Activity Based Costing for Wastewater Treatment and Reuse under Uncertainty: A Fuzzy Approach

Abstract

1. Introduction

- Reduce to the minimum possible, if not eliminate, the production of polluting waste.

- Maximize productivity with increasing sustainability, and

- Implement and maintain effective environmental management systems at the lowest possible cost.

- Costs of environmental control

- Environmental Costs of Prevention

- Environmental Assessment Costs

- Costs of environmental control failures

- Mitigation costs of internal faults

- Costs Mitigation of external faults

- Costs of environmental control

- Investments in anti-pollution technologies;

- Specific materials intended for environmental protection, preservation and recovery;

- Hours of labour consumed in effluent treatment stations.

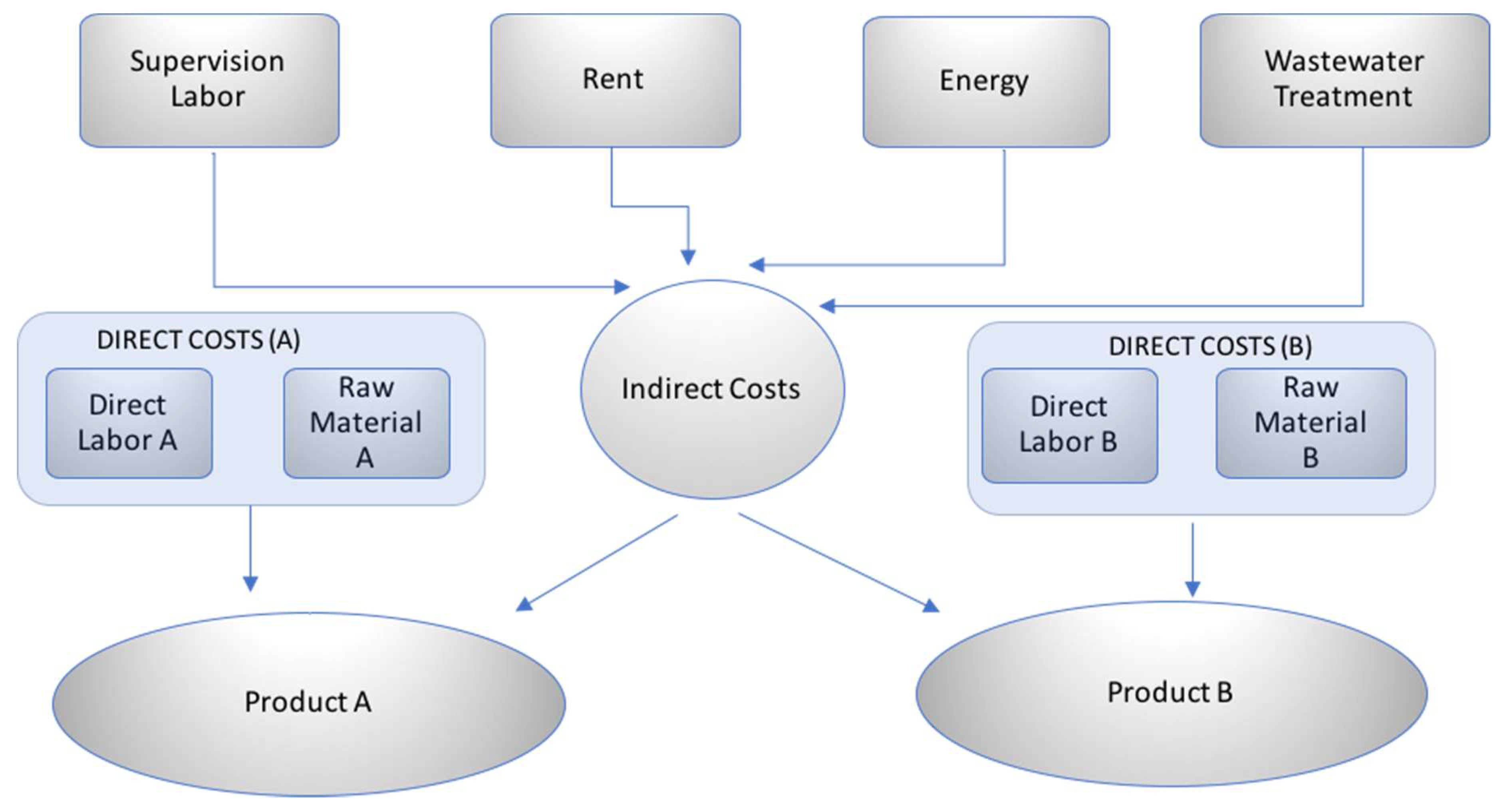

2. Activity-Based Costing (ABC)

- (1)

- They are allocated based on some simple criteria of allocation to the products.

- (2)

- They are accumulated in a costs pool, which means they are not allocated to any specific product, and they are treated as fixed costs or overhead.

- Direct Costs (Capital Investments, Recurring and non-recurring costs)

- Indirect Costs (operating and maintenance, recurring and non-recurring)

- Contingent (future scenarios)

- Intangible (Customer loyalty, working morale and performance)

- External Costs (Societal costs)

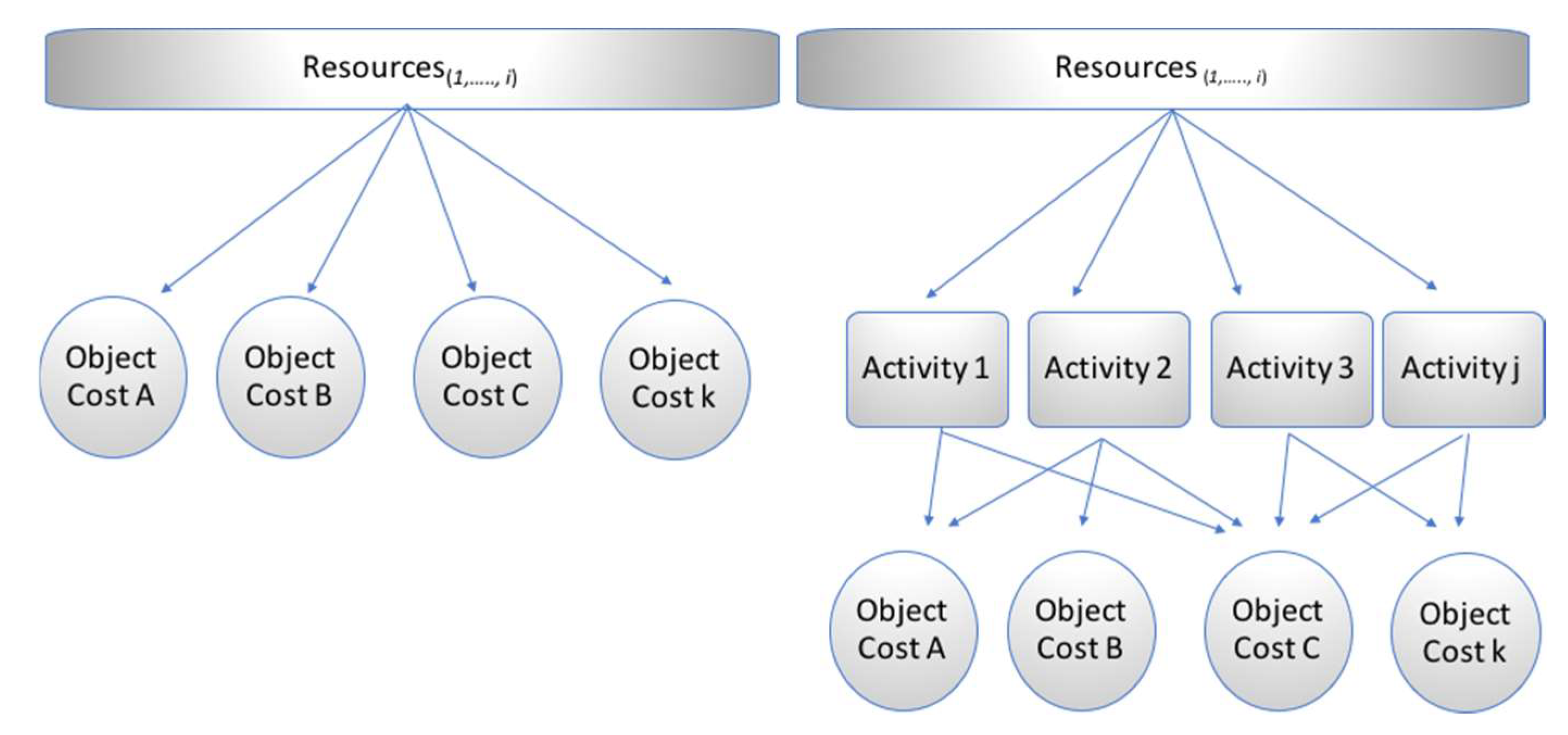

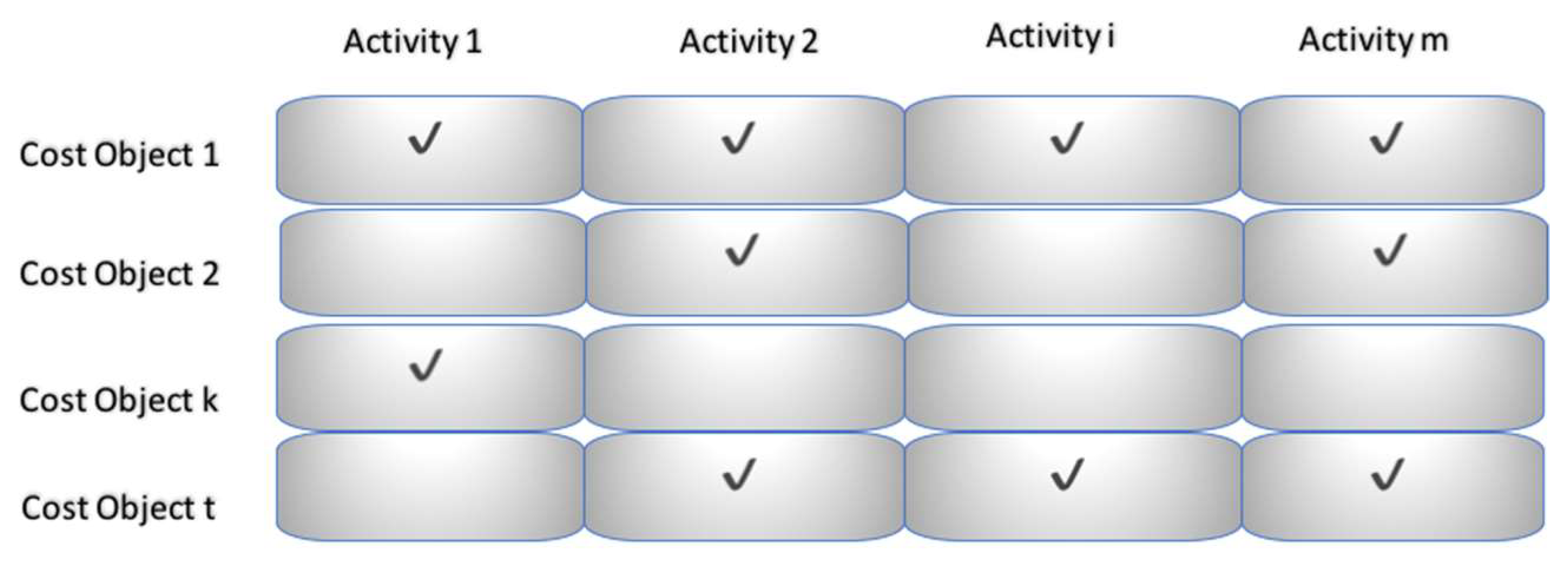

- Identification of activities (activity mapping)

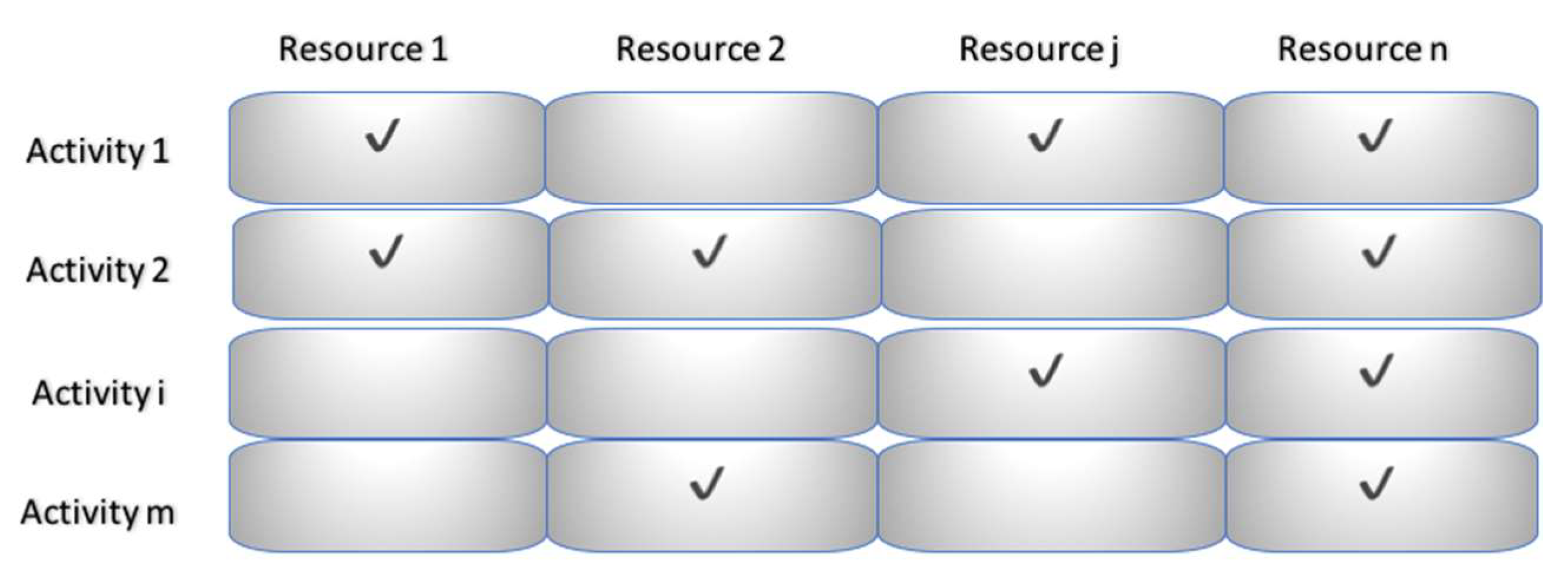

- Listing the resources consumed by each one of the activities.

- List the resources (and their costs) which are consumed by the activities listed in the previous step.

- Determination of the first and second level cost drivers.

- Determination of the activities’ costs.

- Determination of the cost of the costs objects.

3. Proposed Model

4. Case Study

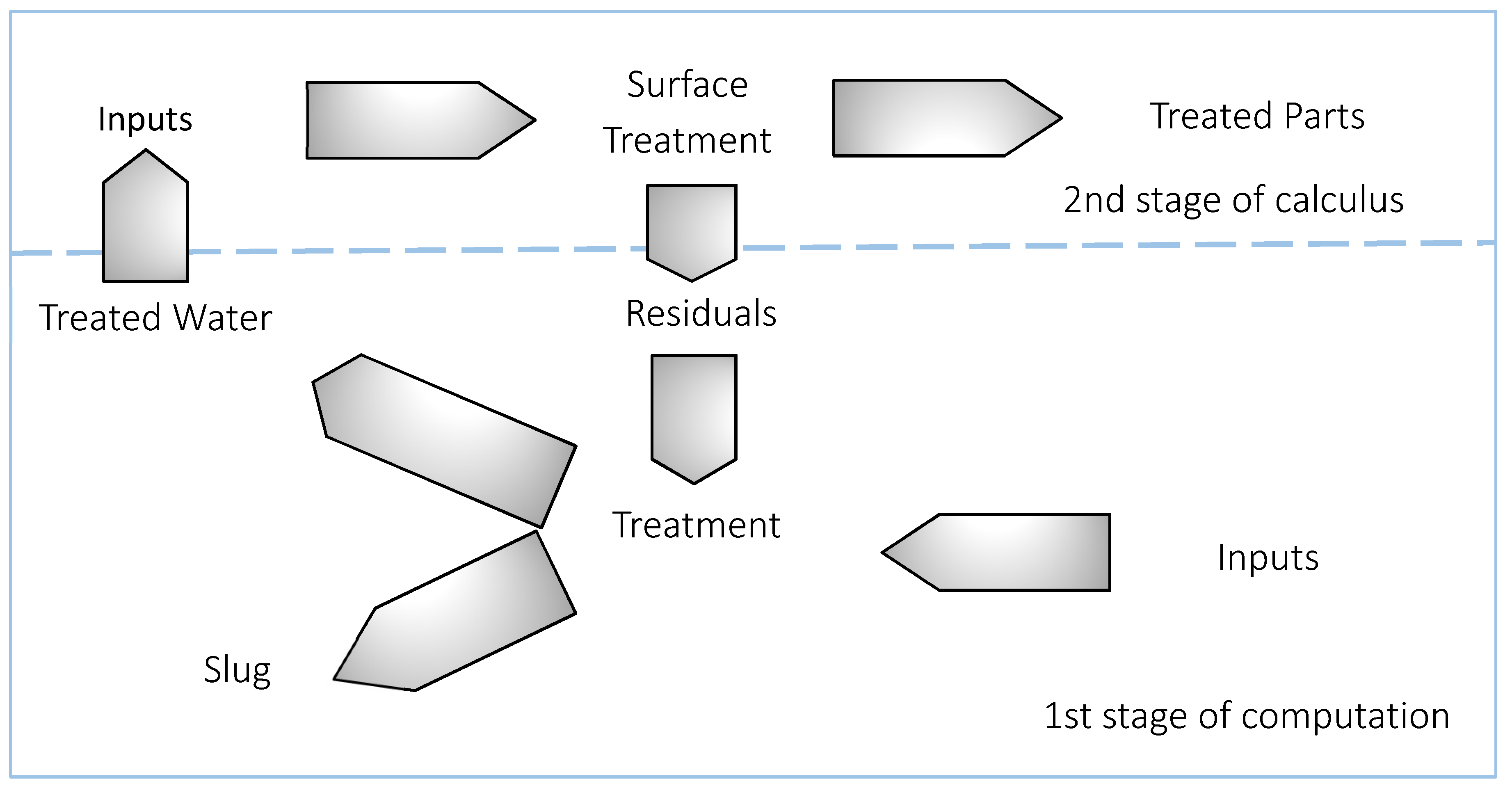

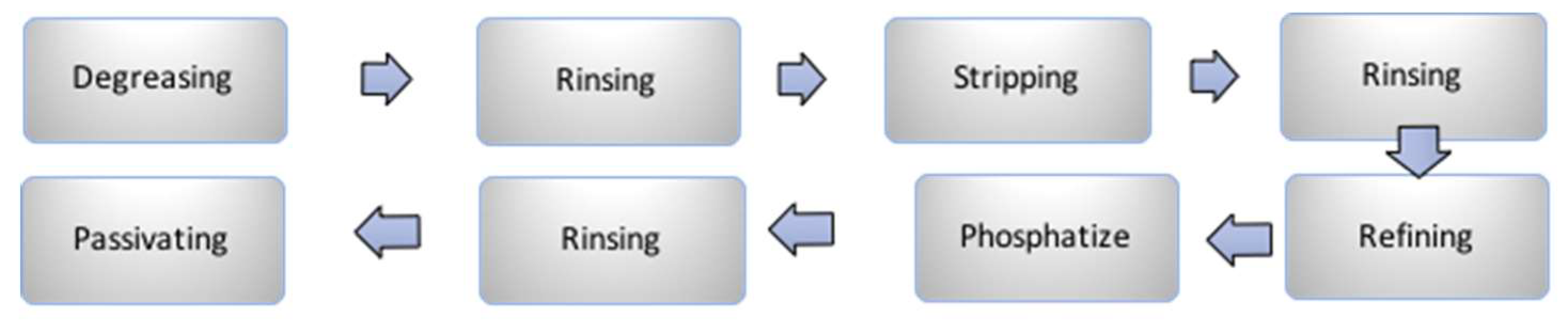

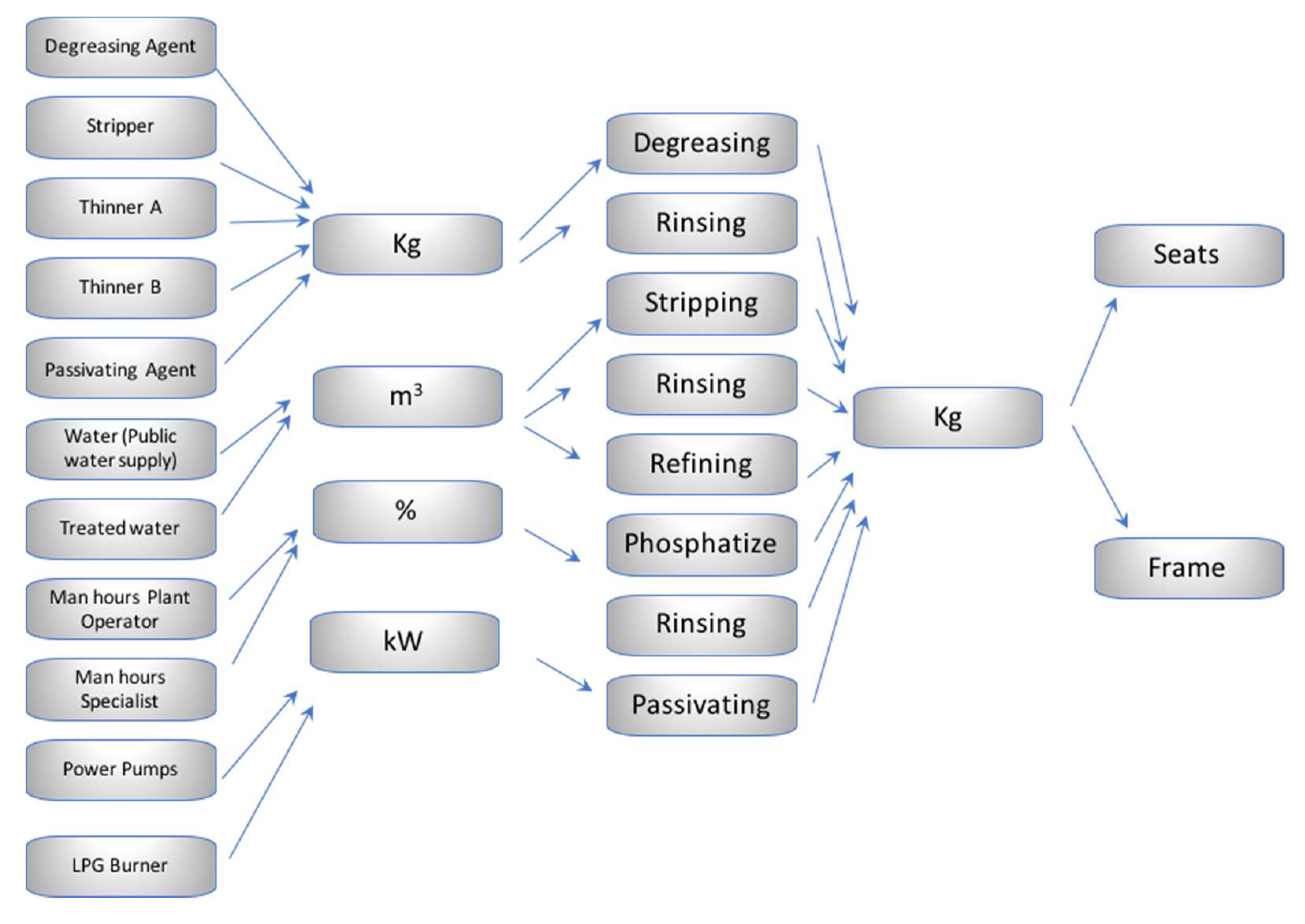

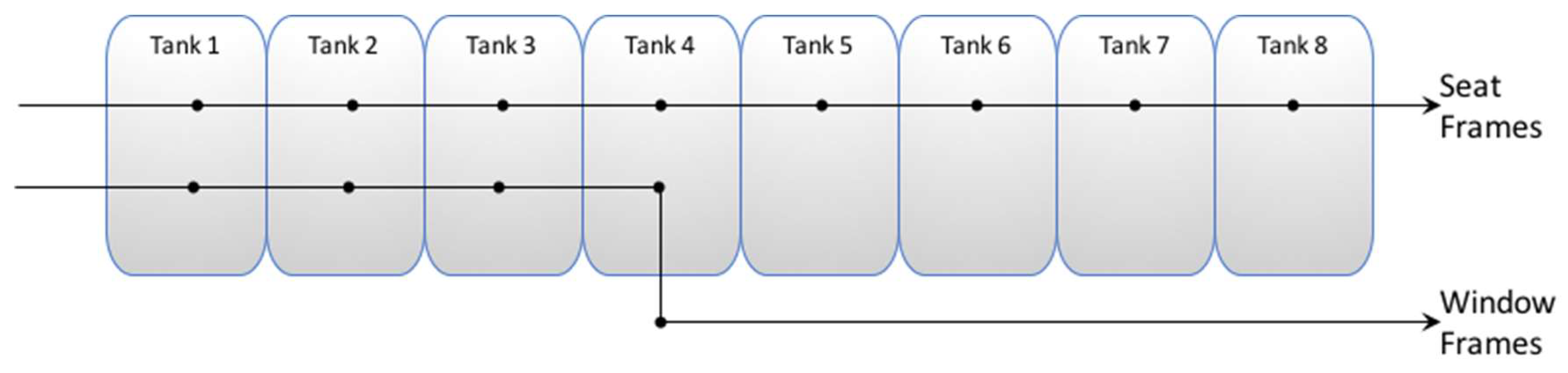

4.1. The Wastewater Recuperation Process

- Liquid Aluminum Sulfate

- Liquid Caustic Soda

- Anionic Polymer

- Hydrated lime.

4.2. Costs Computation

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Burritt, R.; Schaltegger, S. Accounting towards sustainability in production and supply chains. Br. Account. Rev. 2014, 46, 327–343. [Google Scholar] [CrossRef]

- Noodezh, H.R.; Moghimi, S. Environmental costs and environmental information disclosure in the accounting systems. Int. J. Acad. Res. Account. Finance Manag. Sci. 2015, 5, 13–18. [Google Scholar] [CrossRef]

- Jabbour, C.J.C.; de Sousa Jabbour, A.B.L.; Govindan, K.; Teixeira, A.A.; de Souza Freitas, W.R. Environmental management and operational performance in automotive companies in Brazil: The role of human resource management and lean manufacturing. J. Clean. Product. 2013, 47, 129–140. [Google Scholar] [CrossRef]

- Yang, M.G.M.; Hong, P.; Modi, S.B. Impact of lean manufacturing and environmental management on business performance: An empirical study of manufacturing firms. Int. J. Product. Econ. 2011, 129, 251–261. [Google Scholar] [CrossRef]

- Okafor, G.O.; Okaro, S.C.; Egbunike, F.C. Environmental cost accounting and cost allocation (A study of selected manufacturing companies in Nigeria). Eur. J. Bus. Manag. 2013, 5, 68–75. [Google Scholar]

- Kim, J.; Jeong, S. Economic and Environmental Cost Analysis of Incineration and Recovery Alternatives for Flammable Industrial Waste: The Case of South Korea. Sustainability 2017, 9, 1638. [Google Scholar]

- Cagno, E.; Micheli, G.J.; Trucco, P. Eco-efficiency for sustainable manufacturing: An extended environmental costing method. Product. Plan. Control 2012, 23, 134–144. [Google Scholar] [CrossRef]

- Nicolăescu, E.; Alpopi, C.; Zaharia, C. Measuring corporate sustainability performance. Sustainability 2015, 7, 851–865. [Google Scholar] [CrossRef]

- Senthil, K.D.; Ong, S.K.; Nee, A.Y.C.; Tan, R.B. A proposed tool to integrate environmental and economical assessments of products. Environ. Impact Assess. Rev. 2003, 23, 51–72. [Google Scholar] [CrossRef]

- Campos, L.M.D.S.; Trierweiller, A.C.; Carvalho, D.N.D.; Santos, T.H.S.D.; Peixe, B.C.S.; Bornia, A.C. Selection process theoretical framework on environmental costs: An exploratory vision. Latin Am. J. Manag. Sust. Dev. 2015, 2, 47–63. [Google Scholar] [CrossRef]

- Molinos-Senante, M.; Mocholí-Arce, M.; Sala-Garrido, R. Estimating the environmental and resource costs of leakage in water distribution systems: A shadow price approach. Sci. Total Environ. 2016, 568, 180–188. [Google Scholar] [CrossRef] [PubMed]

- Henri, J.F.; Boiral, O.; Roy, M.J. Strategic cost management and performance: The case of environmental costs. Br. Account. Rev. 2016, 48, 269–282. [Google Scholar] [CrossRef]

- Szadziewska, A. Corporate environmental costs–classification and disclosures in external reports. Zesz. Teoretyczne Rachunkowości 2012, 65, 45–70. [Google Scholar]

- Ruiz-Rosa, I.; García-Rodríguez, F.J.; Mendoza-Jiménez, J. Development and application of a cost management model for wastewater treatment and reuse processes. J. Clean. Product. 2016, 113, 299–310. [Google Scholar] [CrossRef]

- Sgroi, M.; Vagliasindi, F.G.; Roccaro, P. Feasibility, sustainability and circular economy concepts in water reuse. Curr. Opin. Environ. Sci. Health 2018, 2, 20–25. [Google Scholar] [CrossRef]

- Insel, G.; Gumuslu, E.; Cokgor, E.U.; Olmez-Hanci, T.; Tas, D.O.; Babuna, F.G.; Dizge, N. The Effect of Wastewater Reuse on Product Quality for an Oven Manufacturing Plant. In Proceedings of the Sixth International Conference on Environmental Management, Engineering, Planning & Economics, Thessaloniki, Greece, 25–30 June 2017. [Google Scholar]

- Insel, G.; Gumuslu, E.; Yuksek, G.; Ucar, S.N.; Cokor, U.E.; Hanci, O.T.; Erturan, O. Evaluation of water reuse in a metal finishing industry. In Proceedings of the 18th International Symposium on Environmental Pollution and its Impact on Life in the Mediterranean Region, Crete, Greece, 26–30 September 2015; pp. 27–30. [Google Scholar]

- Sato, T.; Qadir, M.; Yamamoto, S.; Endo, T.; Zahoor, A. Global, regional, and country level need for data on wastewater generation, treatment, and use. Agric. Water Manag. 2013, 130, 1–13. [Google Scholar] [CrossRef]

- Water, U.N. Managing Water under Uncertainty and Risk, the United Nations World Water Development Report 4; UN Water Reports; World Water Assessment Programme: Paris, France, 2012. [Google Scholar]

- The United Nations World Water Development Report, WWDR. Water for a Sustainable World 2015; UNESCO: Paris, France; Available online: http://unesdoc.unesco.org/images/0023/002318/231823E.pdf (accessed on 21 May 2018).

- Hetzer, K. Cash Flows Where Water Does. UNEP FI 2007, 7, 4–6. [Google Scholar]

- Vergine, P.; Salerno, C.; Libutti, A.; Beneduce, L.; Gatta, G.; Berardi, G.; Pollice, A. Closing the water cycle in the agro-industrial sector by reusing treated wastewater for irrigation. J. Clean. Product. 2017, 164, 587–596. [Google Scholar] [CrossRef]

- Costantino, F.; Di Gravio, G.; Tronci, M. Integrating environmental assessment of failure modes in maintenance planning of production systems. Appl. Mech. Mater. 2013, 295, 651–660. [Google Scholar] [CrossRef]

- Güven, D.; Hanhan, O.; Aksoy, E.C.; Insel, G.; Çokgör, E. Impact of paint shop decanter effluents on biological treatability of automotive industry wastewater. J. Hazard. Mater. 2017, 330, 61–67. [Google Scholar] [CrossRef] [PubMed]

- Piao, W.; Kim, Y.; Kim, H.; Kim, M.; Kim, C. Life cycle assessment and economic efficiency analysis of integrated management of wastewater treatment plants. J. Clean. Product. 2016, 113, 325–337. [Google Scholar] [CrossRef]

- Faraji, T.; Maghari, A.; Mirsepasi, N. A framework for assessing cost management system changes: The case of activity-based costing implementation at food industry. Manag. Sci. Lett. 2015, 5, 413–418. [Google Scholar] [CrossRef]

- Tsai, W.H.; Lin, T.W.; Chou, W.C. Integrating activity-based costing and environmental cost accounting systems: A case study. Int. J. Bus. Syst. Res. 2010, 4, 186–208. [Google Scholar] [CrossRef]

- Abdulbaki, D.; Al-Hindi, M.; Yassine, A.; Najm, M.A. An optimization model for the allocation of water resources. J. Clean. Product. 2017, 164, 994–1006. [Google Scholar] [CrossRef]

- Yuksek, G.; Okutman Tas, D.; Ubay Cokgor, E.; Insel, G.; Kirci, B.; Erturan, O. Effect of eco-friendly production technologies on wastewater characterization and treatment plant performance. Desalinat. Water Treat. 2016, 57, 27924–27933. [Google Scholar] [CrossRef]

- Kreuze, J.G.; Newell, G.E. ABC and life-cycle costing for environmental expenditures. Strat. Financ. 1994, 75, 38. [Google Scholar]

- Lockhart, J.; Taylor, A. Environmental considerations in product mix decisions using ABC and TOC. Manag. Account. Quart. 2007, 9, 13. [Google Scholar]

- Rodríguez Rivero, E.J.; Emblemsvåg, J. Activity-based life-cycle costing in long-range planning. Rev. Account. Financ. 2007, 6, 370–390. [Google Scholar] [CrossRef]

- Sun, Y.; Carmichael, D.G. Uncertainties related to financial variables within infrastructure life cycle costing: A literature review. Struct. Infrastruct. Eng. 2017. [Google Scholar] [CrossRef]

- Farr, J.V.; Faber, I.J.; Ganguly, A.; Martin, W.A.; Larson, S.L. Simulation-based costing for early phase life cycle cost analysis: Example application to an environmental remediation project. Eng. Econ. 2016, 61, 207–222. [Google Scholar] [CrossRef]

- Woodward, D.G. Life cycle costing—Theory, information acquisition and application. Int. J. Proj. Manag. 1997, 15, 335–344. [Google Scholar] [CrossRef]

- Zadeh, L.A. Information and control. Fuzzy Sets 1965, 8, 338–353. [Google Scholar]

- Nachtmann, H.; Needy, K.L. Methods for handling uncertainty in activity-based costing systems. Eng. Econ. 2003, 48, 259–282. [Google Scholar] [CrossRef]

- Yang, C.H.; Lee, K.C.; Chen, H.C. Incorporating carbon footprint with activity-based costing constraints into sustainable public transport infrastructure project decisions. J. Clean. Prod. 2016, 133, 1154–1166. [Google Scholar] [CrossRef]

- Goh, Y.M.; Newnes, L.B.; Mileham, A.R.; McMahon, C.A.; Saravi, M.E. Uncertainty in Through-Life Costing—Review and Perspectives. IEEE Trans. Eng. Manag. 2010, 57, 689–701. [Google Scholar] [CrossRef]

- Afonso, P.S.; Paisana, A.M. An Algorithm for Activity-Based Costing Based on Matrix Multiplication. In Proceedings of the 2009 IEEE International Conference on Industrial Engineering and Engineering Management, Hong Kong, China, 8–11 December 2009. [Google Scholar]

- Byrne, P. Fuzzy DCF: A Contradiction in Terms, or a Way to Better Investment Appraisal. 1997. Available online: http://citeseerx.ist.psu.edu/viewdoc/summary?doi=10.1.1.98.6802 (accessed on 4 June 2018).

- Díaz-Madroñero, M.; Satorre, J.R.; Mula, J.; López-Jiménez, P.A. Analysis of a wastewater treatment plant using fuzzy goal programming as a management tool: A case study. J. Clean. Prod. 2018, 180, 20–33. [Google Scholar] [CrossRef]

- Gregory, J.R.; Montalbo, T.M.; Kirchain, R.E. Analyzing uncertainty in a comparative life cycle assessment of hand drying systems. Int. J. Life Cycle Assess. 2013, 18, 1605–1617. [Google Scholar] [CrossRef]

- Kishk, M. Combining various facets of uncertainty in whole-life cost modelling. Const. Manag. Econ. 2004, 22, 429–435. [Google Scholar] [CrossRef]

- Kishk, M.; Al-Hajj, A. A fuzzy model and algorithm to handle subjectivity in life-cycle costing-based decision-making. J. Financ. Manag. Prop. Constr. 2002, 5, 93–104. [Google Scholar]

- Chiu, C.Y.; Park, C.S. Fuzzy cash flow analysis using present worth criterion. Eng. Econ. 1994, 39, 113–138. [Google Scholar] [CrossRef]

- Chang, D.Y. Applications of the extent analysis method on fuzzy AHP. Eur. J. Operat. Res. 1996, 95, 649–655. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Materials | Total Expenses ($) | Driver | Qtty | Unitary Cost ($) |

|---|---|---|---|---|

| Liquid Caustic Soda | $621.76 | kg | 460.56 | $1.35 |

| Liquid Aluminum Sulfate | $1534.50 | kg | 1395.00 | $1.10 |

| Hydrated lime | $56.50 | kg | 113.00 | $0.50 |

| Anionic Polymer | $958.32 | kg | 726.00 | $1.32 |

| ENERGY Pump 1 | $116.00 | kW | 232.00 | $0.50 |

| ENERGY Pump 2 | $3.08 | kW | 6.15 | $0.50 |

| ENERGY Pump 3 | $40.00 | kW | 80.00 | $0.50 |

| ENERGY Pump 4 | $60.00 | kW | 120.00 | $0.50 |

| ENERGY Extractor | $116.00 | kW | 232.00 | $0.50 |

| ENERGY Extractor | $176.00 | kW | 352.00 | $0.50 |

| Operator | $500.00 | $500.00 | ||

| Specialist | $400.00 | $2000.00 | $400.00 | |

| Slugde | $625.00 | kg/d × 20 d | 12,500 | 0.05 |

| TOTAL Expenses Wastewater treatment plant ($) | $5207.15 |

| Product | Unit | Quantity | Unitary Cost | |

|---|---|---|---|---|

| Treated Water | M3/day × 20 days | 800 m3 | $6.51/ m3 | |

| Sludge | kg/day × 20 days | 12,500 kg | $0.05/kg | $625.00 |

| Resources | Driver |

|---|---|

| Degreasing Agent | kg |

| Stripper | kg |

| Thinner A | kg |

| Thinner B | kg |

| Passivating Agent | kg |

| Water (Public water supply) | M3 |

| Recycled water | M3 |

| Manhours (Plant Operator) | $ |

| Manhours (Specialist) | $ |

| Power Pump 1 | kW |

| Power Pump 2 | kW |

| LPG Burner 1 | M3/d |

| LPG Burner 2 | M3/d |

| Unitary Costs (Triangular) $/u | Unitary Cost (Crisp) $/u | |

|---|---|---|

| Seat Frames | (0.08, 0.10, 0.11) | $0.10 |

| Window Frames | (0.02, 0.02, 0.02) | $0.02 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Durán, O.; Durán, P.A. Activity Based Costing for Wastewater Treatment and Reuse under Uncertainty: A Fuzzy Approach. Sustainability 2018, 10, 2260. https://doi.org/10.3390/su10072260

Durán O, Durán PA. Activity Based Costing for Wastewater Treatment and Reuse under Uncertainty: A Fuzzy Approach. Sustainability. 2018; 10(7):2260. https://doi.org/10.3390/su10072260

Chicago/Turabian StyleDurán, Orlando, and Paulo Andrés Durán. 2018. "Activity Based Costing for Wastewater Treatment and Reuse under Uncertainty: A Fuzzy Approach" Sustainability 10, no. 7: 2260. https://doi.org/10.3390/su10072260

APA StyleDurán, O., & Durán, P. A. (2018). Activity Based Costing for Wastewater Treatment and Reuse under Uncertainty: A Fuzzy Approach. Sustainability, 10(7), 2260. https://doi.org/10.3390/su10072260