Skewed Multifractal Cross-Correlations Between Green Bond Index and Energy Futures Markets: A New Perspective Based on Change Point

Abstract

1. Introduction

2. Literature Review

3. Skewed Multifractal Analysis Methodology

3.1. Change Point Test

3.2. Skewed Multifractal Cross-Correlation Analysis

3.3. Mean MF-DCCA Portfolio Construction

4. Data

5. Empirical Results and Discussion

5.1. Cross-Correlation Test

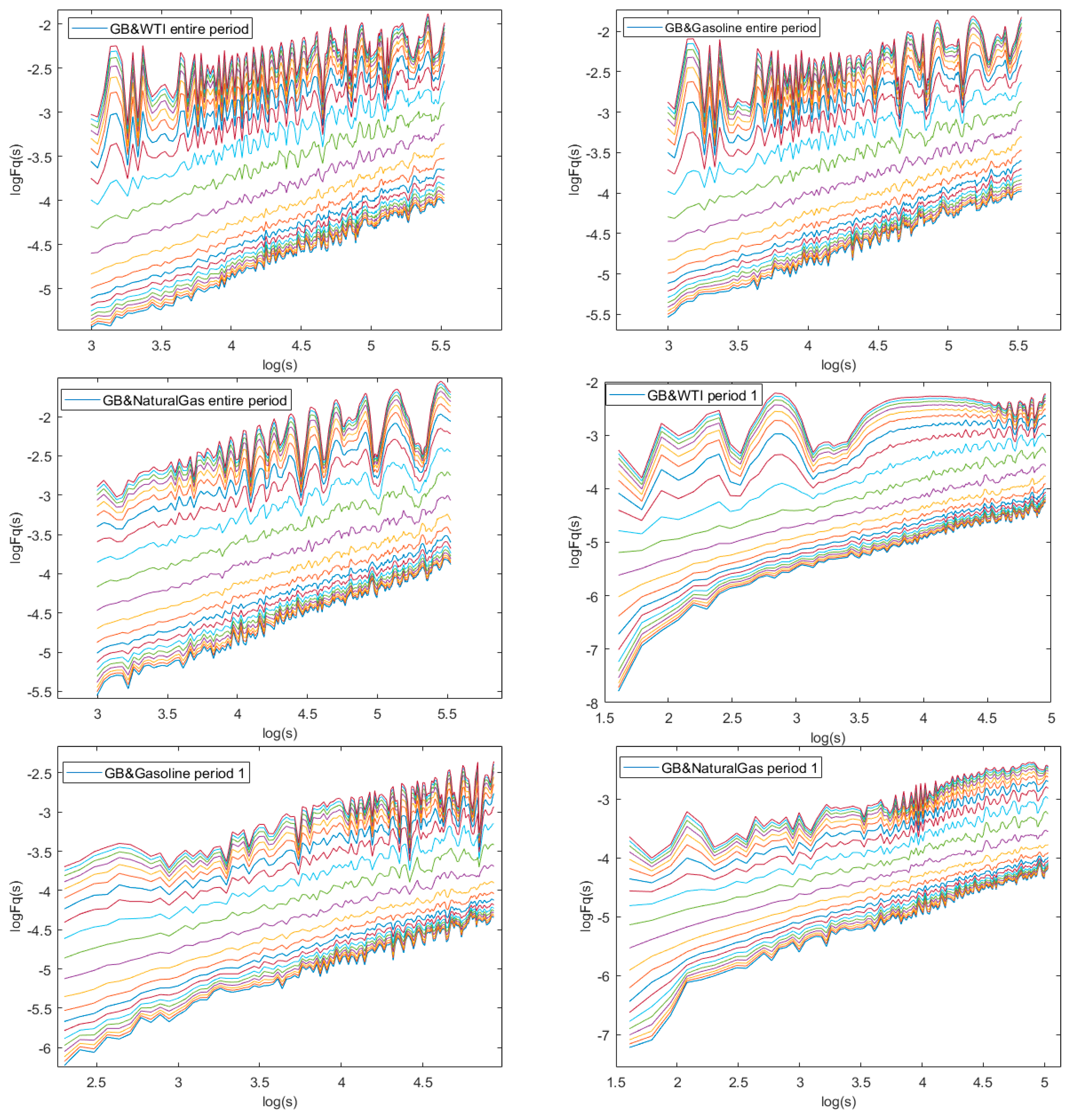

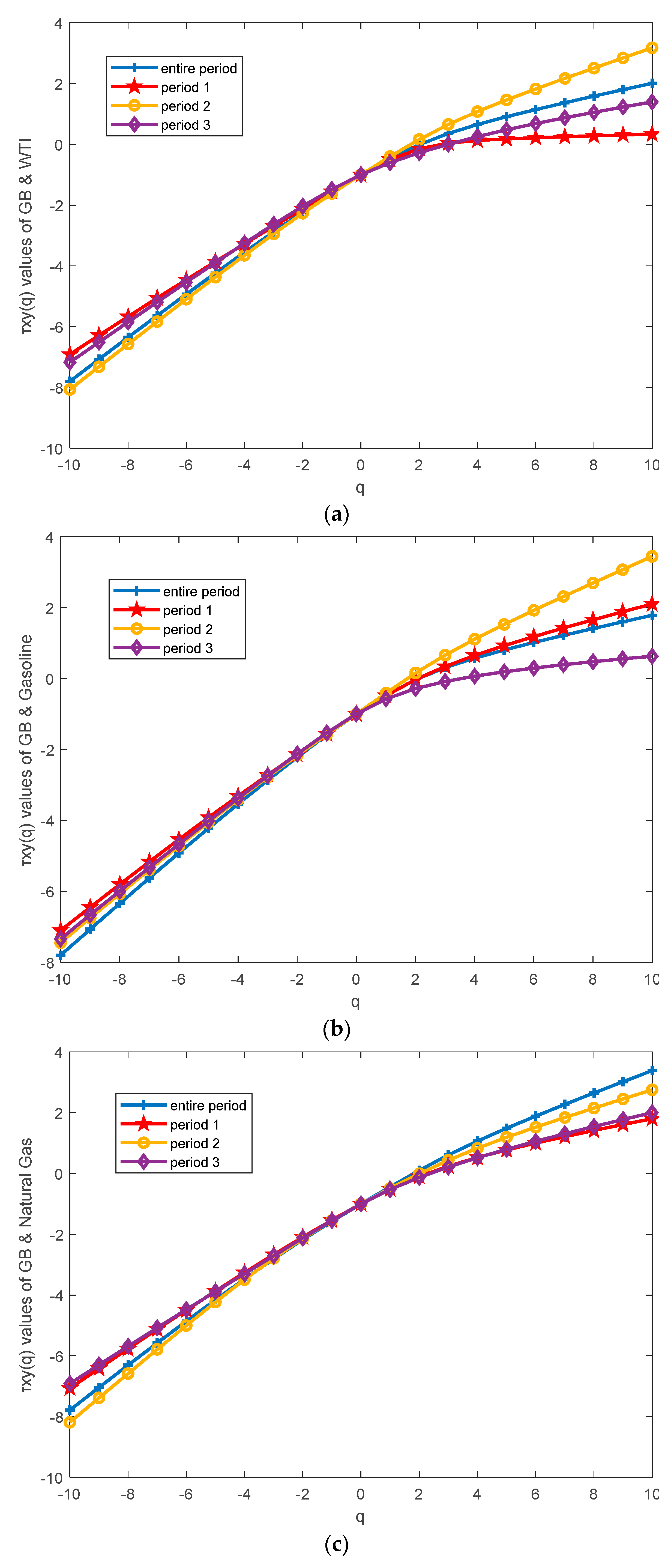

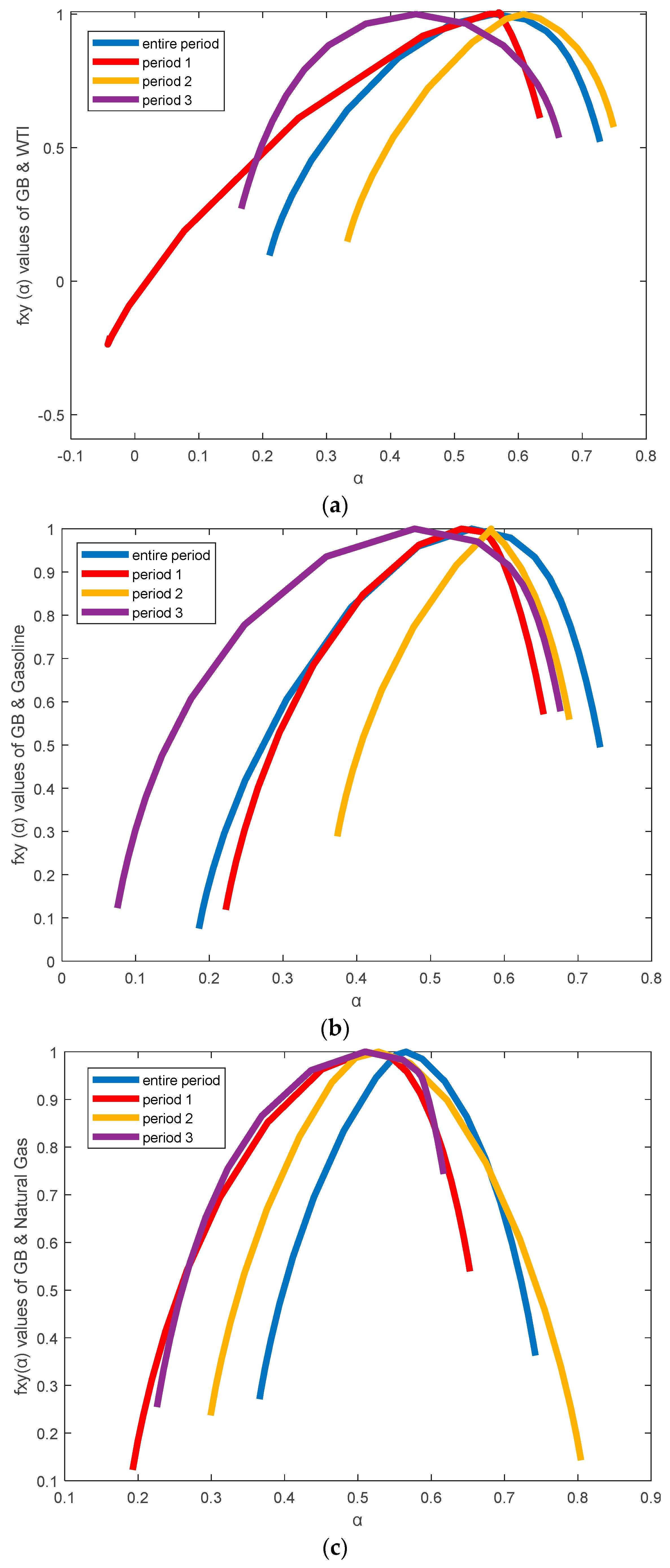

5.2. Skewed Multifractal Detrended Fluctuation Analysis

5.2.1. Results and Analysis of Change Point Identification

5.2.2. Skewed Multifractal Analysis

5.3. Portfolio Management Implications

5.4. Robustness Check of Change Points

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Weckroth, M.; Ala-Mantila, S. Socioeconomic geography of climate change views in Europe. Glob. Environ. Change-Hum. Policy Dimens. 2022, 72, 102453. [Google Scholar] [CrossRef]

- Arif, M.; Naeem, M.A.; Farid, S.; Nepal, R.; Jamasb, T. Diversifier or more? Hedge and safe haven properties of green bonds during COVID-19. Energy Policy 2022, 168, 113102. [Google Scholar] [CrossRef]

- Naeem, M.A.; Bouri, E.; Costa, M.D.; Naifar, N.; Shahzad, S.J.H. Energy markets and green bonds: A tail dependence analysis with time-varying optimal copulas and portfolio implications. Resour. Policy 2021, 74, 102418. [Google Scholar] [CrossRef]

- Naeem, M.A.; Nguyen, T.T.H.; Nepal, R.; Ngo, Q.-T.; Taghizadeh–Hesary, F. Asymmetric relationship between green bonds and commodities: Evidence from extreme quantile approach. Financ. Res. Lett. 2021, 43, 101983. [Google Scholar] [CrossRef]

- Huang, J.; Cao, Y.; Zhong, P. Searching for a safe haven to crude oil: Green bond or precious metals? Financ. Res. Lett. 2022, 50, 103303. [Google Scholar] [CrossRef]

- Dai, Z.; Zhang, X.; Yin, Z. Extreme time-varying spillovers between high carbon emission stocks, green bond and crude oil: Evidence from a quantile-based analysis. Energy Econ. 2023, 118, 106511. [Google Scholar] [CrossRef]

- Ren, X.; Xiao, Y.; Kun, D.; Urquhart, A. Spillover effects between fossil energy and green markets: Evidence from informational inefficiency. Energy Econ. 2024, 131, 107317. [Google Scholar] [CrossRef]

- Lucey, B.; Ren, B. Time-varying tail risk connectedness among sustainability-related products and fossil energy investments. Energy Econ. 2023, 126, 106812. [Google Scholar] [CrossRef]

- Li, Z.; Tian, Y. Skewed multifractal cross-correlation between price and volume during the COVID-19 pandemic: Evidence from China and European carbon markets. Appl. Energy 2024, 371, 123716. [Google Scholar] [CrossRef]

- Fama, E.F. Efficient Capital Markets: A Review of Theory and Empirical Work. J. Financ. 1970, 25, 383–417. [Google Scholar] [CrossRef]

- Mantegna, R.N.; Stanley, H.E. Stock market dynamics and turbulence: Parallel analysis of fluctuation phenomena. Phys. A Stat. Mech. Its Appl. 1997, 239, 255–266. [Google Scholar] [CrossRef]

- Yuan, Y.; Zhuang, X.-T.; Liu, Z.-Y.; Huang, W.-Q. Time-clustering behavior of sharp fluctuation sequences in Chinese stock markets. Chaos Solitons Fractals 2012, 45, 838–845. [Google Scholar] [CrossRef]

- Peng, C.K.; Buldyrev, S.V.; Havlin, S.; Simons, M.; Stanley, H.E.; Goldberger, A.L. Mosaic organization of DNA nucleotides. Phys. Rev. E 1994, 49, 1685–1689. [Google Scholar] [CrossRef]

- Podobnik, B.; Stanley, H.E. Detrended cross-correlation analysis: A new method for analyzing two nonstationary time series. Phys. Rev. Lett. 2008, 100, 084102. [Google Scholar] [CrossRef]

- Kantelhardt, J.W.; Zschiegner, S.A.; Koscielny-Bunde, E.; Havlin, S.; Bunde, A.; Stanley, H.E. Multifractal detrended fluctuation analysis of nonstationary time series. Phys. A Stat. Mech. Its Appl. 2002, 316, 87–114. [Google Scholar] [CrossRef]

- dos Santos Maciel, L. Brazilian stock-market efficiency before and after COVID-19: The roles of fractality and predictability. Glob. Financ. J. 2023, 58, 100887. [Google Scholar] [CrossRef]

- Telli, S.; Chen, H.Z. Multifractal behavior in return and volatility series of Bitcoin and gold in comparison. Chaos Solitons Fractals 2020, 139, 109994. [Google Scholar] [CrossRef]

- Gu, R.B.; Liu, S.N. Nonlinear analysis of economic policy uncertainty: Based on the data in China, the US and the global. Phys. A Stat. Mech. Its Appl. 2022, 593, 126897. [Google Scholar] [CrossRef]

- Zhou, W.X. Multifractal detrended cross-correlation analysis for two nonstationary signals. Phys. Rev. E 2008, 77, 066211. [Google Scholar] [CrossRef]

- Li, Z.; Lu, X. Cross-correlations between agricultural commodity futures markets in the US and China. Phys. A Stat. Mech. Its Appl. 2012, 391, 3930–3941. [Google Scholar] [CrossRef]

- Fernandes, L.H.S.; Silva, J.W.L.; de Araujo, F.H.A. Multifractal risk measures by Macroeconophysics perspective: The case of Brazilian inflation dynamics. Chaos Solitons Fractals 2022, 158, 112052. [Google Scholar] [CrossRef]

- Feng, Y.; Yang, J.; Huang, Q. Multiscale correlation analysis of Sino-US corn futures markets and the impact of international crude oil price: A new perspective from the multifractal method. Financ. Res. Lett. 2023, 53, 103691. [Google Scholar] [CrossRef]

- Fernandes, L.H.S.; Silva, J.W.L.; de Araujo, F.H.A.; Tabak, B.M. Multifractal cross-correlations between green bonds and financial assets. Financ. Res. Lett. 2023, 53, 103603. [Google Scholar] [CrossRef]

- Inacio, C.M.C.; Kristoufek, L.; David, S.A. Dynamic price interactions in energy commodities benchmarks: Insights from multifractal analysis during crisis periods. Phys. A Stat. Mech. Its Appl. 2025, 659, 130314. [Google Scholar] [CrossRef]

- Acikgoz, T.; Gokten, S.; Soylu, A.B. Multifractal Detrended Cross-Correlations between Green Bonds and Commodity Markets: An Exploration of the Complex Connections between Green Finance and Commodities from the Econophysics Perspective. Fractal Fract. 2024, 8, 117. [Google Scholar] [CrossRef]

- Kojic, M.; Mitic, P.; Schlueter, S.; Rakic, S. Complex non-linear relationship between conventional and green bonds: Insights amidst COVID-19 and the RU-UA conflict. J. Behav. Exp. Financ. 2024, 43, 100966. [Google Scholar] [CrossRef]

- Adekoya, O.B.; Asl, M.G.; Oliyide, J.A.; Izadi, P. Multifractality and cross-correlation between the crude oil and the European and non-European stock markets during the Russia-Ukraine war. Resour. Policy 2023, 80, 103134. [Google Scholar] [CrossRef]

- Saâdaoui, F. Skewed multifractal scaling of stock markets during the COVID-19 pandemic. Chaos Solitons Fractals 2023, 170, 113372. [Google Scholar] [CrossRef]

- Saâdaoui, F. Segmented multifractal detrended fluctuation analysis for assessing inefficiency in North African stock markets. Chaos Solitons Fractals 2024, 181, 114652. [Google Scholar] [CrossRef]

- Zhaoa, K.G.; Wulder, M.A.; Hu, T.X.; Bright, R.; Wu, Q.S.; Qin, H.M.; Li, Y.; Toman, E.; Mallick, B.; Zhang, X.; et al. Detecting change-point, trend, and seasonality in satellite time series data to track abrupt changes and nonlinear dynamics: A Bayesian ensemble algorithm. Remote Sens. Environ. 2019, 232, 111181. [Google Scholar] [CrossRef]

- Wang, L.; Fu, A.; Bashir, B.; Gu, J.; Sheng, H.; Deng, L.; Deng, W.; Alsafadi, K. Characteristics and Driving Mechanisms of Coastal Wind Speed during the Typhoon Season: A Case Study of Typhoon Lekima. Atmosphere 2024, 15, 880. [Google Scholar] [CrossRef]

- Yang, L.; Wang, C.; Zhou, P.; Xie, N.; Tian, M.; Wang, K. Change point detection in brucellosis time series from 2010 to 2023 in Xinjiang China using the BEAST algorithm. Sci. Rep. 2025, 15, 3830. [Google Scholar] [CrossRef]

- Jewell, S.; Fearnhead, P.; Witten, D. Testing for a Change in Mean After Changepoint Detection. J. R. Stat. Soc. Ser. B Stat. Methodol. 2022, 84, 1082–1104. [Google Scholar] [CrossRef]

- Piotr, F. Wild binary segmentation for multiple change-point detection. Ann. Stat. 2014, 42, 2243–2281. [Google Scholar] [CrossRef]

- Li, J.; Wu, X.; Zhang, L.; Feng, Q. Research on the portfolio model based on Mean-MF-DCCA under multifractal feature constraint. J. Comput. Appl. Math. 2021, 386, 113264. [Google Scholar] [CrossRef]

- Podobnik, B.; Grosse, I.; Horvatic, D.; Ilic, S.; Ivanov, P.C.; Stanley, H.E. Quantifying cross-correlations using local and global detrending approaches. Eur. Phys. J. B 2009, 71, 243–250. [Google Scholar] [CrossRef]

- Zebende, G.F. DCCA cross-correlation coefficient: Quantifying level of cross-correlation. Phys. A Stat. Mech. Its Appl. 2011, 390, 614–618. [Google Scholar] [CrossRef]

- Xiang, S.; Cao, Y. Green finance and natural resources commodities prices: Evidence from COVID-19 period. Resour. Policy 2023, 80, 103200. [Google Scholar] [CrossRef]

- Wei, J.-W.; Wang, H.-Y.; Cao, G.-X. Multifractal Analysis of International Energy and Agricultural Markets Under the Influence of Russia-Ukraine Conflict. Fluct. Noise Lett. 2024, 23, 2450034. [Google Scholar] [CrossRef]

- Vides, J.C.; Feria, J.; Golpe, A.A.; Martín-Álvarez, J.M. How do supply or demand shocks affect the US oil market? Financ. Innov. 2024, 10, 16. [Google Scholar] [CrossRef]

- Mensi, W.; Selmi, R.; Al-Kharusi, S.; Belghouthi, H.E.; Kang, S.H. Connectedness between green bonds, conventional bonds, oil, heating oil, natural gas, and petrol: New evidence during bear and bull market scenarios. Resour. Policy 2024, 91, 104888. [Google Scholar] [CrossRef]

- Mensi, W.; Vo, X.V.; Ko, H.-U.; Kang, S.H. Frequency spillovers between green bonds, global factors and stock market before and during COVID-19 crisis. Econ. Anal. Policy 2023, 77, 558–580. [Google Scholar] [CrossRef]

- Patino-Artaza, H.; King, L.C.; Savin, I. Did COVID-19 really change our lifestyles? Evidence from transport energy consumption in Europe. Energy Policy 2024, 191, 114204. [Google Scholar] [CrossRef]

- Baek, J. Does Crude Oil Production Respond Differently to Oil Supply and Demand Shocks? Evidence from Alaska. Commodities 2024, 3, 62–74. [Google Scholar] [CrossRef]

- Zhao, L.-T.; Xing, Y.-Y.; Zhao, Q.-R.; Chen, X.-H. Dynamic impacts of online investor sentiment on international crude oil prices. Resour. Policy 2023, 82, 103506. [Google Scholar] [CrossRef]

- Talus, K. Adapting international natural gas and LNG agreements in the light of the energy transition. J. World Energy Law Bus. 2023, 16, 492–505. [Google Scholar] [CrossRef]

- Labandeira, X.; Labeaga, J.M.; López-Otero, X. A meta-analysis on the price elasticity of energy demand. Energy Policy 2017, 102, 549–568. [Google Scholar] [CrossRef]

- Liu, M.; Liu, H.; Ping, W. Dynamic spillovers between Shanghai crude oil futures and China’s green markets: Evidence from quantile-on-quantile connectedness approach. Econ. Anal. Policy 2025, 85, 78–93. [Google Scholar] [CrossRef]

- Wang, M.-C.; Jiang, P.; Chang, T. Re-examining China and the u.s.’s respective green bond markets in extreme conditions: Evidence from quantile connectedness. N. Am. J. Econ. Financ. 2025, 75, 102286. [Google Scholar] [CrossRef]

- Nguyen, T.T.H.; Naeem, M.A.; Balli, F.; Balli, H.O.; Vo, X.V. Time-frequency comovement among green bonds, stocks, commodities, clean energy, and conventional bonds. Financ. Res. Lett. 2021, 40, 101739. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Green Bond | WTI Crude Oil | Natural Gas | Gasoline | |

|---|---|---|---|---|

| Mean | −0.1214 × 10−4 | −0.0001 | −0.0002 | −0.0003 |

| Median | 0.0000 | 0.0008 | −0.0007 | 0.0010 |

| Maximum | 0.0227 | 0.2374 | 0.4253 | 0.2686 |

| Minimum | −0.0241 | −0.4808 | −0.1945 | −0.2638 |

| Std. Dev. | 0.0038 | 0.0287 | 0.0362 | 0.0272 |

| Skewness | −0.0835 | −2.1489 | 0.5932 | −0.5511 |

| Kurtosis | 7.1020 | 45.5525 | 12.9178 | 18.0911 |

| Jarque–Bera | 1766.2050 * | 191,683.5800 * | 10,455.1620 * | 23,992.7640 * |

| N | 2515 | 2515 | 2515 | 2515 |

| GB & WTI | GB & Gasoline | GB & Natural Gas | |

|---|---|---|---|

| Period 1 | 1 August 2014 to 20 April 2020 | 1 August 2014 to 6 March 2020 | 1 August 2014 to 22 September 2020 |

| Period 2 | 21 April 2020 to 11 July 2022 | 9 March 2020 to 1 July 2022 | 23 September 2020 to 14 September 2022 |

| Period 3 | 12 July 2022 to 28 August 2024 | 5 July 2022 to 28 August 2024 | 15 September 2022 to 28 August 2024 |

| Entire period | 1 August 2014 to 28 August 2024 | 1 August 2014 to 28 August 2024 | 1 August 2014 to 28 August 2024 |

| Entire period | Period 1 | |||||

| q | GB&WTI | GB&Gasoline | GB&NG | GB&WTI | GB&Gasoline | GB&NG |

| −10 | 0.6800 | 0.6796 | 0.6784 | 0.5888 | 0.6105 | 0.6067 |

| −8 | 0.6689 | 0.6677 | 0.6632 | 0.5803 | 0.6006 | 0.5958 |

| −6 | 0.6551 | 0.6532 | 0.6434 | 0.5715 | 0.5897 | 0.5822 |

| −4 | 0.6378 | 0.6351 | 0.6179 | 0.5638 | 0.5792 | 0.5655 |

| −2 | 0.6119 | 0.6085 | 0.5873 | 0.5596 | 0.5696 | 0.5458 |

| 0 | 0.5650 | 0.5591 | 0.5624 | 0.5485 | 0.5482 | 0.5160 |

| 2 | 0.4940 | 0.4831 | 0.5519 | 0.4385 | 0.4844 | 0.4510 |

| 4 | 0.4130 | 0.3940 | 0.5162 | 0.2740 | 0.4128 | 0.3815 |

| 6 | 0.3573 | 0.3360 | 0.4813 | 0.1841 | 0.3638 | 0.3335 |

| 8 | 0.3232 | 0.3011 | 0.4563 | 0.1359 | 0.3319 | 0.3019 |

| 10 | 0.3010 | 0.2783 | 0.4386 | 0.1069 | 0.3104 | 0.2805 |

| ΔH | 0.3791 | 0.4012 | 0.2398 | 0.4818 | 0.3001 | 0.3262 |

| Period 2 | Period 3 | |||||

| q | GB&WTI | GB&Gasoline | GB&NG | GB&WTI | GB&Gasoline | GB&NG |

| −10 | 0.7069 | 0.6441 | 0.7186 | 0.6173 | 0.6339 | 0.5913 |

| −8 | 0.6968 | 0.6337 | 0.6976 | 0.6061 | 0.6240 | 0.5855 |

| −6 | 0.6831 | 0.6202 | 0.6668 | 0.5900 | 0.6114 | 0.5797 |

| −4 | 0.6632 | 0.6027 | 0.6227 | 0.5643 | 0.5943 | 0.5736 |

| −2 | 0.6336 | 0.5827 | 0.5708 | 0.5177 | 0.5636 | 0.5609 |

| 0 | 0.6061 | 0.5808 | 0.5259 | 0.4398 | 0.4863 | 0.5145 |

| 2 | 0.5804 | 0.5770 | 0.4967 | 0.3615 | 0.3587 | 0.4361 |

| 4 | 0.5195 | 0.5269 | 0.4585 | 0.3130 | 0.2668 | 0.3793 |

| 6 | 0.4701 | 0.4876 | 0.4207 | 0.2804 | 0.2158 | 0.3432 |

| 8 | 0.4385 | 0.4620 | 0.3940 | 0.2568 | 0.1843 | 0.3183 |

| 10 | 0.4176 | 0.4446 | 0.3754 | 0.2393 | 0.1630 | 0.3003 |

| ΔH | 0.2893 | 0.1995 | 0.3432 | 0.3780 | 0.4709 | 0.2910 |

| Cross Correlation | αxy (0) | Wxy | Γ | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Entire Period | Period I | Period II | Period III | Entire Period | Period I | Period II | Period III | Entire Period | Period I | Period II | Period III | |

| GB&WTI | 0.5619 | 0.5693 | 0.6078 | 0.4397 | 0.5171 | 0.6761 | 0.4167 | 0.4970 | 0.9203 | 1.1876 | 0.6856 | 1.1304 |

| GB&Gasoline | 0.5558 | 0.5420 | 0.5821 | 0.4784 | 0.5442 | 0.4311 | 0.3147 | 0.6008 | 0.9791 | 0.7954 | 0.5407 | 1.2559 |

| GB&NG | 0.5656 | 0.5107 | 0.5282 | 0.5096 | 0.3764 | 0.4599 | 0.5051 | 0.3911 | 0.6655 | 0.9006 | 0.9563 | 0.7675 |

| Period | Portfolios | Weight: GB/WTI | SR | RRE | Weight: GB/Gasoline | SR | RRE | Weight: GB/NG | SR | RRE |

|---|---|---|---|---|---|---|---|---|---|---|

| Period 1 | energy only | 0/100 | −4.13 | - | 0/100 | −3.37 | - | 0/100 | −2.13 | - |

| equal weighted | 50/50 | −4.69 | 49.81 | 50/50 | −3.84 | 49.72 | 50/50 | −2.49 | 49.61 | |

| MV | 98.46/1.54 | −5.60 | 88.70 | 98.37/1.63 | −4.43 | 87.93 | 98.86/1.14 | −3.55 | 88.69 | |

| MaxSR | 0/100 | −4.13 | 0.00 | 0/100 | −3.37 | 0.00 | 0/100 | −2.13 | 0.00 | |

| MD | 99.04/0.96 | −5.41 | 88.69 | 98.47/1.53 | −4.40 | 87.93 | 99.07/0.93 | −3.52 | 88.69 | |

| Mean-MF-DCCA MV | 97.27/2.73 | −0.80 | 92.79 | 98.34/1.66 | −1.17 | 91.03 | 94.31/5.69 | 0.12 | 91.86 | |

| Mean-MF-DCCA MaxSR | 100/0 | −0.90 | 92.50 | 0/100 | 5.12 | 86.10 | 100/0 | −0.15 | 91.62 | |

| Mean-MF-DCCA MD | 99.04/0.96 | −0.84 | 92.69 | 98.89/1.11 | −1.11 | 91.01 | 94.91/5.09 | −0.12 | 91.65 | |

| Period 2 | energy only | 0/100 | 7.12 | - | 0/100 | 3.66 | - | 0/100 | 6.65 | - |

| equal weighted | 50/50 | 5.92 | 49.54 | 50/50 | 2.30 | 49.29 | 50/50 | 5.25 | 49.88 | |

| MV | 99.5/0.5 | −11.24 | 90.24 | 99.6/0.4 | −11.85 | 88.97 | 99.15/0.85 | −15.61 | 91.50 | |

| MaxSR | 0/100 | 7.12 | 0.00 | 0/100 | 3.66 | 0.00 | 0/100 | 6.65 | 0.00 | |

| MD | 98.9/1.1 | −10.71 | 90.22 | 99.65/0.35 | −11.87 | 88.97 | 98.61/1.39 | −15.07 | 91.49 | |

| Mean-MF-DCCA MV | 98.4/1.6 | −0.50 | 90.19 | 92.33/7.67 | −1.67 | 92.14 | 96.54/3.46 | −0.03 | 92.07 | |

| Mean-MF-DCCA MaxSR | 100/0 | −0.54 | 90.05 | 0/100 | 2.90 | 87.38 | 100/0 | −0.26 | 91.86 | |

| Mean-MF-DCCA MD | 98.46/1.54 | −0.54 | 90.06 | 99.65/0.35 | −1.18 | 92.01 | 96.84/3.16 | −0.24 | 91.88 | |

| Period 3 | energy only | 0/100 | −3.85 | - | 0/100 | −5.41 | - | 0/100 | −7.16 | - |

| equal weighted | 50/50 | −3.63 | 48.32 | 50/50 | −5.28 | 48.56 | 50/50 | 1.10 | 49.40 | |

| MV | 94.38/5.62 | −0.50 | 75.69 | 95.39/4.61 | −1.23 | 77.78 | 99.34/0.66 | 1.53 | 88.85 | |

| MaxSR | 100/0 | 0.40 | 75.01 | 100/0 | −0.11 | 77.29 | 100/0 | −6.91 | 88.84 | |

| MD | 94.94/5.06 | −0.41 | 75.68 | 96.87/3.13 | −0.87 | 77.73 | 99.66/0.34 | 1.31 | 88.85 | |

| Mean-MF-DCCA MV | 96.84/3.16 | −0.44 | 91.38 | 94.99/5.01 | −2.29 | 94.39 | 96.3/3.7 | 0.52 | 96.71 | |

| Mean-MF-DCCA MaxSR | 100/0 | −0.50 | 91.24 | 0/100 | 8.09 | 91.78 | 100/0 | −0.28 | 96.44 | |

| Mean-MF-DCCA MD | 99.07/0.93 | −0.46 | 91.34 | 98.61/1.39 | −1.75 | 94.34 | 99.63/0.37 | 0.44 | 96.69 |

| Multifractal Indicator | Period | Group | BEAST-Identified Sequence | Economic Event Sequence |

|---|---|---|---|---|

| Hurst exponent | 1 | GB&WTI | 0.4361 | 0.3941 |

| GB&Gasoline | 0.4844 | 0.4711 | ||

| GB&NG | 0.4510 | 0.4615 | ||

| 2 | GB&WTI | 0.5804 | 0.5138 | |

| GB&Gasoline | 0.6097 | 0.5227 | ||

| GB&NG | 0.4967 | 0.4017 | ||

| 3 | GB&WTI | 0.3615 | 0.3031 | |

| GB&Gasoline | 0.3587 | 0.4520 | ||

| GB&NG | 0.4361 | 0.4768 | ||

| ΔH | 1 | GB&WTI | 0.5471 | 0.4650 |

| GB&Gasoline | 0.3001 | 0.3341 | ||

| GB&NG | 0.3262 | 0.3168 | ||

| 2 | GB&WTI | 0.2893 | 0.3891 | |

| GB&Gasoline | 0.1945 | 0.2629 | ||

| GB&NG | 0.3432 | 0.3971 | ||

| 3 | GB&WTI | 0.3780 | 0.5952 | |

| GB&Gasoline | 0.4709 | 0.3053 | ||

| GB&NG | 0.2910 | 0.2675 | ||

| Wxy | 1 | GB&WTI | 0.6761 | 0.6043 |

| GB&Gasoline | 0.4167 | 0.4770 | ||

| GB&NG | 0.4970 | 0.4568 | ||

| 2 | GB&WTI | 0.4311 | 0.5442 | |

| GB&Gasoline | 0.3147 | 0.3968 | ||

| GB&NG | 0.6008 | 0.5449 | ||

| 3 | GB&WTI | 0.4599 | 0.7522 | |

| GB&Gasoline | 0.5051 | 0.4175 | ||

| GB&NG | 0.3911 | 0.3594 | ||

| Γ | 1 | GB&WTI | 1.1876 | 1.2047 |

| GB&Gasoline | 0.6856 | 0.7925 | ||

| GB&NG | 1.1304 | 0.8178 | ||

| 2 | GB&WTI | 0.7954 | 0.9572 | |

| GB&Gasoline | 0.5407 | 0.7547 | ||

| GB&NG | 1.2559 | 0.8898 | ||

| 3 | GB&WTI | 0.9006 | 1.6849 | |

| GB&Gasoline | 0.9563 | 0.8023 | ||

| GB&NG | 0.7675 | 0.7560 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tian, Y.; Li, Z.; Wang, J.; Wu, X.; Huang, H. Skewed Multifractal Cross-Correlations Between Green Bond Index and Energy Futures Markets: A New Perspective Based on Change Point. Fractal Fract. 2025, 9, 327. https://doi.org/10.3390/fractalfract9050327

Tian Y, Li Z, Wang J, Wu X, Huang H. Skewed Multifractal Cross-Correlations Between Green Bond Index and Energy Futures Markets: A New Perspective Based on Change Point. Fractal and Fractional. 2025; 9(5):327. https://doi.org/10.3390/fractalfract9050327

Chicago/Turabian StyleTian, Yun, Zhihui Li, Jue Wang, Xu Wu, and Huan Huang. 2025. "Skewed Multifractal Cross-Correlations Between Green Bond Index and Energy Futures Markets: A New Perspective Based on Change Point" Fractal and Fractional 9, no. 5: 327. https://doi.org/10.3390/fractalfract9050327

APA StyleTian, Y., Li, Z., Wang, J., Wu, X., & Huang, H. (2025). Skewed Multifractal Cross-Correlations Between Green Bond Index and Energy Futures Markets: A New Perspective Based on Change Point. Fractal and Fractional, 9(5), 327. https://doi.org/10.3390/fractalfract9050327