Abstract

Objective: In recent years, management accounting in higher education institutions has undergone significant changes due to the various New Public Management (NPM) reforms. One of the management accounting tools that has been advised to HEIs is Activity-Based Costing (ABC). With this evolving field of research, this article aims to analyze research in international scientific journals focusing on ABC in HEIs. To this end, this article provides an overview of how research in this area has evolved. We present an overview of the past, present, and future of research in the field of the ABC model applied in HEIs. Methodology: Through a systematic literature review, the Web of Science and Scopus databases were used as a source of articles. Our analysis is based on a total of 139 articles. We used a systematic literature review combining different bibliometric techniques. These allowed us to develop a mapping of the literature on the application of the ABC model in HEIs, which helps us better understand the research related to the topic and its evolution. Results: It is concluded that the existing literature on this topic has developed along three lines of research: implementation of ABC as a cost-control method, TDABC as a time-based cost-control method, and the application of the ABC Method in health services. Originality: Based on the results found, this article identifies avenues of research that can be explored, namely the study of the application of ABC in the education sector, and provides a research agenda for future studies.

1. Introduction

The accelerated growth of the education sector in recent decades has resulted in significant changes in the institutional management process, making administrators prepare to face the challenges of market competitiveness through more complex and effective management systems. Cost information has become more relevant in administration, and associated with it are costing methods, which show the costs incurred to produce services or products. ABC stands out for the wealth of detail in the methodology applied to its implementation. This detail makes it possible to understand the activities that generate costs within an HEI, segregating those that add value from those that do not. The main objective of ABC is to limit all cost-causing activities. It centers on the detailed description of all the tasks and activities involved in obtaining the final product or result. This approach facilitates a holistic view of the institution’s operational framework [1].

In recent decades, the purpose of accounting has changed from simply recording financial transactions to becoming a tool for measuring performance and maximizing the profitability of organizations [2]. In this way, a company can perform well and become successful by reducing costs and eliminating products and/or services that could cause losses [3]. In the 1980s, Johnson and Kaplan recognized the necessity for organizations to access a system that furnished information about strategic variables crucial for creating value within an organization. Consequently, in response to the limitations of prevailing systems known for their lack of timeliness and rigor, Johnson and Kaplan developed the Activity-Based Costing (ABC) system [4]. The ABC method ensures enhanced accuracy in cost-benefit analysis and contributes to the overall improvement of organizational performance [5].

Higher education institutions that are currently facing a reduction in public funding are not dissociated from this reality. Therefore, there is a need to monitor the performance of the activities carried out, requiring management accounting to be able to report on the cost of each student, subject, or training course taught, as well as the cost of each research project or service provided to the outside world [6]. Some authors [7,8] agree that budgeting through ABC/ABM is a useful tool that allows for the management of an organization to achieve continuous improvement by reducing costs, increasing profitability, and establishing competitive and strategic advantages that allow it to achieve its objectives. Others [9] state that it focuses on the management and excellence of institutions, refers to improving the development of activities, and includes management that adds efficiency to the management of resources in the institution by improving their use. It seeks total quality through the formalization of process engineering to achieve higher revenues through lower costs and determines the increase in profitability through a change in activities, stating that the efficiency of the activity remains constant.

In recent years, bibliometric studies have gained significant traction within the accounting domain. These investigations offer a swift route for researchers to pinpoint key research avenues, prominent journals, leading authors, prevalent research methodologies, economic sectors, organizational typologies, and more. They illuminate potential gaps ripe for future exploration. These studies hold weight in their ability to offer informed suggestions grounded in current knowledge, enabling scrutiny of knowledge gaps, researchers, institutions dedicated to a specific topic, and the evolution of foundational theories supporting it [10].

The objective of this study is to present a comprehensive overview of the historical, current, and prospective research on the application of the ABC model in HEIs, aiming to address the existing lack of organized research in this field. To achieve this, we conducted a systematic literature review employing diverse bibliometric techniques. Additionally, we offer a thematic mapping and examination of research trends, aiming for a deeper comprehension of the literature concerning this subject and its developmental trajectory. Thus, within this article, our focal research inquiries are: Is the ABC model being implemented in HEIs? How has the research landscape evolved in this domain? And in what aspects of HEI services is this tool predominantly utilized?

In this research, we employed a blend of bibliometric methods, including citation analysis, co-citations, and network analysis to study the scientific domain and address our research queries. Bibliometric analysis stands as a widely adopted tool for comprehensively assessing existing global literature [11]. This method involves applying a quantitative assessment and examination to publications, encompassing articles and their citations, aiming to gauge the current state of the literature. Additionally, this technique furnishes comprehensive data on all activities within a scientific field, offering overarching insights into the research activities and impacts, particularly concerning researchers, journals, universities, and countries [12,13]. To the best of our knowledge, this particular bibliometric study focusing on the application of the ABC model in HEIs marks a pioneering endeavor within the literature.

The findings highlight significant prior research in this domain, comprising a total of 139 articles clustered into three categories: ABC implementation for cost control, TDABC as a time-based cost-control approach, and the utilization of the ABC method in health services. Future research stemming from these clusters should pivot towards unexplored areas, addressing additional issues and research topics that hold potential relevance to management concerns associated with the implementation of the ABC model in HEIs.

The article’s structure unfolds as follows: introduction. Section 2 lays out the theoretical framework concerning the topic. Section 3 delineates the research methodology employed to curate the sample of articles encompassing the application of the ABC model in HEIs published between 2003 and 2021. An in-depth descriptive analysis of the results ensues. Section 5 delves into the detailed content analysis of the four clusters. Lastly, Section 6 encapsulates the principal conclusions drawn from the work, proposes a research agenda for future studies, and outlines both the limitations and contributions of this study.

2. Literature Review

2.1. Activity-Based Costing (ABC)

In the past, the standard approach to cost estimation revolved around allocating indirect expenses to various products, predominantly emphasizing direct labor. During a period where raw materials and direct labor held pivotal roles in production, these systems emerged due to restricted market options and reliance on relatively unchanging technology [14,15].

The utilization of the ABC approach, as well as its popularity, arose as a result of organizations seeking to reduce alterations caused by the misallocation of secondary costs. Although the method had been used before, it was only at the end of the 1980s that it became widely known through a study published in the Harvard Business Review entitled “Measure Costs Right: Make the Right Decisions”, in which Kaplan and Cooper [16], as well as explaining the method, named it Activity-Based Costing [17].

This costing method transforms the allocation of departmental indirect costs by first attributing them to activities and, subsequently, to products using cost drivers [17,18]. Within this methodology, drivers symbolize the primary factors influencing activity costs. This approach brings a sense of structure to cost distribution, minimizing arbitrary allocations. The principle is that products bear the costs of activities in alignment with the proportional utilization of the cost objects.

The literature highlights numerous advantages associated with implementing ABC in organizations. Khodadadzadeh [19] asserts that ABC enables the identification of unprofitable products or services within a company, allowing for their elimination and adjustments to the prices of products or services that are wrongly priced.

Cooper and Slagmulder [20] argue that the system’s main advantage lies in its ability to reduce costs and, at the same time, improve the company’s strategic position. It also emphasizes the calculation of real costs and improves the decision-making process by providing reliable information.

Kalicanin [21] emphasizes that the insights offered by ABC prove crucial for company managers, aiding in the assessment of various operational methods and facilitating comparisons with other businesses. This underscores the invaluable role of ABC in devising and executing business strategies.

There has been an increasing necessity to adopt effective management tools for overseeing business resources more efficiently. Cost accounting has emerged as a pivotal competitive edge for companies, which has been deemed a crucial strategic element by managers [22,23]. ABC serves as a framework that offers pertinent insights into production and associated activities, empowering managers to pinpoint potential areas for enhancement to streamline costs. Essentially, this system facilitates access to data regarding the costs and profitability of business processes, heralding an innovative approach in corporate accounting. It addresses the limitations posed by traditional costing systems in an evolving and elaborate business landscape [24].

However, several authors [25,26,27,28] have highlighted critical aspects regarding the adoption of the ABC system. They note that many organizations refrain from implementing it due to the intricacy, challenges, and expenses associated with its setup and maintenance. Kaplan and Anderson [29] specifically address how the system’s complexity, difficulty, and cost hinder its adoption. Fito et al. [30] attribute the interruption in implementing the ABC model to conceptual issues. Ouassini [31] emphasizes the substantial software costs involved in adopting the ABC system, necessitating substantial investment in staff training. Gosselin [32] warns of the “ABC paradox”, underscoring the gap between academic and consultant endorsements of the model and its limited adoption in companies. Rankin [33] suggests that identifying the contextual factors predicting ABC system adoption could illuminate the reasons behind its low adoption rates across different countries.

Due to these crucial considerations, companies should deliberate on the necessity of an ABC system. Certain authors have outlined specific organizational characteristics that warrant the implementation of this method, essentially advocating its use in companies where indirect costs constitute a substantial portion of the total costs. This includes industries involved in the production of diverse products and services for a broad consumer base. Additionally, it applies to those engaging with a diverse clientele necessitating specialized or supplementary services [34,35,36,37,38].

In the literature, various bibliometric studies also explore this topic. For instance, Stefano et al. [39] conducted a study from 1990 to 2011, utilizing international databases ISI Web of Knowledge and Scopus. Their objective was to structure a bibliographic portfolio centered on the application of the ABC method in the service sector. Their findings revealed that the predominant application of the ABC method occurs in organizations providing health services. It was noted that the ABC method is employed in its conventional or modified form, sometimes integrated with other tools such as QFD (Quality Function Deployment) or AHP (Analytic Hierarchy Process). Furthermore, most studies leverage the ABC system to distinguish value-adding activities from those causing losses, aiming to enhance productivity and competitiveness.

Corresponding to the above authors, the effective implementation of ABC hinges on the dedicated commitment of top management to align all objectives with strategy, quality, and performance assessment. Equally crucial is ensuring that managers grasp the requisite time commitment for this implementation and possess expertise in leveraging information technology.

In a study by Zanievicz et al. [10], which focuses on costing methods prevalent at the Brazilian Congress of Costs between 1994 and 2010, the ABC system emerged as the most extensively researched method. It was followed by the theory of constraints and target costing. Subsequently, in 2008, Diehl and Souza [40] conducted an analysis of ABC publications in scientific events. They aimed to scrutinize the attributes of scientific papers related to ABC in Brazilian cost conferences, observing a consistent annual increase in the number of articles produced on research topics.

Barsanti and Souza [41] conducted an analysis of scientific output on the ABC system spanning from 2002 to 2015, utilizing empirical research published in Brazilian accounting journals. Regarding the authors’ demographics, Barsanti and Souza’s analysis revealed that most of the authors were male (60.18%), with 28.7% of the sample holding a Ph.D. They observed a prevalent inclination toward collaborative research. In terms of references, there was a distinct preference for international sources, notably books and journals. Additionally, they highlighted the substantial prevalence of exploratory and qualitative research, particularly through methodologies like case studies and interviews for data collection. Their findings mirrored conclusions akin to those derived from the study conducted by Souza et al. [42], which aimed to scrutinize research published on ABC between 2001 and 2010 in the principal Brazilian accounting journals.

In a review from 1990 to 2005, Gosselin [32] investigated the adoption rates of ABC. Despite the manifold advantages associated with this model, the findings across most studies consistently indicated remarkably low adoption rates.

2.2. Application of the ABC Model in HEIs

Over the last few decades, several authors [2,43,44,45] have discussed the practical application of management accounting, which is now considered fundamental, as many theoretical models have failed due to the fact that they ignored the costs and benefits associated with its applicability [46]. The development of a management control system (SG) has warranted studies in an extensive variety of sectors due to its greater importance on the private sector, while its application in the public sector is often relegated to the background. However, the collection of relevant information in the field of costs is also crucial in the public sector, not only because they are an important source of information for internal and external users of public bodies [47] but also because of the constant need to prioritize the allocation of resources and minimize costs due to the scarcity of resources and budgetary pressures.

Similarly, institutions make decisions on a daily basis, such as hiring employees. Other decisions are not made on a daily basis, such as adding a new product or service and ensuring the continuity of existing ones, seeking to maximize profits, and improving service delivery and optimizing resources, for which they need adequate information, which allows for greater efficiency in decision-making. Also, it needs to be considered that the acceptance of implementing a method will always depend on the staff that makes it work [48].

In higher education institutions, curriculum renewal is a complicated decision that not only depends on establishing a project based on the institutional objective but must also consider the resources needed to implement it and, at the same time, ensure that they are solvent in financial terms. When an academic career is evaluated, its results vary from one to another due to the characteristics that define them, so the cost obtained for the curricular renewal of one career is not transferred to another in its entirety; they must be evaluated independently in order to obtain objective results. The university system seeks to achieve efficient financing of educational models, minimizing its economic needs to ensure success based on appropriate management and decision-making [6]. This is where the importance of cost accounting lies, from which the break-even point is determined. It is defined as a valuable tool for analyzing institutional innovations, which is the point of activity where no profit or loss is generated because revenues are equal to costs. There are several studies investigating the application of CS in higher education institutions. In one of these studies, Lutilsky and Dragija [49] conclude that ABC has a low degree of implementation in European universities since only a tiny group applies the method in its entirety. However, they point out that many universities partially use the ABC method in their CS.

Carvalho et al. [50] and Valderrama and Sanchez [51] considered that the ideal costing system should combine traditional and ABC methods. This so-called European approach assumes that each cost center includes several activities, and that costs should be shared. Hernández et al. [52] also agree with the idea of the partial use of the ABC method in universities since the proposed system is based on traditional systems with the analysis philosophy of the ABC method, i.e., it breaks down the cost centers and relates them to the activities that permit the costs. However, the basic element of the system is calculating costs by cost center. The article by Keel et al. [53] sought mainly to discover the motivations for applying TDABC in organizations that provide health services and how the seven-step approach to its implementation recommended by Kaplan and Porter [54] is being used in the area. Unlike the previous ones, this study involved seven databases, including SCOPUS and Web of Science, thus reaching international publications. It resulted in a sample of 25 articles, which explicitly showed implementations of the TDABC method. This study concludes that the number of applications of TDABC has been growing, with 80% of the articles found having been published from 2013 to January 2016 alone. It also found that 14 articles implemented the method in organizations in the United States (USA), seven in organizations in Europe, and two in Brazilian companies, while Canada, China, and India had only one application each (one of the studies involved two countries: USA and India). Finally, the applications of TDABC generally do not cover the entire treatment cycle of a medical condition but are restricted to a specific organizational context.

3. Research Methodology

Method

The articles were selected through two database searches, Web of Science and Scopus, using the keywords “Activity-based cost*”, to which we added the following: “higher educat*” or “universit*” or “HEI” (Higher Education Institution) or “HEO” (Higher Education Organization) to specify the context in question. The search on Web of Science resulted in 105 articles, and on Scopus in 175 articles, for a total of 280 results. A filter was then applied by area, considering the theme and context of the application of this study. The following areas were selected from the Web of Science: business finance, education, educational research, management, business, education scientific disciplines, economics, interdisciplinary social sciences, public administration, and multidisciplinary sciences. After applying this filter, the sample was reduced to 62 results.

The Scopus database selected the following areas: business management and accounting, social sciences, economics, econometrics, finance, and decision sciences. By applying this filter, the sample was reduced to 141 articles. Finally, it was decided to select only scientific articles, reviews, and early access articles, excluding other publications such as books, conference proceedings, or so-called grey literature.

In the “selection” phase, after eliminating duplicate articles (47 articles), the titles, abstracts, and keywords of the 156 articles were read. Finally, 17 articles were excluded, resulting in a final sample of 139. These 139 documents were the subject of bibliometric analysis.

These 139 publications contain 15,484 citations of other publications, including books and articles published in journals, which are the subject of this analysis (Co-citation Analysis—CA).

Co-citation refers to the joint citation of two articles in subsequent literature [55]. Co-citation Analysis (CA) operates under the premise that when two or more documents or authors are consistently cited together in subsequent research, there exists a thematic, conceptual, or methodological proximity perceived by the citing author [56]. Hence, the higher the frequency of concurrent citations between two documents or authors, the stronger the indication of their content-related relationship [57], showcasing the knowledge foundation within a scientific domain. The connection and association between two documents are forged not by their authors but by the scientific community, which appropriates and links these contents to foster new knowledge.

Bibexcel was used to organize the data for the bibliometric analysis and the Statistical Package for the Social Sciences (SPSS) to conduct the exploratory factor analysis (EFA), which aims to analyze the pattern of correlations between variables and use these correlation patterns to group the variables into a smaller number of dimensions [58].

As for the criteria for selecting the co-cited publications to be analyzed, it should be emphasized that the current literature does not specify a minimum or maximum quantity to be adopted, and, therefore, it is at the researcher’s own discretion. However, in order to carry out Exploratory Factor Analysis, the first indicator to be observed is the Kaiser–Meyer–Olkin (KMO) measure of sample adequacy, which must be greater than 0.60 [58], as only values between 0.6 and 1.0 indicate that factor analysis is appropriate for that dataset. In the process of selecting the co-cited publications to be analyzed, several attempts were made to insert data from publications with more than three co-citations, for a total of 38 publications. However, one was among the most cited only because it dealt with methodology and was irrelevant to this study. This publication was excluded from the sample, leaving 40 publications used to generate the co-citation matrix and subsequent exploratory factor analysis in SPSS.

In the EFA, the data were grouped into four dimensions, and the procedures recommended by Hair et al. [58] were followed, assessing overall KMO (above 0.6), Bartlett’s test of sphericity (<0.05), and the KMO of each variable in the anti-image matrix (above 0.5). Then, the model was adjusted by excluding variables with a commonality below 0.5, as well as variables with cross-loadings (above 0.5 in more than one factor). The orthogonal factor rotation method was Varimax, one of the most widely used methods, considered by Hair et al. [58] to be superior to other orthogonal factor rotation methods when a simplified factor structure is to be achieved. Each publication selected for the EFA was treated as a variable. It should be noted that only one variable was excluded at a time. Thus, the EFA was run several times to ensure that the variables were adjusted. After excluding the variables with an individual KMO of less than 0.50, the rotating matrix generated in SPSS was analyzed. This left 19 variables that comprise the structure of scientific production in the area of entrepreneurship. In the EFA results, with 19 variables, the overall KMO was 0.799, the total variance explained was 90%, and Bartlett’s test of Sphericity was 0.000.

4. Results

4.1. Data Base Information

As this research was studied in 2022, we limited our search to articles published until the last year (2021). The search resulted in a total of 139 articles. We provide a summary of the search results in Table 1.

Table 1.

Research information.

Table 1 presents a summary of the information gathered from articles investigating the application of the ABC System in HEIs over the last three decades. A total of 139 articles by 502 authors were obtained, with an average of almost nine citations per document. Most of the papers were co-authored, with an average of 3.59 authors per document. The analysis covers a period of three decades, from 1991 to 2021.

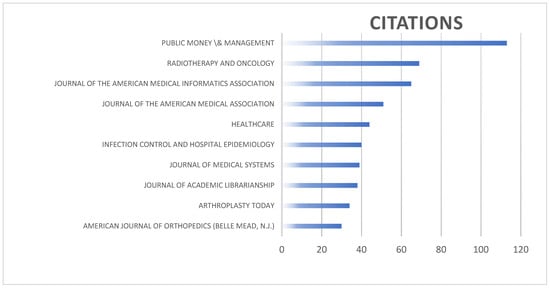

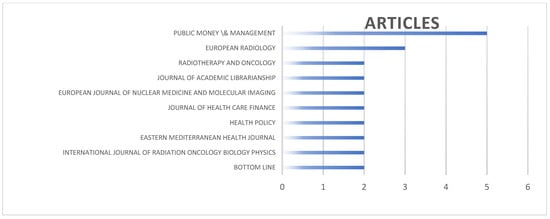

Figure 1 and Figure 2 list the 10 journals with the highest number of published articles and the highest number of citations. The journals with the most publications are Public Money and Management (five articles), European Radiology (three articles), and Annales de Pathologie, among others (two articles). The journals with the most citations are Public Money and Management (123 citations), Radiotherapy and Oncology (69 citations), Journal of the American Medical Informatics Association (65 citations), and Journal of the American Medical Association (51 citations).

Figure 1.

Distribution of articles and total citations by journal.

Figure 2.

Distribution of articles by journal.

4.2. Analysis of Co-Citations: Multidimensional Scales, Cluster Analysis, and Factor Analysis

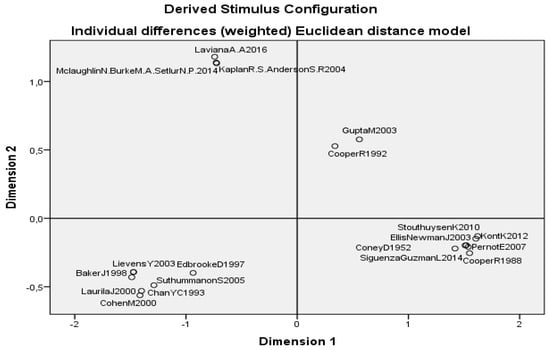

The bibliometric approach involved employing co-citation analysis to identify key publications related to the ABC model within HEIs. This analysis constructed a co-citation matrix, capturing the frequency of joint citations between pairs of documents or authors addressing the ABC model within HEIs across various publications. This method facilitated the examination of citation relationships and the identification of prevailing research approaches in the domain. Articles with more than three co-citations were selected, initially yielding 38 articles, which were ultimately narrowed down to 19 articles after meeting all criteria. Using Multidimensional Scaling (MDS), a map was generated to explore the relationships between these articles, revealing the dimensions that best illustrated their similarities and differences. Subsequently, cluster analysis grouped these articles based on commonalities. Factor analysis then identified articles within each factor and assessed their contributions through factor loadings. The resulting two-dimensional map, derived from multidimensional analysis using data from the co-citation matrix and ASCAL routines in the IBM SPSS 26.0 for Windows statistical program, is depicted in Figure 3. Evaluation indices, such as Kruskal’s Stress (0.024) and RSQ (0.97), indicated a mapping very closely aligned with reality.

Figure 3.

Multidimensional dimensioning and cluster analysis.

Although the axes’ construction is rooted in a dimensional scale, the articles’ positions on the map imply significance for the axes. Utilizing Ward’s hierarchical method for cluster analysis determined the grouping of articles showcased on the multidimensional scale graph. The article grouping in the figure above aligns with the classification along Dimension 1, illustrating the implementation of ABC as a cost-control method (Clusters 2 and 3), while Dimensions 2 and 3 denote TDABC as a time-based cost-control method and the application of the ABC Method in health services, respectively. Table 2 outlines the articles encompassed within each of the identified three clusters.

Table 2.

Studies by cluster.

Observing the set established by prior studies, we conducted the analysis using Varimax rotation, drawing data from the co-citation matrix. In our factor analysis, we only considered published articles where their factor weight equaled or exceeded 0.3. We posited a substantial contribution to the corresponding paradigm if an article had a factor loading equal to or greater than 0.5. Table 3 illustrates the outcomes of the factor analysis. The Scree Plot revealed evidence of four factors, accounting for 48.5% of the variance. Notably, several references boasted a factor load surpassing 0.7, reaffirming these articles’ significance within associated paradigms. It is evident that certain articles had a factor load exceeding 0.3 in multiple factors, serving as mediators between paradigms and potential links formed among them.

Table 3.

Rotated component matrix a.

Our identification of three approaches (thematic groupings) derived from the multidimensional scale analysis, cluster analysis, and factor analysis. Factors 1 and 3 showcased pivotal authorship roles, corroborated by their weight within the respective approaches. Factor 1 aligned with Cluster 1: Family Capital, prominently featuring articles by Cooper, R. [59], and Pernot, E. [60], bore considerable weight, which indicated their significance within this approach. Cluster 2 was composed of articles from Factor 3, with all articles holding substantial weight, notably Laviana, A. [75]. Conversely, Cluster 3 encompassed articles from Factor 2, spotlighting authors Chan, Y. [68] and Laurila, J. [69]. Interestingly, Cluster 2 articles were exclusive to that factor, unlike those in Factors 1 and 3, which displayed minimal weights across other factors.

4.3. ABC Applied in HEIs

Cluster 1: Implementation of ABC as a cost-control method

Coney [63] highlights a notable deficiency in the depth of knowledge and specific guidance concerning management among library managers and authors focusing on library management. The literature produced by librarians often tends to be descriptive rather than analytical, leaning toward a more simplistic approach than a nuanced understanding. There is a significant gap in articles that effectively merge theoretical knowledge with practical application, especially in terms of “connecting” literature. To address this, there is a necessity for a method that acquaints librarians with management concepts and demonstrates their application within library settings.

Cooper and Kaplan [59] highlight the substantial expansion of product lines and marketing channels. Direct labor, once a significant cost for companies, now represents a minor fraction, while expenses in factory support, marketing, and sales have surged. Despite this shift, most companies persist in dispersing their direct labor costs across growing overheads and shrinking support functions. Similarly, activity-based costing has the potential to transform how managers assess new process technologies. Instead of prompting automatic decisions, it furnishes more precise information about production, support activities, and product costs. This enables management to concentrate on products and processes that wield the most substantial impact on profits. The ABC model empowers managers to make superior decisions regarding product design, pricing, and marketing while fostering a culture of continuous operational improvement.

Cooper and Kaplan [65] outline the fundamental principles behind establishing and implementing a novel activity-based costing (ABC) system. Traditional costing systems hinge on quantity-based allocations, like attributing organizational costs to specific products and customers by directly calculating labor expenses, machine hours, and cost of goods sold. When activity usage exceeds the existing resource quantity, the costs related to securing these resources rise. Conversely, if activity utilization falls short of the available supply, resource costs do not automatically decrease. To bolster profits, business owners must utilize available capacity to generate more business (thus boosting revenues) or eliminate idle capacity to reduce resource expenditure. Proactive efforts are crucial in addressing this situation. Costs and profits remain stagnant only when management refrains from action and neglects idle capacity.

Ellis–Newman [76] argues that university financial reports fail to adequately provide administrators with essential information to determine service costs and make optimal decisions regarding limited resource allocation. Activity-Based Costing (ABC) systems stand out as powerful tools to comprehend cost behavior and improve cost systems. The rationale for applying ABC in universities mirrors its effectiveness in manufacturing and industry. Indirect costs are assigned to goods and services based on the factors most influential to them. Utilizing diverse cost categories and factors within ABC allows for more precise and detailed calculations of product costs compared to traditional costing systems. This approach revolves around individual activities by linking costs to activities according to their resource usage. Such a focus empowers managers to evaluate the necessity of specific activities, potentially eliminating non-value-added services while retaining those that contribute value. This streamlining leads to cost savings for universities. However, a generalized approach involving the uniform allocation of resource costs to cost objects (services) contradicts the varying resource usage by individual services. While cost-effective, this method of cost attribution within ABC often yields less reliable data.

Gupta and Galloway [64] demonstrate how the ABC/M (Activity-Based Costing/Management) system serves as a practical tool for enhancing operational decision-making processes. They introduce the “Operations Hexagon”, a conceptual framework that outlines how an ABC/M system influences various aspects of operation management decisions. This framework covers product planning and design, quality management and control, inventory management, capacity management, and workforce management. By highlighting the substantial improvement in operational decision-making, the ABC/M system emphasizes its role in empowering operations managers to enhance the quality of their decision-making processes. However, a critical aspect of implementing an ABC/M system at the business unit level involves incorporating all functional areas. While accountants identify activities valuable to both customers and the organization, it falls upon operations managers to execute these activities. Companies must collaboratively prioritize enhancing customer value, thereby refining the products that deliver this value.

Kont and Jantson [62] argue that the historical approach to implementing cost accounting systems in libraries has primarily focused on technical innovation rather than organizational or management innovation. They emphasize that librarians cannot be treated like machines set at a constant speed, expected to produce uniform outputs. The TDABC model offers a viable method that department managers can test and implement, even for individual library departments. This model considers various factors impacting employee efficiency and performance, such as rest periods, break times, arrival and departure, and non-work-related communication and reading. However, they suggest the involvement of cost and economic experts in this process.

Pernot et al. [60] assert that while numerous articles have discussed implementing ABC and TDABC systems in libraries, there is a scarcity of research or surveys delving into these issues from the viewpoint of employees. Historically, implementing cost-accounting systems in libraries has been approached more as a technical innovation rather than an organizational or management one. A critical consideration highlighted is that a librarian cannot be likened to a machine programmed for a specific pace and expected to deliver consistent outcomes. The TDABC model offers flexibility by allowing department heads in individual library departments to test and implement it. This model considers various factors impacting an employee’s efficiency and performance, such as break times, commuting, communication, and non-work-related reading. However, they recommend the involvement of economic and cost experts in this process to ensure comprehensive implementation and understanding.

Siguenza–Guzman et al. [61] highlight the significant contributions of this case study to the literature on implementing advanced cost models within library processes, particularly focusing on cataloging activities. Future research avenues could involve expanding this study to various cataloging activities, including collaborative, contractual, and outsourced tasks. TDABC offers an opportunity to explore how these evolving trends in the cataloging process impact cataloging units. It allows for an analysis of whether these trends create opportunities for catalogers to allocate time to other cataloging activities, such as enhancing existing records. Another intriguing area for future investigation is conducting a similar analysis on the cataloging of diverse materials like audiovisual items, historical books, non-print materials, and maps. Additionally, comparing libraries based on best practices using TDABC presents another promising prospect for future analysis.

Cluster 2: TDABC as a time-based cost-control method

Kaplan et al. [66] note that activity-based costing has revealed an essential insight over the past 15 years: not all revenues are advantageous, and not all customers are profitable. Yet, the challenges associated with traditional ABC systems have hindered their effectiveness, timeliness, and relevance as management tools. The time-based ABC approach addresses these challenges by offering a swift and straightforward implementation process. It seamlessly integrates with existing data in ERP systems and newly installed systems, requiring minimal cost, swift implementation, and easy maintenance. This methodology offers the advantage of scalability to company-wide models and easy integration of specific characteristics related to orders, processes, suppliers, and customers. This approach enhances visibility regarding processing efficiency and capacity utilization, enabling the prediction of future resource requirements based on anticipated order volume and complexity. These features transform activity-based costing from a complex and costly financial system implementation into a tool that promptly delivers actionable data to managers in a cost-effective manner.

Mclaughlin et al. [67] contend that the TDABC model’s piloting and implementation phases effectively involved healthcare providers in evaluating processes and costs. This model acted as a catalyst for reshaping cost-conscious care. Specifically, in the neurosurgery microvascular decompression (MVD) and urology benign prostatic hyperplasia (BPH) pilots, not only did the piloting and implementation phases engage healthcare providers within these departments, but they also involved personnel across the organization in evaluating processes and costs. The TDABC model has the potential to inspire a healthcare redesign, aiding stakeholders in comprehending and accepting the service delivery process while acknowledging the true cost of resources needed for each activity. This approach demonstrates significant promise in driving a transformation toward cost-conscious healthcare and optimizing the performance of health systems.

Laviana et al. [75] found that employing TDABC aids in scrutinizing oncology services and offers insights into strategies for reducing costs in an era concentrated on enhancing value. Their study revealed significant cost variations among competing treatments across all phases of low-risk prostate cancer, spanning from diagnosis and treatment to a 12-year follow-up period.

Cluster 3: The application of the ABC method in health services

Chan [68] highlights that integrating activity-based costing with the creation of the Standard Cost Profile per unit of service and the Standard Treatment Protocol per DRG empowers healthcare administrators to pinpoint unprofitable treatments that incur costs higher than the fixed payment received from Medicare. Identifying these costly treatments enables administrators to take proactive measures by either reducing or eliminating non-essential treatment activities. Alternatively, adjustments can be made to the array of health services offered to the public, aiming to minimize expensive services. The integration of activity-based costing leads to more precise product costing and provides comprehensive cost information, offering valuable insights for healthcare administrators to enhance decision-making. In the face of shrinking revenue sources and escalating expenses, activity-based costing emerges as a crucial tool for administrators in cost management and strategic decision-making within healthcare organizations.

Cohen et al. [70] propose that ABC analysis can segment academic radiology into three distinct activities: teaching, research, and clinical, providing a comprehensive insight into the cost structure of each. This segmentation offers opportunities to enhance service quality, productivity, and cost-effectiveness within each sector. However, it is crucial to recognize that ABC analysis alone cannot serve as the sole management tool for optimizing a radiology department’s services. Integration with sophisticated computer systems, customer surveys, market analysis, a quest for new opportunities to enhance cash flow, and a readiness to implement change are necessary for its efficacy. Their strategic analysis reveals that the traditional radiology department can be delineated into three distinct businesses: clinical, teaching, and research. Despite the same radiologists contributing predominantly to each sector, the ABC analysis demonstrates that each business possesses a unique cost structure.

Edbrooke et al. [74] highlight the limitations of cost averaging and critical care cost-assessment systems, citing their inability to ascertain the precise resource consumption of individual patients. They introduce a methodology capable of evaluating the resources utilized by individual patients or patient groups, offering a valuable tool for economically assessing different treatments. Kalicanin [21] referenced average costs per patient day in the ICU at GBP 1148 but did not present the cost variation among patients. In their study, the mean daily care cost was GBP 1152, accompanied by a standard deviation of GBP 243. However, these values require careful interpretation. Firstly, the cost distribution does not follow a Gaussian pattern, so the mean alone does not sufficiently depict average treatment costs. Secondly, the impact of case mixes on these figures remains unknown and warrants further investigation. Moreover, there is a need for a cross-national, inflation-independent approach to presenting healthcare costs. This approach would facilitate comparisons between studies conducted in different countries and at different times. Ultimately, their findings align with Gyldmark’s suggestion advocating for a standardized costing model for ICU care.

Laurila et al. [69] emphasize that employing Activity-Based Costing (ABC) significantly enhances the granularity and accuracy of costing while notably reducing the proportion of unspecified overhead costs. This refined information substantially aids in effectively managing radiology departments, as it allows for the identification of the entire process of radiology procedures through unique activities, facilitating corrective measures and process enhancements. ABC facilitates the differentiation of various patient types based on their needs and distinguishes between different activities. For instance, Laurila et al.’s study compares procedures conducted in a hospital ward with those in a radiology department, revealing the latter as more cost-effective—an aspect often overlooked in radiology literature despite its significance in activity planning. The study underscores ABC’s crucial role as a management tool for radiology departments, portraying work processes as activities with known unit costs. Cost-management strategies can target activities with unfavorable cost–benefit ratios, prompting adjustments in how activities are executed and how resources are allocated. These strategic actions are pivotal as poorly structured activities can lead to missed deadlines, unfinished projects, customer dissatisfaction, and unpredictable costs. Consequently, activity redesign can be orchestrated by applying Continuous Quality Improvement (CQI) techniques, as both methods are rooted in a process-oriented approach.

Lievens et al. [73] present Activity-Based Cost (ABC) models as a pragmatic tool for assessing the genuine cost framework within radiotherapy departments and appraising prospective alterations in resources and operations. This method involves calculations involving radiotherapy costs and activity quantity, striving for a notably detailed breakdown to generate precise product costs. The level of detail in this approach can be adjusted based on preferences within each department. Opting for a lower level of detail reduces the workload involved in collecting the data essential for the daily utilization of these ABC programs.

Suthummanon et al. [71] note previous studies demonstrating the viability of employing activity-based costing (ABC) within hospital settings. However, many of these studies primarily discuss ABC’s general application in healthcare institutions. The findings highlight ABC’s capacity to enhance resource allocation, serving as a vital tool for managerial decision-making, particularly in price optimization and improving cost accuracy. It aids in identifying underutilized resources and their associated costs, ultimately leading to cost savings. Moreover, ABC systems assist hospitals in cost control, enhancing care quality and efficiency while effectively managing resources. By offering a more precise foundation for comprehending cost information compared to traditional systems, ABC enables healthcare managers to pinpoint high-cost and unprofitable procedures. Once these costly procedures are identified, additional methods, such as time management, can be employed to minimize or eliminate non-value-added activities within them. Integrating ABC with case management, critical path analysis, and other hospital control mechanisms presents a substantial opportunity for containing costs. ABC offers a structured approach for activity analysis, service costing, cost reduction, and quality enhancement. However, it is essential to acknowledge that implementing an ABC system is time-consuming and labor-intensive, and that it is heavily reliant on comprehensive participation from all departments within the organization.

Baker’s book, “Activity-based Costing and Activity-based Management for Healthcare” [72], boasts a team of editors and contributing authors with extensive expertise in finance and management. Comprising 24 chapters that blend theoretical concepts with practical applications, the initial sections introduce activity-based costing (ABC) and management within healthcare contexts. The book highlights the advantages of ABC over volume-based costing, emphasizing its abilities to have a “(1) more accurate costing of services provided, (2) better discrimination between profitable and unprofitable services and service lines, (3) better pricing and contracting strategies, (4) improved managerial decision-making capabilities, (5) easier determination of relevant costs, and (6) reduction of non-value-added costs (p. 27).” Full instructions for conducting time studies are provided, emphasizing the significance of structural decisions in understanding an organization’s cost structure by tracking direct costs and allocating indirect ones. Executives must ensure alignment between ABC reports generated by activity-based management (ABM) and the organization’s measurement and management goals. The book incorporates various elements such as quality measurement, budgeting, benchmarking, Pareto analysis, and clinical pathways, alongside ABC and control. Case studies across family physicians, primary care physicians, hospitals, home health agencies, skilled nursing facilities, and school-based health centers illustrate the content. The final chapter delves into the future prospects of ABC/ABM in healthcare.

5. Theoretical and Managerial Implications

This study holds substantial significance for the literature by highlighting the relevance of the ABC model’s applicability. It accomplishes this by identifying previously investigated issues, their respective contributions, and primary conclusions. In doing so, it offers a comprehensive map of the literature, providing insight into the main themes discussed, key findings, areas of uncertainty, and avenues for future research. Additionally, the study offers considerable managerial implications, presenting the primary managerial implications for each cluster within Table 4.

Table 4.

Implications of prevailing theoretical approaches.

The primary constraints of this study revolve around the utilization of solely the Web of Science and Scopus databases, as well as applying specific filters such as timeframes, restricted categories, and the exclusion of non-empirical sources like books, dissertations, theses, presentations, and working documents. The search criteria employed involved articles containing specific terms like “higher education*”, “university*”, or “HEI” (university), appended with “activity-based costing*” or “HEO” (Higher Education Institute). While this method was comprehensive, it may have overlooked other relevant articles not explicitly categorized under these terms. Additionally, the study’s focus solely on ABC led to the exclusion of related or similar costing and management systems like Activity-Based Management (ABM) and Time-Driven ABC (TDABC), potentially missing out on valuable insights from these alternative approaches.

6. Conclusions, Contributions, and Research Agenda

The ABC costing model can serve as an integrated strategic framework to enhance the competitive advantage and performance of higher education institutions. It offers valuable guidance for effective and efficient cost control [77].

The significance of the ABC model’s impact on Higher Education Institutions (HEIs) has notably increased since 2000. Initially, the first article on the ABC model in HEIs, published in 1991, received 31 citations. However, from 2004 onwards, the citation count surged to 208, with consistent annual increments. The recent growth in citation count hovered around 1% in 2021. Surprisingly, older articles received more citations than anticipated. Among the most cited articles, Kawamoto [78] stands out with 65 citations and an average of 8.2 citations per year. This article, titled “Value-driven Outcomes: A Pragmatic Modular and Extensible Software Framework for Understanding and Improving Healthcare Costs and Outcomes”, showcases the successful implementation of the ABC model within 6 months at the University of Utah Health Sciences Center. It elucidates that the framework, iteratively enhanced over time, has become a pivotal tool for delivering high-value care. This framework underscores the ABC model’s swift implementation to offer a pragmatic, modular, and scalable approach to understanding and enhancing healthcare value. Similarly, Van de Werf [79], in the article “The Cost of Radiotherapy in a Decade of Technological Evolution”, emphasizes the ABC model’s role in delineating the financial implications of technological advancements and evolving practices. Such insights are essential as a foundational step to substantiate cost-effectiveness, thereby supporting optimal reimbursement and provision within radiotherapy departments. Both articles pivot around cost calculations, affirming the ABC model’s relevance and efficacy within healthcare units.

Public Money & Management journal articles account for nearly 23% of all citations within our sample of journals. Specifically, five articles from this journal have contributed significantly to these citations: “Development and Implementation of a university costing model” by Valderrama and Sanchez [51] with eight citations, “Activity-based costing in UK Universities” by Mitchell [80] with 20 citations, “Activity-based costing in universities five years on” by Cropper and Cook [81] with 23 citations, “Development activity-based costing in universities 5 years on” (Cropper and Cook [81]) with 27 citations and “Activity-based costing and central overhead cost allocation in universities, a case study” (Goddard and Ooi [82]) with 35 citations.

The author with the most articles in this area is Kont K, with six articles How to optimize the cost and time of the acquisitions process” [83]; “How much does it cost to catalog a document a case study in Estonian university libraries” [84]; “What do acquisition activities really cost a case study in Estonian university libraries” [85]; “ To buy or to borrow evaluating the cost of an ebook in Taltech library” [86]; “If time and money matter ebook program challenges in Tallinn university of technology library” [87]; “Activity-based costing ABC and time-driven activity-based costing of TDABC applicable methods for university libraries” [88], the latter being the most cited with 10 citations.

The second author with the most published articles is Kesteloot K. with four articles (“Activity cost analysis of laboratory tests in clinical chemistry” [89]; “Chart in lung cancer economic evaluation and incentives for implementation” [90]; “Economic consequence of local control with radiotherapy cost analyses of the internal mammary and medial supraclavicular lymph node radiotherapy in breast cancer” [90]; “Cost calculation of pathologies in hospitals an ABC application for the placement of a hip prosthesis kosprijs calculate van pathologies in the ziekenhuizen” [91], the most cited article being “Chart in lung cancer economic evaluation and incentives for implementation” [90], with 14 citations written by Lievens Y, Kesteloot K, and Van D published in Clinical Chemistry and Laboratory Medicine.

Kaplan R, with the same number of articles published, secures the third position as the most cited author, amassing a total of 121 citations. The most cited article is “Administrative costs associated with physician billing and insurance-related activities at an academic health care system” from 2018 [92], with 51 citations, followed by “Variation in the cost of care for primary total knee arthroplasties” from 2017 [93], with 34 citations, “Dissecting costs of CT study application of TDABC (time-driven activity-based costing) in a tertiary academic center” [94] with 30 citations, and, lastly the article “Time-driven activity-based cost analysis for outpatient anticoagulation therapy direct costs in a primary care setting with optimal performance”, from 2019 [95] with six citations.

The bibliometric analysis of the ABC model application in higher education institutions revealed three distinct clusters, each representing a recognized classification. Notably, the literature on the first cluster, “Implementation of ABC as a cost-control method”, appears more advanced compared to the others. There exists considerable potential for advancing knowledge concerning activities and institutional variances leading to the adoption of a hybrid model in choosing the costing methodology. Upon scrutinizing this cluster, it becomes apparent that many authors advocate for adopting a hybrid model, leveraging traits specific to the ABC system; in particular, departments and services. Some suggest employing traditional cost-calculation systems in departments where implementing ABC might pose challenges. Certain departments within HEIs might operate as auxiliary sections, complicating the establishment of a direct relationship between service costs and cost objects. Consequently, authors have argued that defining activities to attribute costs to other services within the institution can be challenging. Regarding financial and student-support departments, authors have conceded the feasibility of utilizing any of the available cost-calculation systems without a stringent preference for one over the other.

The authors specify that within the remaining two clusters, they establish the TDABC model as the most apt for the dynamics and services found in Hospitals/Health Centers and Libraries. They assert that the TDABC method distinguishes itself from the ABC model primarily through its temporal focus and the differentiation it provides between resource supply and consumption. This approach enables organizations to pragmatically assess the cost and utilization of their processes, evaluating the profitability associated with orders, products, and customers. By employing the TDABC model, organizations gain the ability to delineate process priorities, streamline products and services, and enhance customer-relationship management, thereby optimizing overall operational efficiency.

In this approach, as per these authors, resource costs are directly allocated to cost objects using two key parameters: the cost of supplying resource capacity and the corresponding capacity cost rate. Through TDABC, the practice of interviewing employees to assign resource costs to activities prior to attributing them to cost objects becomes unnecessary.

It should also be noted within these two clusters that another model can be very useful within HEIs. The authors refer to the ABM model as ideal in supporting decision-making. The authors argue that ABM, in turn, aims to manage activities, which involves, in particular, understanding which activities, in fact, create value for the customer/user and contribute to the generation of profit/efficiency overall organization. They also highlight the fact that this system encompasses the analysis of activities, cost drivers, and performance, with ABC as its main source of information.

The list of potential research areas for the application of the ABC model in HEIs is not comprehensive. Yet the results from the bibliometric analysis underscore the need for a substantially greater academic commitment to enhance our understanding of the ABC model’s application in HEIs. Increased recognition of academic contributions in leading journals focused on business, economics, management, and administration should serve as a catalyst, further incentivizing scholars to delve into research on these pertinent matters.

This study offers significant contributions to the implementation of the ABC model in HEIs. Initially, we conducted a systematic review of the ABC model’s application in HEIs, employing bibliometric techniques. Our review not only reveals the current state of literature regarding the ABC model in HEIs but also lays the foundation for subsequent research. It synthesizes key gaps in understanding this subject matter, setting the stage for future studies and outlining potential directions for research in this domain.

Additionally, our study challenges prevailing theoretical and conceptual assumptions in research on the ABC model’s application in HEIs. It introduces fresh theoretical and conceptual perspectives that aim to steer future research in this domain. Moreover, we establish a structured roadmap delineating an informed research agenda, offering multiple yet clearly defined directions. These encompass the utilization and advancement of innovative theory to unlock new research pathways and theoretical constructs. Furthermore, our agenda seeks to foster a deeper understanding of the concept and its adaptability while addressing content-related gaps across various levels of analysis concerning the ABC model’s application in HEIs.

In summary, our study enhances comprehension of the intricacies surrounding the application of the ABC model in HEIs and pinpoints potential gaps within the existing literature. Our approach adheres to recommended best practices and draws from prior published studies in this field.

Author Contributions

Conceptualization, P.B., M.d.C.A. and R.S.; methodology, P.B., M.d.C.A. and R.S.; software, R.S.; validation, P.B., R.S. and M.d.C.A.; formal analysis, P.B.; investigation, P.B., M.d.C.A. and R.S.; resources, P.B., R.S. and M.d.C.A.; data curation, R.S.; writing—original draft preparation, P.B., R.S. and M.d.C.A.; writing—review and editing, M.d.C.A., R.S. and P.B.; visualization, P.B., R.S. and M.d.C.A.; supervision, R.S. and M.d.C.A.; project administration, P.B., R.S. and M.d.C.A.; funding acquisition, R.S. All authors have read and agreed to the published version of the manuscript.

Funding

This research is supported by national funds, through the FCT–Portuguese Foundation for Science and Technology under the project UIDB/04011/2020 (https://doi.org/10.54499/UIDB/04011/2020), and by NECE-UBI, Research Centre for Business Sciences, Research Centre under the project UIDB/04630/2022 and by CEECINST/00127/2018/CP1501/CT0010.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data are contained within the article.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Anthony, J.C.; Yoshizawa, F.; Anthony, T.G.; Vary, T.C.; Jefferson, L.S.; Kimball, S.R. Leucine stimulates translation initiation in skeletal muscle of postabsorptive rats via a rapamycin-sensitive pathway. J. Nutr. 2000, 130, 2413–2419. [Google Scholar] [CrossRef]

- Johnson, H.T.; Kaplan, R.S. The rise and fall of management accounting. IEEE Eng. Manag. Rev. 1987, 15, 36–44. [Google Scholar] [CrossRef]

- Hardan, A.S.; Shatnawi, T.M. Impact of applying the ABC on improving the financial performance in Telecom companies. Int. J. Bus. Manag. 2013, 8, 48–61. [Google Scholar] [CrossRef]

- Krishnan, A. An Application of Activity Based Costing in Higher Learning Institution: A local Case Study. Contemp. Manag. Res. 2007, 2, 75–90. [Google Scholar] [CrossRef]

- Sorros, J.; Karagiorgos, A.; Mpelesis, N. Adoption of Activity-Based Costing: A Survey of the Education Sector of Greece. Int. Adv. Econ. Res. 2017, 23, 309–320. [Google Scholar] [CrossRef]

- Améstica-Rivas, L.; Llinas-Audet, X.; Oriol Escardíbul, J. Costos de la renovación curricular: Una propuesta metodológica para la valorización económica de carreras universitarias. Form. Univ. 2017, 10, 89–100. [Google Scholar] [CrossRef]

- Ríos, M.; Rodríguez, L. Sistema de custeio baseado em atividades um instrumento viável para pequenas e médias empresas no caso do México. Manag. Stud. 2014, 220–232. [Google Scholar] [CrossRef]

- López, M.; Rodríguez, J.A. Peculiaridades de custo nas universidades. Sci. J. Account. 2018, 21, 103–115. [Google Scholar] [CrossRef]

- Parra, J.F.; Peña, Y.C. The Theory of Hidden Performance Preserves: A Theoretical Approach. Cad. Contab. 2014, 12, 15–39. [Google Scholar] [CrossRef]

- Zanievicz, M.; Beuren, I.; Santos, P.; Kloeppel, N. Métodos de Custeio: Uma metaanálise dos artigos apresentados no Congresso Brasileiro de Custos no período 1994–2010. Rev. Bras. Gestão Negócios 2013, 15, 601–616. [Google Scholar]

- Mutschke, P.; Mayr, P.; Schaer, P.; Sure, Y. Science models as value-added services for scholarly information systems. Scientometrics 2011, 89, 349–364. [Google Scholar] [CrossRef]

- Hawkins, D.T. Unconventional uses of on-line information retrieval systems: Online bibliometric studies. J. Am. Soc. Inf. Sci. 1977, 28, 13–18. [Google Scholar] [CrossRef]

- Using Bibliometrics: A Guide to Evaluating Research Performance with Citation Data; Thomsom Reuters: Toronto, ON, Canada, 2008.

- Altawati, N.; Kim-Soon, N.; Ahmad, A.; Elmabrok, A. A Review of Traditional Cost System versus Activity Based Costing Approaches. Adv. Sci. Lett. 2018, 24, 4688–4694. [Google Scholar] [CrossRef]

- Akyol, D.; Tuncel, G.; Bayhan, G. A comparative analysis of activity-based costing and traditional costing. Int. J. Ind. Manuf. Eng. 2005, 1, 136–139. [Google Scholar]

- Kaplan, R.S.; Cooper, R. Cost and Effect: Using Integrated Cost Systems to Drive Profitability and Performance; Harvard Business School: Boston, MA, USA, 1998. [Google Scholar]

- Bornia, A.C. Análise Gerencial de Custos: Aplicação em Empresas Modernas, 3rd ed.; Atlas: São Paulo, Brazil, 2019. [Google Scholar]

- Catânio, A.R.; Pizzo, J.C.M.; Moraes, R.O. Time-Driven Activity-Based Costing (TDABC): Um estudo bibliométrico das publicações nacionais. In Anais do Congresso Brasileiro de Custos; Anais do Congresso Brasileiro de Custos Foz do Iguaçu, Brazil. 2015, p. 22. Available online: https://anaiscbc.emnuvens.com.br/anais/article/view/3913 (accessed on 10 November 2023).

- Khodadadzadeh, T. A state-of-art review on activity-based costing. Accounting 2015, 1, 89–94. [Google Scholar] [CrossRef]

- Cooper, R.; Slagmulder, R. Strategic cost management: Expanding scope and boundaries. Cost Manag. 2003, 17, 23–30. [Google Scholar]

- Kalicanin, D. Activity-Based Costing as an Information Basis for an Efficient Strategic Management Process. Econ. Ann. 2013, 58, 95–119. [Google Scholar] [CrossRef]

- da Costa, C.V.; de Sene Carvalho, M.; Pinto, D.A.; Visentin, I.C.; de Souza, F.M.A. Contabilidade de Custos Aplicada à Gestão Hospitalar Uma Revisão Teórica. Cost Accounting Applied to Hospital Management: A Theoretical Review. Humanidades Tecnol. Finom 2021, 29. Available online: http://revistas.icesp.br/index.php/FINOM_Humanidade_Tecnologia/article/view/1589 (accessed on 14 January 2024).

- Kaplanog, V. Application of activity-based costing to a land transportation company: A case study. Int. J. Prod. Econ. 2008, 116, 308–324. [Google Scholar]

- Quesado, P.; Silva, R. Activity-based costing (ABC) and its implication for open innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 41. [Google Scholar] [CrossRef]

- Pietrzak, Z.; Wnuk-Pel, T.; Christauskas, C. Problems with Activity-Based Costing Implementation in Polish and Lithuanian Companies. Eng. Econ. 2020, 31, 26–38. [Google Scholar] [CrossRef]

- Stratton, W.; Desroches, D.; Lawson, R.; Hatch, T. Activity-based costing: Is it still relevant? Manag. Account. Q. 2009, 10, 31–40. [Google Scholar]

- Askarany, D.; Yazdifar, H. Why ABC is Not Widely Implemented? Int. J. Bus. Res. 2007, 7, 93–98. [Google Scholar]

- Bornia, A. Análise Gerencial de Custos em Empresas Modernas; Bookman: Porto Alegre, Brazil, 2002. [Google Scholar]

- Kaplan, R.; Anderson, S. Time-Driven Activity Based Costing; Campus: Rio de Janeiro, Brazil, 2007. [Google Scholar]

- Fito, A.; Llobet, J.; Cuguero, N. The activity-based costing model trajectory: A path of lights and shadows. Intang. Cap. 2018, 14, 146–161. [Google Scholar] [CrossRef]

- Ouassini, I. An analysis of Panasonic Group in Terms of Activity—Based Costing, Justin-Time Production and Quality and Environment Costing. J. Oper. Manag. 2019, 18, 49–65. [Google Scholar]

- Gosselin, M. A Review of Activity-Based Costing: Technique, Implementation and Consequences. Handb. Manag. Account. Res. 2007, 2, 641–674. [Google Scholar]

- Rankin, R. The Predictive Impact of Contextual Factors on Activity-Based Costing Adoption. J. Account. Financ. 2020, 20, 66–81. [Google Scholar]

- Wegmann, G. A typology of cost accounting practices based on activity-based costing—A strategic cost management approach. Pac. Manag. Account. J. 2019, 14, 161–184. [Google Scholar] [CrossRef]

- Järvinen, J.; Väätäjä, K. Customer Profitability Analysis Using Time-Driven Activity-Based Costing: Three Interventionist Case Studies. Nord. J. Bus. 2018, 67, 27–47. [Google Scholar]

- Major, M.; Vieira, R. Activity-Based Costing/Management. In Contabilidade e Controlo de Gestão: Teoria, Metodologia e Prática; Major, M.J., Vieira, R., Eds.; Escolar Editora: Lisbon, Portugal, 2017; pp. 297–329. [Google Scholar]

- Major, M.; Hoque, Z. Activity-Based Costing: Concepts, Issues and Practice. In Handbook of Cost and Management Accounting; Hoque, Z., Ed.; Spiramus: London, UK, 2005; pp. 83–103. [Google Scholar]

- Foster, G.; Swenson, D. Measuring the success of activity-based cost management and its determinants. J. Manag. Account. Res. 1997, 9, 109–141. [Google Scholar]

- Stefano, N.; Lisbôa, M.; Casarotto Filho, N. Activity-Based Costing: Estado da Arte Proposta pelo Pesquisador e Revisão Bibliométrica da Literatura. Iberoam. J. Proj. Manag. 2012, 3, 1–22. [Google Scholar]

- Diehl, C.; Souza, M. Publicações Sobre o Custeio Baseado em Atividades (ABC) em Congressos Brasileiros de Custos no Período de 1997 a 2006. Rev. Contab. Vista E Rev. 2008, 1, 39–57. [Google Scholar]

- Barsanti, H.; Souza, A. Método de Custeio Baseado em Atividades: Uma Pesquisa Bibliométrica. Pensar Contábil 2018, 20, 44–54. [Google Scholar]

- Souza, A.; Avelar, E.; Boina, T. Custeio Baseado em Atividades: Uma Análise das Pesquisas Brasileiras Desenvolvidas na Primeira Década do Século XXI. Rev. De Informação Contábil 2016, 10, 1–19. [Google Scholar]

- Baldvinsdottir, G.; Mitchell, F.; Nørreklit, H. Issues in the relationship between theory and practice in management accounting. Manag. Account. Res. 2010, 21, 79–82. [Google Scholar] [CrossRef]

- Scapens, R.W. Understanding management accounting practices: A personal journey. Br. Account. Rev. 2006, 38, 1–30. [Google Scholar] [CrossRef]

- Spicer, B.H. The resurgence of cost and management accounting: A review of some recent developments in practice, theories and case research methods. Manag. Account. Res. 1992, 3, 1–37. [Google Scholar] [CrossRef]

- Bromwich, M.; Scapens, R.W. Management accounting research: 25 years on. Manag. Account. Res. 2016, 31, 1–9. [Google Scholar] [CrossRef]

- Kurunmäki, L. Management accounting, economic reasoning and the new public management reforms. In Handbook of Management Accounting Research; Chapman, C., Hopwood, A.G., Shields, M.D., Eds.; Elsevier Science: Amsterdam, The Netherlands, 2009; Volume 3, pp. 1371–1383. [Google Scholar]

- Peralta, H.; Costa, F.A. Competência e confiança dos professores no uso das TIC. Síntese de um estudo internacional. Sísifo 2016, 3, 77–86. [Google Scholar]

- Lutilsky, I.D.; Dragija, M. Activity based costing as a means to full costing—Possibilities and constraints for European universities. J. Contemp. Manag. Issues 2012, 1, 33–57. [Google Scholar]

- Carvalho, J.; Costa, T.C.; Macedo, N. A contabilidade analítica ou de custos no sector público administrativo. Rev. OTOC 2008, 96, 30–41. [Google Scholar]

- Valderrama, T.G.; Sanchez, R.D. Development and implementation of a university costing model. J. Public Money Manag. 2006, 26, 251–255. [Google Scholar] [CrossRef]

- Hernández, A.L.; Díaz, D.C.; Toledano, D.S.; Ramos, D.Á.; Angulo, J.G.; Armenteros, J.H.; Martínez, V.J. Livro Blanco de Los Costes en Las Universidades, 3rd ed.; Oficina de Cooperación Universitaria, S.A.: Madrid, Spain, 2010. [Google Scholar]

- Keel, G.; Savage, C.; Rafiq, M.; Mazzocato, P. Time-driven activity-based costing in health care: A systematic review of the literature. Health Policy 2017, 121, 755–763. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Porter, M.E. How to solve the cost crisis in health care. Harv. Bus. Rev. 2011, 89, 47–64. Available online: https://www.vbhc.nl/wp-content/uploads/2021/10/Robert-S.-Kaplan-Michael-E.-Porter-How-to-Solve-The-Cost-Crisis-In-Health-Care-Harvard-Business-Review-2011.pdf (accessed on 10 November 2023).

- Small, H. Co-citation in the scientific literature: A new measure of the relationship between two documents. J. Assoc. Inf. Sci. Technol. 1973, 24, 265–269. [Google Scholar] [CrossRef]

- Smiraglia, R.P. ISKO 11’s diverse bookshelf: An editorial. Knowl. Organ. 2011, 38, 179–186. [Google Scholar] [CrossRef]

- Bellardo, T. The use of co-citations to study science. Libr. Res. 1980, 2, 231–237. [Google Scholar]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E.; Tatham, R.L. Análise Multivariada de Dados; Bookman: Porto Alegre, Brazil, 2009. [Google Scholar]

- Cooper, R.; Kaplan, R.S. Measure costs right: Make the right decisions. Harv. Bus. Rev. 1988, 66, 96–103. [Google Scholar]

- Pernot, E.; Roodhooft, F.; Van den Abbeele, A. Time-Driven Activity-Based Costing for Inter-Library Services: A Case Study in a University. J. Acad. Librariansh. 2007, 33, 551–560. [Google Scholar] [CrossRef]

- Siguenza-Guzman, L.; den Abbeele, A.; Vandewalle, J.; Verhaaren, H.; Cattrysse, D. Using time-driven activity-based costing to support library management decisions: A case study for lending and returning processes. Libr. Q. 2014, 84, 76–98. [Google Scholar] [CrossRef]

- Kont, K.R.; Jantson, S. Cost accounting and managerial accounting for reducing the impacts of financial crisis in university libraries: The case of the Baltic states. Soc. Sci. 2012, 77, 88–96. [Google Scholar] [CrossRef][Green Version]

- Coney, D. Management in college and university libraries. Libr. Trends 1952, 1, 83–94. [Google Scholar]

- Gupta, M.; Galloway, K. Activity-based costing/management and its implications for operations management. Technovation 2003, 23, 131–138. [Google Scholar] [CrossRef]

- Cooper, R.; Kaplan, R.S. Activity-based systems: Measuring the costs of resource usage. Account. Horiz. 1992, 6, 1–13. [Google Scholar]

- Kaplan, R.S.; Anderson, S.R. Time-driven activity-based-costing. Havard Bus. Rev. 2004, 82, 131–138, 150. [Google Scholar] [CrossRef]

- McLaughlin, N.; Burke, M.A.; Setlur, N.P.; Niedzwiecki, D.R.; Kaplan, A.L.; Saigal, C.; Mahajan, A.; Martin, N.A.; Kaplan, R.S. Time-driven activity-based costing: A driver for provider engagement in costing activities and redesign initiatives. Neurosurg. Focus 2014, 37, E3. [Google Scholar] [CrossRef]

- Chan, Y.C.L. Improving hospital cost accounting with activity-based costing. Health Care Manag. Rev. 1993, 18, 71–77. [Google Scholar] [CrossRef]

- Laurila, J.; Suramo, I.; Brommels, M.; Tolppanen, E.-M.; Koivukangas, P.; Lanning, P.; Standertskjöld-Nordenstam, C.-G. Activity-based costing in radiology: Application in a pediatric radiological unit. Acta Radiológica 2000, 41, 189–195. [Google Scholar] [CrossRef]

- Cohen, M.D.; Hawes, D.R.; Hutchins, G.D.; McPhee, W.D.; LaMasters, M.B.; Fallon, R.P. Activity-based cost analysis: A method of analyzing the financial and operating performance of academic radiology departments. Radiology 2000, 215, 708–716. [Google Scholar] [CrossRef]

- Suthummanon, S.; Omachonu, V.K.; Akcin, M. Applying activity-based costing to the nuclear medicine unit. Health Serv. Manag. Res. 2005, 18, 141–150. [Google Scholar] [CrossRef]

- Baker, J.J. Activity-Based Costing and Activity-Based Management for Health Care; Jones & Bartlett Learning: Burlington, MA, USA, 1998. [Google Scholar]

- Lievens, Y.; van den Bogaert, W.; Kesteloot, K. Activity-based costing: A practical model for cost calculation in radiotherapy. Int. J. Radiat. Oncol. Biol. Phys. 2003, 57, 522–535. [Google Scholar] [CrossRef]

- Edbrooke, D.L.; Stevens, V.G.; Hibbert, C.L.; Mann, A.J.; Wilson, A.J. A new method of accurately identifying costs of individual patients in intensive care: The initial results. Intensive Care Med. 1997, 23, 645–650. [Google Scholar] [CrossRef]

- Laviana, A.A.; Ilg, A.M.; Veruttipong, D.; Tan, H.J.; Burke, M.A.; Niedzwiecki, D.R.; Kupelian, P.A.; King, C.R.; Steinberg, M.L.; Kundavaram, C.R.; et al. Utilizing time-driven activity-based costing to understand the short-and long-term costs of treating localized, low-risk prostate cancer. Cancer 2016, 122, 447–455. [Google Scholar] [CrossRef]

- Ellis-Newman, J. Activity-based costing in user services of an academic library. Libr. Trends 2003, 51, 333–348. [Google Scholar]

- Marlina, E.; Tjahjadi, B.; Ningsih, S. Factors affecting student performance in e-learning: A case study of higher education institutions in Indonesia. J. Asian Financ. Econ. Bus. 2021, 8, 993–1001. [Google Scholar]

- Kawamoto, T.; Ura, T.; Nittono, H. Intrapersonal and interpersonal processes of social exclusion. Front. Neurosci. 2015, 9, 62. [Google Scholar] [CrossRef]

- Van de Werf, E.; Verstraete, J.; Lievens, Y. The cost of radiotherapy in a decade of technological evolution. Radiother. Oncol. 2012, 102, 148–153. [Google Scholar] [CrossRef]

- Mitchell, G.J. Clarifying the contributions of qualitative research findings. Nurs. Sci. Q. 1996, 9, 143–144. [Google Scholar] [CrossRef]

- Cropper, P.; Cook, R. Developments: Activity-Based Costing in Universities—Five Years On. Public Money Manag. 2000, 20, 61–68. [Google Scholar] [CrossRef]

- Goddard, A.; e Ooi, K. Custeio baseado em atividades e alocação central de custos indiretos em universidades: Um estudo de caso. Dinheiro Público Gestão 1998, 18, 31–38. [Google Scholar]

- Kont, K.-R. How to optimize the cost and time of the procurement process? Collect. Build. 2015, 34, 41–50. [Google Scholar] [CrossRef]

- Kont, K. How much does it cost to catalog a document? A case study in Estonian university libraries. Cat. Classif. Q. 2015, 53, 825–850. [Google Scholar] [CrossRef]

- Kont, K.-R. What do acquisition activities really cost? A case study in Estonian university libraries. Libr. Manag. 2015, 36, 511–534. [Google Scholar] [CrossRef]

- Kont, K.-R. To buy or to borrow? Evaluating the cost of an eBook in TalTech library. Bottom Line 2020, 33, 74–93. [Google Scholar] [CrossRef]