Abstract

The European automotive industry, particularly in Germany, faces a significant crisis, heavily impacting suppliers reliant on OEMs. To enhance resilience, participation in the platform economy has been proposed as a solution. This study employs a qualitative research approach by conducting 18 expert interviews with automotive companies in the Northern Black Forest region to assess their awareness, perceived potential, and support needs regarding platform-based business models. The findings reveal diverse perspectives: smaller firms perceive higher risks, while larger companies recognize potential but struggle with limited expertise. The results highlight the novelty of the platform economy within the supplier industry and the need for increased awareness, strategic guidance, and tailored support measures. This study provides original insights into regional supplier engagement with platform ecosystems, contributing to the limited research on this topic and offering a foundation for future industry adaptation strategies.

1. Introduction

The platform economy has transformed industries by serving as an intermediary, efficiently connecting supply and demand [1]. Companies such as Airbnb, Uber, and eBay have established marketplaces that facilitate transactions between users without owning the underlying assets. Similarly, Amazon, Meta, and Google dominate their respective sectors through a “winner-takes-all” model, leveraging network effects and vast data resources to scale and innovate [2,3]. Despite the availability of alternative platforms, these companies remain market leaders, shaping industries and influencing consumer behavior. The platform economy fosters innovation by lowering entry barriers and enabling participants to monetize assets while exploring new business models. However, the dominance of major platforms can hinder competition and limit opportunities for smaller players. This dual role—as both drivers of innovation and market consolidators—emphasizes the need for regulatory frameworks that ensure fairness and long-term sustainability [4].

The platform economy is entering the automotive sector [5], driven by companies like Foxtron, a subsidiary of Foxconn [6]. As the industry transitions from internal combustion engines (ICEs) to electric mobility, Foxtron’s open automotive architecture seeks to integrate suppliers by providing standardized components, enabling automakers to reduce costs [7]. While this model promotes innovation and collaboration, it also presents significant challenges for traditional suppliers, particularly those embedded in established OEM-driven ICE value chains [8].

Further electrification introduces fluctuating production volumes, rising costs, and economic uncertainties while intensifying competition, accelerating product commoditization, reducing differentiation opportunities, and exerting significant price and margin pressures on suppliers [9,10]. Shifting customer preferences toward electrification, autonomous driving, and connectivity further challenge traditional suppliers, who now compete with software and tech companies [11,12].

These topics are prominent in discourse; however, the platform economy, exemplified by the Taiwanese manufacturer Foxtron, represents an emerging phenomenon within the automotive sector [13]. Despite the growing relevance of platform-based business models across various industries, their adoption and impact on the automotive supply chain, particularly among regional suppliers, remain underexplored. The Northern Black Forest region, home to numerous small and medium-sized enterprises (SMEs) and automotive suppliers, faces profound structural challenges due to digitalization, electrification, and changing industry dynamics. While large OEMs and multinational corporations are increasingly integrating platform-based strategies, little is known about the awareness, preparedness, and strategic positioning of automotive suppliers in regional ecosystems. Existing research primarily focuses on OEM-driven transformations, such as platform-based vehicle architectures, but lacks supplier-level insights into the barriers, risks, and opportunities associated with participation in the platform economy. It remains unclear to what extent suppliers recognize and comprehend the platform economy and its potential implications for their business models and value chains. Although companies like Foxtron are pioneering platform-based automotive models, regional suppliers have little visibility on whether such structures offer growth opportunities or intensify competitive pressures. Additionally, research has not systematically examined how SMEs versus large suppliers engage with platform-based business models, nor does it provide a comprehensive dataset that reflects their attitudes, strategic initiatives, or barriers to adoption. Moreover, the specific support measures required to help these suppliers assess and respond to platform economy challenges—whether financial, technological, regulatory, or training-related—remain insufficiently explored. Addressing these gaps, this study conducts 18 expert interviews with automotive suppliers in the Northern Black Forest to assess their level of awareness, strategic responses, and perceived support needs. It identifies whether suppliers view platform economy models as an opportunity or a risk and examines the factors influencing their ability to participate. Furthermore, this study provides practical insights into the types of support measures that could enable a smoother transition into platform-based business models, ensuring that regional suppliers remain competitive within evolving value chain structures. Against this backdrop, this study explores two key research questions (RQs):

- RQ 1: To what extent is the concept of the platform economy recognized and understood by regional suppliers?

- RQ 2: Which support measures do automotive companies in the Northern Black Forest require to evaluate opportunities and risks of the platform economy along the value chain?

This paper examines the concept of the platform economy and its impact on the automotive supply chain in the Northern Black Forest. Section 2 provides the theoretical foundations of the platform economy, analyzes the current state of the region, and identifies key challenges faced by automotive suppliers. Section 3 outlines the research methodology, detailing the interview design, data collection, and analytical approach. Section 4 presents the study’s findings, focusing on supplier awareness, perceptions of opportunities and risks, and the necessary steps for adaptation. Section 5 critically discusses and contextualizes the results within the broader automotive industry. Finally, Section 6 summarizes the key insights and offers strategic recommendations for facilitating the transition to platform-based business models in the automotive sector.

2. Background

2.1. Platform Economy

The term platform economy refers to an overarching economic principle that encompasses a wide range of business models in which value creation is either entirely or predominantly driven by digital platforms. These platforms serve as virtual spaces, utilizing the capabilities of the internet to facilitate efficient and economically advantageous interactions between multiple independent groups, such as producers, consumers, service providers, and developers. Digital platforms act as intermediaries, creating structured environments where participants can exchange goods, services, information, or other resources. They rely on advanced technologies to streamline transactions, foster collaboration, and support the development of innovative business ecosystems. This dynamic approach allows for the aggregation of diverse actors while simultaneously enabling scalability, flexibility, and the reduction in transaction costs [14,15,16].

Platforms are defined by their ability to connect diverse groups of actors through internet- and data-based systems, enabling seamless interactions. Their success relies on a two- or multi-sided structure, where multiple user groups are served simultaneously, allowing the platform to act as an intermediary for economic exchanges. To achieve this, platforms must first reach a critical mass of users. Without this “critical mass”, the frequency of interactions decreases, leading to a decline in user trust and, ultimately, the platform’s viability [15,17,18].

A central economic feature of platforms is their reliance on network effects. Direct network effects occur when the platform’s value increases as more users from the same group join, such as in social networks. Indirect network effects arise when the presence of a larger user base on one side (e.g., sellers) enhances the value for the other side (e.g., buyers), and vice versa. For instance, consumers benefit from a broader selection of goods and more transparent pricing, while providers gain access to a larger audience and increased revenue potential [15,19,20].

Another significant advantage of platforms lies in their ability to minimize transaction costs through optimized (digital) processes. This efficiency, combined with their inherent scalability, allows platforms to achieve substantial economies of scale, especially as network effects drive exponential growth [15,21].

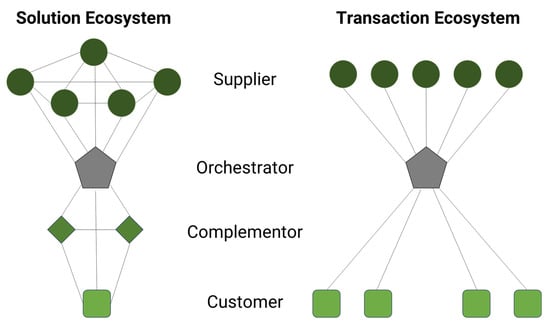

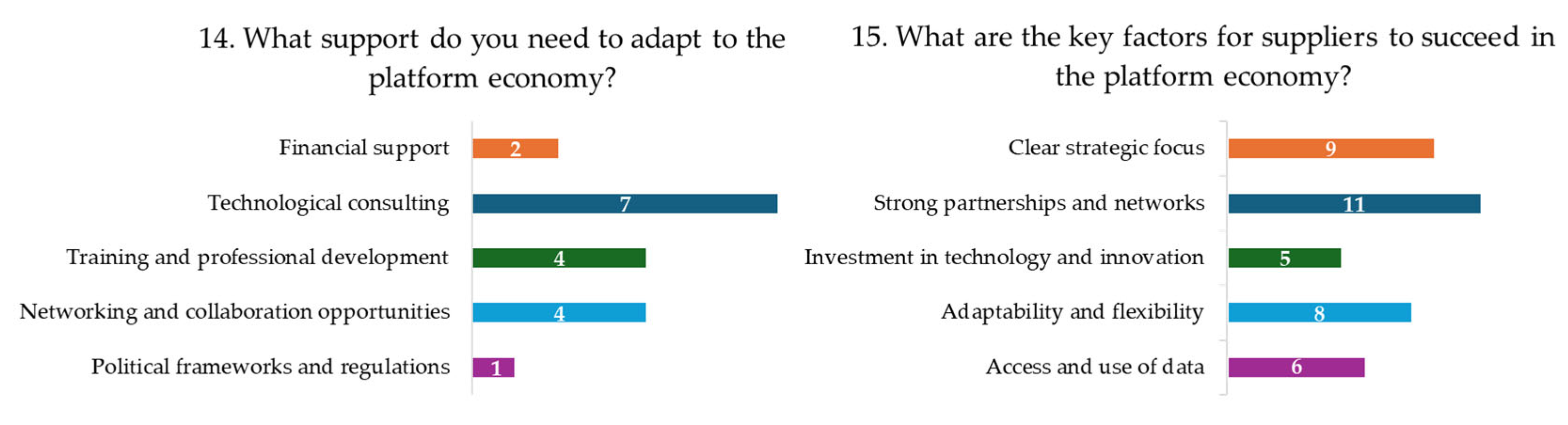

Business ecosystems can be broadly categorized into two types: solution ecosystems and transactional ecosystems. Each type serves distinct purposes and operates under different dynamics, which are depicted in Figure 1:

Solution Ecosystem

These ecosystems focus on coordinating various contributors to collaboratively create and deliver products or services. A central, or core, firm plays a pivotal role in orchestrating the activities of complementary parties and their offerings. During the solution development process, suppliers are integral members of the ecosystem, working alongside other contributors to develop the final product. Once the product is complete, suppliers transition to roles within a traditional hierarchical supply chain. While customers significantly influence the selection and combination of solution options provided by the ecosystem’s complementors, they are typically not considered members of the ecosystem itself. This dynamic emphasizes the collaborative nature of solution ecosystems, with the goal of producing integrated offerings through a network of interdependent participants [13,22].

Transactional Ecosystem

These ecosystems are commonly found in two-sided markets, where their primary objective is to connect producers and consumers through a centralized platform. This platform serves as the intermediary, enabling seamless interactions and exchanges between the two groups. Transactional ecosystems leverage both direct and indirect network effects to enhance their value proposition. Direct network effects occur as the number of users on one side of the platform increases, enhancing the experience for that side (e.g., more producers lead to greater choice for consumers). Indirect network effects emerge when the growth of one side benefits the other (e.g., a larger consumer base attracts more producers, and vice versa). This interconnected structure drives the success of the ecosystem by fostering mutual benefits for all participants [13,22].

Figure 1.

Solution vs. Transaction Ecosystem Types–own adaptation based on Pidun et al. [22].

Figure 1.

Solution vs. Transaction Ecosystem Types–own adaptation based on Pidun et al. [22].

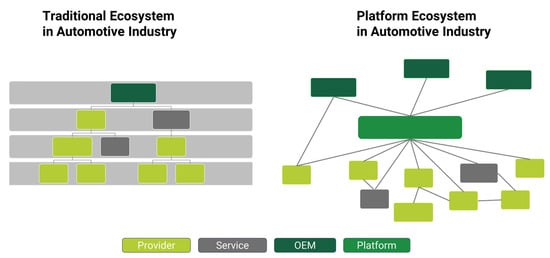

A study conducted by e-mobility BW highlights that the integration of platform-based approaches is driving a transformative shift in the automotive industry. This transformation facilitates the optimization of processes, the creation of innovative business models, and significant cost reductions [15].

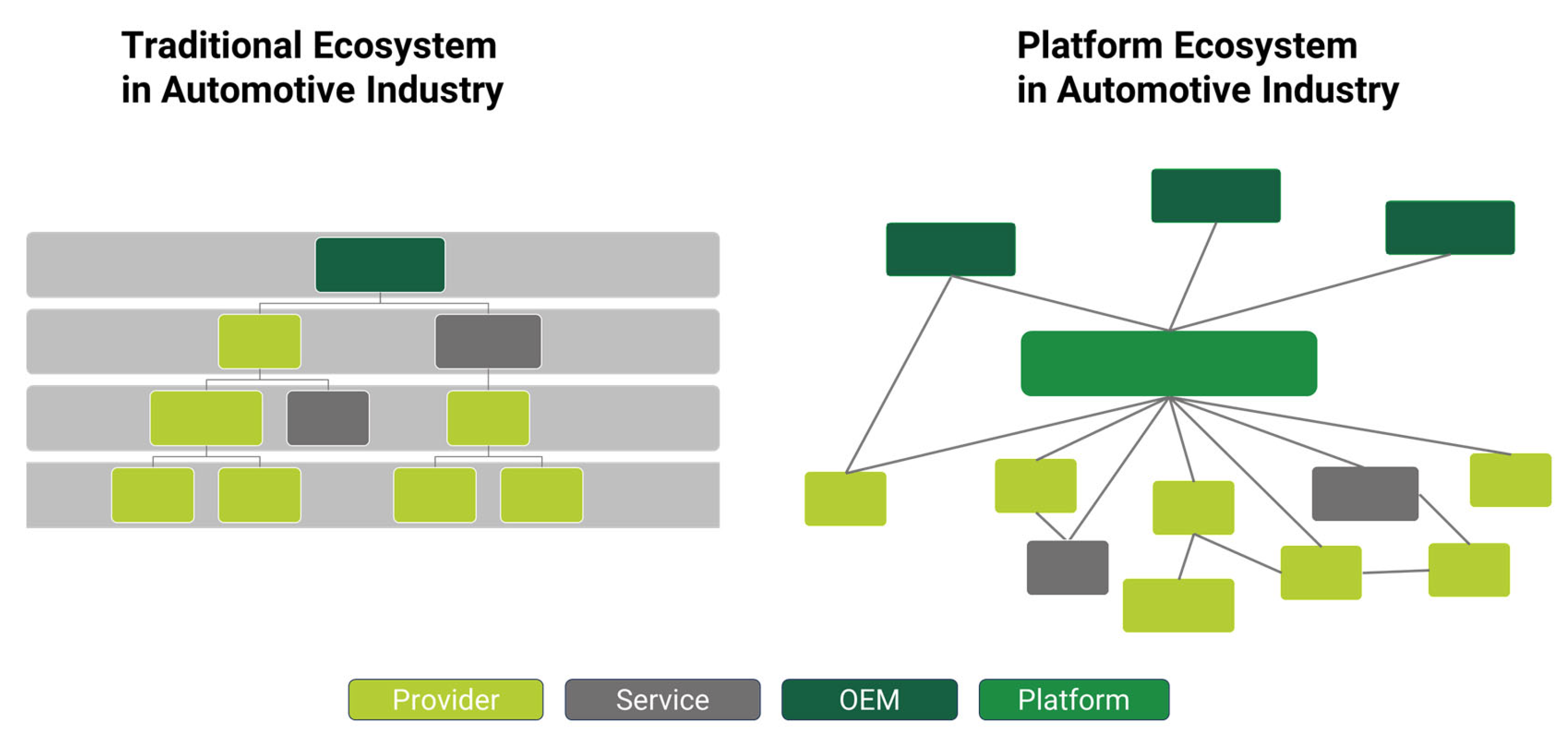

These platforms can be characterized as overarching business models that provide or license a predefined and standardized vehicle architecture as an open network. The primary aim is to facilitate interaction and mediation between supply and demand within the automotive ecosystem. This definition highlights the unique role of platforms in fostering collaboration and creating value through open networks. The interaction and mediation within such ecosystems are driven by their interconnected nature, enabling seamless connectivity between participants. The added value emerges from the open network established by the platform operator, which introduces competition into the interplay between suppliers and users. On the supply side, providers gain access to high-volume markets and new sales opportunities, while on the user side, participants benefit from reduced production costs and access to a broad pool of suppliers. The platform operator manages this complexity, ensuring smooth interactions and deriving profits from the economies of scale generated by increased competition. From the perspective of end customers, these systems ensure that the predefined and (semi-)standardized vehicle architecture is implemented in the most cost-effective manner possible. This balance between economic efficiency and networked collaboration exemplifies the transformative potential of platforms in reshaping the traditional automotive supply chain. By creating a unified ecosystem, platforms reduce barriers to entry, foster innovation, and enable the rapid scaling of solutions tailored to the needs of a dynamic market [13]. This aspect is reflected in Figure 2.

Figure 2.

Ecosystems in the automotive industry.

2.2. Northern Black Forest Region

The Northern Black Forest region, located in southwestern Germany, is a dynamic and economically diverse area. It spans 2340 square kilometers and is home to 614,402 residents. The region consists of the three counties of Enzkreis, Calw, and Freudenstadt, as well as the urban district of Pforzheim. Structurally, the northern part of the region is influenced by urbanized zones around Pforzheim, a major regional center, and Mühlacker, a mid-sized town. Both are strategically positioned along the development corridor between Karlsruhe and Stuttgart. In contrast, the southern portion of the region, encompassing the counties of Calw and Freudenstadt, is predominantly rural. Major cities in the region include Pforzheim, Mühlacker, Calw, Nagold, Freudenstadt, and Horb am Neckar [23].

The region hosts a wide range of industries, with notable sectors including fine mechanics, plastics technology, medical technology, timber, healthcare, and tourism. Additionally, the automotive industry and its suppliers, alongside the electronics sector, are among the region’s key economic drivers. The Northern Black Forest is distinguished by its high concentration of owner-managed SMEs, which are central to its economic identity. The industrial heart of the region is in its northern areas, particularly around Pforzheim, where leading suppliers to the automotive and mechanical engineering industries operate alongside innovative companies in precision and medical technology. In contrast, the southern counties are marked by strong presences in machinery manufacturing, timber, and plastics technology, as well as service-oriented industries such as tourism and healthcare. Across the 70 municipalities in the region, over 30,000 businesses operate, reflecting its diverse and vibrant economy [24,25]. Economically, the Northern Black Forest is strategically well positioned, with transport connections along the Stuttgart–Pforzheim–Karlsruhe and Stuttgart–Bodensee–Zurich axes. The region’s proximity to neighboring countries such as Switzerland, France, and Austria further enhances its appeal as a hub for business and trade.

The region is home to numerous family-run businesses with long-standing traditions and specialized expertise. Many of these companies are globally successful, including market leaders such as Arburg, Boysen, Doduco, Elumatec, Fischerwerke, Friedrich Münch, MAHLE, Schmid Brothers, Häfele, Homag, Georg Oest Mineralölwerk, Leuco, Memminger-IRO, Richard Wolf, Robert Bürkle, Schmalz, and Witzenmann. These firms play a crucial role in the region’s economic prosperity. The automotive trade also contributes significantly to the regional economy, underpinning much of the value creation in the vehicle and supplier industries [25].

The automotive sector is a cornerstone of the regional economy. In 2018, 1305 businesses—8.7% of all companies in the region—were active in this sector, marking a 1.8% increase since 2009. Socially insured employment in the automotive industry reached 30,229 workers in 2018, representing 14.0% of the regional workforce, up from 26,996 in 2009. Growth occurred across all subsectors. Employment in upstream components manufacturing increased by 5.3%, from 14,946 in 2009 to 15,737 in 2018. Downstream sectors, including trade, maintenance, and other services, experienced a 28.3% increase in employment, growing from 8087 to 10,376 in the same period. Core automotive manufacturing also grew by 3.9%, from 3969 employees in 2009 to 4116 in 2018 [26].

However, the region’s automotive suppliers are predominantly positioned in the lower tiers of the value chain (Tier 2 and beyond), with limited direct interaction with OEMs. This structural position exposes them to significant margin pressures and limits their influence on innovation. These challenges are further compounded by transformative trends in the automotive industry, including the rise in platform economies, alternative drivetrains, electrification, digitalization, and automation. These developments are expected to disrupt traditional supply chain structures and relationships, presenting both significant challenges and opportunities for the region’s businesses [27].

The Northern Black Forest region serves as an ideal case study due to its high concentration of automotive suppliers, many of which are SMEs heavily dependent on OEM-driven value chains. The region faces significant transformation pressures, including electrification, commoditization, and competition from platform-based market entrants like Foxtron, making it highly relevant for analyzing the impact of the platform economy. Additionally, many regional suppliers lack digital expertise and strategic flexibility, which presents unique barriers to integrating into platform ecosystems. As these challenges are not unique to this region, insights gained from this case study can be transferred to other European automotive supplier clusters, contributing to a broader industry discourse. This study, therefore, provides critical empirical insights into how traditional supplier regions can navigate digital transformation in the evolving automotive landscape.

2.3. Challenges for Supplier Companies

The Northern Black Forest region is deeply intertwined with the automotive industry, making it highly susceptible to the sector’s ongoing transformation. With counties such as Calw and Pforzheim exhibiting an above-average share of employees involved in ICE production—3.6% and 3.5%, respectively—the region faces considerable risks as the industry transitions to alternative powertrains. This shift threatens to render traditional components and production processes obsolete, with the associated jobs at imminent risk of permanent loss. Many of the region’s workers lack the skills needed to adapt to these changes, emphasizing the urgent need for comprehensive retraining and upskilling programs [26].

Emerging megatrends, including alternative drivetrains, electrification, lightweight construction, and connected vehicle technologies, are reshaping not only products but also production processes and entire value chains [28]. Innovations now focus on reducing emissions, energy consumption, and vehicle weight while enhancing connectivity and enabling autonomous driving. These trends are driven primarily by advancements in electronics and software, which have become essential enablers of modern automotive innovation. Consequently, the industry’s shift from hardware-driven solutions to software-centric systems is fundamentally altering the competitive landscape [29,30]. The transformation is further compounded by volatile supply chains, fluctuating raw material markets, and increasing demands for sustainable business practices. In this context, the electrification of powertrains is a particularly disruptive force for the Northern Black Forest region. Entire categories of components traditionally supplied by regional firms, such as ICE parts, conventional drivetrains, and certain chassis components, are rapidly becoming obsolete. Moreover, research suggests that high R&D investments by German automotive suppliers often fail to yield proportional profit margins, highlighting the economic strain on these businesses [31].

The structural transition within the automotive sector necessitates strategic adaptations among regional companies. However, the success of these strategies is contingent on the uncertain trajectory of the industry. For instance, if ICE vehicles retain significant market share in the medium term, suppliers with a strong focus on ICE-related products may identify short- to mid-term profitability pathways. While not sustainable in the long run, this approach could secure revenues for several years. Conversely, an accelerated transition to electric mobility (e-mobility) would require suppliers to pivot toward the production of components for electric drivetrains, battery systems, and related technologies. The fundamental uncertainty surrounding technological, societal, political, and economic developments in the automotive industry renders reliance on historical data insufficient for future-oriented decision-making [32].

The Northern Black Forest region is further characterized by a high number of Hidden Champions—specialized, often family-owned companies that dominate niche markets. However, the success of these firms is frequently tied to a narrow product range, limiting their capacity to adapt independently to broad and rapid market changes. Many of these businesses lack the financial and strategic resources needed to invest in new technologies or diversify their portfolios. This vulnerability underscores the need for targeted support and strategic alignment to ensure their long-term viability [25].

Additionally, the global automotive ecosystem is increasingly evolving toward platform economies, especially in high-volume vehicle production. This shift is exemplified by manufacturers like Mercedes-Benz, which has announced a strategic pivot toward low-volume premium segments, leaving the mass-market vehicle segments to platform-oriented automakers [33]. If other premium manufacturers, many of which are based in southern Germany, follow this trend, the Northern Black Forest region, which is highly dependent on automotive suppliers, must prepare for alternatives. Without preparation, the region’s companies risk losing access to key markets and production volumes [13,34].

One of the critical challenges in the Northern Black Forest is the lack of collaboration and networking among its numerous automotive suppliers. Synergistic partnerships and cooperative efforts are essential to address the complexities of this industrial transformation effectively. However, such initiatives are currently underdeveloped, leaving companies to face these challenges in isolation. This fragmented approach increases the likelihood of companies falling behind in the transformation process, jeopardizing their market positions and potentially leading to economic decline across the region [35].

The disruption extends beyond individual companies, affecting the region’s economic stability. The pressures of global competition, the rise in platform economies [36], and the increasing reliance on software-driven innovations necessitate substantial adjustments in workforce skills, business strategies, and operational models. To address these challenges, the region requires coordinated efforts to foster innovation, enhance connectivity among businesses, and develop forward-looking policies that enable companies to align with emerging demands [37].

In conclusion, the Northern Black Forest is at a pivotal moment as the automotive industry undergoes transformative changes. The region’s reliance on traditional ICE production and its concentration of SME suppliers amplifies its vulnerability. However, this transformation also presents opportunities for companies to innovate, diversify, and integrate into new market opportunities such as platform economies [38].

3. Research Methodology

To gather insights, a structured survey methodology was employed, targeting automotive suppliers in the Northern Black Forest. The survey aimed to assess current industry sentiment and the awareness of platform economies while identifying perceived opportunities, risks, and required support measures. Participants were selected based on regional relevance and involvement in the automotive supply chain, ensuring diverse yet industry-specific perspectives [39].

A standardized questionnaire was developed, incorporating closed-ended questions for quantitative analysis and an open-ended section for qualitative insights. Key terms were introduced to establish a common understanding. Data collection took place from August to September in 2024 with a mix of online and in-person interviews. The exact approach to survey design, data collection, and data analysis is detailed in the subsequent sections, providing a comprehensive overview to ensure accuracy, validity, and alignment with the research objectives.

3.1. Survey Design

This study aims to clearly define the RQs and objectives of the survey. Platform economy, as a powerful business model, has become well established and dominant in areas such as ride-hailing, accommodation services, and digital devices. However, in the automotive sector—particularly in relation to value creation—this model remains relatively novel. It is currently experiencing significant growth, particularly in the Asian market. The European automotive industry, having underestimated the transition from ICE to electric vehicles, now faces the challenge of catching up. This shift also exerts pressure on suppliers, particularly with the emergence of platform economies in the automotive sector. The concept involves offering standardized vehicle components on open automotive platforms or architectures. This approach enables manufacturing by companies that focus less on development expertise and more on production efficiency, reducing the technical demands on production facilities and favoring low-cost production locations.

The study focuses on the Northern Black Forest region, encompassing the districts of Enzkreis, Calw, Freudenstadt, and the city of Pforzheim. A significant proportion of companies in this area contribute to the value chain of the nearby automotive industry in Stuttgart. Many of these companies are specialized in developing and manufacturing ICE vehicles and now face considerable challenges due to the rise in electromobility. This study aims to determine whether the concept of platform economy is known in this region and whether it is perceived primarily as a risk or as an opportunity.

Given the complexity of the topic, the limited availability of company representatives, and the need for comparable results, structured interviews were chosen. These were implemented in the form of a standardized questionnaire using Microsoft Forms. In addition to the structured questions, an open-ended question was included to capture further suggestions, opinions, and comments, allowing for more nuanced insights beyond the predefined framework.

The survey questions were designed to be concise and precise, primarily employing closed-ended formats. Response options included binary answers (e.g., yes/no) and Likert-scale-based choices, along with an additional “Cannot assess” option to avoid introducing bias. The questions were specifically crafted to address the primary RQs, breaking them down into detailed aspects to cover all relevant dimensions. The questionnaire was tested internally and subsequently piloted with a lead partner at the beginning of the interview series. Minor adjustments were made based on the feedback received during this initial phase [39].

The questionnaire was structured to begin with general concepts, gradually transitioning to more specific and sensitive topics. The sequence included an introduction to key concepts, followed by sections exploring the familiarity with the platform economy, perceived opportunities, risks, and support needs.

To ensure the comparability of responses, key terms such as a platform (general), the platform economy in the automotive industry, and specific examples of platform economy applications were clearly explained at the beginning of the interview. This approach established a uniform knowledge baseline among participants.

Ethical principles were adhered to by focusing on the aggregated results rather than individual participants or companies. Anonymity was maintained, and specific names were excluded from the publication. Participants were fully informed about the objectives and intended use of the data collected in this study. Their consent was obtained, ensuring they were aware that the interviews would contribute to this research.

This structured approach ensures the reliability, validity, and ethical integrity of the study while addressing the key RQs in a scientifically rigorous manner.

3.2. Data Collection

The sampling strategy for this study was developed to ensure the inclusion of relevant and representative participants based on clearly defined criteria [40]. Companies were selected if they were in the Northern Black Forest region or its adjacent areas and operated within the automotive supplier industry. It was not required for these companies to generate most of their revenue from the automotive sector, but they had to contribute to the automotive value chain through a direct production or service step. This inclusive approach ensured that a diverse range of relevant businesses was represented, capturing insights from different facets of the supplier industry. Furthermore, participation in this study required a willingness to cooperate, an interest in the topic, and a general openness to discussing the implications of the platform economy. Companies that demonstrated engagement with digital transformation topics or showed curiosity about platform-based business models were prioritized to ensure meaningful insights. To meet the target of conducting 15 to 20 interviews, over 150 companies were contacted via email and phone, demonstrating a proactive recruitment process aimed at maximizing participation. The interviews were conducted between 30 August 2024, and 26 September 2024, providing a focused timeline for engagement and data collection.

Interviews were conducted following a rigorous process to ensure consistency and minimize potential bias. The team of three interviewers underwent joint training sessions to establish a shared understanding of the questionnaire and its interpretation. These discussions facilitated uniformity in conducting the interviews. Initially, two interviewers conducted the interviews together to refine and align their approaches, ensuring consistency across all sessions. Responses were meticulously documented during the interviews using Microsoft Forms, enabling real-time data input. This method ensured both accuracy and efficiency in capturing participant responses.

Participant recruitment was supported by targeted outreach efforts through research and the assistance of the Northern Black Forest Economic Development Agency. The agency played a vital role in identifying relevant companies that met the criteria and facilitating initial contact. Participants were further motivated to join the study by highlighting the opportunity to engage with a novel and forward-looking topic. The discussion allowed participants to reflect on their own position within the ongoing transformation of the automotive industry and gain fresh perspectives from external collaborators.

To provide participants with a comfortable and distraction-free experience, the study accommodated various modes of interview delivery based on individual preferences. Some interviews were conducted in person at company sites, allowing for direct interaction and an enriched exchange of ideas. Others were held online via Microsoft Teams, offering flexibility and convenience, especially for participants unable to meet in person. In two cases, interviews were conducted by phone, demonstrating adaptability to ensure maximum participation despite logistical constraints.

During the interviews, responses were systematically recorded. The structured format of Microsoft Forms facilitated this process by requiring each question to be addressed before progressing to the next. This sequential mechanism ensured that all questions were covered comprehensively and in order. Following the interview, the data were reviewed for completeness and clarity, with the systematic use of Microsoft Forms providing a robust framework for capturing and managing the data. This meticulous approach to data collection not only ensured accuracy and reliability but also created a dataset that was ready for immediate analysis.

By employing these strategies, the study maintained a high level of scientific rigor, ensuring that the sampling, data collection, and documentation processes were comprehensive, standardized, and aligned with the research objectives. The combination of targeted participant selection, careful interview preparation, and structured data recording created a strong foundation for generating meaningful and actionable insights.

3.3. Data Analysis

To ensure a systematic and structured analysis of the interview data, we applied thematic analysis following the approach by Braun and Clarke [41]. This method enables the identification, coding, and categorization of key themes from the interview responses, ensuring a replicable and transparent interpretation of the data. The analysis followed a six-step process, beginning with familiarization with the data through repeated reading of transcripts, followed by initial coding to identify key concepts. Next, similar codes were grouped into themes, which were then reviewed to ensure coherence and refined where necessary. Subsequently, themes were defined and named, ensuring that they accurately reflected the data, before producing the final analysis, in which themes were linked to the research questions to derive meaningful insights.

The inductive approach was used, allowing themes to emerge organically from the data rather than being predefined. Coding was conducted manually, with multiple researchers involved in cross-checking to refine theme definitions and minimize bias. The final themes were structured around barriers to engagement, perceived opportunities, strategic responses, and support needs related to the platform economy. This thematic structuring enhances validity and transparency, ensuring that the findings align with the study’s objectives.

To maintain accuracy, the transcription of interview data was performed systematically, ensuring consistency with the study’s research framework [42,43]. Depending on the responses and analysis requirements, data were processed as verbatim transcripts or summarized versions. The use of Microsoft Forms facilitated the initial organization and visualization of survey results, allowing for structured data representation and ease of further thematic categorization. These steps followed the outlined research objectives, ensuring a comprehensive and structured approach to data preparation.

For qualitative analysis, the thematic approach focused on identifying recurring patterns, central themes, and relationships within open-ended survey responses. While the study’s sample size of 18 companies does not allow for fully representative conclusions, it serves as a valuable case study of the current state of automotive suppliers in the Northern Black Forest region. The qualitative insights complement the quantitative data, providing a deeper context to the statistical findings.

Quantitative analysis was conducted using statistical methods to evaluate closed-ended questions and Likert-scale responses. Frequency analyses were performed to identify trends and key areas of interest, highlighting patterns of consensus or divergence among participants. These quantitative findings are presented in Section 4, structured according to the frequency and relevance of responses within different survey categories.

Ensuring validity and reliability was a key priority throughout the study. Validity was maintained by aligning the survey results with the study’s research questions and objectives, confirming that the data collected directly addressed the study’s scope. The structured questionnaire design and systematic interview process contributed to reliability, minimizing inconsistencies or bias in data collection.

The results were interpreted and visualized with an emphasis on clarity, accessibility, and practical relevance. They are presented in Section 4, organized by key themes and survey categories. To enhance comprehension, findings are communicated through textual explanations, tables, and visual diagrams, ensuring that the study provides actionable insights for both academic and industry stakeholders.

Finally, conclusions and recommendations were derived from the analysis, linking findings to the broader context of the automotive supplier industry. These insights are detailed in Section 5 (Discussion) and Section 6 (Conclusions), which also provide a transparent discussion of study limitations. Key constraints, such as sample size and regional focus, are acknowledged, and suggestions for future research are provided to address these limitations and explore related themes in greater depth. This comprehensive analytical approach ensures that the study meaningfully contributes to academic discussions and offers practical value for industry stakeholders navigating the evolving challenges of the platform economy in the automotive sector.

4. Results

This section presents the findings of the study, which are structured into six key thematic areas and supported by Figure 3, Figure 4, Figure 5, Figure 6, Figure 7 and Figure 8 for clarity. The first part provides an overview of the survey respondents, detailing company size, industry affiliation, and job roles, offering essential context for interpreting the study’s findings. The second section examines the awareness and perceived relevance of the platform economy among the surveyed companies, assessing the extent to which businesses recognize and integrate platform-based models into their operations. This study further explores the opportunities and risks associated with platform engagement, outlining potential benefits such as market expansion, efficiency improvements, and enhanced collaboration, while also addressing critical challenges such as increased competition, dependency on dominant platforms, and the loss of differentiation. In response to these opportunities and risks, this study investigates strategic approaches to the platform economy, distinguishing between proactive companies that are investing in platform integration and those that remain hesitant due to financial constraints, uncertainty, or a lack of technological readiness. Additionally, this study highlights barriers to implementation, including technological constraints, resource limitations, and organizational resistance, which prevent many suppliers from actively participating in the platform economy. Finally, this study identifies key success factors and support needs that companies consider crucial for a smooth transition. These include training programs, financial resources, regulatory clarity, and stronger industry collaboration, all of which are necessary to facilitate engagement with digital platforms and reduce risks associated with this business model. Open-ended responses provided further qualitative insights into global competition, investment feasibility, and the alignment of platform models with existing supply chain strategies. These perspectives help contextualize the results and offer a deeper understanding of how automotive suppliers perceive and engage with the platform economy.

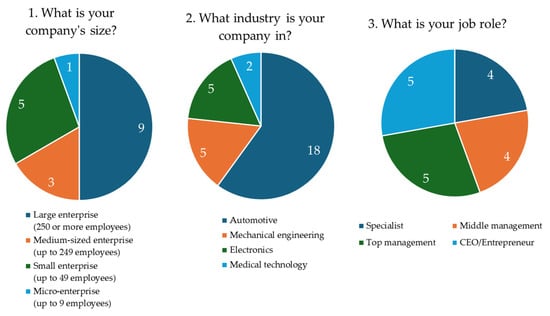

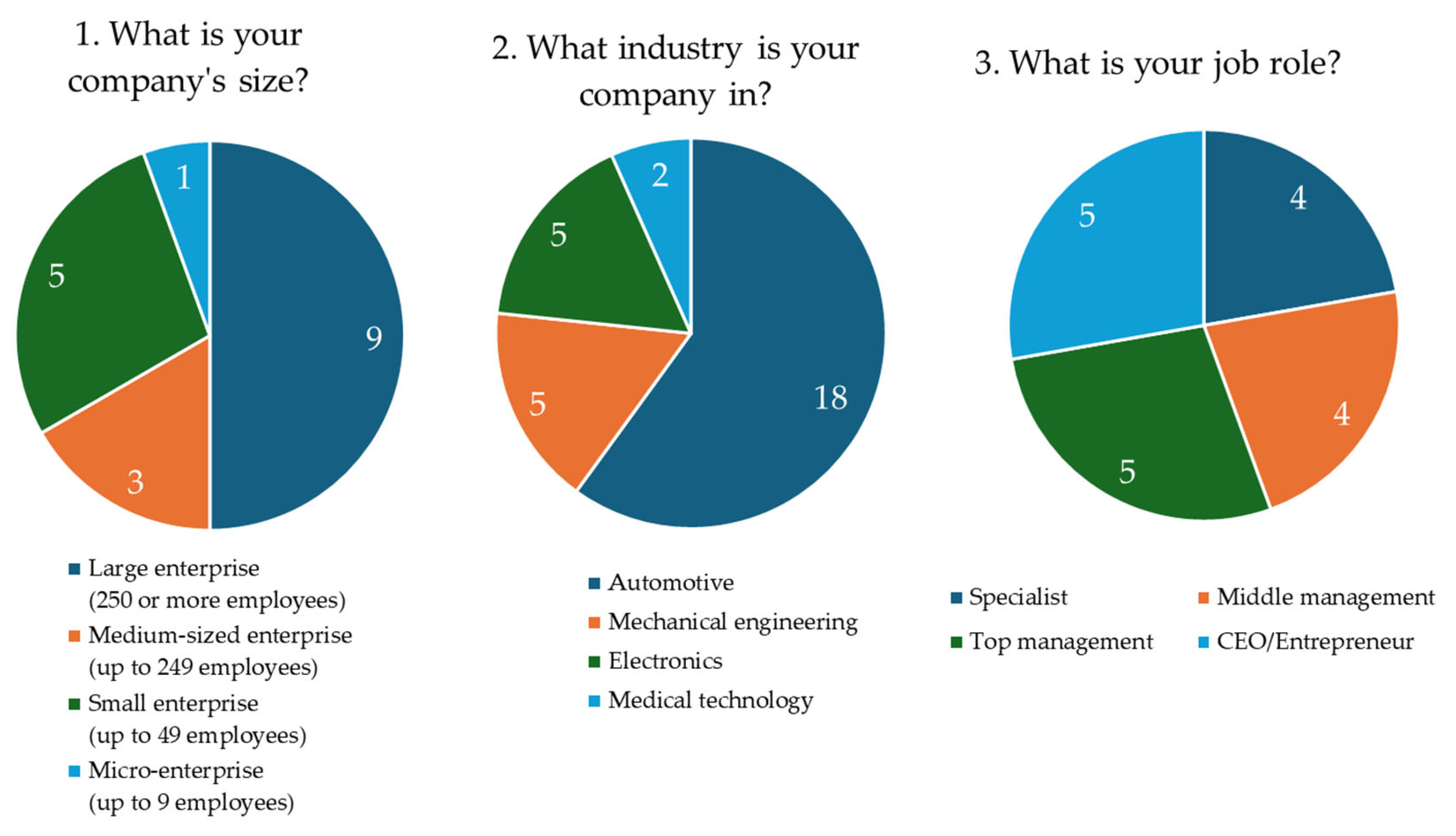

Figure 3.

Results on general information of the interviewees.

4.1. General Background of Respondents

The respondents represent a diverse mix of business sizes, industrial sectors, and organizational roles, ensuring a comprehensive analysis of perspectives on the platform economy. The sample includes one micro-enterprise, five small enterprises, three medium-sized enterprises, and nine large companies. Many of these companies maintain extensive production facilities, reflecting the Northern Black Forest’s strong presence in the automotive supply chain and its strategic role in national and international markets. In terms of industry affiliation, all participating companies identify themselves as part of the automotive industry, with five companies also engaged in mechanical engineering and electronics and two companies operating in the field of medical technology. This cross-sector representation ensures that the study captures a broad range of supplier perspectives. Furthermore, the survey captures a balanced representation of organizational roles. The respondents include five CEOs or company founders responsible for corporate strategy, five top managers involved in high-level decision-making, four middle managers overseeing operations, and four subject-matter experts providing specialized insights into platform-based business models. This diversity allows the study to explore both strategic and operational perspectives on platform economy adoption. The demographic distribution of the respondents is visually summarized in Figure 3, which provides an overview of company sizes, industry sectors, and job roles within the surveyed sample.

4.2. Awareness and Understanding of the Platform Economy

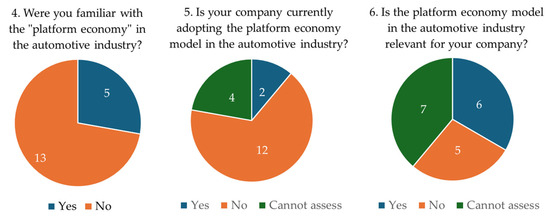

This study finds that awareness of the platform economy remains low among automotive suppliers in the Northern Black Forest region. Among the 18 surveyed companies, 13 reported being unfamiliar with the concept before the interview, while only 5 had some level of awareness. However, just two companies have already taken concrete steps toward integrating platform-based models into their business operations. Two primary barriers to awareness were identified. First, many respondents viewed platform economies as primarily relevant to consumer-oriented industries, such as e-commerce, mobility services, and digital marketplaces, and therefore less applicable to the traditional automotive supply chain. Second, a lack of industry-specific information and real-world case studies made it difficult for suppliers to assess how platform models could be effectively implemented in their own operations. This study also reveals a divided perspective on the perceived relevance of platform economies. Six companies believe that platform business models are relevant to their industry, while five do not, and seven remain uncertain. These findings suggest that without targeted awareness-building initiatives, many suppliers struggle to evaluate the potential impact of platform-based models on their business strategies. Figure 4 provides a visual representation of the level of awareness and perceived relevance of the platform economy among the surveyed companies.

Figure 4.

Awareness and relevance of the platform economy in the surveyed companies.

Figure 4.

Awareness and relevance of the platform economy in the surveyed companies.

4.3. Perceived Opportunities and Risks

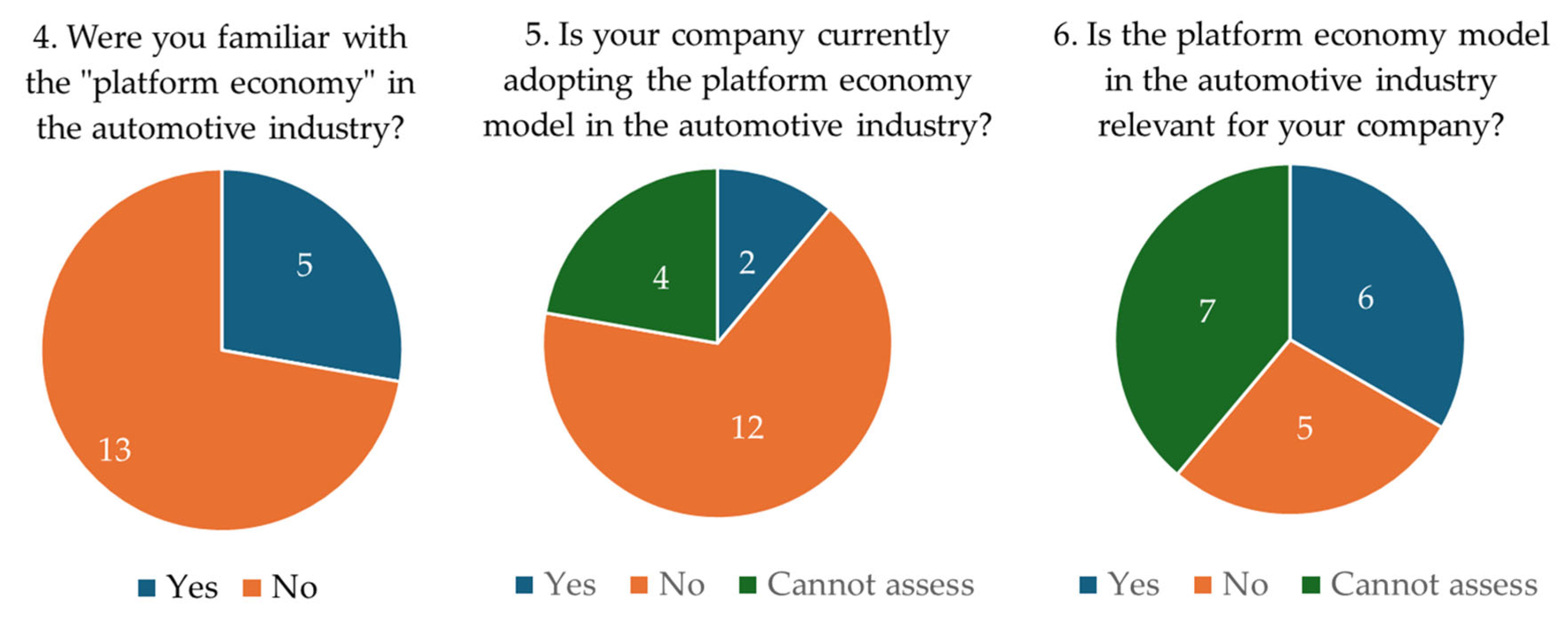

This study identifies both opportunities and risks associated with participation in the platform economy. Among the key opportunities, companies recognize expanded market access, as platform models can facilitate new relationships with OEMs and increase production volumes. Many respondents also highlighted efficiency gains, with digital platforms enabling streamlined logistics, optimized supply chain management, and reduced operational costs. Additionally, network effects and collaboration present an opportunity for suppliers to engage in broader innovation ecosystems and benefit from shared technological advancements. However, companies also express concerns regarding major risks associated with platform adoption. The most frequently cited risk is increased dependency on dominant platform providers, which could lead to a loss of strategic control over business operations. Many respondents also fear heightened price competition and a loss of differentiation, as platform models tend to standardize supplier offerings, making price a dominant factor in competition. Finally, a lack of internal expertise in digital platform integration is seen as a critical barrier, as many suppliers lack the technological capabilities and workforce skills necessary to transition successfully into platform-driven business environments. Figure 5 presents a visual summary of the key opportunities and risks identified by the respondents.

Figure 5.

Opportunities and risks of the platform economy in surveyed companies.

Figure 5.

Opportunities and risks of the platform economy in surveyed companies.

4.4. Strategic Responses of Companies

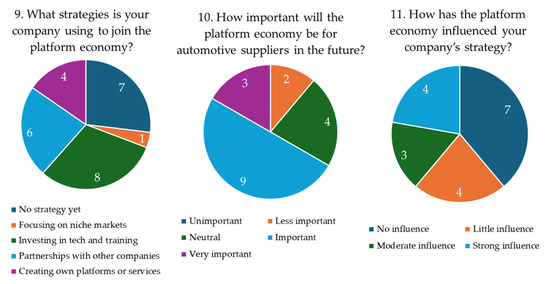

Companies exhibit two distinct strategic approaches regarding the platform economy. Larger firms tend to be proactive adapters, actively investing in technology, workforce development, and strategic partnerships to prepare for platform-based business models. Some of these companies have already initiated collaborations with technology providers, while others have begun developing their own platform services to maintain their competitiveness. Conversely, many smaller companies, particularly SMEs, remain passive observers. These firms express hesitation toward platform adoption, citing financial risks, uncertainty about return on investment, and a lack of immediate applicability. Many SMEs prefer to monitor industry trends before committing to significant changes. Survey data indicate that seven companies have no defined platform strategy, while eight have made initial investments in digital transformation; six have formed industry partnerships, and four are actively developing platform-based solutions. These findings are visually summarized in Figure 6, which depicts the strategic responses of companies based on their perception of the platform economy.

Figure 6.

Strategic approaches to the platform economy by the surveyed companies.

Figure 6.

Strategic approaches to the platform economy by the surveyed companies.

4.5. Challenges and Success Factors

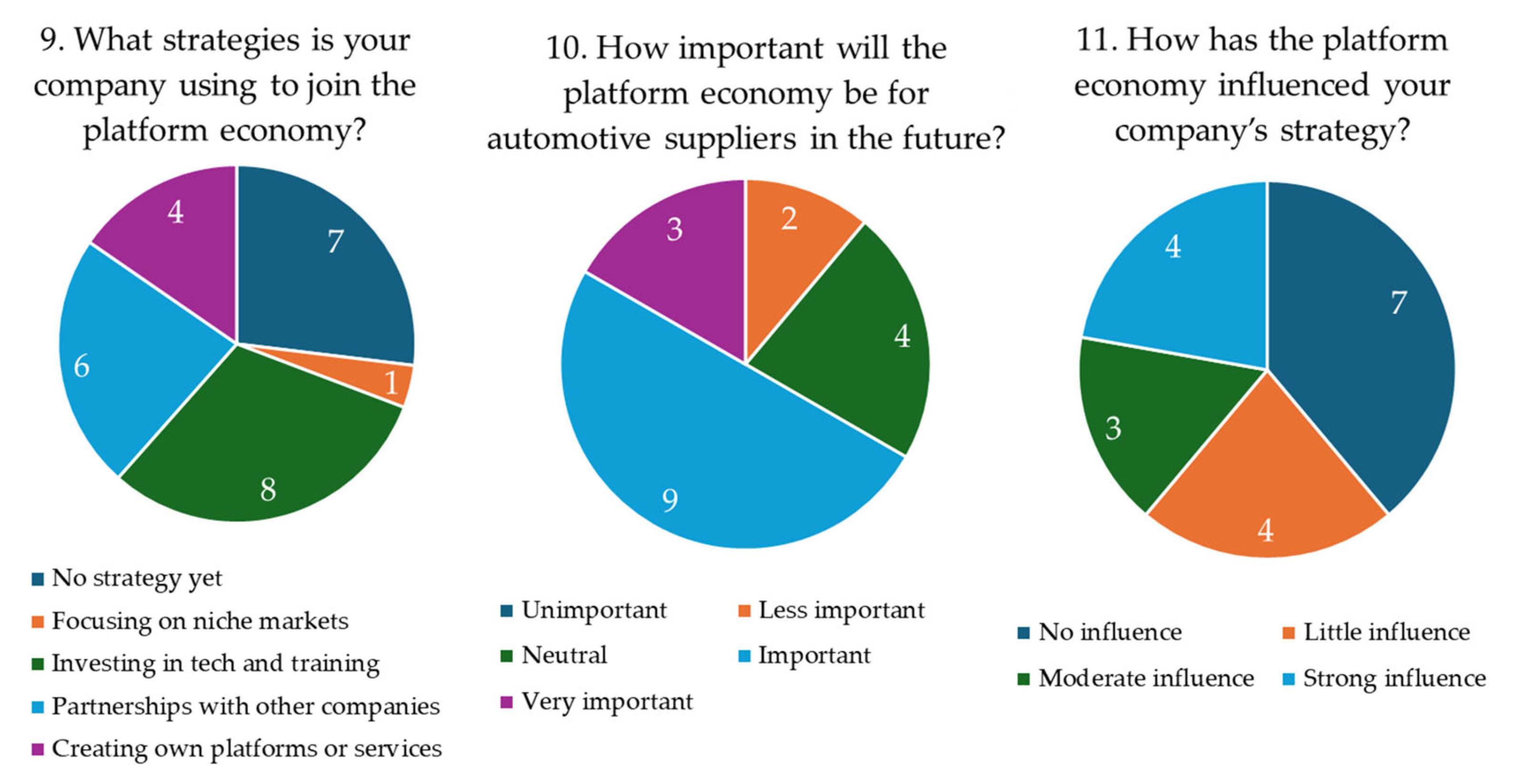

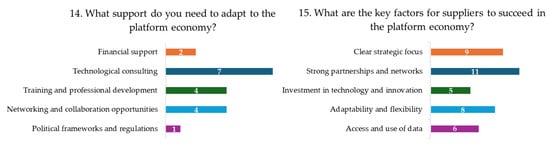

A critical area of inquiry concerns the challenges companies face when implementing the platform economy. This study examines the role of partnerships and networks in facilitating platform adoption, as well as the barriers that hinder successful implementation. The findings reveal divergent perspectives on the importance of collaborative ecosystems. While a minority of respondents downplay the role of partnerships, the majority (9 out of 18 companies) emphasize their critical importance for integrating platform-based business models. Beyond collaboration, companies also highlight specific obstacles to platform adoption. The most frequently cited challenge is technical difficulties, with 11 companies struggling with the integration of platform solutions into existing operations. Additionally, six companies cite the absence of a well-defined strategy, while seven companies identify cultural resistance within their organizations as a major barrier. Other constraints include a shortage of skilled personnel and insufficient training programs, which were mentioned by six respondents, and financial constraints were identified as a significant hurdle by five companies. These challenges illustrate the complexity of transitioning to platform economies, particularly for companies that lack technological expertise and strategic guidance. The findings also indicate a strong demand for support measures that would enable companies to successfully transition to platform-based business models. The most pressing need is for technical assistance and consulting services, as identified by seven companies, followed by workforce training and development, which were highlighted by four companies. Similarly, four companies emphasize the importance of building industry networks and fostering collaboration. Financial incentives, including funding programs and regulatory guidance, are also regarded as critical enablers, although they were mentioned by a smaller group of respondents. Beyond specific support needs, companies also identify key success factors that would facilitate the effective implementation of platform-based models. Most respondents (11 companies) highlight the necessity of strong partnerships and well-functioning networks, reinforcing the notion that collaborative ecosystems play a central role in platform adoption. Additionally, nine companies stress the importance of a clear strategic focus, while eight companies cite adaptability and flexibility as essential attributes for success. The findings also reveal that access to data and digital infrastructure is viewed as a key requirement by six companies, whereas five companies emphasize the need for greater investment in technology and innovation. These insights are visualized in Figure 7, which depicts the challenges that companies face in adopting platform business models, and Figure 8, which highlights the key success factors for platform economy integration.

Figure 7.

Challenges of the platform economy in surveyed companies.

Figure 7.

Challenges of the platform economy in surveyed companies.

Figure 8.

Success factors for the platform economy from surveyed companies.

Figure 8.

Success factors for the platform economy from surveyed companies.

4.6. Additional Insights from Open-Ended Responses

The final part of the survey provided qualitative insights from open-ended responses, further contextualizing the findings on platform adoption, investment feasibility, and global competition. A key theme emerging from the responses is the influence of China in the platform economy. While some respondents recognize China’s dominance in global supply chains and production capacity, concerns persist about its reliability as a long-term partner. This underscores the need for strategic caution when engaging with platform models influenced by Chinese manufacturers and market structures. Another recurring theme is the economic feasibility of investing in platform business models. Several companies express skepticism about large-scale investments, citing current economic uncertainties and unpredictable market conditions. However, respondents also identify specific niche applications where platform-based models could provide value, particularly in the distribution of spare parts and highly specialized supplier segments where scalability is less critical. Additionally, companies highlight the alignment between platform economies and just-in-time (JIT) supply chain strategies. Some respondents note that platform models offer greater flexibility, real-time responsiveness, and enhanced operational efficiency, making them particularly suited for industries that rely on dynamic demand management and lean logistics. These insights suggest that while widespread adoption remains uncertain, platform economies could become increasingly relevant in specific areas of automotive supply chain management.

5. Discussion

The findings of this study indicate that the concept of the platform economy remains largely unfamiliar to most surveyed automotive suppliers in the Northern Black Forest region. Of the 18 companies interviewed, 13 were previously unaware of the term, suggesting either its novelty within the sector or its perceived disconnect from practical business applications. Despite explanations provided at the beginning of the survey, several respondents struggled to fully grasp its implications, reflecting a gap between academic discussions and industry awareness. Consequently, only two companies reported having taken initial steps toward engaging with the platform economy, while the majority either denied any involvement or were unable to assess their position on the topic. However, some companies recognized its potential, with six out of eleven indicating that the platform economy business model, as described in this study, could be relevant to their organization. At the same time, seven companies were uncertain about its applicability, highlighting the need for further exploration and guidance to bridge this knowledge gap.

The results suggest a divergence in perception regarding the opportunities and risks associated with the platform economy. While approximately half of the companies identified potential benefits, such as leveraging network effects, expanding market access, and enhancing collaboration with complementary businesses, the perceived risks outweighed the advantages for most respondents. Key concerns included increased competition from low-cost manufacturers, pricing pressures, and a dependency on dominant platform providers. This fear of losing control over market positioning and strategic autonomy was particularly pronounced among SMEs, which are more vulnerable to industry shifts driven by larger platform players.

The strategic responses of surveyed companies can be categorized into two main groups. The first group—mainly larger firms—recognized the competitive pressures introduced by platform-based business models and was beginning to adjust its strategies accordingly. These companies emphasized investments in technology, workforce development, and partnerships to enhance their adaptability. The second group, consisting primarily of SMEs, reported a minimal impact on its current strategic orientation, indicating a lack of proactive engagement with platform-driven transformations. The absence of structured strategic planning in many organizations further reinforces the notion that the platform economy’s impact is not yet fully understood or prioritized within the regional automotive supply chain. This study, therefore, highlights an important tension: while companies acknowledge the long-term relevance of the platform economy, there is a significant gap between recognition and concrete strategic action.

Several barriers to adoption were identified, including technological constraints, financial limitations, and a shortage of skilled personnel. Many respondents also expressed uncertainty regarding the expected outcomes of platform-based business models, which contributes to hesitancy in making substantial investments in this direction. Interestingly, only six companies explicitly cited the lack of a clear strategic direction as a primary challenge, suggesting that practical concerns, such as financial viability and technical feasibility, are more immediate obstacles than strategic uncertainty.

Another key finding relates to the type of support measures companies consider essential. Contrary to initial expectations, respondents did not prioritize financial incentives or regulatory support. Instead, they emphasized the need for greater awareness of technological advancements, targeted training programs, and access to collaborative networks. The importance of peer learning and partnerships was particularly evident, as many companies expressed interest in engaging with organizations that have already navigated platform-based transformations. This finding underscores the necessity of knowledge-sharing initiatives, industry workshops, and cross-sector collaborations to facilitate informed decision-making and reduce uncertainty about the transition to platform-based business models.

This study also revealed a size-dependent variation in attitudes toward the platform economy. SMEs exhibited greater skepticism, largely due to their limited resources and unfamiliarity with the concept. Their cautious approach reflects the challenges of assessing long-term implications in an industry undergoing rapid transformation. In contrast, larger enterprises displayed a more open and adaptive stance, recognizing both the risks and opportunities associated with platform-based models. However, even among larger firms, concerns regarding standardization pressures and the erosion of differentiation strategies remained prevalent.

A fundamental question emerging from these findings is whether the platform economy should be seen primarily as an opportunity or a risk for the European and German automotive industries. Traditionally, these industries have been characterized by highly customized production and strong product innovation. The shift toward standardized platform-based architectures, as exemplified by Foxtron [6,7], raises concerns that German suppliers may be reduced to mere component manufacturers competing primarily on cost rather than innovation [13]. This transition challenges the existing value creation structures and necessitates a strategic reassessment of competitive positioning within platform ecosystems.

This study contributes to the growing body of research on the platform economy by offering empirical insights from a regional perspective, which has been largely overlooked in the existing literature. While most research focuses on OEMs and large multinational corporations, this study shifts the focus to automotive suppliers in a specific regional cluster, highlighting their unique challenges and support needs. The findings suggest that regional ecosystems require tailored adaptation strategies to ensure that SMEs and mid-sized firms can effectively participate in platform-based value networks rather than being marginalized by dominant players.

A limitation of this study is the sample size, which includes 18 companies from the automotive sector. While this provides valuable initial insights, a larger and more diverse sample would be needed to strengthen the generalizability of the findings. Future research should explore comparative studies between different regions to assess whether supplier attitudes toward the platform economy vary across industrial clusters. Longitudinal studies tracking how companies adapt their strategies over time in response to platform-based transformations would also be beneficial. Additionally, industry-wide collaborations between suppliers, policymakers, and platform operators could help define best practices for navigating platform-based ecosystems.

This study underscores the limited awareness and preparedness of automotive suppliers in the Northern Black Forest regarding the platform economy. While larger firms are beginning to adjust their strategies, SMEs face significant barriers to engagement, including technological constraints, competitive pressures, and a lack of knowledge-sharing opportunities. The results emphasize the need for greater awareness, targeted training, and strategic partnerships to bridge the gap between recognition and actionable transformation. By addressing these challenges, regional suppliers can better position themselves within evolving platform-based ecosystems, ensuring their competitiveness in the rapidly changing automotive landscape.

6. Conclusions

This study is the first of its kind to investigate the platform economy within the automotive sector, with a particular emphasis on the supplier industry and a regional focus on the Northern Black Forest. The research aimed to assess the level of awareness and understanding of platform-based business models among automotive suppliers while identifying challenges and potential measures to foster their adoption. To gather comprehensive insights, in-depth interviews were conducted during the summer of 2024 with representatives from 18 companies in the region, spanning various sizes and specializations within the automotive supply chain. The discussions centered on their familiarity with platform-driven strategies, readiness for digital transformation, and the perceived impact of platform ecosystems on business operations and market competitiveness. The analysis indicates that innovative approaches, such as the platform economy, are gradually entering established markets, including the German automotive industry and, more specifically, regionally embedded companies in the Northern Black Forest. However, due to the still-uncertain implications of this transformation, companies are only cautiously engaging with it. While they are expected to face significant challenges with their existing business models in the future, as outlined in the Introduction Section, they are currently still able to sustain their operations. Although the pressure for transformation is increasing, it does not yet appear to be sufficiently high, or it may be underestimated or deemed irrelevant by companies and their decision-makers. The findings of this study provide a valuable foundation for shaping targeted support measures and fostering a more collaborative and innovative platform economy in the automotive supply sector. Moreover, ongoing observation of regional developments is essential to determine whether emerging patterns could provide insights applicable to global markets.

This study’s results presented a diverse range of outcomes. While the concept is not entirely unknown, many respondents were unfamiliar with the platform economy. However, when the topic was introduced to and explained to the participants, they expressed interest and recognized its potential to create opportunities for regional and corporate diversification, thereby enhancing future competitiveness. Nevertheless, it also became evident that the full implications of the concept remain unclear. A significant proportion of respondents expressed uncertainty regarding the platform economy’s status as either a transient trend or a sustainable business model. This uncertainty is further compounded by the associated risks, including the necessity of substantial resources, expertise, and technological innovation capabilities for effective participation. The interviews that were conducted led to critical discussions on the subject, emphasizing both the relevance and the curiosity surrounding the concept of the platform economy. These insights directly address RQ 1, which concerns the awareness and perceived relevance of the concept.

In response to RQ2, which examines the support measures required by automotive companies in the Northern Black Forest to assess opportunities and risks associated with the platform economy along the value chain, the findings highlight several key requirements. Companies emphasize the necessity of enhanced access to relevant information resources, engagement with knowledgeable partners, and structured mechanisms for identifying applicable use cases. Furthermore, firms require systematic approaches to evaluate the compatibility of platform-based models with their existing business strategies. This includes analytical frameworks that facilitate a nuanced assessment of whether the platform economy constitutes an opportunity for growth or a potential risk to established operations. By addressing these needs, businesses can make informed strategic decisions regarding their participation in digital platform ecosystems.

In this study, we provide an initial examination of the challenges faced by the supplier industry in the Northern Black Forest region, extending beyond the transition from combustion engines to electric mobility. These challenges are further intensified by the emergence of new value chain structures driven by Asian manufacturers such as Foxtron. Our findings indicate that regional companies perceive the platform economy in a specific way and recognize potential engagement opportunities. We also identify the necessary steps to facilitate their participation, as some companies are already establishing value creation networks within platform ecosystems. This transformation could enable them to operate under entirely new conditions and paradigms in the future.

To build on this research, we propose several next steps to enhance the generalizability of our findings and develop practical support measures for suppliers. Future studies should expand the scope to include a broader range of companies across different regions and industry segments. A comparative analysis between regional clusters could help us understand how geographic and technological factors influence supplier attitudes toward the platform economy. Additionally, longitudinal research would allow us to track how companies adapt over time, identifying evolving barriers and success factors. To address the identified weaknesses, we aim to focus on developing targeted support measures, such as training programs, knowledge-sharing networks, and financial models, to help suppliers navigate platform ecosystems. Additionally, further investigation into funding mechanisms and regulatory frameworks could provide insights into reducing financial risks and ensuring compliance. We also propose employing scenario-based modeling to anticipate market shifts and strategic responses, helping companies make informed decisions about their platform engagement strategies. We recommend that the development of these trends be closely monitored, with continued engagement and dialog with companies to explore the implications and potential responses to these transformative shifts in the automotive sector. Ongoing collaboration will be essential in understanding the evolving dynamics of the platform economy and its impact on regional suppliers. The success of this transition depends on the implementation of proactive measures, including workforce retraining, strategic diversification, and fostering collaboration within the region. By addressing these gaps, our future research can provide actionable insights to help regional suppliers adapt, compete, and thrive, ensuring the Northern Black Forest remains a competitive and resilient hub in the evolving global automotive industry.

Author Contributions

The manuscript was prepared with input from all authors. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Ethical review and approval were waived for this study because the research involved minimal risk to participants; no sensitive personal data were collected, and informed consent was obtained prior to data collection. This study was conducted in accordance with the ethical guidelines of the Declaration of Helsinki.

Informed Consent Statement

Written informed consent for the processing and publication of the interview data was obtained from all participants prior to the commencement of data collection.

Data Availability Statement

The datasets generated and/or analyzed during the current study are available from the corresponding author on reasonable request.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- Kenney, M.; Zysman, J. The rise of the platform economy. Issues Sci. Technol. 2016, 32, 61. [Google Scholar]

- Xue, C.; Tian, W.; Zhao, X. The Literature Review of Platform Economy. Sci. Program. 2020, 2020, 8877128. [Google Scholar] [CrossRef]

- van der Aalst, W.; Hinz, O.; Weinhardt, C. Big Digital Platforms. Bus Inf. Syst. Eng. 2019, 61, 645–648. [Google Scholar] [CrossRef]

- Belleflamme, P.; Peitz, M. Platforms and network effects. In Handbook of Game Theory and Industrial Organization; Corchón, L.C., Marini, M.A., Eds.; Edward Elgar Publishing: Cheltenham, UK; Northampton, MA, USA, 2018; ISBN 9781788112789. [Google Scholar]

- Steinberg, M. From Automobile Capitalism to Platform Capitalism: Toyotism as a prehistory of digital platforms. Organ. Stud. 2022, 43, 1069–1090. [Google Scholar] [CrossRef]

- Bork, H. Foxconn Wird Zulieferer und Autohersteller. Automobil Industrie. 22 October 2024. Available online: https://www.automobil-industrie.vogel.de/foxconn-autozulieferer-autohersteller-a-fd3ed7cdda0e75ee91724416ea537f67/ (accessed on 23 January 2025).

- Technologies, F.V. Foxtron Vehicle Technologies. Available online: https://www.foxtronev.com/en/about (accessed on 27 January 2025).

- Grimm, A.; Pfaff, M. Transformation der Wertschöpfung in der Automobilbranche: Teilbericht Arbeitspaket 4: Entwicklungen im Regime; Working Paper Forschungsförderung; Hans-Böckler-Stiftung: Düsseldorf, Germany, 2022. [Google Scholar]

- Galgóczi, B. Towards a Just Transition: Coal, Cars and the World of Work; ETUI European Trade Union Institute: Brussels, Belgium, 2019; ISBN 9782874525452. [Google Scholar]

- Schwabe, J. Risk and counter-strategies: The impact of electric mobility on German automotive suppliers. Geoforum 2020, 110, 157–167. [Google Scholar] [CrossRef]

- Zhang, C.; Ma, H.-M. E-retailer information sharing with suppliers online selling mode. Inf. Sci. 2023, 622, 1252–1272. [Google Scholar] [CrossRef]

- Altenburg, T.; Corrocher, N.; Malerba, F. China’s leapfrogging in electromobility. A story of green transformation driving catch-up and competitive advantage. Technol. Forecast. Soc. Change 2022, 183, 121914. [Google Scholar] [CrossRef]

- Koelmel, B.; Fischer, L.; Juraschek, E.; Peuker, L.; Stemmler, N.; Vielsack, A.; Bulander, R.; Hinderer, H.; Kilian-Yasin, K.; Brugger, T.; et al. Navigating the Challenges of Commodity Traps and Platform Economies: An Assessment in the Context of the Northern Black Forest Region and Future Directions. Commodities 2024, 3, 314–333. [Google Scholar] [CrossRef]

- Demary, V.; Rusche, C. The Economics of Platsforms; Institut der deutschen Wirtschaft: Köln, Germany, 2018; Available online: https://www.iwkoeln.de/studien/vera-demary-christian-rusche-the-economics-of-platforms.html (accessed on 27 December 2024).

- Bratzel, S.; Böbber, F. Digitalisierung in der Mobilitätswirtschaft: Erfolgsfaktoren der Daten- und Plattformökonomie; e-mobil BW GmbH: Stuttgart, Germany, 2023; Available online: https://www.e-mobilbw.de/fileadmin/media/e-mobilbw/Publikationen/Studien/e-mobilBW_Studie_Digitalisierung_in_der_Mobilitaetswirtschaft_Daten-_und_Plattformoekonomie.pdf (accessed on 27 December 2024).

- Acs, Z.J.; Song, A.K.; Szerb, L.; Audretsch, D.B.; Komlósi, É. The evolution of the global digital platform economy: 1971–2021. Small Bus. Econ. 2021, 57, 1629–1659. [Google Scholar] [CrossRef]

- Gabriel, L. Digitale Plattformen: Grundlagen und Erscheinungsformen; Universität Trier: Trier, Germany, 2020; Available online: https://www.uni-trier.de/fileadmin/fb4/prof/BWL/AMK/Forschungsberichte/Gabriel_2020_Digitale_Plattformen.pdf (accessed on 27 December 2024).

- Derave, T.; Prince Sales, T.; Gailly, F.; Poels, G. Comparing Digital Platform Types in the Platform Economy. In Advanced Information Systems Engineering; La Rosa, M., Sadiq, S., Teniente, E., Eds.; Springer International Publishing: Cham, Switzerland, 2021; pp. 417–431. ISBN 978-3-030-79381-4. [Google Scholar]

- Falck, O.; Koenen, J. Industrielle Digitalwirtschaft: B2B-Plattformen. 2020. Available online: https://bdi.eu/publikation/news/Industrielle-Digitalwirtschaft-B2B-Plattformen/ (accessed on 27 December 2024).

- Drewel, M.; Özcan, L.; Gausemeier, J.; Dumitrescu, R. Platform Patterns—Using Proven Principles to Develop Digital Platforms. J. Knowl. Econ. 2021, 12, 519–543. [Google Scholar] [CrossRef]

- Hoffmann, M.; Schröder, C.; Pasing, P. Digitale B2B-Plattformen: Status quo und Perspektiven der Industrie in Deutschland; WISO Diskurs: Bonn, Germany, 2021; Available online: https://library.fes.de/pdf-files/wiso/17339.pdf (accessed on 24 December 2024).

- Pidun, U.; Reeves, M.; Schüssler, M. Chapter 2 Do You Need a Business Ecosystem? In Business Ecosystems; Reeves, M., Pidun, U., Eds.; De Gruyter: Berlin, Germany, 2022; pp. 13–26. ISBN 9783110775167. [Google Scholar]

- Regionalverband Nordschwarzwald. Daten & Fakten—Regionalverband Nordschwarzwald. Available online: https://nordschwarzwald-region.de/verband/daten-fakten/ (accessed on 23 January 2025).

- Industrie- und Handelskammer Nordschwarzwald. Konjunkturbericht Nordschwarzwald—Wirtschaft sendet Warnsignal an die Politik. Available online: https://www.ihk.de/nordschwarzwald/produktmarken/standort/wirtschaftsstandort-nordschwarzwald/konjunkturberichte/konjunkturbericht-2614058 (accessed on 23 January 2025).

- IHK Region Stuttgart. Die größten Unternehmen in Baden-Württemberg; IHK Region Stuttgart: Stuttgart, Germany, 2024. [Google Scholar]

- Bundesagentur für Arbeit. Arbeitsmarktreport—Länder, Kreise, Regionaldirektionen und Agenturen für Arbeit; Bundesagentur für Arbeit: Nuremberg, Germany. 2019; Available online: https://statistik.arbeitsagentur.de/SiteGlobals/Forms/Suche/Einzelheftsuche_Formular.html?nn=15024&r_f=bw_Nagold+bw_Pforzheim+rd_Baden-Wuerttemberg_RD+bw_Enzkreis+bw_Calw&topic_f=amr-amr (accessed on 27 December 2024).

- Sunmola, F.; Mbafotu, O.R.; Salihu-Yusuf, M.L.; Sunmola, H.O. Lean green practices in Automotive Components Manufacturing. Procedia Comput. Sci. 2024, 232, 2001–2008. [Google Scholar] [CrossRef]

- Yeung, G. Competitive dynamics of lead firms and their systems suppliers in the automotive industry. Environ. Plan A 2024, 56, 454–475. [Google Scholar] [CrossRef]

- Richter, A.; Waidelich, L.; Kölmel, B.; Bulander, R.; Glaser, P.; Proske, M.; Brügmann, S. Digitalisation and Future Challenges in Rural Areas: An Open Innovation based Research. 16th International Conference on e-Business; SCITEPRESS—Science and Technology Publications. In Proceedings of the 16th International Joint Conference on e-Business and Telecommunications, Prague, Czech Republic, 26–28 July 2019; pp. 147–153, ISBN 978-989-758-378-0. [Google Scholar]

- Intarakumnerd, P. Technological Upgrading and Challenges in the Thai Automotive Industry. J. Southeast Asian Econ. 2021, 38, 207–222. [Google Scholar] [CrossRef]

- Felser, K.; Wynn, M. Managing the Knowledge Deficit in the German Automotive Industry. Knowledge 2023, 3, 180–195. [Google Scholar] [CrossRef]

- Rahim, M.A.; Rahman, M.A.; Rahman, M.M.; Asyhari, A.T.; Bhuiyan, M.Z.A.; Ramasamy, D. Evolution of IoT-enabled connectivity and applications in automotive industry: A review. Veh. Commun. 2021, 27, 100285. [Google Scholar] [CrossRef]

- Li, X. An Analysis of Mercedes-Benz Marketing Strategy. Front. Bus. Econ. Manag. 2022, 6, 87–89. [Google Scholar] [CrossRef]

- Andersen, M.S. Challenges facing the USA in matching Germany on advanced manufacturing for green growth. Int. J. Innov. Stud. 2024, 8, 13–24. [Google Scholar] [CrossRef]

- Regionalverband Nordschwarzwald. Gemeinsam für die Region: Strategiefelder und Entwicklungsziele der Entwicklungsstrategie Nordschwarzwald 2030+; Regionalverband Nordschwarzwald: Pforzheim, Germany, 2020; Available online: https://nordschwarzwald-region.de/wp-content/uploads/2024/03/broschuere-entwicklungsstratgie-nordschwarzwald-2030-data.pdf (accessed on 27 December 2024).

- Hind, S.; Kanderske, M.; van der Vlist, F. Making the Car “Platform Ready”: How Big Tech Is Driving the Platformization of Automobility. Soc. Media Soc. 2022, 8, 20563051221098697. [Google Scholar] [CrossRef]

- Liu, Z.; Zhang, W.; Zhao, F. Impact, Challenges and Prospect of Software-Defined Vehicles. Automot. Innov. 2022, 5, 180–194. [Google Scholar] [CrossRef]

- Waidelich, L.; Kölmel, B.; Bulander, R.; Brugger, T. Approaching a regional innovation ecosystem in the Northern Black Forest for a future-orientated economy and society. Procedia Comput. Sci. 2022, 204, 253–260. [Google Scholar] [CrossRef]

- Nardi, P.M. Doing Survey Research: A Guide to Quantitative Methods, 4th ed.; Routledge Taylor & Francis Group: New York, NY, USA; London, UK, 2018; ISBN 9781315172231. [Google Scholar]

- Barrett, D.; Twycross, A. Data collection in qualitative research. Evid. Based Nurs. 2018, 21, 63–64. [Google Scholar] [CrossRef] [PubMed]

- Braun, V.; Clarke, V. Using thematic analysis in psychology. Qual. Res. Psychol. 2006, 3, 77–101. [Google Scholar] [CrossRef]

- Aithal, A.; Aithal, P.S. Development and Validation of Survey Questionnaire & Experimental Data—A Systematical Review-based Statistical Approach. Int. J. Manag. Technol. Soc. Sci. 2020, 2, 233–251. [Google Scholar] [CrossRef]

- Knowledge-Based Intelligent Information and Engineering Systems (Vol. # 4253): 10th International Conference, KES 2006, Bournemouth, UK, 9–11 October 2006; Proceedings, Part III; Springer: Berlin/Heidelberg, Germany, 2006; ISBN 978-3-540-46544-7.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).