ESG Factor Integration into Private Equity

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

- RQ1: Do PE firms consider ESG factors important?

- RQ2: Why do PE firms believe that ESG factors are important?

- RQ3: What kinds of activities do PE firms engage in relative to ESG factors?

- RQ4: What tools do PE firms mainly use for ESG integration?

- RQ5: What criteria do PE firms rely on when deciding whether to perform ESG due diligence?

- RQ6: What are the dominant barriers to ESG integration into PE?

2. ESG Factors and Their Integration into Private Equity

3. Materials and Methods

- Do you have direct experience with ESG factor integration into PE activities?

- Do you think there is a need to integrate ESG factors into due diligence? If so, why?

- What are the dominant barriers to ESG integration into PE?

- How are ESG factors integrated into PE activities?

- In which ESG aspects are you most interested?

- Do you think that ESG factors depend on the industry?

- Do you have ESG experts on your team?

- Do you refer to external experts?

- Do you have your own ESG assessment methodology?

- Do you refer to standards?

- Do you refer to external ESG assessment experts?

- Did your investors explicitly ask for ESG integration?

- Have you ever increased the value of a firm in your portfolio through ESG initiatives?

- Do you think that ESG public information is enough?

4. Results

5. Discussion

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

- (1)

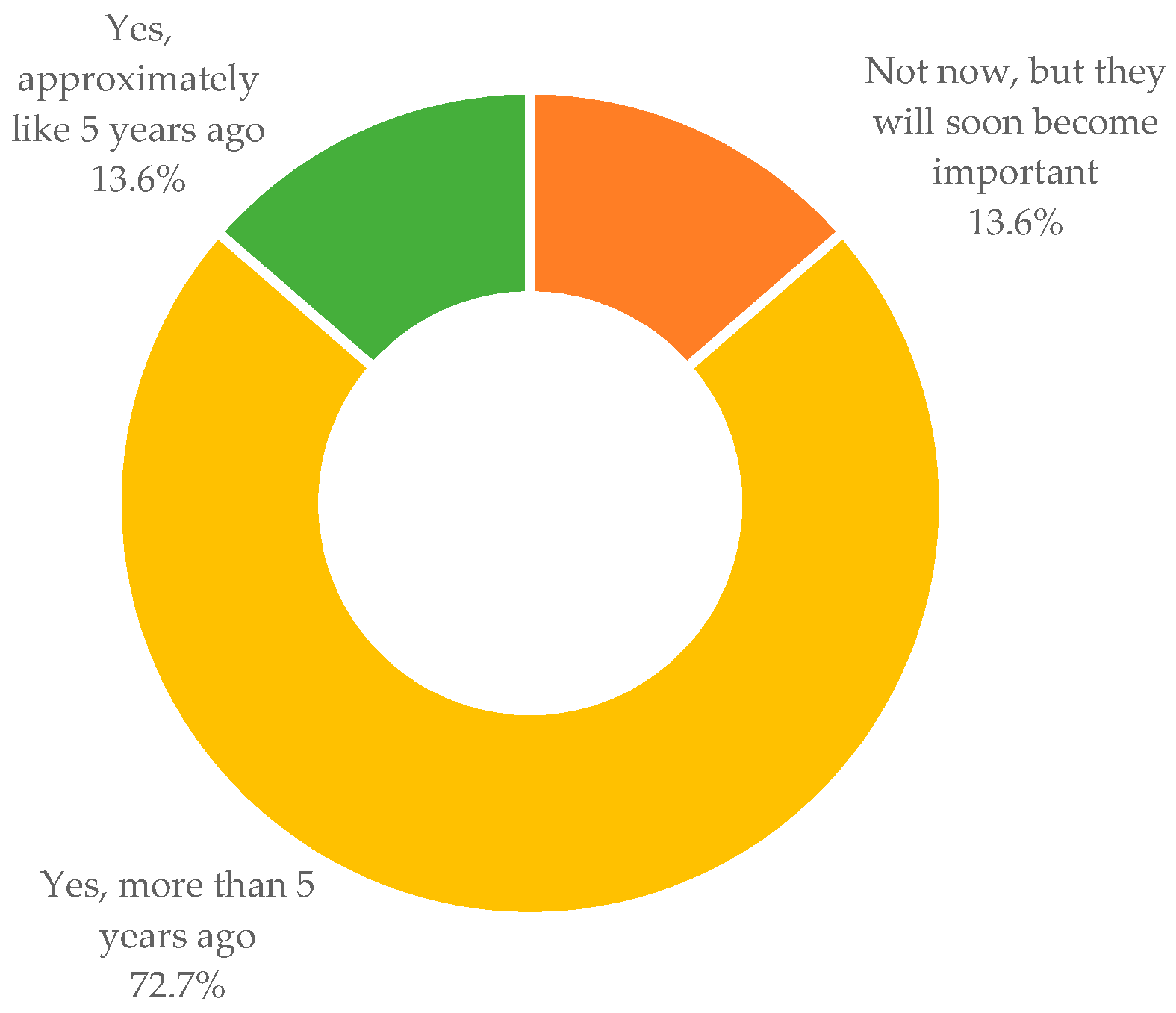

- Does your firm consider environmental, social and governance (ESG) factors important in Private Equity activities?

- Yes, more than 5 years ago

- Yes, approximately like 5 years ago

- Not now, but they will soon become important

- Not at all

- (2)

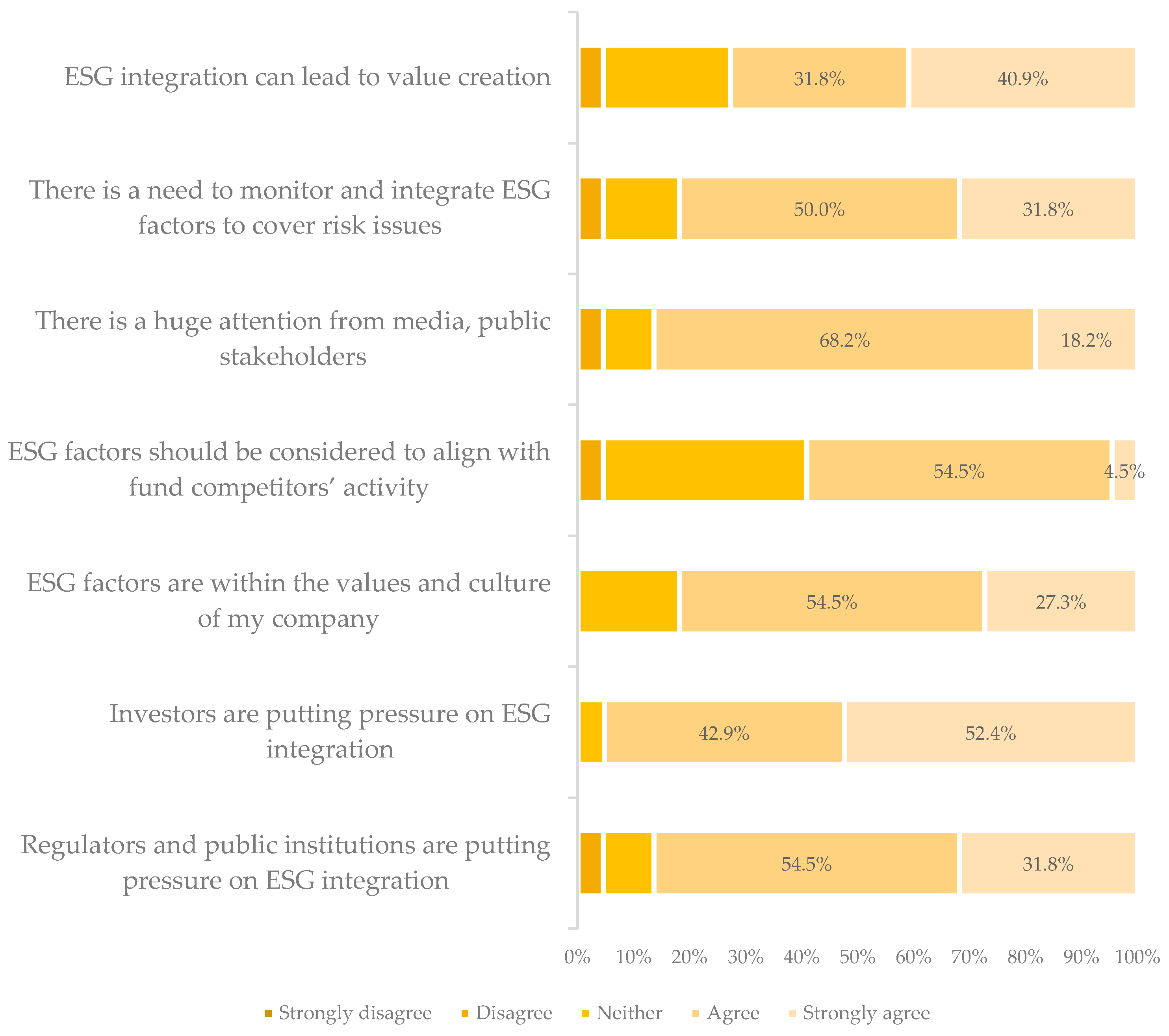

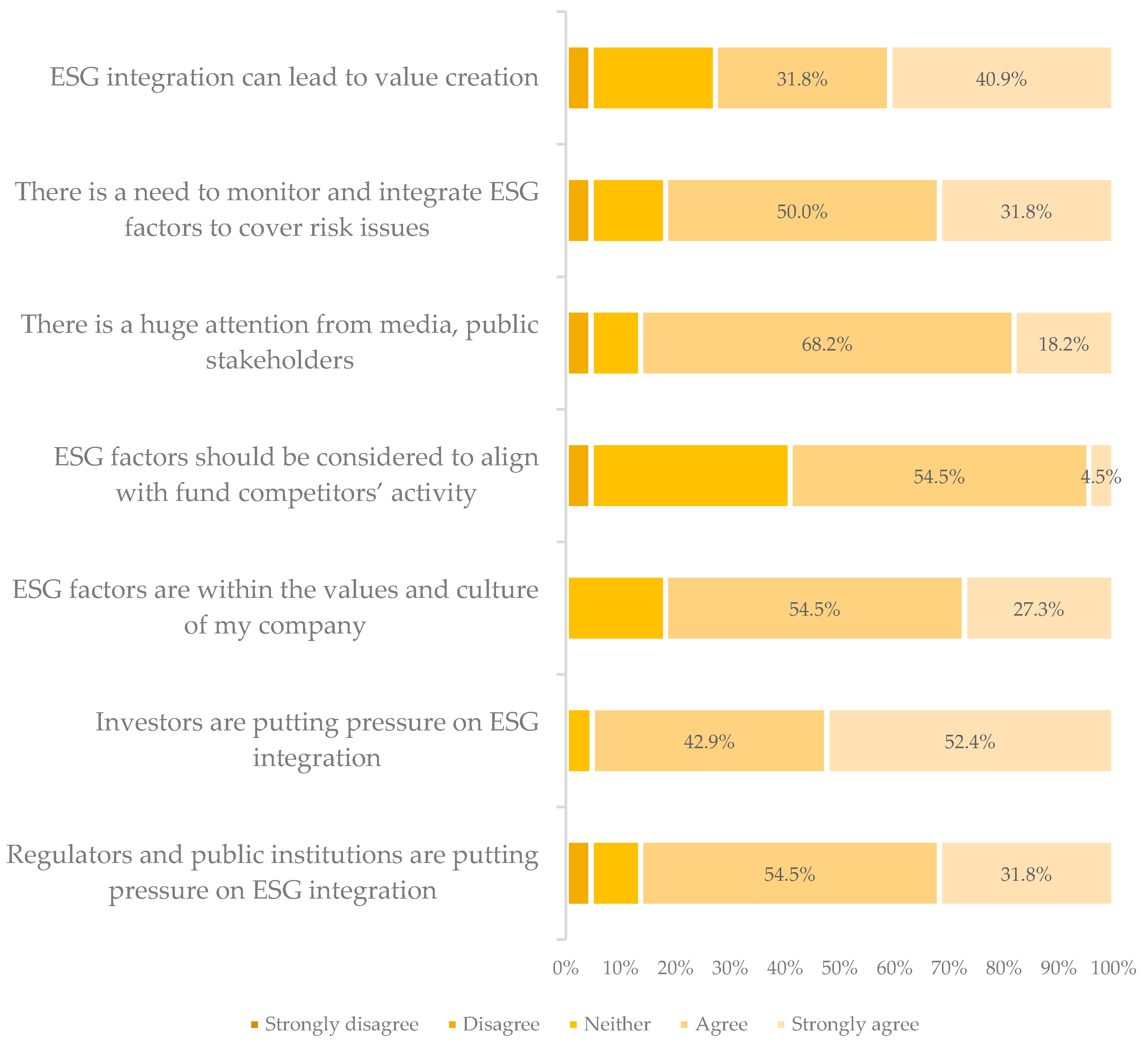

- Why ESG factors are becoming increasingly important? (1 = Strongly disagree, 2 = Disagree, 3 = Neither, 4 = Agree, 5 = Strongly agree)

- Regulators and public institutions are putting pressure on ESG integration

- Investors are putting pressure on ESG integration

- ESG factors are within the values and culture of my company

- ESG factors should be considered to align with fund competitors’ activity

- There is a huge attention from media, public stakeholders

- There is a need to monitor and integrate ESG factors to cover risk issues

- (3)

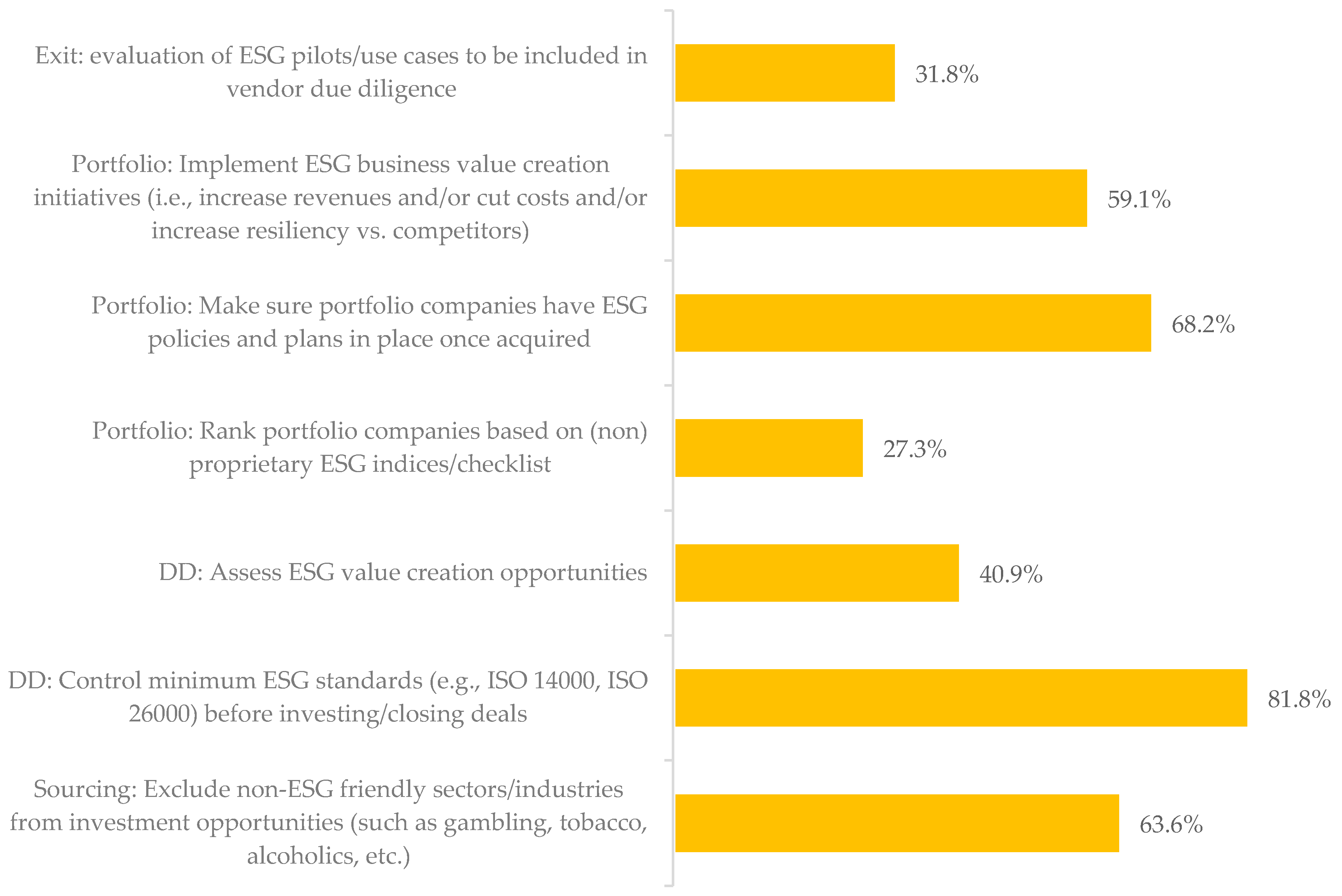

- Regarding ESG, what does your firm do?

- Sourcing: Exclude non-ESG friendly sectors/industries from investment opportunities (such as gambling, tobacco, alcoholics, etc.)

- DD: Control minimum ESG standards before investing/closing deals

- DD: assess ESG value creation opportunities

- Portfolio: Rank portfolio companies based on (non) proprietary ESG indices/checklist

- Portfolio: Make sure portfolio companies have ESG policies and plans in place once acquired

- Portfolio: Implement ESG business value creation (i.e., increase revenues and/or cut costs and/or increase resiliency versus competitors)

- Exit: evaluation of ESG pilots/use cases to be included in vendor due diligence

- Nothing

- Other (please specify)

- (4)

- Considering your firm due diligence activities, indicate how strongly do you agree or disagree with each statement. (1 = Strongly disagree, 2 = Disagree, 3 = Neither, 4 = Agree, 5 = Strongly agree)

- Environmental factors are more important today versus 5 years ago

- Environmental factors will become more important in 5 years versus today

- Social factors are more important today versus 5 years ago

- Social factors will become more important in 5 years versus today

- Governance factors are more important today versus 5 years ago

- Governance factors will become more important in 5 years versus today

- (5)

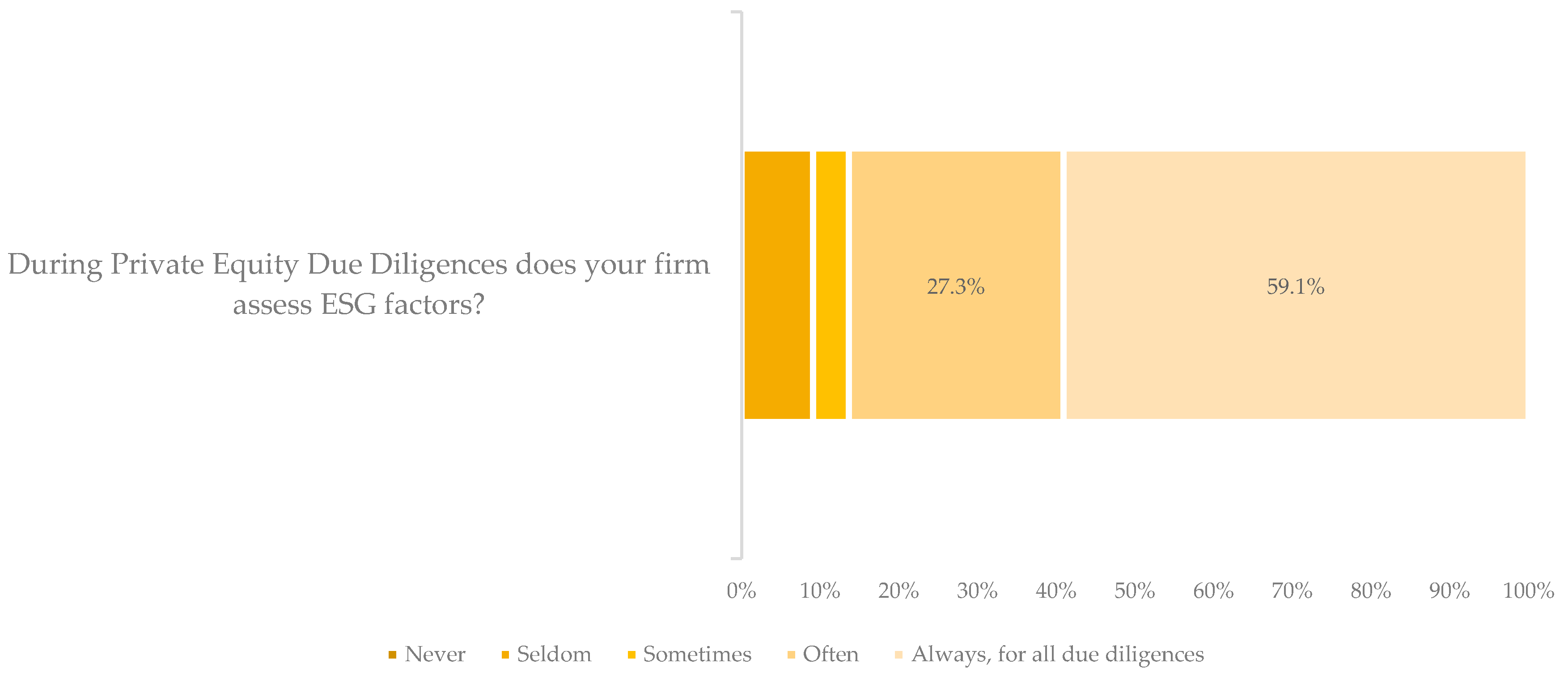

- During private equity due diligences, does your firm assess ESG factors?

- Always, for all due diligences

- Often

- Sometimes

- Seldom

- Not at all

- (6)

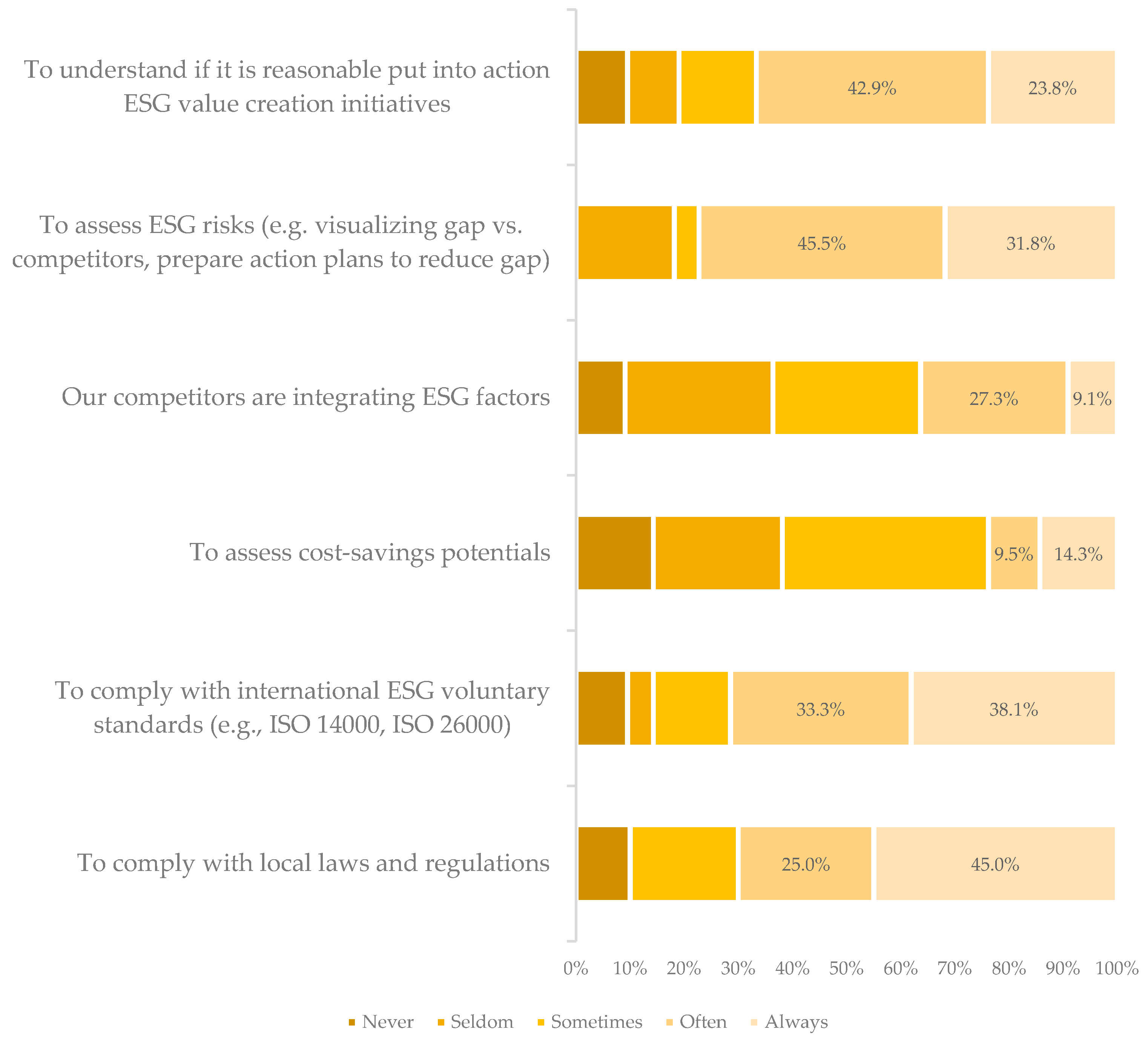

- Which are the main reasons why your firm perform ESG due diligences? (1 = Never, 2 = Seldom, 3 = Sometimes, 4 = Often, 5 = Always)

- To comply with local laws and regulations

- To comply with international ESG voluntary standards

- To assess cost-savings potentials

- Our competitors are integrating ESG factors

- To assess ESG risks (e.g., visualizing gap versus competitors, prepare action plans to reduce gap)

- To understand if it is reasonable put into action ESG value creation initiatives

- For other reasons

- (7)

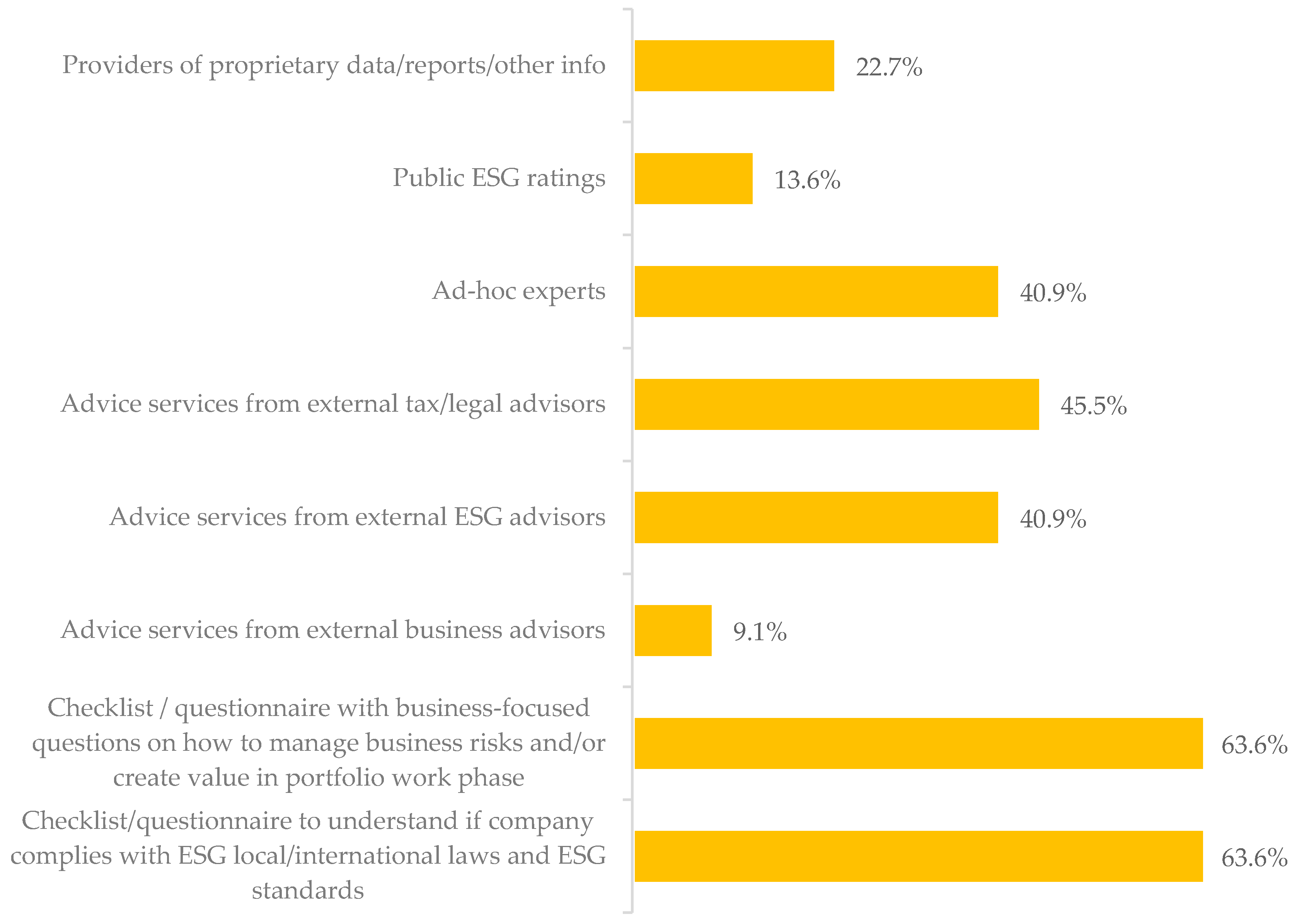

- When assessing ESG factors, which of the following tools does your firm use?

- Checklist/questionnaire to understand if company complies with ESG local/international laws and ESG standards

- Checklist/questionnaire with business-focused questions on how to manage business risks and/or create value in portfolio work phase

- Advice services from external business advisors

- Advice services from external ESG advisors

- Advice services from external tax/legal/other advisors

- Ad-hoc experts (e.g., industry experts with previous work on ESG, former ESG directors of PE funds, etc.)

- Public ESG ratings

- Providers of proprietary data/reports/other info

- Others

- (8)

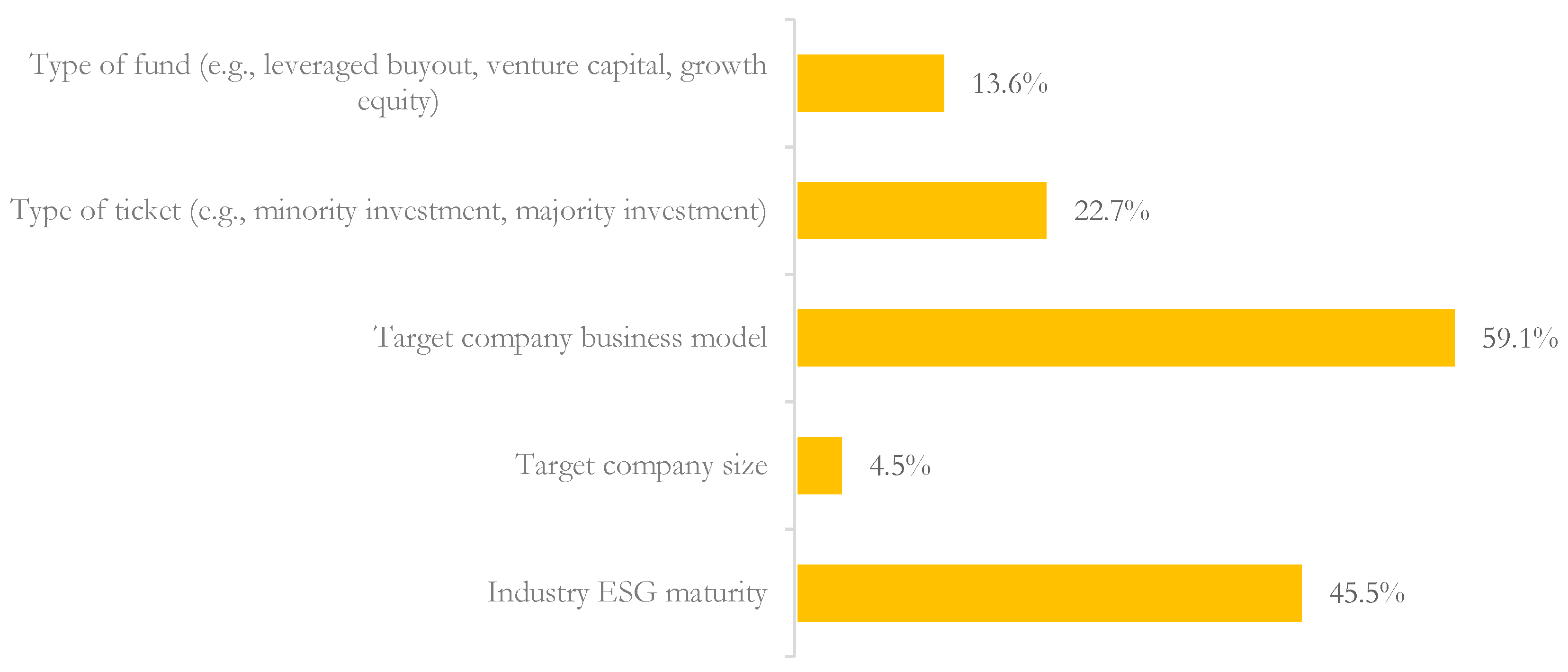

- Which criteria does your firm rely on when deciding whether to perform an ESG due diligence?

- Industry ESG maturity

- Target company size

- Target company business model

- Type of ticket (e.g., minority investment, majority investment)

- Type of fund (e.g., leveraged buyout, venture capital, growth equity)

- Other

- (9)

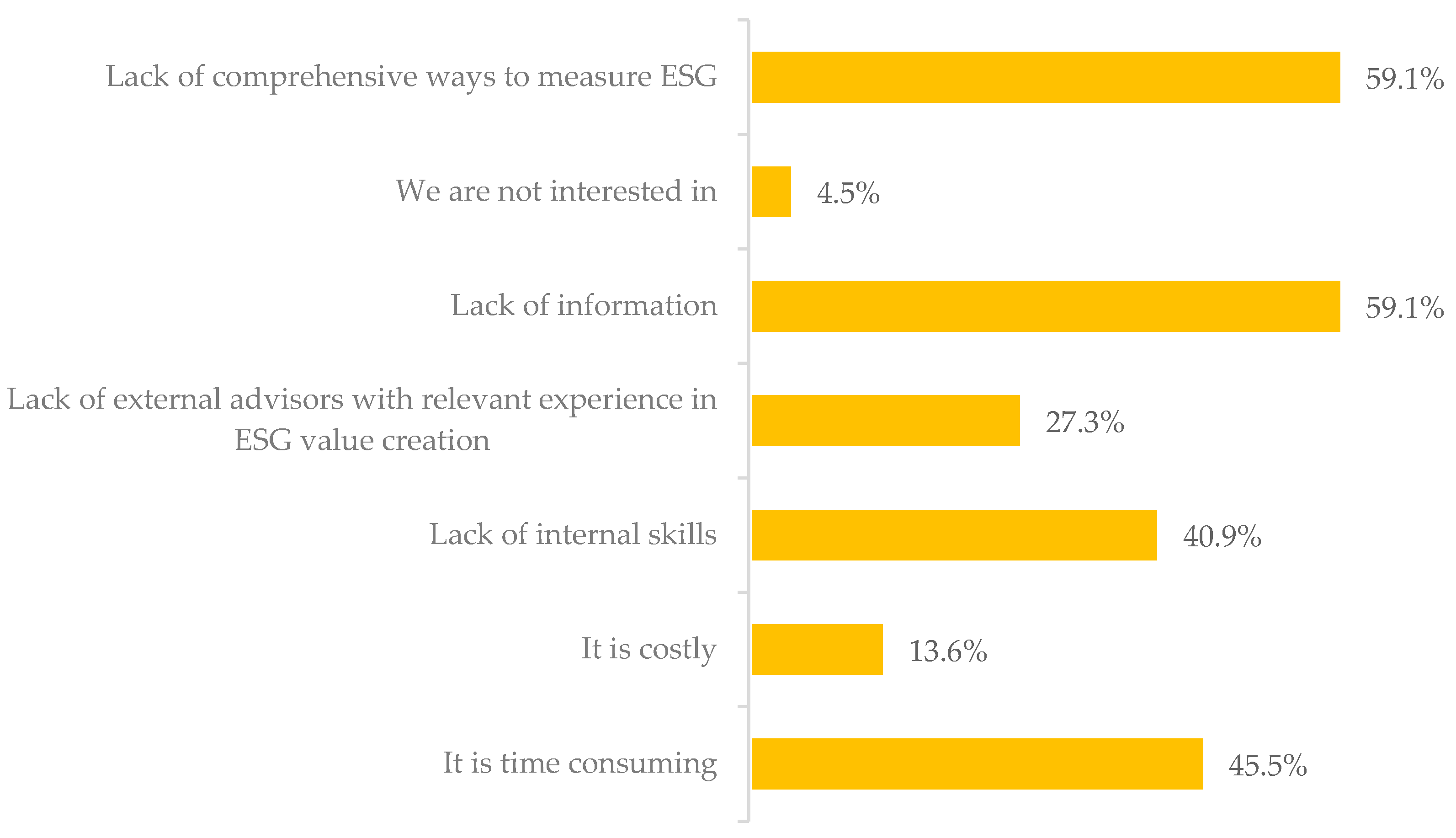

- Which are the dominant barriers for ESG integration into due diligence?

- It is time consuming

- It is costly

- Lack of internal skills

- Lack of external advisors with relevant experience in ESG value creation

- Lak of information

- We are not interested in

- Lack of comprehensive ways to measure ESG

- Other

References

- Freestone, O.M.; McGoldrick, P.J. Motivations of the ethical consumer. J. Bus. Ethics 2008, 79, 445–467. [Google Scholar] [CrossRef]

- Shaw, D.; Shiu, E. The role of ethical obligation and self-identity in ethical consumer choice. Int. J. Consum. Stud. 2002, 26, 109–116. [Google Scholar] [CrossRef]

- Pedrini, M.; Ferri, L.M. Socio-demographical antecedents of responsible consumerism propensity. Int. J. Consum. Stud. 2014, 38, 127–138. [Google Scholar] [CrossRef]

- Young, W.; Hwang, K.; McDonald, S.; Oates, C.J. Sustainable consumption: Green consumer behaviour when purchasing products. Sustain. Dev. 2010, 18, 20–31. [Google Scholar] [CrossRef]

- Perrons, D. The new economy and the work–life balance: Conceptual explorations and a case study of new media. Gend. Work Organ. 2003, 10, 65–93. [Google Scholar] [CrossRef]

- Di Fabio, A. Positive Healthy Organizations: Promoting well-being, meaningfulness, and sustainability in organizations. Front. Psychol. 2017, 8, 1938. [Google Scholar] [CrossRef]

- Pedrini, M.; Ferri, L.M.; Riva, E. Institutional pressures and internal motivations of work-life balance organisational arrangements in Italy. Int. J. Hum. Resour. Dev. Manag. 2018, 18, 257–281. [Google Scholar] [CrossRef]

- Guo, Y.; Xia, X.; Zhang, S.; Zhang, D. Environmental regulation, government R&D funding and green technology innovation: Evidence from China provincial data. Sustainability 2018, 10, 940. [Google Scholar]

- Amel-Zadeh, A.; Serafeim, G. Why and how investors use ESG information: Evidence from a global survey. Financ. Anal. J. 2018, 74, 87–103. [Google Scholar] [CrossRef]

- Escrig-Olmedo, E.; Rivera-Lirio, J.M.; Muñoz-Torres, M.J.; Fernández-Izquierdo, M.Á. Integrating multiple ESG investors’ preferences into sustainable investment: A fuzzy multicriteria methodological approach. J. Cleaner Prod. 2017, 162, 1334–1345. [Google Scholar] [CrossRef]

- Eccles, R.G.; Klimenko, S. The investor revolution. Harv. Bus. Rev. 2019, 97, 106–116. [Google Scholar]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Bansal, P.; Roth, K. Why companies go green: A model of ecological responsiveness. Acad. Manag. Rev. 2000, 43, 717–748. [Google Scholar]

- Hemingway, C.A.; Maclagan, P.W. Managers’ personal values as drivers of corporate social responsibility. J. Bus. Ethics 2004, 50, 33–44. [Google Scholar] [CrossRef]

- Barnett, M.L.; Salomon, R.M. Beyond dichotomy: The curvilinear relationship between social responsibility and financial performance. Strateg. Manag. J. 2006, 27, 1101–1122. [Google Scholar] [CrossRef]

- Luo, X.M.; Bhattacharya, C.B. Corporate social responsibility, customer satisfaction, and market value. J. Mark. 2006, 70, 1–18. [Google Scholar] [CrossRef]

- Margolis, J.D.; Walsh, J.P. Misery loves companies: Rethinking social initiatives by business. Adm. Sci. Q. 2003, 48, 268–305. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Zhao, C.; Guo, Y.; Yuan, J.; Wu, M.; Li, D.; Zhou, Y.; Kang, J. ESG and corporate financial performance: Empirical evidence from China’s listed power generation companies. Sustainability 2018, 10, 2607. [Google Scholar] [CrossRef]

- Ramchander, S.; Schwebach, R.G.; Staking, K. The informational relevance of corporate social responsibility: Evidence from DS400 index reconstitutions. Strateg. Manag. J. 2012, 33, 303–314. [Google Scholar] [CrossRef]

- Schramade, W. Bridging sustainability and finance: The value driver adjustment approach. J. Appl. Corp. Financ. 2016, 28, 17–28. [Google Scholar]

- Eccles, R.G.; Serafeim, G.; Krzus, M.P. Market interest in nonfinancial information. J. Appl. Corp. Financ. 2011, 23, 113–127. [Google Scholar] [CrossRef]

- Lydenberg, S. Integrating systemic risk into modern portfolio theory and practice. J. Appl. Corp. Financ. 2016, 28, 56–61. [Google Scholar]

- Indahl, R.; Jacobsen, H.G. Private Equity 4.0: Using ESG to Create More Value with Less Risk. J. Appl. Corp. Financ. 2019, 31, 34–41. [Google Scholar] [CrossRef]

- Crifo, P.; Forget, V.D.; Teyssier, S. The price of environmental, social and governance practice disclosure: An experiment with professional private equity investors. J. Corp. Financ. 2015, 30, 168–194. [Google Scholar] [CrossRef]

- Halbritter, G.; Dorfleitner, G. The wages of social responsibility—Where are they? A critical review of ESG investing. Rev. Financ. Econ. 2015, 26, 25–35. [Google Scholar] [CrossRef]

- Goodland, R. The concept of environmental sustainability. Annu. Rev. Ecol. Syst. 1995, 26, 1–24. [Google Scholar] [CrossRef]

- Littig, B.; Griessler, E. Social sustainability: A catchword between political pragmatism and social theory. Int. J. Sustain. Dev. 2005, 8, 65–79. [Google Scholar] [CrossRef]

- Soppe, A. Sustainable corporate finance. J. Bus. Ethics 2004, 53, 213–224. [Google Scholar] [CrossRef]

- Eccles, R.G.; Kastrapeli, M.D.; Potter, S.J. How to Integrate ESG into Investment Decision-Making: Results of a Global Survey of Institutional Investors. J. Appl. Corp. Financ. 2017, 29, 125–133. [Google Scholar] [CrossRef]

- Odell, J.; Ali, U. ESG investing in emerging and frontier markets. J. Appl. Corp. Financ. 2016, 28, 96–101. [Google Scholar]

- Kirkland, R. Bring the problem forward: Larry Fink on climate risk. In The McKinsey Quarterly; Copyright McKinsey & Company, Inc.: New York, NY, USA, 2020. [Google Scholar]

- Urban, M.A.; Wójcik, D. Dirty banking: Probing the gap in sustainable finance. Sustainability 2019, 11, 1745. [Google Scholar] [CrossRef]

- GSIA. Global Sustainable Investment Review. 2016. Available online: http://www.gsi-alliance.org/wp-content/uploads/2017/03/GSIR_Review2016.F.pdf (accessed on 14 July 2020).

- Metrick, A.; Yasuda, A. The economics of private equity funds. Rev. Financ. Stud. 2010, 23, 2303–2341. [Google Scholar] [CrossRef]

- Phalippou, L.; Gottschalg, O. The performance of private equity funds. Rev. Financ. Stud. 2009, 22, 1747–1776. [Google Scholar] [CrossRef]

- Froud, J.; Williams, K. Private equity and the culture of value extraction. New Political Econ. 2007, 12, 405–420. [Google Scholar] [CrossRef]

- Schell, J.M. Private Equity Funds: Business Structure and Operations; Law Journal Press: New York, NY, USA, 2020. [Google Scholar]

- Crifo, P.; Forget, V.D. Think global, invest responsible: Why the private equity industry goes green. J. Bus. Ethics 2013, 116, 21–48. [Google Scholar] [CrossRef]

- Cappucci, M. The ESG integration paradox. J. Appl. Corp. Financ. 2018, 30, 22–28. [Google Scholar] [CrossRef]

- Majoch, A.A.; Hoepner, A.G.; Hebb, T. Sources of stakeholder salience in the responsible investment movement: Why do investors sign the principles for responsible investment? J. Bus. Ethics 2017, 140, 723–741. [Google Scholar] [CrossRef]

- Paetzold, F.; Busch, T. Unleashing the powerful few: Sustainable investing behaviour of wealthy private investors. Organ. Environ. 2014, 27, 347–367. [Google Scholar] [CrossRef]

- Bettinazzi, E.L.; Zollo, M. Stakeholder orientation and acquisition performance. Strateg. Manag. J. 2017, 38, 2465–2485. [Google Scholar] [CrossRef]

- Alsayegh, M.F.; Abdul Rahman, R.; Homayoun, S. Corporate economic, environmental, and social sustainability performance transformation through ESG disclosure. Sustainability 2020, 12, 3910. [Google Scholar] [CrossRef]

- Tarmuji, I.; Maelah, R.; Tarmuji, N.H. The impact of environment, social and governance (ESG) on economic performance: Evidence from ESG scores. Int. J. Trade Econ. Financ. 2016, 7, 67–74. [Google Scholar] [CrossRef]

- Ong, T.S.; Teh, B.H.; Ang, Y.W. The impact of environmental improvements on the financial performance of leading companies listed in Bursa Malaysia. Int. J. Trade Econ. Financ. 2014, 5, 386–391. [Google Scholar] [CrossRef]

- Brown, H.S.; De Jong, M.; Lessidrenska, T. The rise of the Global Reporting Initiative: A case of institutional entrepreneurship. Environ. Politics 2009, 18, 182–200. [Google Scholar] [CrossRef]

- Friede, G.; Busch, T.; Bassen, A. ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. J. Sustain. Financ. Investig. 2015, 5, 210–233. [Google Scholar] [CrossRef]

- Landi, G.; Sciarelli, M. Towards a more ethical market: The impact of ESG rating on corporate financial performance. Soc. Responsib. J. 2019, 15, 11–27. [Google Scholar] [CrossRef]

- Velte, P. Does ESG performance have an impact on financial performance? Evidence from Germany. J. Glob. Responsib. 2017, 8, 169–178. [Google Scholar] [CrossRef]

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zaccone, M.C.; Pedrini, M. ESG Factor Integration into Private Equity. Sustainability 2020, 12, 5725. https://doi.org/10.3390/su12145725

Zaccone MC, Pedrini M. ESG Factor Integration into Private Equity. Sustainability. 2020; 12(14):5725. https://doi.org/10.3390/su12145725

Chicago/Turabian StyleZaccone, Maria Cristina, and Matteo Pedrini. 2020. "ESG Factor Integration into Private Equity" Sustainability 12, no. 14: 5725. https://doi.org/10.3390/su12145725

APA StyleZaccone, M. C., & Pedrini, M. (2020). ESG Factor Integration into Private Equity. Sustainability, 12(14), 5725. https://doi.org/10.3390/su12145725