1. Introduction

Over the decades, food insecurity concerns have been emerging, along with the growth of the world population. Among the United Nations Sustainable Development Goals [

1] to be achieved by 2030, ending hunger and establishing food security hold an important place. However, despite the best efforts of the international community to combat food insecurity across the globe, the number of undernourished people has resumed growth in 2015, after a steady decline during the 1990–2000s. The Food and Agriculture Organization (FAO) reports that over 820 million people in the world suffer from hunger, while about two billion people experience moderate or severe food insecurity [

2]. In view of the fact that an additional 60 million people have become affected by hunger since 2014, the number of undernourished people is projected to exceed 840 million by 2030 [

3]. In the past, the main reasons for food shortages used to be droughts and other natural disasters. With the emergence of globalization, food security has become an economic rather than an agricultural issue. Being a combination of the physical availability of food and economic access to adequate supply [

4], food security at the national level is increasingly influenced by international exchange, foreign trade policies, and macroeconomic parameters of the global food market.

Most recently, the global food supply system has encountered one of the most vigorous pressure tests ever due to the outbreak of COVID-19. Vos et al. [

5] emphasize the difference between the new pandemic and many of the previous ones. While, for example, Severe Acute Respiratory Syndrome (SARS), Middle East Respiratory Syndrome (MERS), and avian flu led to food shortages in affected areas causing direct damage to livestock sectors, the COVID-19 outbreak in just a few months has emerged into one of the greatest global health challenges. By the end of June 2020, 188 countries had reported cases of COVID-19 [

6]. In the first two quarters of 2020, more than 11 million cases of infection and more than 530 thousand deaths had been confirmed [

6]. The outbreak has turned out to be an economic challenge. While in past years, the FAO recognized military conflicts and climate extremes as main threats to food security, the 2020 report emphasized that pandemic-related economic slowdowns and downturns undermined efforts to end hunger worldwide [

3]. The pandemic is not only impacting people’s lives but is disrupting food supply chains [

7,

8,

9]. As the virus spreads and public health protection measures tighten, there are many ways in which the global food system has been strained (border closures, quarantines, supply chain disruptions, etc.). Welsh [

10] explains that the pandemic is affecting food systems directly by distorting supply and demand internationally, and indirectly by degrading the purchasing power of the population and by undermining the capacity to produce and distribute food. Devereux et al. [

11], Bakalis et al. [

12], and Farrell et al. [

13] also emphasize the two-faced nature of direct (disrupted food systems) and indirect (undermined economic access to food) effects of COVID-19 on food security. According to the United Nations World Food Program (WFP) [

14], the economic impact of the pandemic could result in doubling the number of people suffering acute hunger by the end of 2020. The FAO estimates that the COVID-19 pandemic may add 83–132 million people to the number of the undernourished in 2020 [

3].

For several years now, global trade systems have been increasingly distorted by various protectionist measures and trade restrictions. Commonly, governments seek to make their countries self-sufficient in food by protecting domestic food producers. In many developing and least developed countries (LDCs), export bans have been introduced to curb food inflation and establish reserves of staple foods. The World Trade Organization (WTO) [

15] reports that since the start of the pandemic, Kyrgyzstan, North Macedonia, Ukraine, Thailand, and Egypt notified export prohibitions on various food and agricultural products and specifically attributed those measures to COVID-19. Russia, the world’s largest wheat exporter, and Vietnam, the third-largest rice exporter, introduced temporary export-restrictive measures. The pandemic has aggravated US–China trade tensions, in which tariffs on food trade have been intensively used as a tool of economic pressure. Most countries have implemented higher customs controls on cargo vessels, with a particular risk to perishable foods and with the risk of jeopardizing shipping activities [

16]. There have been policy measures aimed at avoiding the spread of COVID-19 that might slow down food production and increase market prices globally (for instance, more stringent health standards in farms and food factories, restrictions on the movement of seasonal agricultural workers, shortage of fertilizers, veterinary medicines, and other input) [

16]. In total, at least two-thirds of countries have put in place a variety of protectionist measures [

15] that currently affect around 5% of globally traded food and agricultural products [

17].

As governments across the world impose food export restrictions and lockdowns, such responses to the emerging health threat could create extreme volatilities in the market, provoking food shortages and resulting in food crises. For instance, during the 2007–2008 global economic downturn, the doubling of world food prices was mainly attributed to trade restrictions imposed by the largest exporters of rice, wheat, and soybeans [

18,

19,

20,

21]. The actions aimed to avert national shortages in some countries contributed to breaking the logistics chains for staple foods in many national markets [

22]. Developing countries are particularly vulnerable to such distortions. In 2020, the WFP estimates the most substantial increase in the number of people suffering acute hunger to happen across LDCs in Sub-Saharan Africa and developing economies of the Middle East and Latin America [

14]. Most of these countries are net importers of food and agricultural products. According to the FAO [

2], out of 65 developing economies and LDCs where recent adverse impacts of the economic downturn due to the COVID-19 pandemic on food security have been strongest, 52 countries rely heavily on agricultural imports. In a situation of disrupting food supply, dependence on imports tremendously threatens the food security of those nations, especially when export restrictions are imposed by the world’s leading suppliers like Russia, Vietnam, and Ukraine. As the spread of COVID-19 and strict quarantine measures trigger economic decline, even developed economies experience food price rises unless the governments take preventive actions or retailers absorb some of the costs. Since February 2020, the global average price for rice has increased by 7.1%, for meat of cattle—by 7.0%, for meat of chicken—by 5.5%, for potatoes—by 8.3% [

23]. Due to a limited capacity to produce staple crops domestically, developing economies are more vulnerable to food inflation and supply shortages. In just the first three months of 2020 at the very onset of the COVID-19 outbreak, over fifteen developing countries already experienced an increase in the cost of a basket of food staples (over 10%) [

24]. At many markets, food prices have been increasing because of local logistical problems [

16]. There is also a dependence of developing countries with their limited resources on a small range of food products exported to a few markets [

25], many of which have been affected by the COVID-19 outbreak [

15]. In one of the trade scenarios simulated by Vos et al. [

5], a 1% global economic slowdown due to the pandemic could cause a decline in developing-country agri-food exports by almost 25%.

There is an array of studies that address trade aspects of food supply [

26,

27,

28,

29,

30], but the majority of them focus on food self-sufficiency rather than food security. According to the FAO [

31], a self-sufficient country satisfies its needs in food by means of domestic production. Although some developing countries of Africa (Mali and Senegal) and Latin America (Bolivia, Ecuador, and Venezuela) have embraced the idea of food self-sufficiency in their national policies [

32], progressing liberalization of food trade over the past few decades has refocused attention from self-sufficiency, a concept that is often related to protectionism and even autarky [

33], to food security. The latter incorporates a wider range of parameters of food availability, economic access to adequate nutrition, utilization of nutrients, and stability of food supply [

4]. While Wegren and Elvestad [

34], Meskhia [

35], Clapp [

36], and Saidi and Diouri [

37], among others, argue that food security is about establishing a balance between domestic production and imports, many studies categorize food security as agricultural [

38,

39], economic [

40,

41], or health [

42,

43,

44] issues rather than as a trade one.

However, at the height of the COVID-19 crisis, both larger demand gaps and higher food price surges suggest that international trade policies play a more pervasive role in ensuring food security at the national level than previously thought. Against the backdrop of the health crisis, an increase in the number of undernourished people is coupled with a global economic slowdown [

2]—a trilemma that has not been adequately explored in previous studies. Lockdowns, export restrictions, and quarantine measures exacerbate these problems and call for the investigation of trade and economic impacts on food security in a new reality of food chain disruptions. So far, empirical assessments of the pandemic’s effects on food and agriculture sectors have been grouped around international organizations, such as FAO (Food and Agriculture Organization of the United Nations), WHO (World Health Organization), WFP (World Food Programme), UNCTAD (United Nations Commission on Trade and Development), and IFPRI (International Food Policy Research Institute). In a collective study compiled by the UNCTAD’s Committee for the Coordination of Statistical Activities [

45], three dozen organizations and institutions identified the pandemic’s primary channels of transmission to food and agriculture sectors, and quantified the potential impacts of COVID-19 outbreak on agricultural input markets, food trade, and food consumption. Since the report covered a wide range of topics, it thus was not particularly focused on the analysis of trade-related aspects of food security. In the regional section of the report, the economic and trade impacts of COVID-19 on food security were not detailed for developing economies and LDCs. In the IFPRI study that particularly focused on developing countries, Vos et al. [

5] applied a general equilibrium model to assess possible impacts of the pandemic on prices, income, and poverty. The impacts of productivity declines on prices of some food products were forecasted, as well as on income of households, but the parameters of food availability and access to food and agricultural products were not addressed.

Similarly, trade impacts on food supply chains have remained scantily explored across the array of studies on COVID-19 that have emerged in 2020. Most of these recent papers have particularly emphasized the aspects of food safety [

46], agriculture productivity [

47,

48], and healthy nutrition [

49], rather than of food imports and trade balance as dimensions of food availability. The impacts of both international exchange fluctuations and food inflation on the access pillar of food security have also remained under investigated. The link between price increase and access to food has been primarily considered in terms of supply disruptions and shortages along the retail food supply chain [

50,

51], not currency exchange rates. To the best of the authors’ knowledge, there are no comprehensive studies that link the incidence rates of COVID-19 with either the number of undernourished people or the degree of dependency on food imports.

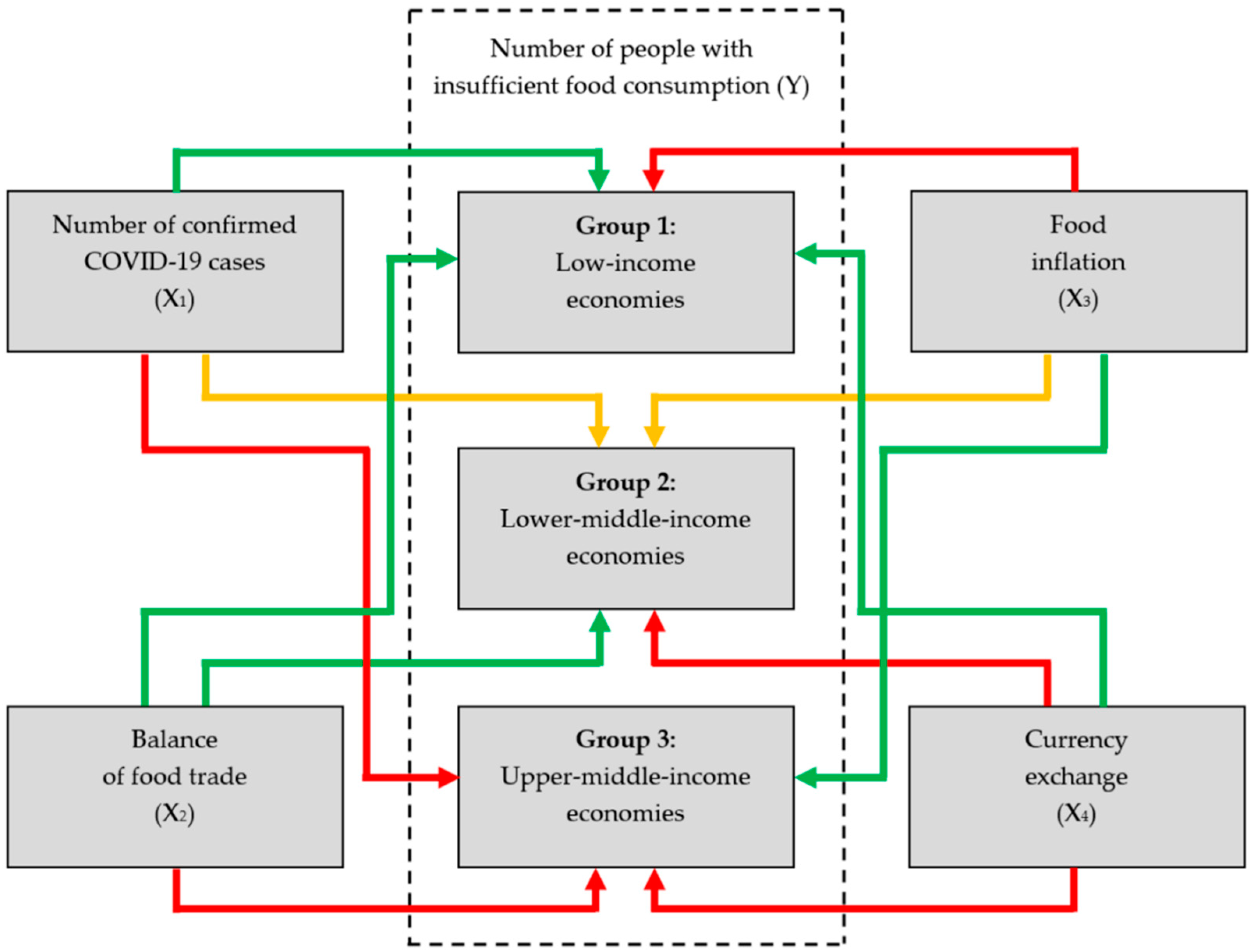

In this study, the authors attempt to bridge the said gaps in the “COVID-19–trade–food security” agenda by (1) identifying interactions between the number of COVID-19 cases on one side and availability and access pillars of food security on the other; (2) assessing the cointegration between the pandemic-induced trade parameters of food availability and the number of undernourished people; (3) revealing the impacts of food inflation and currency exchange volatilities amid the global health crisis on economic access to food in domestic markets; and (4) detailing the analysis of above-mentioned health, food security, trade, and economic parameters across an array of developing economies and LDCs.

3. Results

The results of the ADF and the PP tests across three groups of countries (see

Supplementary Materials to this paper, Tables S1–S3) demonstrate that all five variables are stationary at a level of either I(0) or I(1). In all cases, the calculated F-statistics values exceed the upper bound (

Table 4). It means that the precondition for co-integration between

Y and

X1–4 is established in all countries included in the study. The stationarity of the data series along with the revealed co-integration between the variables both confirm the appropriateness of the established data set for the ARDL analysis.

Since the study includes six periods (months), it is mainly centered on explaining the short-run relationship between the number of people with insufficient food consumption and independent variables. The ARDL short-run estimates for the three groups of countries are summarized in

Table 5, the detailed per-country calculations are provided in

Supplementary Materials (Tables S4–S6).

In Group 1 countries, the strongest effect on the growth of Y is caused by an increase in food inflation X3. This effect is statistically significant across the group. Some variables also exert strong direct influence on Y, for instance, X2 in Sierra Leone and Yemen and X4 in Haiti and Niger. When other factors remain constant, an increase in the number of registered COVID-19 cases by 1% results in the growth of Y by 0.14% in Tajikistan and by 0.05% in Mozambique and Sierra Leone. In Niger, a 0.18% increase in the number of people with insufficient food consumption is caused by a 5% rise in X1 (0.16% in Guinea, 0.14% in Tanzania, and 0.03% in Afghanistan).

In Group 2 countries, we see kaleidoscopic linkages between Y and X1. In Pakistan and India, the countries of South Asia which have been severely hit by the pandemic, an increase in COVID-19 cases by 1% results in the growth of the number of people with insufficient food consumption by 0.56% and 0.53%, respectively. In East Asia, on the contrary, we see that the food security status of the households improves when the number of registered COVID-19 cases goes up (when other variables remain constant). In Cambodia and Vietnam, where the growth of ∆X1 in January–June 2020 was more moderate compared to some of their neighbors in South Asia, we see a negative X1-to-Y relationship. The lower portion of imports in the balance of food trade has a positive and statistically significant impact on the number of people with insufficient food consumption in Cameroon, Kenya, Tunisia, and India, whereas, in Cambodia, the relationship between X2 and Y is negative. The effects of X3 and X4 on Y are positive in all countries, except Cambodia, but not that significant compared to X1 and X2.

While the increase in the number of confirmed COVID-19 cases is found to have a significant positive effect on Y in the countries of Latin America and the Caribbean, in the case of many other Group 3 countries, there is a negative relationship between these variables (Botswana, Namibia, Libya, Jordan, and Iran). The strongest impact of X1 on Y is revealed for Peru and Ecuador, where an increase in COVID-19 cases by 1% is associated with the growth of the number of people with insufficient food consumption by 0.54% and 0.40%, respectively. Statistically strong interplays are reveled between Y and X2 in Algeria, Botswana, and Colombia, between Y and X3 in Sri Lanka and Turkey, and between Y and X4 in Ecuador and Namibia. The negative influence of X2 on Y is identified to be statistically significant in Sri Lanka and Iran, of X3 on Y—in Algeria, Dominican Republic, Iran, and Iraq, of X4 on Y—in Sri Lanka. Error correction measure is statistically significant in the case of all three groups of countries.

The results of the fully-modified ordinary least squares (FMOLS) and dynamic ordinary least squares (DOLS) tests are employed to check the robustness of the ARDL estimates (

Table 6 for a group-based summary,

Tables S7–S9 for country-specific data).

The number of registered COVID-19 cases is confirmed to result in higher food insecurity across three types of economies included in the study, except some countries of Sub-Saharan Africa (Burkina Faso, Chad, Ethiopia, Zambia, Botswana, and Namibia), Middle East and North Africa (Yemen, Iran, Jordan, and Libya), and East Asia and Pacific (Cambodia and Vietnam). Among these twelve countries, for which we see a reverse relationship between COVID-19 cases and the number of people with insufficient food consumption, there are representatives of various income groups. Reasoning from this fact, we can assume that in a particular country, the direction of the

Y-

X1 link does not depend on GNI per capita. However, when the relationship between these two parameters is positive, there is evidence of a stronger

Y-

X1 correlation in Group 3 countries compared to that in Group 1 low-income economies. The Toda–Yamamoto test demonstrates the most significant causality flowing from the number of COVID-19 cases to the number of people with insufficient food consumption in Group 3 countries of Latin America (Colombia, Ecuador, and Peru) and Europe (Turkey), whereas, in low-income economies, the

X1Y causality is weaker (

Table 7,

Tables S10–S12).

Similarly to bidirectional interactions between COVID-19 cases and food insecurity across all groups of countries, both the FMOLS and DOLS tests confirm divergent relationships between the number of people with insufficient food consumption and the balance of food trade. In Group 2 and Group 3,

Y-

X2 relations are positive (except for Cambodia, Iran, and Sri Lanka), while in Group 1, they are negative for almost half of the countries. In Sub-Saharan Africa (Burkina Faso, Chad, Mali, Niger, and Tanzania), an increase in the balance of food trade is identified to be effective at reducing the number of people with insufficient food consumption. From the estimation of the Toda–Yamamoto causality test (

Table 7), we see the unidirectional

X2Y causality in Group 1 countries, but the significance of the link is low.

The strongest influence of food access on food security is revealed in low-income economies of Sub-Saharan Africa (Burkina Faso, Ethiopia, Guinea, Mali, Mozambique, and Sierra Leone), as well as some countries of Central Asia (Tajikistan) and Middle East (Yemen). In some Group 3 countries, robustness tests show a negative relationship between X3 and Y when the number of people with insufficient food consumption goes up amid food deflation. We also see examples of such reversal links in upper-middle-income countries of the Middle East (Iran and Iraq), where food prices are to a large extent under government control. Confronting Hypothesis 3, in lower-middle-income economies of Southeast Asia (Cambodia, India, Indonesia, Pakistan), seasonal retreat in food prices does not immediately result in higher food security expectations among people. In these countries, the X3Y causality link is weak due to the high portion of locally produced seasonal food in consumption. Among Group 2 economies, more significant causality flowing from food inflation to food insecurity is revealed for the countries of Sub-Saharan Africa (Cote d’Ivoire, Nigeria, Zambia, Kenya), where diversity of locally-produced staples is narrower compared to Asia. When a portion of marketed food in supply is higher, a deterioration in economic access to marketed products imposes a more significant impact on the aggravation of food insecurity.

It is assumed that in the countries where a large portion of the food supply is ensured by imports, food inflation might correlate with currency exchange. However, we see that in low-income economies, where food access strongly correlates with food inflation, the number of people with insufficient food consumption is marginally affected by currency exchange fluctuations. The weaker link between Y and X4 across Group 1 stems from the fact that low-income economies import a considerably lower amount of high-quality and expensive food products compared to lower-middle and upper-middle-income countries. As contrasted with low-income countries, Group 3 economies are deeper integrated into global supply chains of value-added food products. From this perspective, amid the COVID-19 pandemic, the most significant causal relationships between volatilities in currency exchange and food supply are found in the countries with the highest GNI per capita among those included in the study—Turkey, Colombia, and Peru.

With the current dynamics of registered COVID-19 cases across three groups of countries, the extrapolation of the short-run ARDL estimates to the future forecasts a gradual increase in the proportion of food insecurity variance explained by the effects of the pandemic. Variance decomposition of

Y-X(1–4) interactions (

Table 8,

Tables S13–S15) indicates a diversity of potential causality impacts of COVID-19 cases, balance of food trade, food inflation, and currency exchange on the number of people with insufficient food consumption.

For Group 1 countries, the decomposition analysis suggests a rather stable and weak

Y-X1 linkage over a three-quarters horizon (

Table S13). Only in Nepal, Yemen, and Mali, the food security situation could be significantly predicted by the variations of

X1. But even in these countries, we see that the expected proportions of

X4 and

X3 in

Y nearly equal that of

X1 in size. For most of the low-income economies, variance decomposition projects an increase in the proportion of

Y explained by food inflation (14.84% in Ethiopia, 13.70% in Chad, 11.12% in the Democratic Republic of the Congo) and currency exchange (9.01% in Burkina Faso, 7.72% in Mali, 6.65% in Niger).

In lower-middle-income economies, the number of people with insufficient food consumption seems to be increasingly affected by food availability. By March 2021, in import-dependent Kenya and Kyrgyzstan, the proportion of

Y explained by the balance in food trade is forecasted to exceed 10% (

Table S14). The weight of food access in establishing food security will grow in the countries of East Asia (15.98% and 15.27% of

Y explained by

X3 in Vietnam and Cambodia, respectively) and Sub-Saharan Africa (12.44% in Cote d’Ivoire and 11.60% in Zambia). The projected causality between

Y and

X1 is the strongest in the countries of South Asia. In India, at the current rate of registered COVID-19 cases, almost 14.50% of the proportion of insufficient food consumption will be impacted by the pandemic. It is the highest expected impact of the pandemic on food security among forty-five countries included in the study. In Bangladesh, the strength of the

Y-X1 linkage will exceed 12.00% by the second quarter of 2021. Across Sub-Saharan Africa and East Asia, a relatively low number of registered COVID-19 cases allows one to predict the moderate role of

X1 in the explanation of

Y variations over a nine-month horizon.

Among upper-middle-income countries, the impact of the pandemic on the number of people with insufficient food consumption is not expected to vary significantly from region to region. The proportion of

Y explained by

X1 is expected to peak in the countries, where the number of COVID-19 cases per capita in January–June 2020 was the highest among Group 3 economies. Over the entire time horizon considered in this study, the growth in

X1 will most likely and consistently be converted into a higher percentage of the population in food insecurity status in Peru, Iran, and Turkey (

Table S15). Variance decomposition also projects significant contributions of

X1 to

Y in Colombia (8.93%), Algeria (8.35%), and Ecuador (6.91%).

4. Discussion

The revealed interplays between the variables across three groups of countries allowed us to test the hypotheses:

Hypothesis 1: Not confirmed. The X1-Y relationship is uneven across Group 1–3 countries, where the strength of causal interaction between the two variables increases with the growth of income level.

The effect of the COVID-19 outbreak on the number of people with insufficient food consumption is observed across the three groups of countries. This finding supports the expectations of the FAO [

3,

16], the WFP [

14], and the WTO [

15], as well as the projections of many scholars [

5,

10,

50], who say that the spread of COVID-19 may bring damage to global food security, particularly painful in the least developed and developing economies. According to our results, the number of registered COVID-19 cases is indeed associated with higher food insecurity in many countries included in the study. The

Y-

X1 linkage is statistically significant in the countries (primarily, middle-income economies) where the number of registered COVID-19 cases per capita is high (Pakistan, India, Peru, Ecuador, Turkey).

Across low-income economies; however, the impact of COVID-19 on food insecurity is much weaker compared to that in upper-middle-income countries. This result well agrees with the FAO’s estimation that higher-income countries are more likely to face food supply disruptions during the novel health crisis, given their deeper integration in global supply chains and capital-intensive agricultural systems [

45]. In 2019, the WFP [

14] reported Yemen, the Democratic Republic of Congo, Afghanistan, Venezuela, Ethiopia, South Sudan, Syria, Sudan, Nigeria, and Haiti to constitute the worst food crises. Confronting the established Hypothesis 1, we see that in most of these countries, the relationship between the number of people with insufficient food consumption and the number of COVID-19 cases is not strong but moderate. For example, in Afghanistan, where at least 35% of the population is in a state of food crisis [

14], the increase in the number of COVID-19 cases by 5% results in the growth in food insecurity by only 0.03%. Moreover, we see that in several low-income countries, the dynamics of COVID-19 cases is related to

Y in a negative way. In some countries, where the number of COVID-19 cases remained low during January–June 2020, there is a reversal

Y-

X1 relationship. In Haiti, an increase in the number of COVID-19 cases by 1% is associated with the improvement in the food security status of the population by 0.11% (by 0.03% in Nepal and by 0.02% in Chad). Such a relationship can be explained by a statistically insignificant correlation between

X1 and

Y due to the low number of confirmed COVID-19 cases per capita.

Still, the effects of the pandemic on food security in low-income countries should not be underestimated. Even without considering the direct health-related influences of the spreading COVID-19 virus, the FAO projects low-income economies of Africa to overtake both lower-middle-income and upper-middle-income countries of Asia and Latin America to become the region with the highest number of undernourished people in 2030 [

3]. COVID-19 could exacerbate this trend, while the effects of the current health crisis on food security may be amplified by local outbreaks of other diseases that have been endemic in Africa and Asia. Many scholars, including Mouloudj et al. [

128], Bakalis et al. [

12], Poudel et al. [

129], and Siche [

130], witnessed significant adverse effects of SARS, MERS, avian and swine flu, Ebola, and other outbreaks on both agricultural production and food consumption behavior. On a smaller scale and in a more localized context, endemic diseases cause disruptions across local food supply chains similar to those the COVID-19 pandemic does to the global food supply. According to Ceylan and Ozkan [

131], both SARS and MERS had a downsizing effect on the production and supply of food, as well as on labor demand in agriculture. Kodish et al. [

132] and Wernery and Woo [

133] found movement restriction policies and quarantines introduced during MERS, Ebola, and other more local outbreaks to have substantial effects on agricultural production, food industry, as well as on distribution and retailing of many staples. Dounamou et al. [

134] revealed a significant shift in consumption patterns during Ebola outbreaks in West Africa. In an attempt to avoid the consumption of wild meat potentially associated with the Ebola virus disease, many people tend to switch to domestic meat and fish. In a situation when affordability and availability of alternative protein sources are deteriorated by trade and economic factors (as we see it amid the COVID-19 pandemic), local outbreaks of other diseases may substantially aggravate both health and food security status of broad segments of the population.

Transmissibility of COVID-19 is estimated to be 2.5 compared with 2.4 for SARS. Other recent pandemics had lower basic reproductive rates—1.5 for the 2009 influenza pandemic and only 0.9 for MERS [

135]. Despite comparable transmissibility rates, the trajectories of COVID-19 and SARS are different. While SARS 2003 outbreak was contained within eight months with a global total of 8098 reported cases across 26 countries [

136] and MERS caused 2494 reported cases in 27 countries [

137], COVID-19 is spreading rapidly with over 10 million known cases as the end of June 2020. But the unprecedented spread of COVID-19 throughout the world compared with other pandemics of the past is caused by greater ease of global transportation [

138] and higher population density [

12] the world has achieved by 2020, not exclusively by higher contagiousness or better transmissibility of the novel coronavirus. With the growing globalization, any local outbreak has its chance to emerge to the global pandemic, while climate change and environmental degradation may increase the appearance of zoonotic diseases in humans [

139,

140]. In LDCs and developing countries of Africa, Asia, and the Middle East, the impact of outbreaks on the food security status of people is particularly severe in transitional food value chains, such as wet markets [

141]. They bring together large numbers of people in crowded spaces at considerable risk of contagion [

142]. According to Hasöksüz et al. [

143] and Silva-Jaimes [

144], in such traditional food markets where human–wildlife interactions and cross-species infections are frequent, novel coronaviruses are likely to emerge periodically. Petersen et al. [

135] also expect a post-COVID-19 pandemic of another coronavirus, an influenza virus, a paramyxovirus, or a completely new disease to be highly likely in the nearest future. Due to rather high economic and social costs of bringing local outbreaks under a successful level of control at early stages [

145], LDCs and developing countries of Africa and South Asia are particularly vulnerable to the frequency and intensity of disease cycles that may realize their “pandemic potential”.

On top of the health and economic effects of COVID-19, there are climatic pressures that often aggravate supply-side food shocks in Africa and Asia (droughts, heatwaves, locust swarms, etc.) [

7]. In 2020, production declines due to dry weather conditions are expected in Morocco and Tunisia [

146]. In East Africa and South Asia, significant rainfall amounts resulted in floods and caused damages to farmland and livestock deaths. Zurayk [

50] has recognized locust invasion in the countries of the Middle East and East Africa as a further destabilizer of the stability of food supply in the times of the pandemic. Shilomboleni [

147] prognoses the COVID-19 pandemic to put a further strain on Africa’s agricultural sector amid the recent desert locust outbreak in the Horn of Africa. In West Africa, COVID-19 lockdowns are limiting population movement and causing local labor supply shortages [

146]. According to FAO’s crop prospects [

146], adverse weather resulted in a below-average output in North Africa and Central Asia and near-average cereal harvests in Central America and the Caribbean. Amid such climate-change driven disruptions of food systems, the pressure of both COVID-19 and local outbreaks on food consumption may be intensified by lower harvests and higher food prices in Group 1 countries, as well as across a wider community of developing economies. Mouloudj et al. [

128] and Janssens et al. [

148] expect developing countries of Africa and Asia in which agriculture contributes significantly to GDP (Sierra Leone, Chad, Niger, Mali, Cambodia, and Vietnam) to be affected by both climate and economic effects of the pandemic (suspension of agricultural activities, agricultural labor lockdowns, etc.). According to the FAO estimates [

146], over 14 million people in Africa in 2020 need urgent food assistance, including 7 million in Nigeria, 2.1 million in Burkina Faso, 2 million in Niger, 1.3 million in Mali and Sierra Leone, and 1 million in Chad. With respect to food availability, domestic agricultural production in LDCs and developing countries of Africa may be severely affected by the disruption of the supply of various inputs [

13], including animal feed and ingredients for food product preparation, especially if they need to be imported [

145].

Hypothesis 2: Partly confirmed.In Group 1 economies, the influence of food inflation over access to food and agricultural products is stronger than that of food trade over food availability.

In low-income economies, the food security status of people is significantly influenced by both the physical availability of and economic access to food products. According to FAO’s most recent food security report, a key reason of growing food insecurity in developing countries is that many people cannot afford the increasing cost of healthy diets, while the nutritional status of vulnerable population groups has been deteriorated due to the economic impacts of COVID-19 [

3]. Martin and Anderson [

20] and Freund and Özden [

149] assumed that protectionist trade policy could bring a risk of additional economic losses for developing countries by insulating domestic markets from global food price fluctuations. The FAO’s monitoring of food price changes [

23] since February 2020 demonstrates that amid the COVID-19 crisis, trade restrictions are imposed against the backdrop of growing food prices. The FAO Food Price Index averaged 93.2 points in June 2020 (by 2.4% higher than in May 2020) [

150]. Zurayk [

50] reports a global price increase in the food basket of 20% to 50% with the prices of dairy products, vegetable oils, sugar, and other food and agricultural products rebounded to multi-month highs [

150]. Our results indicate that rising food inflation deteriorates food access across Group 1 countries as it is tightly linked with the increasing number of people with insufficient food consumption. This correlates with FAO’s estimation that the cost of a healthy diet in 2020 has exceeded the international poverty line, making it unaffordable for the poor and thus fueling food insecurity in most developing countries, particularly in Sub-Saharan Africa and Southern Asia [

3]. Healthy diets have become 60% less affordable compared to the nutrient adequate diets and five times more expensive than diets that meet only dietary energy needs through a starchy staple [

3]. Many scholars, including Bakalis et al. [

12], Berkowitz et al. [

151], Gundersen and Ziliak [

152], and Garcia et al. [

153], associate undernourishment with adverse health outcomes, including chronic conditions, mental health challenges, and increased risk of mortality. Niles et al. [

154] found that lower economic access to food forced many food-insecure households to disrupt eating, cut meals, eat less to stretch their food, or even go hungry. This link between the cost of a diet and food security status has an important impact on individual health. An increase in food inflation is confirmed to have a significant effect on food insecurity in Group 1 countries, thereby supporting Hypothesis 2 and confirming previous findings of Smith et al. [

59], Power [

66], Sonnino et al. [

67], Esturk and Ören [

155], and many other authors who linked food insecurity with the level of income rather than with food imports. In our study, the strongest influence of food inflation on the number of people with insufficient food consumption is revealed in low-income economies of Sub-Saharan Africa (Burkina Faso, Ethiopia, Guinea, among others), as well as some countries of Asia and the Middle East. The UNCTAD [

45] also acknowledged the countries of Sub-Saharan Africa to be particularly exposed to demand-side risks of food access during the COVID-19 crisis, including contracting incomes, downturns in economic growth, undernutrition, and micronutrient deficiencies in response to income shocks.

Food inflation affects demand, but inflation itself is often a product of changing demand patterns. During the economic crisis of 2008–2009, reduced income made people spend less and resulted in shrinking demand for food [

16]. The novel health crisis is quite a different story. On the back of rising lockdown fears in February–March 2020, food inflation was fueled by higher demand due to panic buying [

145,

156]. Although Yuen et al. [

157], Zurayk [

50], and Fawzi et al. [

156] did not account for the level of income as a factor that affected such consumer behavior, we may assume the contribution of panic buying to food inflation to be more significant in Group 3 countries. In low and lower-middle-income economies, people have less free money to stock up food, while most cases of panic buying have been evidenced in developed countries [

158,

159]. In LDCs and developing economies, no significant spikes in food demand have been registered in the first quarter of 2020. On the contrary, the FAO [

16] expects the crisis-induced economic downturn to alter dietary patterns in the developing world due to a disproportionately larger decline in consumption of higher-value products like meat, fish, fruits, and vegetables.

Many scholars [

160,

161,

162] have found the likelihood of food insecurity to increase with income inequality. According to the FAO [

2], the inequality–insecurity link is 20% stronger for low-income economies compared with middle-income ones. This well agrees with our finding of the disproportional effects of food inflation on food insecurity across the three groups of countries. For instance, in Mozambique (Group 1), keeping other variables constant, a 1% increase in food inflation leads to a growth in the number of people in food insecurity status by 0.80% (by 0.71% in Tajikistan, by 0.53% in Burkina Faso, 0.41% in Guinea, and so on down the list of Group 1 economies). In Group 2, the

X3-

Y link is weaker while that in Group 3 is the weakest among the countries included in the study. There are even negative relationships between

X3 and

Y in some Group 3 countries of the Middle East and Southeast Asia.

With that said, our study demonstrates that in lower-middle and upper-middle-income developing countries, the causality link between food inflation and food security is weaker compared with that in LDCs. Generally, in low-income countries, food supply is for the most part ensured by local staple foods, whereas extensive import is prohibitively expensive. According to the FAO [

3], low-income countries rely more on staple foods and less on fruits and vegetables and animal source foods than high-income countries. As previously found by Thome et al. [

65], Ritchie et al. [

62], and Elbushra and Ahmed [

163], weak cointegration between food inflation and food security in low-income economies could be explained by the high portion of locally produced staples in consumption. Amid the COVID-19 outbreak, some countries have decreased food purchases from abroad, thus automatically increasing their foreign trade balances due to the lower portion of imports. As more households switched to locally produced staples, their food security status improved. However, as noticed by Devereux et al. [

11] and Farrell et al. [

13], a closure of open-air markets and a ban on street vendors (the two most common food outlets in poorer countries) may disrupt food access even in a situation when consumption is reoriented on local products. Prior to the current health crisis, many food-insecure households have reported such food coping strategies as, for example, seeking resources from the charitable food sector or relying on social networks for support [

164,

165]. Amidst COVID-19 lockdowns and restrictions, most of the nutrition assistance programs have been frozen.

Therefore, it is revealed that food availability seems to be strongly related to the food security status of households, but through local supply, not import. Following Deuss [

166], Martin and Anderson [

20], and Hendrix [

19], we assume that food trade restrictions were more pronounced in the countries with a higher import dependency. According to Wood et al. [

167], for import-dependent economies, both global food chain disruptions and protectionist trade policies on the part of key suppliers could have serious negative consequences for food security. This agrees with Puma et al. [

21], who found that LDCs suffer greater import losses due to disruption of food supply chains through their increased dependence on imports of staple foods. There is a unidirectional

X2Y causality across Group 1, but the significance of the link is low even in the countries where food availability largely depends on imports (Haiti, Guinea, Tajikistan). These findings do not support Hypothesis 2. With an increase in the level of income, the link between food trade balance and food availability becomes tighter. The strongest effect of

X2 on

Y is revealed for import-dependent upper-middle-income economies (Jordan, Lebanon, Botswana, Algeria, Colombia). In most low-income countries, we see how a lower proportion of food imports in trade amid the COVID-19 outbreak is associated with a reduction in the number of people with insufficient food consumption.

Hypothesis 3: Confirmed.Different from the low-income economies, in Group 3 countries, the food security status of people is affected by food trade and currency exchange rather than by food inflation.

As recognized by Wood et al. [

167] and Hendrix [

19], food import is particularly essential to LDCs for meeting the dietary needs of their population during the COVID-19 outbreak. Our results; however, suggest that Group 1 and Group 2 economies rely on less diversified imports compared to Group 3 countries which are deeper integrated into global supply chains. For the latter, higher dependence on imports results in a stronger influence of food trade balance and currency exchange on food supply and, consequently, on the food security status of people. While Devereux et al. [

11] stated that COVID-19 had not compromised food supply globally, Mouloudj et al. [

128] and Toffolutti et al. [

8] found food security status of developing countries that depended on imports of staples to be particularly threatened by disruptions of the food supply in the first half of 2020. In import-dependent developing countries, currency depreciation drives up the cost of food imports [

49]. Thus amid market uncertainties induced by the COVID-19 crisis, currency exchange becomes a factor of both food availability (more expensive imports due to currency depreciation) and access to food (the higher price of imported food on the domestic market when expressed in national currency). The UNCTAD [

45] revealed heightened risks to food security in those countries of North Africa and the Middle East that rely on food imports and thus are dependent on currency volatilities triggered by the pandemic. In support of this UNCTAD’s estimation, the strongest effects of

X2 and

X4 on

Y are found for Algeria and Turkey. In furtherance of Hypothesis 3, we expect an increase in the proportion of

Y explained by both food trade and currency exchange, particularly, in upper-middle-income countries. In Libya, where the dependency on food imports exceeds 90%, the impact of

X2 on

Y is projected to be the highest among the three groups of countries (18.03%). In Namibia, another Group 3 country largely dependent on imports, the proportion of

X2 in

Y will almost reach 12.20% by March 2021. The importance of currency exchange in securing food supply will go up in the countries deeply integrated into global food supply chains. For instance, in Turkey, 15.21% of

Y will be explained by

X4.

The effect of food inflation on the number of people with insufficient food consumption is found to be weaker across upper-middle-income economies compared to that in low-income countries. This finding both supports Hypothesis 3 and agrees with Frankenberg and Thomas [

168] and Smith and Glauber [

69], who revealed that higher prices for staple foods aggravated poverty traps for low-income households, but might not have much effect on the food security status of relatively well-off households. On the other hand, domestic price volatility may be exacerbated by trade restrictions that have been implemented by some Group 2 and Group 3 countries on the backdrop of the COVID-19 outbreak. In the studies on the effects of export restrictions during the global crisis of 2007–2008, Deuss [

166] and Djuric et al. [

169] demonstrated that protectionist policies did not achieve their objective of reducing price volatility in the country imposing the restriction. There are also studies that show how trade restrictions resulted in food price spikes during the food crises in 1973–1974 [

170], 1986–1988 [

171], 2006–2008 [

21,

172,

173,

174], and 2010–2011 [

20]. Dawe and Timmer [

175] and Abbott [

176] found that, in the short-run, an export ban could be a successful decision to ensure the food security of a country by both establishing a reserve of staples and isolating domestic market from the global price volatility. For instance, in Cambodia, that limited exports of certain agricultural products in March–April 2020, we see how both negative balances of food trade and low food inflation resulted in the reduction in the number of people with insufficient food consumption. For Vietnam and Turkey, on the contrary, their decisions to restrict food export have not brought much success. The ARDL analysis demonstrates that in Vietnam, a 1% change in the food trade balance is associated with an increase in food insecurity by 0.02%. In Turkey, the

X2-

Y relationship is weaker but still positive. In both countries, we revealed substantial causal interaction between

X3 and

Y (5%

0.35% in Turkey and 5%

0.31% in Vietnam). This result supports the estimations of Anderson and Nelgen [

177], Giordani et al. [

178], and Rude and An [

179], who found that trade protectionism might trigger food inflation and thus aggravate food insecurity.

{kind=link}

{kind=link}