Diffusion of Solar PV Energy in the UK: A Comparison of Sectoral Patterns

Abstract

:1. Introduction

1.1. Background

1.2. Modelling the Diffusion of RES: A Short Review

1.3. Contribution and Paper Organization

2. Data and Methodology

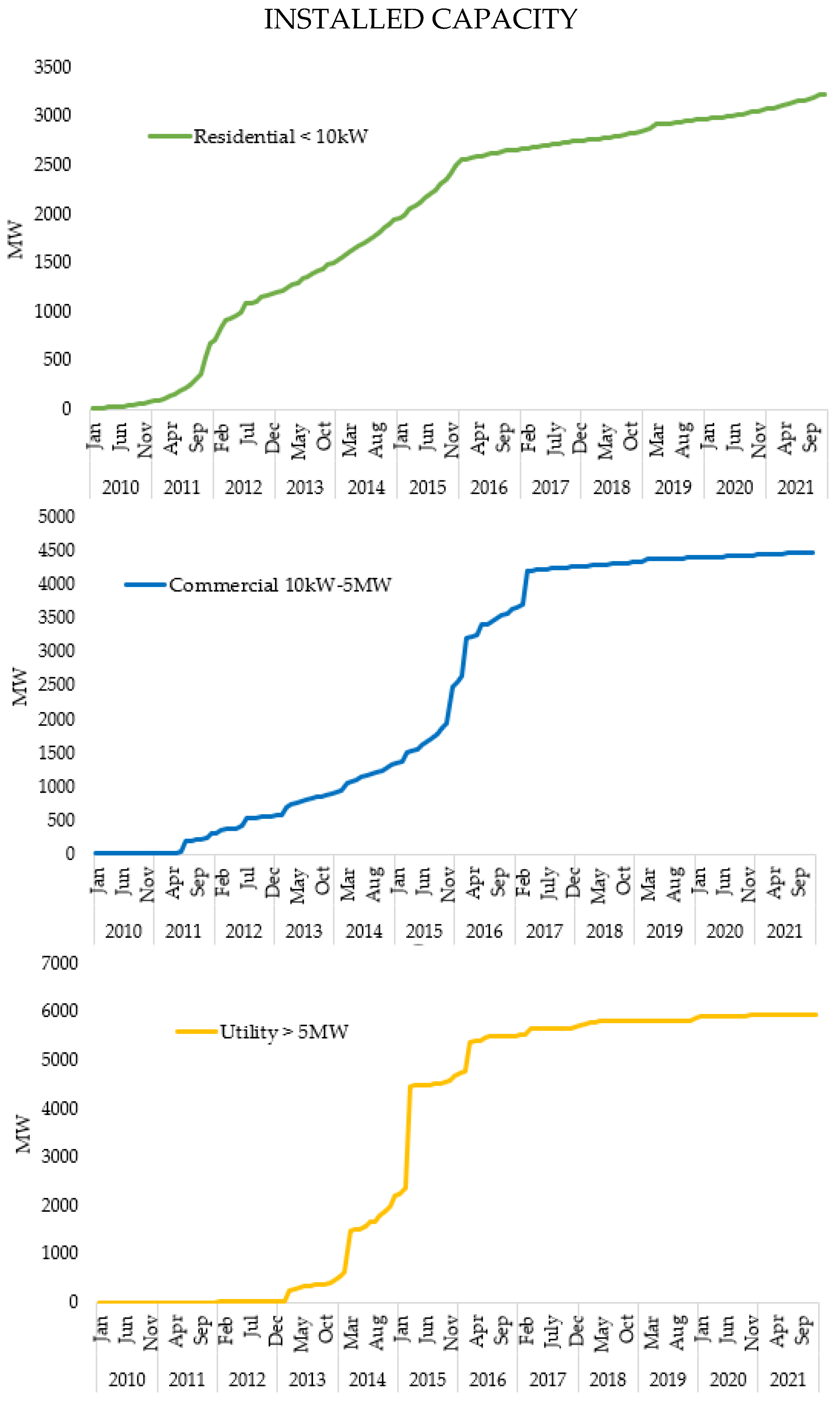

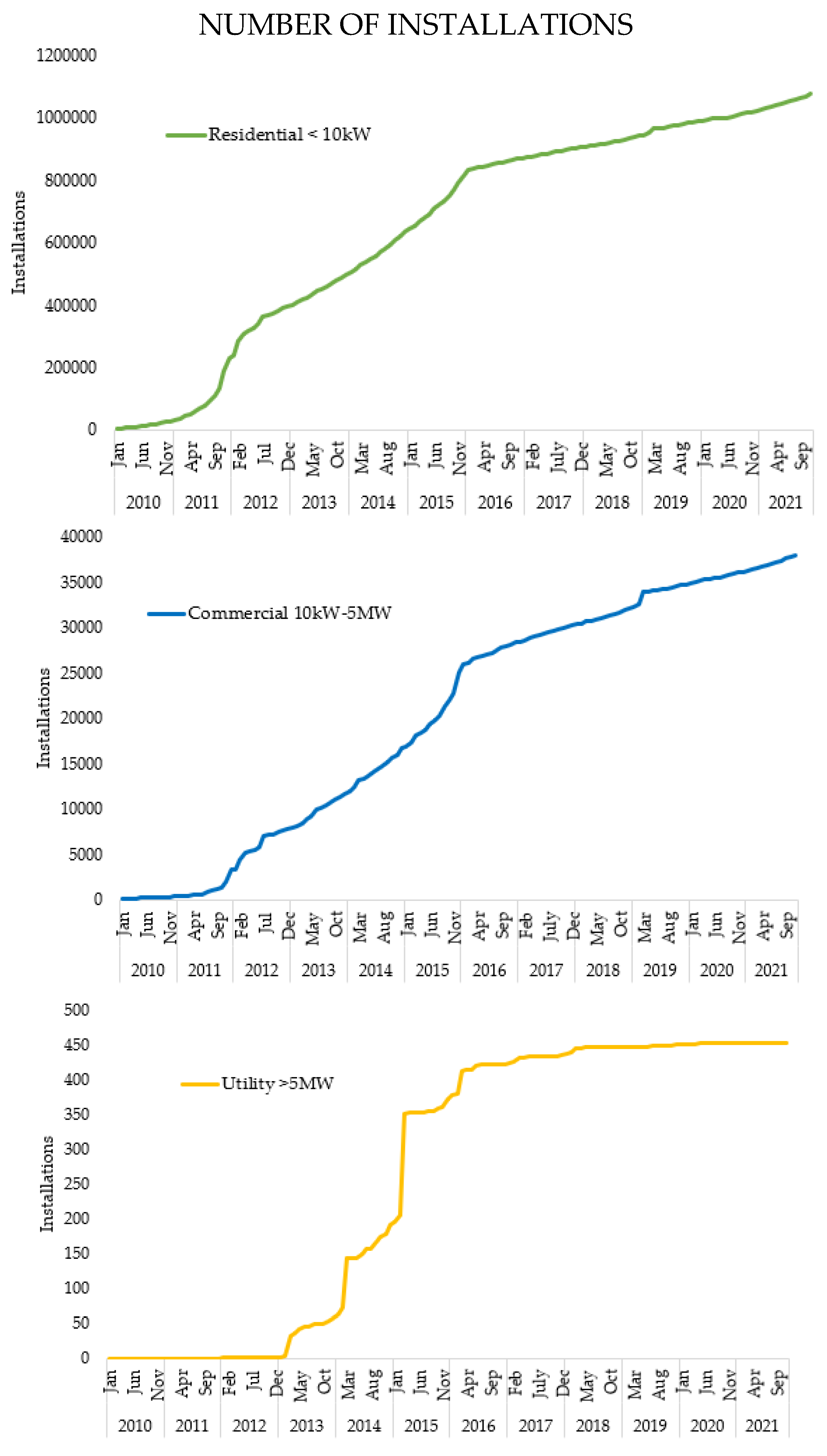

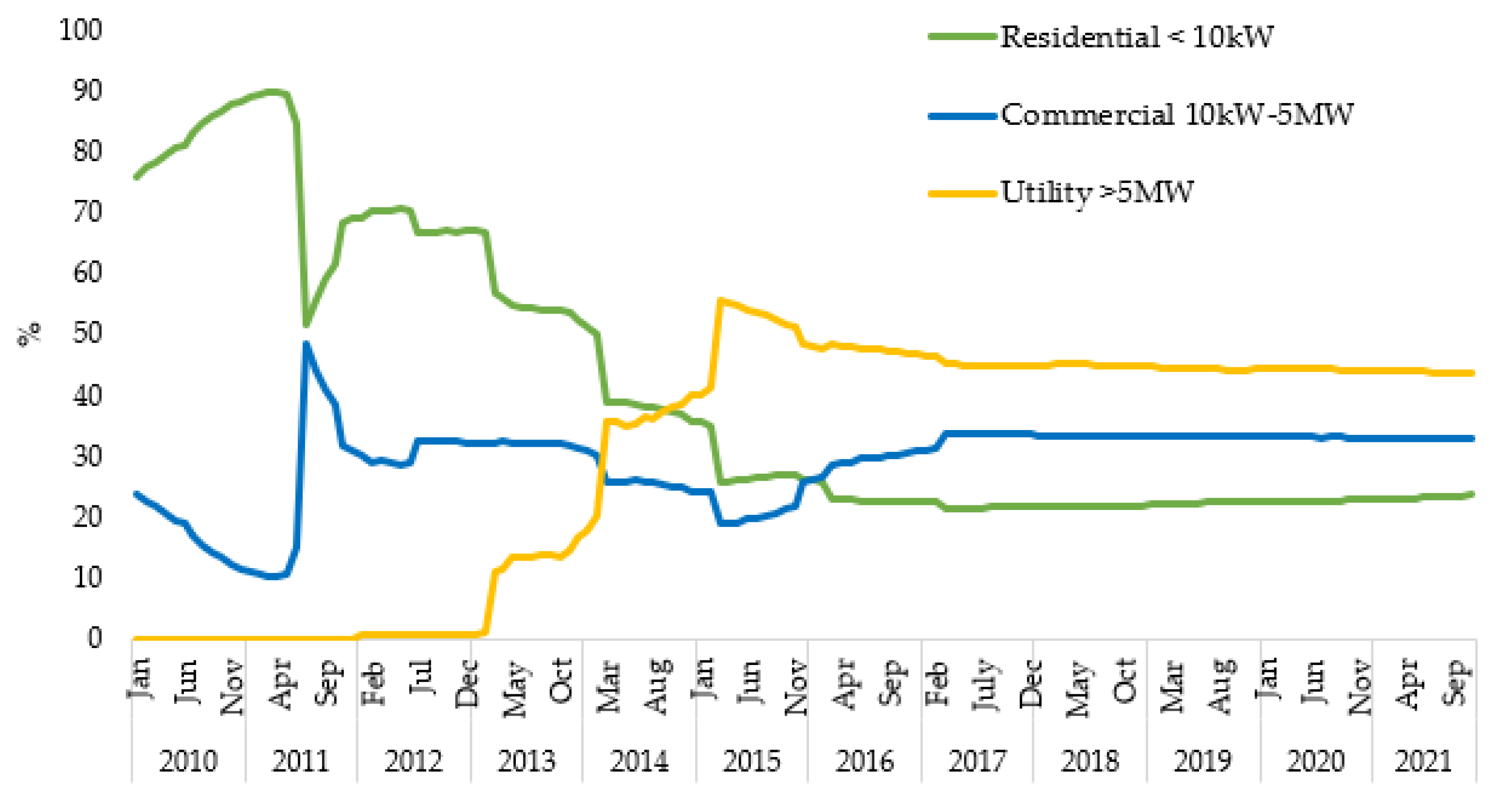

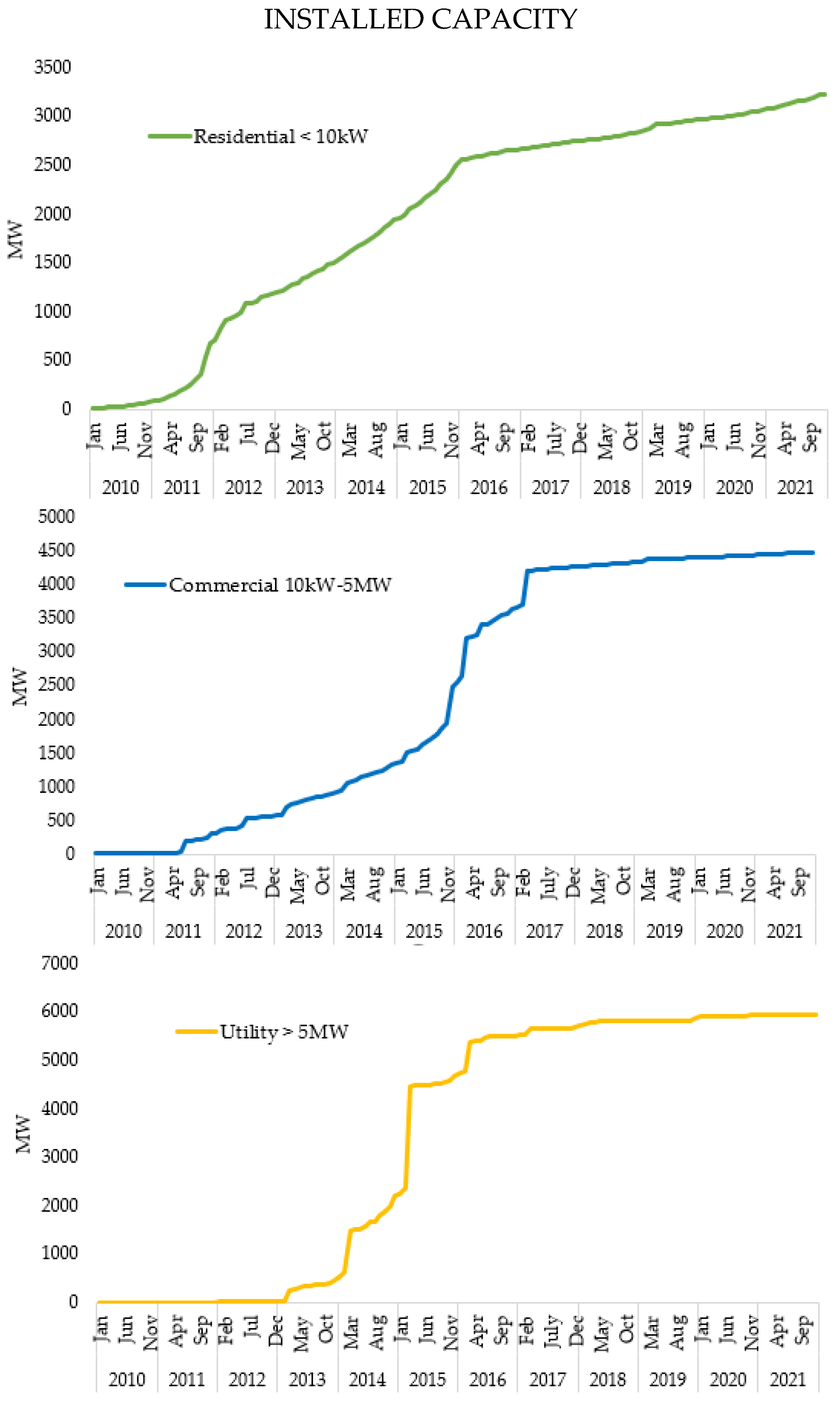

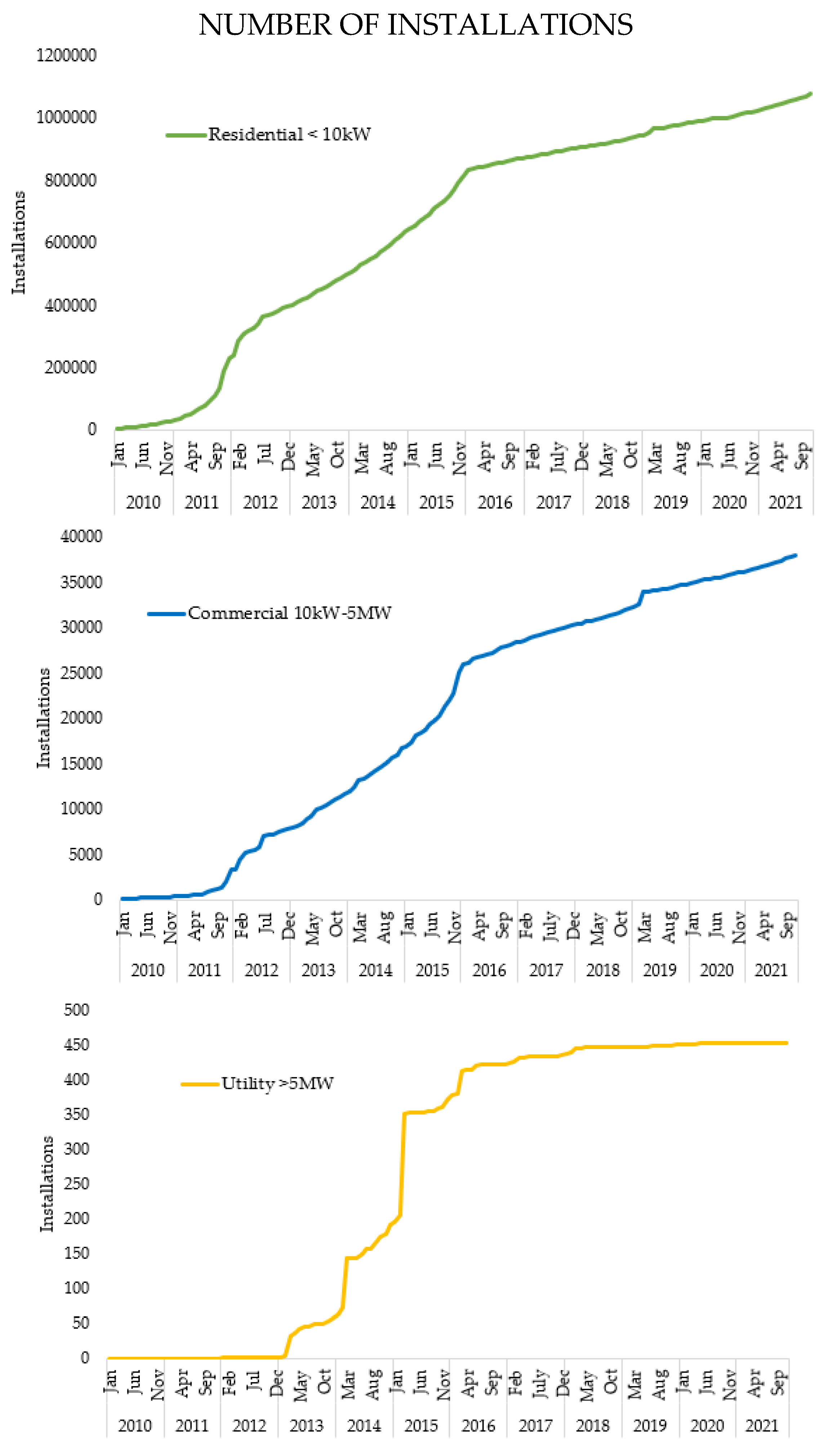

2.1. Data: Solar PV Adoption Data in UK

2.2. Methodology: Generalized Bass Model

2.3. Methodology: Estimation of Model Parameters

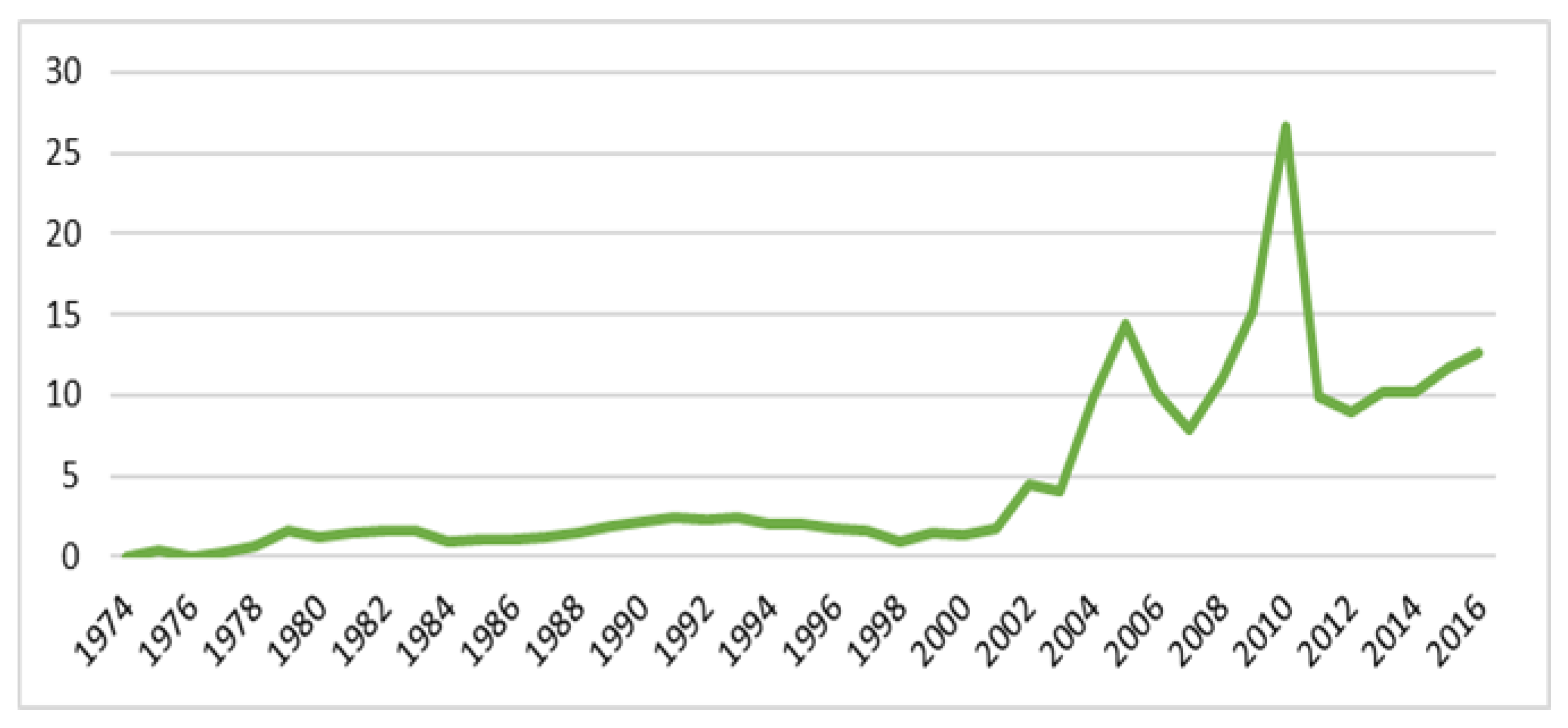

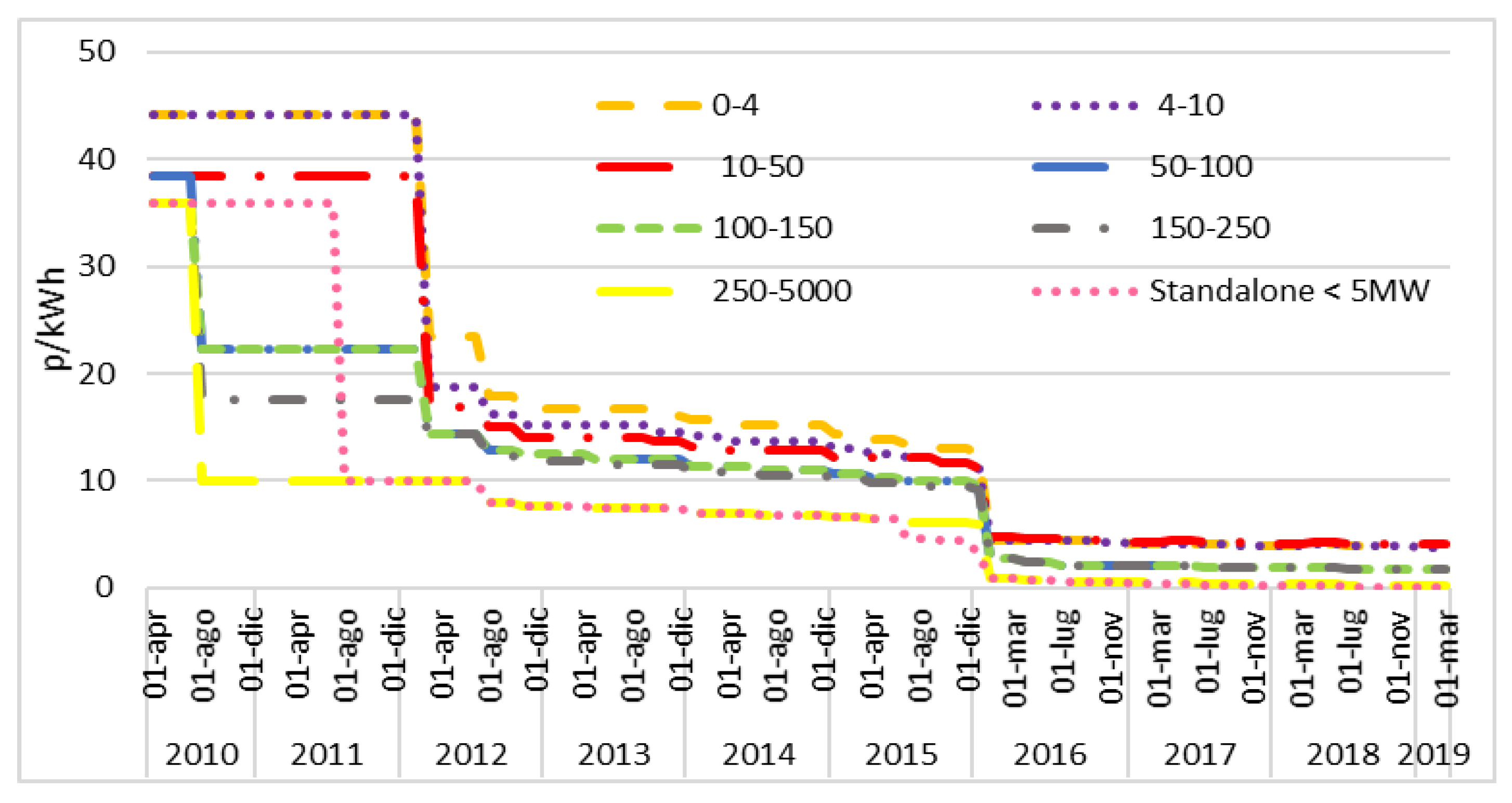

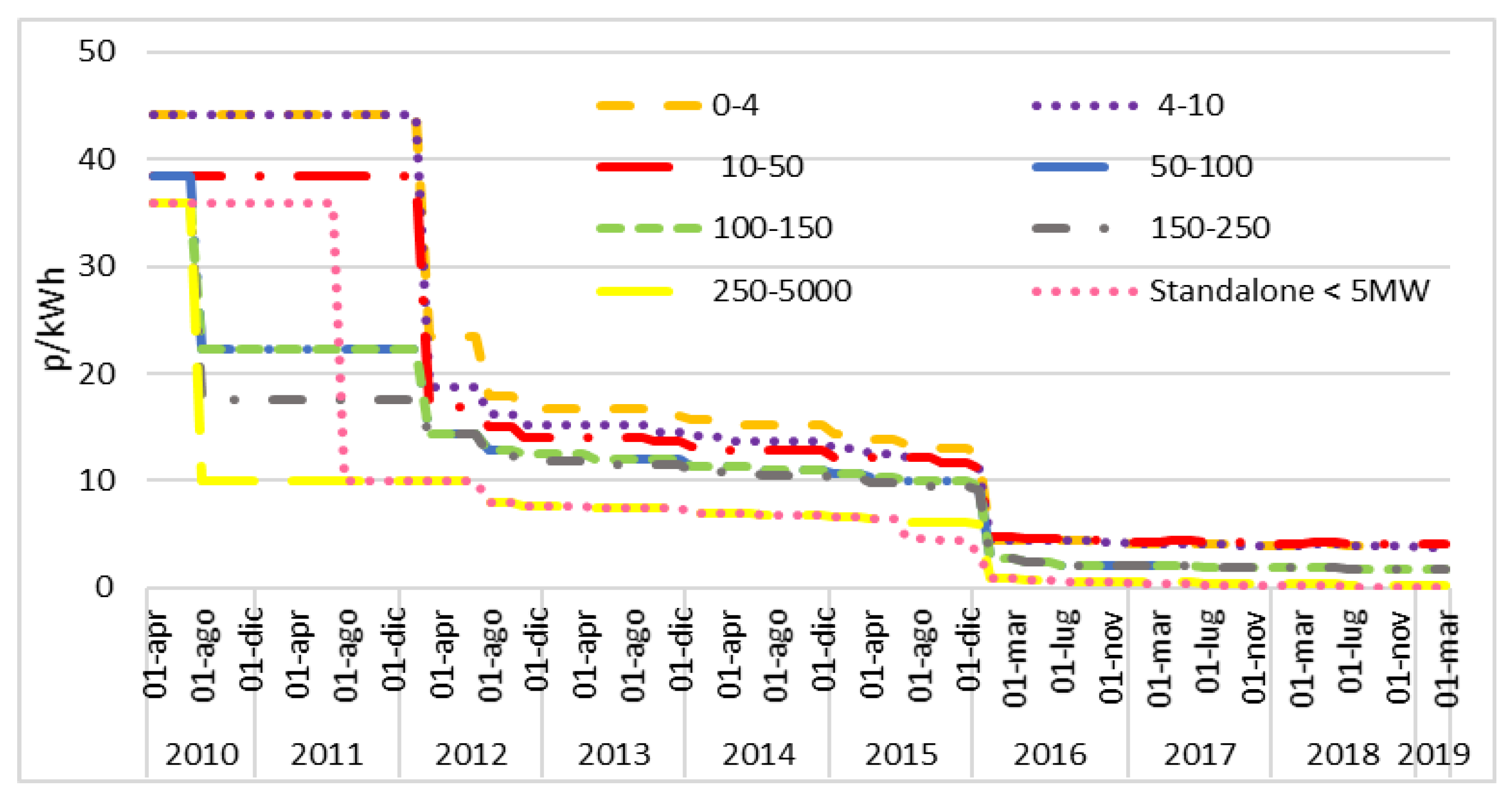

3. Solar PV Policies in the UK

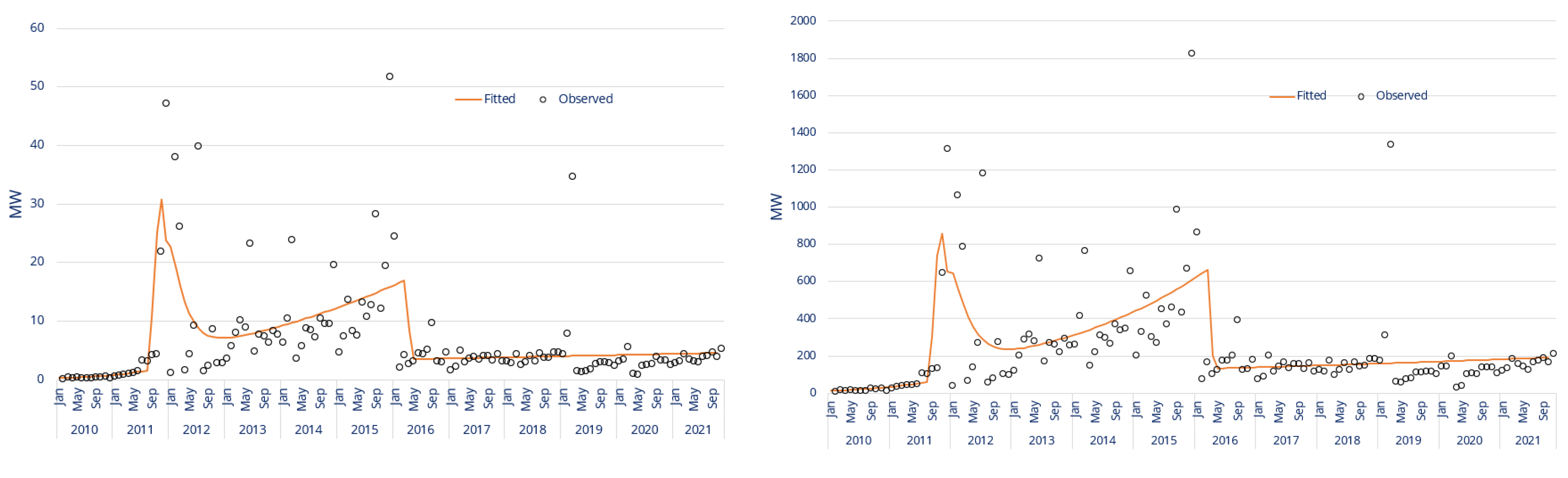

4. Results

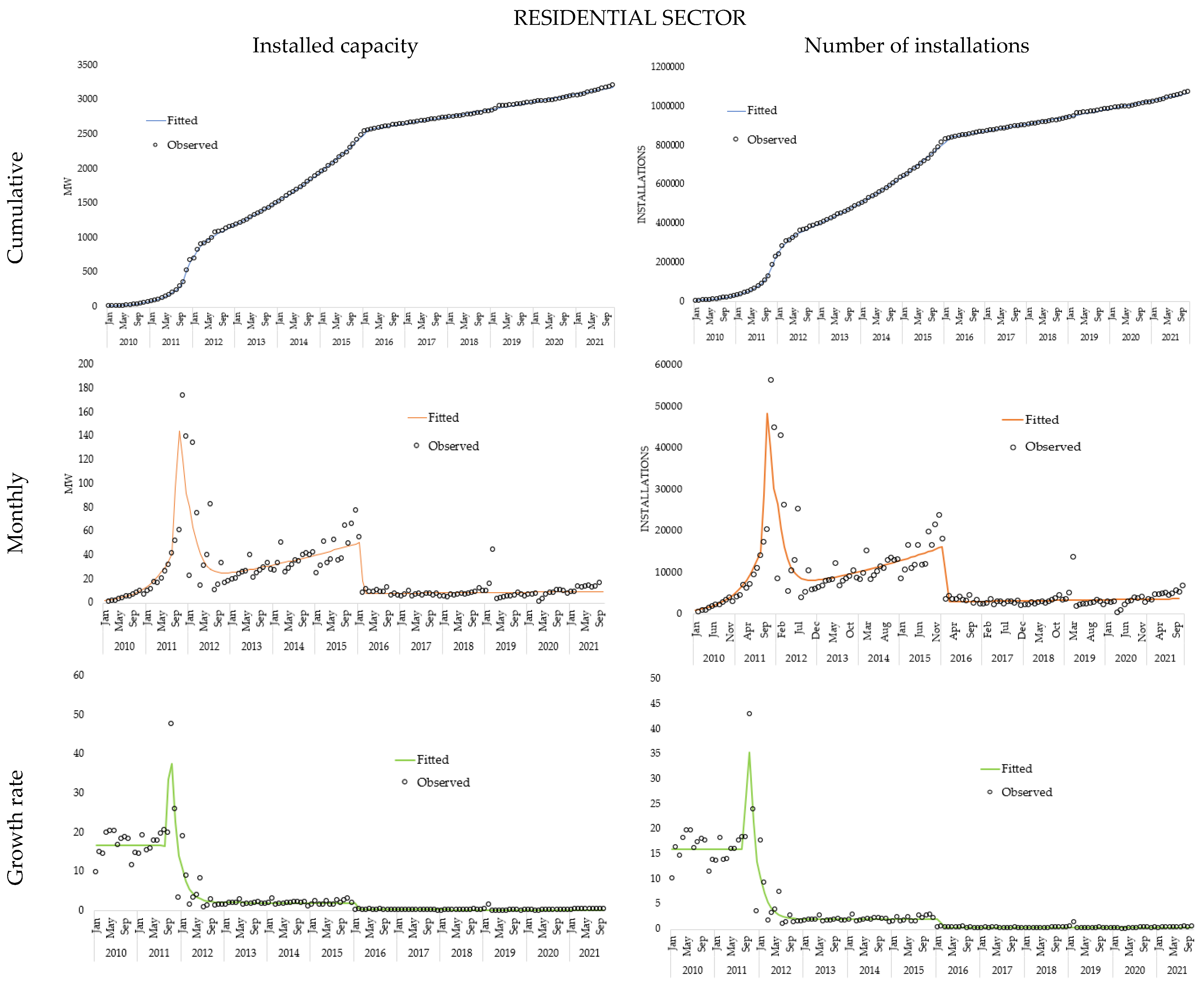

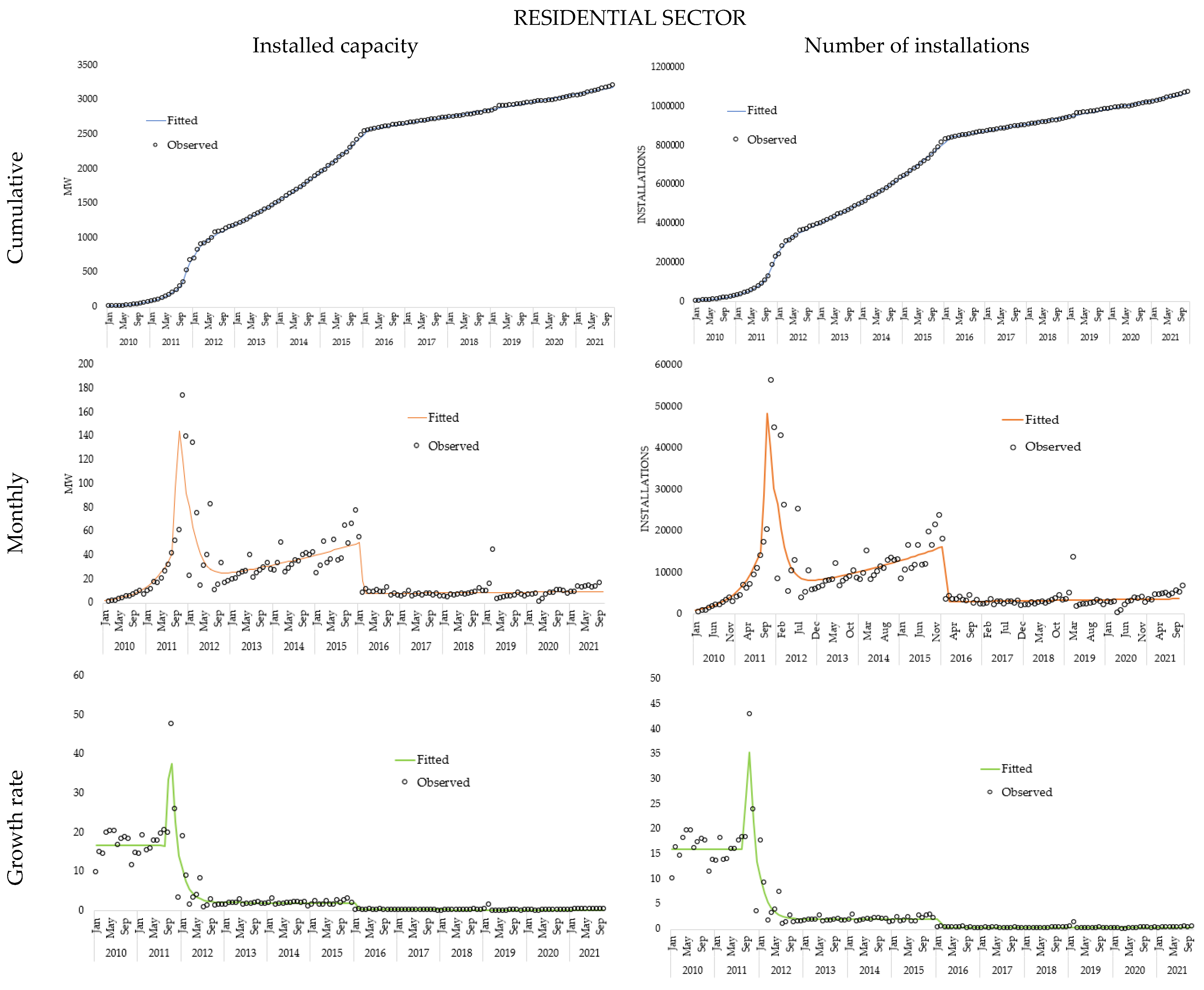

4.1. Residential Sector

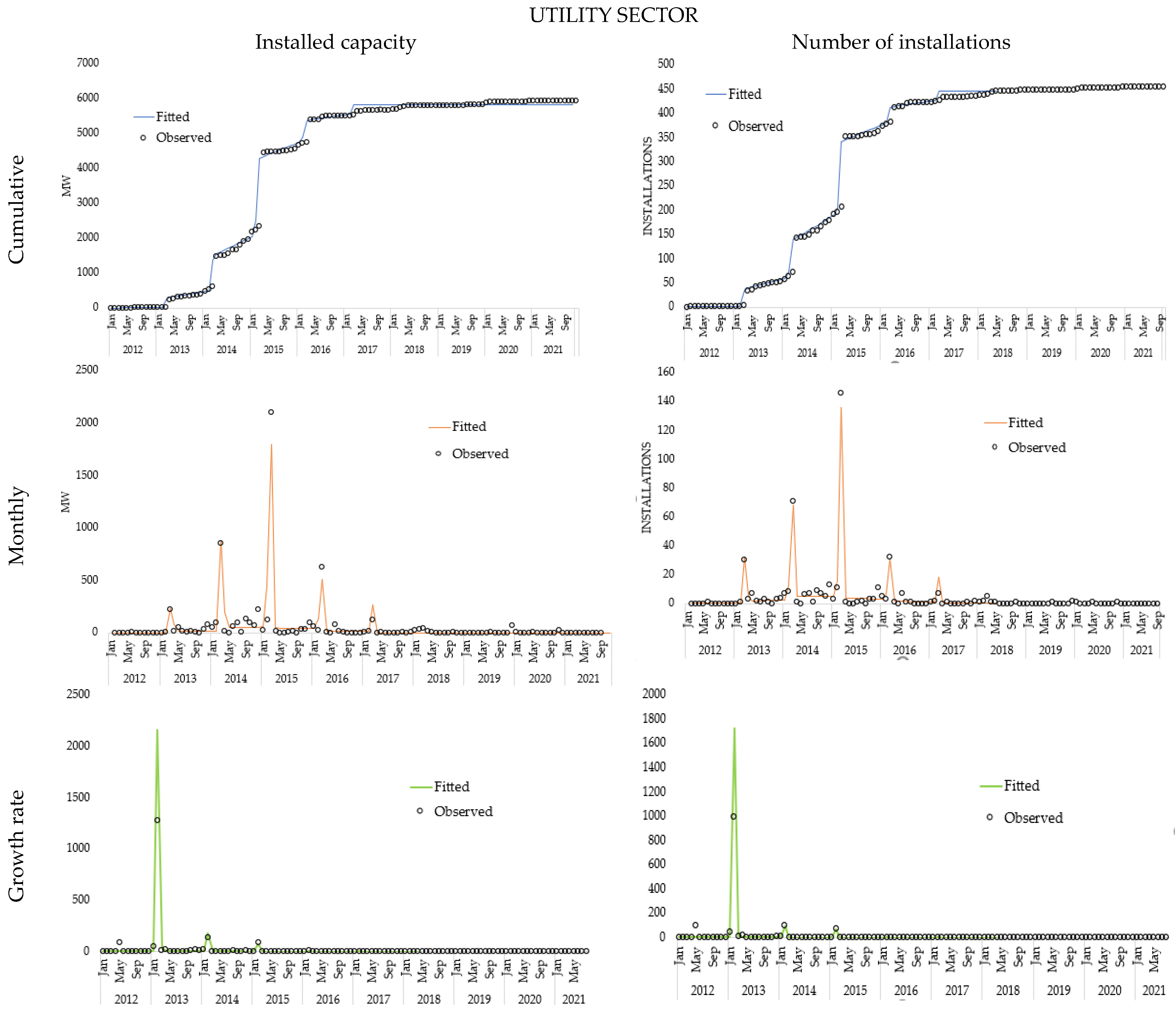

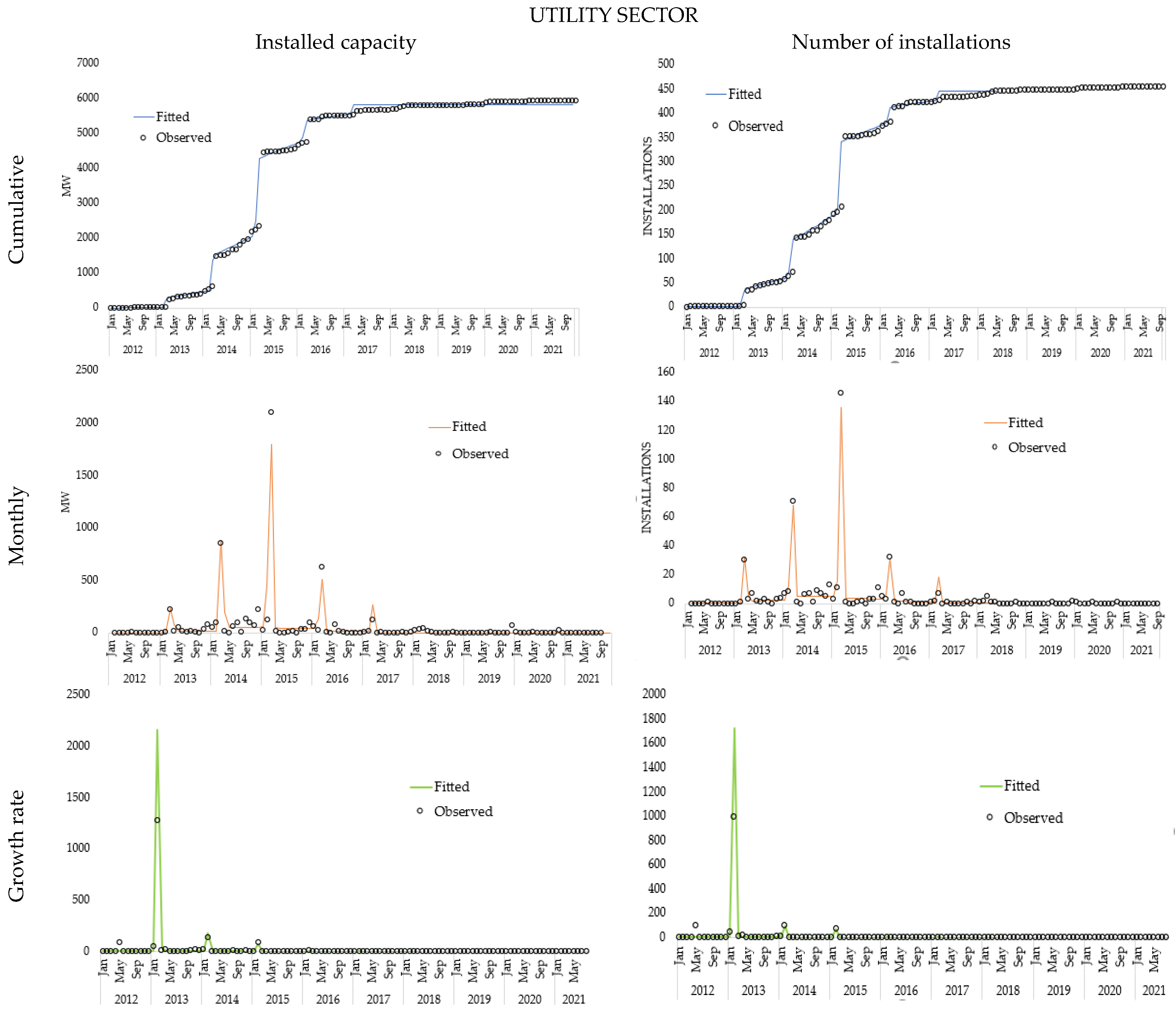

4.2. Utility Sector

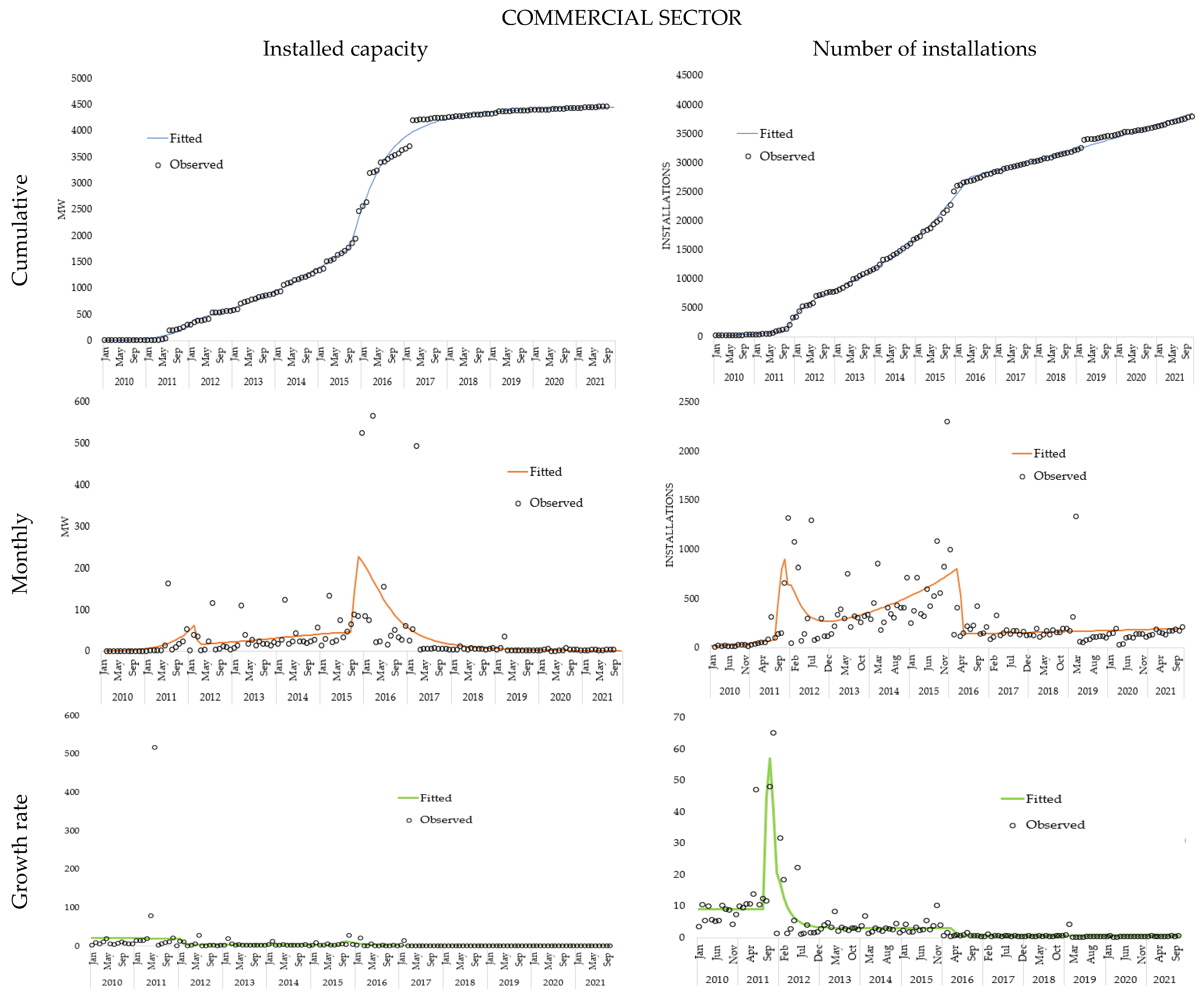

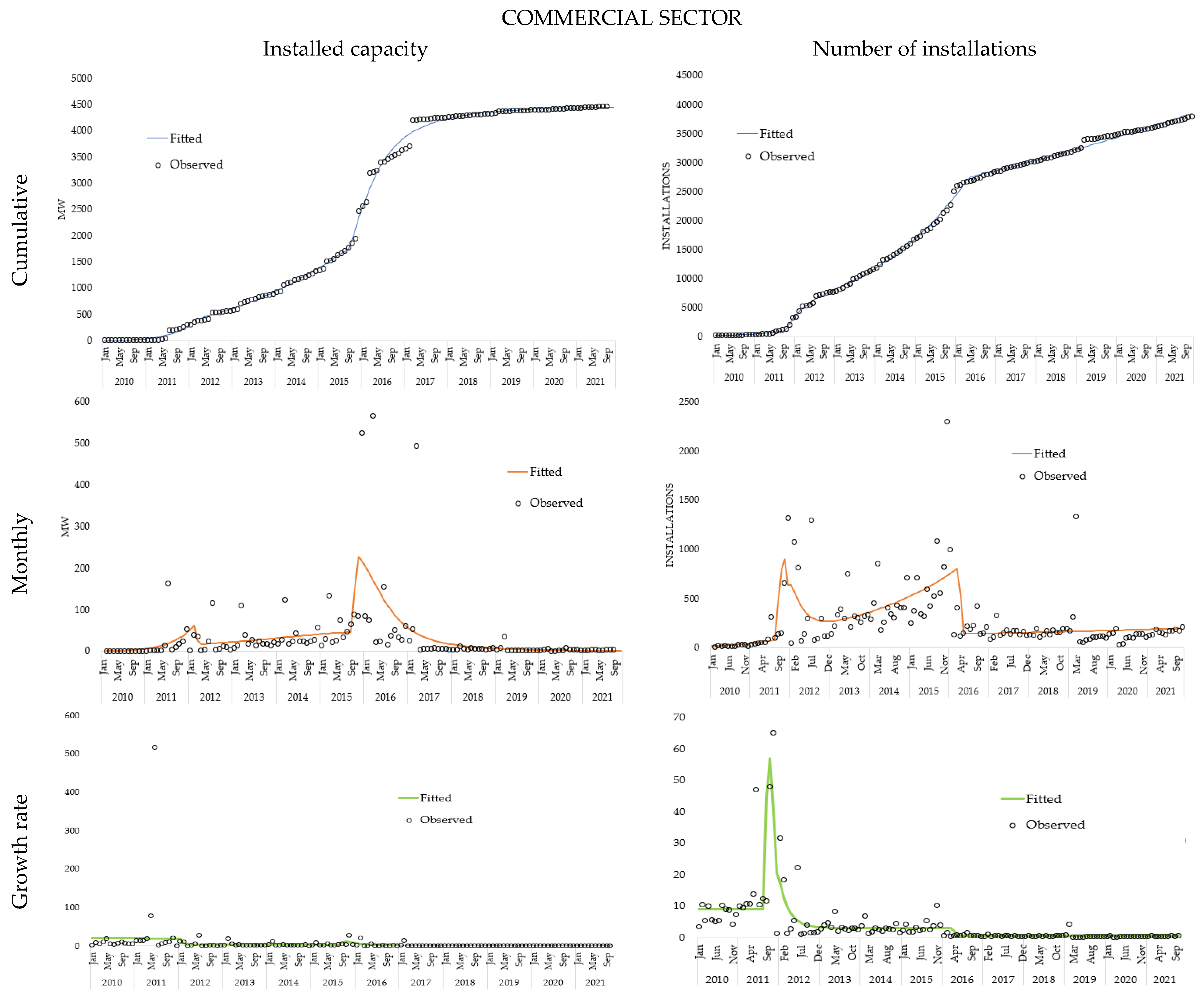

4.3. Commercial Sector

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Abbreviations

| PV | photovoltaic |

| RES | renewable energy sources |

| IEA | International Energy Agency |

| UK | United Kingdom |

| GBM | Generalized Bass model |

| GIM | Generalized Internal model |

| GW | Giga Watt |

| MW | Mega Watt |

| KW | Kilo Watt |

| BM | Bass model |

| NLS | Nonlinear Least Squares |

| LCBP | Low Carbon Building Program |

| NFFO | Non-Fossil Fuel Obligation |

| ROC | Renewable Obligation Certificates |

| CfD | Contracts for Difference |

| FIT | Feed-in tariff |

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

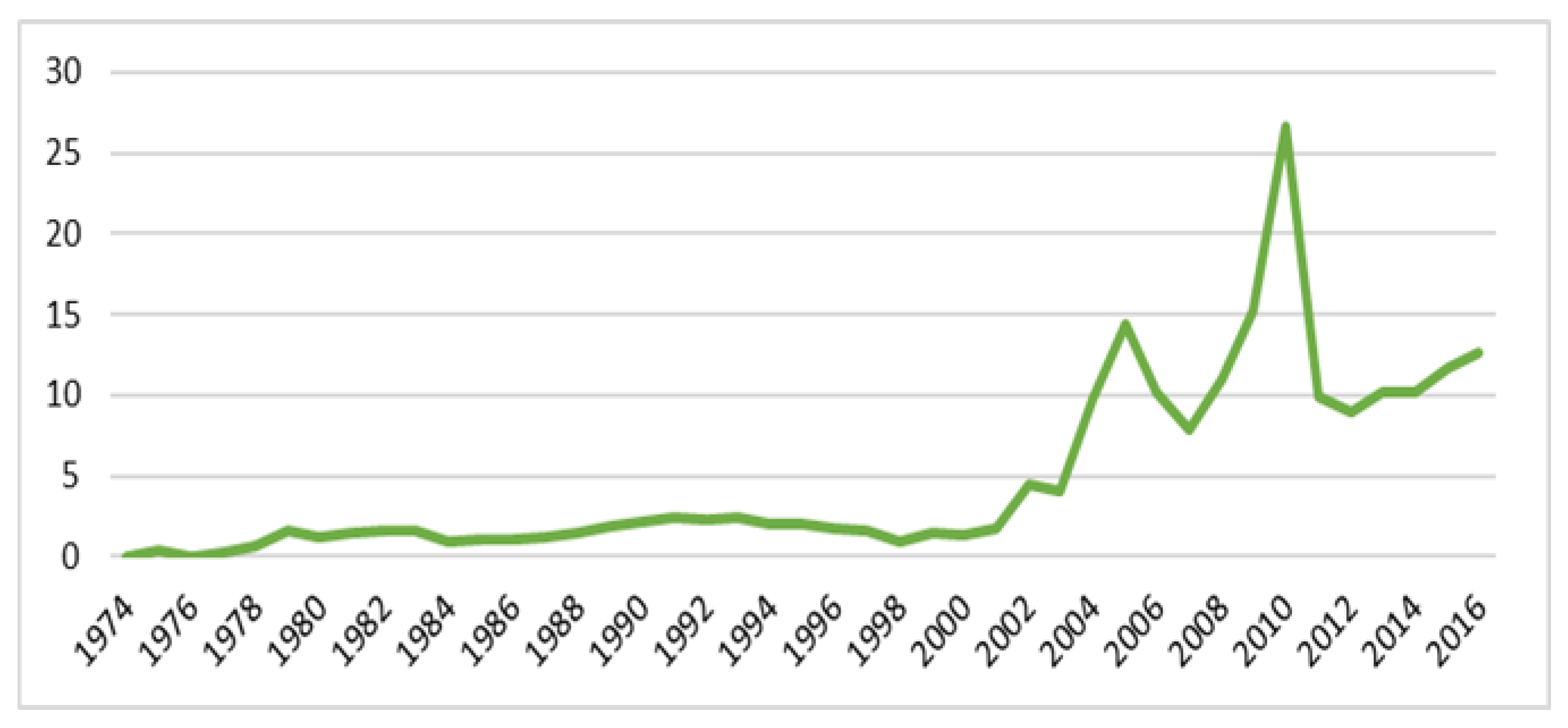

| Obligation Period (from 1 April to 31 March) | Supply (%) | Supply Growth Rate (p.p.) | Buy Out Price (£/MWh) | Effective Price per Unit (p/kWh) |

|---|---|---|---|---|

| 2002–2003 | 3 | £30.00 | 0.09 | |

| 2003–2004 | 4.3 | 1.3 | £30.51 | 0.13 |

| 2004–2005 | 4.9 | 0.6 | £31.39 | 0.15 |

| 2005–2006 | 5.5 | 0.6 | £32.33 | 0.18 |

| 2006–2007 | 6.7 | 1.2 | £33.24 | 0.22 |

| 2007–2008 | 7.9 | 1.2 | £34.30 | 0.29 |

| 2008–2009 | 9.1 | 1.2 | £35.76 | 0.33 |

| 2009–2010 | 9.7 | 0.6 | £37.19 | 0.36 |

| 2010–2011 | 11.1 | 1.4 | £36.99 | 0.41 |

| 2011–2012 | 12.4 | 1.3 | £38.69 | 0.48 |

| 2012–2013 | 15.8 | 3.4 | £40.71 | 0.64 |

| 2013–2014 | 20.6 | 4.8 | £42.02 | 0.87 |

| 2014–2015 | 24.4 | 3.8 | £43.30 | 1.06 |

| 2015–2016 | 29 | 4.6 | £44.33 | 1.29 |

| 2016–2017 | 34.8 | 5.8 | £44.77 | 1.56 |

| 2017–2018 | 40.9 | 6.1 | £45.58 | 1.86 |

| 2018–2019 | 46.8 | 5.9 | £47.22 | - |

| 2019–2020 | 48.4 | 1.6 | £48.78 | - |

| 2020–2021 | 47.1 | −1.3 | £50.05 | - |

| 2021–2022 | 49.2 | 2.1 | £50.80 | - |

| Installed Capacity | Number of Installations | |||||||

|---|---|---|---|---|---|---|---|---|

| Sector | R | C | U | Agg | R | C | U | Agg |

| α | 0.0061 | 0.0004 | 0.0005 | 0.0005 | 0.0066 | 0.0026 | 0.0010 | 0.0065 |

| q | 0.04 | 0.08 | 0.16 | 0.08 | 0.03 | 0.05 | 0.14 | 0.03 |

| m | 3091 | 4540 | 5816 | 13,456 | 1,043,260 | 37,037 | 448 | 1,081,618 |

| First Shock | Second Shock | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Country | Selected Model | Q and Time to the 99th Percentile of the Minimum Target | Year of Achievement of the Minimum Target | Peak | C1 | A1 | A1 | C2 | A2 | A2 |

| GBR | F3 + F3 | 0.31 (2044) | 2029 | Yes | 1.75 | 17.28 | 33.06 | 2.53 | 21.43 | 23.18 |

| Small-Size (10–15 kW) Commercial Sector | ||

|---|---|---|

| Installed Capacity | Number of Installations | |

| Best Model | 3-shock (F1 + F2 + F1) | 3-shock (F1 + F2 + F1) |

| q | 0.006 | 0.006 |

| m | 5256 | 24,544,092 |

| A1 | 14.8 | 13.3 |

| a1 | 0.0 | 0 |

| b1 | 23 | 23 |

| A2 (c2) | 0.4 | 0.4 |

| a2 | 20 | 21 |

| b2 (A2) | 137 | 107 |

| A3 | 3.9 | 4.1 |

| a3 | 24 | 24 |

| b3 | 75 | 75 |

References

- Heffron, R.J.; Körner, M.F.; Schöpf, M.; Wagner, J.; Weibelzahl, M. The role of flexibility in the light of the COVID-19 pandemic and beyond: Contributing to a sustainable and resilient energy future in Europe. Renew. Sustain. Energy Rev. 2021, 140, 110743. [Google Scholar] [CrossRef] [PubMed]

- Bessi, A.; Guidolin, M.; Manfredi, P. The role of gas on future perspectives of renewable energy diffusion: Bridging technology or lock-in? Renew. Sustain. Energy Rev. 2021, 152, 111673. [Google Scholar] [CrossRef]

- IEA, Renewables. 2021. Available online: https://www.iea.org/reports/renewables-2021 (accessed on 21 January 2022).

- Geels, F.W.; McMeekin, A.; Pfluger, B. Socio-technical scenarios as a methodological tool to explore social and political feasibility in low-carbon transitions: Bridging computer models and the multi-level perspective in UK electricity generation (2010–2050). Technol. Forecast. Soc. Chang. 2020, 151, 119258. [Google Scholar] [CrossRef]

- Geels, F.W. Disruption and low-carbon system transformation: Progress and new challenges in socio-technical transitions research and the Multi-Level Perspective. Energy Res. Soc. Sci. 2018, 37, 224–231. [Google Scholar] [CrossRef]

- Sovacool, B.K.; Hess, D.J.; Amir, S.; Geels, F.W.; Hirsh, R.; Medina, L.R.; Yearley, S. Sociotechnical agendas: Reviewing future directions for energy and climate research. Energy Res. Soc. Sci. 2020, 70, 101617. [Google Scholar] [CrossRef]

- Hirt, L.F.; Sahakian, M.; Trutnevyte, E. What socio-technical regimes foster solar energy champions? Analyzing uneven photovoltaic diffusion at a subnational level in Switzerland. Energy Res. Soc. Sci. 2021, 74, 101976. [Google Scholar] [CrossRef]

- Reindl, K.; Palm, J. Installing PV: Barriers and enablers experienced by non-residential property owners. Renew. Sustain. Energy Rev. 2021, 141, 110829. [Google Scholar] [CrossRef]

- Schulte, E.; Scheller, F.; Sloot, D.; Bruckner, T. A meta-analysis of residential PV adoption: The important role of perceived benefits, intentions and antecedents in solar energy acceptance. Energy Res. Soc. Sci. 2022, 84, 102339. [Google Scholar] [CrossRef]

- Martinopoulos, G.; Tsalikis, G. Diffusion and adoption of solar energy conversion systems–The case of Greece. Energy 2018, 144, 800–807. [Google Scholar] [CrossRef]

- Martinopoulos, G. Are rooftop photovoltaic systems a sustainable solution for Europe? A life cycle impact assessment and cost analysis. Appl. Energy 2020, 257, 114035. [Google Scholar] [CrossRef]

- Peng, J.; Lu, L.; Yang, H. Review on life cycle assessment of energy payback and greenhouse gas emission of solar photovoltaic systems. Renew. Sustain. Energy Rev. 2013, 19, 255–274. [Google Scholar] [CrossRef]

- IEA-PVPS (2021), Snapshot of Global PV Markets 2021. Available online: https://iea-pvps.org/snapshot-reports/snapshot-2021/ (accessed on 21 January 2022).

- Rogers, E.M. Diffusion of Innovations, 4th ed.; Simon and Schuster: New York, NY, USA, 2010. [Google Scholar]

- Bass, F.M. A new product growth for model consumer durables. Manag. Sci. 1969, 15, 215–227. [Google Scholar] [CrossRef]

- Rao, K.U.; Kishore, V.V.N. A review of technology diffusion models with special reference to renewable energy technologies. Renew. Sustain. Energy Rev. 2010, 14, 1070–1078. [Google Scholar] [CrossRef]

- Petropoulos, F.; Apiletti, D.; Assimakopoulos, V.; Babai, M.Z.; Barrow, D.K.; Taieb, S.B.; Bergmeir, C.; Bessa, R.J.; Bijak, J.; Boylan, J.E.; et al. Forecasting: Theory and practice. Int. J. Forecast. 2022, in press. [Google Scholar] [CrossRef]

- Guseo, R.; Dalla Valle, A.; Guidolin, M. World Oil Depletion Models: Price effects compared with strategic or technological interventions. Technol. Forecast. Soc. Chang. 2007, 74, 452–469. [Google Scholar] [CrossRef]

- Bass, F.M.; Krishnan, T.V.; Jain, D.C. Why the Bass model fits without decision variables. Market. Sci. 1994, 13, 203–223. [Google Scholar] [CrossRef]

- Guidolin, M.; Mortarino, C. Cross-country diffusion of photovoltaic systems: Modelling choices and forecasts for national adoption patterns. Technol. Forecast. Soc. Chang. 2010, 77, 279–296. [Google Scholar] [CrossRef] [Green Version]

- Bunea, A.M.; Della Posta, P.; Guidolin, M.; Manfredi, P. What do adoption patterns of solar panels observed so far tell about governments’ incentive? Insights from diffusion models. Technol. Forecast. Soc. 2020, 160, 120240. [Google Scholar] [CrossRef]

- Islam, T.; Meade, N. The impact of attribute preferences on adoption timing: The case of photo-voltaic (PV) solar cells for household electricity generation. Energy Policy 2013, 55, 521–530. [Google Scholar] [CrossRef] [Green Version]

- Islam, T. Household level innovation diffusion model of photo-voltaic (PV) solar cells from stated preference data. Energy Policy 2014, 65, 340–350. [Google Scholar] [CrossRef]

- Snape, J.R. Spatial and temporal characteristics of PV adoption in the UK and their implications for the smart grid. Energies 2016, 9, 210. [Google Scholar] [CrossRef] [Green Version]

- Balta-Ozkan, N.; Yildirim, J.; Connor, P.M.; Truckell, I.; Hart, P. Energy transition at local level: Analyzing the role of peer effects and socio-economic factors on UK solar photovoltaic deployment. Energy Policy 2021, 148, 112004. [Google Scholar] [CrossRef]

- Castaneda, M.; Zapata, S.; Cherni, J.; Aristizabal, A.J.; Dyner, I. The long-term effects of cautious feed-in tariff reductions on photovoltaic generation in the UK residential sector. Renew. Energy 2020, 155, 1432–1443. [Google Scholar] [CrossRef]

- GOV.UK—National Statistics Solar Photovoltaics Deployment. Available online: https://www.gov.uk/government/statistics/solar-photovoltaics-deployment (accessed on 28 December 2021).

- Keirstead, J. The UK domestic photovoltaics industry and the role of central government. Energy Policy 2007, 35, 2268–2280. [Google Scholar] [CrossRef]

- CEBR: Solar Powered Growth in the UK. 2014. Available online: https://cebr.com/reports/solar-powered-growth-in-the-uk/ (accessed on 7 February 2019).

- International Finance Corporation: Utility-Scale Solar Photovoltaic Power Plants, World Bank Group. 2015. Available online: http://documents.worldbank.org/curated/en/690161467992462412/Utility-scale-solar-photovoltaic-power-plants-a-project-developer-s-guide (accessed on 7 February 2019).

- Seber, G.A.F.; Wild, C.J. Nonlinear Regression; John Wiley & Sons: New York, NY, USA, 1989. [Google Scholar]

- Van den Bulte, C.; Lilien, G.L. Bias and Systematic Change in the Parameter Estimates of Macro-Level Diffusion Models. Mark. Sci. 1997, 16, 338–353. [Google Scholar] [CrossRef]

- Faiers, A.; Neame, C. Consumer attitudes towards domestic solar power systems. Energy Policy 2006, 34, 1797–1806. [Google Scholar] [CrossRef] [Green Version]

- Hammond, G.P.; Harajli, H.A.; Jones, C.I.; Winnett, A.B. Whole systems appraisal of a UK Building Integrated Photovoltaic (BIPV) system: Energy, environmental, and economic evaluations. Energy Policy 2012, 40, 219–230. [Google Scholar] [CrossRef]

- Yamaguchi, Y.; Akai, K.; Shen, J.; Fujimura, N.; Shimoda, Y.; Saijo, T. Prediction of photovoltaic and solar water heater diffusion and evaluation of promotion policies on the basis of consumers’ choices. Appl. Energy 2013, 102, 1148–1159. [Google Scholar] [CrossRef]

- GOV.UK—Legislation. Available online: www.legislation.gov.uk (accessed on 5 July 2019).

- National Archive—Reform of the Renewables Obligation. May 2007. Available online: http://webarchive.nationalarchives.gov.uk/+/http:/www.berr.gov.uk/files/file39497.pdf (accessed on 5 July 2019).

- Duan, H.B.; Zhu, L.; Fan, Y. A cross-country study on the relationship between diffusion of wind and photovoltaic solar technology. Technol. Forecast. Soc. Chang. 2014, 83, 156–169. [Google Scholar] [CrossRef]

- Da Silva, P.P.; Dantas, G.; Pereira, G.I.; Câmara, L.; De Castro, N.J. Photovoltaic distributed generation–An international review on diffusion, support policies, and electricity sector regulatory adaptation. Renew. Sustain. Energy Rev. 2019, 103, 30–39. [Google Scholar] [CrossRef]

- GOV.UK—Government Response to the Consultation on Proposals for the Levels of Banded Support Under the Renewables Obligation for the Period 2013–17 and the Renewables Obligation Order. 2012. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/42852/5936-renewables-obligation-consultation-the-government.pdf (accessed on 28 December 2021).

- OFGEM—Renewables Obligation (RO). Available online: https://www.ofgem.gov.uk/environmental-programmes/ro/about-ro/ro-closure (accessed on 28 December 2021).

- GOV.UK—Contracts for Difference. Available online: https://www.gov.uk/government/publications/contracts-for-difference/contract-for-difference (accessed on 28 December 2021).

- PV Magazine—UK: Solar Still Being Blocked in Next CFD Auction. Available online: https://www.pv-magazine.com/2016/11/09/uk-solar-still-being-blocked-in-next-cfd-auction_100026847/ (accessed on 28 December 2021).

- OFGEM—Feed-In-Tariffs (FIT). Available online: https://www.ofgem.gov.uk/environmental-programmes/fit/fit-tariff-rates (accessed on 12 January 2022).

- The Eco Experts. Available online: https://www.theecoexperts.co.uk/sites/default/files/filemanager/cost-of-solar-2017-graph (accessed on 12 January 2022).

- Soal Power Portal—Solar Made to Wait for Future Direction as Clean Growth Strategy Defers PV Policy. Available online: https://www.solarpowerportal.co.uk/news/solar_made_to_wait_for_future_direction_as_clean_growth_strategy_defers_pv (accessed on 12 January 2022).

- UK Solar Photovoltaic Roadmap—A Strategy for 2020. Available online: https://www.bre.co.uk/filelibrary/nsc/Documents%20Library/Not%20for%20Profits/KTN_Report_Solar-PV-roadmap-to-2020_1113.pdf (accessed on 12 January 2022).

- Dusonchet, L.; Telaretti, E. Economic analysis of different supporting policies for the production of electrical energy by solar photovoltaics in western European Union countries. Energy Policy 2010, 38, 3297–3308. [Google Scholar] [CrossRef]

- The Guardian—Solar Subsidies Government Loses Court Appeal. 2012. Available online: https://www.theguardian.com/environment/2012/jan/25/solar-subsidies-government-loses-court-appeal (accessed on 15 March 2019).

- Dusonchet, L.; Telaretti, E. Comparative economic analysis of support policies for solar PV in the most representative EU countries. Renew. Sustain. Energy Rev. 2015, 42, 986–998. [Google Scholar] [CrossRef]

- Green Business Watch—UK Domestic Solar Panel Costs and Returns. Available online: https://greenbusinesswatch.co.uk/uk-domestic-solar-panel-costs-and-returns-2010-2014#section4 (accessed on 7 February 2019).

- OFGEM—Renewables Obligation (RO) Buy-Out Price and Mutualisation Ceilings for 2018–19 RO Year. Available online: https://www.ofgem.gov.uk/publications-and-updates/renewables-obligation-ro-buy-out-price-and-mutualisation-ceilings-2018-19-ro-year (accessed on 23 July 2019).

- Soal Power Portal—Let Solar Back into CfDs. Available online: https://www.solarpowerportal.co.uk/news/let_solar_back_into_cfds_energy_uk_urges_government (accessed on 15 March 2019).

- Guidolin, M.; Guseo, R. The German energy transition: Modeling competition and substitution between nuclear power and Renewable Energy Technologies. Renew. Sustain. Energy Rev. 2016, 60, 1498–1504. [Google Scholar] [CrossRef]

| Installed Capacity | Number of Installations | |||||

|---|---|---|---|---|---|---|

| Sector | R | C | U | R | C | U |

| Best Model | 3-shock (F1 + F2 + F1) | 2-shock (F1 + F2) | 6-shock F1 (5 A) | 3-shock (F1 + F2 + F1) | 3-shock (F1 + F2 + F1) | 5-shock F1 (4 A) |

| q | 0.003 | 0.044 | 0.041 | 0.004 | 0.005 | 0.048 |

| m | 31,123 | 4477 | 5914 | 27,457,642 | 28,841,448 | 448 |

| A1 | 44.5 | 3.3 | 97.9 | 40.4 | 15.8 | 110.0 |

| a1 | 0.0 | 0 | 13 | 0 | 0 | 13 |

| b1 | 20 | 25 | 14 | 20 | 23 | 14 |

| A2 (c2) | 0.4 | 0.1 | 36.3 | 0.4 | 0.3 | 40.1 |

| a2 | 20 | 68 | 25 | 20 | 20 | 25 |

| b2(A2) | 154 | 4 | 26 | 133 | 104 | 25 |

| A3 | 5.4 | 79.7 | 4.6 | 5 | 133.8 | |

| a3 | 24 | 37 | 24 | 24 | 36.99 | |

| b3 | 73 | 37 | 74 | 76 | 37.20 | |

| A4 | 22.5 | 20.4 | ||||

| a4 | 49 | 49 | ||||

| b4 | 50 | 50 | ||||

| A5 | 4.6 | 110.0 | ||||

| a5 | 61 | 61.6 | ||||

| b5 | 62 | 62.1 | ||||

| A6 | 97.9 | |||||

| a6 | 94 | |||||

| b6 | 95 | |||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bunea, A.M.; Guidolin, M.; Manfredi, P.; Della Posta, P. Diffusion of Solar PV Energy in the UK: A Comparison of Sectoral Patterns. Forecasting 2022, 4, 456-476. https://doi.org/10.3390/forecast4020026

Bunea AM, Guidolin M, Manfredi P, Della Posta P. Diffusion of Solar PV Energy in the UK: A Comparison of Sectoral Patterns. Forecasting. 2022; 4(2):456-476. https://doi.org/10.3390/forecast4020026

Chicago/Turabian StyleBunea, Anita M., Mariangela Guidolin, Piero Manfredi, and Pompeo Della Posta. 2022. "Diffusion of Solar PV Energy in the UK: A Comparison of Sectoral Patterns" Forecasting 4, no. 2: 456-476. https://doi.org/10.3390/forecast4020026

APA StyleBunea, A. M., Guidolin, M., Manfredi, P., & Della Posta, P. (2022). Diffusion of Solar PV Energy in the UK: A Comparison of Sectoral Patterns. Forecasting, 4(2), 456-476. https://doi.org/10.3390/forecast4020026