Discussing EU Policies and Mechanisms towards the COVID-19 Pandemic Crisis: A Case Study of Greece

Abstract

1. Introduction

2. Previous Research

2.1. Is a Tight Fiscal Policy Effective?

2.2. Fiscal Policy—More Flexible, or Tighten?

2.3. Fiscal Rules in the EMU: Two Sides of the Same Coin

2.4. The EU Economic Bazooka: Escape Clause, SURE Programme & NGEU

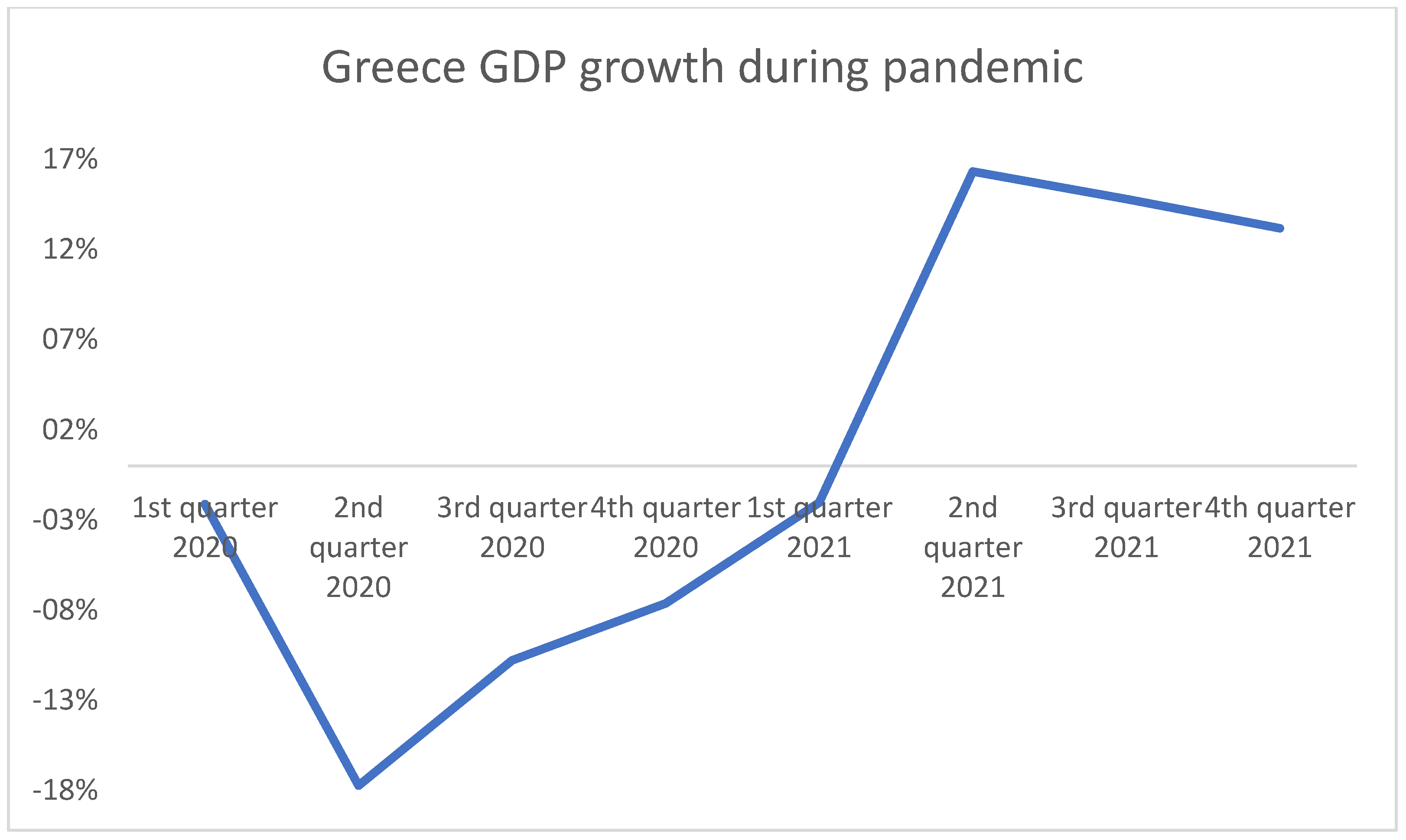

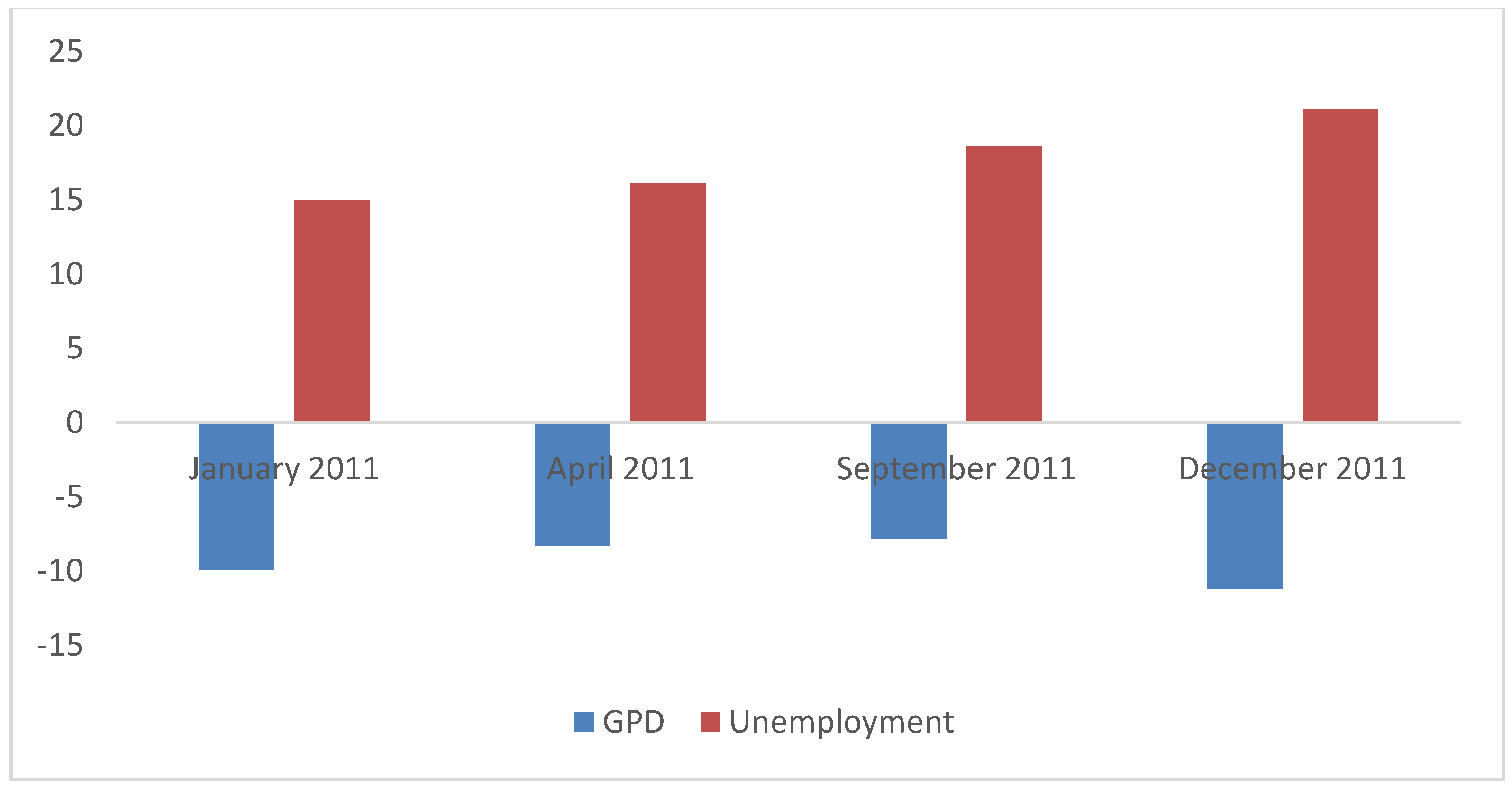

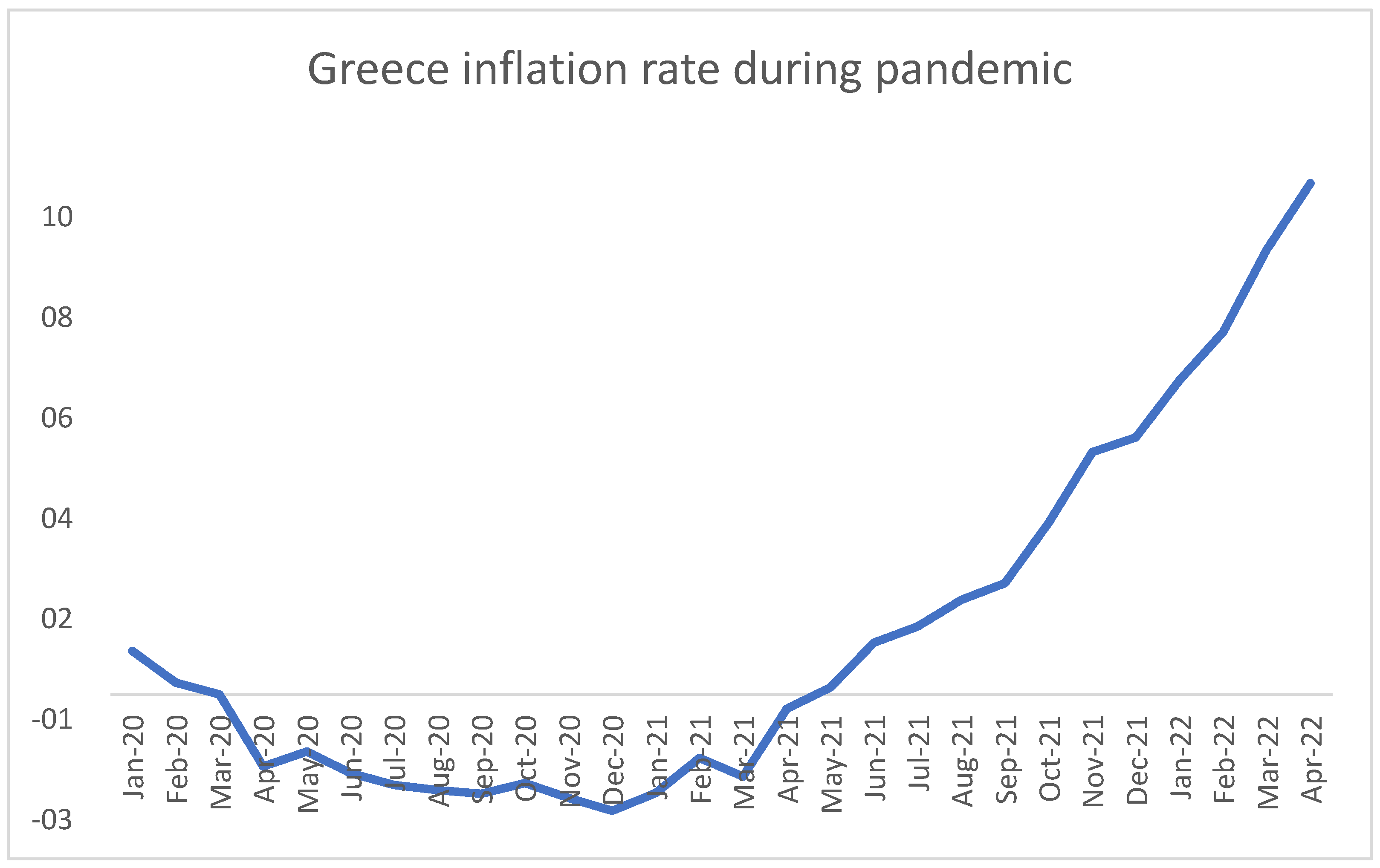

3. The Case of Greece

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Barro, R. Government spending in a simple model ofendogeneous growth. J. Political Econ. 1990, 98 (Suppl. S5), 103–125. [Google Scholar] [CrossRef]

- Arestis, P.; Sawyer, M. The Design Faults of the Economic and Monetary Union. J. Contemp. Eur. Stud. 2011, 19, 21–32. [Google Scholar] [CrossRef]

- Barnett, A.H. The Pigouvian Tax Rule Under Monopoly. Am. Econ. Rev. 1980, 70, 1037–1041. [Google Scholar]

- Werning, I. Managing a Liquidity Trap: Monetary and Fiscal Policy; NBER Working Paper 17344; NBER: Cambridge, MA, USA, 2011. [Google Scholar]

- Pirrong, C. Apocalypse Averted: The COVID-Caused Liquidity Trap, Dodd-Frank, and the Fed. J. Appl. Corp. Financ. 2020, 32, 44–48. [Google Scholar] [CrossRef]

- Lhuissier, S.; Mojon, B.; Ramírez, J.R. Does the Liquidity Trap Exist? Bank for International Settlements: Basel, Switzerland, 2020. [Google Scholar]

- Foster, J.; Frierman, M. Learning Rational Expectations: Classical Conditions Ensure Uniqueness and Global Stability. Economica 1990, 57, 439–453. [Google Scholar] [CrossRef]

- Kotios, A.; Roukanas, S. The political economy of the Greek health sector and the implications of the economic crisis. Eur. Polit. Soc. 2021, 23, 532–574. [Google Scholar] [CrossRef]

- Liargovas, P.; Pilichos, V. Is EU Fiscal Governance Effective? A Case Study for the Period 1999–2019. Economies 2022, 10, 187. [Google Scholar] [CrossRef]

- Charles, P. Understanding Real Business Cycles. J. Econ. Perspect. 1989, 3, 51–77. [Google Scholar]

- Friedman, M. Monetary Policy: Theory and Practice. J. Money Credit. Bank. 1982, 14, 98–118. [Google Scholar] [CrossRef]

- Friedman, M. Monetary policy with a credit aggregate target. Carnegie-Rochester Conf. Ser. Public Policy 1983, 18, 117–147. [Google Scholar] [CrossRef]

- Mundell, R. A Theory of Optimum Currency Areas. Am. Econ. Rev. 1961, 54, 657–665. [Google Scholar]

- Caporale, G.M.; Pittis, N.; Prodromidis, K. Is Europe an Optimum Currency Area? Business Cycles in the EU. J. Econ. Integr. 1999, 14, 169–202. [Google Scholar]

- Abad, P.; Chuliá, H.; Gómez-Puig, M. EMU and European government bond market integration. J. Bank. Financ. 2010, 34, 2851–2860. [Google Scholar] [CrossRef]

- Wong, P.K.; Ho, Y.P.; Autio, E. Entrepreneurship, Innovation and Economic Growth: Evidence from GEM Data. Small Bus. Econ. 2005, 24, 335–350. [Google Scholar] [CrossRef]

- Dornbusch, R. The New Classical Macroeconomics and Stabilization Policy. Am. Econ. Rev. 1990, 80, 143–147. [Google Scholar]

- Minniti, M. The Role of Government Policy on Entrepreneurial Activity: Productive, Unproductive, or Destructive? Entrep. Theory Pract. 2008, 32. [Google Scholar] [CrossRef]

- McCallum, B. New Classical Macroeconomics: A Sympathetic Account. Scand. J. Econ. 1989, 91, 223–252. [Google Scholar] [CrossRef]

- Buiter, W.H. “Crowding out” and the effectiveness of fiscal policy. J. Public Econ. 1977, 7, 309–328. [Google Scholar] [CrossRef]

- Afonso, A.; Aubyn, M.S. Macroeconomic Rates of Return of Public and Private Investment Crowding in and Crowding-Out Effects; European Central Bank (ECB): Frankfurt, Germany, 2008. [Google Scholar]

- Baum, A.; Koester, G.B. The Impact Offiscal Policy Oneconomic Activity over the Business Cycle—Evidence from a Threshold VAR Analysis; Deutsche Bundesbank: Frankfurt, Germany, 2011. [Google Scholar]

- Schuetze, H.J.; Bruce, D. Tax Policy and Entrepreneurship; Economic Council of Sweden: Stockholm, Sweden, 2004. [Google Scholar]

- Trabandt, M.; Uhlig, H. The Laffer curve revisited. J. Monet. Econ. 2011, 58, 305–327. [Google Scholar] [CrossRef]

- Marangos, J. A Political Economy Approach to the Neoclassical Model of Transition. Am. J. Econ. Sociol. 2002, 61, 259–276. [Google Scholar] [CrossRef]

- Liargovas, P.; Psychalis, M. Fiscal reforms in the EMU: The Greek response. Eur. Polit. Soc. 2020, 22, 57–774. [Google Scholar] [CrossRef]

- Apostolopoulos, N.; Psychalis, M.; Liargovas, P.; Pitsikou, V. Investigating Government lending during an economic crisis: A comparative analysis of four EU countries. Eur. Polit. Soc. 2021, 23, 548–562. [Google Scholar] [CrossRef]

- Bańkowski, K.; Ferdinandusse, M.; Hauptmeier, S.; Jacquinot, P.; Valenta, V. The Macroeconomic Impact of the Next Generation EU Instrument on the Euro Area; European Central Bank (ECB): Frankfurt, Germany, 2021. [Google Scholar]

- Roeger, W.; Veld, J.i.; Vogel, L. Fiscal Consolidation in Germany. Intereconomics 2010, 45, 364–371. [Google Scholar] [CrossRef][Green Version]

- Smets, F. Financial Stability Monetary Policy: How Closely Interlinked? Int. J. Cent. Bank. 2018, 10, 263–300. [Google Scholar]

- Fatás, A.; Andersen, T.; Martin, P. Does EMU Need a Fiscal Federation? Econ. Policy 1998, 13, 163–203. [Google Scholar] [CrossRef]

- De Grauwe, P. The European Central Bank as Lender of Last Resort in the Government Bond Markets. CESifo Econ. Stud. 2013, 59, 520–535. [Google Scholar] [CrossRef]

- Garcia-de-Andoain, C.; Heider, F.; Hoerova, M.; Manganelli, S. Central Bank Liquidity Provision and Interbank Market Functioning in the Euro Area; European Central Bank (ECB): Frankfurt, Germany, 2016. [Google Scholar]

- Marmefelt, T. COVID-19 and EconomicPolicy toward the New Normal:A Monetary-Fiscal Nexus after the Crisis? European Parliament: Luxembourg, 2020. [Google Scholar]

- Jones, E. When and How to Deactivate the SGP General Escape Clause? European Parliament: Brussels, Belgium, 2020. [Google Scholar]

- Larch, M.; Noord, P.v.d.; Jonung, L. The Stability and Growth Pact: Lessons from the Great Recession; European Commission: Brussels, Belgium, 2015. [Google Scholar]

- Leaman, A. Common Eurobonds Should Become Europe’s Safe Asset—But They Don’t Need to Be Green; Bruegel: Brussels, Belgium, 2020. [Google Scholar]

- Kraemer, M. Next Generation EU Bonds Might Face a Credit-Rating Challenge; CEPS: Brussels, Belgium, 4 June 2020. [Google Scholar]

- Constâncio, V.; Lannoo, K.; Thomadakis, A. A Common Euro-Bond Market in Sight; European Capital Markets Institute: Brussels, Belgium, 2020. [Google Scholar]

- Claeys, P.; Vašíček, B. Measuring Bilateral Spillover and Testing Contagion on Sovereign Bond Markets in Europe; European Central Bank (ECB): Frankfurt, Germany, 2014. [Google Scholar]

- Davola, A. From the Black Swan, to the Snowball. Risks of COVID-19 Pandemic for Consumer Credit Scores in the Lack of a Harmonized Regulatory Intervention. Opinio Juris Comp. 2020. Opinio Juris Comp. 2020. [Google Scholar] [CrossRef]

- Gaspar, V.; Bascuñán, F.L. Fiscal Policy and International Cooperation in a Covid World; VOX EU CEPR: London, UK, 2021. [Google Scholar]

- Saint-Amans, P. Tax in the Time of COVID-19; OECD: Paris, France, 2020. [Google Scholar]

- Apostolopoulos, N.; Liargovas, P.; Sklias, P.; Makris, I.; Apostolopoulos, S. Private healthcare entrepreneurship in a free-access public health system: What was the impact of COVID-19 public policies in Greece? J. Entrep. Public Policy 2022, 11, 23–39. [Google Scholar] [CrossRef]

- Pagoulatos, G. EMU and the Greek crisis: Testing the extreme limits of an asymmetric union. J. Eur. Integr. 2020, 42, 363–379. [Google Scholar] [CrossRef]

- Romer, C.D. The Fiscal Policy Response to the Pandemic; Brookings Papers on Economic Activity; Brookings: Washington, DC, USA, 2021; pp. 89–110. [Google Scholar]

- Prachowny, M.F.J. Okun’s Law: Theoretical Foundations and Revised Estimates. Rev. Econ. Stat. 1993, 75, 331–336. [Google Scholar] [CrossRef]

- Jalles, J.T.; Furceri, D.; Loungani, P. On the Determinants of the Okun’s Law: New Evidence from Time-Varying Estimates. Comp. Econ. Stud. 2020, 62, 661–700. [Google Scholar]

- Maris, G. Introduction: Eurozone and the Greek economic crisis in 2020: Current challenges and prospects. Eur. Polit. Soc. 2021, 23, 443–446. [Google Scholar] [CrossRef]

- Maris, G.; Sklias, P.; Maravegias, N. The political economy of the Greek economic crisis in 2020. Eur. Polit. Soc. 2021, 23, 447–467. [Google Scholar] [CrossRef]

- Liargovas, P.; Psychalis, M. Phillips Curve: The Greek Case. Eur. Rev. 2022, 30, 244–261. [Google Scholar] [CrossRef]

- Apeti, A.E.; Combes, j.-L.; Debrun, X.; Minea, A. Did Fiscal Space Foster Covid-19’s Fiscal Stimuli? Covid Econ. 2021, 74, 71–93. [Google Scholar]

- Benmelech, E.; Tzur-Ilan, N. The Determinants of Fiscal and Monetary Policies during the COVID-19 Crisis; National Bureau of Economic Research: Cambridge, MA, USA, 2020. [Google Scholar]

- Gentiloni, P. The EU’s Pandemic Response: Tackling COVID-19, Building the Future. Intereconomics 2020, 55, 242–243. [Google Scholar] [CrossRef]

- Liargovas, P.; Psychalis, M. Do Economic Adjustment Programmes Set Conflicting Objectives? The Case of Greece. Theor. Econ. Lett. 2019, 9, 3065–3087. [Google Scholar] [CrossRef]

- Paule-Viane, J.; Orden-Cruz, C.; Escamilla-Solano, S. Influence of COVID-induced fear on sovereign. Econ. Res. -Ekon. Istraživanja 2022, 35, 2173–2190. [Google Scholar] [CrossRef]

- Makin, A.J.; Layton, A. The global fiscal response to COVID-19: Risks and repercussions. Econ. Anal. Policy 2021, 69, 340–349. [Google Scholar] [CrossRef]

- Sklias, P.; Roukanas, S.; Galatsidas, G. Greek Political Economy in a Period of Economic Crisis: The Need for a National Growth Strategy Plan. Theor. Econ. Lett. 2022, 12, 371–391. [Google Scholar] [CrossRef]

- Maris, G.; Flouros, F. Economic crisis, COVID-19 pandemic, and the Greek model of capitalism. Evol. Inst. Econ. Rev. 2022, 19, 469–484. [Google Scholar] [CrossRef]

- Arestis, P. Coordination of Fiscal with Monetary and Financial Stability Policies Can Better Cure Unemployment. Rev. Keynes. Econ. 2014, 3, 233–247. [Google Scholar] [CrossRef]

- Psychalis, M. Fiscal Balance and Growth in the EMU: Friends or Foes? Empir. Econ. Lett. 2020, 19. Available online: http://www.eel.my100megs.com/volume-19-number-9.htm (accessed on 15 September 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Date | Employed | Unemployed | Non-Active |

|---|---|---|---|

| 19 December | 3906 | 764 | 3239 |

| 20 December | 3878 | 717 | 3256 |

| 21 December | 4062 | 598 | 3188 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Apostolopoulos, N.; Psychalis, M.; Liargovas, P. Discussing EU Policies and Mechanisms towards the COVID-19 Pandemic Crisis: A Case Study of Greece. World 2022, 3, 772-782. https://doi.org/10.3390/world3040043

Apostolopoulos N, Psychalis M, Liargovas P. Discussing EU Policies and Mechanisms towards the COVID-19 Pandemic Crisis: A Case Study of Greece. World. 2022; 3(4):772-782. https://doi.org/10.3390/world3040043

Chicago/Turabian StyleApostolopoulos, Nikolaos, Marios Psychalis, and Panagiotis Liargovas. 2022. "Discussing EU Policies and Mechanisms towards the COVID-19 Pandemic Crisis: A Case Study of Greece" World 3, no. 4: 772-782. https://doi.org/10.3390/world3040043

APA StyleApostolopoulos, N., Psychalis, M., & Liargovas, P. (2022). Discussing EU Policies and Mechanisms towards the COVID-19 Pandemic Crisis: A Case Study of Greece. World, 3(4), 772-782. https://doi.org/10.3390/world3040043