Stock Market Volatility and Trading Volume: A Special Case in Hong Kong With Stock Connect Turnover

Abstract

1. Introduction

2. Methodology

2.1. Volatility Measure

2.2. Classification of Stock Connect Volume

2.3. Vector Autoregressive Framework and Granger Causality Test

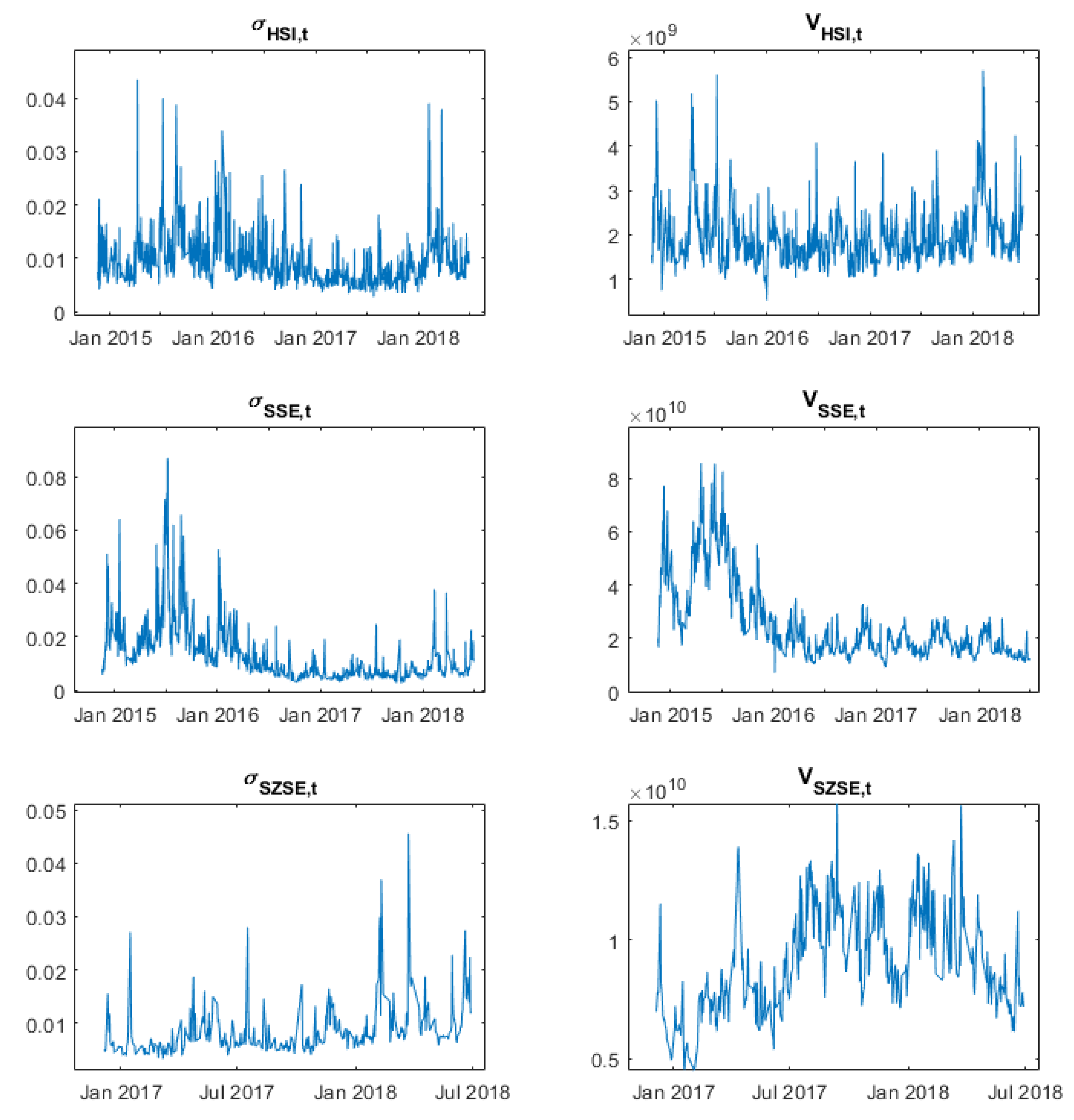

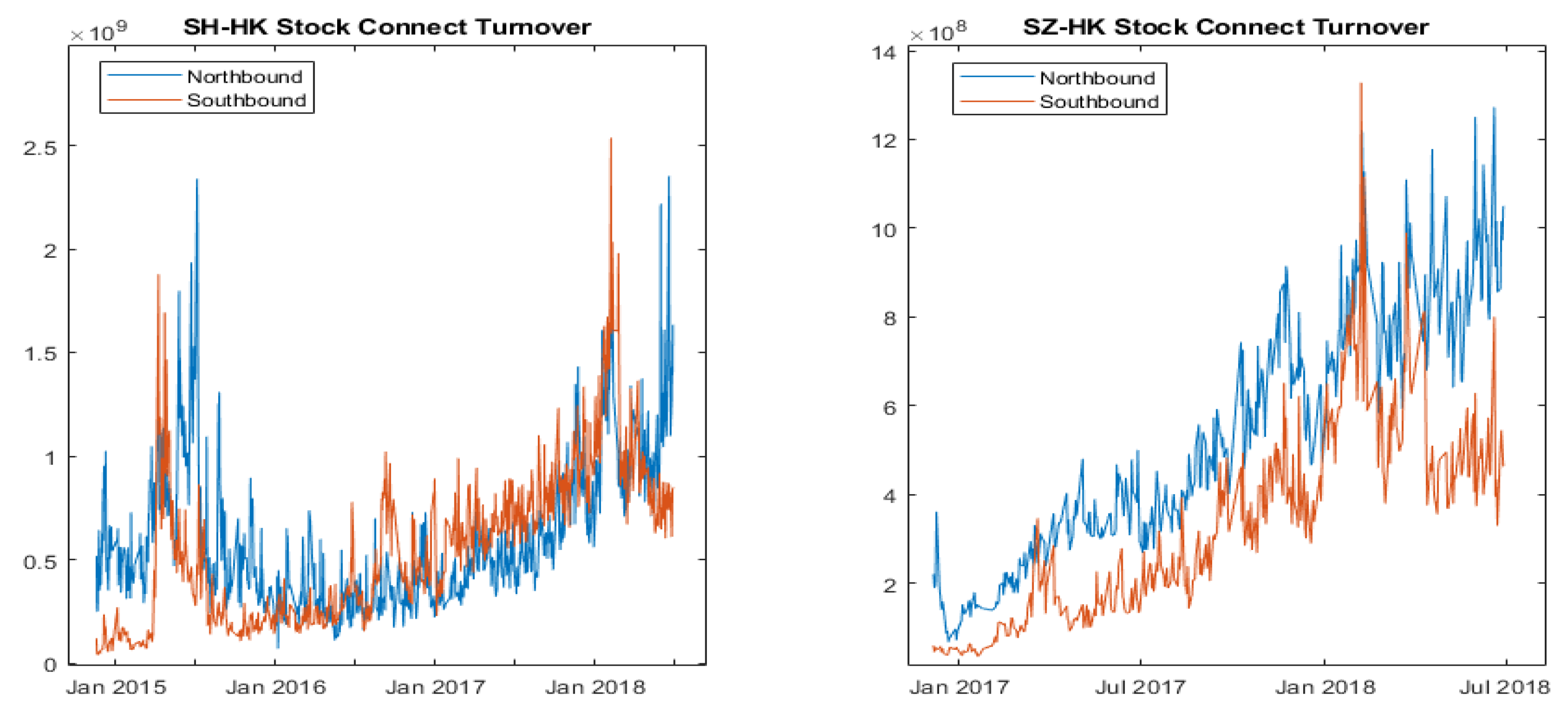

3. Data Description

3.1. Data Transformation

3.2. Data Summary

4. Empirical Findings and Discussion

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

References

- Andersen, Torben G., Tim Bollerslev, Francis X. Diebold, and Paul Labys. 2003. Modeling and forecasting realized volatility. Econometrica 71: 579–625. [Google Scholar] [CrossRef]

- Barndorff-Nielsen, Ole E., and Neil Shephard. 2002. Econometric analysis of realized volatility and its use in estimating stochastic volatility models. Journal of the Royal Statistical Society Series B Part 2 64: 253–80. [Google Scholar] [CrossRef]

- Burdekin, Richard C.K., and Pierre L. Siklos. 2018. Quantifying the impact of the November 2014 Shanghai-Hong Kong stock connect. International Review of Economics and Finance 57: 156–163. [Google Scholar] [CrossRef]

- Chen, Gong-meng, Michael Firth, and Oliver M. Rui. 2001. The dynamic relation between stock returns, trading volume, and volatility. Financial Review 36: 153–74. [Google Scholar] [CrossRef]

- Chiang, Thomas C., Zhuo Qiao, and Wing-Keung Wong. 2010. New evidence on the relation between return volatility and trading volume. Journal of Forecasting 29: 502–15. [Google Scholar] [CrossRef]

- Clark, Peter K. 1973. A subordinated stochastic process model with finite variance for speculative prices. Econometrica 41: 135–55. [Google Scholar] [CrossRef]

- Darrat, Ali F., Shafiqur Rahman, and Maosen Zhong. 2003. Intraday trading volume and return volatility of the DJIA stocks. Journal of Banking and Finance 27: 2035–43. [Google Scholar] [CrossRef]

- De Medeiros, Otavio Ribeiro, and Bernardus Ferdinandus Nazar Van Doornik. 2006. The Empirical Relationship Between Stock Returns, Return Volatility and Trading Volume in the Brazilian Stock Market. Available online: https://ssrn.com/abstract=897340 (accessed on 8 August 2018).

- Dickey, David A., and Wayne A. Fuller. 1979. Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association 74: 427–31. [Google Scholar] [CrossRef]

- Economics, Thomas E. Copeland. 1976. A model of asset trading under the assumption of sequential information arrival. Journal of Finance 31: 1149–68. [Google Scholar] [CrossRef]

- Gallant, A. Ronald, Peter E. Rossi, and George Tauchen. 1992. Stock prices and volume. The Review of Financial Studies 5: 199–242. [Google Scholar] [CrossRef]

- Hong Kong Exchanges and Clearing Limited. 2008. Stock Connect Another Milestone Information Book for Market Participants. Available online: http://www.hkex.com.hk/-/media/HKEX-Market/Mutual-Market/Stock-Connect/Getting-Started/Information-Booklet-and-FAQ/Information-Book-for-Market-Participants/EP_CP_Book_En_(13July18).pdf (accessed on 8 August 2018).

- Hui, Eddie C.M., and Ka Kwan Kevin Chan. 2018. Does the Shanghai–Hong Kong Stock Connect significantly affect the AH premium of the stocks? Physica A: Statistical Mechanics and its Applications 492: 207–14. [Google Scholar] [CrossRef]

- Huo, Rui, and Abdullahi D. Ahmed. 2017. Return and volatility spillovers effects: Evaluating the impact of Shanghai-Hong Kong Stock Connect. Economic Modelling 61: 260–72. [Google Scholar] [CrossRef]

- Jennings, Robert H., Laura T. Starks, and John C. Fellingham. 1981. An equilibrium model of asset trading with sequential information arrival. Journal of Finance 36: 143–61. [Google Scholar] [CrossRef]

- Lee, Bong-Soo, and Oliver M. Rui. 2002. The dynamic relationship between stock returns and trading volume: Domestic and cross-country evidence. Journal of Banking and Finance 26: 51–78. [Google Scholar] [CrossRef]

- Mestel, Roland, Henryk Gurgul, and Paweł Majdosz. 2003. The Empirical Relationship Between Stock Returns, Return Volatility and Trading Volume on the Austrian Stock Market. Styria, Austria: University of Graz, Institute of Banking and Finance, Research Paper. [Google Scholar]

- Schwarz, Gideon. 1978. Estimating the dimension of a model. The Annals of Statistics 6: 461–64. [Google Scholar] [CrossRef]

- Wang, Hanfeng. 2004. Dynamic Volume-Volatility Relation. Available online: http://ssrn.com/abstract=603841 (accessed on 8 August 2018).

- Wang, Qiyu, and Terence Tai-Leung Chong. 2018. Co-integrated or not? After the Shanghai–Hong Kong and Shenzhen–Hong Kong Stock Connection Schemes. Economics Letters 163: 167–71. [Google Scholar] [CrossRef]

- Wang, Yang-Chao, Jui-Jung Tsai, and Qiaoqiao Li. 2017. Policy impact on the Chinese stock market: From the 1994 bailout policies to the 2015 Shanghai-Hong Kong stock connect. International Journal of Financial Studies 5: 4. [Google Scholar] [CrossRef]

- Wu, Tingting, and Xiaoying Gao. 2015. Factors of Price Difference between A-Shares and H-Shares under SH-HK Stock Connect. Paper presented at Proceedings of the International Conference on Transnational Corporations and Emerging Markets, Wuhan, October 29–31. [Google Scholar]

| 1. | There are two exceptional cases which are volatility of Shenzhen market in northbound of SZ-HK equation and second lagged term of market volume of Shanghai market in Northbound SH-HK equation. Both are rejected at 5% significance level. |

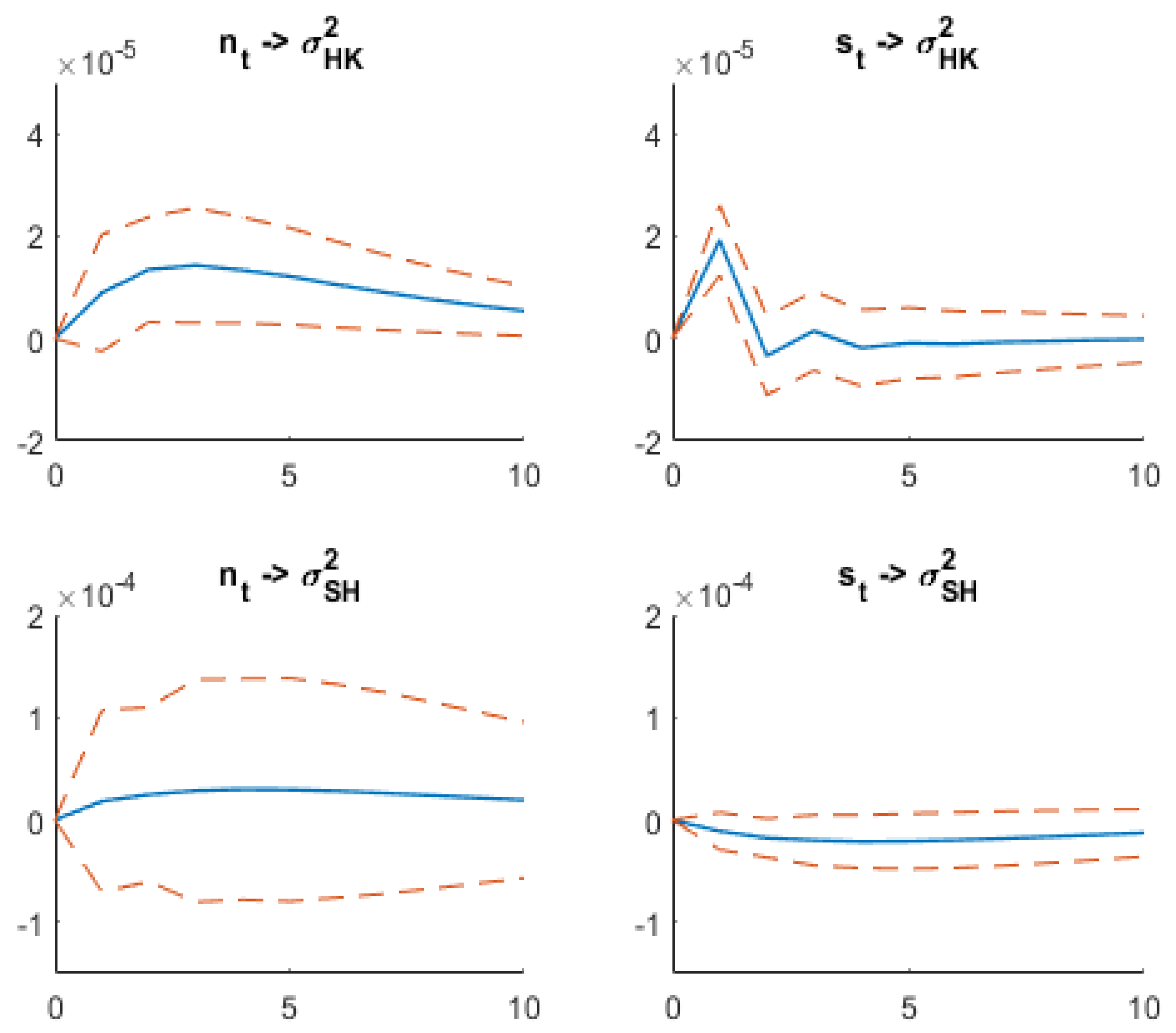

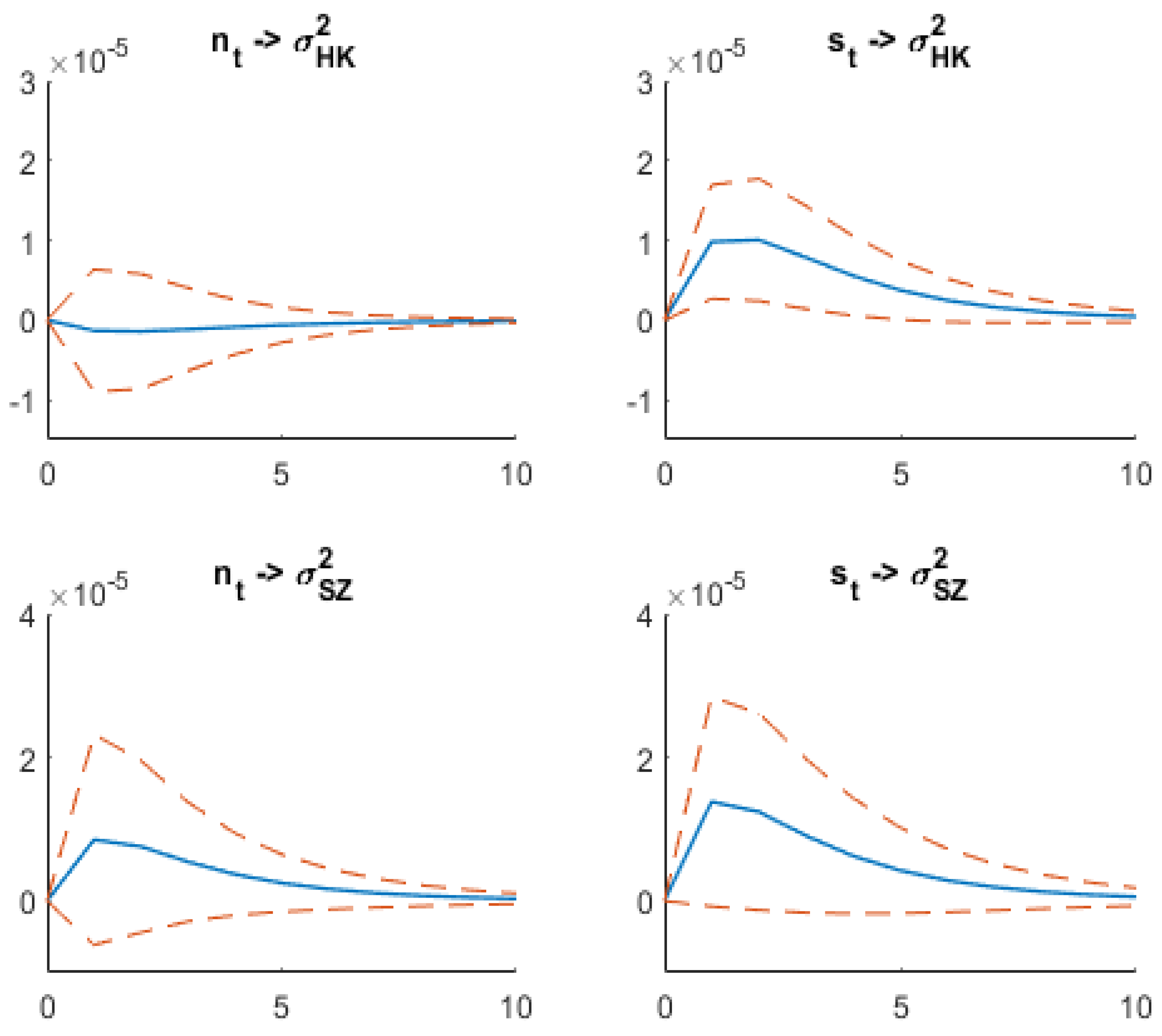

| 2. | The Impulse responses are computed using a Cholesky orthogonalization. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | Definition |

|---|---|

| Total volume of Shanghai Stock Exchange Composite Index | |

| Total volume of Shenzhen Stock Exchange Component Index | |

| Total volume of Hong Kong Hang Seng Index | |

| Total turnover of Northbound via SH-HK stock connect | |

| Total turnover of Southbound via SH-HK stock connect | |

| Total turnover of Northbound via SZ-HK stock connect | |

| Total turnover of Southbound via SZ-HK stock connect |

| (a) SH-HK Stock Connect | |

| Stock market | Vector of endogenous variables |

| Hong Kong | |

| Shanghai | |

| (b) SZ-HK Stock Connect | |

| Stock market | Vector of endogenous variables |

| Hong Kong | |

| Shanghai | |

| (a) Panel A: Volume Series Regression | |||||||

| SSE | SZSE | HSI | SH-HK Northbound | SH-HK Southbound | SZ-HK Northbound | SZ-HK Southbound | |

| 2.064 | 0.586 | 1.206 | 1.499 | 0.524 | 0.198 | −0.065 | |

| (49.484) ** | (19.499) ** | (34.047) ** | (32.608) ** | (10.701) ** | (6.175) ** | (−1.095) | |

| −4.625 | 5.433 | −1.629 | −5.287 | −4.824 | 4.249 | 7.391 | |

| (−19.423) ** | (13.752) ** | (−8.055) ** | (−20.143) ** | (−1.725) | (10.070) ** | (9.526) ** | |

| 3.70 | −1.31 | 2.08 | 7.52 | 3.08 | 1.37 | −5.67 | |

| (12.981) * | (−12.061) ** | (8.576) * | (23.932) * | (9.197) * | (1.181) | (−2.648) ** | |

| 0.534 | 0.382 | 0.085 | 0.472 | 0.531 | 0.854 | 0.694 | |

| (b) Panel B: Unit Root Test | |||||||

| SSE | SZSE | HSI | SH-HK Northbound | SH-HK Southbound | SZ-HK Northbound | SZ-HK Southbound | |

| RV | |||||||

| 2 | 2 | 3 | |||||

| −6.389 ** | −5.235 ** | −6.743 ** | |||||

| Detrended volume | |||||||

| 3 | 5 | 2 | 3 | 3 | 4 | 3 | |

| −5.556 ** | −4.884 ** | −9.460 ** | −6.966 ** | −5.262 ** | −5.064 ** | −3.680 ** | |

| SSE | SZSE | HSI | SH-HK Northbound | SH-HK Southbound | SZ-HK Northbound | SZ-HK Southbound | |

|---|---|---|---|---|---|---|---|

| RV: | |||||||

| Mean | 2.862 | 9.508 | 1.175 | ||||

| Median | 7.807 | 5.154 | 6.724 | ||||

| Maximum | 7.575 | 2.073 | 1.892 | ||||

| Minimum | 6.614 | 1.093 | 7.528 | ||||

| SD | 6.328 | 1.682 | 1.760 | ||||

| Skewness | 5.532 | 7.032 | 5.256 | ||||

| Kurtosis | 43.524 | 68.568 | 39.199 | ||||

| Observation | 808 | 350 | 808 | ||||

| Raw trading Volume: | |||||||

| Mean | 2.536 | 9.056 | 1.945 | 5.897 | 5.423 | 5.321 | 3.284 |

| Median | 1.984 | 8.705 | 1.782 | 4.855 | 4.864 | 4.844 | 3.001 |

| Maximum | 8.571 | 1.573 | 5.702 | 2.352 | 2.536 | 1.273 | 1.327 |

| Minimum | 7.057 | 4.514 | 5.260 | 6.887 | 3.965 | 6.746 | 3.502 |

| SD | 1.463 | 2.139 | 6.800 | 3.523 | 3.661 | 2.758 | 2.164 |

| Skewness | 1.654 | 0.392 | 1.851 | 1.533 | 1.042 | 0.364 | 0.852 |

| Kurtosis | 5.171 | 2.613 | 8.028 | 6.046 | 4.721 | 2.205 | 3.936 |

| Observation | 808 | 350 | 808 | 808 | 808 | 350 | 350 |

| (a) SH-HK Stock Connect Correlation Matrix | ||||||

| 1 | ||||||

| 0.460 | 1 | |||||

| 0.528 | 0.200 | 1 | ||||

| 0.369 | 0.514 | 0.318 | 1 | |||

| n | 0.326 | 0.250 | 0.307 | 0.548 | 1 | |

| s | −0.170 | 0.094 | −0.159 | 0.421 | 0.565 | 1 |

| (b) SZ-HK Stock Connect Correlation Matrix | ||||||

| 1 | ||||||

| 0.749 | 1 | |||||

| 0.250 | 0.250 | 1 | ||||

| 0.411 | 0.525 | 0.305 | 1 | |||

| n | 0.386 | 0.382 | 0.421 | 0.441 | 1 | |

| s | 0.410 | 0.513 | 0.491 | 0.578 | 0.874 | 1 |

| (a) Panel A: Stock Connect turnover against Market RV and Market Volume | |||

| Hypothesis | Comments | Optimal Lag | Wald Statistics |

| SH Stock Connect | |||

| SSE | |||

| , | 2 | 6.683 (0.035) ** | |

| , | 2 | 9.466 (0.009) *** | |

| HSI | |||

| , | 2 | 27.910 (0.000) *** | |

| , | 2 | 22.179 (0.000) *** | |

| SZ Stock Connect | |||

| SZSE | |||

| , | 1 | 6.196 (0.013) ** | |

| , | 1 | 12.775 (0.000) *** | |

| HSI | |||

| , | 1 | 3.110 (0.078) * | |

| , | 1 | 6.449 (0.011) ** | |

| (b) Panel B: Market RV and Market Volume against Stock Connect turnover | |||

| Hypothesis | Comments | Optimal Lag | Wald Statistics |

| SH Stock Connect | |||

| SSE | |||

| 2 | 2.539 (0.281) | ||

| 2 | 5.055 (0.080) * | ||

| 2 | 0.018 (0.991) | ||

| 2 | 5.618 (0.060) * | ||

| HSI | |||

| 2 | 0.314 (0.855) | ||

| 2 | 5.778 (0.056) * | ||

| 2 | 6.045 (0.049) ** | ||

| 2 | 0.373 (0.830) | ||

| SZ Stock Connect | |||

| SZSE | |||

| 1 | 0.449 (0.503) | ||

| 1 | 0.425 (0.514) | ||

| 1 | 6.549 (0.010)** | ||

| 1 | 0.144 (0.704) | ||

| HSI | |||

| 1 | 0.269 (0.604) | ||

| 1 | 0.229 (0.632) | ||

| 1 | 1.129 (0.288) | ||

| 1 | 0.097 (0.755) | ||

| (a) Panel A: Summary results of SH-HK Connect | |||||||||||

| RV | Volume | Northbound | Southbound | ||||||||

| Market | SSE | HSI | SSE | HSI | SSE | HSI | SSE | HSI | |||

| 0.289 | 0.588 | 0.012 | 0.005 | −0.004 | 0.016 | 0.001 | 0.046 | ||||

| (4.540) *** | (8.870) *** | (0.557) | (0.121) | (−0.138) | (0.490) | (0.045) | (1.699) * | ||||

| 0.430 | 0.252 | −0.011 | −0.020 | 0.025 | −0.001 | 0.000 | −0.019 | ||||

| (11.855) *** | (6.317) *** | (−0.909) | (−0.873) | (1.590) | (−0.039) | (0.038) | (−1.175) | ||||

| 0.282 | 0.162 | 0.004 | 0.018 | −0.016 | −0.010 | −0.002 | −0.027 | ||||

| (7.794) *** | (4.052) *** | (0.327) | (0.787) | (−1.041) | (−0.514) | (−0.127) | (−1.646) | ||||

| 0.076 | 0.045 | 0.681 | 0.467 | 0.093 | 0.012 | −0.029 | −0.003 | ||||

| (0.605) | (0.580) | (16.629) *** | (10.472) *** | (1.735) * | (0.313) | (−0.646) | (−0.086) | ||||

| 0.040 | −0.036 | 0.162 | 0.077 | −0.026 | −0.083 | 0.085 | 0.018 | ||||

| (0.324) | (−0.475) | (4.006) *** | (1.736) * | (−0.485) | (−2.204) ** | (1.915) * | (0.563) | ||||

| 0.132 | 0.089 | −0.033 | 0.031 | 0.484 | 0.535 | −0.008 | −0.001 | ||||

| (1.324) | (1.126) | (−1.009) | (0.665) | (11.363) *** | (13.832) *** | (−0.215) | (−0.030) | ||||

| 0.064 | 0.131 | 0.060 | 0.050 | 0.241 | 0.270 | 0.014 | 0.053 | ||||

| (0.642) | (1.652) * | (1.824) * | (1.076) | (5.666) *** | (6.945) *** | (0.385) | (1.642) | ||||

| −0.073 | 0.325 | 0.074 | 0.061 | 0.035 | 0.035 | 0.640 | 0.643 | ||||

| (−0.719) | (3.530) *** | (2.210) ** | (1.134) | (0.809) | (0.774) | (17.538) *** | (17.053) *** | ||||

| −0.050 | −0.353 | −0.035 | 0.065 | −0.011 | 0.030 | 0.193 | 0.206 | ||||

| (−0.486) | (−3.832) *** | (−1.047) | (1.209) | (−0.260) | (0.671) | (5.264) *** | (5.466) *** | ||||

| 0.511 | 0.191 | 0.738 | 0.386 | 0.563 | 0.563 | 0.695 | 0.695 | ||||

| (b) Panel B: Summary results of SZ-HK Connect | |||||||||||

| RV | Volume | Northbound | Southbound | ||||||||

| Market | SZSE | HSI | SZSE | HSI | SZSE | HSI | SZSE | HSI | |||

| 0.778 | 0.606 | 0.093 | 0.006 | 0.017 | −0.019 | 0.062 | 0.026 | ||||

| (7.177) *** | (5.774) *** | (1.866) * | (0.118) | (0.313) | (−0.345) | (1.299) | (0.520) | ||||

| 0.224 | 0.391 | −0.098 | −0.005 | −0.020 | 0.017 | −0.067 | −0.030 | ||||

| (3.795) *** | (6.490) *** | (−3.593) *** | (−0.151) | (−0.670) | (0.518) | (−2.559) ** | (−1.063) | ||||

| −0.159 | −0.077 | 0.632 | 0.530 | −0.033 | 0.029 | −0.017 | 0.017 | ||||

| (−1.576) | (−0.670) | (13.579) *** | (9.220) *** | (−0.652) | (0.478) | (−0.380) | (0.311) | ||||

| 0.058 | −0.067 | −0.158 | −0.075 | 0.452 | 0.424 | −0.058 | −0.094 | ||||

| (0.511) | (−0.646) | (−3.013) *** | (−1.449) | (7.934) *** | (7.697) *** | (−1.167) | (−1.928) * | ||||

| 0.232 | 0.221 | 0.151 | 0.152 | 0.165 | 0.118 | 0.737 | 0.722 | ||||

| (2.071) ** | (1.756) * | (2.907) *** | (2.409) ** | (2.922) *** | (1.765) * | (14.877) *** | (12.197) *** | ||||

| 0.078 | 0.179 | 0.383 | 0.350 | 0.271 | 0.270 | 0.437 | 0.427 | ||||

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chan, B.S.F.; Cheng, A.C.H.; Ma, A.K.C. Stock Market Volatility and Trading Volume: A Special Case in Hong Kong With Stock Connect Turnover. J. Risk Financial Manag. 2018, 11, 76. https://doi.org/10.3390/jrfm11040076

Chan BSF, Cheng ACH, Ma AKC. Stock Market Volatility and Trading Volume: A Special Case in Hong Kong With Stock Connect Turnover. Journal of Risk and Financial Management. 2018; 11(4):76. https://doi.org/10.3390/jrfm11040076

Chicago/Turabian StyleChan, Brian Sing Fan, Andy Cheuk Hin Cheng, and Alfred Ka Chun Ma. 2018. "Stock Market Volatility and Trading Volume: A Special Case in Hong Kong With Stock Connect Turnover" Journal of Risk and Financial Management 11, no. 4: 76. https://doi.org/10.3390/jrfm11040076

APA StyleChan, B. S. F., Cheng, A. C. H., & Ma, A. K. C. (2018). Stock Market Volatility and Trading Volume: A Special Case in Hong Kong With Stock Connect Turnover. Journal of Risk and Financial Management, 11(4), 76. https://doi.org/10.3390/jrfm11040076