Abstract

Mobile banking is an innovative solution for improving financial inclusion; however, the use of this technology is still very limited in developing countries. Consequently, this study aims to investigate elements affecting mobile banking adoption in a developing country context by applying the well-known Unified Theory of Acceptance and Use of Technology two (UTAUT2) model. Since most existing investigations on mobile banking using the UTAUT2 neglect the effects of personality traits, this investigation extends the UTAUT2 with a new antecedent not considered in previous studies, the consumer proactive personality. This study empirically tests the proposed partial mediation model using path analysis with data collected from Lebanese bank customers who are current non-users of mobile banking. Results show a full mediation model, confirming that some UTAUT2 drivers fully mediate the effect that proactive personality has on consumer intention to adopt mobile banking and highlighting the relevance of proactive personality on all UTAUT2 drivers. This study expands the Unified Theory of Acceptance and Use of Technology two and examines how a personality trait—proactive personality—relates to mobile banking adoption through the UTAUT2 perceptions in a developing country context.

1. Introduction

The traditional retail banking delivery system has changed because of innovations in information technology [1,2]. Nowadays, in addition to physical branches, banks use ATMs, telebanking, and electronic channels to deliver their services [3]. One of these electronic channels is mobile banking or m-banking.

Mobile banking enables customers to access bank accounts at any time and place through mobile devices (e.g., smartphones) to, among other operations, view statements and account balances, transfer money, make bills and peer-to-peer payments, and sell stocks [4,5]. Other mobile-based innovations in banking services are mobile shopping apps (e.g., [6]) and mobile payment (e.g., [7,8]).

Mobile banking is a self-service technology that benefits consumers and banks. Mobile banking enables banks to lower operating costs [9] and to gather data about bank consumers’ habits [10,11]. These advantages allow banks to improve their efficiency [2,12,13], productivity and profitability [14].

For consumers, some of the main advantages of mobile banking over conventional banking are ubiquity, immediacy, localization, instant connectivity, and proactive functionality [15]. Therefore, mobile banking provides convenience and real-time services [16], so that it is an efficient alternative to branch-visiting banking [17,18]. However, mobile banking also includes a wide variety of disadvantageous characteristics, such as privacy concerns, distrust, security risks, financial risks, and consumer uncertainty [5,19]. For these reasons, despite its advantages and the very high number of mobile phones in circulation, the adoption level of mobile banking is not up to the mark [20].

Currently, many users of banking services have not yet adopted mobile banking, especially in developing countries [21]. However, in these countries, the promotion of mobile banking can contribute to the deepening of financial services, facilitating financial inclusion and economic growth [22]. Since financial inclusion and economic growth at the global level are part of the millennium development goals and sustainable development goals, financial inclusion of basic financial services is a global necessity, especially in developing countries [23]. Thus, mobile banking deserves “the attention of banks located in developing countries” ([24], p. 133).

To encourage the use of mobile banking by consumers, it is necessary to identify and understand the barriers that generate resistance to its adoption [20] and the drivers that lead to it [25]. This stream of research is part of the general framework of the acceptance and use of technological innovations, made up of several information systems/information technology (IS/IT) theories and models. Among these theories, a recent review of mobile banking [26] has found that the Technology Acceptance Model (TAM, [27]), followed by the Unified Theory of Acceptance and Use of Technology (UTAUT, [28]) were the main conceptual frameworks and models adopted by scholars to explain consumers’ intentions of using mobile banking. Given that UTAUT is the result of a comprehensive review of the previously proposed technology adoption models and it “has proven to outperform the eight standalone models and provides a better prediction power” ([29], p. 774), our study is based on this theory.

An important feature of UTAUT is that it considers the use of the new technology in an organizational context. To adapt the UTAUT model to the consumer context, Venkatesh et al. [30] proposed a new version of UTAUT known as UTAUT2. Thus, since our study targets consumer, it uses UTAUT2 as theoretical basis to explain the intention to adopt mobile banking by consumers who currently do not use this technology in their relationships with banks. This is in line with previous studies that examine the determinants of adoption and use of new technologies by consumers (e.g., [31,32]). Moreover, we focus on behavioral intentions because the results of Jadil et al.’s [10] meta-analysis showed that “usage intention is the most critical predictor of use behavior” (p. 354).

Our study considers all antecedents of UTAUT2 except habit, which refers to the extent to which an individual believes that the behavior is set to be automatic [30]. To examine the role of habit, customers should have a rich experience in using such technology [33]. Hence, studies that consider habit (e.g., [34]) analyze the use of mobile banking by current users. Since our study explains the consumer intention to adopt mobile banking, consumers are not yet in the habit of using mobile banking and this habit cannot be measured.

Our study proposes an extension of the UTAUT2 to explain consumers’ intentions to adopt mobile banking. In particular, our investigation adds proactive personality, an individual difference, as a direct antecedent of the UTAUT2 drivers and as an indirect antecedent of the behavioral intentions to adopt m-banking.

Proactive personality is a personality variable that affects motivational aspects and processes [35,36,37,38]. Proactive personality has been studied in plenty of fields, such as employee behavioral and well-being outcomes, entrepreneurial behavior and co-worker emotions and behaviors [39,40,41] and has proven its effect on many outcomes regarding human behavior [42,43].

Although some studies on mobile banking have analyzed the relationship between behavioral intentions and personality variables, the lack of attention to personality variables in models such as the UTAUT2 is surprising, considering the results of the general psychological and technology acceptance research. While the first has shown that personality traits have an important impact on individual behavior [44,45], the second revealed their influence on internet usage [46] and mobile apps [47]. Additionally, in the Theory of Reasoned Action [48], one of the first theories used to explain the adoption of technological innovations, personality was explicitly identified as a relevant exogenous or external variable (see [49]).

In the mobile banking context, only a few TAM-based studies have analyzed the effect of personality variables as antecedents to exogenous model variables (for example, Gu et al. [50] and Singh and Srivastava [51] examined the impact of self-efficacy on perceived ease of use), but none have explicitly considered the mediating effect of these exogenous variables on the personality traits–intention to adopt a mobile banking relationship. This gap is even stronger in the UTAUT/UTAUT2-based studies because these models overlook personal, dispositional factors, in favor of perceptions [52], and the few investigations that have examined the influence of personality variables have only analyzed the direct relationship between personality variables and behavioral intention (for self-efficacy, see [53]) or have considered these variables as moderators (for innovativeness, see [54]).

Therefore, our study, which expands UTAUT2, makes several relevant contributions to the mobile banking literature. First, it performs an updated review of the literature on mobile banking. Second, to the best of our knowledge, this is the only study that combines proactive personality with UTAUT2 in the mobile banking context. Therefore, it contributes to the scarce research that relates personality traits to behavioral intention of using mobile banking. Moreover, integrating proactive personality, expands UTAUT2. This extension follows the recommendation of Tamilmani et al. [55], who after making a systematic literature review and theory evaluation of UTAUT2, identified as lines of improvement the incorporation of exogenous mechanisms to increase its explanatory power. Third, previous investigations have mostly focused on technological perceptions and neglected the effects of personality traits on user adoption of mobile commerce [56]. An exception is Agyei et al. [57], who analyzed the effect of basic personality traits on TAM drivers, which in turn predicted the intention to adopt mobile banking. Nevertheless, the limited research on personality variables and adoption of mobile banking has focused mostly on direct effects without taking into consideration indirect ones [58]. In this line, our study examines the indirect relationship between proactive personality and behavioral intention through UTAUT2 drivers; that is, proposes and tests a partial mediation model in which the UTAUT2 drivers mediate the proactive personality–behavioral intention relationship. To the best of our knowledge, no study has analyzed the UTAUT2 drivers as mediators between a distal individual antecedent and the behavioral intention to use mobile banking.

2. Literature Review and Hypotheses

2.1. M-Banking Concept

Mobile banking has been defined in various ways. Tam and Oliveira [59], based on previous definitions, described mobile banking as “a service or product offered by financial institutions that makes use of portable technologies” (p. 1048). More recently, it has been defined as “the use of handheld devices to access banking information and/or conduct banking transactions via short message service (SMS) messaging services, downloadable applications and/or wireless application protocols to access financial and nonfinancial services” ([60], pp. 272–273). Therefore, mobile banking cannot exist without mobile devices and communication networks [61].

Developments in information and communication technology (ICT), a growing number of owners and users of mobile devices in their daily lives, and the possibility of establishing an effective and more efficient channel, led banks to integrate mobile banking among the services offered to their customers. Researchers have responded by devoting increasing attention to mobile banking, particularly analyzing its acceptance and use.

Although mobile banking is considered a type of digital banking [62], and both innovations seem similar, Laukkanen [1] indicated that their adoption patterns and barriers to adoption are different.

2.2. M-Banking and Technological Innovation Acceptance Models

The first studies on mobile banking were published at the turn of the millennium (e.g., [63,64]); however, there has been a strong increase in their number in recent years, “which is irrefutable proof of the growing popularity of mobile banking” ([26], p. 3).

The literature on mobile banking has resorted to the existing models and theories of technological innovation adoption and use, given that mobile banking is considered a technological innovation and these theories and models have been developed in various contexts that vary on “technology, user type, location, adoption time and task performed” ([55], p. 1).

Table 1 shows the empirical studies on the acceptance and use of mobile banking published from 2019 to January 2022. This literature review was carried out in several phases. First, an electronic search was conducted employing two prominent business/management databases to source literature, Business Source Premier Database and Scopus; the keywords used were mobile banking and m-banking, limiting the search to the title and/or abstract of the articles. Second, a manual search for articles was carried out in scholarly journals in the fields of IS and marketing. Third, another manual search was conducted by scrutinizing citations in previous literature reviews and meta-analysis studies in the field of mobile banking.

Table 1.

Empirical studies on mobile banking acceptance and use conducted from 2019 to January 2022 (except UTAUT/UTAUT2).

2.3. M-Banking and the Unified Theory of Acceptance and Use of Technology Two

The unified theory of acceptance and use of technology (UTAUT) [28], was developed through a review and consolidation of the constructs of eight prominent theories that earlier research had employed to explain information systems usage behavior, including TAM, DoI/IDT, and the social cognitive theory (SCT). UTAUT incorporates three drivers—performance expectancy, effort expectancy, and social influence- that impact behavioral intention to use a technology innovation, while facilitating conditions and behavioral intention influence technology use. UTAUT also includes four key moderators: gender, age, experience, and voluntariness of use. Since its appearance, the UTAUT model has gradually attracted researchers’ attention.

In 2012, Venkatesh, Thong, and Xu extended UTAUT by adapting it to a consumer context. This extension, called UTAUT2, incorporates three key constructs from prior research on behavioral intention (hedonic motivation, price value, and habit); includes a direct relationship between facilitating conditions and behavioral intention; and removed voluntariness as a moderator.

Later, Venkatesh et al. [99] carried out a literature review not limited to mobile banking in the Web of Science, searching from papers from September 2003 until December 2014, to synthesize the literature on UTAUT. The 1267 UTAUT citations identified were classified into four groups: (1) general citation category, which includes papers that cited but not used UTAUT, with 1205 citations; (2) applications, which incorporate empirical studies that employed part or the full UTAUT, with 12 citations; (3) integrations, which contain studies that combine UTAUT with other theories, with 13 citations; and (4) extensions, with 37 citations. The extension papers group was then divided into four types: (1) new exogenous, which incorporates effects of external predictors on the exogenous variables in UTAUT, (2) new endogenous, which adds new predictors to intention and use or enriches the original UTAUT variables, (3) new moderating, which includes new moderating effects, and (4) new outcome mechanisms, which incorporate new consequences of intention and use.

Focused on the mobile banking context, Tamilmani et al. [55] conducted a systematic literature review of UTAUT2 from papers from March 2012 to March 2017. These authors incorporated three new extensions to Venkatesh et al. (2016) classification: (5) new mediating, which adds new mediating variables between intention and new or the original UTAUT exogenous variables, (6) new external, which includes relationships among new variables that were not part of the original UTAUT2 model. and (7) new internal mechanisms, which enriches the existing UTAUT2 variables through new path associations. If both reviews are considered together, a total of seven extensions of the UTAUT2 theory result.

Based on the literature review conducted in the mobile banking context for the period 2019–January 2022, Table 2 shows the empirical UTAUT/UTAUT2-based studies that integrate one of these models fully or partially with another model of theoretical significance or that test these models incorporating new mechanisms.

Table 2.

Empirical UTAUT/UTAUT2-based studies on mobile banking acceptance and use conducted from 2019 to January 2022.

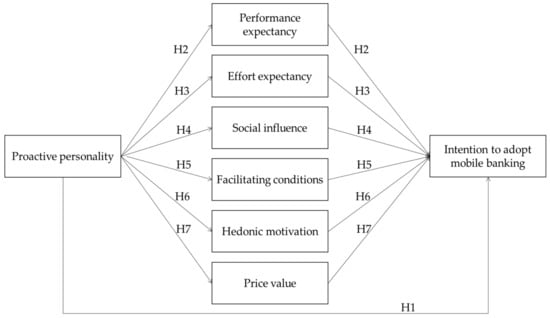

Our study is part of this last stream and attempts to improve the explanatory capacity of UTAUT2 by incorporating a new endogenous mechanism (proactive personality on behavioral intention) and six new exogenous mechanisms (proactive personality on performance expectancy, effort expectancy, social influence, facilitating conditions, hedonic motivation, and price value). That is, our model suggests that customer proactive personality is a distal antecedent of m-banking adoption behavioral intention, whose influence on behavioral intention occurs indirectly through the UTAUT2 drivers.

2.4. Mobile Banking and Proactive Personality

The behavioral literature, especially in the psychological fields, has considered plenty dynamic relations and process interactions between people and the environment. People influence the environment, i.e., individuals influence their situations, and are not only passive recipients of environmental presses ([116].

Empirical studies have revealed many processes through which individuals can influence their environment; including selection (choosing situations in which to participate) [117] cognitive restructuring (perceiving and appraising environments) [118], evocation (evoking reactions from others) [119], and manipulation (trying to shape, alter, and change their interpersonal environment) [120]. However, changing a situation, taking actions, altering circumstances, or even affecting an environment depends on individual differences, so that individuals who take an active role in creating their own environment tend to have a proactive personality.

The first description of proactive personality was simply a “disposition towards taking action to influence one’s environment”, which was primarily based on the person–situation relationship [121]. Another definition was later established by Crant [35], who described it as a narrow personality trait, derived from the Big Five personality traits, which refers to a tendency to identify opportunities and work on such impulses to help change situations and affect the environment. According to Bateman and Crant [121] proactive personality individuals tend to be (i) decision takers, (ii) problem solvers, (iii) forward thinkers, (iv) action-oriented individuals, (v) proactive goal setters, and (vi) new opportunity seekers. Conversely, people without a proactive personality flow with environmental conditions and tend to adapt to situations and express fear of change.

Adopting mobile banking technologies may serve proactive personality individuals’ intentions to change situations and circumstances. According to Parker and Collins [38] and Lin et al. [37] proactive personality influences motivational aspects such as achieving new goals, seek new opportunities and modify the environment. Proactive personality individuals may consider adopting mobile banking technology as an opportunity to increase business or individual performance. In addition, proactive individuals are self-initiated individuals, i.e., “they seek change based on what they personally consider motivating” ([122], p. 828) where mobile banking solutions may be the case. Furthermore, for people who are action oriented, adopting mobile banking services will be a normal action to be involved in since they like changing the status quo. In addition, being forward thinkers, they do not wait for things and opportunities to come to them, instead they develop and take actions to acquire chances and capture opportunities faster and more efficiently than others [35]. Hence,

Hypothesis H1 (H1):

Customers’ proactive personality is positively related to their intention to adopt mobile banking.

2.5. The Mediating Role of Performance Expectancy

Performance expectancy represents an individual’s personal belief that using the new technology will deliver a set of benefits [28]. Some constructs and the corresponding previous theories that pertain to the unification of performance expectancy are perceived usefulness (TAM), relative advantage (IDT), and outcome expectations (SCT) [28]. Performance expectancy “underscores the dominant paradigm of extrinsic motivation in individual technology acceptance research” ([123], p. 222).

According to Compeau and Higgins [124], people are intent to adopt new technology if they expect positive consequences in return for its use. Consequently, individuals are set to adopt mobile banking if they perceive this technology as valuable and useful [27]. In this line, previous research has found that customers’ intention to adopt new technologies is directly related to performance expectancy (e.g., [32,125,126]).

On the other hand, the self-initiative attribute that distinguishes proactive individuals from passive ones stimulates and arouses their search and capture of opportunities [127]. Proactive people tend to seek opportunities rather than wait for chances to come [35,128]. According to Seibert et al. [129], proactive individuals seek new ideas to enhance their skills. Thus, proactive individuals who are future-oriented and opportunity seekers will probably identify mobile banking technologies as a new opportunity to enhance their skills. Moreover, since proactive individuals seek out new opportunities, they are more likely to adopt any new technology that may be distinct and more developed than previous ones. They will probably consider that adopting mobile banking technologies will open new prospects and chances to perform better. Thus, proactive individuals will perceive mobile banking technology services as useful. Hence,

Hypothesis H2 (H2):

Performance expectancy mediates the positive relationship between customers’ proactive personality and their intention to adopt mobile banking.

2.6. The Mediating Role of Effort Expectancy

Effort expectancy represents an individual’s belief regarding the ease of use of a new system [28]. Some constructs and the corresponding previous theories that pertain to the unification of effort expectancy are perceived ease of use (TAM) and ease of use (IDT) [28].

The level of difficulty of a new technology, i.e., the effort required for its use, is an essential predictor of the intention to accept this technology [27]. According to Lin [130], as individuals realize the simplicity of using mobile banking service, they are more willing to use it. Similarly, several authors have confirmed the impact of effort expectancy on customer intention to adopt new technologies (e.g., [32,125,131]).

On the other hand, proactive individuals desire to acquire new ideas and knowledge about their environment more rapidly than others [121]. Therefore, proactive individuals carry out anticipatory actions to obtain additional information, seek new ideas, become aware of policies, and increase their knowledge and knowhow of processes and the environment [128]. In other words, proactive individuals seek cognition [129]. Another characteristic that stands for proactive personality is problem solving. Proactive individuals tend to be problem fixers [121]. They can gather social and political knowledge that helps them identify future risks and problems and tackle them immediately [122]. Moreover, Frohman [132] presented proactive individuals as self-initiators who see a problem and attack it without any previous recommendations on what to do. The foundation for these risky behaviors is their propensity to believe strongly that they can be successful in a specific task [133]. These characteristics will likely make proactive individuals less worried about the complexity of the new technology as they have probably overcome complex situations before. Therefore, proactive individuals will be more likely to view new technologies (mobile banking) as easier to use. Hence,

Hypothesis H3 (H3):

Effort expectancy mediates the positive relationship between customers’ proactive personality and their intention to adopt mobile banking.

2.7. The Mediating Role of Social Influence

Social influence is defined as the extent to which an individual perceives that relevant others believe that he or she should adopt the new system [28]. Some constructs and the corresponding previous theories that pertain to the unification of social influence are subjective norm (in TRA, TAM2, TPB, and DTPB) and image (IDT).

The effect of social influence over new technology adoption and use was demonstrated in several studies (e.g., [31,32,125]). The social pressure exerted by the surrounding environment, such as reference groups, family, opinionated leaders, friends, and colleagues, will influence customer behavioral intentions regarding new technologies [16]. In other words, if most of the individual’s social context is made up of mobile banking users this will encourage him/her to adopt mobile banking as well [14]. In this line, previous research has underlined social influence as a key determinant of behavioral intention toward mobile banking (e.g., [16,18]).

On the other hand, from the interactional perspective, proactive individuals will be more effective in selecting and shaping their environment, so that it matches their needs and values [134]. Since proactive individuals are forward thinkers, action-oriented individuals, and new opportunity seekers [121], they are likely to select a social environment that matches these characteristics. At the same time, proactive individuals are more prone to request feedback [135]. Therefore, they will probably find more people that have adopted or are thinking of adopting mobile banking. Hence,

Hypothesis H4 (H4):

Social influence mediates the positive relationship between customers’ proactive personality and their intention to adopt mobile banking.

2.8. The Mediating Role of Facilitating Conditions

Venkatesh et al. ([28], p. 455) defined facilitating conditions as “the degree to which an individual believes that an organizational and technical infrastructure exists to support the use of the system”. The more resources, help, and support available for people over the online banking channels, the more likely they will be to adopt it [16]. In this line, previous investigations have found a direct impact of facilitating conditions on customer behavior toward new technology (e.g., [34,125,136]).

On the other hand, “proactive individuals may adopt a new technology after considering its facilitating conditions” ([137], p. 351). Thus, proactive individuals may consider the availability of resources and facilities while considering a new technology. However, as proactive individuals carry out anticipatory actions to obtain additional information, be aware of policies and increase their knowledge and knowhow of processes and the environment [128,129], they are more likely to have knowledge on the resources available. Moreover, as they can gather social and political knowledge [122], since they engage in more information exchange [138] and are very good at developing interpersonal relations [139], they will probably acquire more support and, as a result, perceive greater facilitating conditions for the use of a new technology, such as mobile banking. Hence,

Hypothesis H5 (H5):

Facilitating conditions mediate the positive relationship between customers’ proactive personality and their intention to adopt mobile banking.

2.9. The Mediating Role of Hedonic Motivation

Hedonic motivation refers to the level of fun and pleasure derived from using new technology [30]. Under the UTAUT2 model, the hedonic motivation construct encompasses intrinsic utility concepts such as joy, fun, playfulness, entertaining, and enjoyment [30]. It is often regarded as an intrinsic stimulus that makes an individual use new technology services such as mobile banking. At the same time, existing research has supported the effect of hedonic motivation on customers’ intentions to use new technologies (e.g., [125,126,140]).

On the other hand, proactive individuals are self-initiated individuals, i.e., “they seek change based on what they personally consider motivating” ([122], p. 828) This implies that proactive individuals seek new opportunities and modify the environment because they consider these actions entertaining or enjoyable. Some scholars, such as Lin et al. [37] and Parker and Collins [38], highlighted that proactive individuals are intrinsically motivated. In other words, proactive individuals are self-initiated individuals who tend to resolve threats, achieve goals, and alter situations because they consider such actions to be entertaining and fun. At the same time, Brown and Venkatesh [141] and Van der Heijden [142] indicated that innovative technologies comprise novelty seeking and uniqueness. Thus, it can be deduced that proactive individuals tend to seek personal novelty and uniqueness by using new technologies, which produces enjoyment and entertainment, and hedonically motivates them toward these technologies. Hence,

Hypothesis H6 (H6):

Hedonic motivation mediates the positive relationship between customers’ proactive personality and their intention to adopt mobile banking.

2.10. The Mediating Role of Price Value

Price value refers to the ratio of the cost of the technology versus the value it supplies, in other words, price value is positive when the benefits of using the new technology are perceived to be greater than the associated monetary cost [30]. This implies that new technology adoption is considered based on the cost–benefit analysis. Price value derives from the idea of perceived value [143]. Regarding the adoption of new technology, end-users are constantly comparing the cost incurred with the resulting savings and benefits that they might derive from the new technology [144]. In the context of mobile technology, price value has been accounted to have a noteworthy effect on customer decision-making, satisfaction, and loyalty [145,146]. Similarly, previous research has found a positive effect of price value on behavioral intentions regarding new technologies (e.g., [32,61,147].

Proactive individuals are self-initiated individuals who seek change and new ideas to try to capture opportunities [122,127]. Therefore, they are likely to believe that mobile banking technology will open new opportunities and help them improve their skills and perform better. These will favor a more positive consideration regarding the value derived from mobile banking, in turn resulting in a better price-value ratio, which may influence the intention of adoption of new technologies. In other words, proactive individuals with their positive future orientation will probably reflect positively and optimistically regarding mobile banking price value, as they will perceive mobile banking technology as a beneficial new technological opportunity to its associated monetary cost. Hence,

Hypothesis H7 (H7):

Price value mediates the positive relationship between customers’ proactive personality and their intention to adopt mobile banking.

The research model proposed is depicted in Figure 1.

Figure 1.

Proposed model (hypotheses formulation).

3. Research Methodology

3.1. Sample

According to our study objectives, all Lebanese individuals above 18 years old, who own a smart phone, have a bank account and are still non-users of mobile banking, are all units of analysis and members of the whole population. As a result, this shows that according to this study, a huge set of the Lebanese population can be considered. Therefore, the proposed hypotheses were studied in a convenient sample of Lebanese bank customers who have mobile devices with Internet access but are non-users of mobile banking. According to a study conducted in 2017 over the MENA countries regarding the adoption of digital banking, Lebanon recorded the lowest rates [148]. Hence, despite all investments and efforts exerted regarding new technologies in the Lebanese banking sector, Lebanese banking customers still demonstrate low interest toward online banking channels in general, and toward the adoption of mobile banking in particular [149,150].

3.2. Data Collection and Screening

Among research addressing the technology adoption factors, the self-administrated questionnaire has been the most frequently used data collection instrument [151,152,153,154]. In addition, the self-administrated questionnaire is an efficient data collection instrument since it is free of influence, place, time and cost restrictions [151,153,154,155]. Hence, to gather the required data a self-administrated questionnaire was considered as the best data collection instrument for this study. Therefore, 315 valid questionnaires well collected.

After the collection of data, preliminary data analysis is the prerequisite of any further multivariate data analysis. Therefore, data screening methods were applied to ensure valid data, and detect missing values, and outliers [156,157,158]. In particular, this study used MCAR “Missing Completely At Random” and Mahalanobis D-Squared techniques to analyze missing data and outliers relatively. Results showed a non-significant p value of MCAR being greater than 0.05, indicting missing vales are less than 5% and can be treated. Whereas p value regarding D-Squared for each response scored above the cut-off point of 0.001 indicating no outliers.

3.3. Measurement Scales

In order to achieve high-reliability outcomes a Likert scale is intensively recommended [159]. Not surprisingly, the Likert scale format has been intensively used in prior technology adoption studies, such as Venkatesh et al. [28]. Therefore, to measure the constructs considered in this study we employed multi-item five-point Likert scales adapted from previous investigations specifically related to m-banking. The constructs comprised in the UTAUT2 were measured using items extracted from Venkatesh et al. [30]. Regarding the personality trait variable, it was measured in a range of 1 to 5 using 10 items retrieved from Seibert et al. [134]. This scale represents a shortened scale of Bateman and Crant’s [121] original scale. The ten-item scale of proactive personality has been validated by several researchers and has been recently considered the official scale to measure the proactive personality construct (e.g., [122]). Appendix A shows the scales’ measures. Two control variables were included in the model: customer’s age (the natural logarithm of age) and gender.

3.4. Psychographic Properties of the Scales

To ensure correct usage of the scales, a measurement model of all constructs was subjected to confirmatory factor analysis using EQS. The results of the measurement model are included in Appendix A. The overall robust fit indices are indicative of a good fit of the model to the data. Regarding reliability, all variables have a Cronbach’s alpha (α) greater than 0.7, a composite reliability (CR) greater than 0.6 and an average variance extracted (AVE) greater than 0.5. In addition, convergent validity is supported (all lambda parameters are greater than 0.5 and are statistically significant). Regarding discriminant validity, it was tested and supported using two procedures, the approach proposed by Fornell and Lacker [160] (the square root of the variances extracted is greater than the correlations between the constructs), which is shown in Appendix B, and the criterion suggested by Henseler et al. [161] (the heterotrait–monotrait ratio of the correlations (HTMT) is significantly smaller than 1), which is shown in Appendix C.

3.5. Analytical Strategy

To assess the proposed mediation process, we carried out path analysis using Stata. Path analysis offers the possibility to model the relationships among multiple independent and dependent constructs simultaneously, showing a more complete picture of the whole model [162], whilst eliminating the complexity of using latent variables in a large mediation model like the one in this investigation. Thus, we substituted the constructs by the average score of the indicators, grouping them in a single measure. Moreover, to avoid problems when interpreting some coefficients, given the measurement scales of some of the considered variables (which do not include the value zero), the variables were centered on the mean.

4. Results

A statistical description that summarizes the demographical distribution of the current study regarding the respondents’ profile and characteristics was generated. Regarding gender, the distribution was almost equal between male and female, indicating that 52.06% for respondents were males. On the other side, respondents were of different ages ranging from 18 years old to 70 years old with an average of 31.68 years old and 29 years old as the highest age frequency. Finally, the analysis showed that 75.24% of the respondents were employed (had a job) whereas the rest of the respondents (24.76%) were unemployed (had no job).

Regarding data analysis, the results reported in Table 3 reveal that customer proactive personality has a positive effect on the intention to adopt mobile banking; nevertheless, this relationship is only significant when the analysis does not incorporate the UTAUT2 antecedents. Thus, hypothesis 1 is only partially supported. The findings also show that proactive personality has a positive impact on all UTAUT2 antecedents. Conversely, there was no significant relationship between all UTAUT2 antecedents and intention to adopt mobile banking. The results reveal that only performance expectancy, effort expectancy, social influence and facilitating conditions have a positive effect on mobile banking adoption, whereas the impact of price value and hedonic motivation is non-significant. Thus, hypotheses 6 and 7 are not supported.

Table 3.

Results of path analysis.

To further examine the multiple mediation process, we used bootstrapped 95 per cent CIs (resulting from 5000 replications) following Preacher and Hayes [163]. The findings (see Table 4) show that the indirect relationships between customer proactive personality and mobile banking adoption via performance expectancy, effort expectancy, social influence and facilitating conditions are positive and significant, since the bias-corrected confidence intervals do not include the null value. Therefore, hypotheses 2, 3, 4 and 5 are fully supported.

Table 4.

Test of indirect effects on mobile banking adoption intention.

These results suggest that the drivers central to UTAUT, but not the additional ones of UTAUT2, fully mediate the effect that proactive personality has on behavioral intention to adopt mobile banking. Full mediation by UTAUT drivers implies that proactive personality does not exhibit any direct influence on adoption intentions. Rather, such an effect is only exhibited indirectly through its relationship with UTAUT drivers. Table 5 summarizes the hypotheses testing.

Table 5.

Summary of hypothesis testing.

5. Discussion

This study aimed to explore mobile banking adoption from a personality perspective. Specifically, this research attempted to understand how the proactive personality trait affects m-banking intention. For this, the research employed an extended UTAUT2 model as the theoretical lens. The proposed model relates proactive personality to behavioral intention through seven relationships (H1–H7), one direct relationship and six indirect ones, through the UTAUT2 drivers.

Several results of the empirical analysis are relevant. First, although proactive personality was predicted to positively impact the mobile banking adoption intention, findings showed that proactive personality only had a direct effect on mobile banking adoption among respondents when the UTAUT2 constructs were not included in the analysis and ceased to be significant when the UTAUT2 constructs were included.

Second, proactive personality is positively and significantly related to all UTAUT2 drivers, with high coefficients. Therefore, individuals who are forward thinkers are more likely to have positive performance and effort expectations regarding mobile banking, as it has been argued that being a forward thinker increases your sense of positive future expectations [121]. In the same line, people described by their abilities to identify new opportunities and solve problems perceive mobile banking as useful and easy to use. These results are in line with those of Agyei et al. [57], who in their study on the impact of Big Five personality traits on users’ intention to adopt mobile banking through TAM drivers, found that performance utility (corresponding to performance expectancy in UTAUT2) was significantly related to agreeableness, conscientiousness, neuroticism, and openness to new experiences; in addition, the effects of agreeableness, conscientiousness, and openness to new experiences on perceived ease of use (corresponding to effort expectancy in UTAUT2) were also significant.

At the same time, findings show that individuals with a proactive personality usually have the perception that their social environment supports the use of new technologies, probably because they would have selected reference groups, opinionated leaders, colleagues, and friends that match their forward-thinking, action-orientated, and opportunity-seeking characteristics. Therefore, proactive individuals perceive greater social influence toward mobile banking.

Results also indicated the positive influence of proactive personality on facilitating conditions and price value. Since proactive individuals try gathering social and political knowledge [122] and, as a result, acquire and identify more support, they will perceive greater facilitating conditions. Furthermore, mobile banking technology will create new opportunities and help proactive individuals improve their skills and perform better. Therefore, action-oriented proactive individuals will greatly appreciate the retrieved benefits of mobile banking in comparison to its price.

Finally, hedonic motivation was also affected by proactive personality. The more proactive individuals are, the more hedonically motivated toward mobile banking they will be, based on the assumption that they prefer to resolve threats, achieve goals, and alter situations, and that mobile banking technologies may serve the goals and visions of these proactive individuals.

Therefore, findings highlight the relevance of proactive personality in explaining the exogenous UTAUT2 variables.

Third, regarding the influence of the UTUAT2 exogenous variables, two of these antecedents, price value and hedonic motivation, were not related to customers’ intention to adopt mobile banking, while the other UTAUT2 drivers (performance expectation, effort expectations, social influence, and facilitating conditions) are significantly related to behavioral intention.

Performance expectancy emerged as the most relevant predictor of consumer behavioral intention, as it had the greatest influence (0.649). This result is in line with existing research on mobile banking, since Jadil et al.’s [10] meta-analysis of the UTAUT model, including 127 empirical studies from 2004 to 2020, showed that performance expectancy (0.401) was “the strongest antecedent of usage intention” (p. 354). Similarly, Tamilmani et al.’s [164] meta-analysis of UTAUT2 found that the relationship between performance expectancy and behavioral intentions was the most employed and one of the strongest paths.

Effort expectancy was also a significant positive predictor of behavioral intention, reaffirming this relationship in the consumer m-banking domain. In our study, its relative position was the third place (0.146), while in Jadil et al.’s [10] meta-analysis of the UTAUT model in mobile banking research, effort expectancy had the second highest coefficient on the intention to use (0.199). It seems that effort expectancy is particularly relevant in the case of mobile banking technology, since in Tamilmani et al.’s [164] UTAUT2 meta-analysis, the relationship between effort expectancy and behavioral intention, although the second most employed, was the weakest.

In addition to performance expectancy and effort expectancy, social influence and facilitating conditions emerged as significant predictors of consumer intention to adopt mobile banking. Social influence and facilitating conditions occupied, respectively, the fourth and second place for their impact on the intention to adopt (0.118 and 0.195). This is in line with Tamilmani et al.’s [164] UTAUT2 meta-analysis, where facilitating conditions had a greater role in affecting behavioral intentions than social influence, while in Jadil et al.’s [10] meta-analysis of the UTAUT model in mobile banking research, social influence had greater path values than facilitating conditions (0.193 and 0.139).

However, price value and hedonic motivation were found to have a non-significant impact on customers’ intention to adopt mobile banking.

The non-influence of the value price is explained by the fact that mobile banking is a technology done through mobile devices, in other words, through free applications or mobile web browsers on a smartphone or tablet. Since the sample encompasses bank customers’ who already have mobile devices with Internet access, the cost–benefit ratio is probably not relevant to the adoption of mobile innovations. The non-significant relationship between price-value and intention to adopt mobile banking is in line with the results of the meta-analytic evaluation of UTAUT2 performed by Tamilmani et al. [164], who found that half of the studies reported non-significant values and argued that this happened “when the users perceived the product/service offering examined as free of charge” (p. 1001), as it occurs in the case of mobile banking.

Regarding hedonic motivation, even if the positive impact of hedonic motivation or similar factors such as fun, enjoyment, playfulness and perceived entertainment on behavior has been demonstrated by some previous literature on technology adoption [141], other studies have also found a non-significant effect of hedonic motivation on behavior [165]. It appears that the path between hedonic motivation and behavior depends on the subject addressed. Mobile banking technology is not considered a fun and entertaining technology; in fact, it is categorized as a self-business and serious financial service, not employed for its entertaining nature. Consequently, the level of fun and pleasure derived from using mobile banking is not reason enough for customers to decide whether to adopt it. This is in line with that of Tamilmani et al. [164] who found that studies that reported a non-significant effect of hedonic value were focused on utilitarian value.

Third, the indirect effect of proactive personality occurs only through performance expectation, effort expectations, social influence, and facilitating conditions. Forward thinkers find new opportunities easy to imagine and anticipate and predict the future benefits and conveniences of employing new technologies. In this line, proactive banking customers assume that mobile banking is useful and easy to use, which will result in greater intentions to adopt this technology.

Regarding the indirect effect of proactive personality through facilitating conditions, we argue that proactive individuals try gathering social and political knowledge [122] and, as a result, acquire and identify more support, which implies that they will perceive greater facilitating conditions, which will help their adoption of mobile banking.

Finally, proactive personality indirectly influences behavioral intention through social influence. Individuals with a proactive personality usually have the perception that their social environment supports the use of new technologies, probably because they would have selected reference groups, opinionated leaders, colleagues, and friends that match their forward-thinking, action-orientated, and opportunity-seeking characteristics. Therefore, proactive individuals will perceive greater social influence toward mobile banking, which will impact their mobile banking adoption intentions.

The support found for the indirect effect of proactive personality on behavioral intention implies a fully mediated relationship. This result is in line with previous literature that considers personality a distal antecedent of behavior and customer perceptions regarding new technology proximal antecedents [166]. This finding is important because none of the previous studies analyzed proactive personality as a direct and indirect antecedent of consumer behavioral intention to adopt m-banking.

5.1. Theoretical Implications

Our study contributes to the theory and research in several relevant ways. A first theoretical contribution comes from the review of the recent mobile banking UTAUT/UTAUT2-based literature. Another major contribution stems from the empirical validation of the proposed extended UTAUT2 model. Since previous research on the drivers of the UTAUT2 factors is still limited and there is a lack of studies that examine the impact of users’ attributes [99], this investigation contributes to the literature on the UTAUT2 model by extending it and examining the foregoing influence of an external personal variable, proactive personality, on the UTAUT2 variables. Further, since personality is a key factor in understanding individual attitudes and behavior [167], in particular consumer behavior [168], this investigation contributes integrating two research streams—psychological studies and technological innovation adoption studies—by analyzing the relationship between a previously unanalyzed personality trait and mobile banking adoption. Finally, since prior research has mostly centered on the direct antecedents of mobile banking [58], this investigation contributes to research on mobile banking by testing the indirect effect of proactive personality on mobile banking adoption intention through the UTAUT2 drivers.

5.2. Managerial Implications

Meuter et al. ([169], p. 78) stated that “for many firms, often the challenge is not managing the technology, but rather getting consumers to try the technology”. Results of the current study help understand the different factors that influence banking customers’ intentions toward adopting mobile banking technology. The results show the importance of proactive personality and its significant indirect influence on the behavioral intentions of respondents regarding mobile banking through the UTAUT2 drivers.

Proactive individuals have more favorable perceptions of the UTAUT2 drivers than non-proactive individuals and these perceptions mediate the influence of the proactive personality on the intention to adopt mobile banking. However, not all UTAUT2 drivers have a significant effect on the intention to adopt mobile banking, so that the effect of proactive personality on the intention to adopt mobile banking only occurs through performance expectancy, effort expectancy, social influence, and facilitating conditions.

The results suggest the relevance of incorporating proactive personality as a criterion for market segmentation and the need to consider this personality trait to help expanse mobile banking services among customers. Bank managers should not only base their market segmentation on traditional demographic factors but use more fine-grained segmentation criteria to recognize overlooked segments.

To target first individuals with high proactivity facilitates the adoption of mobile banking, since such individuals have more favorable perceptions of the UTAUT2 drivers. For instance, given the significant impact of performance expectancy on behavioral intention, advertising messages should address the usefulness of mobile banking using proactive characteristics.

A greater challenge is to encourage the adoption of mobile banking by non-proactive individuals, who are more prone to perceiving problems to its adoption. Consequently, banks should try influencing perceptions of performance expectancy, effort expectancy, social influence and facilitating conditions, particularly performance expectancy, given its greater relative weight in behavioral intention. To achieve this, banks should spend more time on teaching and educating their clients about the utilitarian advantages and benefits of using mobile banking when performing various financial tasks. Additionally, banks need to encourage developers to focus on adding value. Furthermore, they should develop simple and friendly mobile applications, with unassuming and attractive interfaces, to help their customers’ effort expectations and to increase the convenience of using mobile banking.

Moreover, the positive impact of facilitating conditions on behavioral intentions indicate that banks should provide training programs and support material, which may lead to better understanding and use of mobile banking by consumers. Developers can also provide an additional package of online training to ensure that consumers can see a demonstration or obtain relevant help when using mobile banking. Additionally, banks and financial service providers should implement and make known effective procedures and infrastructures to assist customers with mobile banking and cope with any problems that could arise while using the mobile technology, therefore increasing their perceptions of the support available. Making the necessary resources available to consumers for adopting mobile banking will make the system easier to use and increase usage intention.

Finally, the significance of social influence on behavioral intentions indicates that banks should allocate resources and efforts toward a more active use of societal influence to motivate consumers. Advertising messages should encourage the use of mobile banking through testimonial celebrities. Banks should also improve their use of social media to promote interpersonal word-of-mouth communications to increase the adoption of mobile applications by consumers.

5.3. Limitations and Future Research

Despite all the contributions made by this investigation, there are still some limitations. The main limitation is the possibility of common method bias in the obtained results since all constructs used are self-reported [170]. Another limitation of the study derives from the cross-sectional nature of the data, as the study was conducted at a specific moment in time, and, consequently, it would be necessary to carry out a longitudinal study to reaffirm the causal relationships. Furthermore, the current study has not considered cultural factors, which may be specific to the Lebanese culture, such as masculinity, femininity, communism, individualism, etc. These characteristics may play an important role in causing specific psychological concerns, adopting certain beliefs, and predicting behavior intentions [171,172]. Regarding future studies, researchers might duplicate the proposed model in a different innovation context. They could also study the impact of the Big Five personality traits alongside customer proactive personality on mobile shopping intention. As well, they may also consider investigating the effects of customer proactive personality in a cross-cultural context.

Author Contributions

Writing—original draft and review, A.H., C.V.-N.; editing, C.V.-N. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by Consellería de Cultura, Educación e Universidade da Xunta de Galicia, grant number ED431B 2022/32.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Table A1.

Measurement scales used and properties.

Table A1.

Measurement scales used and properties.

| Items | Standard Loading (λ) |

|---|---|

| Mobile banking adoption intention (CR = 0.955; AVE = 0.875) | |

| I am very likely to adopt mobile banking in the future | 0.957 * |

| I plan to adopt mobile banking in the future | 0.956 * |

| I believe it is worthwhile for me to adopt mobile banking | 0.893 * |

| Effort expectancy (CR =0.875; AVE = 0.637) | |

| I would find mobile banking useful in my daily life | 0.769 * |

| Using mobile banking would increase my chances of achieving things that are important to me | 0.810 * |

| Using mobile banking would help me accomplish things more quickly | 0.894 * |

| Using mobile banking would increase my productivity | 0.709 * |

| Performance expectancy (CR = 0.906; AVE = 0.708) | |

| Learning how to use mobile banking would be easy for me | 0.819 * |

| My interaction with mobile banking would be clear and understandable | 0.913 * |

| I find mobile banking would be easy to use | 0.828 * |

| It would be easy for me to become skillful at using mobile banking | 0.802 * |

| Social influence (CR = 0.934; AVE = 0.826) | |

| People who are important to me think that I should use mobile banking | 0.911 * |

| People who influence my behavior think that I should use mobile banking | 0.935 * |

| People whose opinions that I value prefer that I use mobile banking | 0.879 * |

| Facilitating conditions (CR = 0.856; AVE = 0.604) | |

| I have the resources necessary to use mobile banking | 0.720 * |

| I have the knowledge necessary to use mobile banking | 0.801 * |

| Mobile banking is compatible with other technologies I use | 0.774 * |

| I can get help from others when I have difficulties using mobile banking | 0.810 * |

| Hedonic motivation (CR = 0.918; AVE = 0.788) | |

| Using mobile banking would be fun | 0.877 * |

| Using mobile baking would be enjoyable | 0.910 * |

| Using mobile banking would be very entertaining | 0.875 * |

| Price value (CR = 0.869; AVE = 0.689) | |

| Mobile banking is reasonably priced | 0.814 * |

| Mobile baking is a good value for the money | 0.896 * |

| At the current price, mobile baking provides a good value | 0.776 * |

| Proactive personality (CR = 0.946; AVE = 0.638) | |

| I am constantly on the lookout for new ways to improve my life | 0.888 * |

| Wherever I have been, I have been a powerful force for constructive change | 0.784 * |

| Nothing is more exciting than seeing my ideas turn into reality | 0.603 * |

| If I see something I do not like, I fix it | 0.693 * |

| No matter what the odds, if I believe in something I will make it happen | 0.844 * |

| I love being a champion for my ideas, even against others’ opposition | 0.861 * |

| I excel at identifying opportunities | 0.857 * |

| I am always looking for better ways to do things | 0.817 * |

| If I believe in an idea, no obstacle will prevent me from making it happen | 0.788 * |

| I can spot a good opportunity long before others can | 0.809 * |

Note: S-B CHI-SQUARE: 1158.8003 (D.F. = 499) p < 0.001; CFI: 0.931; IFI: 0.932; RMSEA: 0.043. * p < 0.01.

Appendix B

Table A2.

Discriminant validity.

Table A2.

Discriminant validity.

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | |

|---|---|---|---|---|---|---|---|---|

| 1. Intention to Adopt | 0.875 | |||||||

| 2. Performance Exp. | 0.054 | 0.708 | ||||||

| 3. Effort Exp. | 0.014 | 0.453 | 0.637 | |||||

| 4. Social Influence | 0.027 | 0.482 | 0.166 | 0.826 | ||||

| 5. Facilitating Conditions | 0.016 | 0.514 | 0.500 | 0.365 | 0.604 | |||

| 6. Hedonic Motivation | 0.017 | 0.321 | 0.270 | 0.278 | 0.404 | 0.788 | ||

| 7. Price | 0.005 | 0.281 | 0.192 | 0.187 | 0.321 | 0.200 | 0.689 | |

| 8. Proactive Personality | 0.013 | 0.003 | 0.004 | 0.003 | 0.002 | 0.000 | 0.000 | 0.638 |

Note: Values on the diagonal represent the AVE. Squared correlations are shown.

Appendix C

Table A3.

Heterotrait–Monotrait Ratio (HTMT).

Table A3.

Heterotrait–Monotrait Ratio (HTMT).

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | |

|---|---|---|---|---|---|---|---|---|

| 1. Intention to Adopt | ||||||||

| 2. Performance Exp. | 0.853 | |||||||

| 3. Effort Exp. | 0.626 | 0.681 | ||||||

| 4. Social Influence | 0.592 | 0.671 | 0.397 | |||||

| 5. Facilitating Conditions | 0.679 | 0.708 | 0.705 | 0.586 | ||||

| 6. Hedonic Motivation | 0.448 | 0.564 | 0.514 | 0.493 | 0.643 | |||

| 7. Price | 0.421 | 0.460 | 0.325 | 0.310 | 0.463 | 0.344 | ||

| 8. Proactive Personality | 0.294 | 0.617 | 0.366 | 0.230 | 0.406 | 0.395 | 0.685 |

References

- Laukkanen, T. Consumer adoption versus rejection decisions in seemingly similar service innovations: The case of the Internet and mobile banking. J. Bus. Res. 2016, 69, 2432–2439. [Google Scholar] [CrossRef]

- Shankar, A.; Jebarajakirthy, C.; Ashaduzzaman, M.D. How do electronic word of mouth practices contribute to mobile banking adoption? J. Retail. Consum. Serv. 2020, 52, 101920. [Google Scholar] [CrossRef]

- Baabdullah, A.M.; Rana, N.P.; Alalwan, A.A.; Islam, R.; Patil, P.; Dwivedi, Y.K. Consumers’ Adoption of Self-Service Technologies in the Context of the Jordanian Banking Industry. Inf. Syst. Manag. 2019, 36, 286–305. [Google Scholar] [CrossRef]

- Muñoz-Leiva, F.; Climent-Climent, S.; Liébana-Cabanillas, F. Determinants of intention to use the mobile banking apps: An extension of the classic TAM model. Span. J. Mark. ESIC 2017, 21, 25–38. [Google Scholar] [CrossRef]

- Shareef, M.A.; Baabdullah, A.; Dutta, S.; Kumar, V.; Dwivedi, Y.K. Consumer adoption of mobile banking services: An empirical examination of factors according to adoption stages. J. Retail. Consum. Serv. 2018, 43, 54–67. [Google Scholar] [CrossRef]

- McLean, G.; Osei-Frimpong, K.; Al-Nabhani, K.; Marriott, H. Examining consumer attitudes towards retailers’ m-commerce mobile applications—An initial adoption vs. continuous use perspective. J. Bus. Res. 2020, 106, 139–157. [Google Scholar] [CrossRef]

- Flavián, C.; Guinaliu, M.; Lu, Y. Mobile payments adoption—Introducing mindfulness to better understand consumer behavior. Int. J. Bank Mark. 2020, 38, 1575–1599. [Google Scholar] [CrossRef]

- Zhang, J.; Mao, E. Cash, credit, or phone? An empirical study on the adoption of mobile payments in the United States. Psychol. Mark. 2019, 37, 87–98. [Google Scholar] [CrossRef]

- Santini, F.D.O.; Ladeira, W.J.; Sampaio, C.; Perin, M.G.; Dolci, P.C. A meta-analytical study of technological acceptance in banking contexts. Int. J. Bank Mark. 2019, 37, 755–774. [Google Scholar] [CrossRef]

- Jadil, Y.; Rana, N.P.; Dwivedi, Y.K. A meta-analysis of the UTAUT model in the mobile banking literature: The moderating role of sample size and culture. J. Bus. Res. 2021, 132, 354–372. [Google Scholar] [CrossRef]

- Sahoo, D.; Pillai, S. Role of mobile banking servicescape on customer attitude and engagement: An empirical investigation in India. Int. J. Bank Mark. 2017, 35, 1115–1132. [Google Scholar] [CrossRef]

- Moser, F. M-banking: A fashionable concept or an institutionalized channel in future retail banking? Analyzing patterns in the practical and academic mobile banking literature. Int. J. Bank Mark. 2015, 33, 162–177. [Google Scholar] [CrossRef]

- Shankar, A.; Rishi, B. Convenience Matter in Mobile Banking Adoption Intention? Australas. Mark. J. 2020, 28, 273–285. [Google Scholar] [CrossRef]

- Alalwan, A.A.; Dwivedi, Y.K.; Williams, M.D. Customers’ intention and adoption of telebanking in Jordan. Inf. Syst. Manag. 2016, 33, 154–178. [Google Scholar] [CrossRef]

- Ha, K.-H.; Canedoli, A.; Baur, A.W.; Bick, M. Mobile banking—Insights on its increasing relevance and most common drivers of adoption. Electron. Mark. 2012, 22, 217–227. [Google Scholar] [CrossRef]

- Zhou, T.; Lu, Y.; Wang, B. Integrating TTF and UTAUT to explain mobile banking user adoption. Comput. Hum. Behav. 2010, 26, 760–767. [Google Scholar] [CrossRef]

- Akturan, U.; Tezcan, N. Mobile banking adoption of the youth market: Perceptions and intentions. Mark. Intell. Plan. 2012, 30, 444–459. [Google Scholar] [CrossRef]

- Chawla, D.; Joshi, H. Consumer perspectives about mobile banking adoption in India–a cluster analysis. Int. J. Bank Mark. 2017, 35, 616–636. [Google Scholar] [CrossRef]

- Zhou, T. Examining mobile banking user adoption from the perspectives of trust and flow experience. Inf. Technol. Manag. 2011, 13, 27–37. [Google Scholar] [CrossRef]

- Chaouali, W.; Souiden, N. The role of cognitive age in explaining m-banking resistance among elderly people. J. Retail. Consum. Serv. 2019, 50, 342–350. [Google Scholar] [CrossRef]

- Fall, F.S.; Orozco, L.; Akim, A. Adoption and use of mobile banking by low-income individuals in Senegal. Rev. Dev. Econ. 2020, 24, 569–588. [Google Scholar] [CrossRef]

- Kishore, S.V.; Sequeira, A.H. An empirical investigation on mobile banking service adoption in rural Karnataka. SAGE Open 2016, 16, 2158244016633731. [Google Scholar] [CrossRef]

- Siano, A.; Raimi, L.; Palazzo, M.; Panait, M. Mobile Banking: An Innovative Solution for Increasing Financial Inclusion in Sub-Saharan African Countries. Evidence from Nigeria. Sustainability 2020, 12, 10130. [Google Scholar] [CrossRef]

- Malaquias, R.F.; Hwang, Y. M-banking use: A comparative study with Brazilian and U.S. participants. Int. J. Inf. Manag. 2019, 44, 132–140. [Google Scholar] [CrossRef]

- Giovanis, A.; Athanasopoulou, P.; Assimakopoulos, C.; Sarmaniotis, C. Adoption of m-banking services. Int. J. Bank Mark. 2019, 37, 1165–1189. [Google Scholar] [CrossRef]

- Ali, A.; Subramanian, R. Current Status of Research on Mobile Banking: An Analysis of Literature. Vision 2022, 09722629211073268. [Google Scholar] [CrossRef]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User acceptance of computer technology: A comparison of two theoretical models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.; Davis, G.; Davis, F. User acceptance of information technology: Toward a unified view. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Albashrawi, M.; Kartal, H.; Oztekin, A.; Motiwalla, L. Self-Reported and Computer-Recorded Experience in Mobile Banking: A Multi-Phase Path Analytic Approach. Inf. Syst. Front. 2019, 21, 773–790. [Google Scholar] [CrossRef]

- Venkatesh, V.; Thong, J.Y.; Xu, X. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Q. 2012, 36, 157–178. [Google Scholar] [CrossRef]

- Lee, S.W.; Sung, H.J.; Jeon, H.M. Determinants of Continuous Intention on Food Delivery Apps: Extending UTAUT2 with Information Quality. Sustainability 2019, 11, 3141. [Google Scholar] [CrossRef]

- Shi, Y.; Siddik, A.B.; Masukujjaman, M.; Zheng, G.; Hamayun, M.; Ibrahim, A.M. The Antecedents of Willingness to Adopt and Pay for the IoT in the Agricultural Industry: An Application of the UTAUT 2 Theory. Sustainability 2022, 14, 6640. [Google Scholar] [CrossRef]

- Alalwan, A.A.; Dwivedi, Y.K.; Rana, N.P. Factors influencing adoption of m-banking by Jordanian bank customers: Extending UTAUT2 with trust. Int. J. Inf. Manag. 2017, 37, 99–110. [Google Scholar] [CrossRef]

- Baabdullah, A.M.; Alalwan, A.A.; Rana, N.P.; Kizgin, H.; Patil, P. Consumer use of mobile banking (M-Banking) in Saudi Arabia: Towards an integrated model. Int. J. Inf. Manag. 2019, 44, 38–52. [Google Scholar] [CrossRef]

- Crant, J.M. Proactive behavior in organizations. J. Manag. 2000, 26, 435–462. [Google Scholar] [CrossRef]

- Grant, A.M.; Ashford, S.J. The dynamics of proactivity at work. Res. Organ. Behav. 2008, 28, 3–34. [Google Scholar] [CrossRef]

- Lin, S.H.; Lu, W.C.; Chen, M.Y.; Chen, L.H. Association between proactive personality and academic self–efficacy. Curr. Psychol. 2014, 33, 600–609. [Google Scholar] [CrossRef]

- Parker, S.K.; Collins, C.G. Taking Stock: Integrating and Differentiating Multiple Proactive Behaviors. J. Manag. 2010, 36, 633–662. [Google Scholar] [CrossRef]

- Chen, N.Y.-F.; Crant, J.M.; Wang, N.; Kou, Y.; Qin, Y.; Yu, J.; Sun, R. When there is a will there is a way: The role of proactive personality in combating COVID-19. J. Appl. Psychol. 2021, 106, 199–213. [Google Scholar] [CrossRef]

- Neneh, B.N. From entrepreneurial alertness to entrepreneurial behavior: The role of trait competitiveness and proactive personality. Pers. Individ. Differ. 2019, 138, 273–279. [Google Scholar] [CrossRef]

- Sun, J.; Li, Y.; Li, S.; Li, W.; Liden, R.C.; Zhang, X. Unintended consequences of being proactive? Linking proactive personality to coworker envy, helping, and undermining, and the moderating role of prosocial motivation. J. Appl. Psychol. 2020, 106, 250–267. [Google Scholar] [CrossRef] [PubMed]

- Hough, L.M.; Schneider, R.J. Personality traits, taxonomies, and applications in organization. In Individual Differences and Behavior in Organizations; Murphy, K.R., Ed.; Jossey-Bass: San Francisco, CA, USA, 1996; pp. 31–88. [Google Scholar]

- Spitzmuller, M.; Sin, H.-P.; Howe, M.; Fatimah, S. Investigating the Uniqueness and Usefulness of Proactive Personality in Organizational Research: A Meta-Analytic Review. Hum. Perform. 2015, 28, 351–379. [Google Scholar] [CrossRef]

- Costa, P.; McCrae, R.R. The Five-Factor Model of Personality and Its Relevance to Personality Disorders. J. Pers. Disord. 1992, 6, 343–359. [Google Scholar] [CrossRef]

- Sharif, A.; Raza, S.A. The influence of hedonic motivation, self-efficacy, trust and habit on adoption of internet banking: A case of developing country. Int. J. Electron. Cust. Relatsh. Manag. 2017, 11, 1–22. [Google Scholar] [CrossRef]

- McElroy, J.C.; Hendrickson, A.; Townsend, A.M.; DeMarie, S.M. Dispositional Factors in Internet Use: Personality versus Cognitive Style. MIS Q. 2007, 31, 809. [Google Scholar] [CrossRef]

- Xu, R.; Frey, R.M.; Fleisch, E.; Ilic, A. Understanding the impact of personality traits on mobile app adoption. Insights from a large-scale field study. Comput. Hum. Behav. 2016, 62, 244–256. [Google Scholar] [CrossRef]

- Fishbein, M.; Ajzen, I. Belief, Attitude. Intention and Behavior: An Introduction to Theory and Research; Addison-Wesley: Reading, MA, USA, 1975. [Google Scholar]

- Giovanis, A.; Assimakopoulos, C.; Sarmaniotis, C. Adoption of mobile self-service retail banking technologies: The role of technology, social, channel and personal factors. Int. J. Retail. Distrib. Manag. 2019, 47, 894–914. [Google Scholar] [CrossRef]

- Gu, J.-C.; Lee, S.-C.; Suh, Y.-H. Determinants of behavioral intention to mobile banking. Expert Syst. Appl. 2009, 36, 11605–11616. [Google Scholar] [CrossRef]

- Singh, S.; Srivastava, R. Predicting the intention to use m-banking in India. Int. J. Bank Mark. 2018, 36, 357–378. [Google Scholar] [CrossRef]

- Dwivedi, Y.K.; Rana, N.P.; Jeyaraj, A.; Clement, M.; Williams, M.D. Re-examining the Unified Theory of Acceptance and Use of Technology (UTAUT): Towards a Revised Theoretical Model. Inf. Syst. Front. 2019, 21, 719–734. [Google Scholar] [CrossRef]

- Alalwan, A.A.; Dwivedi, Y.K.; Rana, N.P.P.; Williams, M.D. Consumer adoption of mobile banking in Jordan: Examining the role of usefulness, ease of use, perceived risk and self-efficacy. J. Enterp. Inf. Manag. 2016, 29, 118–139. [Google Scholar] [CrossRef]

- Mohammadi, H. A study of mobile banking loyalty in Iran. Comput. Hum. Behav. 2015, 44, 35–47. [Google Scholar] [CrossRef]

- Tamilmani, K.; Rana, N.P.; Wamba, S.F.; Dwivedi, R. The extended Unified Theory of Acceptance and Use of Technology (UTAUT2): A systematic literature review and theory evaluation. Int. J. Inf. Manag. 2021, 57, 102269. [Google Scholar] [CrossRef]

- Martín-San, S.; Jiménez, N.H.; Camarero, C.; San-Jose, R. The path between personality, self-efficacy, and shopping regarding games apps. J. Theor. Appl. Electron. Commer. Res. 2020, 15, 59–75. [Google Scholar] [CrossRef]

- Agyei, J.; Sun, S.; Abrokwah, E.; Penney, E.K.; Ofori-Boafo, R. Mobile Banking Adoption: Examining the Role of Personality Traits. SAGE 2020, 10. [Google Scholar] [CrossRef]

- Changchun, G.; Haider, M.J.; Akram, T. Investigation of the effects of task technology fit, attitude and trust on intention to adopt mobile banking: Placing the mediating role of trialability. Int. Bus. Res. 2017, 10, 77–91. [Google Scholar] [CrossRef]

- Tam, C.; Oliveira, T. Literature review of m-banking and individual performance. Int. J. Bank Mark. 2017, 35, 1044–1067. [Google Scholar] [CrossRef]

- Karjaluoto, H.; Glavee-Geo, R.; Ramdhony, D.; Shaikh, A.A.; Hurpaul, A. Consumption values and mobile banking services: Understanding the urban–rural dichotomy in a developing economy. Int. J. Bank Mark. 2021, 39, 272–293. [Google Scholar] [CrossRef]

- Baptista, G.; Oliveira, T. Understanding mobile banking: The unified theory of acceptance and use of technology combined with cultural moderators. Comput. Hum. Behav. 2015, 50, 418–430. [Google Scholar] [CrossRef]

- Shaikh, A.A.; Glavee-Geo, R.; Karjaluoto, H. How relevant are risk perceptions, effort, and performance expectancy in mobile banking adoption? Int. J. E-Bus. Res. 2018, 14, 39–60. [Google Scholar] [CrossRef]

- Barnes, S.J.; Corbitt, B. Mobile Banking: Concept and Potential. Int. J. Mob. Commun. 2003, 1, 273–288. [Google Scholar] [CrossRef]

- Laforet, S.; Li, X. Consumers’ attitudes towards online and mobile banking in China. Int. J. Bank Mark. 2005, 23, 362–380. [Google Scholar] [CrossRef]

- Akhtar, S.; Irfan, M.; Sarwar, A.; Asma; Rashid, Q.U.A. Factors influencing individuals’ intention to adopt mobile banking in China and Pakistan: The moderating role of cultural values. J. Public Aff. 2019, 19, e1884. [Google Scholar] [CrossRef]

- Albashrawi, M.; Motiwalla, L. Privacy and Personalization in Continued Usage Intention of Mobile Banking: An Integrative Perspective. Inf. Syst. Front. 2019, 21, 1031–1043. [Google Scholar] [CrossRef]

- Bermeo Giraldo, M.C.; Benjumea-Arias, M.L.; Valencia-Arias, A.; Montoya-Restrepo, I.A. Factors Determining the Use and Acceptance of Mobile Banking in Colombia. J. Telecommun. Digit. Econ. 2021, 9, 44–74. [Google Scholar] [CrossRef]

- Bustami, E.; Situngkir, S.; Yacob, S.; Octavia, A. Customers’ behavioral intention on mobile banking services in Indonesia. Int. J. Res. Bus. Soc. Sci. 2021, 10, 353–362. [Google Scholar] [CrossRef]

- Elhajjar, S.; Ouaida, F. An analysis of factors affecting mobile banking adoption. Int. J. Bank Mark. 2020, 38, 352–367. [Google Scholar] [CrossRef]

- Hassan, H.; Wood, V.R. Does country culture influence consumers’ perceptions toward mobile banking? A comparison between Egypt and the United States. Telemat. Inform. 2020, 46, 101312. [Google Scholar] [CrossRef]

- Lee, J.; Ryu, M.H.; Lee, D. A study on the reciprocal relationship between user perception and retailer perception on platform-based mobile payment service. J. Retail. Consum. Serv. 2019, 48, 7–15. [Google Scholar] [CrossRef]

- Malaquias, R.F.; Silva, A.F. Understanding the use of mobile banking in rural areas of Brasil. Technol. Soc. 2020, 62, 101260. [Google Scholar] [CrossRef]

- Milly, N.; Xun, S.; Meena, M.E.; Cobbinah, B.B. Measuring Mobile Banking Adoption in Uganda Using the Technology Acceptance Model (TAM2) and Perceived Risk. Open J. Bus. Manag. 2021, 09, 397–418. [Google Scholar] [CrossRef]

- Naruetharadhol, P.; Ketkaew, C.; Hongkanchanapong, N.; Thaniswannasri, P.; Uengkusolmongkol, T.; Prasomthong, S.; Gebsombut, N. Factors Affecting Sustainable Intention to Use Mobile Banking Services. SAGE Open 2021, 11. [Google Scholar] [CrossRef]

- Nguyen, V.A.; Nguyen, T.P.T. An Integrated Model of CSR Perception and TAM on Intention to Adopt Mobile Banking. J. Asian Financ. Econ. Bus. 2020, 7, 1073–1087. [Google Scholar] [CrossRef]

- Rehman, Z.; Omar, S.; Zabri, S.; Lohana, S. Mobile Banking Adoption and its Determinants in Malaysia. Int. J. Innov. Technol. Explor. Eng. 2019, 9, 4231–4239. [Google Scholar] [CrossRef]

- Siyal, A.W.; Donghong, D.; Umrani, W.A.; Siyal, S.; Bhand, S. Predicting Mobile Banking Acceptance and Loyalty in Chinese Bank Customers. SAGE Open 2019, 9. [Google Scholar] [CrossRef]

- Tiwari, P.; Tiwari, S.K.; Gupta, A. Examining the Impact of Customers’ Awareness, Risk and Trust in M-Banking Adoption. FIIB Bus. Rev. 2021, 10, 413–423. [Google Scholar] [CrossRef]

- Tam, C.; Oliveira, T. Does culture influence m-banking use and individual performance? Inf. Manag. 2019, 56, 356–363. [Google Scholar] [CrossRef]

- Motiwalla, L.F.; Albashrawi, M.; Kartal, H.B. Uncovering unobserved heterogeneity bias: Measuring mobile banking system success. Int. J. Inf. Manag. 2019, 49, 439–451. [Google Scholar] [CrossRef]

- Sharma, S.K.; Sharma, M. Examining the role of trust and quality dimensions in the actual usage of mobile banking services: An empirical investigation. Int. J. Inf. Manag. 2019, 44, 65–75. [Google Scholar] [CrossRef]

- Chaouali, W.; Lunardo, R.; Ben Yahia, I.; Cyr, D.; Triki, A. Design aesthetics as drivers of value in mobile banking: Does customer happiness matter? Int. J. Bank Mark. 2019, 38, 219–241. [Google Scholar] [CrossRef]

- Jebarajakirthy, C.; Shankar, A. Impact of online convenience on mobile banking adoption intention: A moderated mediation approach. J. Retail. Consum. Serv. 2021, 58, 102323. [Google Scholar] [CrossRef]

- Foroughi, B.; Iranmanesh, M.; Hyun, S.S. Understanding the determinants of mobile banking continuance usage intention. J. Enterp. Inf. Manag. 2019, 32, 1015–1033. [Google Scholar] [CrossRef]

- Chaouali, W.; El Hedhli, K. Toward a contagion-based model of m-banking adoption. Int. J. Bank Mark. 2019, 37, 69–96. [Google Scholar] [CrossRef]

- Albashrawi, M. Mobile banking continuance intention: The moderating role of security and customization. J. Inf. Technol. Res. 2021, 14, 55–69. [Google Scholar] [CrossRef]

- Banerjee, S.; Sreejesh, S. Examining the role of customers’ intrinsic motivation on continued usage of mobile banking: A relational approach. Int. J. Bank Mark. 2021, 40, 87–109. [Google Scholar] [CrossRef]

- Komulainen, H.; Saraniemi, S. Customer centricity in m-banking: A customer experience perspective. Int. J. Bank Mark. 2019, 37, 1082–1102. [Google Scholar] [CrossRef]

- Prodanova, J.; Ciunova-Shuleska, A.; Palamidovska-Sterjadovska, N. Enriching m-banking perceived value to achieve reuse intention. Mark. Intell. Plan. 2019, 37, 617–630. [Google Scholar] [CrossRef]