4.1. The Forecasting Model

The relationship between the degradation of the tool and the number of runs is described by the Black–Scholes formula for the stochastic process sequence

. It is easy to derive a differential iterative formula based on linear alpha-stable motion, which can be expressed as follows:

where

is the increment of the stochastic process,

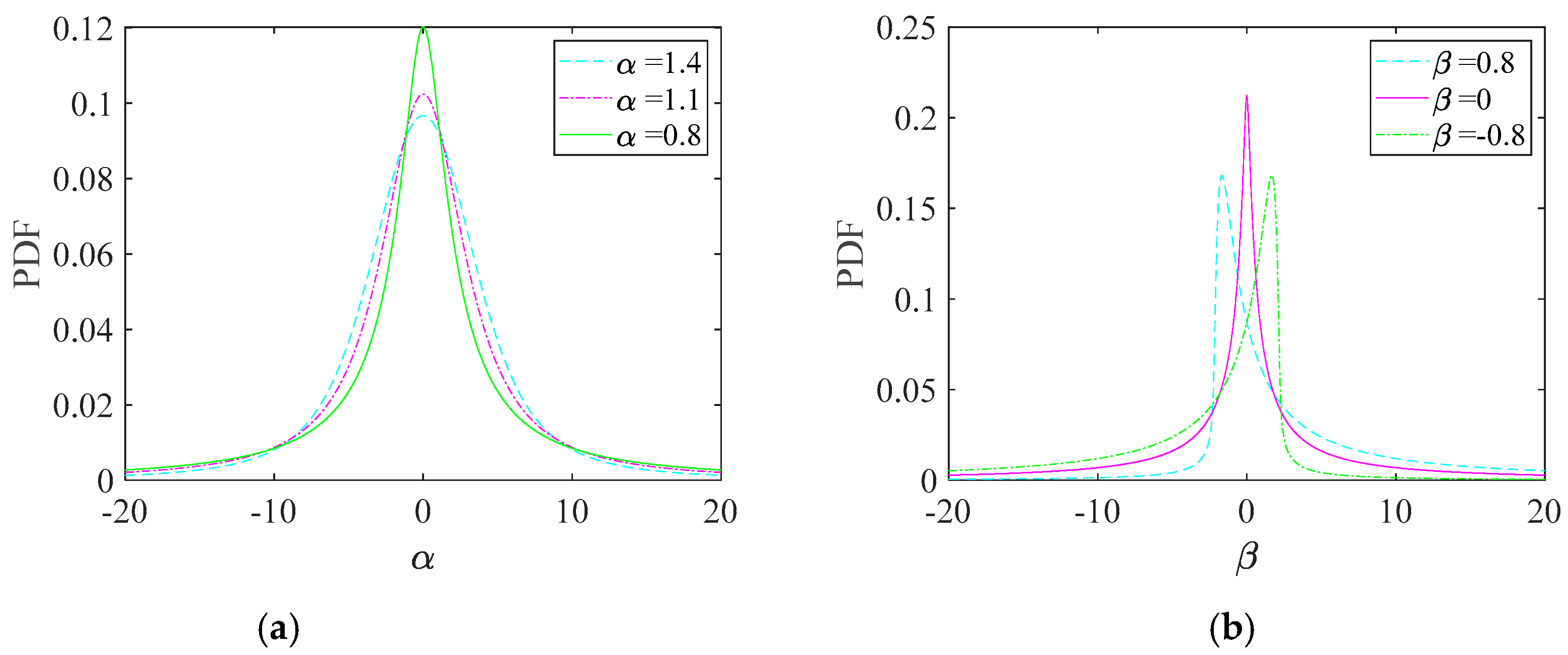

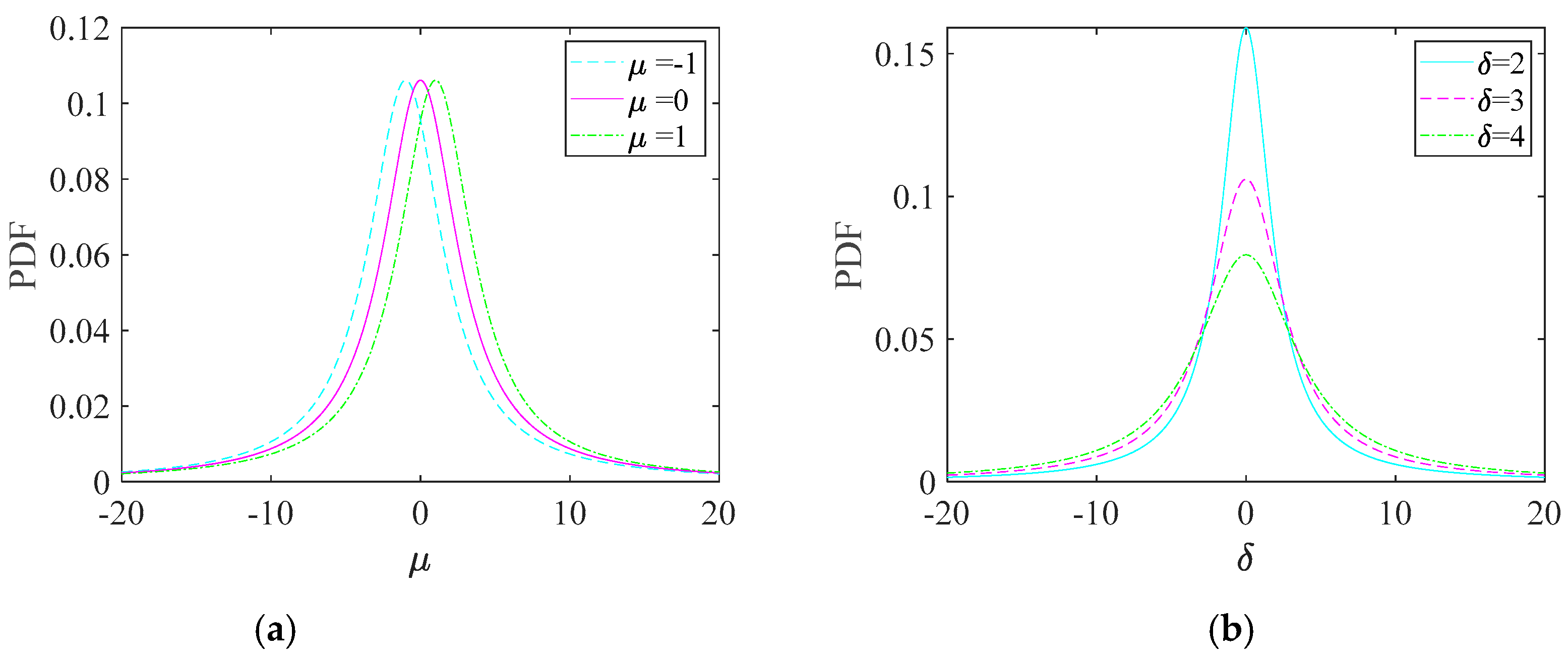

μ is the drift function,

δ is the diffusion function,

μ and

δ depict nonlinear degradation with power-law variation,

is the initial state, and

denotes the increment of linear alpha-stable motion.

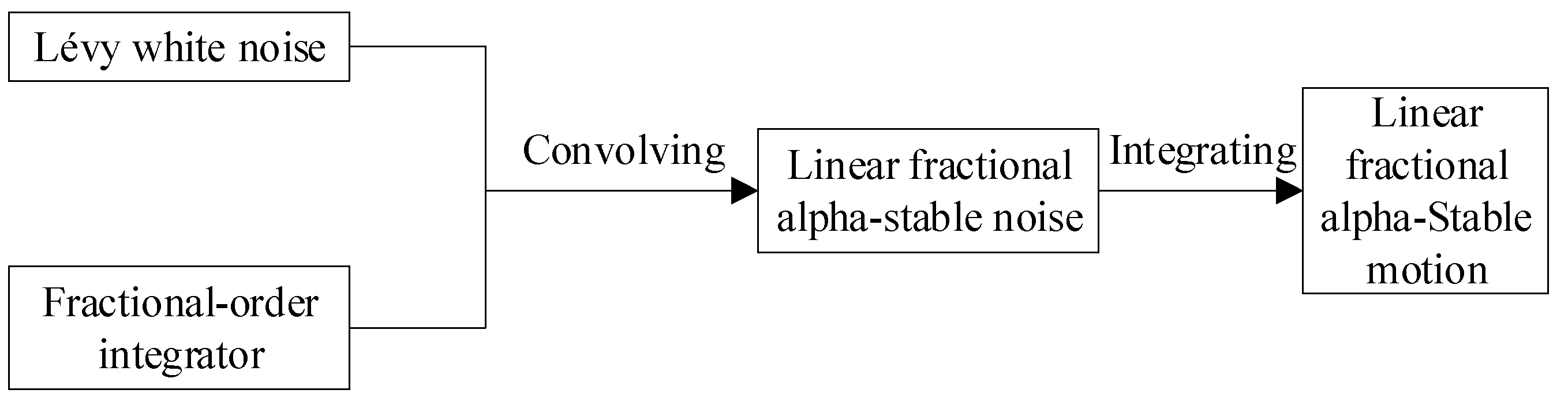

However, Equation (17) is only predicted favorably when it is satisfied that the degradation process has independent step increments. Obviously, it does not apply well to tool vibration with LRD. The LFSM is therefore introduced by modifying the diffusion term, and the results are shown below:

Let the function

, Taylor expansion of a obtains

According to Equation (19), the discrete form of Equation (18) can be obtained as

In turn, the discrete increments of the LFSM can be obtained:

where

is linear fractional alpha-stable motion noise.

Expressing Equation (23) by a differential discrete form

Finally, the iterative difference prediction model based on the LFSM model is obtained in Equation (25).

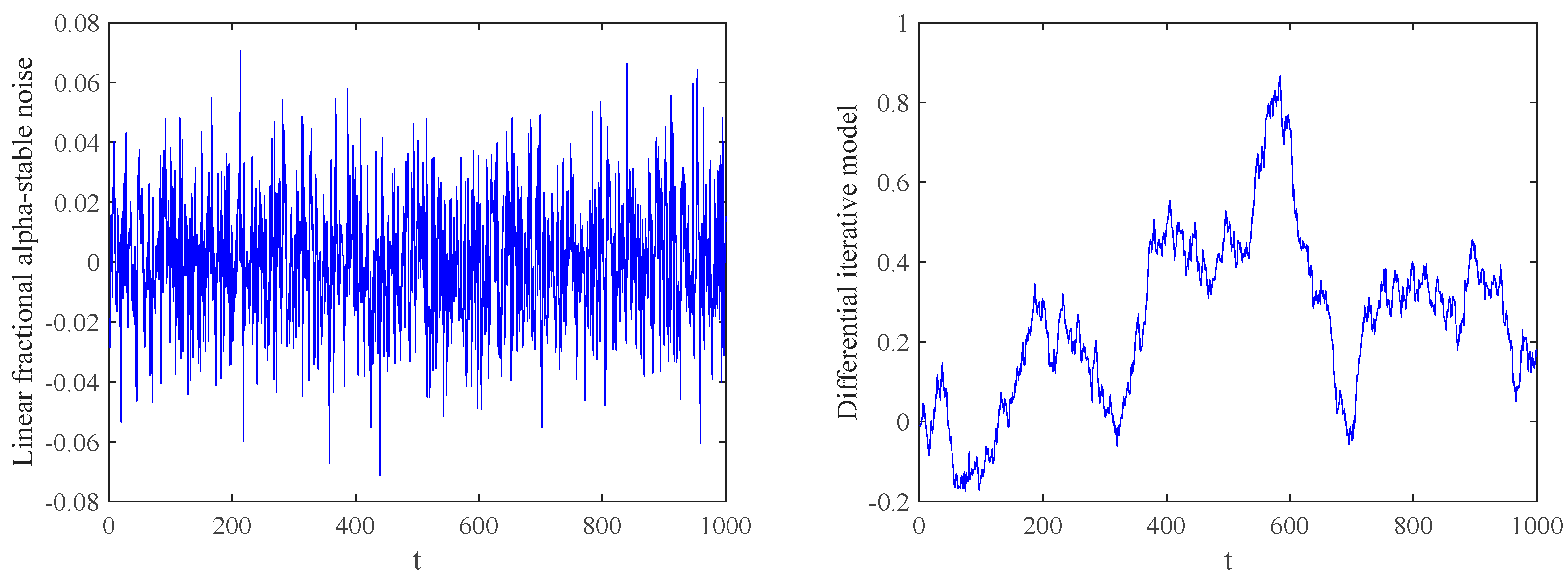

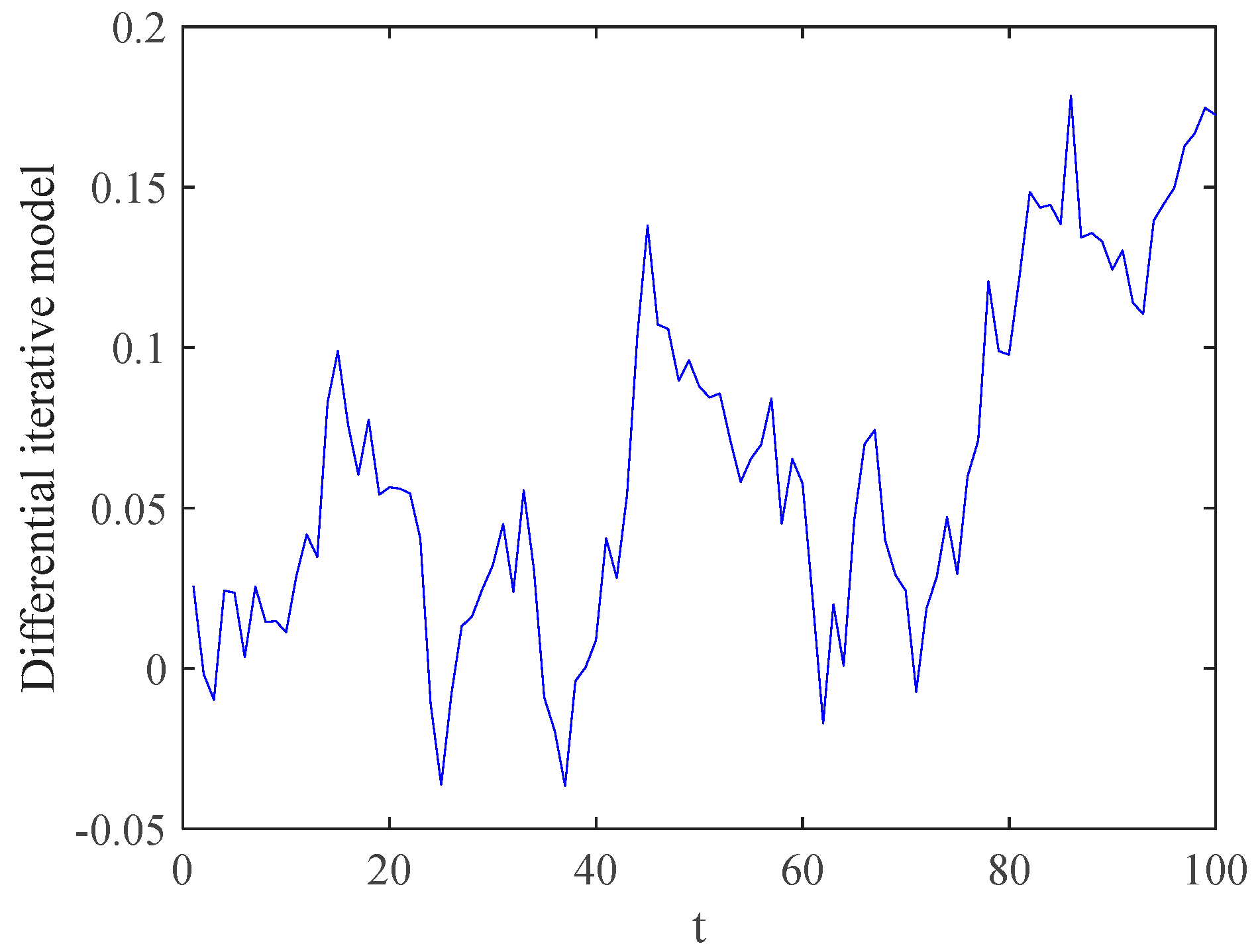

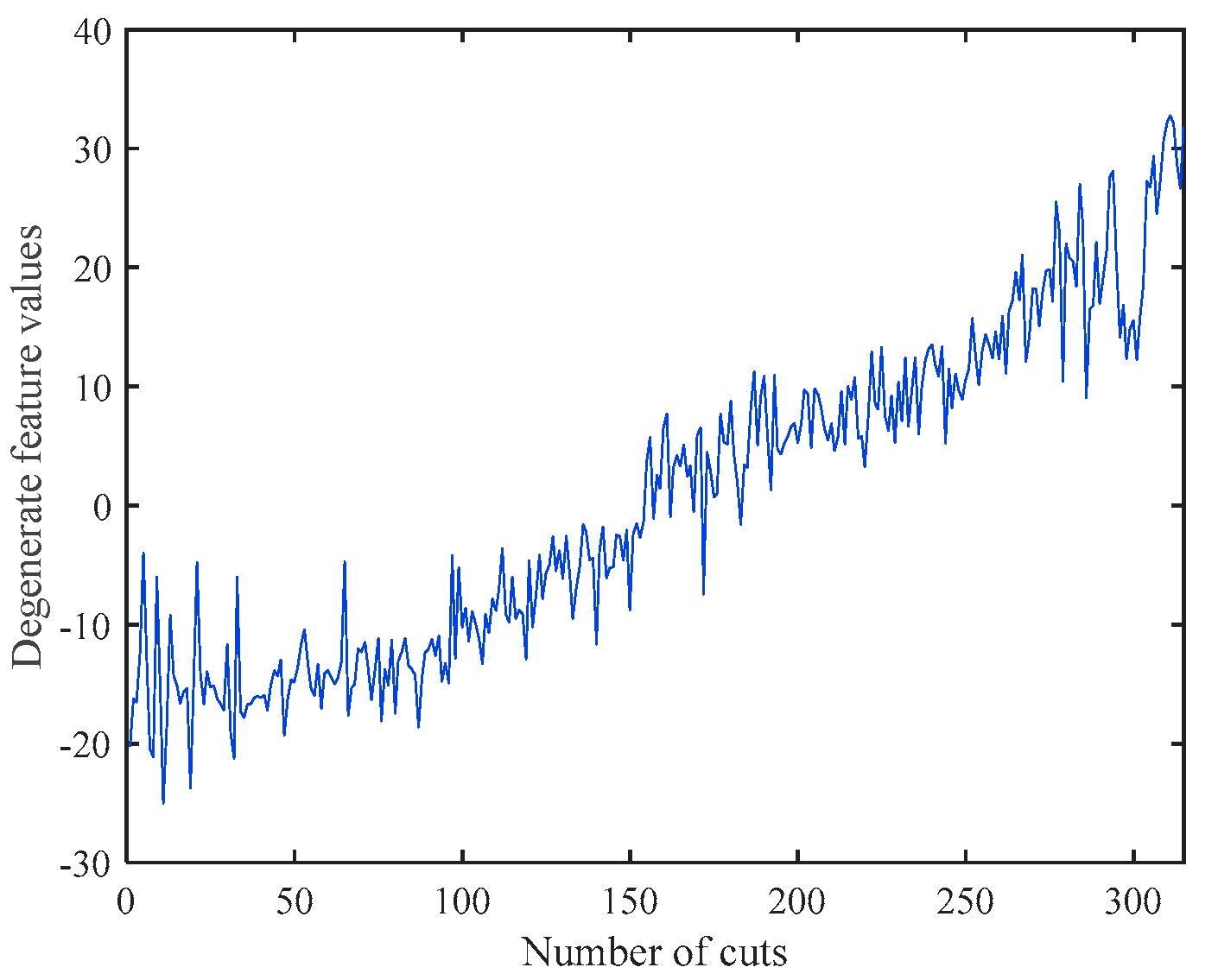

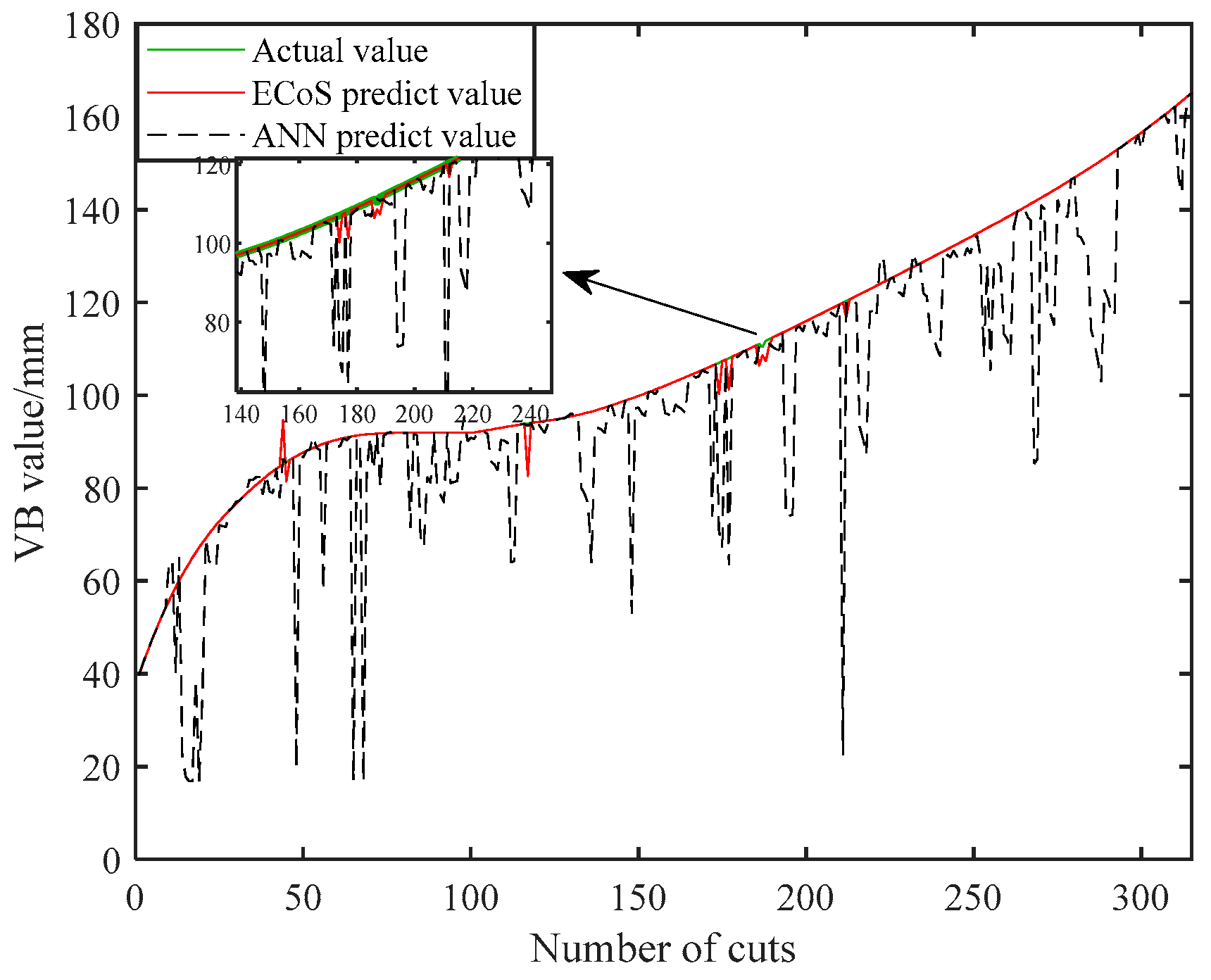

Figure 5 shows the numerical simulation of the model.

4.2. Existence and Uniqueness for the Solution of the Model

Since the accuracy of the actual measured initial data cannot be guaranteed and it is not certain that the tested initial data can be used as the true solution, this subsection discusses the Cauchy problem of Equation (25) or Equation (18), by proving the existence and uniqueness of its solution to the initial value problem. Furthermore, if the initial value creates a negligible small change or its solution similarly produces a negligible small change, the solution’s consistent convergence must be considered.

To ensure that Equation (18) can describe the uncertain variation of a random sequence, the process should be guaranteed to have a unique solution. We abbreviate Equation (18) as follows:

where

follows the definition in

Section 3 and a semimartingale

that consistently converges to

has been obtained. Substituting the semimartingale

into Equation (26) provides:

We have obtained the following two Corollaries.

Since Equation (27) is a semimartingale process, its solution may be obtained using the Ito formula.

Corollary 3. The solution of Equation (27) iswhere , , assuming that the initial value is a bounded random variable. Corollary 4. When the stochastic process is in , and , This is the solution of Equation (26).

Proof. According to Equation (27), we can get

Substitute Equation (30) into Equation (28)

Equation (20) can be written as

Using Ito formula for the above equation

From the above equation, we get

Therefore, Corollary 3 is proved. □

Proof. According to Equation (35), in order to further simplify, it takes

Gathering Equations (36) and (37), we obtain

By putting

in the above equation, we can get:

According to Equation (40), after obtaining the approximation solution, it is necessary to verify that the solution consistently converges to Equation (39) to ensure that when a small change in occurs in the region, a small change in can follow accordingly.

In the following, we will prove that

converges uniformly to

.

According to

, we can get

From the above equation, in

, we can see that

According to the equation

, the other half of Equation (41) has the following relationship

Considering Equations (41), (43), and (45) together, the following results can be obtained

So, Corollary 4 is proved. □

It is also important to demonstrate the uniqueness of Equation (18)’s solution in order to verify that it can be merged with a random sequence of fractional-order stable Lévy white noise.

If and are limits of in , then this solution is unique.

In summary, Equation (25), the solution of the LFSM differential iterative model proposed in this paper, is demonstrated in this section using a semimartingale approximation, proving that the model is reasonable at the theoretical level and can describe the uncertain variation of stochastic sequences.

4.3. Parameter Estimation of LFSM Degradation Model

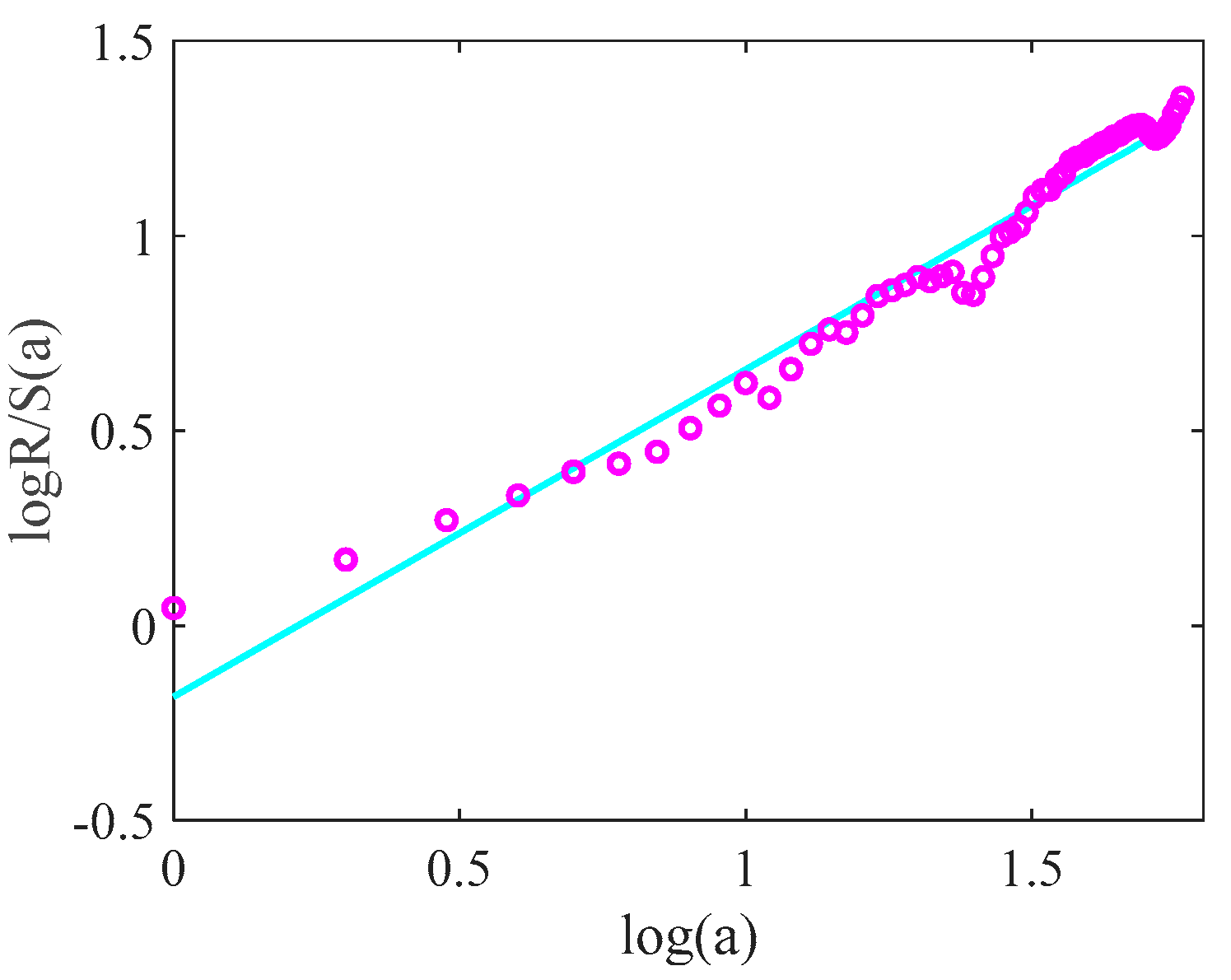

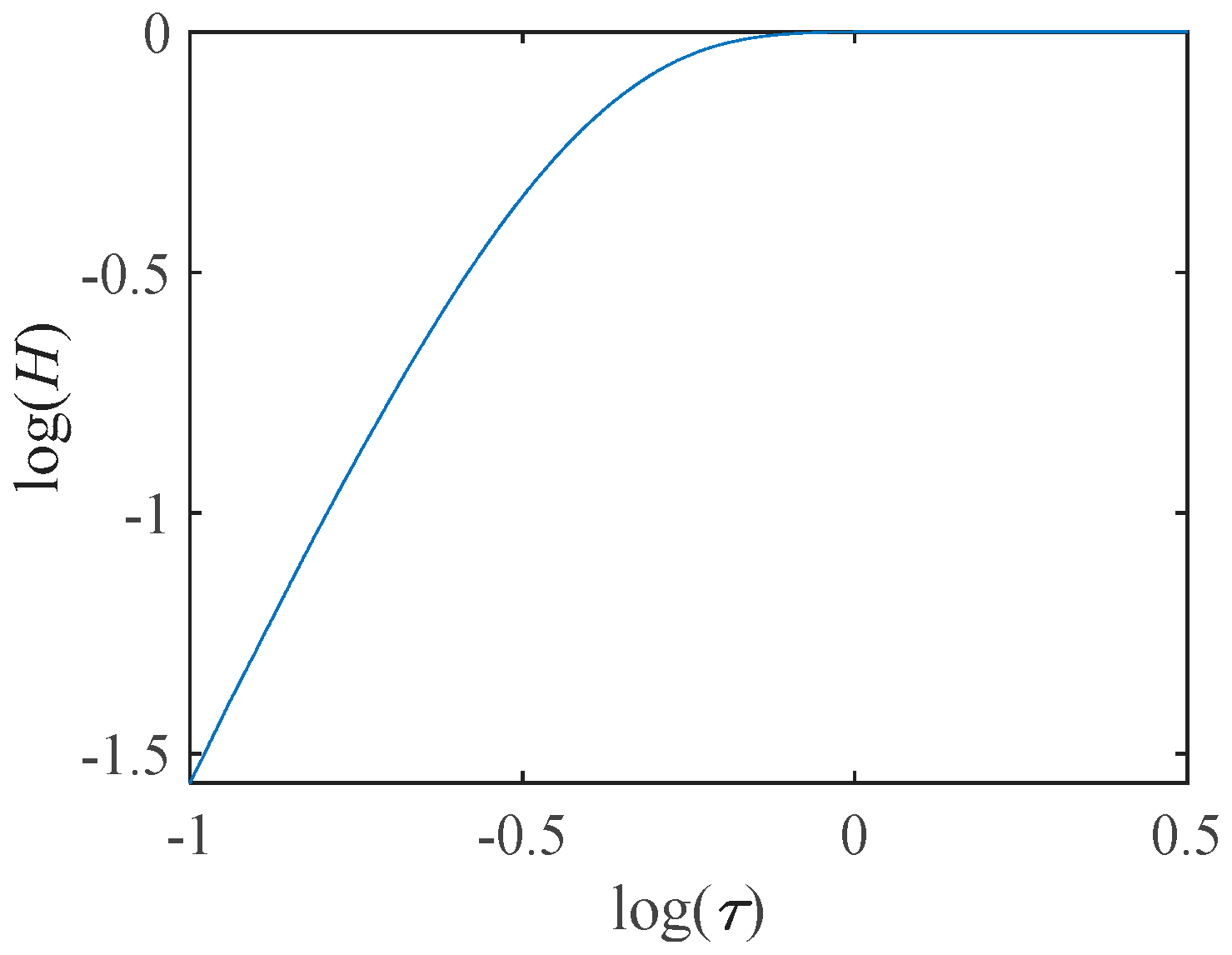

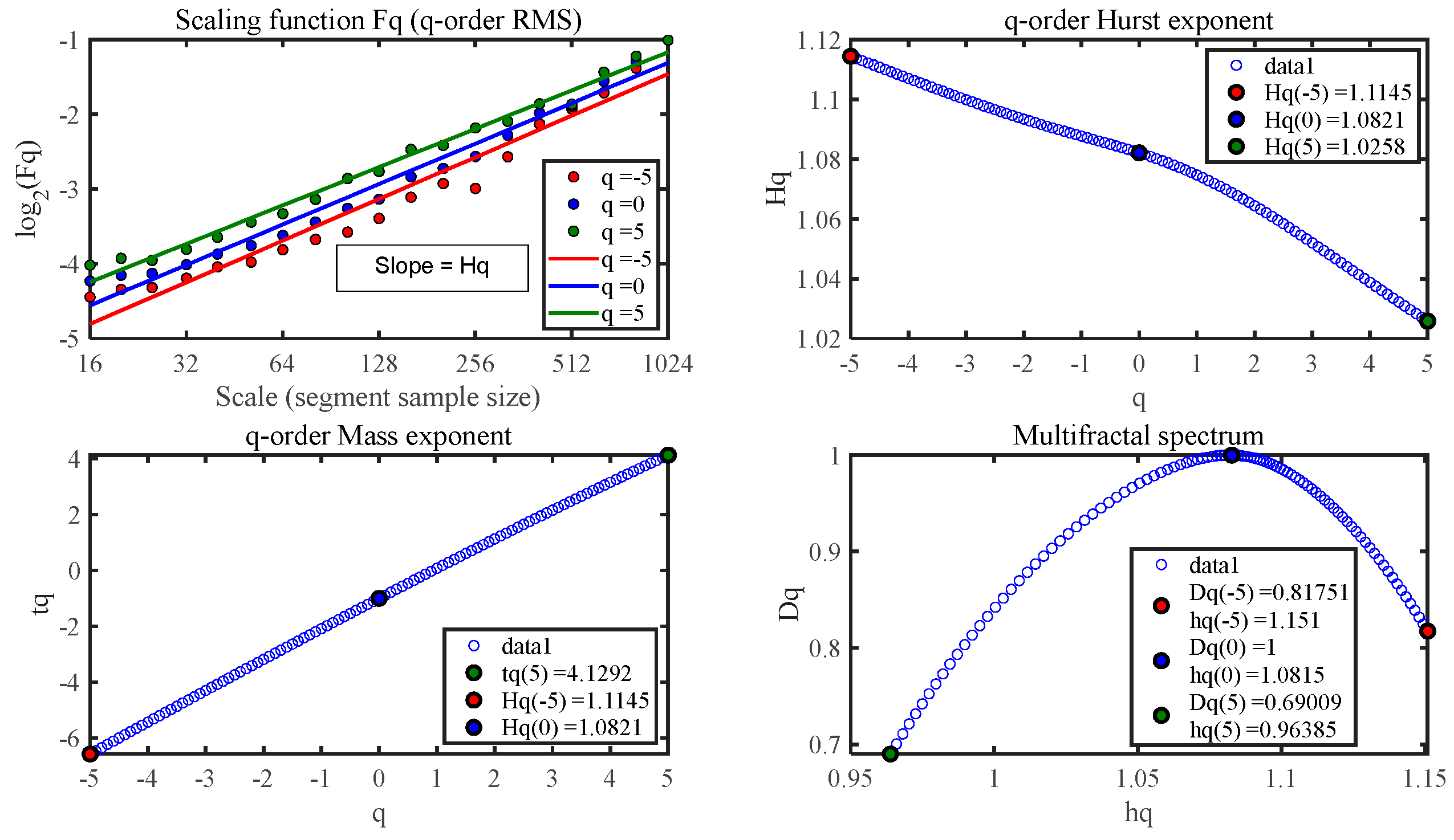

The algorithms for estimating the values of H are primarily divided into two categories: time domain analysis methods, which generally calculate the sample series directly and then obtain the estimated values of Hurst parameters by curve fitting, primarily the variance method, rescaled polar difference method, and absolute value method, etc.; and frequency domain analysis methods, which primarily use Fourier changes to transform the sample data into the frequency domain. The rescaled polar difference method is used in this paper to estimate H, because the implementation process is very simple, and the calculation is simple and easy to understand; the specific process is as follows:

Step 1: The sample input data

of length n is divided into h submodules of equal length (all of which are a), and the mean value of each submodule is determined;

Step 2: Calculate the cumulative deviation for each submodule;

Step 3: Calculate the extreme differences for each submodule;

Step 4: Calculate the standard deviation of each submodule;

Step 5: Divide the polar deviation of each submodule by the standard deviation and average it to get the rescaled polar deviation of each submodule;

Step 6: The supplied sample data is rescaled into submodules. As long as is met, a can take different values, and then Steps 1–5 can be repeated to achieve different rescaled polar deviations;

Step 7: Logarithmize each submodules’ length a and the accompanying

to produce

and log

a, and then fit them using least squares, as shown in

Figure 6.

Figure 6 shows the slope’s H, which is the projected value required in this paragraph.

There are still four parameters with values to be estimated, which are diffusion parameter

δ, stability index

α, skewness index β, and drift coefficient

μ. In this paper, we use the new eigenfunction estimation method. The specific steps are shown in [

39,

40].

The LFSM model, in contrast with the standard Gaussian process that obeys the central limit theorem, is a non-Gaussian process that obeys the modified central limit theorem and lacks a PDF expression in the usual sense of a restricted form. The LFSM model includes an explicit eigenfunction to address the issue of difficult parameter solutions caused by the PDF’s lack of a restricted form. The PDF of the LFSM model may be produced by applying Fourier transforms on the eigenfunctions. As a result, the parameter estimate may be increased using the eigenfunctions. There is one point you should keep in mind,

. This is because the absolute values of the eigenfunctions are equivalent at location

, regardless of the eigenfunction parameters’ values.

Additionally, there is a crucial point

that calculates using

and

, which stands for the Cauchy and Gaussian eigenfunctions.

Assuming that the input sequence is :

Step 1: Estimate the value of

, Equation (54)’s logarithmic likelihood estimate;

Step 2: Estimate the value of

α, combining Equation (56) and Equation (55);

Step 3: Estimate the value of

μ, the logarithmic version of the characteristic function which is used to obtain the estimate of the drift coefficient.

With the help of the two points

and

, the estimated value can be obtained

Since the LFSM model used in this work has a symmetric driving function, in this model.

and

and

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}