1. Introduction

FinTech is an advanced and expanding sector that utilizes technological breakthroughs to deliver novel financial services and models. It is the embodiment of the combination of the economic and technological industries. According to Li and Xu [

1], as well as other sources such as Cheng and Qu [

2] and Thakor [

3], the term FinTech refers to the convergence of finance and technology, with an emphasis on the development of new and improved financial solutions. The FinTech business encompasses a diverse variety of goods, services, and concepts that have the potential to transform monetary transactions internationally. FinTech is a rapidly evolving industry that strives to increase access to the financial system, with a special emphasis on groups that were previously underserved or had limited access to traditional financial services [

4,

5]. FinTech companies are upending the traditional banking system by providing fresh solutions that are more efficient, quicker, and less expensive. FinTech provides a fundamental shift in financial services, implying that traditional banks could be supplanted by digital solutions and other internet-enabled devices. The word refers to businesses that deliver efficient and user-friendly financial services by utilizing the internet, mobile phones, and open-source software. FinTech firms are increasingly offering traditional financial items such as payment services and loans that were previously solely available from banks; these include payment services, loans and credit facilities, investment, wealth management, and so on.

FinTech is making significant advances in the financial services industry, mostly through disruptive innovations. This trend has brought about profound shifts in the industrial environment, challenging existing power structures and providing alternatives to the services previously controlled by major financial institutions. Financial institutions have already begun to incorporate these new technologies in order to promote direct communication between borrowers and investors, potentially shortening the financing process [

5,

6]. However, financial firms are experiencing difficulties adapting their outdated processes to modern technology and need to consider the consequences this could potentially have on a cultural level within the firms and on their people. This challenge highlights how legacy systems and established operational frameworks, the pace of technological change, and the regulatory complexities in traditional financial institutions often pose barriers and add to the adaptation challenges faced by those firms [

4,

5,

6,

7]. This justifies their delay in significantly upgrading their systems and completely adopting FinTech technology, despite having previously begun to invest significantly in this field. Integration and collaboration of banks with FinTech businesses, as well as the creation of new apps, can lead to increased bank efficiency and the introduction of more cost-effective services [

5,

6]. The standards of business operations in the financial industry are being adapted and transformed in order to include the advances brought about by the digital age. The issue for regulators is to guarantee that the operational risks associated with the widespread adoption of new technologies are mitigated in order to avoid the formation of systemic risks that could potentially jeopardize financial system stability [

5,

8].

Technological advancements are producing major changes in the financial industry, not only by enhancing basics such as the speed, security, and transparency of traditional operations, but also by becoming crucial in fostering financial inclusion. By attracting new participants into the market and developing innovative products and services, FinTech allows a significantly broader access, improved quality, and usage of financial services amongst a wider range of the population. Blockchain and crypto technology, e-commerce, digital wallets, and digital currencies (such as Bitcoin) are transforming the way payments are made, making them faster, safer, more transparent, and affordable [

4,

7]. Globally, we are witnessing a growing trend, in which not only giant banks, but also smaller banks, insurance businesses, and asset management firms, are acknowledging the necessity to adopt and integrate FinTech solutions into their operations. They undertake direct investments in this field as well as pioneering partnerships. The growing maturity of FinTech has led to an increasing number of investors, with more active engagement of corporations from diverse industries, in addition to the conventional large banking and insurance institutions [

4,

5,

6].

The digital transformation of financial services is based on innovative business strategies and user adoption of information technology. Due to the range of commodities offered, this technology allows access to new markets. Digital technologies enhance the experience of interacting with people by taking their feedback into account and delivering greater transparency. Many lengthy empirical research studies on the adoption of various forms of technology have been conducted over the past few decades, utilizing diverse methodological techniques. In order to investigate people’s technology adoption behaviors, the Technology Adoption Model (TAM) was established based on the causal relationships of the Theory of Reasoned Action (TRA). TAM focuses on the consumers’ intentions to utilize technology and their degree of adoption of technology. This model varies from the Theory of Reasoned Action in that it focuses on technology adoption directly, merging the user’s personal ideas and behaviors with those of others around them [

9,

10,

11,

12]. According to TAM, the two primary features that predict technology acceptance are ease of use (ease of use) and effort expectation (effort expectancy), both of which have been thoroughly researched and have been confirmed to be accurate indicators for evaluating acceptance [

9,

12,

13].

In this study, we investigated the factors that influence FinTech service adoption, including effort expectancy (EE), government support (GS), performance expectancy (PE), and trust in FinTech services (TF). Our findings reveal that EE and PE have a significant beneficial influence on FinTech adoption, emphasizing the importance of the transparency of use and the perceived benefits. We additionally determined a direct positive association between government support and both EE and TF, highlighting the crucial role of government in building trust and reducing the perceived effort involved in adopting FinTech services. However, government support was not a direct driver of adoption. Instead, it was revealed that trust in FinTech services functioned as a mediator between government support and adoption.

The article is structured as follows:

Section 2 provides the relevant literature review on the current topics and applications of user adoption and the acceptance of technology models in the context of FinTech services. In addition, we place particular emphasis on the factors of trust and technology acceptance with regard to future intentions to use FinTech services. Moreover, we study similar research conducted with the Greek population. In

Section 3, we provide a detailed description of the model we constructed and evaluated in our research, followed by the analysis and presentation of our findings in

Section 4.

Section 5 discusses and interprets the results of our study and identifies the related limitations. Finally, we conclude and provide suggestions for future research.

2. Literature Review and Hypothesis Development

2.1. Determinants of FinTech Adoption

Τhe objective of FinTech solutions is to simplify conventional financial procedures, boost automated processes, minimize expenses, and offer more tailored and user-friendly experiences for both businesses and consumers [

5]. In the realm of financial technology, there are various innovative solutions that have emerged, reshaping the landscape of financial services. These technologies cater to diverse aspects of finance, each contributing to increased efficiency and convenience. FinTech has a widespread impact across all segments of the financial industry, encompassing a wide range of applications from digital payments to blockchain; its influence is not limited to client facing but also encompasses internal financial operations [

14].

One of the many adoptions of FinTech is that of open banking. It is a financial practice and regulatory framework that allows third-party financial service providers to access and use financial data, such as account information and transaction history, from banks and other financial institutions through application programming interfaces [

15]. De Mariz [

16] highlighted the diverse and inclusive roles played by FinTech services in today’s financial landscape; these services encompass digital banking, mobile payments, and microfinance. They emphasize the critical role that regulatory bodies have, particularly in terms of how regulations shape the FinTech industry and benefit consumers. The study of Chan et al. [

17], which focused on the field of open banking and the implementation of FinTech, showed that practitioners are encouraged to emphasize the practical benefits of open banking and to understand and address the social influence and perceived risks [

17]. Policymakers are advised to focus on creating a robust governance framework that instills trust in the open banking system. Collaborative efforts between practitioners and policymakers, along with transparent communication, can contribute to a more successful and widely accepted adoption of open banking services [

11].

Another example of FinTech adoption is the mobile payment. In one study that focused on the Dutch financial system, the researchers found that mobile payment providers enhance technical protection measures and offer incentives to bolster the mobile payment business. Notably, the COVID-19 outbreak has led to a decrease in cash payments and an uptick in contactless payments in the Netherlands, positioning mobile payments as a means to ensure public health and mitigate the spread of the virus [

8]. The rise of FinTech during the COVID-19 pandemic in the context of accessing financial services has been extensively studied [

18,

19]. Also, in this context, the researchers take into account the variable of e-loyalty and make a comparison between the post- and pre-COVID-19 era [

20].

In the study of Kakinuma [

21], the author highlights the importance of leisure, demonstrating that individuals with a strong understanding of financial matters are more inclined to embrace FinTech when they enjoy greater freedom in their lives. This correlation ultimately results in an enhanced quality of life. He suggests that the integration of FinTech usage should be advocated as an essential life skill, one that is equivalent in importance to traditional financial literacy. Recent findings indicate that possessing digital financial literacy has a positive impact on financial behavior and decision-making processes [

22].

From an online survey in Indonesia, the results underscore user innovativeness as a significant predictor which directly and indirectly influences FinTech adoption in the country [

23]. Also, user attitude emerges as the most crucial factor impacting FinTech adoption, while financial literacy is identified as the least significant variable, challenging common beliefs. Two variables that have been studied in depth are perceived benefit and perceived risk. A paper about Islamic finance showed that perceived benefits exhibited a positive and significant impact on trust, while perceived risk had a negative and significant effect on trust for FinTech adoption [

24].

A particularly important aspect in the concept of FinTech is that of government support. The relationship between FinTech and government support is dynamic and evolving, with governments around the world increasingly recognizing the importance of fostering FinTech innovation, especially the e-government part [

25]. In the study by von Hippel and Jin [

26], the authors underlined that FinTech sectors are anticipated to increasingly replace traditional producer-led product and service design across various domains; they take the Chinese state as the case study. This transformation necessitates adjustments in government innovation policies, particularly in areas such as intellectual property rights (IPRs) [

25]. As the global FinTech industry expands, regulatory challenges remain a focal point. Regulatory sandboxes have emerged as a solution to overcome these hurdles, fostering the development of a FinTech ecosystem. In a recent survey, the researchers claimed that there was a highly positive influence of regulatory sandbox adoption on the growth of FinTech venture investments [

27].

The evolving landscape of FinTech presents both opportunities and challenges for financial development, stability, and economic growth. As the sector continues to advance, governments must address internal hurdles such as outdated information systems, inefficient processes, inconsistent data, and the limited institutional capacity to fully embrace FinTech [

28]. Additionally, operational risks, especially in the realm of cybersecurity, and the challenges associated with digital currencies must be carefully managed [

28,

29]. The rise of crypto assets further introduces considerations related to public finances and data privacy. The establishment of a robust digital ID system is crucial to facilitate the widespread adoption of FinTech applications in Personal Financial Management (PFM). In navigating these complexities, regulatory frameworks and timely responses from authorities and policymakers are essential to ensure the successful integration of FinTech innovations [

28,

29].

2.2. FinTech in Europe and Greece

Lavrinenko et al. [

30] explore the impact of financial technology (FinTech) on the financial development of European Union (EU) countries. The study focuses on the Global FinTech Index and the Financial Development Index, along with sub-indices, to assess financial development in EU countries. The findings reveal a positive linear relationship between the Global FinTech Index and the Financial Markets Index, including its sub-indices like financial market depth and efficiency. Specifically, in this analysis Greece belonged to countries that were characterized as new economies that had Financial Development Index values below the EU average value. While Europe leads in the development of financial institutions and markets, it falls behind in the field of financial technology (FinTech) when compared to other regions [

30,

31,

32]. This is primarily due to the banking industry’s dominant position in Europe’s economy, which discourages the high-risk investments required for the FinTech sector. Furthermore, the diversity of regulatory frameworks between European countries, as well as some countries’ predilection for cash payment, has a detrimental impact on the expansion of FinTech in Europe [

33,

34,

35].

Moreover, the paper of Albani et al. [

36], as well as reports from Greek financial bank systems [

31,

37], mentions the impact of digitalization on the Greek financial system, with a specific focus on FinTech as a driver of financial sector development. Greece, by following the example of European banking systems, has started to adapt a model based on FinTech technologies and services in the banking sector [

32,

37,

38]. In the case of Balkan countries, there is evidence that the infiltration of some FinTech activities will remain low in the medium term, although there are opportunities to better serve this market in the savings sector through online services [

33]. A systematic literature review of Panos and Wilson [

34] indicates that in Europe FinTech is rapidly transforming the financial services industry, sparking debates on its potential effects on personal financial planning, well-being, and societal welfare. In an environment marked by increasing student debt, growing digital financial inclusion, and rising threats of online financial fraud, the article advocates policy interventions that prioritize financial education and informed financial advice to enhance overall well-being. Based on the external factors, like the economic crisis targeting Generation Z, particularly Greek university students who experienced the unique and impactful financial crisis, the research explores the interplay between financial literacy, financial fragility, and financial well-being. The findings reveal that factors such as gender, keeping expense records, and a father’s high education level contribute to higher financial literacy among students. Additionally, financially literate students demonstrate better resilience against unexpected financial shocks, positioning financial literacy as a crucial factor in the enhancement of the financial well-being of Greek university students. The study concludes with discussions on potential policy recommendations, considering related behavioral aspects and technological advancements [

39].

Although Europe is behind in the field of FinTech, it has the necessary infrastructure and a profitable environment for the development of its services. With the highest internet access and full electrification coverage worldwide, Europe has solid foundations and leads in the Global Innovation Index in European countries such as England, the Netherlands, Switzerland, and the Nordic countries [

32,

38]. Europe also manages to outperform other markets in some areas, especially with regard to digital payments, including online and mobile transactions, due to the widespread use of the internet [

32,

38].

Research has focused on how FinTech challenges traditional banking and attempts to capitalize on evolving consumer patterns in the Greek market [

40,

41]. Basdekis, Christopoulos, Katsampoxakis, and Lyras [

40] collected data from two distinct samples: consumers of financial products and services in the Greek banking sector and employees within the Greek banking sector; they show that customers of all ages tend to trust traditional banks more than FinTech companies and that the level of mobile transactions among consumers varies based on age and education. The current external environmental situations played a vital role in the adaptation of FinTech services, as stated in the survey. The results revealed that participants believe that recent capital controls imposed by banks have diminished customer trust, while the country’s current economic situation favors the FinTech movement. However, challenges such as the Greek regulatory and taxation system, which is perceived as unsupportive of businesses, and the level of technological familiarity among Greek people pose obstacles to the widespread adoption of FinTech in the region [

37].

2.3. Technology Acceptance Models and FinTech Adoption

Many surveys that are based on the FinTech sector use the Technology Acceptance Model (TAM), a widely used theoretical framework in the field of information systems and technology to understand and predict how users accept and adopt new technologies [

12,

42]. There are many studies that focus on classifying sub-constructs in three dimensions: adoption, behavior, and technology, in order to explore the relationship between these attributes and the implications of FinTech technology [

12,

42]. Its widespread use in studies derives from the fact that it focuses on key elements that effectively predict user acceptance of technology. The model’s adaptability and flexibility allow extensions with additional variables, catering for specific technological nuances, thereby making it highly applicable across various contexts that attempt to understand technology adoption dynamics, including the emerging field of FinTech services.

In our study, we primarily employ the Technology Acceptance Model (TAM) as the foundation to better understand the factors that influence FinTech services adoption. Based on TAM, we further expand our conceptual framework by introducing elements of the Unified Theory of Acceptance and Use of Technology (UTAUT) and its extended version, UTAUT2. This research methodology and approach allows us to explore a broader range of variables that influence and impact FinTech services adoption. In particular, together with the core constructs of TAM, we included additional dimensions and aspects of UTAUT, such as performance expectancy (PE), behavioral intention (BI), and effort expectancy (EE), and the externals factors of trust and government support, as derived from the current literature. This comprehensive conceptual research model facilitates a deeper understanding of the complexity and multifaceted phenomenon of FinTech services adoption and engagement, which has been employed in specific contexts, such as Ghana’s ports, with the findings contributing valuable insights into FinTech adoption in the port industry in sub-Saharan Africa [

7,

10,

12,

43]. Furthermore, alongside [

44], our study utilizes UTAUT’s constructs and acknowledges the significance of integrated financial consumption attributes, highlighting their strong relationships with the intentions of individuals to adopt FinTech and its services. Also, several studies are using the Technology Acceptance Model (TAM) in order to guide a better understanding of the decision factors which act as enablers for the adoption of internet banking [

26,

45,

46].

There is also an empirical study that focused on commercial banks in Saudi Arabia and FinTech services. It used a questionnaire encompassing three key dimensions—financial inclusion (FI), alternative payment methods (APMs), and automation (Auto) [

13]. Multivariate regression analysis was employed to assess the impact of FinTech dimensions as independent variables on Jordanian commercial banks’ financial performance indicators, including total deposits, total loans, and net profit margin [

13]. Another study research attempt implemented structural equation modeling to understand the behavioral intentions toward using financial technology among millennials in Malaysia; it was based on four exogenous constructs, including performance expectancy, effort expectancy, social influence, and facilitating conditions [

21]. They conclude that all exogenous constructs demonstrate statistically significant

p-values, with the exception of effort expectancy [

21]. The use of equation modeling was used in the study of Khan et al. [

47] to underline the antecedents/determinants of behavioral intentions toward the utilization of Islamic financial technology for Middle Eastern customers.

3. Research Methodology

3.1. Methodology and Measurements

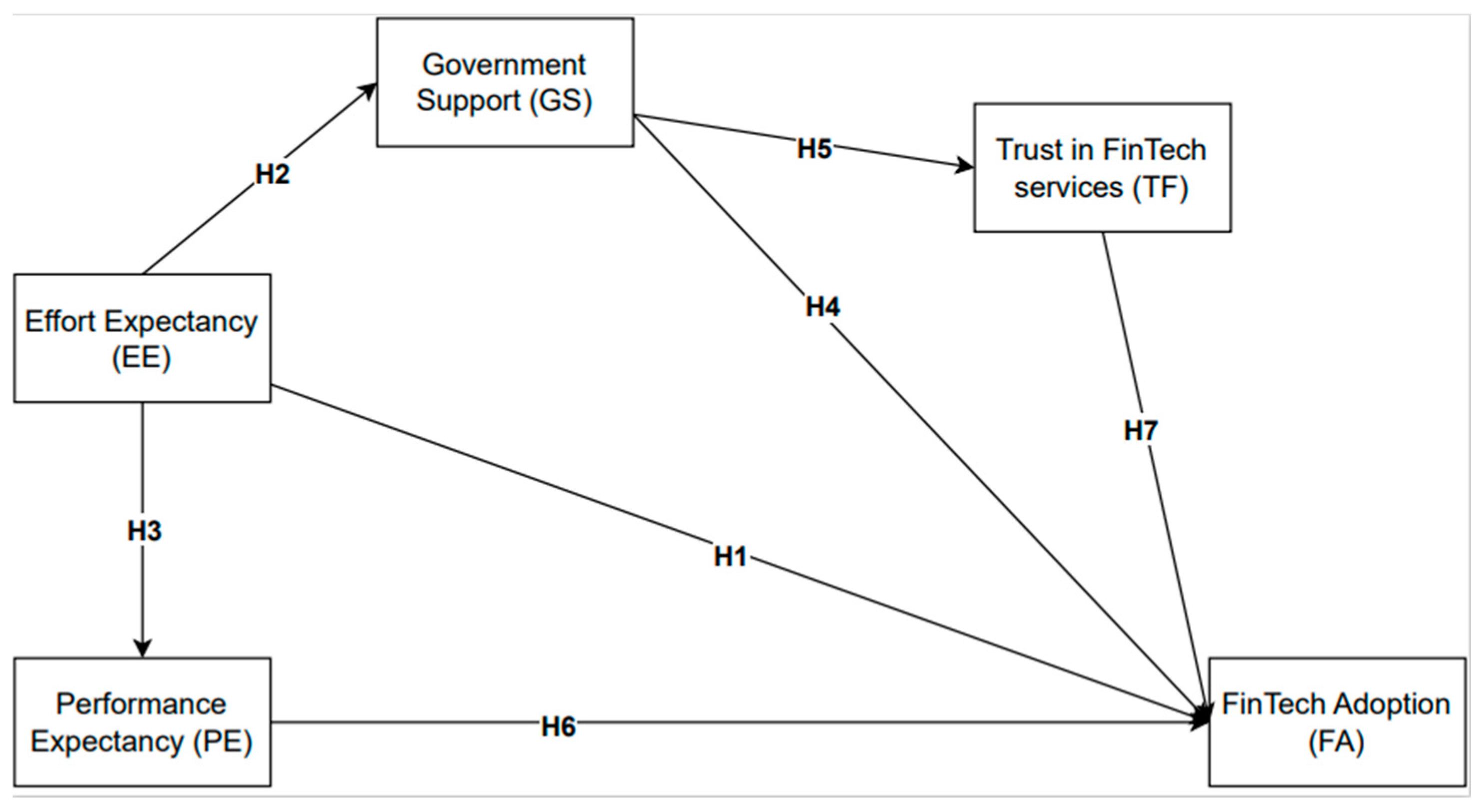

This study introduces a detailed research model that encapsulates the intricate and multifaceted nature of the citizens’ adoption of FinTech services. This model encompasses various elements, such as trust in FinTech services, governmental support, and the users’ perceptions of these services (including performance expectancy and effort expectancy), culminating in the primary focus on the behavioral intentions toward utilizing FinTech services in the future. This model is an all-encompassing approach to the subject; it considers the similarities in terminology used across different research fields, like information systems, public administration, and e-business, as well as the overlapping areas in their application. Understanding human behavior in relation to the adoption and usage of modern technologies or services is complex. This study addresses this complexity by pinpointing crucial influencing factors, exploring their interconnections, and analyzing how these relationships shape the final outcome. The constructs within this model have been tailored specifically for FinTech services, with the anticipation that the model’s validity remains intact regardless of its original context, which could be an e-commerce, generic information systems, or e-government scenario. This assertion is backed by the findings presented in the Data Analysis section. A visual representation of this research model is provided in

Figure 1.

In this study, a quantitative non-experimental correlational methodology was utilized to empirically validate the proposed theoretical framework and offer statistical evidence with the potential for broad generalizability in future studies [

44]. This approach aimed to comprehend the determinants that influence users’ intentions to participate in FinTech services. To gather data, the researchers implemented a structured online survey, which was self-administered, targeting both current and prospective users of FinTech services.

The data were collected through an online survey in Greece, employing a strategic distribution approach that encompassed both universities and the general population. It was designed to capture a diverse range of perspectives, and it aimed to reflect a broad spectrum of the Greek populace and to provide an insight into the FinTech adoption trends that we were able to reach through our survey channels. The questionnaire consisted of 21 items (

Appendix A) and was published on social media platforms to ensure the participation of citizens with diverse backgrounds and to achieve greater diversity within our sample.

Participation in the research endeavor was entirely voluntary. The participants were urged to complete the questionnaire based on their personal perspectives and thoughts on FinTech acceptance, future adoption, and the usage of FinTech services. The participants were informed that the term “FinTech services” in the survey described a broad spectrum of online financial services. These services include digital banking, investing, and economic management tools that are available via various internet platforms and applications. To further extend this, we provided examples that consisted of several different services, such as online banking, digital payment systems, investment platforms, and financial planning tools provided by various financial institutions and FinTech businesses that the users were familiar with. To maximize participation, we utilized several distribution and sample-gathering techniques, such as snowball sampling [

48], encouraging the participants after the completion of the questionnaire to suggest and provide the instrument to people in their close environment (friends, relatives, etc.). Furthermore, to motivate and increase participation when completing the questionnaire, we included the option to enter a EUR 100 gift voucher draw.

Each of the variables in this study focuses on a distinct aspect of behavioral adoption, user acceptance, and trust in FinTech services. The majority of the measuring items were adapted from previous studies, with some being offered for the first time in this study. This study’s instrument was divided into two primary sections: demographics and scale measurements. The demographic section was designed to gather basic information on the characteristics of the sample, such as age, gender, education, and income. These data will be implemented as moderating variables in a future study to assist with data segmentation when considering different target groups.

Performance expectancy (six-item scale) and effort expectancy (four-item scale) were adapted from the TAM theoretical model [

12,

18], while trust in FinTech services was measured with a six-item scale and was adapted from [

49,

50]. The scale includes statements that study the citizens’ perceptions of trust in FinTech services and how they affect future use. The government support construct consists of a three-item scale adapted from Setiawan, Nugraha, Irawan, Nathan, and Zoltan [

23]; the scale measures the influence of government support on the usage of FinTech services. The scale includes the following statements: “The government support and improve the use of FinTech services”, “The government has introduced favorable legislation and regulations for FinTech services”, and “The government is active in setting up all kinds of infrastructure such as telecom network which has a positive role in promoting FinTech services”. Finally, the FinTech adoption construct includes a five-item scale adapted from [

18]. It includes statements that study the intention of citizens to seek useful information through FinTech services, questions consisting of general content regarding their daily service usage by citizens, and their future intentions to adopt and use FinTech services. Thus, based on the existing literature and having extensively studied the factors that influence the adoption and future use of FinTech services, we formed hypotheses to understand the relationships between these factors.

Our hypotheses are derived from the principles of the Technology Acceptance Model (TAM) and the Unified Theory of Acceptance and Use of Technology (UTAUT), which are pivotal frameworks in comprehending technology adoption and user acceptance. In particular, H1, H3, and H6 reflect the core constructs of TAM and UTAUT, where the effort expectancy (EE) and performance expectancy (PE) of FinTech services directly influence their adoption (FA) as critical determinants of technology acceptance. As other studies have derived conclusions and hypotheses regarding the significant roles of government support (GS) and trust in FinTech services (TF), we sought to investigate how external factors like regulatory policies influence user acceptance, whilst with H7 we focused on the relationship between trust in FinTech services (TF) and FinTech services adoption (FA), reinforcing the idea that trust is a fundamental variable in the user adoption decision-making process. The hypotheses evaluated and analyzed in our structural equation model are listed below.

H1. There is a positive relationship between effort expectancy (EE) and FinTech adoption (FA).

H2. There is positive relationship between effort expectancy (EE) and government support (GS).

H3. There is a direct and positive relationship between effort expectancy (EE) and performance expectancy (PE).

H4. There is a direct and positive relationship between government support (GS) and FinTech adoption (FA).

H5. There is a direct and positive relationship between government support (GS) and trust in FinTech services (TF).

H6. There is a direct and positive relationship between performance expectancy (PE) and FinTech adoption (FA).

H7. There is a direct and positive relationship between trust in FinTech services (TF) and FinTech adoption (FA).

All the items were measured on a five-point Likert scale and adapted and translated accordingly to ensure that the meaning of the questions remained intact for statistical validity in our analysis. As the instrument was distributed to Greek citizens, a bilingual academic expert was tasked with appropriately translating the questions. A preliminary analysis was performed to test for unclear context due to the wording of questions, and they were revised accordingly. The pre-test data were excluded from the total dataset.

3.2. Sample Profile

A total of 348 responses were acquired during the data collection process. Gender distribution was evenly split, with 51.4% identifying as male and 48.6% as female. The age range of the participants varied, with 31.3% falling in the “18–25” category, 24.7% in the “26–30” range, and the rest distributed across older age groups. In terms of education, the participants exhibited diverse backgrounds, including 6.0% high school graduates, 32.2% undergraduate students, 27.3% graduates, 17.8% postgraduates, 12.1% postgraduate students, 3.4% PhD candidates, and 1.1% doctoral degree holders. The demographic statistics of the sample are summarized in

Table 1.

4. Data Analysis and Results

This study utilized Smart-PLS4 software (version 4.0.9.9) for data analysis, employing structural equation modeling as the primary technique. This approach is widely adopted in management and social sciences due to its effectiveness as a variance-based structural equation modeling method, as highlighted by Nitzl et al. [

51]. Furthermore, partial least square structural equation modeling (PLS-SEM) is employed for its capability in causal modeling, focusing on maximizing the explained variance of latent dependent constructs. To ensure accurate computation of beta, reliability, and standard error, this research adhered to Wong’s [

52] recommendations. This included confirmation that all the indicators were appropriately aligned with their corresponding latent variables and exhibited outer loadings of at least 0.7 in the assessment of the reflective outer model.

4.1. Measurement Model

The initial stage of PLS-SEM analysis involves the assessment of the measurement model. This research model included constructs measured reflectively, along with composite reliability, indicator reliability, convergent validity, and discriminant validity, as mentioned by Hair et al. [

53]. The first step in defining the measurement model is to assess indicator reliability, which determines how much of an indicator’s variance is explained by its associated construct, as explained by Chin [

54]. These values are represented by outer loadings, as indicated by Wong [

52], and ideally should not surpass 0.70, according to Chin [

55]. Vinzi et al. [

56] note that while factor loadings above 0.7 are preferred, it is common in social science research to encounter lower outer loadings (less than 0.70).

Instead of immediately discarding indicators, it is important to evaluate the impact of removing an item on aspects like composite reliability, content, and convergent validity. Typically, indicators with outer loadings ranging between 0.40 and 0.70 should only be considered for elimination if their removal leads to an improvement in composite reliability or the average variance extracted (AVE) beyond the suggested threshold, as advised by Hair et al. [

57]. As indicated in

Table 2, as part of the measurement model, two items (FA2, PE3) in total were removed due to low factor loadings (<0.500), as indicated by Gefen and Straub [

58].

Reliability in this study was determined using Cronbach’s alpha, rho_A, and composite reliability measures. Each of these surpassed the minimum accepted threshold of 0.700, as suggested by Wasko and Faraj [

59]. The rho_A value, positioned between Cronbach’s alpha and composite reliability, as per Sarstedt et al. [

60], also exceeded 0.7, thus confirming strong reliability, in line with Henseler et al. [

61]. Additionally, the convergent validity was deemed satisfactory, with AVE values exceeding the 0.500 benchmark for most cases, aligning with the standards set by Fornell and Larcker [

62]. To evaluate discriminant validity, we compared the correlations among the latent variables with the square root of the average variance extracted (AVE), following the method outlined by Fornell and Larcker [

62], and we also employed the heterotrait–monotrait (HTMT) ratio of correlations, as suggested by Henseler, Hubona, and Ray [

61]. The values obtained were under the cautious threshold of 0.85. This indicates that discriminant validity was successfully achieved, as shown in

Table 3 and

Table 4.

4.2. Structural Model

The structural model outlined in the research framework is evaluated using R

2, Q

2, and the significance of path relationships, as detailed by Hair Jr et al. [

63]. The R

2 values, which can vary from 0 to 1, show a range in this study: 0.461 for FinTech adoption, 0.228 for government support, 0.402 for performance expectancy, and 0.102 for trust in FinTech services. These R

2 values confirm that they fall within the expected 0 to 1 range. Similarly, the Q

2 values, which indicate predictive relevance, are 0.244 for FinTech adoption, 0.220 for government support, 0.396 for effort expectancy, and 0.095 for trust in FinTech services, thus affirming the model’s predictive strength. Additionally, the model’s robustness was further validated by testing the hypotheses to ascertain the significance of the interrelationships.

The assessment of path coefficient significance in this study was conducted through the bootstrapping method, following the recommendations of Sarstedt, Ringle, and Hair [

60]. In addition, the study incorporated the specific mediation analysis guidelines proposed by Preacher and Hayes [

64]. Also, in line with the suggestion by Streukens and Leroi-Werelds [

65], the analysis used 10,000 bootstrap samples. The results are shown in

Table 5.

The results revealed that EE has a significant impact on FA (β = 0.105, t = 1.976, p < 0.05). Hence, H1 was supported. The results indicated that EE significantly influenced GS (β = 0.478, t = 11.466, p < 0.001). Therefore, H2 was supported. The analysis showed a significant effect of EE on PE (β = 0.634, t = 19.047, p < 0.001), supporting H3. The relationship between GS and FA was not statistically significant (β = 0.085, t = 1.750, p > 0.05), leading to the rejection of H4. The findings demonstrate that GS significantly affects TF (β = 0.320, t = 6.417, p < 0.001), confirming H5 as supported. Moreover, the data revealed a significant positive relationship between PE and FA (β = 0.398, t = 7.576, p < 0.001), thus H6 was supported. Finally, the results showed that TF has a significant impact on FA (β = 0.265, t = 5.690, p < 0.001). Consequently, H7 was supported.

5. Discussion

Our research delves into the intricate and multifaceted aspects of human behavior, specifically focusing on the elements that impact the perception, utilization, and eventual adoption of FinTech services. This investigation aims to understand these influencing factors in depth, which we introduced and examined in our proposed model; the model not only includes concepts of user acceptance though the TAM model but also the approach, and it investigates the concept of trustworthiness.

The hypothesis testing for H1, H3, H6, and H7 examines whether there is a positive and significant statistical correlation between effort expectancy (EE) with government support (GS) and performance expectancy (PE), performance expectancy (PE), and trust in FinTech services (TF) with FinTech services adoption (FA); in our sample, they are all supported. The statistical significance of H1, H3, and H6, which address the issues of effort expectancy and performance expectancy, indicate the significant role of user acceptance in FinTech adoption. The main attraction of FinTech services is the simplicity and convenience they offer in everyday financial transactions. The need for quick and effortless transactions reflects the need of modern society for effective and efficient services, especially in an environment where time is precious. Users can make payments, transfer money, check their accounts, and perform other financial functions easily and quickly via their mobile devices or computers. The ability to conduct transactions in short time intervals contributes significantly to saving users’ time by avoiding the lengthy processes of traditional banking, and it responds directly to financial needs, such as the quick transferal of money in critical situations or the paying of bills instantly. Combined with the fact that they can be used at any time and place, users are no longer limited to banking hours or the need to visit a physical branch. They can conduct transactions at any time and from anywhere, as long as they have access to the internet. Furthermore, in terms of the features that motivate users to use such applications, FinTech applications often feature user-friendly interfaces that make navigating, executing transactions, and managing personal finances easier than ever before. In turn, FinTech services can offer customized functionalities according to the needs and preferences of each user, providing a more personal and personalized experience and making the use of such systems easy and accessible. Another element we incorporated in our study is that of trust in FinTech services (TF), which had positive significant impact on FinTech services adoption (FA) in H7. As FinTech platforms offer advanced solutions to financial transactions, the transparency and control they provide enhance the sense of security and trust on the part of users. The ability to have instant access to detailed financial reports and to monitor their account movements in near real time increases their awareness and understanding of their financial transactions. This awareness contributes to better management of their personal finances and empowers them to make more targeted and informed decisions. Therefore, the confidence that comes from using these management tools and the transparency provided is a fundamental factor that drives users to choose and use FinTech services, as they feel more secure and in control of their financial choices.

With hypotheses H2, H4, and H5, our research design places particular emphasis on the element of government support (GS) and its influence on users’ behavioral and attitudinal changes with regard to adopting FinTech services (FA) and other aspects of user acceptance factors. Our findings reveal a direct positive relationship between EE and GS, suggesting that the perception of government support of these technologies leads users to expect less effort when integrating and using them. At the same time, a direct significant positive relationship was found between GS and trust in FinTech services (TF), reinforcing the view that government support can strengthen consumer trust in potential future usage. However, the hypothesis linking government support directly to the adoption of FinTech services was not supported in our study. This finding is intriguing as it suggests that while government support may enhance trust and reduce the perceived effort, these factors alone may not be sufficient to drive the actual adoption of FinTech services. This could imply that other elements, perhaps user-specific factors, or broader economic and technological conditions, play a more decisive role in the final decision to adopt FinTech services.

Thus, we explored further to uncover the potential influences that could have affected this result. Mediation analysis revealed that trust in FinTech services (TF) mediates the relationship between government support (GS) and FinTech services adoption (FA), which adds an important dimension to the understanding of this dynamic. This finding suggests that while direct government support may not be a standalone factor in driving the adoption of FinTech services, it plays a crucial role in building trust among potential users, which in turn influences their decision to adopt these services. Our study indicates that government support contributes to the creation of a favorable environment for FinTech services by enhancing trust. Users who perceive that these services are endorsed or regulated by the government are more likely to trust them. This trust, once established, becomes a key mediator that positively influences their willingness to adopt FinTech solutions. It highlights the indirect but vital role that government support plays in influencing the public perception and acceptance of new financial technologies.

In summary, our research provides an in-depth analysis of the FinTech services adoption and aligns with and extends the existing literature; it particularly emphasizes the roles of the Technology Acceptance Model (TAM) and the Unified Theory of Acceptance and Use of Technology (UTAUT) as crucial frameworks for understanding user behavior towards financial technologies. This is in line with studies like those in references [

11,

26,

45], and the work of [

66], which also underscore the significance of these models in analyzing FinTech adoption. Moreover, the inclusion of the trust factor and its significance as a mediator in technology acceptance offers a novel perspective on the role of trust in the TAM and UTAUT models [

16,

67,

68,

69], a fact which is particularly relevant in the context of financial technologies and services, where trust plays a more central role as a major determinant in behavioral adoption and user acceptance due to the sensitivity of financial transactions [

66,

67,

70]. Exploring external factors of user behavior and perceptions can add new dimensions to the existing models of TAM or UTAUT. Our study sheds light on the indirect role of government support in FinTech adoption, an aspect that is often overlooked in traditional FinTech adoption models [

13,

26,

27,

66]. A recurring theme in both our research and the broader literature is the importance of trust and government support in influencing FinTech adoption decisions, as seen in studies like those in [

17] and [

27], which highlights the critical role of these factors in the field. Furthermore, our findings on the significance of performance expectancy and effort expectancy as determinants of user acceptance echo those of previous studies [

11,

66,

71], confirming a shared understanding of their impact on the adoption of FinTech services. Our study’s methodological approach, which employs structural equation modeling (SEM), aligns with the trend in FinTech research, as also demonstrated by studies like that in [

66], and reflects the effectiveness of this method in dissecting intricate relationships between diverse variables in the FinTech adoption context.

Understanding the intricacies of the variables that cause behavioral and attitudinal changes can provide an insightful overview of the interrelationships that lead users or citizens to use the technological instruments related to FinTech services. Taking inspiration from the already existing models of user acceptance, we attempted to include additional elements such as those of trust and government support, to enhance our model’s applicability to FinTech, in order to provide an interdisciplinary approach and comprehensive understanding of user acceptance models. This allows researchers to study beyond the direct relationships and focus on the indirect factors like government support and trust, both of which can influence user acceptance. Studying the dynamics of user trust and government support, we can provide suggestions and actionable insights for regulatory frameworks, policies, and governmental bodies to develop user-centric models with trust-enhancing features that foster wider adoption.

6. Conclusions

This study emphasizes the intricate yet complex decision-making process in technology adoption, particularly in dynamic and inventive fields like FinTech. It provides interesting views for academics, policymakers, and FinTech providers and emphasizes the need to involve elements of trust and user acceptance (effort expectancy and performance expectancy) as they reveal a significant and positive relationship with FinTech services adoption; thus, they can be predictive factors of citizens’ future intentions to use FinTech services.

Based on the findings of our research, the practical implications are substantial for both FinTech service providers and policy makers. The positive relationships between effort expectancy, government support, performance expectancy, and trust in FinTech services with FinTech adoption indicates that users prioritize ease of use, efficiency, and trust in choosing financial technologies. For FinTech providers, it is considered particularly important to develop and support user-friendly interfaces that simplify financial transactions and provide personalized experiences. Such dynamic interfaces not only improve the user experience and enhance engagement and satisfaction but also provide advanced features like detailed financial reporting and account monitoring, which can lead users to higher adoption rates. From a policy perspective, governments play an important role in the adoption of such habits by citizens. Governments can alleviate trust issues and foster greater adoption of such technologies simply by taking on their own share of responsibility for their effective development, as well as by enacting favorable legislation. Thus, the issue of trust in FinTech services cannot be overstated. Although in our research the direct relationship between government support and immediate FinTech adoption was not observed, it does not cease to have a significant influence on user trust and perceived effort, which are essential factors in the decision-making process. This fact demonstrates that government entities should concentrate on ordinances that not only promote but also regulate FinTech services in their efforts to boost the public’s trust. For FinTech service providers, they must prioritize the transparency and security of users’ data in order to offer safe, trusted, and transparent services. Demonstrating compliance and cooperation with government standards can be a key marketing strategy, reinforcing trust and reducing perceived user effort. The goal is not only to retain existing users but also to attract new ones, giving them confidence in their choice to manage their financial affairs digitally. Combining all the aforementioned approaches with the trust engendered by government support can significantly influence users’ behavioral and attitudinal changes towards adopting FinTech services. In summary, the practical implications of our research indicate a collaborative ecosystem where user acceptance factors, government support, and trust work in tandem to promote FinTech services adoption. This is an important blueprint for both policymakers and FinTech providers to integrate into the everyday financial transactions of financial services and technology.

This research is not without limitations. This study’s findings are centered on Greece and may not be fully generalized to other regions or countries with different cultural and socio-economic values. In addition, our research does not include socio-economic factors such as those of the Legatum Prosperity Index or the World Values Survey, which could potentially influence FinTech adoption. We acknowledge a significant gap in that the demographic composition of the sample greatly influences the outcomes. Our sample consists primarily of younger individuals, who have the tendency to be open to new experiences and are technologically adept and better adjusted to the demands of a digital society, which could potentially affect their propensity to adopt and use FinTech services. Thus, subsequent research might delve into the influences of various moderating factors and control variables, such as age, gender, and prior user experiences. Additionally, integrating variables from well-known models of user acceptance and adoption, like the Technology Acceptance Model (TAM) and the Unified Theory of Acceptance and Use of Technology (UTAUT), might alter the current model and shed new light on this phenomenon. This study primarily concentrates on the importance of user trust and the elements that drive the intention to use FinTech services in the future. Our study treats FinTech adoption as a homogenous concept, not distinguishing between different types of FinTech services. Future research could explore how our findings can be applied to specific FinTech products, offering a more detailed understanding of adoption across various FinTech categories. Finally, it would be interesting to consider in the future a comparative analysis between emerging markets and countries similar to Greece, to offer valuable insights into FinTech applications and strategies in different economic contexts.

It is important to note that the utilization of FinTech goes beyond the traditional confines of financial services. To formulate a successful strategy for digital innovation in the financial arena, both in Greece and internationally, the establishment of a resolute FinTech development and monitoring division is suggested. This division will take on the role of tracking market trends, pinpointing challenges, and deepening collaborations with financial sector experts. Key strategies for the growth of the FinTech industry include devising a digital innovation strategic plan, enhancing both the availability and demand for FinTech services, and encouraging the creation of new applications via digital technology workshops.

{kind=link}