3. Financing Bottlenecks Faced by Green Technology Investments

Green technologies are emerging technologies that reduce energy consumption, pollution, and carbon emissions and improve ecology.

The green technology innovation system covers energy conservation and environmental protection, clean production, clean energy, ecological protection and restoration, infrastructure, ecological agriculture, and other fields, as well as product design, production, consumption, and recycling.

In terms of actors, the components of the green technology innovation system mainly include enterprises, research institutions, the government, and financial institutions.

The enterprises are the main body of green technology innovation and are the demanders, initiators, and implementers of green technology innovation. Research institutions are important intellectual providers of green technology innovation.

A good interaction between research institutions and enterprises is an important support for green technology innovation. The government is the incentive and beneficiary of green technology innovation.

On the one hand, the government’s incentive policies and mechanisms can largely promote the participation of green technology enterprises, research institutions, and financial institutions in green technology innovation, and on the other hand, green technology innovation is also conducive to the construction of ecological civilization and sustainable development at all levels of government.

Green technology innovation is also conducive to the realization of the objectives of ecological civilization and sustainable development by governments at all levels.

Although the government has issued several policy documents to support green technology innovation, at present, green technology investment by enterprises in China is still insufficient.

For example, the China Environmental Protection Industry Association (CEPIA), published in 2018, shows that The R&D expenditure of nearly 10,000 environmental protection enterprises that were surveyed accounted for 3.0% of their business revenue: a slight increase from the previous year [

15].

This is slightly higher than the level of R&D expenditure of industrial enterprises above the national scale but still lower than the average of 3.8% in developed countries [

16]. For example, in Germany, the R&D expenditure of environmental manufacturing enterprises is generally 4% of their operating income [

17]. Another example is the UK’s low-carbon and environmental service companies in the UK invest, which obtains about 5% of its total revenue in R&D [

18].

The long lead time from R&D to economic benefits is a challenge for smaller enterprises or those with little experience in innovation. The market will be eliminated more quickly and easily if they choose to invest in green technology projects with no short-term returns [

11]. There are several reasons for the lack of investment in green technology in China.

This study focuses on the financing bottlenecks faced by green technology enterprises. These bottlenecks are manifested as follows.

- (i)

Difficulty in obtaining adequate financing from traditional sources such as banks

On the one hand, the greenest technology innovation enterprises are small and medium-sized private enterprises with light assets, lacking collateral assets, while bank loans generally require collateral.

On the other hand, the greenest technology projects have a long investment cycle (some as long as 5–10 years), but the average maturity of traditional bank credit in China is only 2–3 years.

The problem makes it difficult for green technology companies to obtain adequate financing through traditional financial markets, especially from bank loans [

13]. In addition, bond markets generally only provide financing for more mature, larger, and lower-risk enterprises and therefore are not suitable for small and medium-sized green technology enterprises.

Some banks also support high-technology companies. For example, investment-lending products can help address the financing needs of green technology enterprises. However, the amount of capital available to them is still too large compared to the overall large number of SMEs.

The amount of capital available to small and medium-sized green technology enterprises through internet finance companies (P2P) and industrial finance companies is still too small compared to bank loans. It cannot be used as a source of funding for medium to long-term technology investment projects.

- (ii)

Access to finance through private equity and venture capital

In general, the main sources of external financing for technology businesses should include private equity (PE) and venture capital (VC). However, many green technology companies still have immature business models, a limited market size, and low project yields, and there is a significant difference in risk appetite between private equity (PE) and venture capital (VC) investors in China. There are also significant differences in the risk appetite of domestic private equity (PE) and venture capital (VC) investors.

The investment hotspots of domestic PE/VC in recent years have mainly focused on the Internet, biopharmaceuticals, finance and logistics, and transportation industries, with limited investment in green technology. In the first half of 2018, PE/VC investments in new energy and energy conservation and environmental protection accounted for only 0.81% of all PE/VC investments in the sector [

10].

However, in Europe and the US, green technology companies have become a core focus and a new growth area for many large and mid-sized PE/VC funds.

The International Finance Corporation study [

19] reported that US PE/VC investors invested USD49 billion in sustainable technology between 2006 and 2018, compared to USD20 billion in Europe and Asia during the same period.

An important factor that seriously discourages domestic PE/VC from investing in green technology companies is the mismatch of investment maturity and excessive investment risks.

In terms of investment duration, most domestic PE/VC funds have a duration of 5–7 years, while many green technology companies need a growth period of 7–10 years to reach the IPO (lock-in period) threshold.

The growth period for many green technology companies to reach the threshold of IPO is 7–10 years, so funds in China have difficulty favoring technology companies. In contrast, the duration of PE/VC funds in the US is generally around 10 years. An important reason for this difference is that the major investors (LPs) of PE/VC funds in Western countries are pension funds, insurance companies, and other investors.

By contrast, in China, these sources of long-term capital are severely lacking, with many PE/VC investors belonging to enterprises and trusts that rely on the issuance of short and medium-term financial products to raise funds companies, bank wealth management companies, securities company capital management plans, etc.

In addition, as the greenest technology companies are in their formative years and product development phase, their commercial sustainability and return recognition takes longer, are more costly, and the unpredictability of downstream consumer preferences and product revenues poses significant market risks, making many PE/VC funds discouraged.

The long investment period, high risk, and illiquidity of the project are not in line with the investment preference of PE/VC in China, resulting in such enterprises not being well placed to obtain sufficient and stable sources of capital through this channel.

- (iii)

Green projects face a variety of specific industry risks

Many projects using green technologies, due to their technical characteristics, were exposed to risks that are not present in other industries. For example, photovoltaic and wind power face the risk of uncertainty about sunshine hours and wind power, and green buildings face the risk that the technology used will meet energy and water conservation standards.

Many forms of environmental and energy-efficient equipment are at risk of unstable performance.

If users are overly concerned about these risks and there is a lack of risk management tools, this can lead to a lack of demand and thus limit the use and diffusion of green technologies.

Due to the lack of relevant definitions or certification standards for green technologies, some enterprises may engage in “greenwashing”, i.e., they claim to spend money on green technology innovation, but in fact, the relevant technology is not green.

This is the case when companies claim to be using funds for green technology innovation, but in reality, the technology does not generate new environmental benefits but is financed under the guise of green technology [

20].

The causes of ‘green washing’ include a lack of green technology standards and certification and disclosure requirements [

21]. Although China has introduced green credit, green bonds, and green industry definition standards, the country has not been able to meet these standards.

The criteria for green technologies should enable PE and VC investment institutions that focus on investing in green technologies to easily define and identify their investment targets.

The current lack of standards does not allow third-party organizations to use them as a basis for green technology certification, including the quantitative assessment of the environmental benefits of green technology projects.

As a result of the above-mentioned “greenwashing” risks, investors have difficulty identifying potential and legitimate incentives to invest in green technology companies, or the identification process entails significant additional costs for investors. This is one of the reasons for the current difficulties in financing green technology companies.

- (iv)

Lack of policy incentives for investment in green technologies

To promote green technology innovation and the development of green technology enterprises, which are the main market-based mechanisms and social capital support, relevant policy incentives are also important [

22]. Policy incentives, including fiscal incentives and tax breaks, can, on the one hand, provide direct incentives for green technology development.

On the other hand, they can play a leveraging role, giving a positive signal to the market, guiding private and social capital to enter the green technology sector, and using limited government resources to leverage huge market resources to support the development of green technology enterprises.

While China has introduced several incentives to support green credit and bonds (such as green refinancing, green project guarantees, and interest subsidies), they are mainly used to support projects using traditional or mature technologies, while early to mid-stage green technology companies, and projects have had difficulty in obtaining loans and bond financing.

In addition, China’s local carbon market has limited coverage, and a national carbon market has not yet been launched, so it does not provide incentives for most small and medium-sized low-carbon technology enterprises.

4. Suggestions for Strengthening Financial Support for Green Technology Innovation

It was pointed out in the previous analysis that although China’s financial sector has already made several innovations in green technology support, China’s green technology financing of innovation still faces a series of barriers. We believe that to solve the problems faced by green technology development, it is necessary to have a financial services system that effectively supports green technology enterprises.

The system should include the following features:

- (1)

A multi-level financing and risk management model, including the stock market, PE/VC, investment-lending linkages, guarantees, and insurance mechanisms, to address the reluctance of banks to provide financing to green technology enterprises.

- (2)

The government should provide certain incentives, including incubation, guarantees, and interest subsidies, to reduce the financing costs and risk premiums of green technology enterprises and alleviate the environmental externalities of green projects.

- (3)

Provide funds with longer terms to meet the long return cycle of some green technology projects.

- (4)

Establish a set of criteria for defining green technology and green PE/VC funds and environmental benefit assessment criteria, and use digital technology to enhance green assessment capabilities and reduce assessment costs.

Based on the above ideas, we propose the following specific recommendations.

- (i)

Encourage banking and financial institutions to develop investment and lending activities for green technology innovation

As banks’ funds come from customers (e.g., depositors or bond investments) (the “risk-averse”) and are therefore less tolerant of risk, traditional banks are generally reluctant to willingly become involved in lending for technology-based, riskier projects.

The banks, which manage the largest proportion of funds in our financial system and account for around 80% of all social finance, should find appropriate and manageable ways to participate in supporting green technologies.

We suggest that banks should be encouraged to launch pilot investment-lending initiatives in the green technology sector. The green investment-lending linkage refers to the joint support of green technology projects by banks and experienced PE/VC funds or equity investment subsidiaries within a bank group. The PE/VC fund can provide equity financing, and the bank can provide matching loans.

Under this model, the bank can avoid investment mistakes due to the lack of professional staff within the bank. At the same time, external or internal equity institutions, as equity investors, take on greater risk (and enjoy higher future returns), reducing the bank’s risk in these projects [

23].

In April 2016, the former CBRC made investment-lending linkages one of its priorities, and jointly with the Ministry of Science and Technology and the People’s Bank of China, issued the “Guidance on Supporting Banking Financial Institutions to Increase Innovation and Launch Pilot Projects for Science and Innovation Enterprises”. According to the opinions, credit placement was to be conducted by commercial banks, while the main body of equity financing could be provided by external venture capital institutions (PE/VC) or subsidiaries within the commercial bank group with investment qualifications or industry.

The former is called internal investment-lending linkage, while the latter is called external investment-lending linkage.

There are many domestic and international examples of investment-lending linkages. For example, the Silicon Valley Bank, which was established in 1980, specializes in providing comprehensive financial services to small and medium-sized technology-based innovative companies.

The Silicon Valley Bank provides patent loans to technology companies with fewer fixed assets and more patents. Silicon Valley Capital generally invests in these technology companies in conjunction with other venture capital institutions.

In this model, when the Silicon Valley Bank makes a loan, the Silicon Valley Financial Group also receives a portion of the company’s equity or options. The Silicon Valley Bank Group uses warrants to compensate the bank for some of the credit risks it faces.

In practice, in China, China Merchants Bank, Nanjing Bank, Bank of Beijing, Industrial Bank, Minsheng Bank, etc., have launched pilot investment-lending linkages. These banks’ investment-lending linkages are mainly conducted in two modes. The first is the bank + PE/VC/brokerage model, which provides loans and financing for enterprises.

The second is the bank + investment subsidiary model, i.e., direct investment business through the investment subsidiary of a banking group and linking with the bank’s lending business [

24].

Some of the investment-lending projects have involved new energy, energy conservation, environmental protection, and other green areas (for example, the strategic cooperation between China Merchants Bank and SLARZOOM PV Billion, and the energy-saving and environmental protection projects in which Minsheng Bank’s “Qixing” is involved).

However, on the whole, the projects of investment-lending linkage are mainly in medical health, high-end equipment manufacturing, internet application, etc. Not many green technology projects have been supported by the linkage.

Figure 1 shows the causes of problems between investment and lending:

In the future, to strengthen the investment-lending business in the green technology sector, banks should

- (1)

Encourage banks’ internal equity investment subsidiaries and external PE/VC investment management companies to establish professional teams to track green technologies, including the establishment of green technology sub-branches of banks.

- (2)

Cooperate with local green technology incubators and industrial parks to provide incubation and services to small and medium-sized green technology enterprises in the process of investment and loan linkage.

- (3)

Combine the green financial incentives provided by the central bank and local governments (including the People’s Bank of China’s green refinancing loans, rediscounts, and local government subsidies and guarantees) and the green investment and loan linkage business to reduce the financing cost and credit risk of the investment and loan linkage business.

This will reduce the financing cost and credit risk of the investment-lending business.

- (ii)

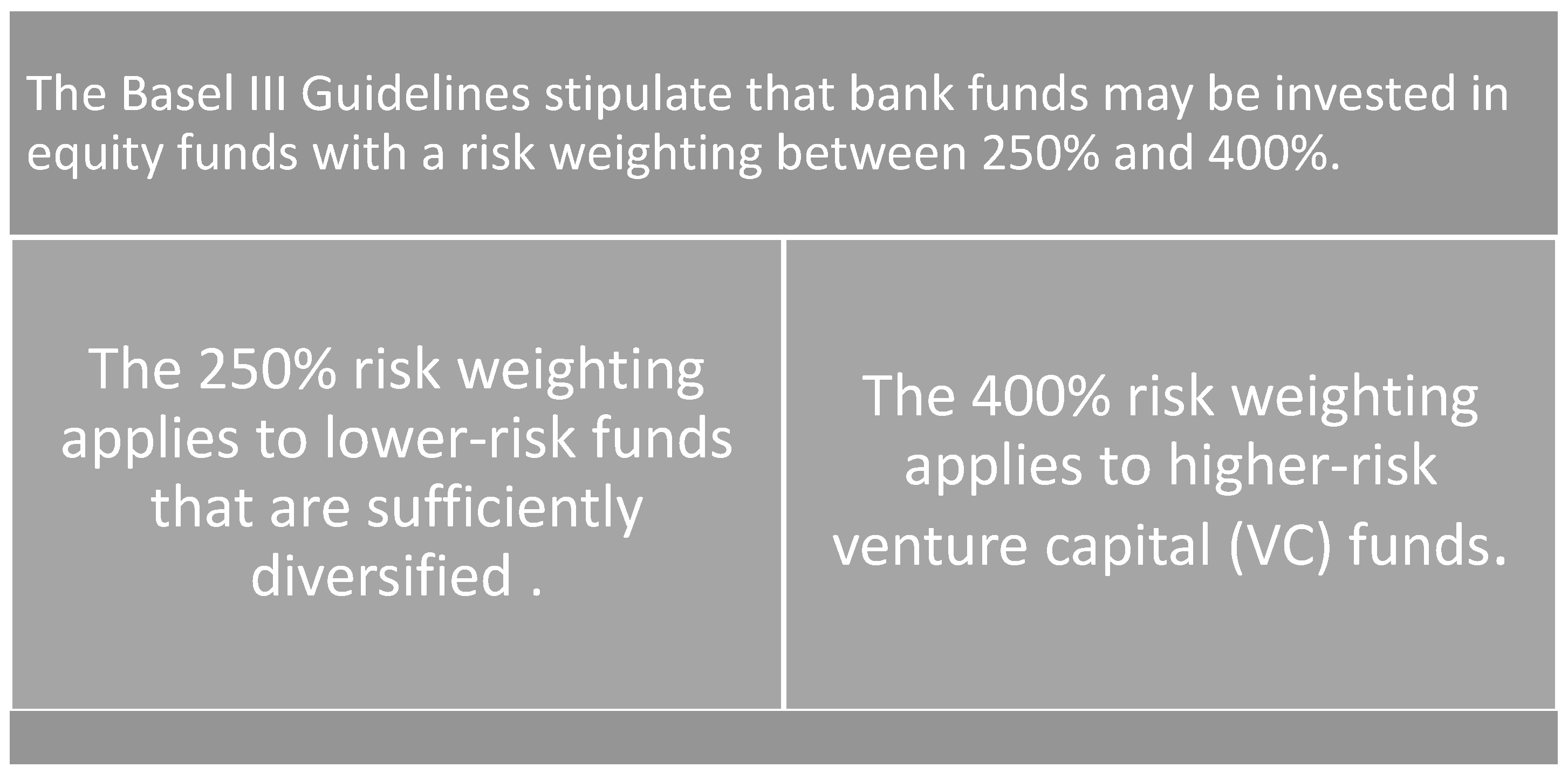

Supporting banks to invest in green funds under the new Basel III regulations on a pilot basis green funds

Currently, banks hold the largest amount of capital in the financial system but are largely uninvolved in technology investments, including green technology investments. The main reason for this is that traditional banking regulatory requirements have largely prevented banks from participating in equity investments.

However, the latest Basel III rules [

14] released in 2017 already allow banks to participate in equity funds with a risk weighting of 250–400%.

Chinese institutions have not yet started to pay attention to and use this reform. We suggest that Basel III rules should be explored.

The Basel III provision, which allows banks to invest in diversified equity assets with a 250 percent risk weighting, should be explored in a pilot program for the green technology industry in China to encourage pilot banks to invest in a risk-controlled manner. The pilot banks are encouraged to invest in professionally managed green equity funds on a risk-controlled basis (e.g., more than 0.5% of the bank’s total assets and with sufficient diversification).

Figure 2 shows the main foundations of Basel III:

Banks in the UK, Europe, and Canada have started to experiment with this type of equity investment in SMEs and have achieved good returns with adequate control and risk diversification. We estimate that, with a risk weighting of 250%, banks can achieve a return on the capital invested in such funds.

As a result, as long as national (and regional) banking supervisors issue implementing rules in line with the Basel rules, there will be a strong incentive for many banks (which will not need to be mobilized but will ask to join) to participate in such funds.

There is a strong incentive for banks to participate in this type of investment, and the establishment of a larger green fund would not require financial contributions from the government. We suggest that a pilot project based on this new regulation is launched in some banks to set up a green fund, part of which could be invested in green technology companies.

- (iii)

Support and nurture private equity and venture capital institutions that focus on investing in green technologies

The lack of professional green PE/VC fund management institutions is a major bottleneck for green technology investment in China at this stage. According to the statistics of the Association, there are currently more than 500 funds registered with the Association under the name of green technology.

The majority of these funds invest in green-listed companies and green projects using mature technologies. We are aware of only a few funds in China that focus on green, clean, or environmental technologies.

In the future, with the intensification of the global climate change strategy and deepening of China’s green development strategy, more and more investors will recognize that there will be greater incentives for green and low-carbon projects in the future (e.g., carbon prices may increase several times or more than ten times in the future, and various tax and green financial incentives will be gradually put in place).

The share of green technologies in the green economy and green investments is bound to increase significantly. Therefore, the future will require not a few but dozens or hundreds of green technology funds. The lack of qualified and experienced green technology fund administrators is a major bottleneck in the development of green technology. To alleviate this bottleneck, we have the following suggestions.

- (1)

The Government should consciously foster green technology venture capital funds, allocate some of the government industrial funds (mother funds) managed by funds to green technology funds to help them build up quality teams and performance, and provide appropriate incentives (e.g., rent waivers, etc.). The green technology innovation fund should be a priority area of support [

25].

- (2)

Encourage banks and industrial fund management institutions to strengthen the capacity building of green investment and support the development of green master funds. Encourage institutional investors to incorporate green investment principles into their investment decision-making process and transform some existing industrial funds into green technology funds. Capacity training for relevant personnel on methods and tools to identify green projects, quantify environmental benefits, disclose environmental information, etc., and enhance their ability to make green investments.

- (3)

Encourage and guide existing fund management teams (not focused on green technology) to shift to the green technology sector by providing a pool of green projects.

- (4)

Support the listing and financing of enterprises invested in the Green Technology Fund, such as giving priority and recommendations to green enterprises to be listed on the GEM under the same conditions.

- (iv)

Encourage insurance companies to develop insurance products that support green technology innovation and green products

One challenge faced by many green technology projects during commercialization is that these technologies and applications face greater market or technical risks. For example, photovoltaic and wind power projects face uncertainties during sunshine hours and when there is a lack of wind power (resulting in uncertain returns).

The insurance institutions should further develop and promote products that support green buildings, clean energy, green transportation, environmental technology and equipment, green agriculture, etc. In addition to providing risk cover for market or technical risks faced by buyers of green technologies, it is recommended that insurance companies innovate to provide risk cover for green technologies.

The insurance companies should cooperate with third-party organizations, integrate risk management resources, strengthen research on the risks faced by green technology projects, enhance the professional service capacity building, and try out “insurance + service”. The insurance solution covers the entire life cycle of the project and includes a package of risks.

Green technology projects face a variety of uncertainties in the eyes of traditional financial institutions. The company’s approach to financing is pledging one’s intellectual property rights to obtain financing, which is a good way for green technology companies to obtain the money they need. This is an option that can be explored by green technology companies. It is recommended that the financial sector should be more closely linked, and insurance companies should work more closely with banks to improve the risk-sharing mechanism.

The risk-sharing mechanism should be improved through the provision of a pledged intellectual property financing guarantee insurance to jointly support green technology innovation.

In the face of the risks associated with green technology innovation, green technology enterprises are generally reluctant to take the initiative to take out the relevant insurance due to lack of awareness, because they are lucky, or due to cost considerations.

To cultivate enterprises’ awareness of the risks and insurance, better use of insurance mechanisms to prevent and control risks, enhance market credit, promote technology diffusion, and increase the efficiency of financial resources, is recommended so that government departments can improve the green finance incentive policy, subsidize the premiums for green technology enterprises to take out relevant technology insurance policies, issue a list of green technology enterprises and insurance policies that are eligible for subsidies, and specify the proportion of subsidies to promote the increase in insurance coverage.

The insurance company has strong bargaining power as an institution and can obtain products and services at reasonable costs and in line with quality standards. It is recommended that insurance companies innovate their business models and try to integrate green technologies and products into their solutions for their clients to increase the purchase of products from green technology suppliers and promote the use of green technologies.

The use of green technologies and products should be promoted on a large scale. For example, the use of green technology and green products in the repair of damaged vehicles for car insurance customers should be maximized.

- (v)

Encourage long-term funds such as insurance and pension funds to invest in green PE/VC funds.

For some reason, the payback period of green technology projects may be slightly longer than that of projects in other industries. These reasons include the fact that some important green projects involve newer technologies and require a period to develop a market. The short-term availability of incentives, means that many carbon-reducing enterprises have not yet been included in the carbon trading mechanism and will not be able to reap the benefits of carbon sinks in the short term but will be able to do so in the long term.

The initial investment of some green projects (compared with non-green projects in the same industry) is larger, and the investment return is more likely to be low then high.

At present, most PE/VC funds in China are funded by government-led funds and listed companies. The incentives of these institutions are generally not inclined to support green technology funds with a longer duration (e.g., nine years).

For example, the government generally emphasizes assessing the annual performance of the funds, and listed companies also tend to look at annual profits.

To address the maturity mismatch between long-term capital needs and short-term funding sources faced by green technology innovation enterprises, we suggest that the government should encourage and support long-term funds such as pensions and insurance to participate in the creation and investment of green technology innovation companies with a longer lifespan.

We recommend that the government should encourage and support the participation of long-term funds such as pensions and insurance in creating and investing in green technology funds with a longer duration (e.g., nine years or longer). The relevant government and regulatory authorities can clarify this intention through documents and regulations.

The relevant government and regulatory authorities can clarify this intention in the form of documents and regulations for the National Council of Social Security Funds (NCSSF) and insurance institutions to invest in green technology funds.

- (vi)

Provide guarantees and other types of risk compensation for green technology innovation enterprises.

The national financing guarantee fund, provincial government financing guarantee institutions, and municipal and county government financing guarantee institutions have been established.

The governmental financial guarantee system, which is linked by equity investment and re-guarantee, has been initially formed with the national financial guarantee fund, provincial governmental financial guarantee institutions, and municipal and county-level governmental financial guarantee institutions.

This system is quasi-public in nature and is based on the principles and aims of alleviating the problems of small businesses.

The aim is to support small and micro enterprises in “three rural areas”, and entrepreneurial and innovative enterprises by mobilizing funds from various sources. However, there are currently no initiatives that focus on supporting loans for guaranteed green technology projects.

There are no policy measures and institutional arrangements that are in line with the characteristics of green enterprises, such as guarantee terms and periods, premium pricing and subsidies, technology incentives and subsidies, credit information system alignment, equity, and risk consideration arrangements, etc.

We suggest that the scope of support for the green technology industry should be clarified as part of the government financing guarantee system. The policy measures and institutional arrangements for guaranteeing support to green technology enterprises should be refined according to the characteristics of green enterprises in terms of capital needs, maturity, and costs.

In addition, there should be support and encouragement for the establishment of a green technology industry guarantee fund and commission professional guarantee institutions to pilot and test green technology enterprise guarantee and investment services to create the conditions for the active, successful, and effective transformation of national green technology results.

We suggest that the newly established National Financial Guarantee Fund should include green technology innovation as one of its key areas of support.

Figure 3 shows the main reasons for the importance of green technology innovation.

The National Guarantee Fund can act as an LP and co-finance with local governments to launch local guarantee funds. In recent years, the frequency of defaults by private enterprises in China has been significantly higher than in previous years.

Under such circumstances, the National Financial Guarantee Fund has increased its support for green technology enterprises. This will not only promote green transformation but also play a positive role in stabilizing national growth and employment.

- (vii)

Support local governments, social capital, and foreign investors to set up green technology incubators and industrial parks

Tens of thousands of technology incubators have been established in China. However, there are still very few incubators and industrial parks that focus on green technology.

Green technology innovation incubators and industrial parks should provide one-stop services and preferential policies on taxation and rent for green technology enterprises, attracting international capital and advanced green technology.

A sound system of soft services, including accounting, legal, information, financing, insurance, marketing, business management consultancies, etc, should be established.

A team of incubator managers with experience in product development, project management, marketing, and business management, and professionals should provide “business coaching”. The Green Technology Industrial Park can be an extension of the incubator, providing a larger space with marketing and management services.

- (viii)

Digital technology to provide green products, technologies, and assets: Certification, labeling, and evaluation services

An important feature that distinguishes green projects from other projects is that they must have environmental benefits, such as reduced pollutants. However, the identification, quantification, certification, and disclosure of these environmental benefits are often difficult or costly. For example, to quantify the environmental benefits, it is necessary to identify, quantify, certify, and disclose the environmental benefits of green technologies.

These quantitative analyses can involve a large number of technical parameters, models and formulas, and reference standards. After the investment, the actual environmental benefits of the project need to monitor the actual environmental benefits generated by the project, often requiring a significant investment in manpower and costly monitoring equipment. In the past, there has been a lack of certification and labeling to obtain market recognition of the “green benefits” of products.

As technologies such as big data, artificial intelligence, the internet of things, and blockchain become more sophisticated, it will become easier and easier to certify, label, and evaluate the environmental benefits of green technologies cost-effectively.

For example, satellite remote sensing technology can be used to monitor companies’ various pollutants and carbon emissions and IoT technologies can be used to monitor organic agricultural products throughout their production, processing, and transport, and smart meters can provide efficient, real-time monitoring of the energy efficiency of green buildings and green appliances, etc. In the future, the use of these digital technologies in green financing should be strongly promoted to help investment institutions capture the environmental benefits of their portfolio companies and projects at a lower cost. These technologies can also be used to create a ‘green asset exchange’ to trade environmentally (e.g., carbon-reducing distributed photovoltaic, forestry assets, etc.).

- (ix)

Establishing green standards and environmental information disclosure systems for PE/VC

Greenwashing” is an important risk that needs to be prevented in the green financial system. The so-called “greenwashing” refers to the practice of enterprises obtaining green financing (e.g., green credit, green bonds, and green finance) in the name of investing in green projects.

In terms of investment, for all types of green financial products, there is a need to guard against the risk of ‘greenwashing’.

In the area of green credit and green bonds, the relevant regulators have introduced green standards, environmental benefit calculation methods, and environmental benefit disclosure standards. However, in the PE/VC sector, there is no clear definition of green PE/VC, nor are there any environmental benefits and disclosure requirements for the projects invested.

We recommend that the CCSF refer to the Ministry of Science and Technology’s Catalogue of Support for Green Industries and the National Development and Reform Commission’s Guidance Catalogue for Green Industries (9th edition).

The design should take into account the recommendations of the TCFD (Climate-Related Financial Disclosure Group).

- (x)

Establish criteria for defining green technologies.

International organizations and developed countries have developed some green technology standards. However, most of these standards are set by developed countries according to their production levels and technology levels.

We suggest that, based on the Ministry of Science and Technology’s “Guidance on Building a Market-oriented Green Technology Innovation System” and in conjunction with the construction of a unified green financial standard system in China [

26], in-depth research should be conducted on the general standards for green technologies in China, and in the area of ecological and environmental pollution.

It should be ensured that the standards for these green technology projects and green technology enterprises can promote fair competition in the market as well as the evaluation and verification of the effectiveness of green technology. This will provide the financial market and financial institutions with a reasonable and practical way to support the development of green enterprises and green technology innovation.

The green technology enterprise standard can promote fair competition in the market and be effectively compatible with international rules.

This will provide the financial market and financial institutions with a reasonable and reliable green project assessment and recognition system to support the development of green enterprises and green technology innovation and facilitate the sustainable development of green technology innovation.

{kind=link}

{kind=link}

{kind=link}