay and Oguledo 2012) note that in fact, a very small part of the population is provided with public health services in Russia. At the same time, the financial performance of the mandatory health insurance system is low. Therefore, the market for additional health insurance can be very extensive; however, the issues of management accounting in insurance organizations should be addressed effectively.

Management accounting also applies its own system of methods and specific techniques (the system of synthetic and analytical accounts, costing and reporting). The essence of the method of full cost in management and financial accounting coincides. Although, the method of reduced costs in management accounting has its own characteristics: the cost value includes only variable manufacturing costs. The exclusion of fixed costs from the point of view of people making management decisions is logical, as it is impossible to influence their amount. This methodology is reflected, in particular, in the formation of prices of insurance services not only in Russia, but also in the world (

Ramsay and Oguledo 2012). In foreign terminology, “variable costs” are referred to as transaction costs; they affect not only the offer price but also the size of the insurance premium. In (

Ramsay and Oguledo 2012) and many other works (

Bokšová 2015;

Jaspersen and Richter 2015), it is noted that variable costs are almost proportional to the volume of contracts. This hypothesis will be further developed.

In the insurance business, variables include the costs connected with the following:

(1) the preparation and conclusion of the contract;

the cost of development of new conditions

the cost of attracting new customers

the cost of risk assessment

(2) the execution of the contract.

Variable costs of insurance companies vary in total in direct proportion to the increase (decrease) in the volume of insurance contracts. For example, if the volume of contracts increased by 15%, then variable costs will increase by 15%. The fixed costs of an insurance company remain unchanged with the change in the volume of contracts concluded during the whole period selected for analysis. For example, the cost of car insurance does not depend on what mileage will be passed by the car. Fixed costs of insurance companies may include, for example, administrative costs, rent, and those that do not change with changes in the volume of contracts. This means that both general and average fixed costs for one contract are, for example, 18,000,000 RUB. If two contracts are concluded during the reporting period, the total fixed costs remain unchanged (18,000,000 RUB), while the average fixed cost per contract is reduced by half (9,000,000 RUB).

With the growth of the volume of contracts, the average fixed cost per contract decreases less and less. For example, the difference in this indicator between the 1st and 2nd signed contracts is 9,000,000 RUB, that between the 10th and 11th contracts is about 1,637,000 RUB, that between the 200th and 201st contracts is about 448 RUB, and that between the 400th and 401st contracts is a little more than 112 RUB. Thus, the greater the volume of contracts, the smaller the share of fixed costs per unit, and thus the more justified the fixed costs of an insurance company.

The main expense of an insurance company under the contract of insurance is the payment of insurance indemnity (security) or funding loss. This group includes the costs for the settlement of damages (payment for the services of rescuers and experts).

In relation to core activities (insurance operations), expenses are divided into two large groups:

- (a)

the costs of the insurance company associated with insurance transactions;

- (b)

the costs of the insurance company, not directly related to insurance activities.

Expenses on insurance operations are presented by the articles reflecting the content of insurance coverage:

expenses for the payment of insurance claims and insurance amounts (insurance amounts are paid in the case of applying accumulative insurance types);

contributions to the replacement funds and policy reserve funds.

These funds are intended for the fulfillment of obligations under insurance contracts in the future.

An insurance company may also accumulate reserves for the financing of preventive measures. The composition of the costs included in the cost of insurance services includes the following:

- (1)

the payments to the reserve for financing preventive measures;

- (2)

reimbursement of payments under contracts of reinsurance;

- (3)

commission on reinsurance contracts;

- (4)

the costs of the proceedings;

- (5)

the expenses for the lease of fixed assets;

- (6)

other costs related to the insurance activities.

Many economic situations and processes require quick decisions. In Russia and in the world, the behavior of customers of insurance companies, to put it mildly, is variable. In (

Kairies-Schwarz et al. 2017), it is shown that about 14% of European customers of insurers demonstrated inconsistent behavior and decisions of low quality. Therefore, in the case of changes in the position of individual clients at the level of a front-end insurance organization or changes in the trends at the level of Chief executive officer (CEO), quick decisions should be made. Therefore, managers of insurance companies must have information about the upcoming profit per week, month, and so on, and must not engage in analysis and control statements. The decision by the insurer should not be lingering on specific insurance cases in order to achieve, for example, consent from the client to reduce compensation. This underlines the weaknesses of insurance companies with low-profit margins. Insurance companies must adapt to the situation in the market, instead of setting their own prices for services on the principle of “expenses plus profit”.

Management accounting uses the direct costing method, which allows dividing an organization’s expenses into variable and constant expenses and, as a result, identifying weak areas that negatively affect the financial result. A report according to the system of management accounting is represented by the indicator of marginal income, which is very important for taking managerial decisions on the prime cost of insurance services.

Thus, the first stage in making operational decisions on the management of an insurance company is dividing the expenses into variable and constant expenses. It is necessary to group the data of primary documents in order to form a list of objects of analytical accounting of insurance payments heterogeneously by the severity of loss. Based the data on variable and constant expenses, the revenue from the received insurance premiums, and the number of concluded contracts, a report on the income and expenses can be compiled for the whole company, its structural subdivisions, and individual types of insurance risks. The second stage includes the calculation of marginal income and preparation of the report. The third stage is determining the funding sources for risk management and the direction of fund use. The next stage is the differentiation of the centers of responsibility in the enterprises for the purpose of better control over the preservation of the insured property (for this purpose, an intracompany ledger is proposed).

It is necessary to build a multistage hierarchical structure of the analytical accounting of payments in insurance organizations, taking into account the severity of loss. With the help of actuarial calculations, the mathematical probability of occurrence of the insured event is calculated, and the frequency and severity of the consequences of inflicted damage are determined both in separate risk groups and for the entire set of insurance objects. As the company makes insurance payments using its insurance reserves, one should determine the amount of insurance reserves. In this regard, an important task of management accounting is to develop a practicable grouping of costs for improving the quality of risk assessment, in order to develop a system of accounts to group the necessary information and reflect the received information in effective (in terms of the process of communication) reporting forms. Thus, the authors propose to implement risk accounting according to the severity of losses.

4. Results and Discussion

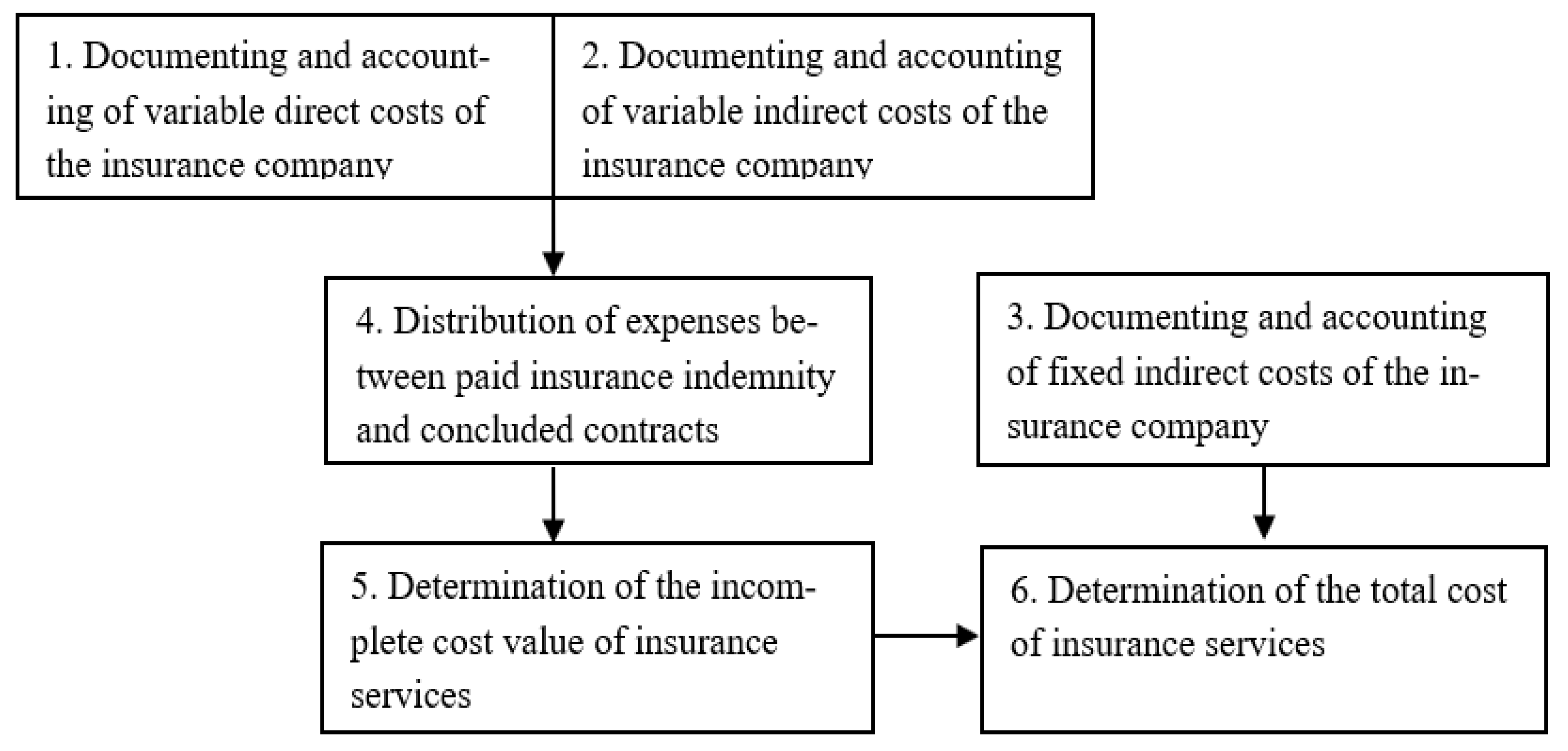

Based on the above, the sequence of execution of accounting procedures in the application of the management accounting system can be represented in the form of a diagram (

Figure 3).

In accordance with the accounting rules adopted in Russia, in the first block on the debit of acc. 20 “Basic production” and 23 “Auxiliary production”, direct variable materials and labor costs of the insurance company are considered. In the second block, variable indirect overhead costs are considered, which at the end of the reporting period, become the debit of acc. 20 “Primary production” and are distributed among insurance risks. In the third block, constant overhead and general expenses of the insurance company are considered. In the fourth block, variable indirect costs are allocated between the paid insurance indemnities and treaties, on which no insured accident had occurred on a certain date. In the fifth block, the variables in the cost of insurance are charged to the cost value of contracts. In the sixth block, the variable cost of issued insurance contracts (incomplete) and fixed costs for conducting insurance business are deducted on account of concluded contracts. The result is the total cost value of contracts.

Based on the data about variable and fixed costs, as well as on revenues from the insurance contributions and the number of contracts, a report on income and expenses for the whole company, its business units, and certain types of insurance risks can be compiled. The report covers the following indicators:

- (1)

income from insurance operations (formed by the incoming insurance premiums, providing the largest share of income from insurance operations; the compensation share of losses on the risks transferred in reinsurance, as well as at the expense of the commission; and brokerage fee when the insurer plays the role of intermediary providing insurance services) D;

- (2)

variable costs of insurance companies Cvar;

- (3)

marginal revenue MR;

- (4)

fixed costs of the insurance company Cfix;

- (5)

profit P.

The increased marginal revenue is very important for managerial decision-making based on the cost value of insurance services. For example, if the company would have to make a decision about additional investment not at the end of the reporting period (before the submission of financial statements for external users of the information), as before, then marginal revenue can help in making operational management decisions.

It can be used to observe how the amount of profit in the interim report for internal use is changing. Information becomes transparent, and the marginal revenue shows the profit on a specific date at the specified number of contracts. In this situation, one can take managerial decisions on changing the volume of variable costs or adjusting the amount of fixed costs of insurance companies, and to calculate the economic effect of the investment project.

Insurance companies need to provide parameters such as a source of financing risk management and usage of funds.

The necessary information about the amount and mechanism of funding insurance companies, as well as the results of their use, can be systematized in this way:

- (1)

operational information;

- (2)

financial account information;

- (3)

accounting information for management purposes.

It is believed (

Dmitrieva 2006) that in Russia, two-thirds of the total volume of economic information is represented by the accounting data. These accounting and planning data are used to assess the results of management decisions.

Firstly, as noted by some researchers, an accountant, by the nature of his/her activities, plays an important role in the solution of many issues in the managerial and business activity of an organization.

Secondly, he/she prepares the information about the course of business needed for the moment; in many cases, accounting is the only source of information needed by the management of an organization.

Focusing the managers’ attention on the information that suits their specific purpose is not always achieved in the hierarchical model of grouping funds in the account that assumes a rigid division of information in a specific sequence. To receive from the totality of the information the data that is needed in the query result, that is, valuable (useful) information, the correlation model of building account items is needed (

Anosova et al. 2008).

Practice shows that the need to build multi-stage hierarchical structures of analytical accounting is long overdue. For example, in the information marketing field, there is a possibility to obtain information about payments under insurance contracts of various degrees of severity of loss in the case of applying analytical accounting of payments.

Accounting in insurance companies has a number of specific features, due to the nature of the insurance business (direct insurance, reinsurance, and retrocession), as well as special reserve funds that serve this activity. Actuarial calculations should provide some features associated with the practice of the insurance business. The most important of them are the following:

events under evaluation are probabilistic in nature and can be measured either with the use of probability theory or by gaming simulation (

Kopoteva and Zatonsky 2014). The last method, as highlighted by many researchers (e.g.,

Du and Jia 2017), is more effective in the absence of reliable statistical characteristics of the behavior of customers. The probabilistic or fuzzy nature of the activities is reflected in the value presented for payment of insurance premiums;

in some years, the general pattern of the phenomenon is manifested through a mass of separate random events, the existence of which suggests significant variations in insurance claims;

calculation of the cost value of the services provided by the insurer is made in respect of the entire insurance population;

it is necessary to allocate special reserves that are at the insurer’s disposal, in order to determine the optimal size of these reserves;

it is necessary to predict the reversal of insurance contracts, and expert assessment of their value is required;

it is necessary to study the rate of interest on loans and trends in a specific time interval;

the presence of full or partial damage associated with the insured accident determines the need to measure its distribution in time and space using special tables;

observance of the principle of equivalence, that is, the establishment of a proper balance between the payments of the policyholder, expressed using the insurance amount, and insurance coverage provided by the insurance company at the expense of the insurance payments received;

determining the risk group in the framework of this insurance population (

Gvozdenko 2004).

In the arsenal of insurance accounting, there are a significant number of specialized primary documents, such as the following:

insurance contract;

insurance policy;

receipts of the form A-7;

insurance act;

application for insurance;

questionnaire of pre-insurance expertise;

notification about the insured accident;

slip;

addendum;

bordereau;

account in reinsurance;

general agreement on the general conditions of facultative (obligatory) reinsurance;

journal of concluded insurance contracts;

journal of the accrued (paid) insurance premiums;

register of agency fees;

journal of reported (paid) losses;

journal of the amount of risks transferred to reinsurance;

journal of settlements with the reinsurers for reinsurance premiums, and so on.

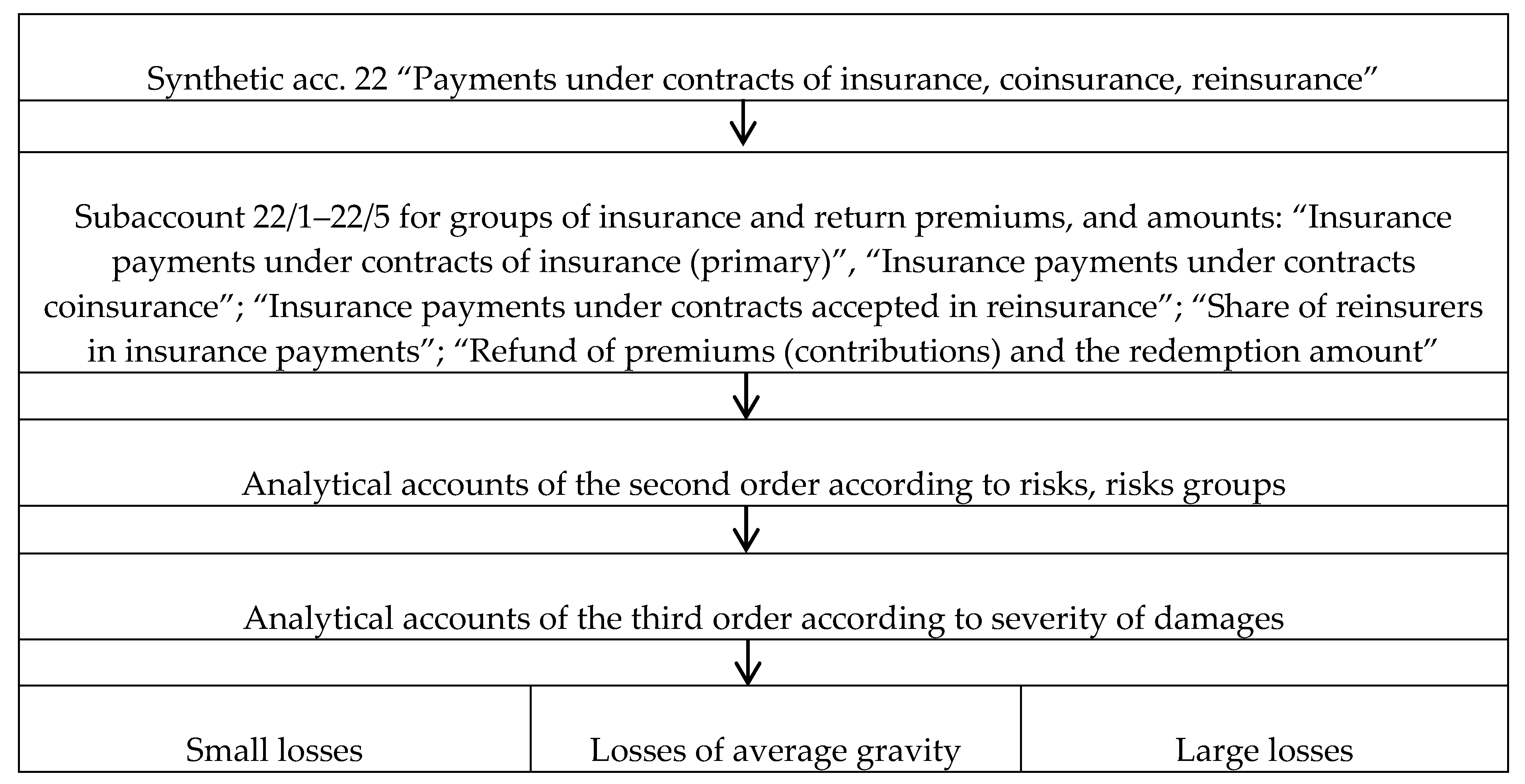

Based on the grouped data of these primary documents, one can create a range of objects of analytical accounting of insurance payments, which is non-uniform in terms of the severity of the loss (

Figure 4).

For a leader, it is important to determine the amount of risk (negligible, small, medium, large, catastrophic risk). Risk perception is largely dependent on the availability of the information base to evaluate the statistical base and financial capacity for compensation. With the help of actuarial calculations, the mathematical probability of the occurrence of the insured accident is calculated, the frequency and severity of consequences of damage are determined, both in certain risk groups and for the entire set of insurance objects. However, in accounting, the severity of the loss is not reflected, which complicates comprehensive analysis and disclosure of the causes of economic, financial, and organizational successes or shortcomings in the insurer’s activities.

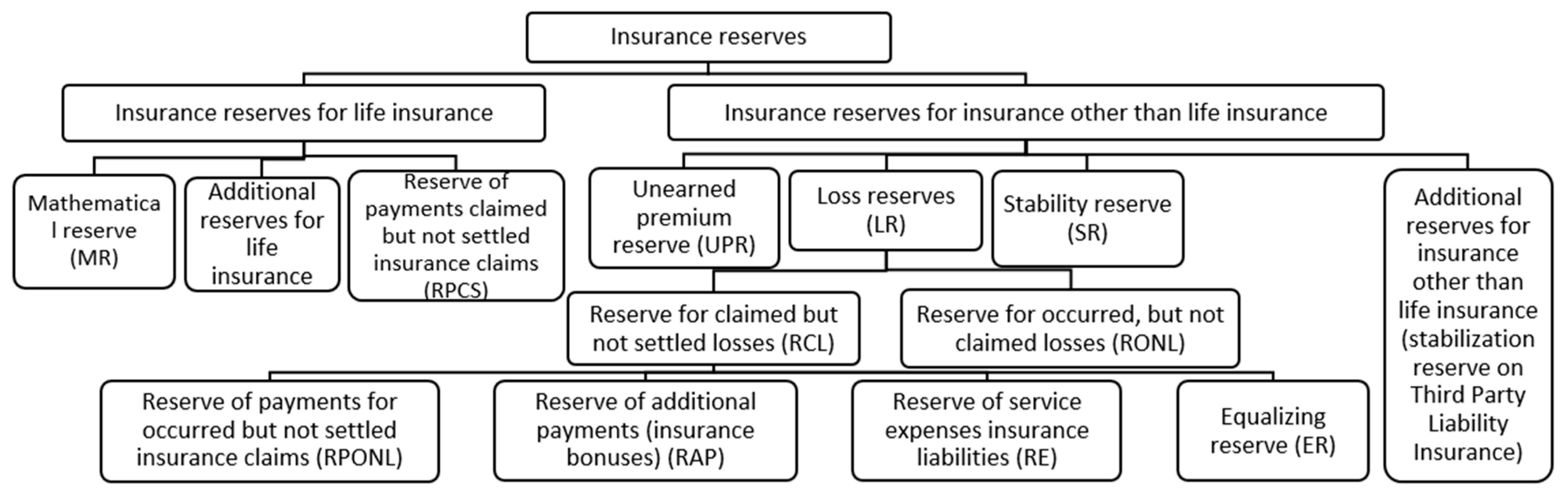

The main function of an insurance company, related to the fulfillment of obligations associated with insurance payments, is realized through insurance reserves. Insurance reserves are calculated for any date.

They are divided into reserves for life insurance and reserves for risky types of insurance (insurance types other than life insurance) (

Figure 5).

The need to establish insurance reserves is the result of the nature of the probability of occurrence of the insured event, the uncertainty of its occurrence, and the extent of damage.

The division of insurance reserves, presented in

Figure 5, is caused by the distinctive features of the content, functions, and tasks of insurance coverage, as well as the risk profile and the methodology for calculating tariffs. The sources of formation of almost all types of insurance reserves are insurance premiums, except for the stabilization reserve, where the source is the own funds of the company. The mathematical and stabilization reserves, as well as the unearned premium reserve, are associated with future payment liabilities. Reserves payments for claimed but not settled insurance claims (RPCS) and loss reserves (LR) are associated with current payment liabilities. The types of risks linked to insurance reserves are presented in

Table 4.

The mathematical reserve corresponds to the valuation of liabilities, which arise in connection with the occurrence of insured accidents of the insurance company.

By its purpose, the mathematical reserve is similar to the unearned premium reserve, although the methods of its estimation are more complicated.

The volume of insurance premium, the liability for which is transferred to the accounting period, is called the earned premium. The earned premium is the income of the insurance company and is directed to the repayment of losses under other insurance contracts, the costs of doing business, and the formation of loss reserves; it can also be used at the discretion of the insurer for its needs. The insurance premium that corresponds to the liability and passes to the next period is called the unearned premium.

In this regard, an important task of management accounting is to develop an acceptable method for practical use grouping of costs to improve the quality of determining the degree of risk, to develop of a system of accounts for grouping the necessary information, and to reflect the obtained information in effective (from the point of view of the communication process) reporting forms.

The managers of responsibility centers need information about the activities of subordinate units. In addition to historical information about costs and revenue, managers need information about the planned future costs and income. However, to increase the profitability of the insurance organization, more information on the insured company is required. For this, risk accounting according to the severity of damages is proposed. A similar approach was also used in (

Gomes-Gonçalves et al. 2015), where the authors use the statistical characteristics of the gravity of losses as the basis of methods for estimating the risk entropy. However, the authors of this article believe that the statistical distribution of losses is subject to Poisson’s law, that is, smaller losses occur far more often than large ones, which is not always the case. For example, it is obvious that when the legislation establishes the maximum amount of payments (as in the case of compulsory third party liability insurance in Russia), Poisson’s smooth distribution (or exponential, or any other monotonically changing distribution) will be violated.

Currently, the relation between the segments of activity and responsibility centers is not completely theoretically defined. To overcome this problem, the authors propose to differentiate the responsibility centers in enterprises so as to better control the safety of the insured property, which will contribute to the increase in the assets of both the insured company and the insurance organization. To do this, the authors propose the “intracompany ledger of the connection between the segments of activity and responsibility centers” (see the form in

Table 5), which contains the value indicators for the insured property, and identifies the responsible persons as well as preventative measures to avoid the insured event.

Risk assessment and control in the context of the severity of potential losses and determination of persons responsible for the safety of the property and preventive measures will reduce the probability of occurrence of the insured accident or at least reduce the severity of loss. This measure is especially effective in the event of significant external influences. For example, in (

Sønderstrup-Andersen and Bach 2017), the authors come to this conclusion based on the analysis of the impact of the 2008 crisis on businesses and the resulting changes in terms of safety in the workplace, which is directly related to the insurance of employees. In Russia, such a measure is even more effective as the economy is influenced not only by global crises, but also by specific events of recent years, which have caused the international sanctions against government officials and separate large enterprises.

Accounting of activity segments is a system that measures (estimates) the plans and actions of each responsibility center, and the main source of information in this system is the intracompany ledger of the connection between segments of activity and responsibility centers, developed by the author. This ledger is of practical value for insurance organizations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}