Crises, Financial Data and Public Sector Reform: Activity-Based Costing and Cost Allocation in Greece—A Case Study of the Independent Authority for Public Revenue †

Abstract

1. Introduction

2. Literature Review

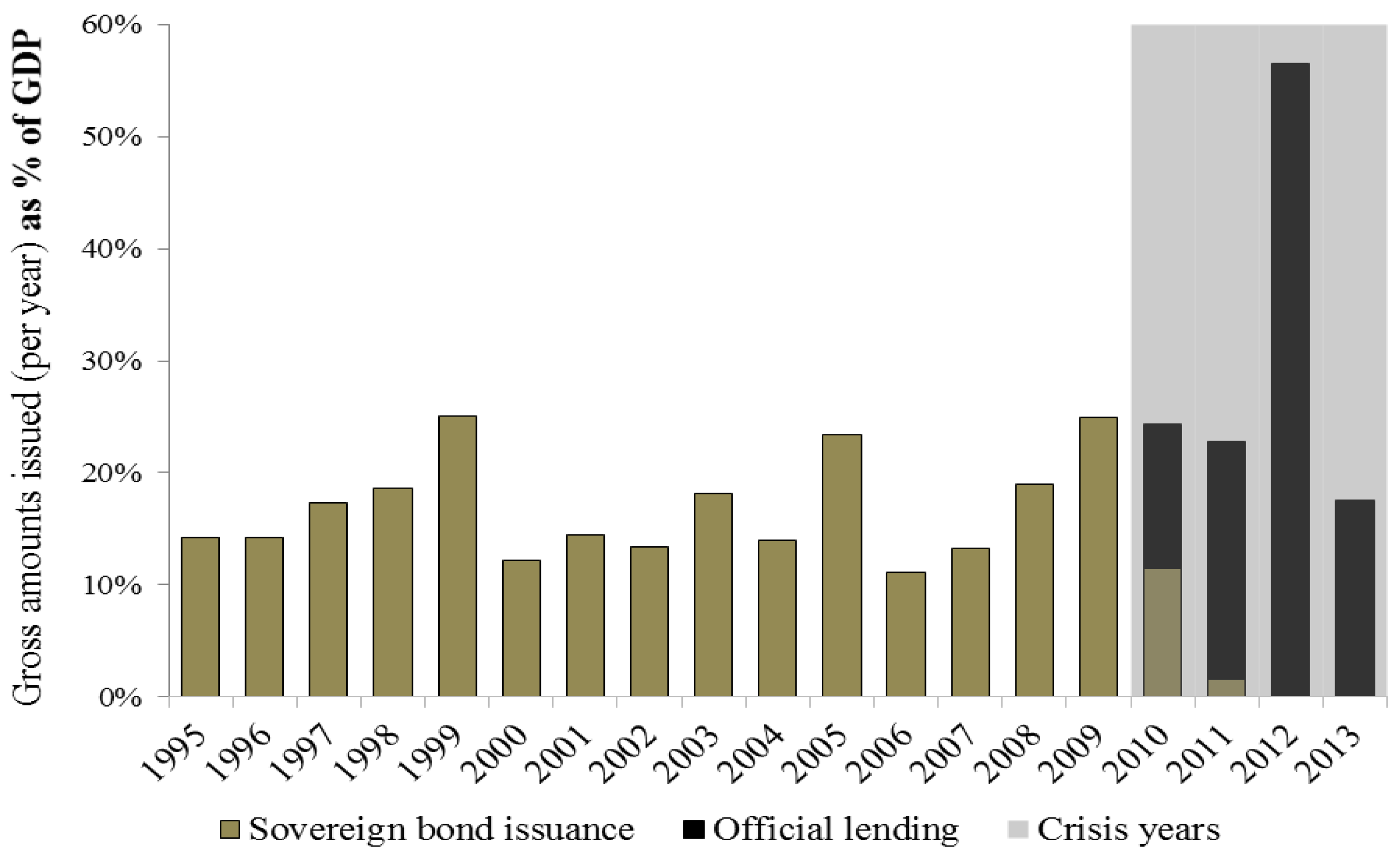

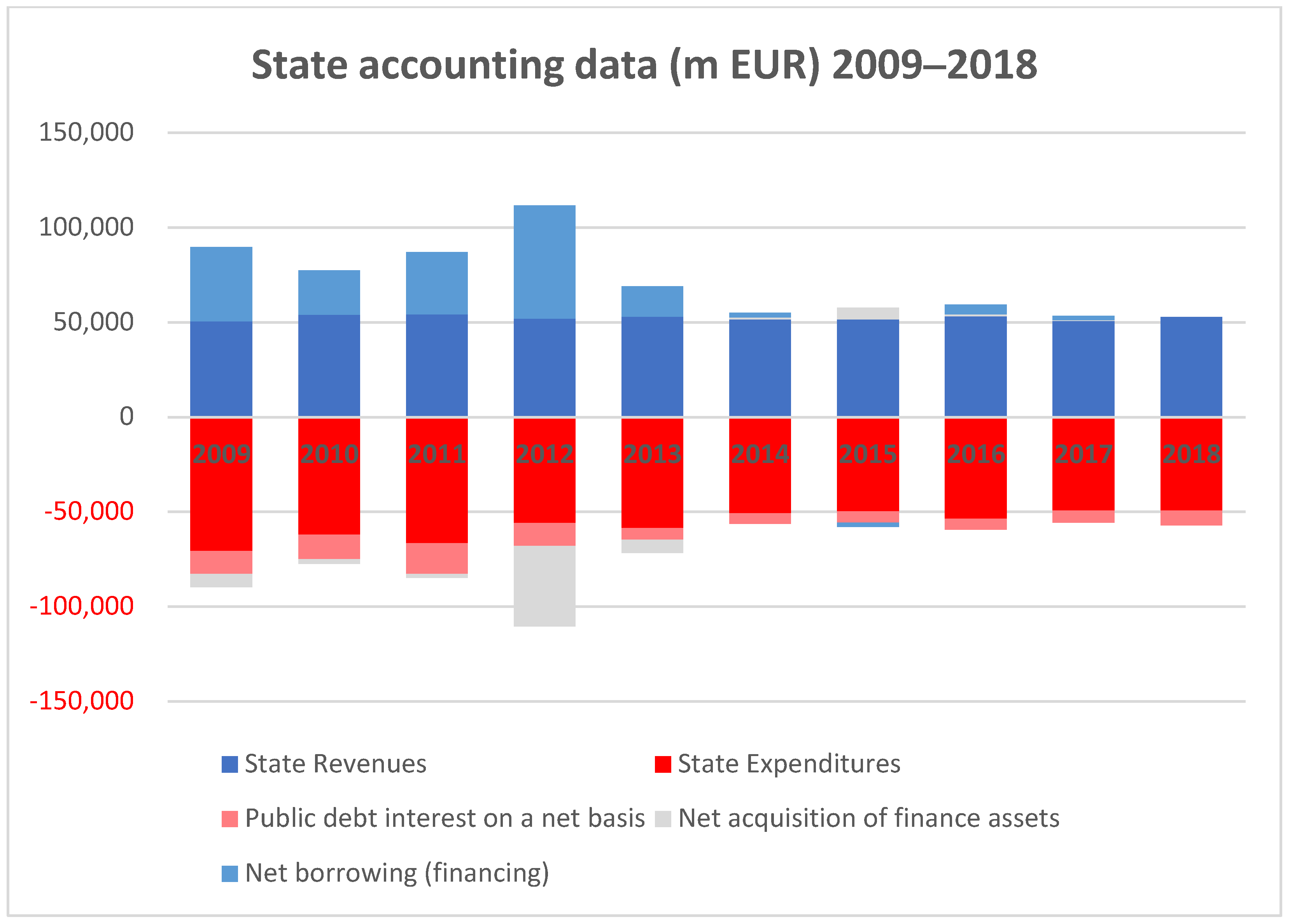

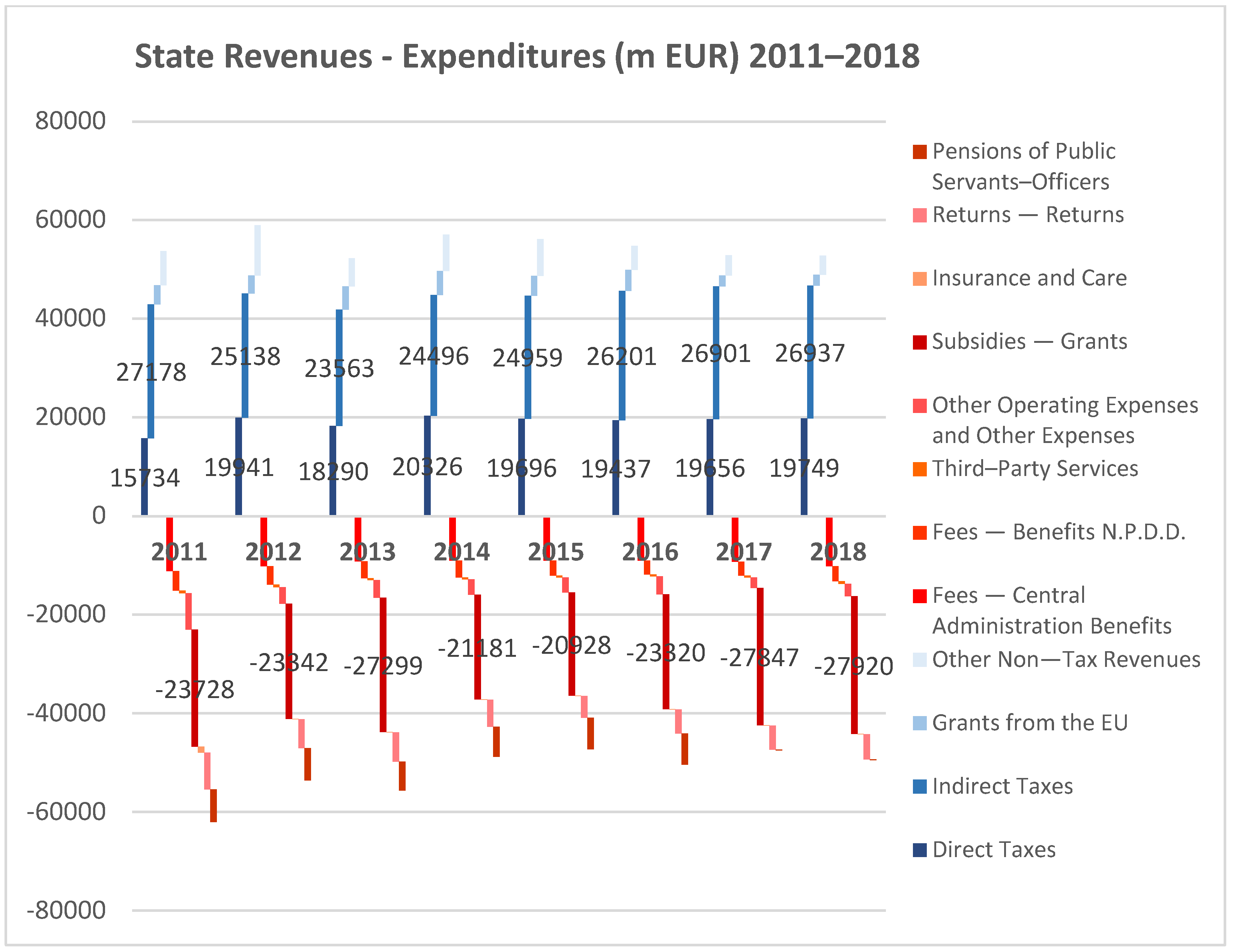

3. Analysis of Greek State Financial Data

4. Short Presentation of Greek Adjustment Programs and Public Structural Changes

4.1. Greek Adjustment Programs

- Austerity measures (reductions in wages/pensions, reductions in the cost of public services such as health, education and social benefits);

- Reducing public investments;

- Raising of taxes;

- Reforms in labor market and public administration;

- Privatization of state-owned assets (for 49 years to 99 years, public property such as ports, airports, railways, energy (electric, gas, wild, solar, etc.), revenues from archeological sites and monuments, etc.);

- Banking systems (many high-risk loans and lower deposits led to recapitalization in 2013, 2014 and 2015); also, capital control measures were taken in June 2015.

4.2. Structural Changes at the Greek Ministry of Finance

4.3. The Independent Authority for Public Revenue of Greece (I.A.P.R.)

- 11 organic units directly reporting to the Governor;

- 5 General Directorates;

- Directorates (22 directorates, 4 stand-alone departments);

- 13 Special Decentralized Services and Regional Services (including the YEDDEs, the DOYs, Customs and local Customs offices and the Chemical Labs).

5. Costing Accounting Methods at Public Authorities

5.1. Methodology of ABC Systems

5.2. Implementation of ABC

- Identify expenses (cost resources).

- Identify end-products/services (outputs–cost objects).

- Identify activities (cost pools).

- Assign resources to activities (based on resource driver).

- Trace/allocate overhead costs to activities and cost objects.

- Assign activities to products/services (based on activity driver).

5.3. Cost Analysis of Independent Authority for Public Revenue (I.A.P.R.)

- Taxation: activities for valid statements/declarations, compliance for non-submission, non-payments and others and activities for audits, inspections, investigations and others.

- Duties: activities for valid custom statements (imports and exports), compliance and others and activities for subsequent audits, prosecution checks, smuggling checks (energy, tobacco and alcohol), illegal trade, inspections and others.

- Chemical analyses: activities for chemical analyses, classification statements and others and activities for audits, inspections (energy, tobacco and alcohol) and supporting measures for the protection of public health and the environment.

- IT: activities for providing and supporting e-services to citizens, businesses and public sector bodies, with a view to facilitating transactions, reducing red tape and simplifying processes and others.

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- World Bank. World Development Report, 1997: The State in A Changing World; The World Bank: Washington, DC, USA, 1997. [Google Scholar]

- Reinhart, C.M.; Rogoff, K.S. This Time is Different: A Panoramic View of Eight Centuries of Financial Crises; NBER Working Papers 13882; National Bureau of Economic Research, Inc.: Cambridge, MA, USA, 2008. [Google Scholar]

- Cooper, R.; Kaplan, R.S. The Design of Cost Management Systems; Prentice Hall: Englewood Cliffs, NJ, USA, 1991; p. 580. [Google Scholar]

- Johnson, H.T.; Kaplan, R.S. Relevance Lost Rise and Fall of Management Accounting; Harvard Business School Press: Boston, MA, USA, 1987. [Google Scholar]

- Vazakidis, A.; Karagiannis, I.; Tsialta, A. Activity-Based Costing in the Public Sector. J. Soc. Sci. 2010, 6, 376–382. [Google Scholar]

- Reinhart, C.M.; Trebesch, R. The Pitfalls of External Dependence: Greece, 1829–2015; Brookings Papers on Economic Activity; Economic Studies Program, The Brookings Institution: Washington, DC, USA, 2015; Volume 2, pp. 307–328. [Google Scholar]

- European Commission. The Second Economic Adjustment Programme for Greece: Fourth Review; Occasional Paper no. 192; European Commission: Brussels, Belgium, 2014. [Google Scholar]

- Kindreich, A. The Greek Financial Crisis (2009–2016); Chartered Financial Analyst (CFA) Institute: Charlottesville, VA, USA, 2017. [Google Scholar]

- Hellenic Ministry of Finance, Hellenic Court of Audit. Available online: https://minfin.gov.gr/apologismos-isologismos-kai-loipes-chrimatooikonomikes-katastaseis/ (accessed on 1 January 2024).

- Ozturk, S.; Sozdemir, A. Effects of Global Financial Crisis on Greece Economy. Procedia Econ. Financ. 2015, 23, 568–575. [Google Scholar] [CrossRef]

- Oseifuah, E.K. Activity Based Costing (ABC) in the public sector: Benefits and challenges. Probl. Perspect. Manag. 2014, 12, 581–587. [Google Scholar]

- Vazakidis, A.; Karagiannis, I. Activity-Based Costing in Higher Education: A Study of Implementing Activity-Based Costing in University of Macedonia. In Proceeding of the 5th Conference of the Hellenic Finance and Accounting Association, Thessaloniki, Greece, 15–16 December 2006; p. 11. [Google Scholar]

- Lima, C.M.F. The applicability of the principles of activity based costing in a higher education institution. Econ. Manag. Res. Proj. Int. J. 2012, 1, 57–65. [Google Scholar]

- The Independent Authority for Public Revenue. Available online: https://www.aade.gr/apologistikes-ektheseis (accessed on 1 February 2024).

- The Transparency Program Initiative. Available online: www.diavgeia.gov.gr (accessed on 1 February 2024).

- Kyriakidou, E.; Vazakidis, A. Financial Crisis and Public Reforms: Moving from Public Administration to Public Management. Cost Allocation and Performance Information for Decision making Process in the Public Sector. The Case of the Greek Public Sector under the Greek Crisis. In Proceedings of the 9th International Conference on Information and Communication Technologies in Agriculture, Food and Environment (HAICTA 2020), Thessaloniki, Greece, 24–27 September 2020; CEUR Workshop Proceeding. Volume 2761, pp. 252–262. [Google Scholar]

- Vazakidis, A.; Kyriakidou, E. Time-Driven Activity-Based Costing in the Public Sector. The Case of Greek General Chemical State Laboratory under the Greek Crisis. J. Soc. Sci. 2020, 16, 49–58. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| State Revenues and Expenditures (m EUR) 1 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|---|---|---|

| Direct Taxes | 15.734 | 19.941 | 18.290 | 20.326 | 19.696 | 19.437 | 19.656 | 19.749 |

| Indirect Taxes | 27.178 | 25.138 | 23.563 | 24.496 | 24.959 | 26.201 | 26.901 | 26.937 |

| Grants from the EU | 3.900 | 3.680 | 4.694 | 4.845 | 4.036 | 4.276 | 2.237 | 2.248 |

| Other Non-Tax Revenues | 6.894 | 10.223 | 5.743 | 7.411 | 7.470 | 4.869 | 4.070 | 3.844 |

| Fees—Central Administration Benefits | −11.179 | −10.183 | −9.212 | −9.019 | −9.017 | −9.069 | −9.276 | −10.191 |

| Fees—Benefits N.P.D.D. | −3.957 | −3.743 | −3.385 | −3.426 | −3.070 | −2.770 | −2.838 | −3.063 |

| Third-Party Services | −518 | −478 | −412 | −422 | −395 | −403 | −375 | −515 |

| Other Operating Expenses and Other Expenses | −7.408 | −3.390 | −3.526 | −3.131 | −3.028 | −3.617 | −2.089 | −2.526 |

| Subsidies—Grants | −23.728 | −23.342 | −27.299 | −21.181 | −20.928 | −23.320 | −27.847 | −27.920 |

| Insurance and Care | −1.174 | −61 | −73 | −58 | −56 | −58 | −63 | −67 |

| Returns—Returns | −7.479 | −5.843 | −5.905 | −5.486 | −4.401 | −4.828 | −4.888 | −5.074 |

| Pensions of Public Servants—Officers | −6.572 | −6.564 | −5.868 | −6.110 | −6.411 | −6.370 | −132 | −113 |

| State Operating Results | −6.298 | 7.390 | −1.377 | 10.259 | 10.870 | 6.364 | 7.373 | 5.327 |

| IARP Expenses (k EUR) 1 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|

| Personnel expenses | 349.049 | 367.388 | 364.517 | 376.099 | 400.944 | 413.510 |

| Supplies of materials, equipment | 366 | 594 | 5.225 | 5.955 | 10.529 | 6.530 |

| Operating, maintenance, travel and other expenses | 11.483 | 12.332 | 6.040 | 5.557 | 13.048 | 11.840 |

| Expenses for legal and technical services | 10.390 | 3.123 | 8 | 26 | 7 | 39 |

| Expenses for banking services | 949 | 1.114 | 3.971 | 8.694 | 3.249 | 12.723 |

| Other expenses (third party) | 19.338 | 3.198 | 7.122 | 465 | 587 | 594 |

| Leasing expenses | 18.635 | 18.989 | 17.942 | 17.676 | 18.569 | 19.063 |

| Subscriptions/contributions to organizations | 46 | 29 | 46 | 29 | 29 | 302 |

| Returns/refunds of special excise tax | 26.950 | 28.972 | 11 | 3 | 0 | 0 |

| Program costs | 401 | 460 | 0 | 0 | 0 | 0 |

| Compensation expenses and other (court decisions, etc.) | 5.922 | 0 | 17.992 | 9.040 | 13.939 | 7.112 |

| Expenditure of public lotteries, etc. | 7.700 | 12.937 | 11.387 | 22.732 | 23.190 | 28.625 |

| Total | 451.229 | 449.134 | 434.260 | 446.276 | 484.091 | 500.338 |

| Personnel per Category 1 | Number | % |

|---|---|---|

| Tax officers | 7.254 | 66% |

| Customs officers | 2.342 | 21% |

| Chemists | 293 | 3% |

| Information technology officers | 223 | 2% |

| Other officers | 932 | 8% |

| Total | 11.044 |

| Number of Financial Audits 1 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|

| Audit Center for Large Companies | 407 | 417 | 455 | 442 | 480 | 593 |

| Audit Center for Taxpayers of High Wealth | 953 | 950 | 1.497 | 761 | 1.200 | 923 |

| Taxation Services of Société Anonyme Companies | 2.465 | 2.771 | 2.283 | 2.071 | ||

| Regional Taxation Services | 22.954 | 22.246 | 22.823 | 21.089 | 11.829 | 13.329 |

| Audit Centers and Regional Taxation Services | 10.481 | 10.186 | ||||

| Total | 26.779 | 26.384 | 27.058 | 24.363 | 23.990 | 25.031 |

| Number of Financial Inspections (On-Site) 1 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|---|---|

| Regional Taxation Services | 86.591 | 86.092 | 79.318 | 36.894 | 39.132 | 59.676 |

| Services for Investigations and Safeguarding Public Revenue (Attica, Thessaloniki, Patras, Iraklion) | 18.148 | 23.952 | 25.469 | 17.923 | 25.307 | 21.087 |

| Total | 104.739 | 110.044 | 104.787 | 54.817 | 64.439 | 80.763 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kyriakidou, E.; Vazakidis, A. Crises, Financial Data and Public Sector Reform: Activity-Based Costing and Cost Allocation in Greece—A Case Study of the Independent Authority for Public Revenue. Proceedings 2024, 111, 29. https://doi.org/10.3390/proceedings2024111029

Kyriakidou E, Vazakidis A. Crises, Financial Data and Public Sector Reform: Activity-Based Costing and Cost Allocation in Greece—A Case Study of the Independent Authority for Public Revenue. Proceedings. 2024; 111(1):29. https://doi.org/10.3390/proceedings2024111029

Chicago/Turabian StyleKyriakidou, Eleftheria, and Athanasios Vazakidis. 2024. "Crises, Financial Data and Public Sector Reform: Activity-Based Costing and Cost Allocation in Greece—A Case Study of the Independent Authority for Public Revenue" Proceedings 111, no. 1: 29. https://doi.org/10.3390/proceedings2024111029

APA StyleKyriakidou, E., & Vazakidis, A. (2024). Crises, Financial Data and Public Sector Reform: Activity-Based Costing and Cost Allocation in Greece—A Case Study of the Independent Authority for Public Revenue. Proceedings, 111(1), 29. https://doi.org/10.3390/proceedings2024111029