Numerical Investigation of the Time-Fractional Black–Scholes Problem Using the Caputo Fractional Derivative in the Financial Industry

Abstract

1. Introduction

2. Basic Concepts and Characteristics of FC and Sawi Transform

3. Formulation of SHPTS

4. Existence and Uniqueness Analysis of the Fractional B-S Model

4.1. Existence and Uniqueness Theorem

4.2. Investigation of Convergence Behavior for the Fractional B-S Problem

5. Numerical Problems

5.1. Problem 1

5.2. Problem 2

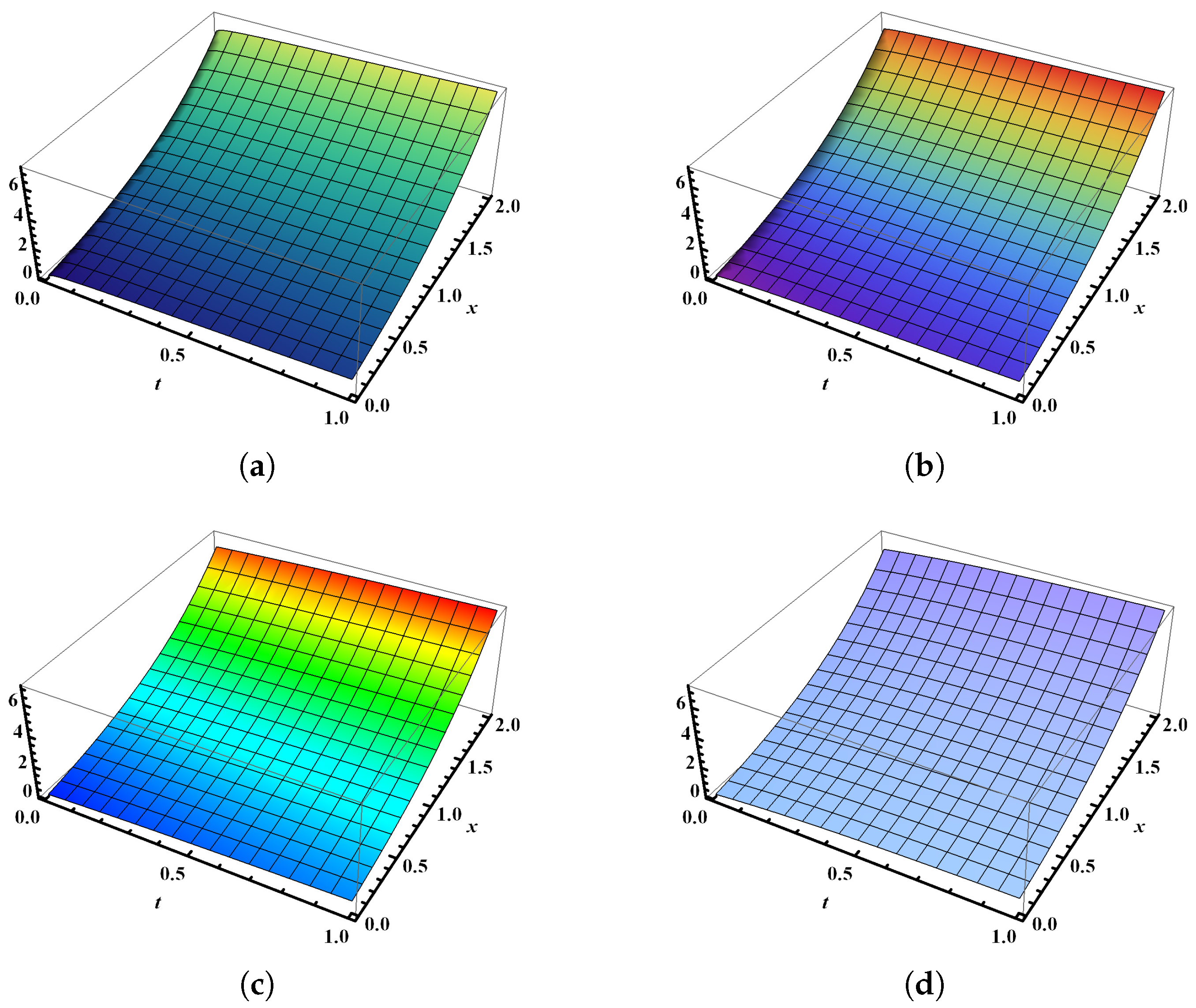

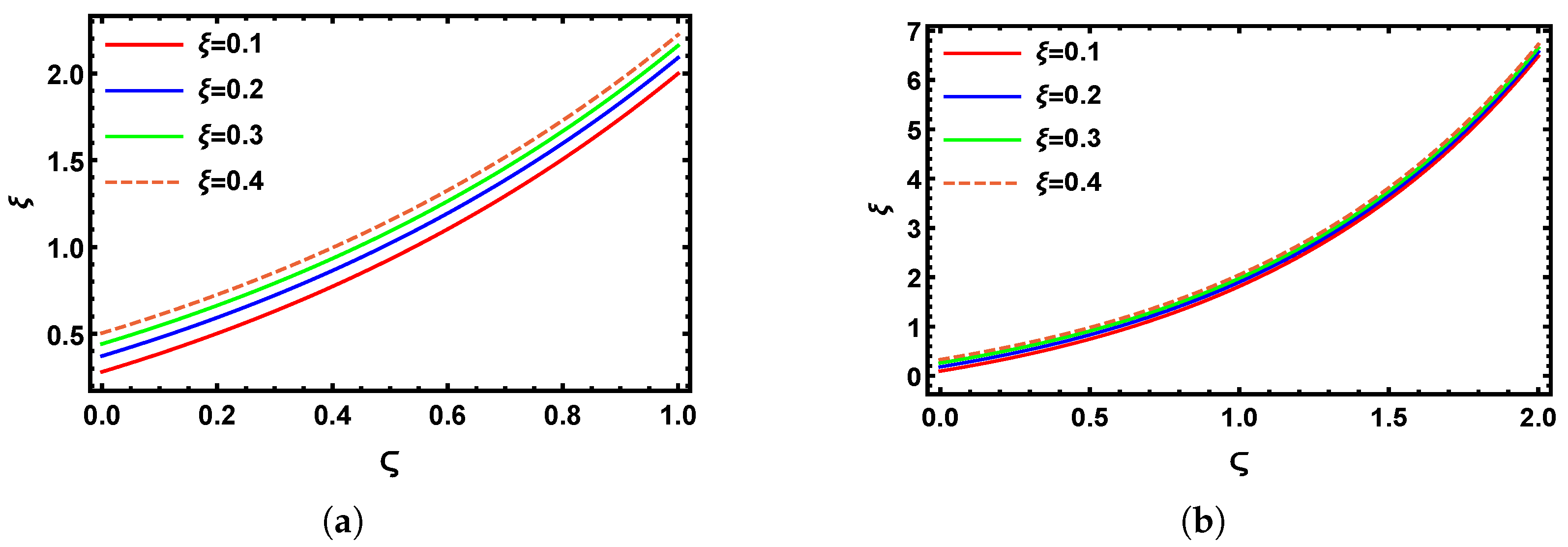

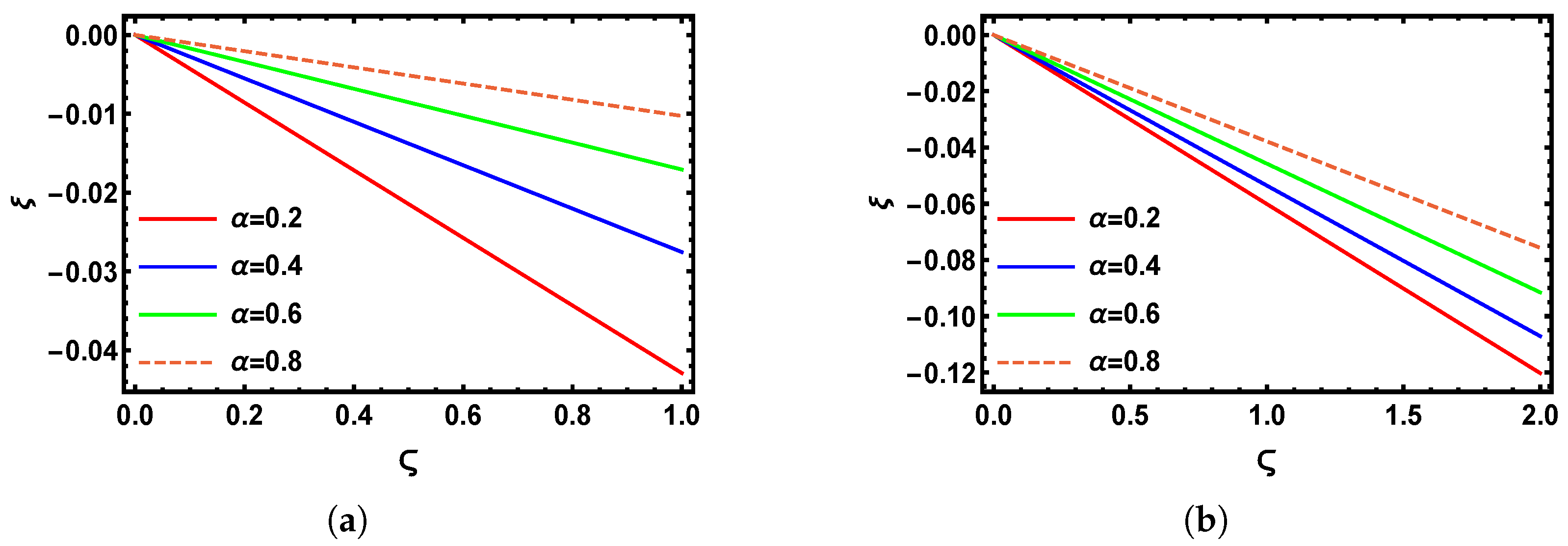

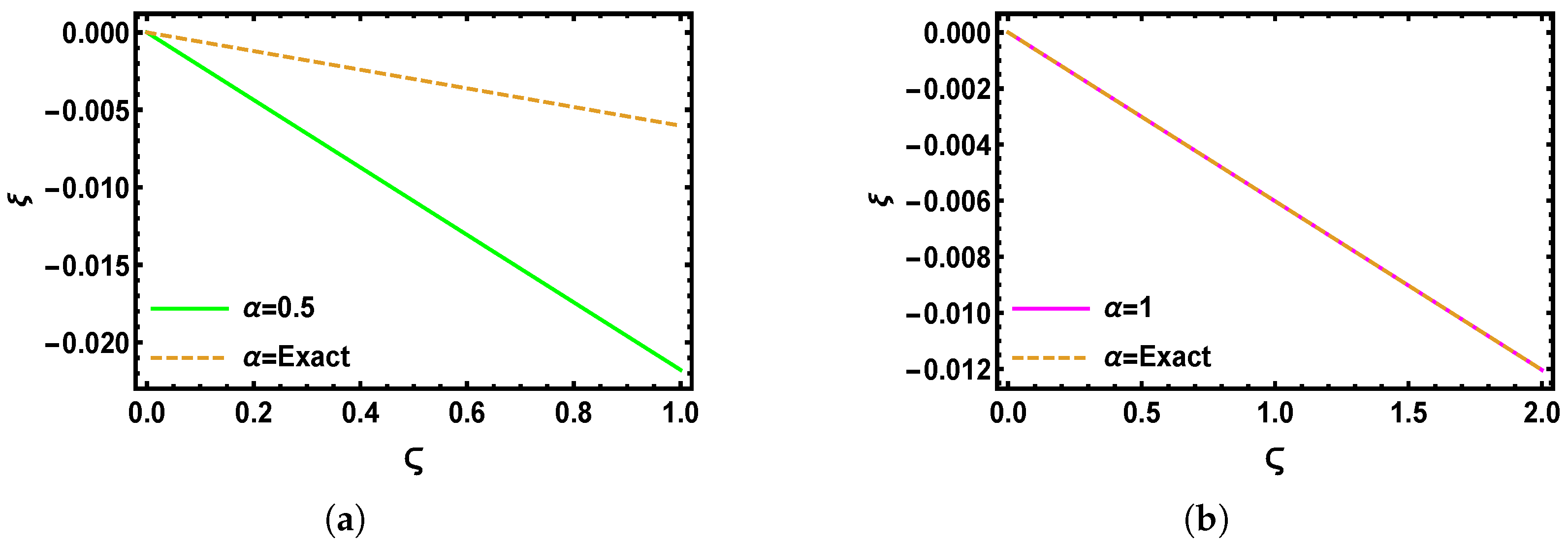

6. Numerical Findings and Analysis

7. Concluding Remarks

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Caputo, M. Linear models of dissipation whose Q is almost frequency independent—II. Geophys. J. Int. 1967, 13, 529–539. [Google Scholar] [CrossRef]

- Garrappa, R. Numerical solution of fractional differential equations: A survey and a software tutorial. Mathematics 2018, 6, 16. [Google Scholar] [CrossRef]

- Jafarian, A.; Mokhtarpour, M.; Baleanu, D. Artificial neural network approach for a class of fractional ordinary differential equation. Neural Comput. Appl. 2017, 28, 765–773. [Google Scholar] [CrossRef]

- Sun, H.; Zhang, Y.; Baleanu, D.; Chen, W.; Chen, Y. A new collection of real world applications of fractional calculus in science and engineering. Commun. Nonlinear Sci. Numer. Simul. 2018, 64, 213–231. [Google Scholar] [CrossRef]

- Magin, R.L. Fractional calculus models of complex dynamics in biological tissues. Comput. Math. Appl. 2010, 59, 1586–1593. [Google Scholar] [CrossRef]

- Hammouch, Z.; Yavuz, M.; Özdemir, N. Numerical solutions and synchronization of a variable-order fractional chaotic system. Math. Model. Numer. Simul. Appl. 2021, 1, 11–23. [Google Scholar] [CrossRef]

- Biswas, S.; Ghosh, U.; Raut, S. Construction of fractional granular model and bright, dark, lump, breather types soliton solutions using Hirota bilinear method. Chaos Solitons Fractals 2023, 172, 113520. [Google Scholar] [CrossRef]

- Nadeem, M.; Li, F.; Ahmad, H. Modified Laplace variational iteration method for solving fourth-order parabolic partial differential equation with variable coefficients. Comput. Math. Appl. 2019, 78, 2052–2062. [Google Scholar] [CrossRef]

- Singh, B.K.; Kumar, P. Fractional variational iteration method for solving fractional partial differential equations with proportional delay. Int. J. Differ. Equations 2017, 2017, 5206380. [Google Scholar] [CrossRef]

- Momani, S.; Shawagfeh, N. Decomposition method for solving fractional Riccati differential equations. Appl. Math. Comput. 2006, 182, 1083–1092. [Google Scholar] [CrossRef]

- Zurigat, M.; Momani, S.; Odibat, Z.; Alawneh, A. The homotopy analysis method for handling systems of fractional differential equations. Appl. Math. Model. 2010, 34, 24–35. [Google Scholar] [CrossRef]

- Akram, S.; Ann, Q.U. Newton raphson method. Int. J. Sci. Eng. Res. 2015, 6, 1748–1752. [Google Scholar]

- Phang, C.; Kanwal, A.; Loh, J.R. New collocation scheme for solving fractional partial differential equations. Hacet. J. Math. Stat. 2020, 49, 1107–1125. [Google Scholar] [CrossRef]

- He, J.H. Homotopy perturbation method: A new nonlinear analytical technique. Appl. Math. Comput. 2003, 135, 73–79. [Google Scholar] [CrossRef]

- He, J.H. Addendum: New interpretation of homotopy perturbation method. Int. J. Mod. Phys. B 2006, 20, 2561–2568. [Google Scholar] [CrossRef]

- Yu, D.N.; He, J.H.; Garcıa, A.G. Homotopy perturbation method with an auxiliary parameter for nonlinear oscillators. J. Low Freq. Noise Vib. Act. Control 2019, 38, 1540–1554. [Google Scholar] [CrossRef]

- Zhang, X.; Zhao, J.; Liu, J.; Tang, B. Homotopy perturbation method for two dimensional time-fractional wave equation. Appl. Math. Model. 2014, 38, 5545–5552. [Google Scholar] [CrossRef]

- Biazar, J.; Eslami, M. A new homotopy perturbation method for solving systems of partial differential equations. Comput. Math. Appl. 2011, 62, 225–234. [Google Scholar] [CrossRef]

- Saberi-Nadjafi, J.; Ghorbani, A. He’s homotopy perturbation method: An effective tool for solving nonlinear integral and integro-differential equations. Comput. Math. Appl. 2009, 58, 2379–2390. [Google Scholar] [CrossRef]

- Ganji, D.D.; Rajabi, A. Assessment of homotopy–perturbation and perturbation methods in heat radiation equations. Int. Commun. Heat Mass Transf. 2006, 33, 391–400. [Google Scholar] [CrossRef]

- Shakeri, F.; Dehghan, M. Inverse problem of diffusion equation by He’s homotopy perturbation method. Phys. Scr. 2007, 75, 551. [Google Scholar] [CrossRef]

- Noor, M.A.; Mohyud-Din, S.T. Homotopy perturbation method for solving sixth-order boundary value problems. Comput. Math. Appl. 2008, 55, 2953–2972. [Google Scholar] [CrossRef]

- Akram, M.; Bilal, M. Analytical solution of bipolar fuzzy heat equation using homotopy perturbation method. Granul. Comput. 2023, 8, 1253–1266. [Google Scholar] [CrossRef]

- Nadeem, M.; Yao, S.W. Solving the fractional heat-like and wave-like equations with variable coefficients utilizing the Laplace homotopy method. Int. J. Numer. Methods Heat Fluid Flow 2021, 31, 273–292. [Google Scholar] [CrossRef]

- Thabet, H.; Kendre, S. Modified least squares homotopy perturbation method for solving fractional partial differential equations. Malaya J. Mat. 2018, 6, 420–427. [Google Scholar] [CrossRef] [PubMed]

- Elbeleze, A.A.; Kılıçman, A.; Taib, B.M. Homotopy Perturbation Method for Fractional Black-Scholes European Option Pricing Equations Using Sumudu Transform. Math. Probl. Eng. 2013, 2013, 524852. [Google Scholar] [CrossRef]

- Ravi Kanth, A.; Aruna, K. Solution of time fractional Black-Scholes European option pricing equation arising in financial market. Nonlinear Eng. 2016, 5, 269–276. [Google Scholar] [CrossRef]

- Jena, R.M.; Chakraverty, S. A new iterative method based solution for fractional Black–Scholes option pricing equations (BSOPE). SN Appl. Sci. 2019, 1, 95. [Google Scholar] [CrossRef]

- Prathumwan, D.; Trachoo, K. On the solution of two-dimensional fractional Black–Scholes equation for European put option. Adv. Differ. Equ. 2020, 2020, 146. [Google Scholar] [CrossRef]

- Roul, P. A high accuracy numerical method and its convergence for time-fractional Black-Scholes equation governing European options. Appl. Numer. Math. 2020, 151, 472–493. [Google Scholar] [CrossRef]

- Zhao, H.; Tian, H. Finite difference methods of the spatial fractional Black–Schloes equation for a European call option. IMA J. Appl. Math. 2017, 82, 836–848. [Google Scholar] [CrossRef]

- Kazmi, K. A second order numerical method for the time-fractional Black–Scholes European option pricing model. J. Comput. Appl. Math. 2023, 418, 114647. [Google Scholar] [CrossRef]

- Sarikaya, M.Z.; Ogunmez, H. On New Inequalities via Riemann-Liouville Fractional Integration. Abstr. Appl. Anal. 2012, 2012, 428983. [Google Scholar] [CrossRef]

- Arora, S.; Mathur, T.; Agarwal, S.; Tiwari, K.; Gupta, P. Applications of fractional calculus in computer vision: A survey. Neurocomputing 2022, 489, 407–428. [Google Scholar] [CrossRef]

- Mathai, A.M.; Haubold, H.J. Special Functions for Applied Scientists; Springer: New York, NY, USA, 2008. [Google Scholar]

- Nadeem, M.; Yilin, C.; Kumar, D.; Alsayyad, Y. Analytical solution of fuzzy heat problem in two-dimensional case under Caputo-type fractional derivative. PLoS ONE 2024, 19, e0301719. [Google Scholar] [CrossRef] [PubMed]

- Attaweel, M.E.; Almassry, H.A. A new application of sawi transform for solving volterra integral equations and volterra integro-differential equations. Libyan J. Sci. 2019, 22, 64–77. [Google Scholar]

- Kumar, S.; Kumar, D.; Singh, J. Numerical computation of fractional Black–Scholes equation arising in financial market. Egypt. J. Basic Appl. Sci. 2014, 1, 177–183. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

at () | at () | Exact () | Absolute Error at () | |

|---|---|---|---|---|

| 0.1 | 1.828630 | 0.737291 | 0.771838 | 0.034547 |

| 0.2 | 1.944860 | 0.853523 | 0.888069 | 0.034546 |

| 0.3 | 2.073320 | 0.981979 | 1.016530 | 0.034555 |

| 0.4 | 2.215290 | 1.123950 | 1.158490 | 0.034540 |

| 0.5 | 2.372180 | 1.280840 | 1.315390 | 0.034550 |

| 0.6 | 2.545580 | 1.454240 | 1.488790 | 0.034550 |

| 0.7 | 2.737210 | 1.645870 | 1.680420 | 0.034550 |

| 0.8 | 2.949000 | 1.857660 | 1.892210 | 0.034550 |

| 0.9 | 3.183060 | 2.091720 | 2.126270 | 0.034550 |

| 1.0 | 3.441740 | 2.350400 | 2.384950 | 0.034550 |

at () | at () | Exact () | Absolute Error at () | |

|---|---|---|---|---|

| 0.1 | 0.089146 | 0.089219 | 0.089247 | 0.000028 |

| 0.2 | 0.178293 | 0.178439 | 0.178494 | 0.000055 |

| 0.3 | 0.267439 | 0.267658 | 0.267742 | 0.000084 |

| 0.4 | 0.356586 | 0.356878 | 0.356989 | 0.000111 |

| 0.5 | 0.445732 | 0.446097 | 0.446237 | 0.000140 |

| 0.6 | 0.534878 | 0.535316 | 0.535484 | 0.000168 |

| 0.7 | 0.624025 | 0.624536 | 0.624731 | 0.000195 |

| 0.8 | 0.713171 | 0.713755 | 0.713979 | 0.000224 |

| 0.9 | 0.802318 | 0.802975 | 0.803227 | 0.000252 |

| 1.0 | 0.891464 | 0.892194 | 0.892474 | 0.000280 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nadeem, M.; Cheng, B.; Iambor, L.F. Numerical Investigation of the Time-Fractional Black–Scholes Problem Using the Caputo Fractional Derivative in the Financial Industry. Fractal Fract. 2025, 9, 490. https://doi.org/10.3390/fractalfract9080490

Nadeem M, Cheng B, Iambor LF. Numerical Investigation of the Time-Fractional Black–Scholes Problem Using the Caputo Fractional Derivative in the Financial Industry. Fractal and Fractional. 2025; 9(8):490. https://doi.org/10.3390/fractalfract9080490

Chicago/Turabian StyleNadeem, Muhammad, Bitao Cheng, and Loredana Florentina Iambor. 2025. "Numerical Investigation of the Time-Fractional Black–Scholes Problem Using the Caputo Fractional Derivative in the Financial Industry" Fractal and Fractional 9, no. 8: 490. https://doi.org/10.3390/fractalfract9080490

APA StyleNadeem, M., Cheng, B., & Iambor, L. F. (2025). Numerical Investigation of the Time-Fractional Black–Scholes Problem Using the Caputo Fractional Derivative in the Financial Industry. Fractal and Fractional, 9(8), 490. https://doi.org/10.3390/fractalfract9080490