Noise and Financial Stylized Facts: A Stick Balancing Approach

Abstract

1. Introduction

2. Materials and Methods

- For , there is a critical threshold for (specifically for and for ), below which the sticks quickly falls, thus the point identified by the initial conditions and in phase space results to be unstable, i.e., a repeller. Above the threshold, the system becomes stable, although the equilibrium point may not coincide with the initial one, and spiral trajectories can be observed approaching the node (in this case, of course, the stick never falls). In other words, in correspondence of the critical threshold , there is a sudden transition from a completely disordered regime to a completely ordered one.

- For , a third type of regime appears. Below a different critical threshold (which for becomes ), we always observe a repeller in the phase space, and the sticks always falls; on the other hand, for , the stick never falls, and we again find a spiral node; finally, for , the stick falls again, but we now observe a spiral repeller.

- For we do not find anymore the regime where the initial point is a spiral node. The stick always falls and we pass from finding a repeller to find a spiral repeller in phase space in correspondence of a critical value starting from and increasing as increases. For and for values of , the transition to spiral repeller is no longer observed.

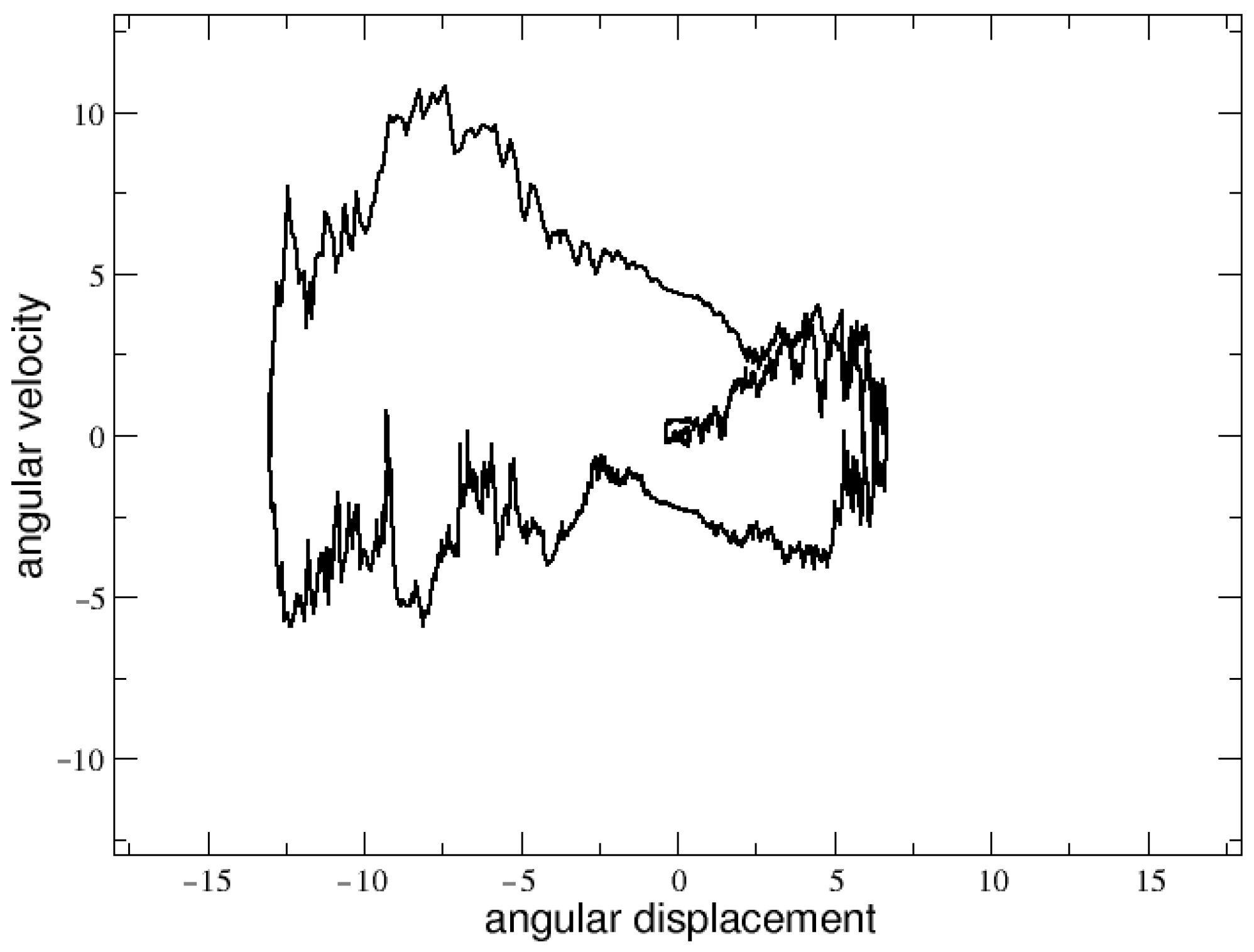

- For values of less than 5, and for less than 4, the stick immediately falls for any initial condition, thus showing repeller behavior. Within the small range , more interesting dynamics start to be observed in the phase space. An example is shown in Figure 1 for and . Finally, for larger values of , the stick still falls but the representative point of the system barely moves from its initial position in the phase space.

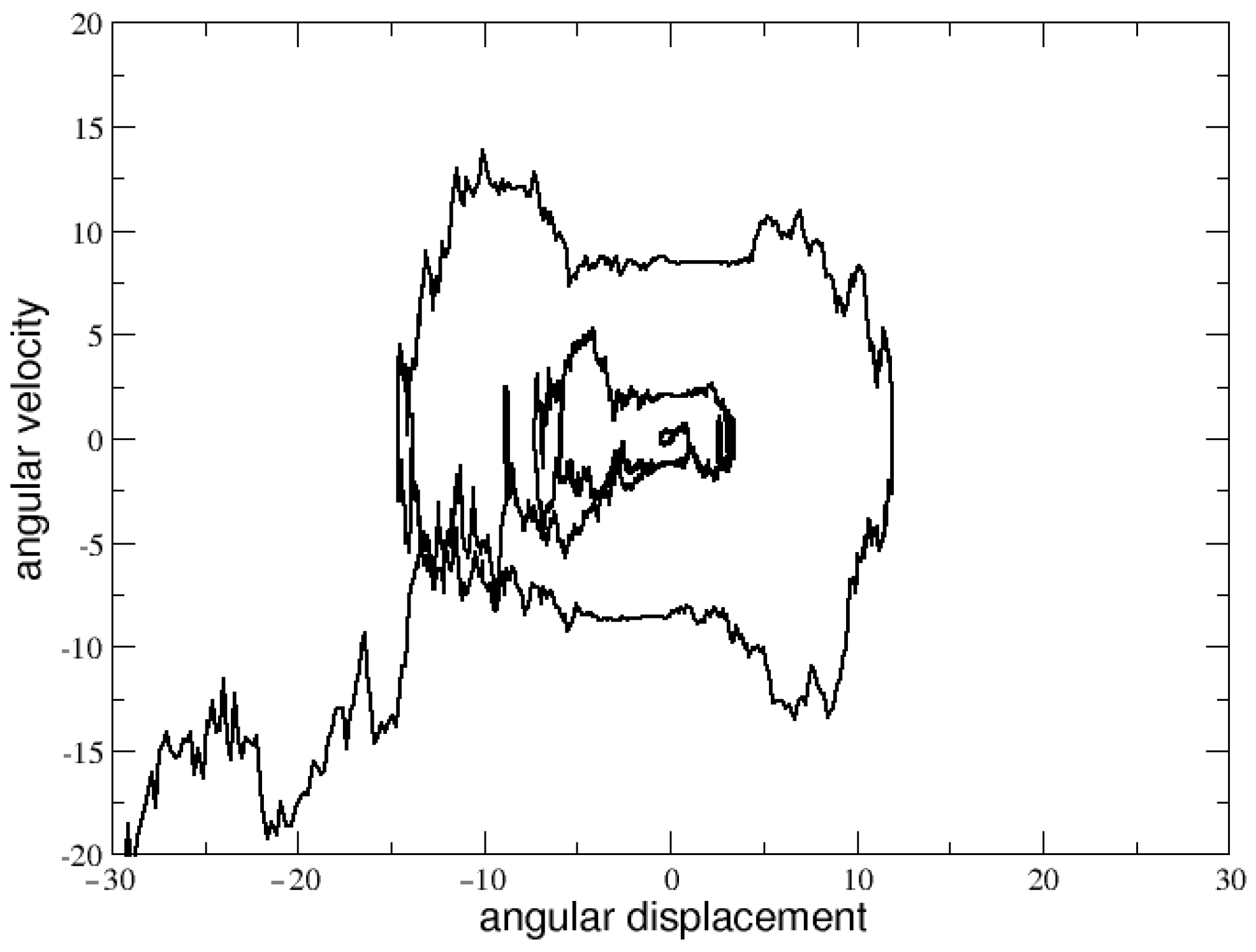

- For , the dynamics start to become very sensitive to the noise, for any . Generally, as increases, a spiral-like repelling behavior emerges for values of . Regardless, for and for , a window of complex behavior does appear, with longer trajectories more suitable for allowing statistical analysis.

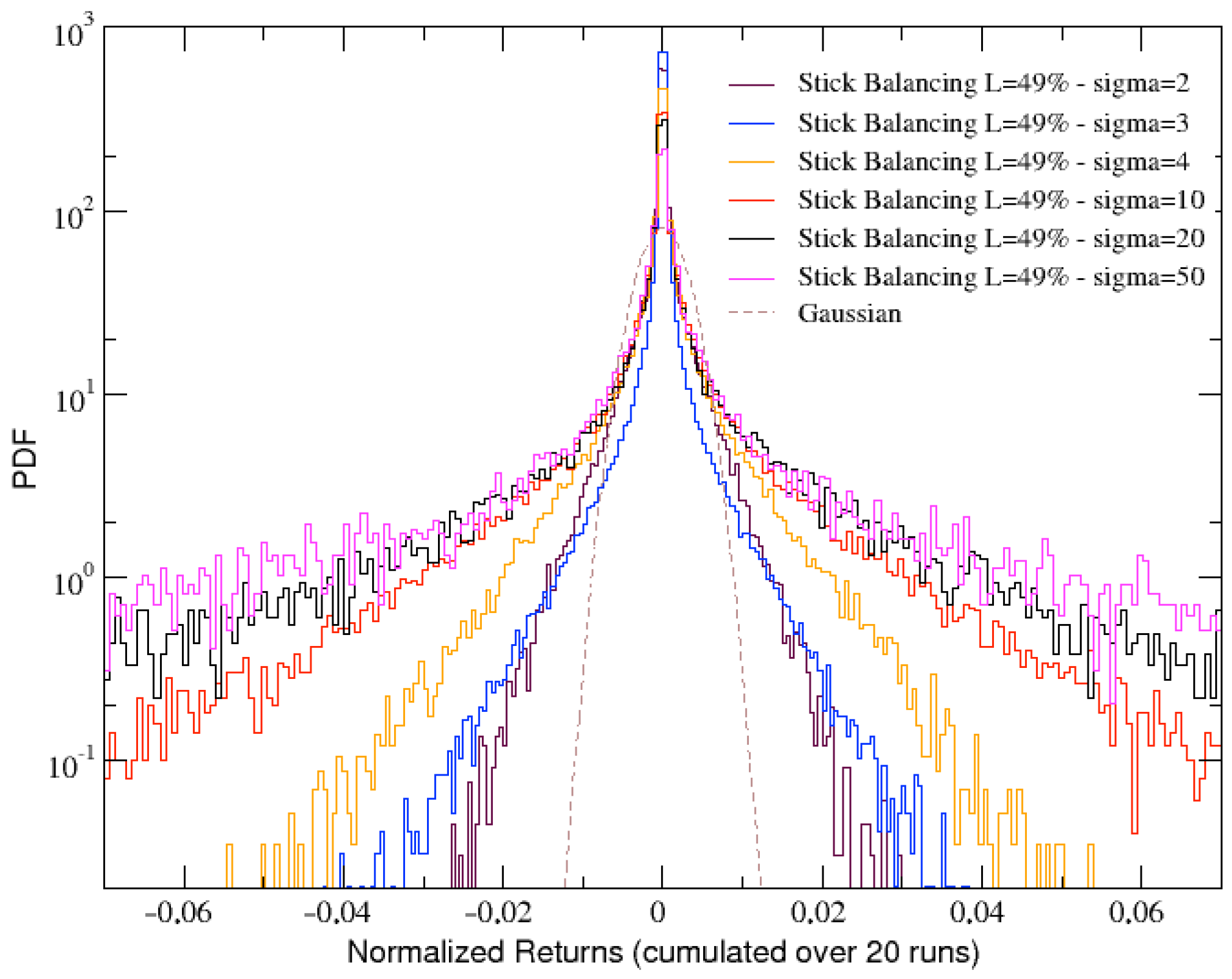

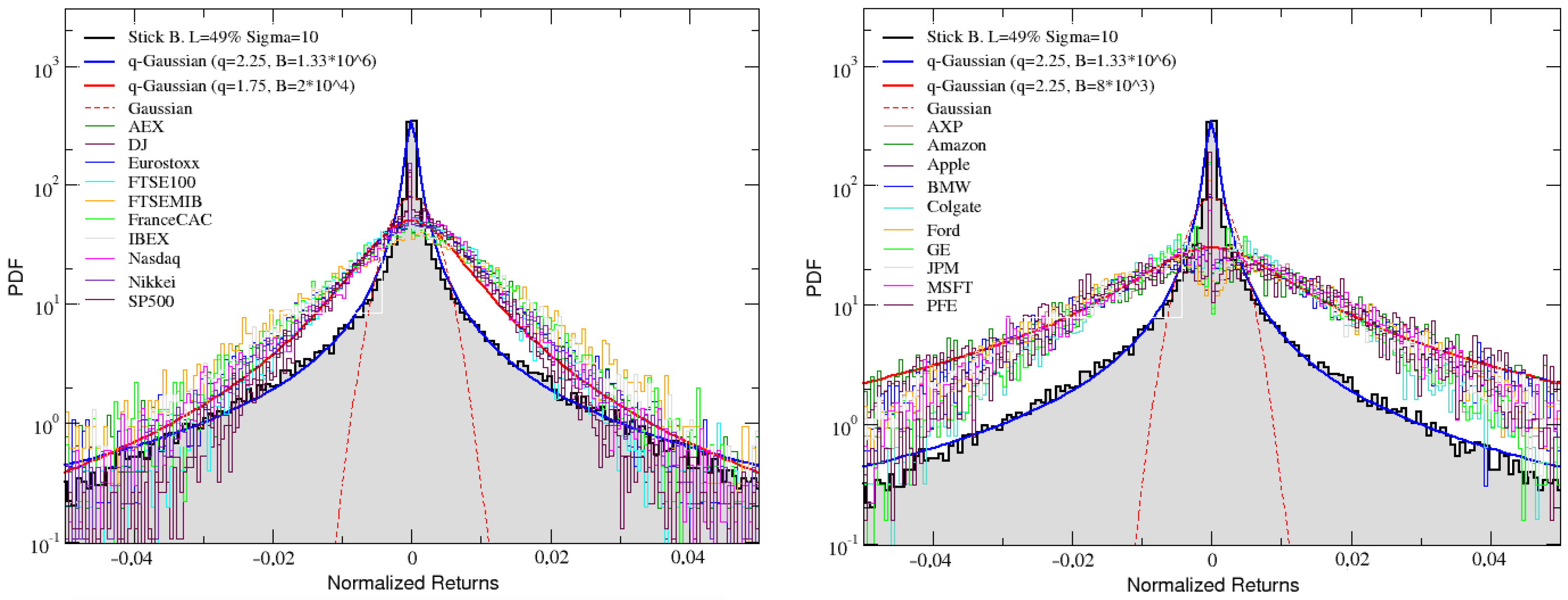

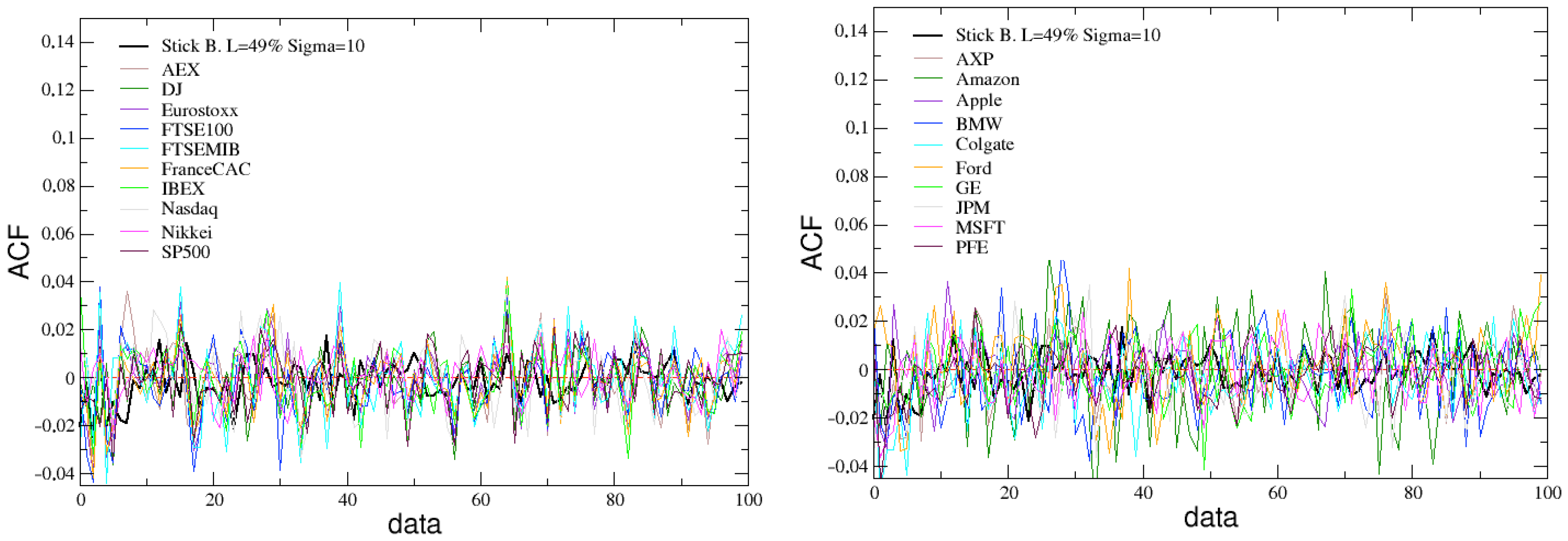

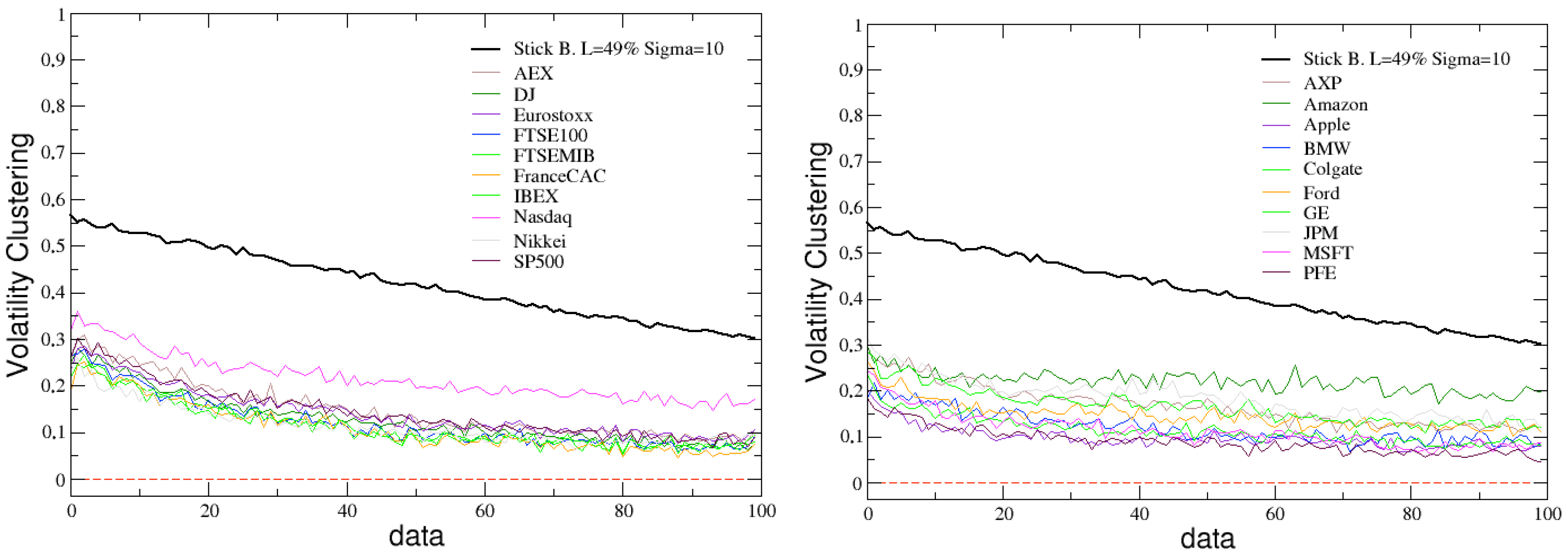

3. Results

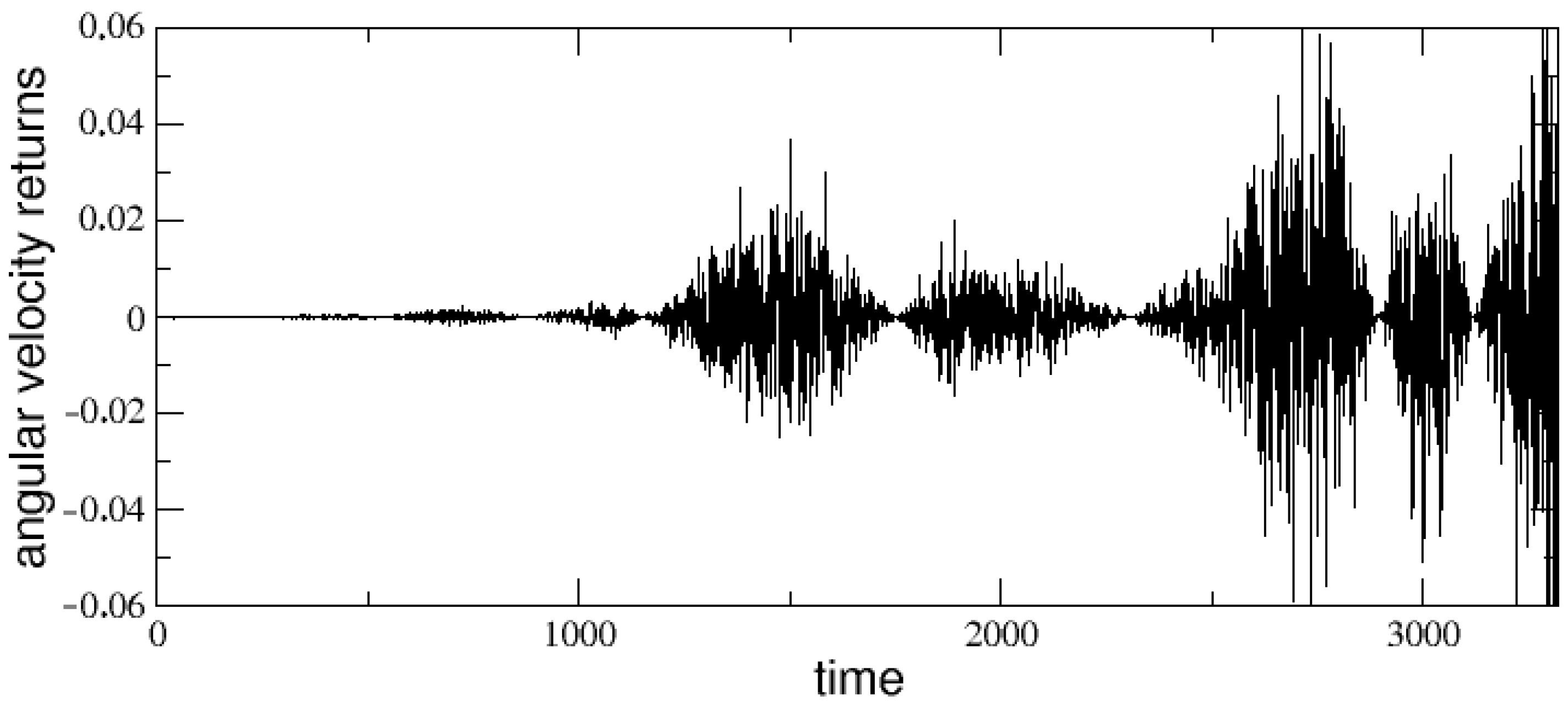

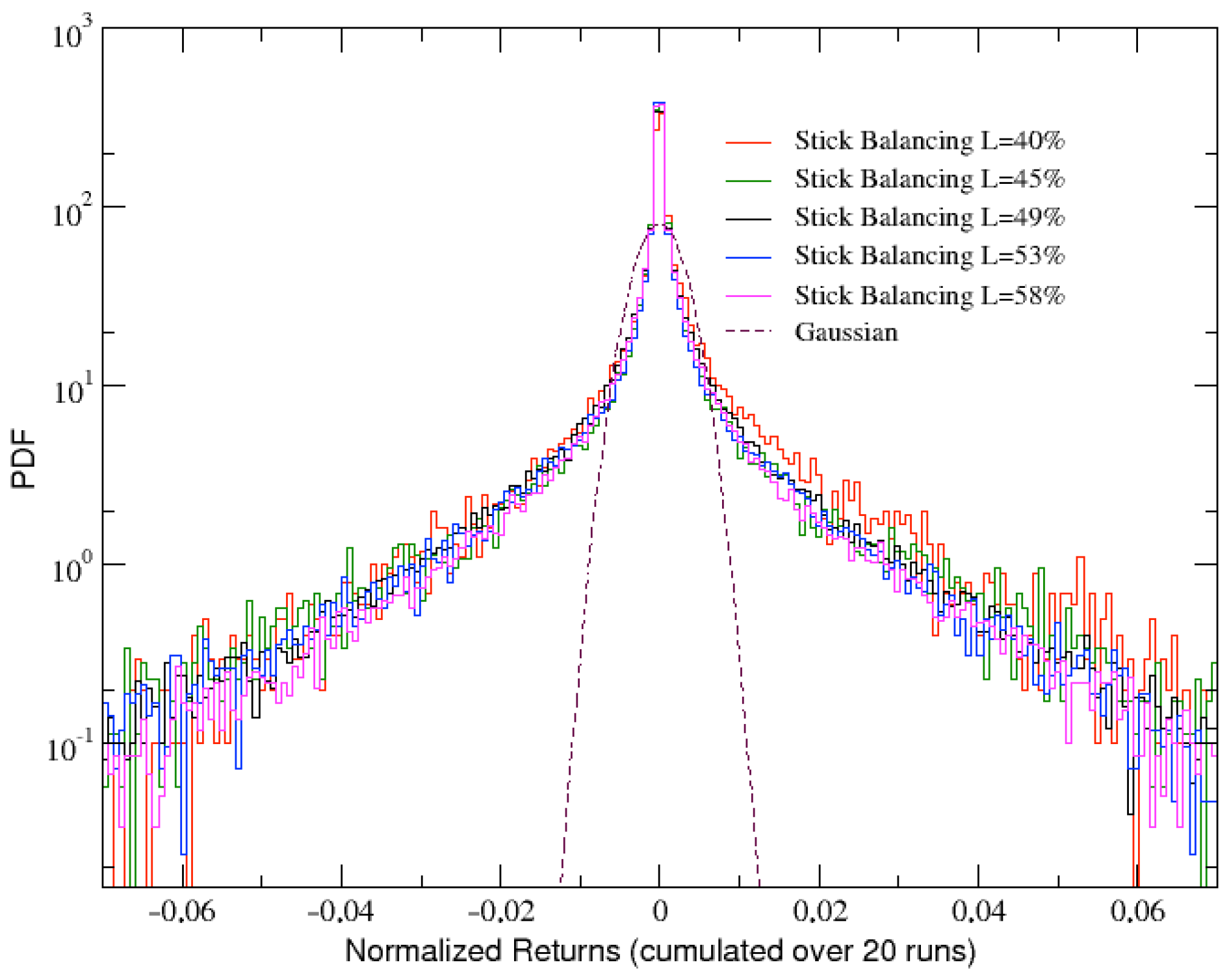

Empirical Data Collection and Comparison with Simulated Data

4. Discussion and Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Mantegna, R.N.; Spagnolo, B. Noise enhanced stability in an unstable system. Phys. Rev. Lett. 1996, 76, 563. [Google Scholar] [CrossRef] [PubMed]

- Kirkpatrick, S.; Gelatt, C.D., Jr.; Vecchi, M.P. Optimization by simulated annealing. Science 1983, 220, 671–680. [Google Scholar] [CrossRef] [PubMed]

- Benzi, R.; Parisi, G.; Sutera, A.; Vulpiani, A. Stochastic resonance in climatic change. Tellus 1982, 34, 10–16. [Google Scholar] [CrossRef]

- Gammaitoni, L.; Hänggi, P.; Jung, P.; Marchesoni, F. Stochastic resonance. Rev. Mod. Phys. 1998, 70, 223. [Google Scholar] [CrossRef]

- Caruso, F.; Huelga, S.F.; Plenio, M.B. Noise-enhanced classical and quantum capacities in communication networks. Phys. Rev. Lett. 2010, 105, 190501. [Google Scholar] [CrossRef]

- Van den Broeck, C.; Parrondo, J.; Toral, R. Noise-induced nonequilibrium phase transition. Phys. Rev. Lett. 1994, 73, 3395. [Google Scholar] [CrossRef]

- Agudov, N.; Spagnolo, B. Noise-enhanced stability of periodically driven metastable states. Phys. Rev. E 2001, 64, 035102. [Google Scholar] [CrossRef]

- Söderlund, G. Positive effects of noise on cognitive performance: Explaining the moderate brain arousal model. In Proceedings of the 9th Congress of the International Comisssion on the Biological Effects of Noise, Mashantucket, CT, USA, 21–25 July 2008; Leibniz Gemeinschaft: Berlin, Germany, 2008; pp. 378–386. [Google Scholar]

- Söderlund, G.B.; Sikström, S.; Loftesnes, J.M.; Sonuga-Barke, E.J. The effects of background white noise on memory performance in inattentive school children. Behav. Brain Funct. 2010, 6, 1–10. [Google Scholar] [CrossRef]

- Jafari, M.J.; Khosrowabadi, R.; Khodakarim, S.; Mohammadian, F. The effect of noise exposure on cognitive performance and brain activity patterns. Open Access Maced. J. Med Sci. 2019, 7, 2924. [Google Scholar] [CrossRef]

- McDonnell, M.D.; Ward, L.M. The benefits of noise in neural systems: Bridging theory and experiment. Nat. Rev. Neurosci. 2011, 12, 415–425. [Google Scholar] [CrossRef]

- Deco, G.; Rolls, E.T.; Romo, R. Stochastic dynamics as a principle of brain function. Prog. Neurobiol. 2009, 88, 1–16. [Google Scholar] [CrossRef] [PubMed]

- Chin, A.; Datta, A.; Caruso, F.; Huelga, S.; Plenio, M. Noise-assisted energy transfer in quantum networks and light-harvesting complexes. New J. Phys 2010, 12, 065002. [Google Scholar] [CrossRef]

- Pluchino, A.; Rapisarda, A.; Garofalo, C. The Peter Principle Revisited: A Computational Study. Phys. A 2010, 389, 467–472. [Google Scholar] [CrossRef]

- Pluchino, A.; Rapisarda, A.; Garofalo, C.; Spagano, S.; Caserta, M. Accidental Politicians: How Randomly Selected Legislators Can Improve Parliament Efficiency. Phys. A 2011, 390, 3944–3954. [Google Scholar] [CrossRef]

- Biondo, A.E.; Pluchino, A.; Rapisarda, A. Micro and macro benefits of random investments in financial markets. Contemp. Phys. 2014, 55, 318–334. [Google Scholar] [CrossRef][Green Version]

- Gao, X.; Ladley, D. Noise trading and market stability. Eur. J. Financ. 2022, 28, 1283–1301. [Google Scholar] [CrossRef]

- Biondo, A.E.; Pluchino, A.; Rapisarda, A.; Helbing, D. Are random trading strategies more successful than technical ones? PLoS ONE 2013, 8, e68344. [Google Scholar] [CrossRef]

- Biondo, A.E.; Pluchino, A.; Rapisarda, A. The beneficial role of random strategies in social and financial systems. J. Stat. Phys. 2013, 151, 607–622. [Google Scholar] [CrossRef]

- Biondo, A.E.; Pluchino, A.; Rapisarda, A.; Helbing, D. Reducing financial avalanches by random investments. Phys. Rev. E 2013, 88, 062814. [Google Scholar] [CrossRef]

- Langton, C.G. Computation at the edge of chaos: Phase transitions and emergent computation. Phys. D Nonlinear Phenom. 1990, 42, 12–37. [Google Scholar] [CrossRef]

- Kitzbichler, M.G.; Smith, M.L.; Christensen, S.R.; Bullmore, E. Broadband criticality of human brain network synchronization. PLoS Comput. Biol. 2009, 5, e1000314. [Google Scholar] [CrossRef] [PubMed]

- Toker, D.; Pappas, I.; Lendner, J.D.; Frohlich, J.; Mateos, D.M.; Muthukumaraswamy, S.; Carhart-Harris, R.; Paff, M.; Vespa, P.M.; Monti, M.M.; et al. Consciousness is supported by near-critical slow cortical electrodynamics. Proc. Natl. Acad. Sci. USA 2022, 119, e2024455119. [Google Scholar] [CrossRef] [PubMed]

- Luppi, A.I.; Craig, M.M.; Pappas, I.; Finoia, P.; Williams, G.B.; Allanson, J.; Pickard, J.D.; Owen, A.M.; Naci, L.; Menon, D.K.; et al. Consciousness-specific dynamic interactions of brain integration and functional diversity. Nat. Commun. 2019, 10, 1–12. [Google Scholar] [CrossRef]

- Cohen, B. The Edge of Chaos: Financial Booms, Bubbles, Crashes and Chaos; Wiley: New York, NY, USA, 2002. [Google Scholar]

- Zetie, K. Adventures on the edge of chaos. Quant. Financ. 2004, 4, C24. [Google Scholar] [CrossRef]

- Litimi, H.; BenSaida, A.; Belkacem, L.; Abdallah, O. Chaotic behavior in financial market volatility. J. Risk Forthcom. 2018, 21, 27–53. [Google Scholar] [CrossRef]

- Peters, E.E. Chaos and Order in the Capital Markets: A New View of Cycles, Prices, and Market Volatility; John Wiley & Sons: New York, NY, USA, 1996. [Google Scholar]

- Dominique, C. How Market Economies Come to Live and Grow on the Edge of Chaos; University Library of Munich: Munich, Germany, 2015. [Google Scholar]

- Sornette, D. Critical Phenomena in Natural Sciences: Chaos, Fractals, Selforganization and Disorder: Concepts and Tools; Springer Science & Business Media: Berlin, Germany, 2006. [Google Scholar]

- Cocchi, L.; Gollo, L.L.; Zalesky, A.; Breakspear, M. Criticality in the brain: A synthesis of neurobiology, models and cognition. Prog. Neurobiol. 2017, 158, 132–152. [Google Scholar] [CrossRef]

- Shew, W.L.; Plenz, D. The functional benefits of criticality in the cortex. Neuroscientist 2013, 19, 88–100. [Google Scholar] [CrossRef]

- Gabaix, X.; Gopikrishnan, P.; Plerou, V.; Stanley, H.E. A theory of power-law distributions in financial market fluctuations. Nature 2003, 423, 267–270. [Google Scholar] [CrossRef]

- Gabaix, X. Power laws in economics and finance. Annu. Rev. Econ. 2009, 1, 255–294. [Google Scholar] [CrossRef]

- Lux, T.; Alfarano, S. Financial power laws: Empirical evidence, models, and mechanisms. Chaos Solitons Fractals 2016, 88, 3–18. [Google Scholar] [CrossRef]

- Giannotti, F.; Pedreschi, D.; Pentland, A.; Lukowicz, P.; Kossmann, D.; Crowley, J.; Helbing, D. A planetary nervous system for social mining and collective awareness. Eur. Phys. J. Spec. Top. 2012, 214, 49–75. [Google Scholar] [CrossRef]

- Bradley, C. Breaking up is hard to do: The interconnection problem in financial markets and financial regulation, a European (banking) union perspective. Tex. Int’l LJ 2014, 49, 271. [Google Scholar]

- Viñals, J.; Tiwari, S.; Blanchard, O. The IMF’S Financial Surveillance Strategy; International Monetary Fund: Washington, DC, USA, 2012. [Google Scholar]

- Awrey, D. Complexity, innovation, and the regulation of modern financial markets. Harv. Bus. L. Rev. 2012, 2, 235. [Google Scholar] [CrossRef]

- El Alaoui, A.O.; Dewandaru, G.; Rosly, S.A.; Masih, M. Linkages and co-movement between international stock market returns: Case of Dow Jones Islamic Dubai Financial Market index. J. Int. Financ. Mark. Inst. Money 2015, 36, 53–70. [Google Scholar] [CrossRef]

- Tokic, D. Emerging markets before the 1997 Asia Pacific financial crisis. Asia Pac. Bus. Rev. 2003, 9, 105–115. [Google Scholar] [CrossRef]

- Giovannetti, G.; Velucchi, M. A spillover analysis of shocks from US, UK and China on African financial markets. Rev. Dev. Financ. 2013, 3, 169–179. [Google Scholar] [CrossRef]

- Berument, H.; Ince, O. Effect of S&P500’s return on emerging markets: Turkish experience. Appl. Financ. Econ. Lett. 2005, 1, 59–64. [Google Scholar]

- Cheung, Y.L.; Mak, S.C. The international transmission of stock market fluctuation between the developed markets and the Asian—Pacific markets. Appl. Financ. Econ. 1992, 2, 43–47. [Google Scholar] [CrossRef]

- Cha, B.; Oh, S. The relationship between developed equity markets and the Pacific Basin’s emerging equity markets. Int. Rev. Econ. Financ. 2000, 9, 299–322. [Google Scholar] [CrossRef]

- Eun, C.S.; Shim, S. International transmission of stock market movements. J. Financ. Quant. Anal. 1989, 24, 241–256. [Google Scholar] [CrossRef]

- Xu, Y.; Corbett, J. Using Network Method to Measure Financial Interconnection; Technical Report; National Bureau of Economic Research: Cambridge, MA, USA, 2019. [Google Scholar]

- Wang, G.J.; Yi, S.; Xie, C.; Stanley, H.E. Multilayer information spillover networks: Measuring interconnectedness of financial institutions. Quant. Financ. 2021, 21, 1163–1185. [Google Scholar] [CrossRef]

- Ashraf, B.N. Stock markets’ reaction to COVID-19: Cases or fatalities? Res. Int. Bus. Financ. 2020, 54, 101249. [Google Scholar] [CrossRef] [PubMed]

- Ederington, L.H.; Lee, J.H. The response of the dollar/yen exchange rate to economic announcements. Financ. Eng. Jpn. Mark. 1994, 1, 111–128. [Google Scholar] [CrossRef]

- Christofis, N.; Kollias, C.; Papadamou, S.; Stagiannis, A. Istanbul Stock Market’s reaction to terrorist attacks. Doğuş Üniv. 2013, 14, 153–164. [Google Scholar] [CrossRef]

- Fama, E.F. Efficient capital markets: A review of theory and empirical work. J. Financ. 1970, 25, 383–417. [Google Scholar] [CrossRef]

- Mantegna, R.N.; Stanley, H.E. Introduction to Econophysics: Correlations and Complexity in Finance; Cambridge University Press: Cambridge, UK, 1999. [Google Scholar]

- Schaefer, I.; Cannon, R. On the control of unstable mechanical systems. Res. Rev. 1966, 5, 11. [Google Scholar]

- Mori, S.; Nishihara, H.; Furuta, K. Control of unstable mechanical system control of pendulum. Int. J. Control 1976, 23, 673–692. [Google Scholar] [CrossRef]

- Åström, K.J.; Furuta, K. Swinging up a pendulum by energy control. Automatica 2000, 36, 287–295. [Google Scholar] [CrossRef]

- Henders, M.; Soudack, A. “In-the-large” behaviour of an inverted pendulum with linear stabilization. Int. J. Non-Linear Mech. 1992, 27, 129–138. [Google Scholar]

- Maletinsky, W.; Senning, M.; Wiederkehr, F. Observer based control of a double pendulum. IFAC Proc. Vol. 1981, 14, 3383–3387. [Google Scholar]

- Kawazoe, Y. Manual control and computer control of an inverted pendulum on a cart. In Proceedings of the First International Conference on Motion and Vibration Control, Yokohama, Japan, 7–11 September 1992. [Google Scholar]

- Cabrera, J.L.; Milton, J.G. On-off intermittency in a human balancing task. Phys. Rev. Lett. 2002, 89, 158702. [Google Scholar] [CrossRef] [PubMed]

- Cabrera, J.L.; Milton, J.G. Human stick balancing: Tuning Lévy flights to improve balance control. Chaos Interdiscip. J. Nonlinear Sci. 2004, 14, 691–698. [Google Scholar] [CrossRef] [PubMed]

- Cabrera, J.L.; Bormann, R.; Eurich, C.; Ohira, T.; Milton, J. State-dependent noise and human balance control. Fluct. Noise Lett. 2004, 4, L107–L117. [Google Scholar] [CrossRef]

- Cabrera, J.L.; Luciani, C.; Milton, J. Neural control on multiple time scales: Insights from human stick balancing. Condens. Matter Phys. 2006, 9, 373–383. [Google Scholar] [CrossRef]

- Cabrera, J.; Milton, J. Stick balancing, falls and Dragon-Kings. Eur. Phys. J. Spec. Top. 2012, 205, 231–241. [Google Scholar] [CrossRef]

- Cluff, T.; Riley, M.A.; Balasubramaniam, R. Dynamical structure of hand trajectories during pole balancing. Neurosci. Lett. 2009, 464, 88–92. [Google Scholar] [CrossRef] [PubMed]

- Treffner, P.J.; Kelso, J.S. Dynamic encounters: Long memory during functional stabilization. Ecol. Psychol. 1999, 11, 103–137. [Google Scholar] [CrossRef]

- Milton, J.G.; Ohira, T.; Cabrera, J.L.; Fraiser, R.M.; Gyorffy, J.B.; Ruiz, F.K.; Strauss, M.A.; Balch, E.C.; Marin, P.J.; Alexander, J.L. Balancing with vibration: A prelude for “drift and act” balance control. PLoS ONE 2009, 4, e7427. [Google Scholar] [CrossRef]

- Bouchaud, J.P.; Gefen, Y.; Potters, M.; Wyart, M. Fluctuations and response in financial markets: The subtle nature ofrandom’price changes. Quant. Financ. 2003, 4, 176. [Google Scholar] [CrossRef]

- Mandelbrot, B.B. The variation of certain speculative prices. J. Bus. 1967, 36, 394–419. [Google Scholar] [CrossRef]

- Gopikrishnan, P.; Plerou, V.; Amaral, L.A.N.; Meyer, M.; Stanley, H.E. Scaling of the distribution of fluctuations of financial market indices. Phys. Rev. E 1999, 60, 5305. [Google Scholar] [CrossRef] [PubMed]

- Pagan, A. The econometrics of financial markets. J. Empir. Financ. 1996, 3, 15–102. [Google Scholar] [CrossRef]

- Cont, R.; Potters, M.; Bouchaud, J.P. Scaling in stock market data: Stable laws and beyond. In Scale Invariance and Beyond; Springer: Berlin, Germany, 1997; pp. 75–85. [Google Scholar]

- Wilensky, U. NetLogo; Center for Connected Learning and Computer-Based Modeling, Northwestern University: Evanston, IL, USA, 1999. [Google Scholar]

- yahoo. 2022. Available online: https://finance.yahoo.com (accessed on 6 July 2022).

- Refinitiv. 2022. Available online: https://solutions.refinitiv.com/datastream-macroeconomic-analysis (accessed on 6 July 2022).

- Tsallis, C. Introduction to Nonextensive Statistical Mechanics, 2nd ed.; Springer: Berlin, Germany, 2023. [Google Scholar]

- Tsallis, C.; Anteneodo, C.; Borland, L.; Osorio, R. Nonextensive Statistical Mechanics and Economics. Phys. A 2003, 324. [Google Scholar] [CrossRef]

- Biondo, A.E.; Pluchino, A.; Rapisarda, A. Modeling financial markets by self-organized criticality. Phys. Rev. E 2015, 92, 042814. [Google Scholar] [CrossRef] [PubMed]

- Biondo, A.E.; Pluchino, A.; Rapisarda, A. Order book, financial markets, and self-organized criticality. Chaos Solitons Fractals 2016, 88, 196–208. [Google Scholar] [CrossRef]

- Biondo, A.E.; Pluchino, A.; Rapisarda, A. A multilayer approach for price dynamics in financial markets. Eur. Phys. J. Spec. Top. 2017, 226, 477–488. [Google Scholar] [CrossRef]

- Cont, R. Empirical properties of asset returns: Stylized facts and statistical issues. Quant. Financ. 2001, 1, 223. [Google Scholar] [CrossRef]

- LeBaron, B. Agent-based financial markets: Matching stylized facts with style. In Post Walrasian Macroeconomics: Beyond the DSGE Model; Cambridge University Press: Cambridge, UK, 2006; pp. 221–235. [Google Scholar]

- Raberto, M.; Cincotti, S.; Focardi, S.M.; Marchesi, M. Agent-based simulation of a financial market. Phys. A Stat. Mech. Its Appl. 2001, 299, 319–327. [Google Scholar] [CrossRef]

- Fabretti, A. On the problem of calibrating an agent based model for financial markets. J. Econ. Interact. Coord. 2013, 8, 277–293. [Google Scholar] [CrossRef]

- Cafferata, A.; Tramontana, F. A financial market model with confirmation bias. Struct. Chang. Econ. Dyn. 2019, 51, 252–259. [Google Scholar] [CrossRef]

- Alfi, V.; Cristelli, M.; Pietronero, L.; Zaccaria, A. Minimal agent based model for financial markets I: Origin and self-organization of stylized facts. Eur. Phys. J. B 2009, 67, 385–397. [Google Scholar] [CrossRef]

- Biondo, A.E. Order book modeling and financial stability. J. Econ. Interact. Coord. 2019, 14, 469–489. [Google Scholar] [CrossRef]

- Wu, F.; Zhang, D.; Ji, Q. Systemic risk and financial contagion across top global energy companies. Energy Econ. 2021, 97, 105221. [Google Scholar] [CrossRef]

- Banerjee, S.; Guhathakurta, K. Change-point analysis in financial networks. Stat 2020, 9, e269. [Google Scholar] [CrossRef]

- Trevino, I. Informational channels of financial contagion. Econometrica 2020, 88, 297–335. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Index | First Day | Last Day |

|---|---|---|

| AEX | 03/01/1983 | 06/07/2022 |

| Dow Jones | 04/05/1950 | 06/07/2022 |

| Euro stoxx 50 | 31/12/1986 | 06/07/2022 |

| FTSE 100 | 30/12/1983 | 06/07/2022 |

| FTSE MIB | 31/12/1997 | 06/07/2022 |

| France CAC 40 | 09/07/1987 | 06/07/2022 |

| IBEX 35 | 05/01/1987 | 06/07/2022 |

| Nasdaq | 05/02/1971 | 06/07/2022 |

| Nikkei 225 | 03/04/1950 | 06/07/2022 |

| S&P 500 | 31/12/1963 | 06/07/2022 |

| Asset | First Day | Last Day |

|---|---|---|

| American Express | 12/12/1972 | 06/07/2022 |

| Amazon | 16/05/1997 | 06/07/2022 |

| Apple | 15/12/1980 | 06/07/2022 |

| BMW | 11/11/1996 | 06/07/2022 |

| Colgate | 03/05/1973 | 06/07/2022 |

| Ford | 02/06/1972 | 06/07/2022 |

| General Electric | 03/01/1962 | 06/07/2022 |

| JP Morgan | 18/03/1980 | 06/07/2022 |

| Microsoft | 14/03/1986 | 06/07/2022 |

| Pfizer | 02/06/1972 | 06/07/2022 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Biondo, A.E.; Mazzarino, L.; Pluchino, A. Noise and Financial Stylized Facts: A Stick Balancing Approach. Entropy 2023, 25, 557. https://doi.org/10.3390/e25040557

Biondo AE, Mazzarino L, Pluchino A. Noise and Financial Stylized Facts: A Stick Balancing Approach. Entropy. 2023; 25(4):557. https://doi.org/10.3390/e25040557

Chicago/Turabian StyleBiondo, Alessio Emanuele, Laura Mazzarino, and Alessandro Pluchino. 2023. "Noise and Financial Stylized Facts: A Stick Balancing Approach" Entropy 25, no. 4: 557. https://doi.org/10.3390/e25040557

APA StyleBiondo, A. E., Mazzarino, L., & Pluchino, A. (2023). Noise and Financial Stylized Facts: A Stick Balancing Approach. Entropy, 25(4), 557. https://doi.org/10.3390/e25040557