Adapting Management Control Systems to Organizational Contingency Factors: A Study of Moroccan Industrial Companies

Abstract

1. Introduction

2. Theoretical Background: Management Control Systems—Contingency Factors

2.1. Management Control Concepts

- -

- Forecasting means quantifying the objectives, resources and action plans, and translating them into financial terms.

- -

- Measuring means ensuring that operations are carried out.

- -

- Taking action means identifying, understanding, and analyzing any discrepancies between the targets and forecasts, which may indicate malfunctions. It means anticipating the company’s future in order to take corrective action.

2.1.1. The Dashboard

2.1.2. Reporting

2.1.3. Budgetary Control

2.2. Contingency Theory in Management Control

2.3. Variables of Organizational Contingency Theory

2.3.1. Size

2.3.2. The Environment

2.3.3. Technology

2.3.4. Organizational Structure

3. Methodological Approach to Research

3.1. Finalization of Theoretical Model and Operationalization of Variables

- ➢

- Operationalization of the variables

- ➢

- Operationalization of the “Environment” construct

- Operationalization of the “Technology“ construct

- Operationalization of the “Organizational structure” construct

3.2. Sample and Data Collection

4. Presentation and Discussion of Results

4.1. Exploratory Factor Analysis (EFA)

4.1.1. Results of the Validation Tests of the “Environment“ Measurement Scales

4.1.2. Results of the Validation Tests of the “Technology” Measurement Scales

4.1.3. Results of the Validation Tests of the “Organizational Structure” Measurement Scales

4.2. Correlation and Regression Analysis

4.2.1. Correlation Analysis

4.2.2. Regression Analysis

4.3. Discussion of Results

4.3.1. Size

4.3.2. Environment

4.3.3. Technology

4.3.4. Organizational Structure

5. Conclusions

5.1. Theoretical Implications

5.2. Practical Implications

5.3. Research Limitations

5.4. Research Prospects

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Jukka, T. Does business strategy and management control system fit determine performance? Int. J. Prod. Perform. Manag. 2023, 72, 659–678. [Google Scholar]

- Chenhall, R.H.; Moers, F. The role of innovation in the evolution of management accounting and its integration into management control. Account. Organ. Soc. 2015, 47, 1–13. [Google Scholar] [CrossRef]

- Gerdin, J. Management control as a system: Integrating and extending theorizing on MC complementarity and institutional logics. Manag. Account. Res. 2020, 49, 100716. [Google Scholar] [CrossRef]

- Bedford, D.S. Conceptual and empirical issues in understanding management control combinations. Account. Organ. Soc. 2020, 86, 101187. [Google Scholar] [CrossRef]

- Barros, R.S.; Ferreira, A.M.D.S.D.C. Management control systems and Innovation: A levers of control analysis in an innovative company. J. Account. Organ. Chang. 2022, 18, 571–591. [Google Scholar] [CrossRef]

- Lewinson Skörd, J.; Racov, T. Management Control Systems, Performance and Uncertainty: A Quantitative Study on the Role of MCS in Uncertain Contexts. Master’s Thesis, JÖNKÖPING University, Jönköping, Sweden, 2023. [Google Scholar]

- Anthony, R.N. Planning and Control Systems: A Framework for Analysis; Harvard Business School: Boston, MA, USA, 1965; pp. 80–160. [Google Scholar]

- Selmer, C. Concevoir le Tableau de Bord: Outil de Contrôle, de Pilotage et d’Aide à la Décision. Ph.D. Dissertation, Université Mouloud Mammeri, Paris, France, 1998. [Google Scholar]

- Ragaign, C. Dashboard and Performance Management; Business Insights Press: Armonk, NY, USA, 2023. [Google Scholar]

- Butler, J.B.; Henderson, S.C.; Raiborn, C. Sustainability and the balanced scorecard: Integrating green measures into business reporting. Manag. Account. Q. 2011, 12, 1. [Google Scholar]

- Merchant, K.A.; Van der Stede, W.A. Management Control Systems-Performance Measurement, Evaluation and Incentives, 4th ed.; Pearson: London, UK, 2017. [Google Scholar]

- Charles, A. The impact of technological innovation on organizational performance. Ind. Eng. Lett. 2014, 4, 24–36. [Google Scholar]

- Hayes, J. The Impact of Technology on Modern Society. Technol. Rev. 75 2020, 3, 45–58. [Google Scholar]

- Otley, D. The contingency theory of management accounting and control: 1980–2014. Manag. Account. Res. 2016, 31, 45–62. [Google Scholar] [CrossRef]

- Fisher, J.G. Contingency theory, management control systems and firm outcomes: Past results and future directions. Behav. Res. Account. 1998, 10, 47. [Google Scholar]

- Kihara, P.; Bwisa, H.; Kihoro, J. The role of technology in strategy implementation and performance of manufacturing small and medium firms in Thika, Kenya. Int. J. Bus. Soc. Sci. 2016, 7, 156–165. [Google Scholar]

- Diana, N.; Sudarmiatin, S.; Hermawan, A. Model of Accounting Information System and SMEs Performance in Contingency Theory Perspective. Asian J. Manag. Entrep. Soc. Sci. 2023, 3, 47–69. [Google Scholar]

- Desreumaux, A. Stratégie et organisation: Un état de l’art. Rev. Française Gest. 1998, 122, 45–62. [Google Scholar]

- Sponem, S. La fonction contrôle de gestion: Proposition d’une typologie. Comptab.-Contrôle-Audit 2009, 15, 113–144. [Google Scholar]

- Burkert, M.; Davila, A.; Mehta, K.; Oyon, D. Relating alternative forms of contingency fit to the appropriate methods to test them. Manag. Account. Res. 2014, 25, 6–29. [Google Scholar] [CrossRef]

- Brignall, S.; Joan, B. Strategic enterprise management systems: New directions for research. Manag. Account. Res. 2004, 15, 225–240. [Google Scholar] [CrossRef]

- Komarev, I. La Place Des Budgets Dans le Dispositif de Contrôle de Gestion: Une Approche Contingente. Ph.D. Dissertation, Université Montesquieu-Bordeaux IV, Pessac, France, 2007. [Google Scholar]

- Chapellier, P. Comptabilités et Système D’information du Dirigeant de PME. Essai D’observation et D’interprétation des Pratiques. Ph.D. Dissertation, Université de Montpellier II, Mende, France, 1994. [Google Scholar]

- Kalika, M. Structure Organisationnelle et Technologie, Institut de Gestion de Touraine; Université de Tours: Tours, France, 1987. [Google Scholar]

- Zian, H. Contribution à L’étude des Tableaux de Bord Dans L’aide à la Décision Des PME en Quête de Performances. Ph.D. Dissertation, Montesquieu University, Bordeaux, France, 2013. [Google Scholar]

- Merchant, K.; Van Der Stede, W. Management Control Systems: Performance Measurement, Evaluation and Incentives, 2nd ed.; Prentice Hall: London, UK, 2007; pp. 154–186. [Google Scholar]

- Malhotra, N.K. Etudes Marketing avec SPSS, 4th ed.; Pearson Education: Paris, France, 2004. [Google Scholar]

- Saunders, M.N.K.; Lewis, P.; Thornhill, A. Research Methods for Business Students, 7th ed.; Pearson Education: Harlow, UK, 2016. [Google Scholar]

- Nguyen, T.H.; Nguyen, D.T.; Nguyen, T.A.; Nguyen, C.D. Impacts of contingency factors on the application of strategic management accounting in Vietnamese manufacturing enterprises. Cogent. Bus. Manag. 2023, 2, 2218173. [Google Scholar] [CrossRef]

- Henri, J.F. Organizational culture and performance measurement systems. Account. Organ. Soc. 2006, 31, 77–103. [Google Scholar] [CrossRef]

- Bedford, D.S.; Malmi, T.; Sandelin, M. Management control effectiveness and strategy: An empirical analysis of packages and systems. Account. Organ. Soc. 2016, 51, 12–28. [Google Scholar] [CrossRef]

- Chenhall, R.H. Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Account. Organ. Soc. 2003, 28, 127–168. [Google Scholar] [CrossRef]

- Ghosh, D.; Lee Willinger, G. Management Control Systems, Environmental Uncertainty, and Organizational Slack: Empirical Evidence. In Advances in Management Accounting; Emerald Group Publishing Limited: Leeds, UK, 2012; Volume 21, pp. 87–117. [Google Scholar]

- Curtis, E.; Sweeney, B. Managing different types of innovation: Mutually reinforcing management control systems and the generation of dynamic tension. Account. Bus. Res. 2017, 47, 313–343. [Google Scholar] [CrossRef]

- Korsen, E.B.H.; Holmemo, M.D.Q.; Ingvaldsen, J.A. Digital technologies and the balance between control and empowerment in performance management. Meas. Bus. Excell. 2022, 26, 583–596. [Google Scholar] [CrossRef]

- Grozovskiy, G.I.; Levina, T.; Noskova, V.E.; Ershov, D. The adaptability of a quality management system to external and internal factors at manufacturing companies. In AIP Conference Proceedings; AIP Publishing: Melville, NY, USA, 2024; Volume 3063. [Google Scholar]

{kind=link}

{kind=link}

| Variable | Items |

|---|---|

| Environment | The dynamism of the external environment is very stable (slow evolution). |

| The dynamism of the external environment is average (average trends). | |

| The external environment is very dynamic (rapid change). |

| Variable | Items |

|---|---|

| Technology | The existence of an information system. |

| The degree of technology within a company. |

| Variable | Items |

|---|---|

| Organizational structure | Advising managers (management, operations, etc.). |

| Forecasting (budget, operational and strategic plans, etc.). | |

| Taking action (implementing and monitoring action plans, budgetary control). | |

| Closing and reporting (reporting, dashboard, etc.). | |

| Analyze costs (cost accounting). | |

| Develop tools (information systems, procedures, processes, etc.). | |

| Advising managers (management, operations, etc.). |

| Target | Surveys Distributed | Surveys Retrieved | Surveys Unretrieved | ||

|---|---|---|---|---|---|

| Number of Surveys Distributed | Number of Surveys Retrieved | Percentage % | Number of Unrecoverable Surveys | Percentage % | |

| Moroccan industrial companies | 250 | 190 | 76% | 60 | 24% |

| Sample Characteristics | Workforce | Percentage | Percentage Cumulative |

|---|---|---|---|

| Firm legal status SA SARL Total | 25 165 190 | 13.2 86.8 100 | 13.2 100 |

| Employees Between 10 and 99 employees Between 100 and 200 employees Over 200 Total | 15 115 60 190 | 7.9 60.5 31.6 100 | 7.9 68.4 100 |

| Years of existence Less than 5 years Between 5 and 10 years Between 10 and 25 years Over 25 years Total | 15 50 109 16 190 | 7.9 26.3 57.4 8.4 100 | 7.9 34.2 91.6 100 |

| Precision measurement of Kaiser–Meyer–Olkin sampling. | 0.753 | |

| Bartlett’s sphericity test | Approximate chi-square | 625,430 |

| ddl | 1 | |

| Meaning of Bartlett | 0.000 | |

| Component Matrix | Representation Quality | ||

|---|---|---|---|

| Axis1 component | Initial | Extraction | |

| ENV1 | 0.981 | 1 | 0.961 |

| ENV2 | 0.993 | 1 | 0.984 |

| ENV3 | 0.994 | 1 | 0.987 |

| Eigenvalues | 2.933 | ||

| Total variance explained | 97.77 | ||

| Cronbach’s Alpha | 98.9 | ||

| Precision measurement of Kaiser–Meyer–Olkin sampling. | 0.560 | |

| Bartlett’s sphericity test | Approximate chi-square | 629,500 |

| ddl | 1 | |

| Meaning of Bartlett | 0.000 | |

| Component Matrix | Representation Quality | ||

|---|---|---|---|

| Component Axis 1 | Initial | Extraction | |

| TECH | 0.975 | 1 | 0.590 |

| DEG.TECH | 0.975 | 1 | 0.590 |

| Eigenvalues | 1.90 | ||

| Total variance explained | 94.98 | ||

| Cronbach’s Alpha | 58.5 | ||

| Precision measurement of Kaiser–Meyer–Olkin sampling. | 0.746 | |

| Bartlett’s sphericity test | Approximate chi-square | 629,500 |

| ddl | 1 | |

| Meaning of Bartlett | 0.000 | |

| Component Matrix | Representation Quality | ||

|---|---|---|---|

| Component Axis 1 | Initial | Extraction | |

| CG.OBJ1 | 0.990 | 1 | 0.980 |

| CG.OBJ2 | 0.964 | 1 | 0.929 |

| CG.OBJ3 | 0.979 | 1 | 0.958 |

| CG.OBJ4 | 0.979 | 1 | 0.958 |

| CG.OBJ5 | 0.974 | 1 | 0.948 |

| CG.OBJ6 | 0.990 | 1 | 0.980 |

| Eigenvalues | 11.826 | ||

| Total variance explained | 84.473 | ||

| Cronbach’s Alpha | 97.4 | ||

| Variable | Number of Items | Variance Recovered Following Factorization | Cronbach’s Alpha |

|---|---|---|---|

| Environment | 3 | 97.77 | 98.9 |

| Technology | 2 | 94.98 | 58.5 |

| Organizational structure | 6 | 84.473 | 98.4 |

| Variables | SIZE | ENV | TECH | STR | SCM |

|---|---|---|---|---|---|

| SIZE | 1 | ||||

| ENV | −0.004 | 1 | |||

| TECH | 0.009 | 0.040 | 1 | ||

| STR | −0.085 | −0.009 | 0.041 | 1 | |

| SCM | 0.090 | 0.223 | 0.158 | −0.012 | 1 |

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate | Durbin–Watson |

|---|---|---|---|---|---|

| 1 | 0.744 | 0.554 | 0.547 | 0.39275 | 1.746 |

| Model | Sum of Squares | df | Mean Square | F | Sig. | |

|---|---|---|---|---|---|---|

| 1 | Regression | 67.986 | 5 | 12.400 | 80.386 | 0.000 |

| Residual | 54.123 | 185 | 0.154 | |||

| Total | 122.109 | 190 | ||||

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | Collinearity Statistics | |||

|---|---|---|---|---|---|---|---|---|

| B | Std. Error | Beta | Tolerance | VIF | ||||

| 1 | (Constant) | −1.680 | 0.315 | −6.553 | 0.000 | |||

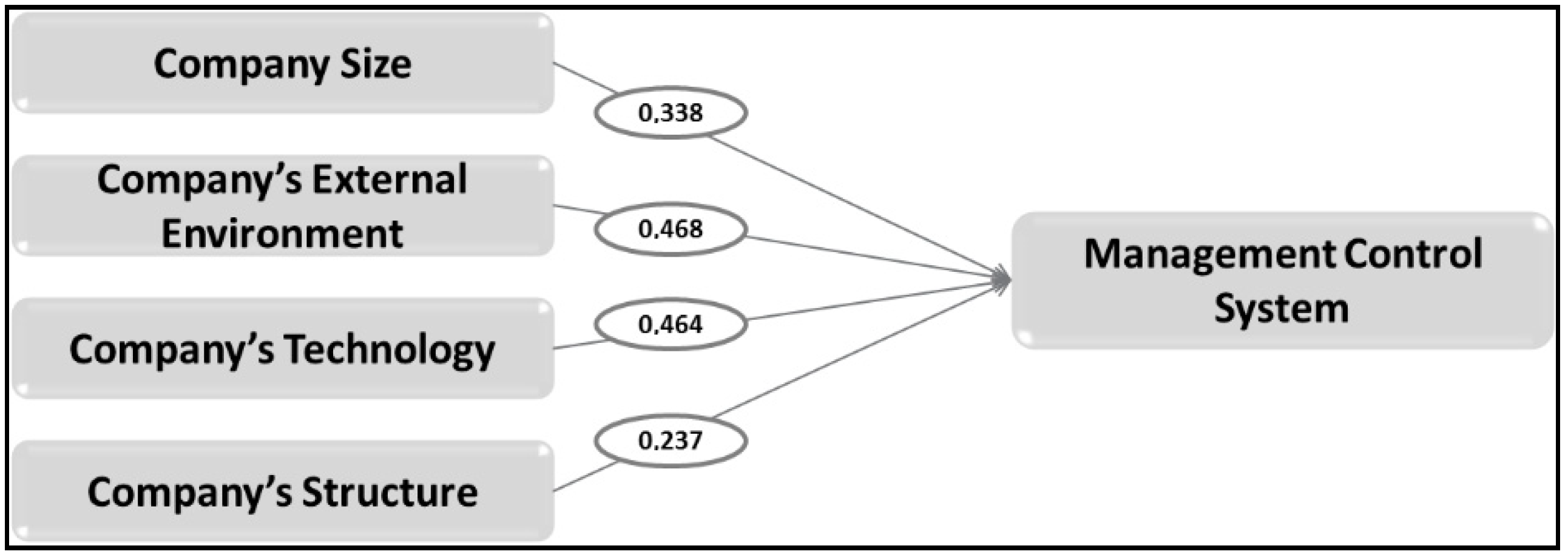

| SIZE | 0.335 | 0.048 | 0.338 | 6.962 | 0.000 | 0.980 | 1.014 | |

| ENV | 0.423 | 0.045 | 0.468 | 8.320 | 0.000 | 0.975 | 1.022 | |

| TECH | 0.418 | 0.046 | 0.464 | 9.120 | 0.000 | 0.968 | 1.019 | |

| STR | 0.202 | 0.035 | 0.237 | 4.213 | 0.000 | 0.900 | 1.020 | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hammouch, H.; Manta, O.; Palazzo, M. Adapting Management Control Systems to Organizational Contingency Factors: A Study of Moroccan Industrial Companies. Businesses 2024, 4, 883-898. https://doi.org/10.3390/businesses4040048

Hammouch H, Manta O, Palazzo M. Adapting Management Control Systems to Organizational Contingency Factors: A Study of Moroccan Industrial Companies. Businesses. 2024; 4(4):883-898. https://doi.org/10.3390/businesses4040048

Chicago/Turabian StyleHammouch, Hind, Otilia Manta, and Maria Palazzo. 2024. "Adapting Management Control Systems to Organizational Contingency Factors: A Study of Moroccan Industrial Companies" Businesses 4, no. 4: 883-898. https://doi.org/10.3390/businesses4040048

APA StyleHammouch, H., Manta, O., & Palazzo, M. (2024). Adapting Management Control Systems to Organizational Contingency Factors: A Study of Moroccan Industrial Companies. Businesses, 4(4), 883-898. https://doi.org/10.3390/businesses4040048