1. Introduction

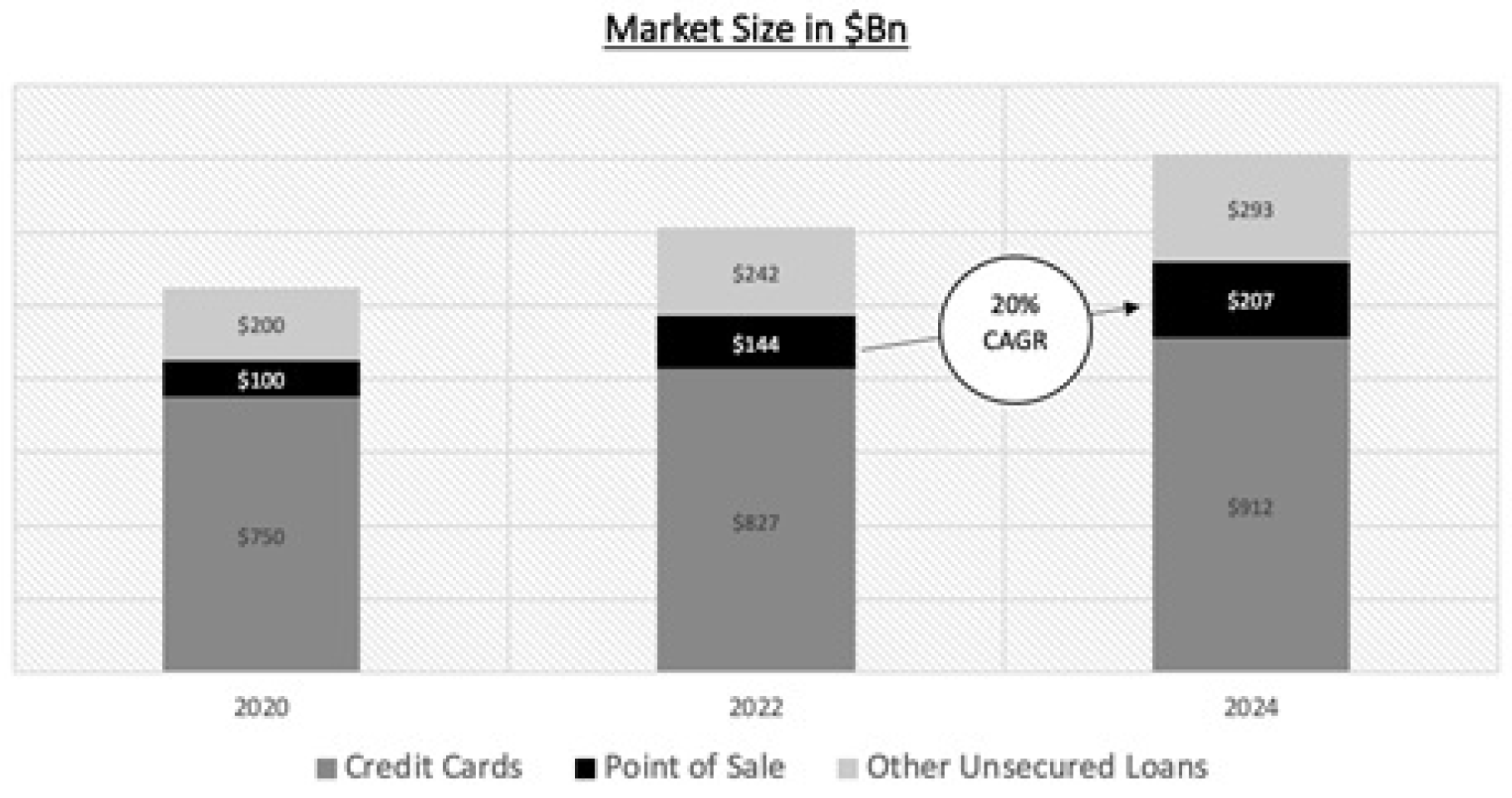

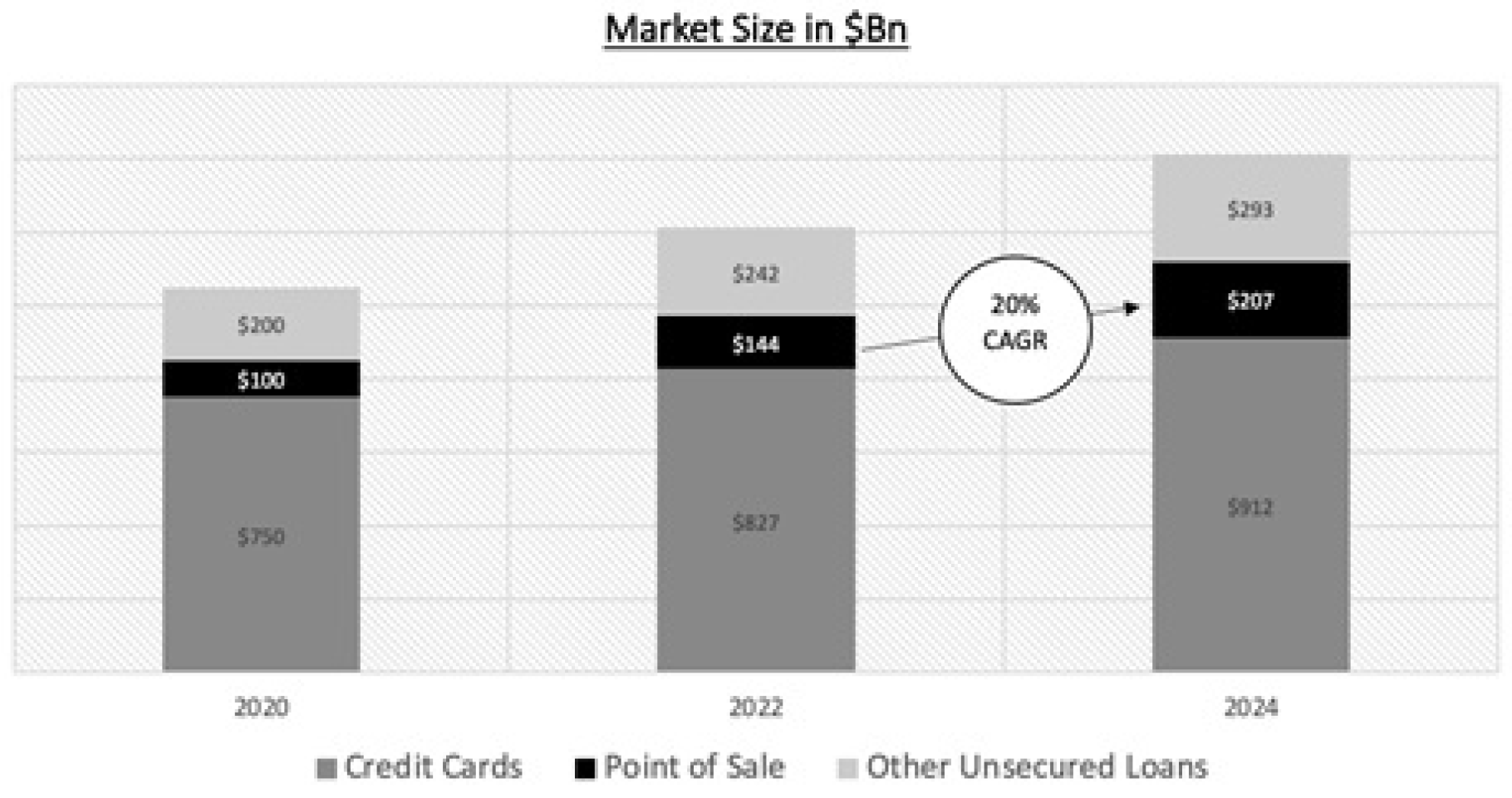

Point-of-sale (POS) financing (otherwise known as BNPL), now accounts for about 10% of the total unsecured lending balances in the United States, according to data from the Federal Reserve. In 2020, credit card balances were at about

$750 billion while POS balances were about

$100 billion. However, POS financing is growing faster than any other type of unsecured lending, and is projected to grow at a compound annual growth rate (CAGR) of 20% for the next 5 years. Growth is observed in the smaller ticket purchases, led by consumer electronics (

$600 spend on average), beauty products and apparel (

$200 on average), and household goods (

$1000 on average). Several merchants offer these Buy-Now-Pay-Later (BNPL) solutions on big ticket home improvement projects as well, which are typically in the

$10,000–

$50,000 range (see

Figure 1).

The POS market is largely covered by FinTechs all over the world. Lately, many traditional financial institutions are beginning to take notice and desire to enter in this space. While financial institutions are aware of the what-to-do’s, many aspects of the how-to-do’s are not clear. Specifically, the framework behind the different business models for POS lending needs proper articulation. This is important because a lending institution will want to enter the market at a different time, scale and different levels of involvement. In this article, we describe the different models for entry, clarify the relationships between the different parties, and provide an implementation road-map for a lender seeking to enter the POS lending market.

Section 2 talks about the drivers of growth in the POS market, and

Section 3 showcases the current lead FinTechs have in this space. We then clarify the market participants and business mechanics in

Section 4, followed by the detailed analysis on modes of market entry in

Section 5. We make concluding remarks in

Section 6.

2. Drivers of the POS Market

A large part of the growth is driven by consumers opting for POS financing over private label credit cards and personal loans. These early adopters of POS are typically millennial’s, who value the degree of control and transparency these products offer over traditional financing (a trend commonly observed in every financial innovation where FinTechs dominate, [

2]). Consumers also prefer POS lending, as it is affordable, and the no credit score impact is an alternative to credit cards, bypassing credit limits and other fees. Consumers like the fewer fixed payment style loans, and ability to separate debt from other types. Better UI and purchase journey integration has also played a big role in driving this market. Such preferences distinguish consumers (specifically millenials vs GenZ), and FinTechs have been very agile in adapting to these special needs (see [

3,

4]).

Merchants offering POS financing also observe several advantages. They are able to boost sales, upsell and increase repeat purchase rates. Monthly incoming payments also help in smoothing cash flow for the Merchant. This financing option competes with private label credit cards, and while the revenue per customer is low, the number of transactions and the ROA are much higher. Adoption is also increasing, as consumers observe multiple proof points across industries. POS financing is now available in the healthcare, medical, fitness, jewelry, electronics, travel and retail industries. Consumers can begin their purchase journey from the lender’s app or website, as well as at the merchant location. This is clearly observed in the Chinese market, where financial services have been offered via a variety of applications on mobile phones, see [

5]. COVID-19 has accelerated the online penetration of this market in many verticals.

3. Fintech Dominance

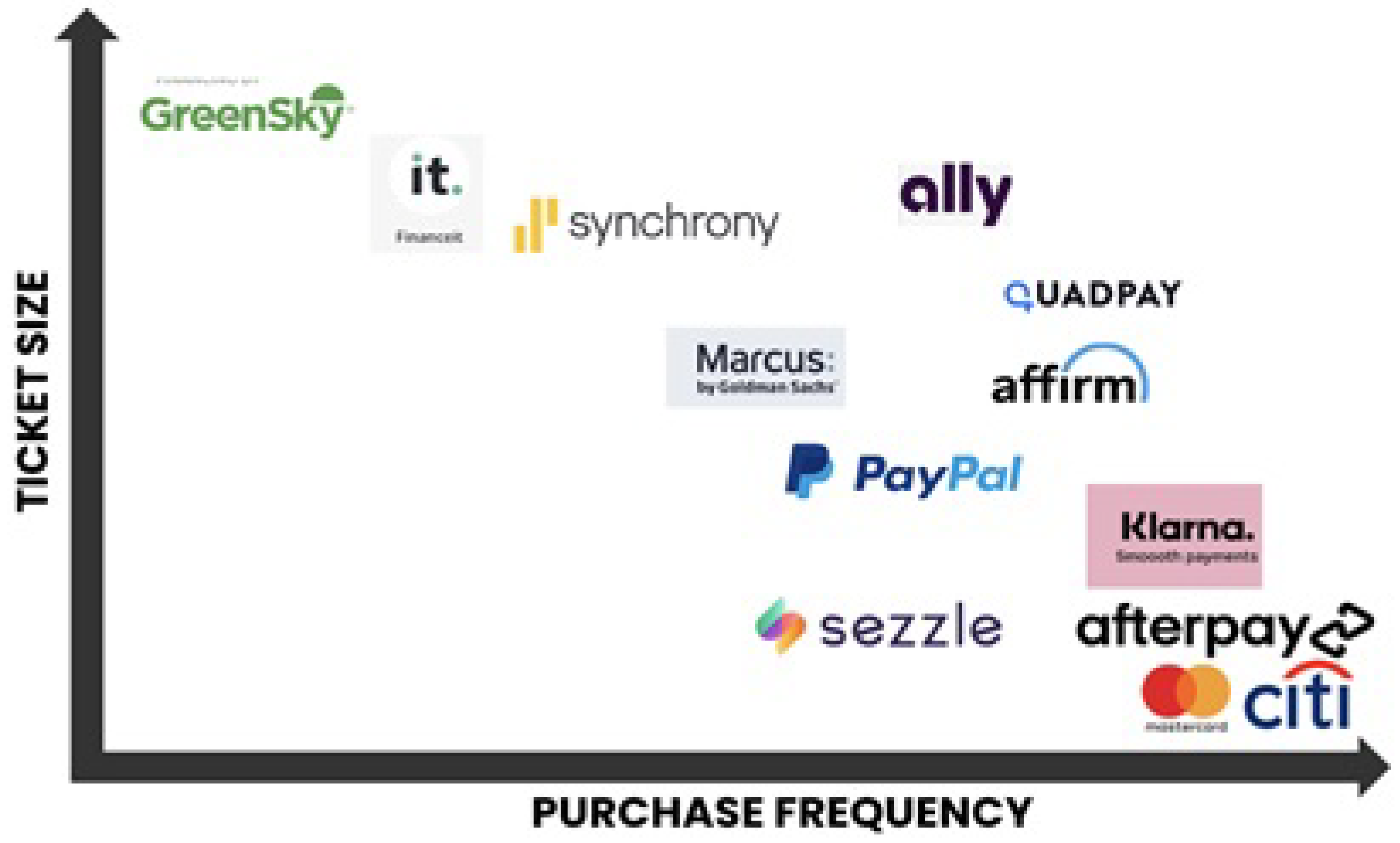

POS financing is making a serious dent in the space traditionally occupied by credit cards and personal loans. FinTechs are leading the charge in this space, following the general trend around the world where FinTechs have been dominating in every financial innovation (see [

2]). This is taking the business away from the traditional financial institutions (see

Figure 2 and

Figure 3).

Few banks are taking the leap into this space, and many will lose out on market share if they fail to participate or underestimate the market. POS financing is used largely by young consumers, those new to credit and the underserved. As premium merchants have already started offering these products, consumers with high credit scores have entered the space (Affirm offers POS loans on Peloton’s products).

Banks are set to lose access to these new and young consumers in the short term, and if they do not enter this space soon they may lose market share in the long term. As you can see in

Figure 3, FinTechs lead the market in both project and retail financing, with few traditional banking participants such as Citi and Goldman Sachs (which owns GreenSky [

6]). Given the demographics of BNPL adopters (younger customers and credit builders), banks could lose customers for life if they do not participate in this vertical. This article outlines several strategies for banks/lenders on how they can enter the POS financing space.

4. Market Participants and Business Mechanics

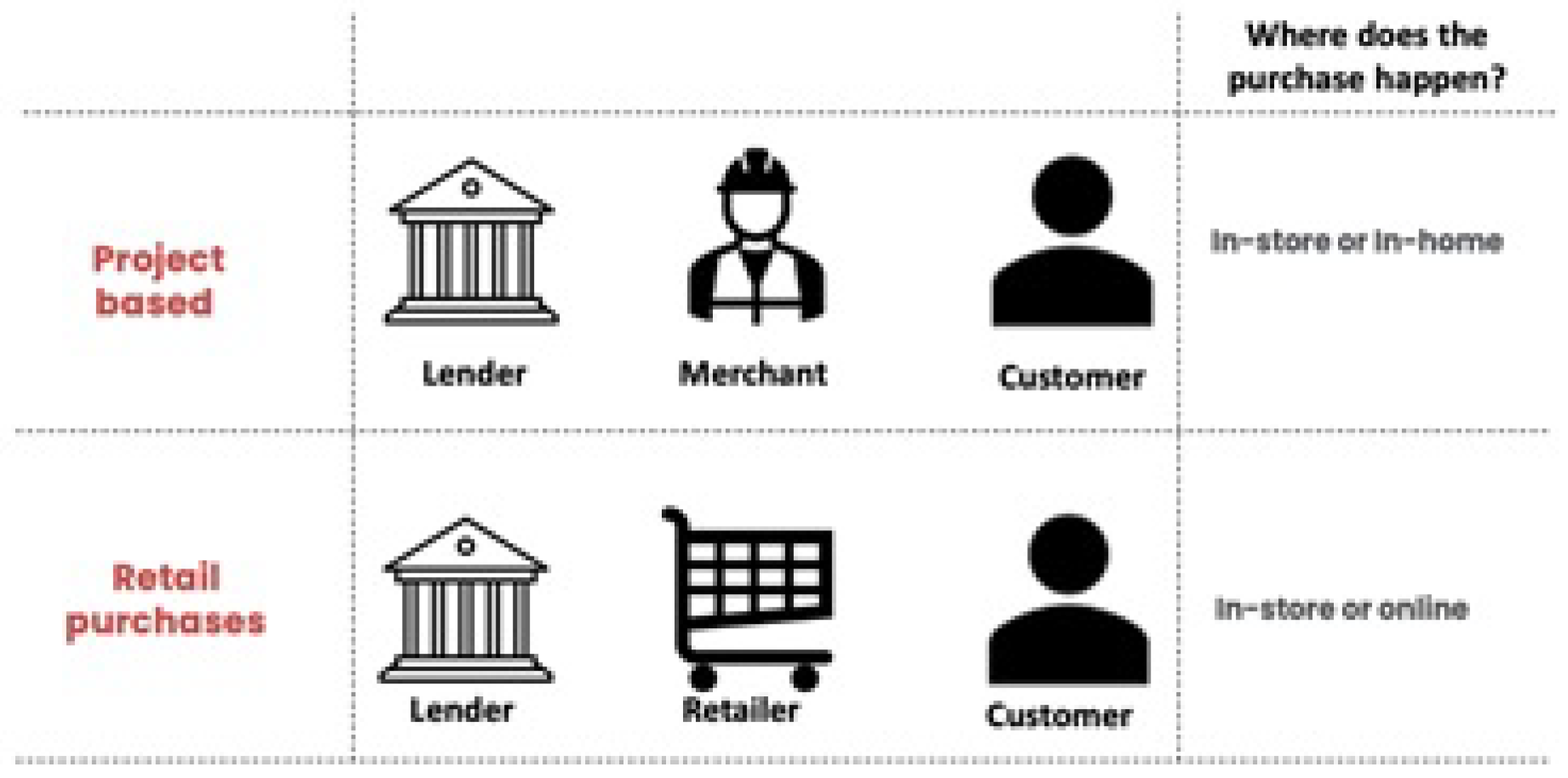

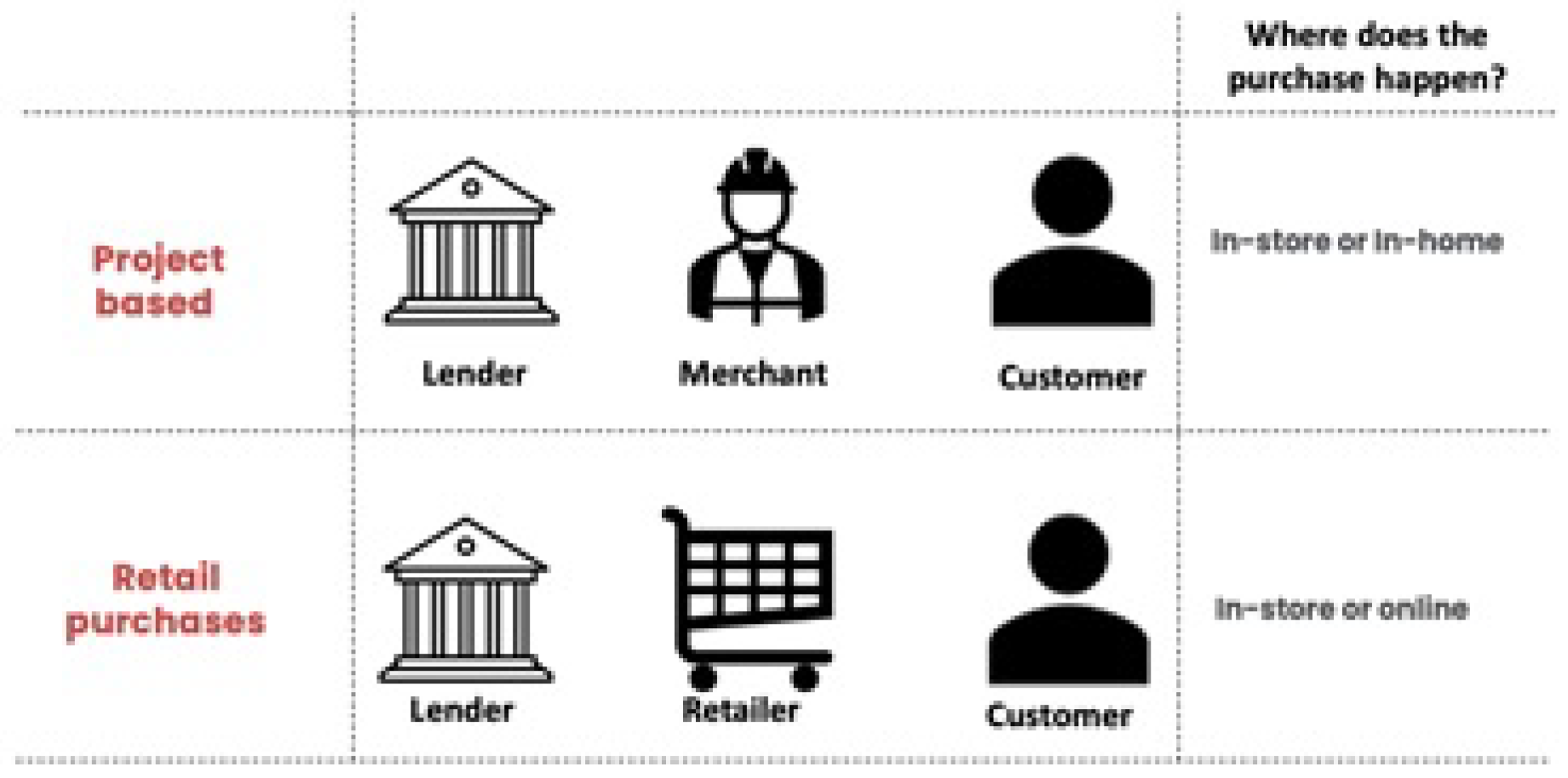

The POS market has multiple categories of loans, and can be broadly divided into two sets—project based and retail based (see

Figure 4). Retail based POS purchases happen in-store or online and typically have a low ticket size (<

$1000), while project based ones are typically in-home or in-store and have larger ticket sizes.

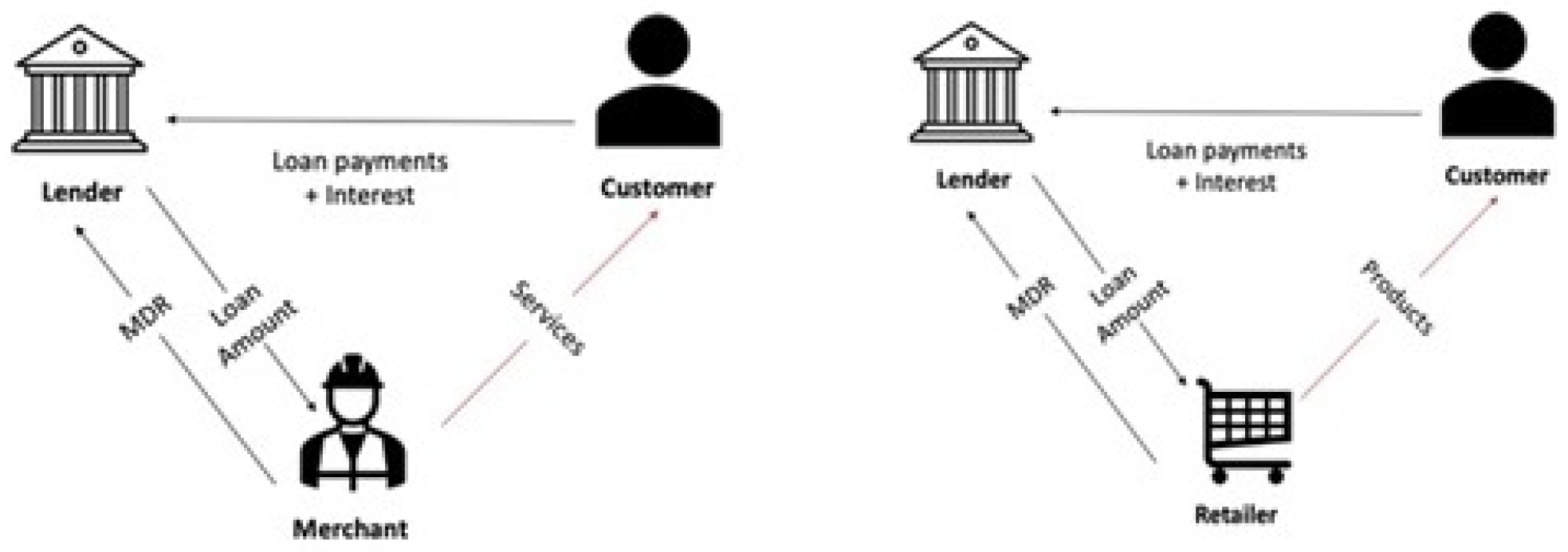

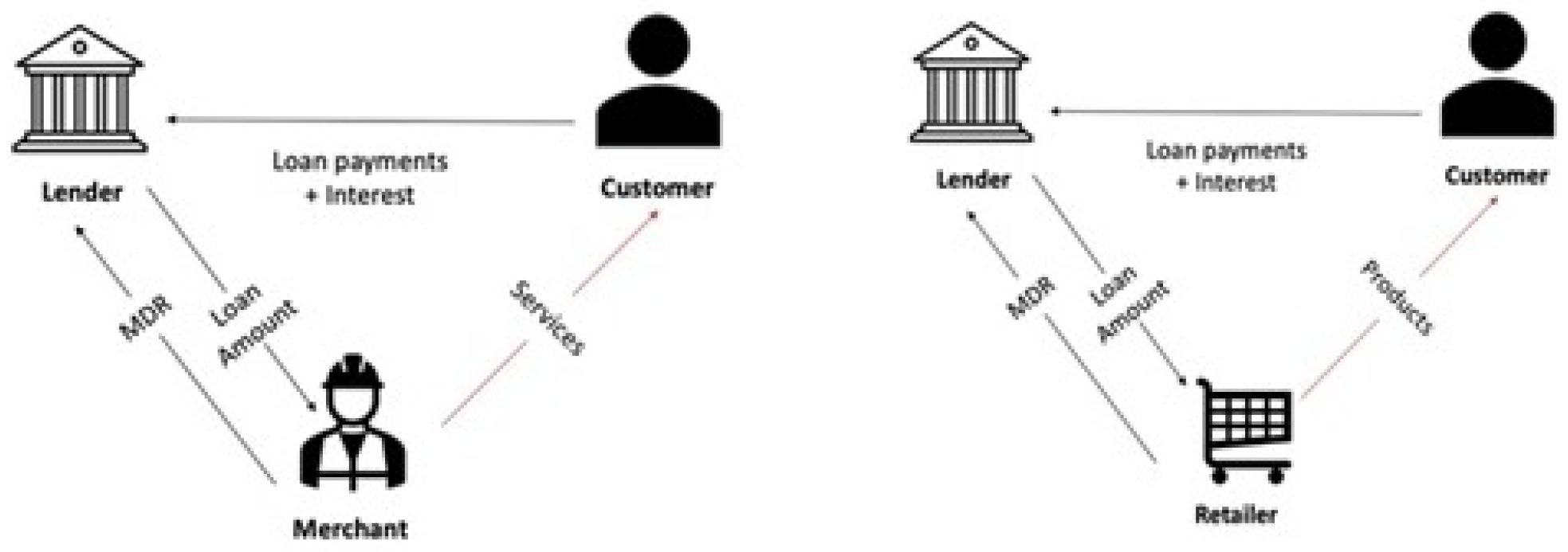

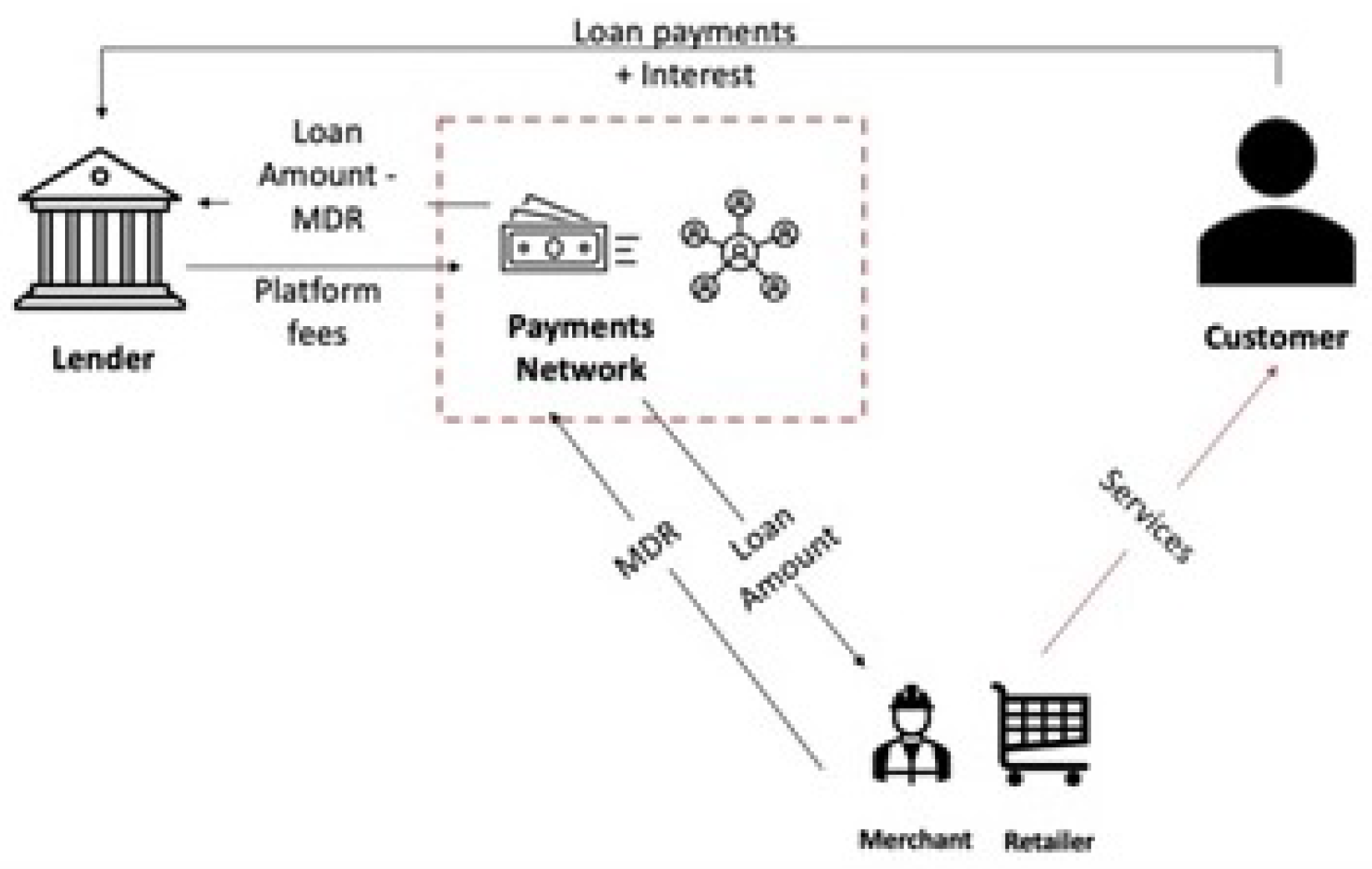

POS transactions involve the consumer, the lender and either the merchant or retailer. The consumer interacts directly with the retailer or merchant, receives a service or a product, and agrees to pay the balance in several installments to the lender (see

Figure 5). The merchant or retailer receives the entire balance minus a “merchant discount rate” (or MDR) from the lender.

The lender earns the MDR and net interest margin (NIM), incurs operating expenses and has to account for default risks. In comparison to a personal loan, the bank earns the NIM (which is typically higher), incurs operating costs and customer acquisition costs, and has to account for default risks (which are typically lower). This may result in a ROA lower or equivalent to a personal loan per customer, but because the life of a POS loan is much smaller, the annualized ROA will be much higher. This is why POS loans are very attractive (see

Table 1). POS is also easy to scale (given access to large pools of customers through the merchant networks/retailers).

5. Market Entry

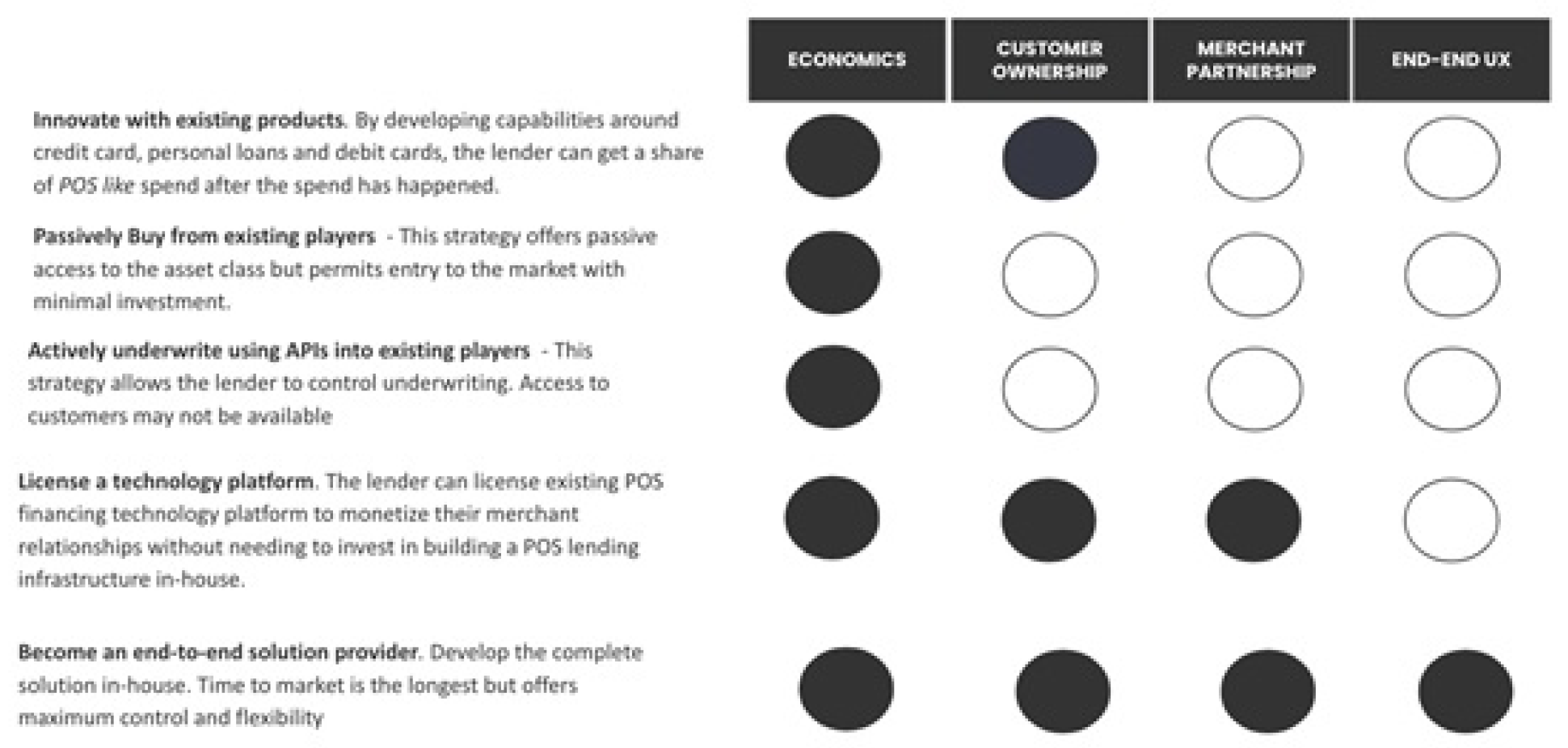

Banks can enter the POS market in several ways, at different levels of involvement [

8]. Starting with offering POS style refinancing to an end-to-end user interface/shopping app, banks can evaluate which mode (or modes) of entry are right for them depending on variables such as cost, capability and time to market (see

Figure 6).

The quickest way to enter the market is to get a share of POS-style spend after a consumer has already made a purchase with a credit card [

9], or has been approved for a personal loan. For example, when a consumer buys a new phone with a credit card, the lender can make a pay-in-installments style offer. This requires low investment in building capability and can be launched quickly. Alternatively, banks can passively access the POS asset class by buying from existing POS loan providers such as Affirm or Greensky. This is a low investment/capability approach with very low time to market entry. While these approaches are quick and require low or no costs, the return on investment is also low (see

Figure 7).

The first two approaches leave the banks with no control over the underwriting of the loans and no access to consumers. Banks can enter the market in other ways, by extending more control over the underwriting and consumer acquisition process. By using APIs into existing players such as Affirm or Greensky, banks can take control over the underwriting of these POS or BNPL loans. This option has a higher cost and a longer capability journey, but banks may not have access to the consumers. Banks will have to build sales capabilities to create partnerships with retailers and merchants. Current players in this market are Affirm, Klarna, AfterPay and Sezzle and the typical retailers or merchants can be firms like H&M and Target. The ticket sizes in this market are under $250, with payment terms lasting upto 6 months. Investment capability requirement is quite low, but the bank will need to spend time on building the bank-end technology. A lender planning to enter the POS space in this way should have a successful track record of building in the FinTech space, or are planning to monetize what they build in the future. This option can also be attractive if the lender has resources to spare, or has partnered with a large retailer/merchant that can drive future growth.

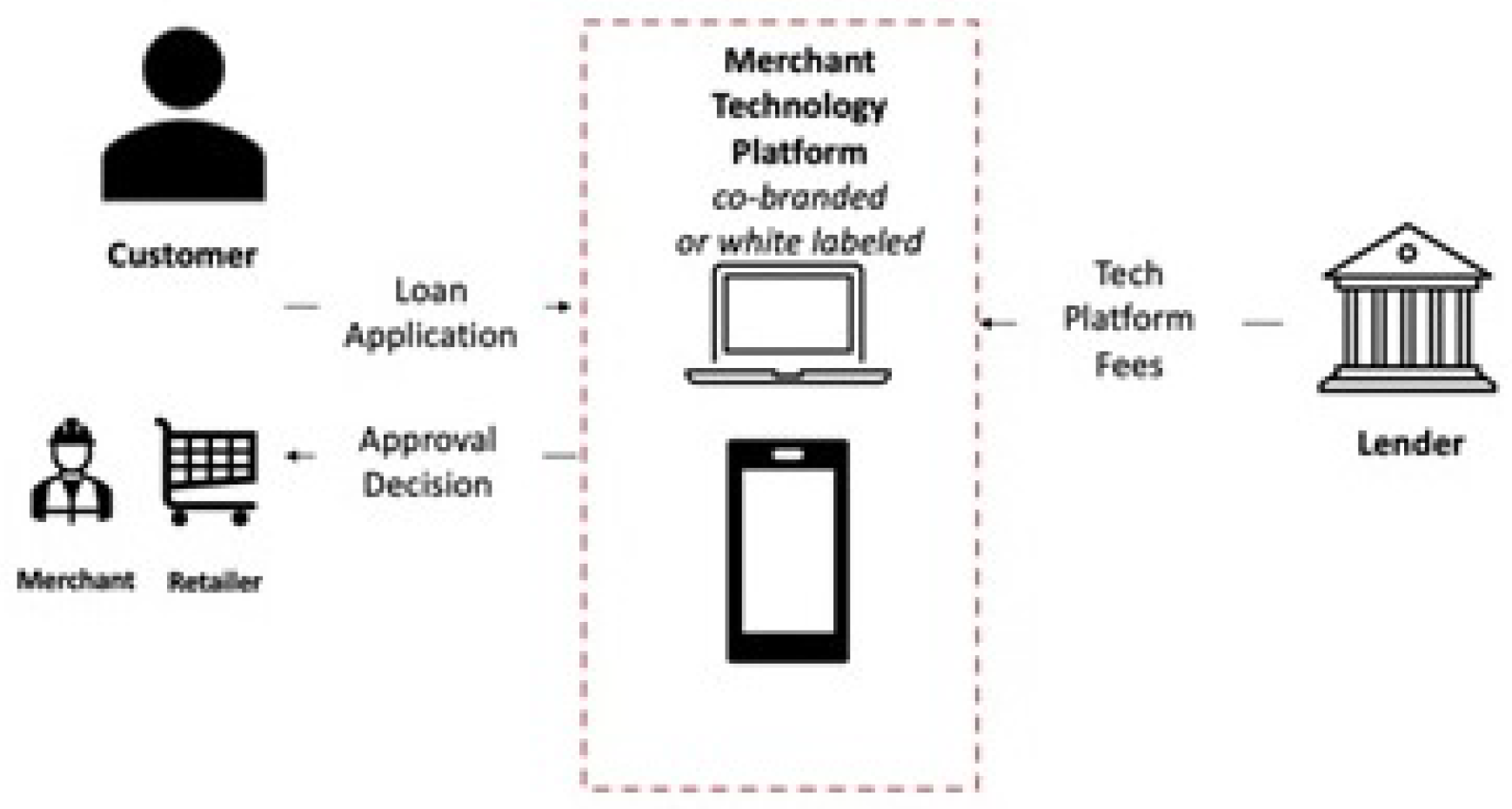

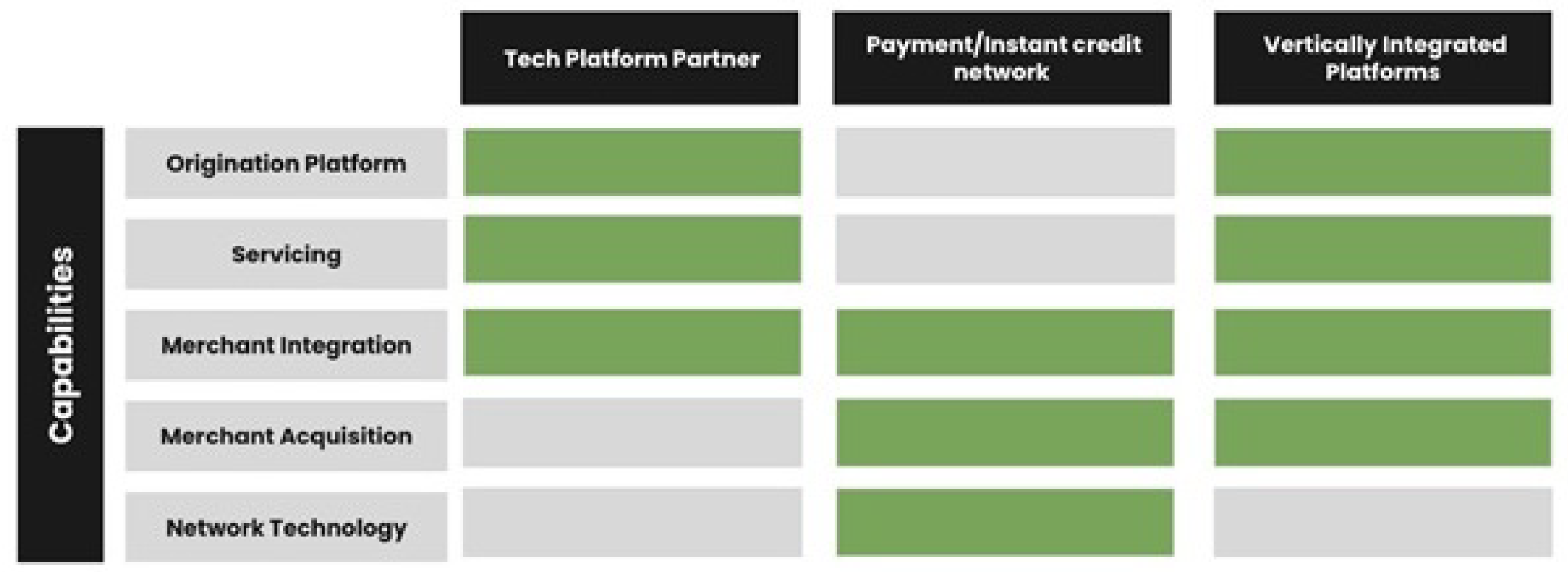

The final two entry options require significant capability building and have a higher time to market, but banks are set to gain consumer ownership and merchant partnerships. Currently banks are significantly behind in engaging with these methods, as evident in several markets in the world (for example, see [

10]). Banks can license an existing POS technology platform instead of building their own POS lending infrastructure in-house (see

Figure 8). While this enables them to quickly monetize their existing relationships with merchants, it increases costs in the form of tech platform fees. However, the bank does not have to build sales capabilities to acquire merchants. It also frees the lender from setting up a merchant operations team to handle complaints, fraud and other issues. Alternatively, lenders can partner with payment networks and marketplaces to quickly get access to multiple merchants and can scale easily (see

Figure 9).

Banks also have the option to become an end-to-end service provider. This has the longest time to market but offers maximum control and flexibility over the entire process. Banks will own the entire value chain from merchant partnerships to technology capability and servicing. While it might be difficult to build ‘super-apps’ that exist in China, lenders can build the technology that helps them connect with the entire purchase journey of a consumer. POS financing is already a big market, and an integrated platform also allows the lender to generate revenue from cross sales.

Current leaders in the market are Afterpay and Klarna. Consumers are beginning their purchase journey through these apps, and often benefit from the BNPL features when it is not offered at the merchant or if the merchant does not have the solution integrated. Integrated apps significantly decrease the cost of customer acquisition, and FinTechs are aggressively promoting other products such as bank accounts, credit cards and pay-in-4 integrated debit cards (Klarna offers traditional bank accounts and Affirm is launching its integrated pay-in-4 debit card).

6. Conclusions and Final Remarks

Despite the recent drop in valuations of big POS players (summer 2022), POS lending is here to stay and will grow rapidly in the next several years. This is because POS lending creates value for the three market participants—the retailer/merchant, the lender and the customer. POS lending is already taken off in many markets in the world, such as Australia, India and Europe [

11]. As lenders and merchants/retailers get more sophisticated and consumer trust in POS increases, the growth in the market should be self-sustaining due to the reinforcement effect on the three participants.

For the merchants/retailers, this leads to an increase in gross merchandise value/sales and increased customer loyalty (sticky behavior). It is therefore crucial for merchants to find the right lending partner that is willing to sign up with competitive Merchant Discount Rates (MDR), and are willing to customize payment programs and user journeys to fit their needs. For lenders, this provides an opportunity to acquire high quality customers with intent as compared to direct-to-consumer marketing. It is therefore important to lenders that they select the right retail partners/merchants, helping them improve brand perception and create awareness that drives growth in other areas. Lenders should also view this as an opportunity to cross-sell other credit and banking products. For customers, POS lending is a no brainer. It provides ease of purchase, and a low cost alternative to credit cards. Automatic payments also help in avoiding negative credit consequences. It is important for customers to not overstretch themselves in order to not fall into the same pitfalls of credit cards. This one aspect of POS lending that governments can regulate.

In this article, we outline existing business models for lenders to enter POS lending. We discuss the benefits and mechanisms of POS lending. What lenders need to assess is how they can impact consumer choice in the lending market in the long run, and whether they are positioned well to adapt to this change. Lenders need to start making investments in this market soon, as it is likely that the market participants will change with time.

Our article is limited by business models and technology that currently exist, and it is likely that there will be advances on both fronts in the near future. Similarly, the market participants can start collaborating differently; depending on future economic conditions, geographic locations and governmental regulations. In particular, government regulations will/can play a major role on how the POS lending industry will evolve. Moreover, our article focuses on the lender, and future work can take the point of view of the merchant/retailer.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}