Abstract

In today’s globalized world, one of the great challenges for enterprises is integrating CSR adoption into their operations. The study aims to investigate how stakeholder pressure influences the adoption of corporate social responsibility (CSR) practices by Chinese medium and large-scale manufacturing enterprises in Ethiopia. This study used a mixed-methods research approach that includes primary and secondary data sources. The employed research data were analyzed using stakeholder theory, structural equation modeling, and multivariate regression analysis to identify the causal relationship between the stakeholder pressures and CSR adoption. The finding shows that overseas Chinese medium and large-scale enterprises at least have CSR awareness to meet compliance requirements. Comparatively, employees, community, and customers are the most influential and significant factors determining the enterprises’ stakeholder pressure on the CSR engagement. The finding indicates that Chinese enterprises are unrecognized for their CSR contribution due to a lack of public relation in displaying what they display the firms are doing. There is no strong link between Chinese manufacturing enterprises and the regulatory stakeholders to implement inclusive CSR awareness and eliminate conflicts of interest on legal frameworks. The study proposed some recommendations to solve the gaps regarding indifference to CSR adoption, the community’s lack of concern for CSR, and lack of proactive involvement. Government laws are required to legally control unbalanced practices and distorted views, as well as to guide fixing conflicts of interest. These finding are important for enterprises, policymakers, government officials, and local and foreign investors to identify, understand, and use the driving factors of stakeholder pressures on CSR practices.

1. Introduction

Although the concept of CSR may be unfamiliar to some, the need for socially responsible business is emerging [1]. Even if it is a novel concept, customers and investors want an enterprise that is environmentally and socially responsible. Companies’ approaches to social responsibility vary, but one thing they all have in common is a greater emphasis on satisfying and influencing stakeholders’ requirements. In this regard, stakeholder theory asserts that stakeholder pressure is the most important driving factor influencing CSR adoption [2]. During this shifting set of expectations, businesses globally face increasing pressure to adopt or improve CSR endeavors. Hence, CSR is defined as a strategy that provides a competitive edge to businesses [3]. It is also viewed as an integrated part of an enterprise’s competitive advantage that enhances the competitive landscape without jeopardizing its societal responsibilities [4]. CSR is defined as a framework to mitigate the negative consequences of business processes and improve consumers’ well-being and all other stakeholders, including the environment [5]. CSR’s primary and explicit message is that no harm should done to humans or their environment. CSR can also be defined as a firm’s commitment to improving economic development while enhancing the lives of its employees, their families, and society at large [6]. CSR generally refers to a company’s responsibilities to society, stakeholders, and those impacted and affected by its policies and practices [7]. Although the concept of CSR has been variously defined and explored in theory and practice, there is no universal consensus yet on what it means instead of giving contextual meanings.

However, various researchers have explored the relationship between stakeholder pressures and the adoption of CSR practices. Concerning the influence of stakeholders on CSR practice, some studies show positive, negative, mixed, or neutral results. According to stakeholders theory and CSR, social responsibility influences stakeholder pressure positively and significantly to address the minimizing of negative environmental impacts, promoting social progress, and increasing economic growth simultaneously [8]. Studies found that CSR and foreign direct investment are closely associated, with investment-based relationships being stronger than trade-based ties [9]. In addition, primary, secondary, and other symbolic and practical CSR practices have been identified by [10], with primary stakeholder influence positively affecting symbolic CSR and secondary stakeholder influence positively affecting practical CSR. Furthermore, stakeholder demands mainly influenced the companies’ action and CSR efforts in varied and diverse enterprises. As a result, community stakeholders, regulatory stakeholders, organizational stakeholders, and the media pressure businesses [11].

On the other hand, stakeholder pressures have decoupled risk by adopting symbolic rather than substantive actions because of the ownership of the enterprises or the chief executive officer [12]. Stakeholders are becoming increasingly concerned about whether the companies they are affiliated with act in a socially responsible manner [13]. Thus, employees and shareholders have a direct financial interest in those companies that may assure that a company’s actions result in some financial benefit. CSR positively affects social outcomes and can be conveyed through corporate communications to notify the firm’s internal and external stakeholders to contribute value [14]. Accordingly, stakeholders play a unique role in CSR implementation. Hence, meeting stakeholder demands needs to be prioritized to gain stable values. For instance, employees want to work for socially responsible businesses, customers want to buy from companies that meet their needs, and suppliers want to work with socially responsible firms. All of this results in attractive benefits for everyone [15]. Hence, stakeholders show an increasing interest in whether the enterprises interact socially and environmentally ethically [16].

In contrast, the external CSR enhances a firm’s market value and is negatively related to operational profitability of enterprises as stakeholders approach; also, internal CSR increases a firm’s operational profitability but does not affect a firm’s market value [17]. On the contrary, enterprises can connect with marginal stakeholders when managers’ emotions influence managers’ decisions. According to [18], the engagement can elevate the beneficiary stakeholder group to the point where, paradoxically, they become important stakeholders for the firms. Relatively, studies from [19] revealed that stakeholder salience, manager strategic stance, and resource availability, though insufficient in and of itself, are required to explain enterprise environmental performance. In addition, an uncertain business environment has a direct positive influence and a complex business environment has a direct negative influence on a firm’s environmental CSR strategy, and complexity has a negative moderating influence on the relationship between a firm’s stakeholder pressure integration capability and its environment [20]. From another perspective, consumers, internal managers and employees, competitors, and non-governmental organizations are the primary determinants considerably influencing corporate citizenship behavior, particularly in emerging markets [21].

The above findings show that the relationship between the influence of stakeholder pressures and various dimensions of CSR endeavors are inconsistent under different theoretical perspectives and empirical results, with contextual, methodological and variable disparities. This indicates that diversified stakeholder groups inherently have distinct resources and expectations. Besides, they may affect enterprises’ CSR engagement through the business practices. Meanwhile, companies in different countries and enterprises might interpret and implement CSR practices in several mechanisms, due to a varying business culture and institutional features. Moreover, concerning the other gap, most of the existent literature concerning the influences of different stakeholder groups on CSR adoption have been conducted in the context of developed economies, large corporations, and listed firms. Regarding CSR and stakeholders, particularly in the context of medium and large-sized enterprises, in emerging economies is still too underexplored to maximize the significance of stakeholders aligned with social responsibility.

However, there have been few studies on CSR in Ethiopia. According to the comparative case study of [22], CSR in Ethiopia is a concept that is only known within academic circles and not understood by the rest of society. According to [23], community, labor, customer, and social license are significant determinants of CSR. Firms, corporate governance, situational characteristics, and socio-economic and socio-cultural settings were reviewed as determinants of CSR practices [24]. The firms’ learning of social responsibility has been explored in which the state and foreign market pressures are the critical motivators for CSR implementation while regulating environmental and labor conditions. The state offers incentives for higher economic responsibility of firms [25]. Likewise, even though different research studies have been conducted in this area, there is a lack of studies and a limited understanding of whether stakeholder pressure influences CSR adoption of manufacturing enterprises.

Ethiopia has emerged as a preferred destination for international direct investment and as a manufacturing hotspot [26]. Ethiopia has become a crucial destination for foreign direct investment (FDI) because it is the center of the African Union [27]. Furthermore, Chinese investors in Ethiopia are the major manufacturers, and their products are a better partner for the country’s development needs. However, there is also an increasing inquiry of FDI in the manufacturing sectors and CSR concerns in Ethiopia, particularly regarding overseas business enterprises. Above all, Chinese companies are increasingly incorporating CSR guidelines into their business plans, and they are making significant progress in defining and implementing CSR. There are low regulatory standards and scarce research about Chinese companies investing in foreign developing countries in CSR, especially not on the mega projects in East Africa, including Ethiopia [28]. The manufacturing industry is an important sector in Ethiopia. Still, there is limited research in the areas of stakeholder pressures on the adoption of CSR in foreign firms. This knowledge gap is critical to a developing country such as Ethiopia, where social responsibility is still in its infancy stage [29]. Therefore, this research aims to fill the gaps identified from previous studies. The purpose of this study is to look into the relationship between the five factors of stakeholder pressure that influence CSR behavior. Mainly, the study proposed a conceptual research model supported by a structural equation model and growth path techniques. This study tried to address the following basic three research questions: (1) What is the driving factors of stakeholder pressures that influence the adoption of CSR practices for Chinese medium and large-scaled manufacturing enterprises in Ethiopia? (2) How do those driving factors of stakeholder pressure influence the adoption of CSR endeavors? (3) How does a CSR-focused business culture mediate the relationship between stakeholder pressure and CSR adoption? (4) Is there a relationship between the factors of stakeholder pressure, CSR-oriented business culture, and CSR adoption?

2. Literature Review and Theoretical Framework

2.1. The Effects of CSR Practices

Although the concept of CSR has been discussed in the literature since the 1950s, there is still no widely agreed-on definition or understanding that exists. It is often linked to stakeholder theory, which is more strongly tied to a corporation’s CSR strategy [30]. In this regard, CSR is an enterprise’s duty for its social repercussions, and the basic strategy of such an enterprise should be developed in close collaboration with its stakeholders [31]. Furthermore, CSR seeks to identify what duties businesses should perform, but the stakeholder paradigm focuses on who businesses should be accountable to, and the two concepts are interrelated [32]. Effective CSR helps boost favorable organizational competitiveness by responding to various stakeholders’ demands and economic, social, ethical, and environmental requirements that make up the enterprise’s environment [33]. Moreover, the effectiveness of CSR has determined how companies use their resources and capable competencies to implement CSR. Hence, a company’s dynamic capability is its ability to integrate, build, and restructure internal and external competences in response to environmental changes [34].

Furthermore, companies can pursue sustainable development by having a consistent economic, social, and environmental view on how CSR should be managed. As a result, CSR must become an inherent part of the corporate management system [35]. It plays a significant role in deteriorating the relationship between the company and its major stakeholders, both internally and externally. Besides, CSR activities are more significant to shareholders’ investment and financing decisions as stakeholders because they lower the cost of equity capital [36]. That means the findings have significant consequences for investors and other stakeholders in the enterprise.

Furthermore, when CSR understanding is poor, CSR practices mostly focus on company governance, environmental management, occupational development, economic responsibility, and community development [37]. In this situation, state-owned enterprises are more concerned with communal responsibility, whereas private enterprises are more concerned with economic and employee development. Similarly, companies have been pushed to embrace policies beyond their economic features to be socially responsible and consider CSR implementation in their enterprises’ activities [38]. As a result, socially responsible businesses are developing highly valued CSR issues to gain stakeholder trust [39]. In this context, the features that generate stakeholder trust correspond to the ethical actions of business firms. As a result, great enterprises can improve the lives of their communities by creating value for stakeholders rather than focusing solely on profit for shareholders. Mainly, better interactions with those inside and outside the business result from a more ethical atmosphere. Such improved interactions with stakeholders lead to better outcomes.

In contrast, stakeholder and legitimacy theory examines the issue of stakeholders’ pressure effect on a firm’s CSR behavior. In comparison, CSR addresses the issue of stakeholders’ pressure effect on a firm’s CSR activity [40]. As a result, the effects of CSR’s impacts emphasize the distinct identity of stakeholders and legitimacy and the influence of two actors who have rarely been regarded as primary and most significant stakeholders. On the other hand, local primary stakeholders (management, employees, customers, suppliers, shareholders, creditors/banks, and competitors) positively impact responsive CSR activities but do not influence strategic CSR activities [41]; in contrast, local secondary stakeholders in host countries substantially influence both responsive and strategic CSR activities. That means secondary stakeholders such as the government, media, the community, and civic organizations have a greater influence on strategic CSR operations than on responsive CSR activities [38]. Even though the effect of CSR in business culture is the value of the actor, it eventually sets the aim of the desired stakeholder engagements. The stakeholder engagement does not always imply responsible company activity [42]. Subsequently, the claim that stakeholder involvement may be linked to enterprise accountability to stakeholders is oversimplified. In other words, perceptions of corporate social responsibility may differ based on a society’s culture, traditions, and era. In the practice of firms’ social responsibility, there can be a focus on one or even several extremely important actions, indicating that the firms have not yet digested the valuable content of the CSR idea and is increasing its activity while ignoring a key principle of inner development [43].

To conclude, CSR has attracted and gained attention in Western countries as a viable strategy for legitimizing a corporation’s image in the eyes of various stakeholders. CSR ideas have a more fragile foundation in other regions of the world, such as Ethiopia. As a result, when considering whether to engage in CSR, businesses consider stakeholder pressures. Companies are also willing to participate in CSR to fulfil a moral aim or do the right thing. However, several studies have focused on the impact of stakeholder pressures on CSR. There is still a lack of studies on how stakeholder demands affect the adoption of CSR practices by business culture as a mediator. Some research looked at the relationship between stakeholders and CSR from a primary and secondary stakeholder perspective. In contrast, others believe the secondary stakeholder is the most important determining factor, with few studies considering the primary stakeholder. In the following, this study uses a mediator variable with a structural equation and a growth path model to investigate the five factors that influence stakeholder pressure on CSR adoption.

2.2. The Relation between Factors of Stakeholders Pressure and CSR

2.2.1. Employees

The primary stakeholders are possibly the most powerful groups in a firm’s internal stakeholder entities [44]; they are directly involved in an enterprise’s establishment, design, structure, and operation. If the stated goals are to be met, employees’ motivation, loyalty, and organizational support are critical. Employee views about an enterprise may also impact external stakeholders’ perceptions of the company [45]. Employees are involved in developing and implementing company strategies, particularly those linked to CSR, as well as reflecting, representing, and supporting social norms. Besides, the contributions of enterprises to their existing and prospective workforces are fundamental to the CSR perception of society. It has been empirically supported that being a socially responsible employer positively affects relevant institutional results [46]. In this case, employees are primarily at the top of the CSR agenda in most firms. CSR activities have been influenced through employee performance, and there is a positive association between employee perception of corporate social responsibility and employee outcomes [47].

In contrast, the influence of the media and social activist groups are often viewed as the major and most significant stakeholders [40]. Here, this implies a mismatch between the media and social activist groups as significant, influential stakeholders, requiring further discussion and research to determine their position as primary or secondary stakeholders. Some researchers have seen media and social activist groups as secondary stakeholders, while others saw them as primary and most significant. Social identity theory [46] suggest that the CSR of social and non-social stakeholders, employees, and customers are significant predictors of organizational commitment. Likewise, employees are the most powerful stakeholders in a company’s CSR since they are both affected by the actions of the enterprise [48]. In other words, from an internal stakeholder’s perspective, CSR practices have a substantial influence on both the employees and organization’s performance [49]. That means both CSR and employees simultaneously have a multiplying effect on employee engagement and improved productivity.

Furthermore, employees’ perceived CSR indirectly relates to each of the factors via organization commitment [50]. For instance, the negative relationship between perceived CSR and turnover intention was stronger when employees had a higher moral identity. The positive relationship between perceived CSR and in-role job performance and helping behavior could be amplified by moral identity. The effects of CSR on employment relationships show that socially responsible actions significantly encourage employers to use performance-based pay and efficiency-based work practices [51], but also a negative relationship between CSR and employment growth and increased labor flexibility through contingent employment. CSR has a positive impact on an employee’s organizational identity as well as their perception of doing meaningful work, which motivates them to work harder while neglecting other aspects of their lives, such as private relationships or health [52]. Thus, CSR indirectly leads to work addiction.

On the other hand, organizational identification and work meaningfulness act as moderating variables in the relationship, reducing CSR’s negative impact on work addiction and diminishing CSR’s positive impact in the workplace. However, employee attitudes and support for company actions are significant to enterprise management. There are still some disparities in the links between employees and CSR practices that need to be addressed in future studies. As a result, the goal of this study is to look into the effects of employee stakeholder pressure on CSR adoption. We thus developed and tested the hypothesis below.

Hypothesis 1 (H1).

Employee stakeholders positively and significantly affect the adoption of CSR practice.

2.2.2. Customers

Customer purchasing intentions have been positively influenced by CSR actions both directly and indirectly by boosting brand image and trust, while customer awareness of CSR activities plays a mitigating function [53]. Therefore, CSR improves business performance, enhances export volume and performance, improves business image and reputation, and increases satisfaction among important stakeholders [54]. CSR is a multidimensional cultural construct that directly and indirectly affects customer loyalty [55]. Hence, customers have been identified and co-created because of CSR initiatives. As the authors in [56] observed, socially responsible employees and suppliers positively impact customer value co-creation behavior. Customer engagement is a mental condition that influences customer behavior regarding CSR adoption. As a result, the authors in [57] indicate that a CSR image causes customer engagement, which leads to behavioral responses such as customer loyalty, word-of-mouth, and feedback.

On the other side, the authors in [58] found that when a company is defined by customer closeness, in terms of product or service visibility for consumers, CSR reporting has a large impact on the market, but that the effect is beneficial for family businesses and negative for non-family enterprises. In comparison, researchers in [59] found that CSR seemed to harm customer trust while also positively impacting corporate reputation and word of mouth; this indicates a company’s reputation positively influences word-of-mouth and customer trust. Here, as the previous findings show, there are research gaps concerning the relationship between customers’ stakeholders and CSR practices. This study has initiated an investigation into the influence of customers on CSR implementation. As the above literature indicates, there are research gaps regarding the interaction between customer stakeholders and CSR practices. This study aims to identify the relationship between customer provision and CSR implementation. As such, we have created and tested the following hypothesis.

Hypothesis 2 (H2).

Customer stakeholder pressure positively affects the adoption of CSR activity.

2.2.3. Community

The community consists of the public at large, consumers, and special interest groups, whose impressions of an enterprise reflect its status and reputation [60], as well as how it is positioned concerning other organizations. Consequently, CSR has a beneficial impact on community stakeholders and has a significant association with them [61], indicating that CSR can help to improve community collective ability, action, and responsiveness. Moreover, long-term corporate communications, experience with the firm and its products, and perceptions of an organization’s societal impacts shape community stakeholders’ perceptions [62,63]. The community has a variety of functions, including those of consumers, who directly influence enterprises decisions. CSR activities substantially impact business value and social change, which increases either from low to fast growth or from rapid to high-quality growth to seek sustainable progress [64].

Furthermore, as [65] demonstrated, the greater the effect of communities on business operational parameters, the more powerful their demands are in the eyes of management. Expectations of corporate behavior, a shift in how communities express their expectations, and increasing stakeholder capacity to influence enterprise operations are all significant factors in how enterprises respond to the local community and social expectations. In contrast, Consumers can boycott companies for their unethical behavior, resulting in a shortage of socially responsible operations [66]. In this scenario, irresponsible enterprises may harm CSR and the community. Hence, improper business behavior can have long-term consequences, harming both company reputation and firm performance.

Although firms are considered as having an obligation to respect society’s long-term requirements and expectations, which indicates that they engage in activities that promote societal advantages while minimizing the negative impacts of their actions, as long as the company is not biased by doing so. As key stakeholders, enterprises disregard CSR, and vice versa, the community does not care about CSR instead of giving priority to today. This study intended to examine to what extent the community influence CSR practice. Therefore, the following hypothesis, which is linked with the study’s aims, was developed and tested.

Hypothesis 3 (H3).

There is a favorable relationship between the impact of community stakeholder and CSR.

2.2.4. Government

Although CSR is more closely linked to important corporate stakeholders, the role of the federal, state, and local governments also must be taken into account. Thus, government policies are the most important variables in fostering a better understanding of CSR since they have such a large impact on the context of economic actions as part of the system’s rules. Moreover, the government-imposed legislation, rules, and public policies are generally the primary principles for implementing social responsibility in host nations [38] and are coercively and widely applied to company activity within their borders. According to the findings, CSR positively influenced both primary (consumers, internal management, employees, and business partners) and secondary stakeholders (governments, media, local community, and NGOs). Hence, governments have recently became the most essential change agents influencing corporate practices by defining the rules of the system. [67]. Similarly, mixed approaches, which combine industry standardization with government control, may be the best policy option. The social desirability of this form of self-regulation remains a mystery because this comparison is incredibly difficult to establish in practice. In this regard, the government has long been seen as the most important change agents in influencing corporate behavior by defining the rules of the game [68]. Based on stakeholder salience theory, the authors in [69] tested how political connections changes the managers’ perception of stakeholders’ relative importance and cause changes in the stakeholders’ satisfaction level of their social responsibility requirement. The result shows that political connection has a positive influence on private companies’ CSR; companies with political connection are significantly better than the ones without political connection regarding society-oriented and customer-oriented responsibility. Therefore, this implies that companies with political connections are worse than the ones without political connection.

In contrast, the relevant regulatory parties are required to intervene to mitigate the external costs imposed, particularly by developing nations that do not get adequate compensation from firms liable for social and environmental damage [70]. Whereas the link between CSR activities and business financial performance is still debatable, the relationship is influenced, at least in part, by how the CSR project is implemented [71]. Given that, CSR initiatives are often in collaboration with non-governmental organizations, which focus on factors that influence the effectiveness of collaboration. In addition, some [38] have demonstrated that business collaborators have a negative and significant effect between the influences of stakeholders on CSR. On the hand, there is no link between the CSR of a government and the commitment level of employees [46]. Further, the authors in [72] looked at the impact of geographical distance between companies and governments on CSR activities, and found that the effect of distance between nations on CSR also applies within countries, with distance and CSR being negatively associated.

However, as the previous research findings indicate, there is a disparity in the perspective of government and CSR adoption based on various constraints. Still, there is a debate regarding the impacts of government stakeholders and CSR adoption either country to country or enterprise to enterprise, which needs further investigation, particularly in developing countries such as Ethiopia. In this study, we intended to support the substantial influence derived from the relationship between the government and CSR practice in the context of Chinese medium and large-sized manufacturing enterprises in Ethiopia. Therefore, we derived and tested the following hypothesis.

Hypothesis 4 (H4).

There is a substantial and significant impact between the relationship of government and CSR.

2.2.5. Media

The media’s job is to keep the public informed about important issues. A neutral and unbiased media can also have a substantial impact on public perception [73], which looks into how news media presents corporate environmentally sustainable development activities and if they focus on specific sectors or firms with greater market visibility. The media plays an important role in the firm’s communication with its stakeholders [74]. The media serves as an important medium for communication between the company and its stakeholders. As a result, having continuing interactions with the media and delivering relevant information can help enterprises gain favorable media exposure. Moreover, the media plays an important role in improving communications between the company and its stakeholders. In this regard, keeping continuing relationships with the media and offering interesting information might help a company obtain good media support. On the other hand, firms do not have control over the media; therefore, support will be more variable. As a result, the media has the capacity to influence how other stakeholders perceive an enterprise’s aggregate operations [75].

Furthermore, to develop trust in the adoption of CSR indoctrination in an uncertain, volatile, and changing business culture, it is necessary to form an integrated collaboration among inter-organizational actors and other stakeholders. CSR helps to establish relationships by reinforcing trust [76]; for instance, social media is a resource integrator, and CSR supports relationship building. As a social network, the authors in [77] investigated the need for media to transform the way corporations express their CSR issues by moving to a two-way communication model, comparable to other kinds of enterprises’ relationship with their stakeholders. Therefore, citizens, elites, local corporate enterprises, and overseas investment businesses all have a significant role in influencing public perceptions toward and influence over foreign policy, so that media stakeholder’s play a critical role in this process. On the other hand, firms improve their CSR performance and spend more on philanthropic contributions when the public perception of their CSR is negative and media coverage is extensive [78]. Likewise, firms with a higher proportion of long-term institutional investors spend more on philanthropy [79]. As a result, the findings show that unfavorable CSR news about the company affects its product market share. This demonstrates that in terms of philanthropy, media stakeholders have an inverse relationship with CSR. In this research, the study is motivated and desired to investigate the deriving factors of media stakeholders’ influence on CSR practice. Even though there is the debated issue concerning multiplier influences of media and CSR, the study tried to state and test a hypothesis to support the influence of media stakeholders on the adoption of CSR, as per the aims of the study, as follows.

Hypothesis 5 (H5).

There is a positive and significant influence between media stakeholders and CSR.

2.3. The Mediating Effects of Business Culture on Stakeholders and CSR

The economic, ecological, and social efficiency of an enterprise is primarily determined on its organizational culture. According to various literature, organizational (business or corporate) culture has described as a system of shared understanding and meaning among members of an organization or enterprise that defines how things can be done in the organization, according to various literature [80]. Habits, beliefs, values, customs, and philosophies that influence how things work and that differentiate between enterprises are all part of the business [81]. Hence, the authors in [82] investigated organizational climate, flexibility, change support, teamwork, and employee empowerment as characteristics that influence organizational culture in the context of CSR-oriented business culture. Moreover, employee development, harmony, and customer orientation of the corporate culture mediate CSR to employees and customers, but CSR to stakeholders is partially mediated [83]. Similarly, a CSR-focused business culture plays a favorable and significant moderating impact between stakeholder pressures and adoption of CSR practice [2].

On the other side, the authors in [84] revealed that corporate image and stakeholder pressure are influencing factors towards prioritization of the philanthropic dimension of CSR, and are mediated by the role of cultural influence. Cultural factors have considerable impacts on CSR performance, both positively and negatively depending on a given CSR component, as the findings in [85] reveal. According to the findings in [86], some organizational cultures moderate the association between CSR and financial outcomes. As a result, organizational culture plays a significant role in increasing the positive relationship between CSR and enterprise performance, even if corporate behavior and the pattern of social life within the corporation are influenced by organizational culture [87]. Because CSR entails managing social, environmental, and economic risks in the decision-making process, the corporate culture is significantly accountable for CSR as a driver [88]. Therefore, the focus of this study was on the role of business culture in mediating stakeholder pressures on CSR initiatives. The following hypothesis was developed and tested to support mediation effects between the response and outcome variables.

Hypothesis 6 (H6).

CSR-oriented business culture mediates factors of stakeholder pressures and CSR practices.

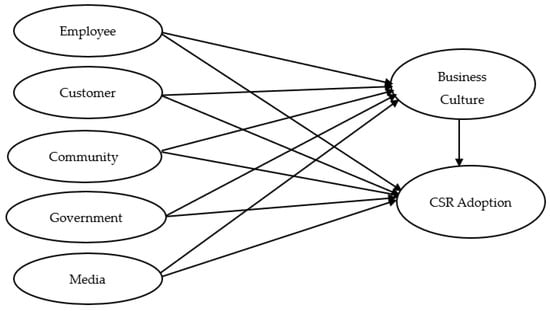

2.4. Conceptual Research Model

This study proposed the following conceptual research model to explore the empirical relationships among all driving factors of stakeholder pressures on CSR adoption. The independent variables are stakeholder pressure with the driving factors of employee, customer, community, government, and media. The outcome variable is adoption of CSR practice. Hence, the conceptual framework of the derived model tried to verify, estimate the fitness, and supported by the stated hypothesis in line with the indirect and direct effects of mediation variable CSR-oriented business culture.

Therefore, the proposed conceptual research model is constructed using the assumptions of structural equation, path modeling and growth path modeling analysis to support the findings of the results as shown in Figure 1.

Figure 1.

Authors’ own conceptual research model.

3. Materials and Methods

3.1. Study Design

This study focused on Chinese medium and large-scale manufacturing enterprises operating in Ethiopia. This research used a quantitative and qualitative research design, or mixed methods [89]. The study employed a mixed-methods approach, in which authors used a variety of mixed-methods designs to collect, analyze, verify, and integrate quantitative and qualitative data. In this study, the deriving factors of stakeholder pressures, such employee, customer, community, government, and media, were taken as the predictor variables. It also considered the CSR practice as a dependent variable, and business culture as a mediator variable. The study used primary and secondary sources of data. The primary sources of data were gathered from individual respondents such as the enterprise management, employees, and regulatory bodies. Accordingly, all the study variables were collected and measured using structured, self-administered questionnaires with 26 five-point Likert-scale items.

3.2. Sample Selection and Sampling Techniques

The sample size was determined using the total population of 1290 employees. The sample size was estimated using purposive sampling techniques, which resulted in 291 samples [90]. This study sample consisted of participants and a cluster of companies to make better use of quantitative research methods, which is more likely different from others. Individual respondents were chosen to fill out the questionnaires using simple random sampling techniques [90]. The Morgan sample determination table [87] was used to determine the specified sample of 291 [91]. The researchers attempted interviews with 20 respondents in order to obtain additional information. This interview was conducted to support the qualitative research approach of the study. Hence, five Chinese medium and large enterprises that are most likely to have economic, social, and environmental CSR concerns were selected. Those selected manufacturing enterprises are found in the Kombolcha, Bahir Dar, Debre Birhan, Addis Ababa, and Hawassa industrial parks.

3.3. Methods of Data Analysis

After fulfilling the necessary assumptions tests, all of the obtained data were evaluated. As a result, using the SPSS/AMOS 23 statistical software version, the acquired and validated data were coded, processed, and analyzed. To measure all the instruments, nominal scales were utilized considering the type of variables. The stated hypotheses were also put to the test and found to be correct. Structural equation modeling and path diagram modeling were employed in this research. Finally, depending on the proposed conceptual study, the estimated findings were more likely supported.

3.4. Measurement Items

3.4.1. Corporate Social Responsibility Practices

In this study, the measuring items of the dependent variable, CSR practices, were adopted from previously validated findings [92]. The practices of CSR were measured based on five contextualized items by using predefined five-point Likert-scale questions. Therefore, the response options ranged from 1 = ‘strongly disagree’ to 5 = ‘strongly agree’. The contextualized questionnaires are attached in Appendix A (Table A1).

3.4.2. Independent Variables

Employees are the primary stakeholders who have an impact on the corporate social responsibility. Thus, in order to perform the investigation as a targeted respondent, this study focused on employees, including managers. Even though employee stakeholder pressures on CSR implementation have been measured in a variety of methods. This study attempted to measure and adopt the findings from two prior studies [21,47]. In order to meet the study’s objectives, the contextualized instruments included four construct measuring items.

The variable customer stakeholders were quantified and contextualized aligned with the CSR practices [83]. Four instrument items were used to judge the causal influence of customer stakeholder pressures and CSR. In addition, the government’s influence was measured using previously validated findings in line with the study objectives. In this regard, the government regulatory variable was formed in three items. Likewise, the measurement items for determining the influence of community and media stakeholders on CSR practice were based on previously validated and confirmed findings [21]. Lastly, the newly contextualized measurement items of the media were evaluated in three questions. Similarly, as shown in Appendix A, the media stakeholder pressures were measured by three items.

3.4.3. Measurements of Mediator Variable

The study used previously validated measuring items [2] to assess the impact of the mediator variable CSR-oriented business culture, which was aligned with the company culture. Organizational culture and business culture are essentially the same thing, as in the two sides of one coin. In this study, five deriving factors, such as employee, customer, community, government, and media, were taken to predict the outcome variable CSR practice using the mediation impacts of a CSR-focused business culture. Thus, five construct items were used to evaluate the effects at large.

4. Results and Discussion

4.1. Analysis of Demographic Data

The demographic data of 291 sample respondents indicated that 71 percent (207) and 29 percent (84) of respondents were male and female, respectively. According to the age of the respondents, the majority (36%) of the respondents were 31–40 years old, 30.9% were 41–50 years old, 17.3% were 20–30 years old, and 15.8% were over 50 years old. The majority of the participants were mature and productive. The respondents were able to understand the researcher’s inquiry and provided reasonable responses. The majority of respondents (41.3%) were undergraduates (degree holders), 18.6% had diplomas, 19.4% were in high school, and 20.7% were postgraduates. This means that the vast majority of the respondents were able to provide useful information to the study.

4.2. Reliability and Validity Test

To meet the validity and reliability assumptions, all of the relevant questionnaire items were completely validated and confirmed using SPSS/AMOS statistical software in this study. Furthermore, all of the expected tests of validity, reliability, discriminatory validity, and multidimensionality checking enabled evaluation, verification of the model fit indices, and hypothesis testing. Hence, the study focused and confirmed the Cronbach alpha, factor loading, composite reliability (CR), and average variance extracted (AVE). Having this, the estimated value of Cronbach alpha for all variables ranged from 0.869 to 0.974, which has satisfied the recommended threshold value of an alpha greater than 0.70 [93]. Here, the result implies that the estimated values of alpha declared the goodness of the internal consistency of reliability and validity as above the calculated variance value.

Furthermore, the purpose of the factor analysis is to find the unexplained factors that influence the co-variation of several observations. The variance explained by a variable on a particular factor may be represented by factor loading values. Therefore, a factor loading of 0.70 or higher in a structural equation model technique indicates that the factor takes enough variance from the variable. Thus, the estimated values of the factor loading for the entire variable items results are more likely significant, which ranged from 0.783 to 0.968, demonstrating the strong convergent validity of the measurement constructs. In addition, the estimated composite reliability (CR) values of all the latent constructs ranged from 0.910 to 0.980, and are thus above the acceptable level of reliability, the threshold value of alpha being >0.70 [94]. This means that at a p-value of 0.05, the regressed weighted critical ratio (CR > 1.96) becomes a significant parameter. The estimates of the average variance extracted (AVE) values for all the derived construct items are adequate, ranging from 0.757 to 0.928, which is greater than the threshold values of alpha (>0.50) [95]. This shows that the measuring questions used in this study’s proposed conceptual model can better reflect the features of each research variable. Finally, Table 1 shows the results of the reliability and validity tests.

Table 1.

Reliability and validity test analysis.

4.3. Correlation Matrix and Discriminant Validity

As for the constructs, the covariance values reveal a high correlation between the outcome variable, CSR practices, and the individual constructs employee, customer, government, community, media, and CSR-oriented business culture. The square root of the average variance extracted (AVE) from the observed variables indicates that there is a positive and significant association between all independent and dependent variables at p-values 0.05. Therefore, the covariance values indicated that all constructs are interrelated.

Moreover, there is also positive and significant relationship between employee (EMP), customer (CUS), government (GOV), community (COM), media (MED), and the outcome variable CSR adoption. The mediation variable, CSR-oriented business culture (CBC), also supports the interrelations between variables, as demonstrated in Table 2.

Table 2.

Correlation matrix and discriminant validity result analysis.

4.4. Weighted Multiple Regression Analysis

Weighted multiple regression analysis is essential for determining which coefficient should be used as an indicator in multiple regression analysis to determine a variable’s contribution to prediction [96]. The weighted multiple regression results are important in this study because they allow opportunities to examine the interactions between the explanatory and response variables. Hence, this research looked at employee, customer, government, community, and media as drivers of stakeholder pressure, with CSR practices as the outcome variable and business culture as the mediation variable. The determined values of all parameter estimates (β) ranged from government (GOV) 0.702, media (MED) 0.802, customer (CUS) 0.841, community (COM) 0.894, employee (EMP) 0.952, to CSR practice (CSRP) 0.820, which more likely have positive and significant connections, with a direct impact as shown by the weighted multiple regression analysis result.

On the other hand, the parameter estimate (β) values ranging from community (COM) 0.791, media (MED) 0.802, customer (CUM) 0.815, government (GOV) 0.869, employee (EMP) 0.931, to CSR-oriented business culture (CBC) 0.768, which have more potentially positive and significant interactions indirectly, and which is supported by the mediation variable business culture. Further, when the parameter estimates (β) were compared to their relevant standard error (S.E), their critical ratio (C.R) weighted score was greater than 1.96, with a 0.05 p-value, indicating positive and significant integration, as shown in Table 3.

Table 3.

Regression weights for the level of significant and critical ratio.

4.5. Mediation Effects of Business Culture

In this research, SPSS/AMOS was used to examine the mediation effect of CSR-oriented business culture using the structural equation model and growth path model. As a result, the mediator’s direct and indirect effects were calculated using growth path modeling and weighted multiple regression analysis. Moreover, the study examined the deriving factors of stakeholder pressures on CSR practices by using business culture as a mediation variable. The Sobel-test was used to measure the magnitude of the mediator effect in boosting over other determined predictors and outcome variables aligned with the objectives of the study. Besides, as the estimation of Sobel test yields the test statistics value of the Z-score, which is greater than 1.96, the mediation effects exists [97,98,99]. The relationship between the deriving factors of stakeholder pressure and CSR activity was fully supported by the mediation effects of business culture. Because the Z-score of the Sobel test was above 1.996 and up to 5.948, and significant at p-value 0.05, it met the threshold of greater than 1.96, as indicated in Table 3.

Furthermore, as Table 3 depicts, the results of the mediation effects and Sobel test is highly significant, confirming that the dual effect (direct and indirect effect) is significant. It implies that the business culture trustfully mediates the relationship between variables of stakeholders’ pressure and the adoption of CSR practice. In other words, the Chinese business culture is more likely significant in Ethiopia‘s business enterprises. Therefore, this implies that socially responsible business boosts overseas investments, as the CSR-oriented business culture supports other constraints, as shown in Table 4.

Table 4.

Results of the mediation effects.

4.6. The Structural Equation Model and Growth Path Modeling Result Analysis

4.6.1. Structural Equation Model Goodness-of-Fit Indices

In this research, the study used a structural equation model to evaluate and check the goodness-of-fit indices, which has been proposed as a conceptual research model. Moreover, the derived conceptual model was analyzed using SPSS/AMOS statistical software to support the findings through a quantified model.

Hence, this study investigated the effect of the observed variables considering three structural equation modeling indices, namely, the comparative fit index (CFI), the Tucker–Lewis index (TLI), and the root mean square error of approximation (RMSEA). As the goodness-of-fit indices summary table indicates, the goodness of the model fit indices are acceptable, because all the estimated indices are above the recommended criteria values of the basic assumptions [100,101]. Therefore, the Chi-square (ꭕ2/df) for the model is 1.794, which satisfies the criteria of being less than 3.0; the GFI (goodness-of-fit index) value is 0.958, which is above the threshold values of greater than 0.90. Similarly, the AGFI (adjusted goodness of fit) is also acceptable at 0.957, which is greater than 0.90, the previously recommended value. The NFI (normed fit index) value is also 0.946, which is greater than the requirement criteria of 0.90. The IFI (incremental fit index) value is 0.974, which is above the recommended value of greater than 0.90. Even the CFI (comparative fit index) estimated value is 0.982, which is greater than 0.90, and the TLI (Tucker–Lewis index) is 0.984, which is greater than the recommended value of 0.90. To conclude, the proposed conceptual research model of this study has fulfilled the expected and recommended requirements of the goodness-of-fit indices, which was supported by the proofed structural equation model, as shown in Table 5.

Table 5.

Goodness-of-fit indices.

4.6.2. Growth Path Modeling Goodness-of-Fit Inferences

The pattern of the relationships between the variables was described in this study using a path diagram that incorporates growth path modeling assumptions. If a structural equation model comprises both factors and composites, path modeling is the method of choice [102]. SEM path modeling can used as a confirmatory tool according to Sobel tests of exact fit. Moreover, the study took into account the estimated values of the path modeling coefficients or the standardized estimate (β) as well as the explained variance of model fitness (R2), which were supported by the path-modeling diagram analysis results. As a result, the estimated values of the variables’ standardized coefficients reveal the level of model fitness and the effects of all the constraints on the outcome variable. In this regard, the proposed conceptual research model’s R-square (R2) estimated value is 0.794 (79.4%) at a p-value of 0.000. The indirect impacts of the model fitness R-square (R2) on the bases of the mediation variable is 0.728 (72.8%) at a p-value of 0.000.

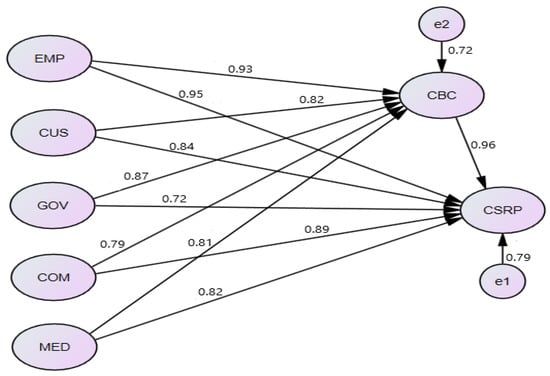

Furthermore, the derived variables regarding stakeholder pressure affect CSR practice in the setting of Chinese medium and large-scaled manufacturing businesses, as evidenced by the structural equation model and path modeling the goodness of fit. Mainly, employee (β = 0.952 ***), community (β = 0.894 ***), customer (β = 0.841 ***), media (β = 0.802 ***), and government (β = 0.702 ***) have a strong and positive direct effect on the dependent variable CSR practice, as illustrated in path diagram modeling in Figure 2. On the other hand, employees (β = 0.931 ***), government (β = 0.869 ***), customers (β = 0.815 ***), the media (β = 0.806 ***), and the community (β = 0.791 ***) all have an impact on the outcome of CSR activities, which is strongly supported and mediated by business culture at the estimate of β = 0.964 ***.

Figure 2.

Standardized path coefficients and significance of the structural equation model.

In order to identify the causal relationship, it is necessary to look the inferences on how the stakeholder pressures affect CSR practices on the bases of ceteris paribus. Assume that all other things being equal or held constant, as one unit of the independent variable improved by 1%, the dependent variable also increases by the same amount. When one unit of employee, customer, government, community, and media stakeholder pressure make a change, the outcome of the CSR practice is also directly shifted by one unit, significantly so.

In addition, when the mediation variable, CSR-oriented business culture, improved by one unit, indirectly, the deriving factors of stakeholder pressure were more likely affected, positively and significantly, by the mediation effects of the business culture, or they influence the adoption of the CSR activities, and vice versa. Therefore, employee, community, and customer stakeholder pressure are major factors on the influence of CSR practices, which has emanated from the direct interactions of Chinese enterprises. Comparatively, government, customer, and media are more likely the major forces that influence the Chinese enterprises indirectly.

In general, the mediation of a CSR-oriented business culture has a substantial multiplier effects while CSR activity in Chinese manufacturing enterprises is significantly higher in the community and customers, next to employee stakeholders, as the findings and interview analyses revealed. This implies that the interaction of Chinese enterprises is low with local government and media. In contrast, the local government, the community, and media stakeholder pressures is very low in pressurizing Chinses enterprises to give attention regarding the actions of CSR activities. As the findings revealed, the mediation of a CSR-oriented business culture has a strong multiplier effect, whereas CSR activity in Chinese manufacturing enterprises has a much higher significant impact on employee, community, and customer stakeholders. In contrast, this implies that Chinese business enterprises have weak engagement with local governments, community, and the media. On the other hand, the local government, community, and media stakeholder pressures have a quite low involvement and interaction in pressuring Chinese companies to pay attention to CSR initiatives.

4.7. The Level of Stakeholder Pressures and Enterprises CSR Trust

This study examined the various levels of stakeholder pressures in order to determine the extent to which Chinese firms and the deriving factors of stakeholder demands are satisfied. Firms’ trust and CSR practices highly affected through the extent of stakeholder pressures. When adopting the CSR measurement matrix to define stakeholders’ pressure, it is possible to determine whether the company’s activities build dialogue at a satisfactory level or if it needs to be improved [103]. In this regard, this study assessed and categorized the level of stakeholder pressures and enterprises CSR trust, as shown in Table 6.

Table 6.

The level of stakeholders and enterprises CSR trust.

4.8. Test of Hypothesis and Decisions

This research attempted to formulate and test six different hypotheses as per the aims of the study. Furthermore, all the hypotheses were generated based on various previous research findings’ discussion, which had some inconsistencies and disagreements. In this regard, the purpose of this study was to fill certain gaps by supporting hypothetical conclusions about how stakeholder pressures influence the adoption of CSR practices in Chinese medium and large manufacturing businesses in Ethiopia. As a result, all of the hypotheses that were determined and evaluated were recognized as significantly and positively supporting the success or failure of CSR outcome, as shown in Table 7.

Table 7.

Tests of hypotheses and decisions.

5. Conclusions

5.1. Conclusions

This paper investigates how stakeholder pressures influence CSR adoptions. The study also sought to see whether Chinese manufacturing enterprises that claim to be involved in CSR adoptions have better working conditions or closer interactions with CSR stakeholder groups. The findings of the study suggest to the following conclusions about the adoption of CSR initiatives and the factors that influence stakeholder pressures aligned with the research questions.

As the finding of the study show, the mediation of a CSR-oriented business culture has a strong multiplier effect, whereas the adoption of CSR activity in Chinese manufacturing enterprises has a much higher significant impact on employee, community, and customer stakeholders. In addition, Chinese manufacturing business enterprises have weak engagement with local governments, community, and the media. On the other hand, the local government, community, and media stakeholder pressures are quite low involvement and attachment in pressuring Chinese companies to pay attention to CSR initiatives.

The Chinese enterprises’ awareness of and engagement in CSR can be appreciated, though there are big variation between them on the issue. While some enterprises are well aware of the importance of CSR and demonstrate a higher degree of commitment, others are completely unaware that CSR may have a business justification, resulting in a low level of business commitment.

Despite the uncertainty among respondents in one of the four firms, managers in the other three had a positive attitude toward CSR, which may have led to the substantial CSR that in Chinese companies were found to be largely active.

Although Chinese enterprises have a high level of CSR activity in Ethiopia, much of the motivation appears to come from community and organizational stakeholders. The pressure from the Ethiopian government or the Ethiopian media has been determined to be negligible, which may have resulted in insignificant pressure on Chinese enterprises to increase their CSR efforts. The government is most likely focusing on environmental issues.

In general, the CSR involvement of Chinese manufacturing enterprises in Ethiopia is substantial as compared to other foreign companies operating in Ethiopia, according to the findings of this study. However, there is some evidence that Chinese enterprises are not well known for their CSR contributions as a result of poor communication with the public about what they are doing. On the other hand, companies from other countries operating in Ethiopia were found to be so creative in their communication that they gain a better level of awareness and credit for their CSR efforts, however symbolic they may be. In addition, according to the respondents’ interviews, the concept of CSR contributing to short-term performance is problematic, as it is has been generally assumed that CSR is in firms’ long-term interests.

5.2. Theoretical Implications

According to the study’s findings, a CSR-oriented business culture has a strong multiplier effect between stakeholder pressures and CSR adoptions, whereas CSR adoption in Chinese manufacturing businesses has a highly significant influence on employee, community, and consumer stakeholders. Furthermore, Chinese manufacturing enterprises have satisfactory influences and limited involvement in local governments, the community, and the media. Moreover, the findings are consistent and coincide with previous literature studies’ theoretical implications. The contribution of this study increases the theoretical concepts, mainly stakeholder pressure and CSR adoption. As a result, this research is important because it adds theoretical understanding to stakeholder and CSR adoption.

5.3. Practical Implications

The study’s findings have practical implications for overseas enterprises, government, employees, labor, policy makers, civic institutions, and media. According to the findings of this study, Chinese manufacturing enterprises differ in their willingness and attempts to invest resources in CSR initiatives in Ethiopia. The study is essential for enterprises to understand themselves and to get started on re-evaluating their CSR practices. The government can ratify the rules and practices that push for a state’s empowerment over social responsibility. The study also helps primary and secondary stakeholders where businesses operate to put pressure on businesses to engage in CSR activities.

5.4. Limitations and Directions for Further Research

This study has certain limitations. The study is only limited in Ethiopia, in the setting of five Chinese industrial parks, with the goal of focusing on Chinese medium and large-scale manufacturing enterprises only. As a result, the study is limited not to extend the sample, beyond manufacturing enterprises, to other types of overseas businesses from this research context. The other variables that influence stakeholder pressures on the CSR adoptions were not considered, such as suppliers, competitors, shareholders, creditors/banks, and civic organizations. Thus, further research is required in this area.

This study suggests some future research directions in order to increase stakeholder pressure on CSR adoptions in Ethiopia, particularly in the overseas manufacturing business and industrial parks investment. However, Chinese enterprises have played a vital role in Ethiopia’s holistic manufacturing development, benefiting from CSR through knowledge and technology transfer, as well as the country’s rapid economic progress and social capital changes. Still, CSR adoption is not strongly advocated and incorporated into enterprises at large, and companies’ perceptions of various stakeholders are unbalanced. As a result, both foreign and domestic enterprises in Ethiopia should promote their CSR policies and practices to various stakeholders in order to build shared value and enhance awareness about what they are doing, including CSR-oriented business culture collaborations. Ethiopia’s government should adopt strict rules and regulations to ensure that enterprises are appropriately undertaking CSR initiatives. Thus, more research in this area is required in the future.

Author Contributions

Conceptualization, design and outline, M.Y., H.S. and G.A.T.; methodology, software, validation, and formal analysis, investigation, resources, data curation, wrote—original draft preparation, G.A.T.; critical revision—review, editing, supervision, and final approval, M.Y. and H.S. All authors have read and agreed to the published version of the manuscript.

Funding

This study has no received external funding sources.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The corresponding author will provide all of the necessary data to support the research outcome.

Acknowledgments

The authors express their gratitude to all those who took part in the survey and provided valuable feedback. We thank all of the support given from Wuhan University of Technology’s School of Management.

Conflicts of Interest

The authors declared no conflict of interest.

Originality Statement

We confirm that it is our own original work using authors’ own knowledge, containing no materials previously published by another person. The authors also collected the required data, information, materials, and analyzed them in a unique consideration of conceptual research model in Chinese manufacturing enterprise in the Ethiopia.

Appendix A

Table A1.

Measurements of Construct Items.

Table A1.

Measurements of Construct Items.

| Variables | Items | Source |

|---|---|---|

| CSR Practices | (1) Our company implements special programs to minimize its negative impact on the natural environment; (2) The management of our enterprise is primarily concerned employees’ needs and wants. (3) Our company contributes to campaigns and projects that promote the safety of society. (4) Our company targets sustainable growth that considers future generations. | [92] |

| Employee | (1) Our managers and employees perceive CSR as an important mechanism potentially contributing to the creation of corporate value. (2) Our managers and employees perceive that CSR enhances competitive advantage, and eventually improves the economic value of the firm. (3) Our managers and employees believe enterprises need to contribute to national and local levels, societies and markets. (4) Our managers and employees believe being ethical and socially responsible is the most important thing a firm should do. | [21,47] |

| Customer | (1) Respects customer rights beyond the legal requirements. (2) Customer satisfaction is highly important for our company. (3) Treats customers’ complaints or suggestions seriously. (4) Provides full and accurate information about its products to its customers. | [83] |

| Government | (1) The government has stricter regulations to protect the consumers. (2) The government has effective regulations to encourage firms to improve their product and services quality. (3) There are complete laws and regulations to ensure fair competition. | [67] |

| Community | (1) Communities expect companies to contribute to society development by volunteering time and effort to local activities. (2) Local communities expect companies to contribute to society development by getting involved in community event in non-financial ways. (3) Local communities expect companies to contribute to society development by providing jobs and treating their employees well. | [21] |

| Media | (1) Media plays a pivotal role in maintaining and improving public relations between firms and consumers in the local market. (2) Mass media has a strong power in shaping enterprise image in the local market. (3) Compared with other countries, mass media in Ethiopia pays more attention to the societal role of enterprises in the local market. | [21] |

| CSR-oriented Business Culture | (1) The employees have a strong degree of awareness on the CSR (2) Our leader believes and values the adoption of CSR (3) Our organization develops strategy on the CSR activities (4) Our organization has the CSR-training program for the employees (5) Our organization keeps a special department for CSR management | [2] |

References

- Carroll, A.B.; Shabana, K.M. The Business Case for Corporate Social Responsibility: A Review of Concepts, Research and Practice. Int. J. Manag. Rev. 2010, 12, 85–105. [Google Scholar] [CrossRef]

- Yu, Y.; Choi, Y. Stakeholder pressure and CSR adoption: The mediating role of organizational culture for Chinese companies. Soc. Sci. J. 2014, 53, 226–234. [Google Scholar] [CrossRef]

- Newman, C.; Rand, J.; Tarp, F.; Trifkovic, N. Corporate Social Responsibility in a Competitive Business Environment. J. Dev. Stud. 2020, 56, 1455–1472. [Google Scholar] [CrossRef]

- Kowalczyk, R.; Kucharska, W. Corporate social responsibility practices incomes and outcomes: Stakeholders’ pressure, culture, employee commitment, corporate reputation, and brand performance. A Polish–German cross-country study. Corp. Soc. Responsib. Environ. Manag. 2019, 27, 595–615. [Google Scholar] [CrossRef]

- Bonsu, S. Deceptive Advertising: A Corporate Social Responsibility Perspective. Int. J. Health Econ. Dev. 2020, 6, 1–15. [Google Scholar]

- Gulavani, S.; Nayak, N.; Nayak, M. Corporate Social Responsibility Issues and Challenges in India. Int. J. Commer. IT Soc. Sci. 2016, 3, 22–27. [Google Scholar]

- Morsing, M.; Schultz, M. Corporate social responsibility communication: Stakeholder information, response and involvement strategies. Bus. Ethics A Eur. Rev. 2006, 15, 323–338. [Google Scholar] [CrossRef]

- Xia, B.; Olanipekun, A.; Chen, Q.; Xie, L.; Liu, Y. Conceptualising the state of the art of corporate social responsibility (CSR) in the construction industry and its nexus to sustainable development. J. Clean. Prod. 2018, 18, 340–353. [Google Scholar] [CrossRef]

- Chiou, C.L.; Shu, P.G. How does foreign pressure affect a firm’s corporate social performance? Evidence from listed firms in Taiwan. J. Multinatl. Financ. Manag. 2019, 51, 1–22. [Google Scholar] [CrossRef]

- Kim, C.; Kim, J.; Marshall, R.; Afzali, H. Stakeholder influence, institutional duality, and CSR involvement of MNC subsidiaries. J. Bus. Res. 2018, 91, 40–47. [Google Scholar] [CrossRef]

- Berman, S.L.; Wicks, A.C.; Kotha, S.; Jones, T.M. Does stakeholder orientation matter? The relationship between stakeholder management models and firm financial performance. Acad. Manag. J. 1999, 42, 488–506. [Google Scholar]

- Marquis, C.; Zhang, J.; Zhou, Y. Regulatory Uncertainty and Corporate Responses to Environmental Protection in China. Pestic. Outlook 2014, 54, 39–63. [Google Scholar] [CrossRef]

- Toit, E.d.; Lekoloane, K. Corporate social responsibility and financial performance: Evidence from the Johannesburg Stock Exchange, South Africa. Comp. Econ. Res. 2018, 21, 11. [Google Scholar]

- Khuong, M.N.; Truong an, N.K.; Thanh Hang, T.T. Stakeholders and Corporate Social Responsibility (CSR) programme as key sustainable development strategies to promote corporate reputation—Evidence from vietnam. Cogent Bus. Manag. 2021, 8, 1917333. [Google Scholar] [CrossRef]

- Freeman, R.E.; Velamuri, S.R. A New Approach to CSR: Company Stakeholder Responsibility. Corp. Soc. Responsib. 2006, 1, 9–23. [Google Scholar]

- Soobaroyen, T.; Sheik-Ellahi, A. A case study on the influence of corporate governance beyond the boardroom: Perceptions from business unit managers. Corp. Gov. 2008, 8, 179–190. [Google Scholar] [CrossRef]

- Yoon, B.; Chung, Y. The effects of corporate social responsibility on firm performance: A stakeholder approach. J. Hosp. Tour. Manag. 2018, 37, 89–96. [Google Scholar] [CrossRef]

- Awan, A.; Murillo, D.; Mellen, T. CSR and battered women: Stakeholder engagement beyond salience? Bus. Res. Q. 2021, 24, 160–173. [Google Scholar] [CrossRef]

- Husillos, J. A Stakeholder-Theory Approach to Environmental Disclousures by Small and Medium Enterprises (SMES). Rev. Contab. 2008, 11, 125–156. [Google Scholar]

- Rueda-Manzanares, A.; Aragón-Correa, J.A.; Sharma, S. The influence of stakeholders on the environmental strategy of service firms: The moderating effects of complexity, uncertainty and munificence. Br. J. Manag. 2008, 19, 185–203. [Google Scholar] [CrossRef]

- Park, B.; Ghauri, P.N. Determinants influencing CSR practices in small and medium sized MNE subsidiaries: A stakeholder perspective. J. World Bus. 2015, 50, 192–204. [Google Scholar] [CrossRef]

- Robertson, D.C. Corporate social responsibility and different stages of economic development: Singapore, Turkey, and Ethiopia. J. Bus. Ethics 2009, 88, 617–633. [Google Scholar] [CrossRef]

- Mulugeta, A. Determinants of Corporate Social Responsibility Practice of Manufacturing Firms in Dire Dawa Administration. Dev. Ctry. Stud. 2020, 10, 21–35. [Google Scholar]

- Deyassa, K. CSR From Ethiopian Perspective. Int. J. Sci. Technol. Res. 2016, 5, 299–328. [Google Scholar] [CrossRef]

- Mathias Nigatu Bimir Corporate Social Responsibility Learning in the Ethiopian Leather and Footwear Industry. Int. J. Sci. Eng. Res. 2015, 7, 1–14.

- Chakrabarty, M. Ethiopia—China Economic Relations: A Classic Win-Win Situation ? Pluto J. 2016, 7, 226–248. [Google Scholar] [CrossRef]

- Nicolas, F. Chinese Investors in Ethiopia: The Perfect Match? Ifri Center for Aisian Studies: Ifri, France, 2017; pp. 4–42. Available online: https://www.ifri.org/sites/default/files/atoms/files/nicolas_chinese_investors_ethiopia_2017.pdf (accessed on 8 August 2021).

- Mohammadi, D. Corporate Social Responsibility along the Chinese Financed Railway Mega-Project in East Africa. Res. Brief 2020, 3, 1–7. [Google Scholar]

- Khan, S.; Al-Maimani, K.; Al-Yafi, W. Exploring Corporate Social Responsibility in Saudi Arabia: The Challenges Ahead. J. Leadersh. Account. Ethics 2013, 10, 65–78. [Google Scholar]

- Perrini, F.; Russo, A.; Tencati, A. CSR Strategies of SMEs and Large Firms. Evidence from Italy. J. Bus. Ethics 2007, 74, 285–300. [Google Scholar] [CrossRef]

- CEC. A Renewed EU Strategy 2011-14 for Corporate Social Responsibility; European Commision: Brussels, Belgium, 2011; Volume 13. [Google Scholar]

- Kakabadse, N.K.; Rozuel, É.; Lee-Davies, L. Corporate social responsibility and stakeholder approach: A conceptual review. Int. J. Bus. Gov. Ethics 2005, 4, 277–302. [Google Scholar] [CrossRef]

- Barrena Martínez, J.; López Fernández, M.; Romero Fernández, P.M. Corporate social responsibility: Evolution through institutional and stakeholder perspectives. Eur. J. Manag. Bus. Econ. 2016, 25, 8–14. [Google Scholar] [CrossRef]

- Li, J.C.; Benamraoui, A.; Shah, N.; Mathew, S. Dynamic Capability and Strategic Corporate Social Responsibility Adoption: Evidence from China. Sustainability 2021, 13, 5333. [Google Scholar] [CrossRef]

- Luchenciuc, E.-G.; Rus, M.; Tasente, T. Organizational communication and corporate social responsibility. Case study: Romanian vs. International CSR. Tech. Soc. Sci. J. 2020, 3, 76–81. [Google Scholar]

- Chouaibi, Y.; Rossi, M. The Effect of Corporate Social Responsibility and the Executive Compensation on Implicit Cost of Equity: Evidence from French ESG Data. Sustainability 2021, 13, 11510. [Google Scholar] [CrossRef]

- Xie, L.; Xu, T.; Le, Y.; Chen, Q.; Xia, B.; Skitmore, M. Understanding the CSR Awareness of Large Construction Enterprises in China. Hindawi Adv. Civ. Eng. 2020, 2020, 8866511. [Google Scholar] [CrossRef]

- Park, B.I.; Chidlow, A.; Choi, J. Corporate social responsibility: Stakeholders influence on MNEs’ activities. Int. Bus. Rev. 2014, 23, 966–980. [Google Scholar] [CrossRef]

- Nichols, P.M.; Dowden, P.E. Maximizing stakeholder trust as a tool for controlling corruption. Crime Law Soc. Chang. 2018, 71, 171–195. [Google Scholar] [CrossRef]

- Lucchini, A.; Moisello, A.M. Stakeholders’ Pressure and CSR Engagement. A Case in the Apparel Sector. Am. J. Ind. Bus. Manag. 2019, 9, 169–190. [Google Scholar] [CrossRef]

- Rhee, Y.P.; Park, C.; Petersen, B. The Effect of Local Stakeholder Pressures on Responsive and Strategic CSR Activities. Bus. Soc. 2018, 60, 582–613. [Google Scholar] [CrossRef]

- Mohammed, W.F.; Xiao, A.; Hilton, E. A Critical Analysis of Corporate Social Responsibility in Ghana’s Telecommunications Industry. S. Afr. J. Commun. Theory Res. 2019, 45, 4–22. [Google Scholar] [CrossRef]

- Žukauskas, P.; Vveinhardt, J.; Andriukaitienė, R. Philosophy and Paradigm of Scientific Research. Manag. Cult. Corp. Soc. Responsib. 2018, 8, 2–17. [Google Scholar]

- Rupp, D.E.; Ganapathi, J.; Aguilera, R.V.; Williams, C.A. Employee reactions to corporate social responsibility: An organizational justice framework. J. Organ. Behav. 2006, 27, 537–543. [Google Scholar] [CrossRef]

- de Chernatony, L.; Harris, F. Developing Corporate Brands Through Considering Internal and External Stakeholders. Corp. Reput. Rev. 2000, 3, 268–274. [Google Scholar] [CrossRef]

- Turker, D. Measuring corporate social responsibility: A scale development study. J. Bus. Ethics 2009, 85, 411–427. [Google Scholar] [CrossRef]

- Sarfraz, M.; Qun, W.; Abdullah, M.I.; Alvi, A.T. Employees’ Perception of Corporate Social Responsibility Impact on Employee Outcomes: Mediating Role of Organizational Justice for (SMEs). Sustainability 2018, 10, 2429. [Google Scholar] [CrossRef]

- Begum, H.; Doyduk, B. Corporte Social Responsibility from Employees ’ Perspective. Turk. Stud.-Soc. Sci. 2020, 15, 160–172. [Google Scholar]

- Adu-Gyamfi, M.; He, Z.; Nyame, G.; Boahen, S.; Frempong, M.F. Effects of Internal CSR Activities on Social Performance: The employee perspective. Sustainability 2021, 13, 6235. [Google Scholar] [CrossRef]

- Wang, W.; Fu, Y.; Qiu, H.; Moore, J.H.; Wang, Z. Corporate social responsibility and employee outcomes: A moderated mediation model of organizational identification and moral identity. Front. Psychol. 2017, 8, 1906. [Google Scholar] [CrossRef] [PubMed]

- Jung, H.J.; Kim, D.O. Good Neighbors but Bad Employers: Two Faces of Corporate Social Responsibility Programs. J. Bus. Ethics 2016, 138, 295–310. [Google Scholar] [CrossRef]

- Brieger, S.A.; Anderer, S.; Fröhlich, A.; Bäro, A.; Meynhardt, T. Too Much of a Good Thing? On the Relationship Between CSR and Employee Work Addiction. J. Bus. Ethics 2017, 166, 311–329. [Google Scholar] [CrossRef]

- Zhang, Q.; Ahmad, S. Analysis of Corporate Social Responsibility Execution Effects on Purchase Intention with the Moderating Role of Customer Awareness. Sustainability 2021, 13, 4548. [Google Scholar] [CrossRef]

- Martos-Pedrero, A.; Cortés-García, F.J.; Jiménez-Castillo, D. The Relationship between Social Responsibility and Business Performance: An Analysis of the Agri-Food Sector of Southeast Spain. Sustainability 2019, 11, 6390. [Google Scholar] [CrossRef]

- Raza, A.; Saeed, A.; Iqbal, M.K.; Saeed, U.; Sadiq, I.; Faraz, N.A. Linking Corporate Social Responsibility to Customer Loyalty through Co-Creation and Customer Company Identification: Exploring Sequential Mediation Mechanism. Sustainability 2020, 12, 2525. [Google Scholar] [CrossRef]