1. Introduction

The economic growth model has been extensively followed and studied by economists since the 1950s [

1,

2,

3,

4,

5]. Analyzing the dynamics and trends of economic growth helps to grasp macroeconomic operation as well as formulate economic policies. As the cornerstone of economic growth theory, the Solow model [

6] provided a groundbreaking theoretical framework for subsequent research work on growth. The model explains how capital stock, saving rate, labor force growth rate, capital depreciation, technological progress interact and affect a nation’s total output. Solow’s theory suggests the convergence of economy towards a steady-state path and emphasizes the role of technological progress as the ultimate driving force behind the long-run growth. Despite voluminous works flourishing in the growth literature [

7,

8], the Solow model is still of great theoretical and empirical significance, attracting enormous professional interest.

The Solow model is actually presented in the form of an ordinary differential equation describing the process of capital accumulation. However, a differential equation of integer order sometimes shows restriction for economic models since amnesia is assumed in all economic agents and memory fading is neglected. Therefore, a fractional derivative is developed to construct economic models due to its nonlocality and memory characteristics in evolutionary processes [

9,

10]. Compared with the integer-order derivative, the fractional derivative shows global correlation and better description of long-term dependencies and memory in economic data. Numerous experimental results indicate that the fractional-order model is superior to the integer model when dealing with economic dynamic problems [

11,

12,

13].

The fractional derivative, as the main mathematical tool to describe economic dynamics with memory, has been widely studied in modern mathematical economic theory. A review on the history of economic application of fractional dynamics was provided [

14]. It divided the economic dynamics evolution into five stages of development. The first two stages were characterized by fractional brownian motion [

15]. Long-term dependencies in economic data were pointed out and a time-fractional Black–Scholes equation was proposed. The following two stages were characterized by econophysics and deterministic chaos [

16]. Many papers were devoted to the description of power-law memory and fractional-dynamic behaviors in financial processes. The most recent is the mathematical economics stage beginning with the proposal of generalizations of basic economic concepts and classic models. New concepts primarily include economic multiplier with memory, elasticity and marginal value of fractional order etc. [

17,

18]. Generalizations of classical models include the Harrod–Domar model, Keynes model, Phillips model and Kaldor model etc. [

19,

20].

Time delay is a common phenomenon widely existing in economic systems. Since most of the economic processes are not only affected by the present state, but also depend largely on related indicators and factors in the past, the delayed mathematical models are more suitable for depicting economic phenomenon. Therefore, some integer-order and fractional-order differential equation models with time delays are proposed in the economic growth literature, and some significant results have been drawn in recent years. A continuous-time neoclassical growth model with time delay was developed to find erratic fluctuations in the capital accumulation process [

21]. Shortly thereafter, a generalized Cai model with endogenous labor shift was studied by choosing the delay as the parameter and gave some conditions of stability and bifurcation [

22]. Furthermore, the existence and global attractivity of almost periodic solutions were proven for a delayed differential neoclassical growth model [

23]. More recently, a generalization of the Keynesian macroeconomic model was proposed with gamma-distributed lag and using fractional differential equations [

18].

In terms of economic growth forecasting, empirical researches have been carried out based on different models. A replicable forecasting model was proposed to find an L-shaped GDP growth path in China and predict an annual GDP growth rate close to the 6.5% official target in the next five years [

24]. Underlying factors of China’s strong growth were explored using a general framework of cross-country analysis. The forecast results showed a significant decline of China’s potential GDP growth in the coming decade [

25]. In terms of fractional calculus, both integer order and fractional order differential equation models were considered to predict the economic growth of the countries in the Group of Twenty [

26].

In this paper, we propose an adaptive fractional economic growth model where a time delay is introduced to describe the time lag from capital input to effect. Therefore, our method can effectively capture memory characteristics within economic operations. The traditional Solow model is based on a harsh assumption that the technological progress is completely exogenous, which is not consistent with practical experience. To make up for the gap, we assume in our model that technological progress is endogenous and related to both population and capital. The proposed model is presented in the form of a fractional differential equations system. To explore the steady state of long-term economic growth, we analyze the stability of the equilibrium point and how stability changes when parameters vary. Based on the model, we use China’s economic data to conduct economic forecast and empirical analysis. To achieve this, we first estimate the fractional order of each equation through optimization and analyze the trends of main variables affecting China’s economy. As a meaningful exploration, we compare the delayed fractional model with the integer derivative model and the no delay model, respectively. We also exhibit the impacts of different fractional derivatives and delay parameters on predictions. On this basis, we predict China’s GDP in the next thirty years and analyze its growth potential. The proposed model shows excellent stability properties and predictive results, making it a practicable and attractive approach for analyzing long-term economic growth trends in real applications.

The remainder of this paper is organized as follows.

Section 2 provides some definitions and lemmas in fractional differential equation as well as the detailed description of the proposed model.

Section 3 shows the main theoretical results on the stability of equilibrium points. Numerical simulation and parameter sensitivity analysis are given in

Section 4. Finally, China’s economic growth forecast and analysis in the next thirty years are shown in

Section 5.

3. Main Results

Theorem 1. If , when , and or , then the positive equilibrium point of system (8) is Lyapunov locally asymptotically stable for any , where y is any real root of the equation , and the coefficients of the equation are denoted as Proof. When

, by setting

and solving the equations

we obtian the unique positive steady-state solution

of system (

8) as

when the delay

is introduced, the equilibrium point keeps the same and, therefore, we can take the local coordinates

and centre the system’s singular point at the origin. If we have

, the linear centralized system (

8) can be written in the following vector form

where

and

denote the Jacobian matrix

According to matrix (

2), applying Laplace transform on both sides of system (

12), one has the following characteristic matrix

Then, it follows that the characteristic equation

is given as

Next, it will be verified that the characteristic Equation (

16) has no pure imaginary roots for any

. The fact is testified by contradiction. It is obvious that there are no pure imaginary roots in equation

when

. Therefore, we consider the equation

Suppose that

is one of the pure root imaginary of Equation (

17) and has the form

, where

w is a positive real number. The substitution of

into Equation (

17) gives:

Separating its real part and imaginary part, we obtain

and

Thus, Equations (

19) and (

20) can be changed into

We square both sides of Equation (

22) and add them together

Substituting expression (

21) into Equation (

23), we obtain

where

when

and

y satisfies the inequations

or

, then there exists no real roots in Equation (

17), where

y is any real root of the cubic equation

. That is to say, the characteristic equation

has no pure imaginary roots for any

.

When

, the coefficient matrix

M of system (

12) satisfies

.

and its characteristic equation is

We can obtain its eigenvalues

. If

, one gets

According to (

27), one can ensure the three eigenvalues of the coefficient matrix

M have negative real parts, so that all the eigenvalues of

M satisfy

. Based on

, system (

8) is Lyapunov asymptotically stable at the positive equilibrium point

.

Theorem 2. If , when , and or , then the positive equilibrium point of system (8) is Lyapunov locally asymptotically stable for any , where y is any real root of the equation , and the coefficients of the equation are denoted as Proof. When

. By setting

and solving the equations

We obtain the unique positive steady-state solution

of system (

8) as

Adopting the same approach of Theorem 1, we can get the equation similar to Equation (

24) as follows

where the coefficients are denoted as (

28).

When

and

y satisfies the inequations

or

, then there exists no real roots in Equation (

31), where

y is any real root of the cubic equation

. That is to say, the characteristic equation

has no pure imaginary roots for any

.

When , the coefficient matrix M satisfies

and its characteristic equation is

We can obtain its eigenvalues

. If

, one gets

According to (

33), one can ensure the three eigenvalues of the coefficient matrix

M have negative real parts, so that all the eigenvalues of

M satisfy

. Based on

, system (

8) is Lyapunov asymptotically stable at the positive equilibrium point

. □

Theorem 3. If , when , , , and or , then the positive equilibrium point of system (8) is Lyapunov locally asymptotically stable for any , where is notations in Equation (13). y is any real root of the equation , and the coefficients of the equation are denoted as Proof. The proof is similar to Theorems 1 and 2, so it is omitted. □

4. Numerical Simulation

In order to present the dynamic operation state of the fractional order system, some numerical simulations are adopted in this section. Firstly, some numerical examples are given to illustrate the theoretical results above and demonstrate the comparison between the fractional model (

) and the memoryless model (

). Secondly, a particular case is used to determine the effect of parameter variation on the operation state and the equilibrium point. In the simulation process, we adopt the Adams–Bashforth–Moulton predictor–corrector scheme [

39] and take the step-length

.

We assign specific values to some of the parameters in system (

8) and consider the following equation

Take the data of China in 1978 as the initial value .

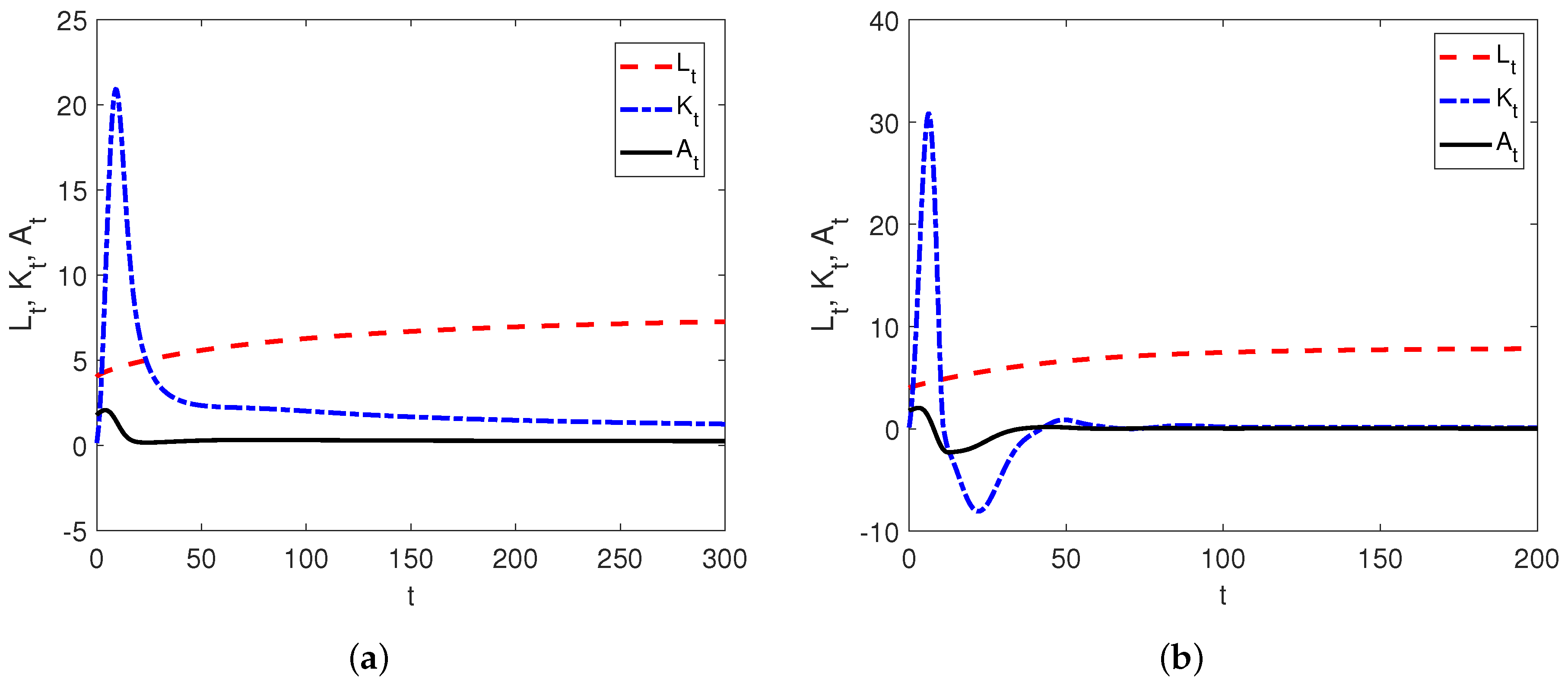

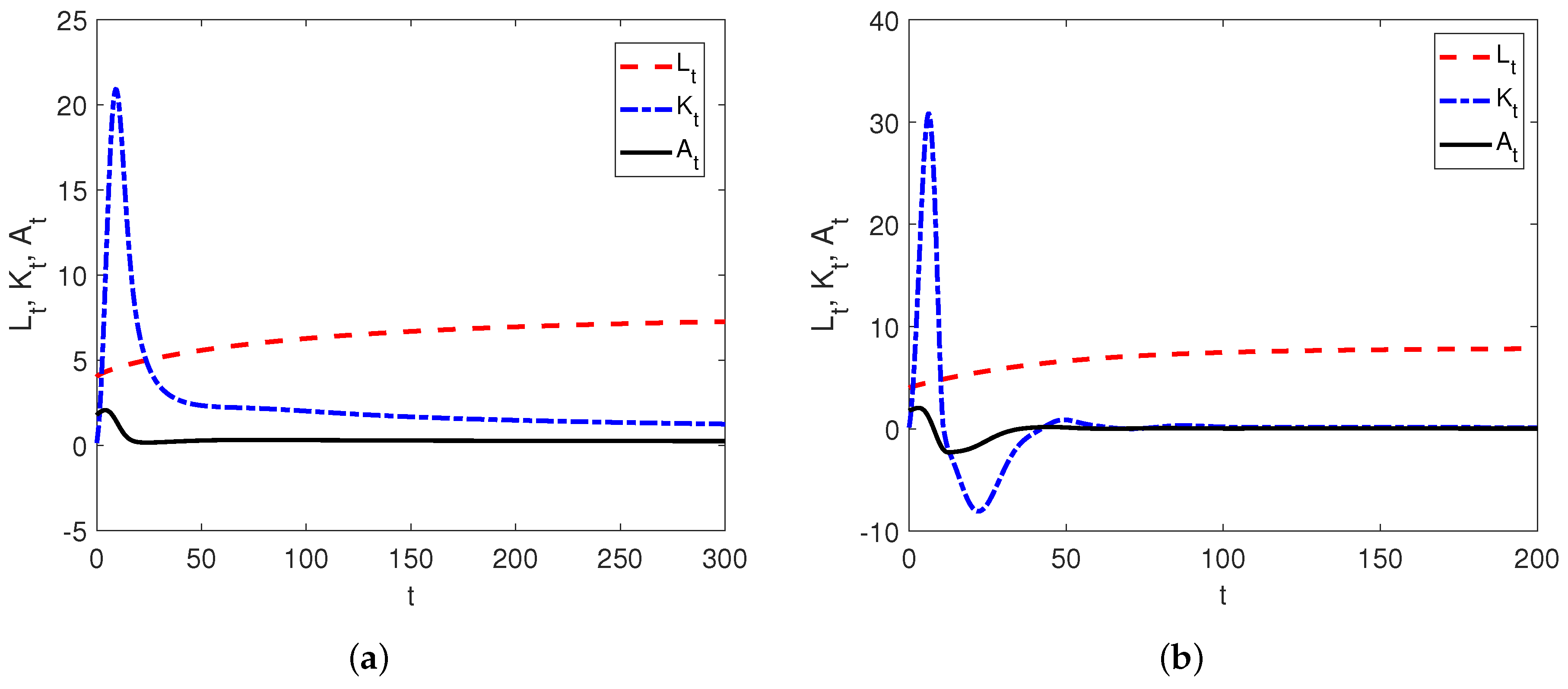

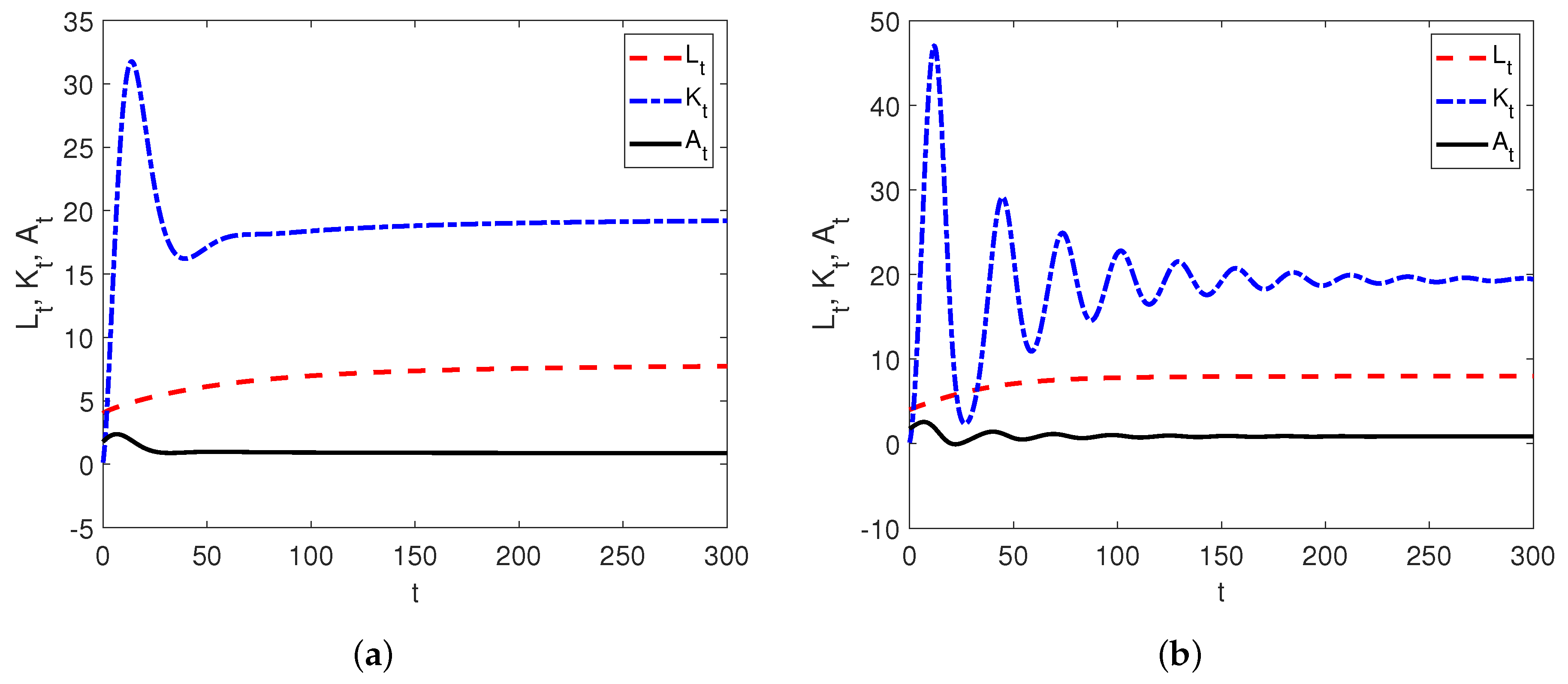

Case 1. To verify Theorem 1, we set The positive equilibrium point of system (

35) is calculated to be

. It can be verified that corresponding conditions in Theorem 1 are satisfied. According to Theorem 1, the equilibrium point

is Lyapunov asymptotically stable, and the convergence behavior of the response curve is shown in

Figure 1a. For comparison, we also simulate the response curve in the case of

in

Figure 1b.

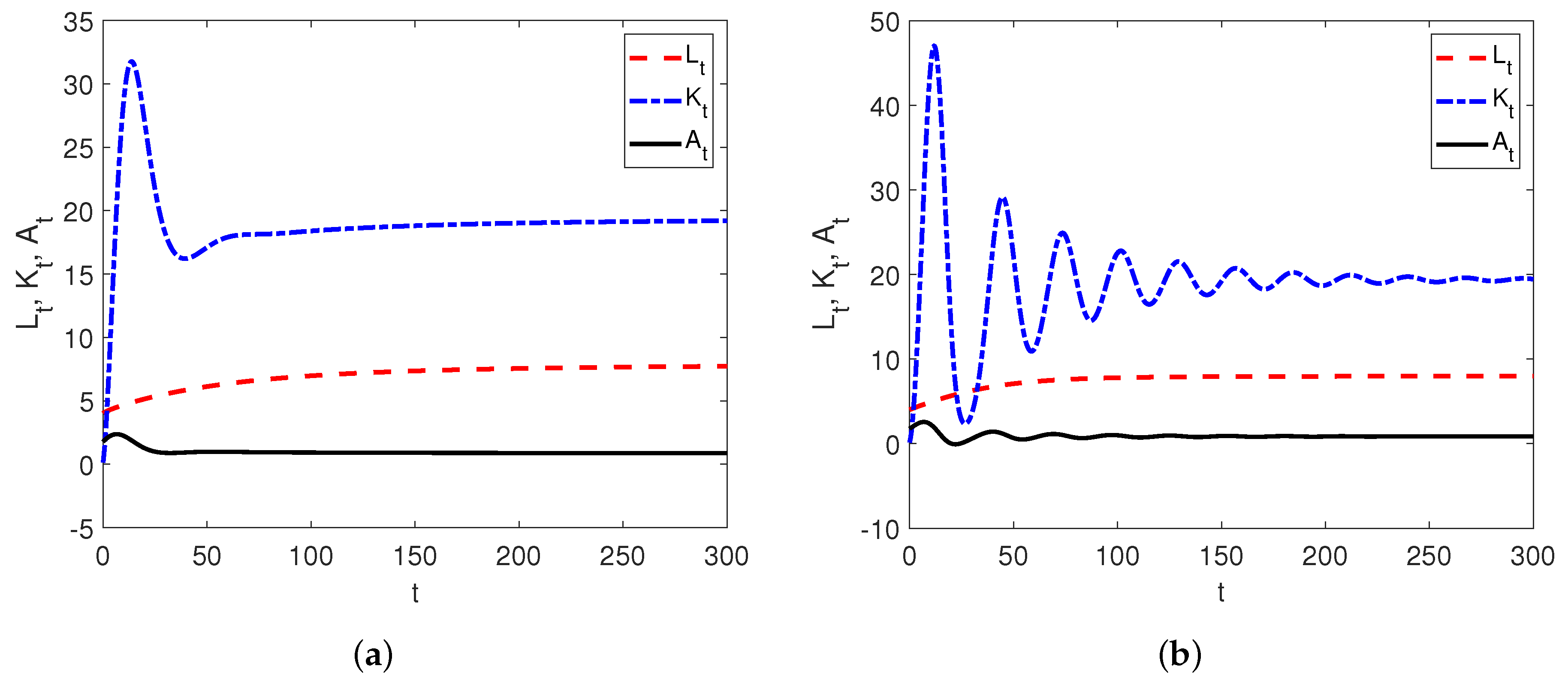

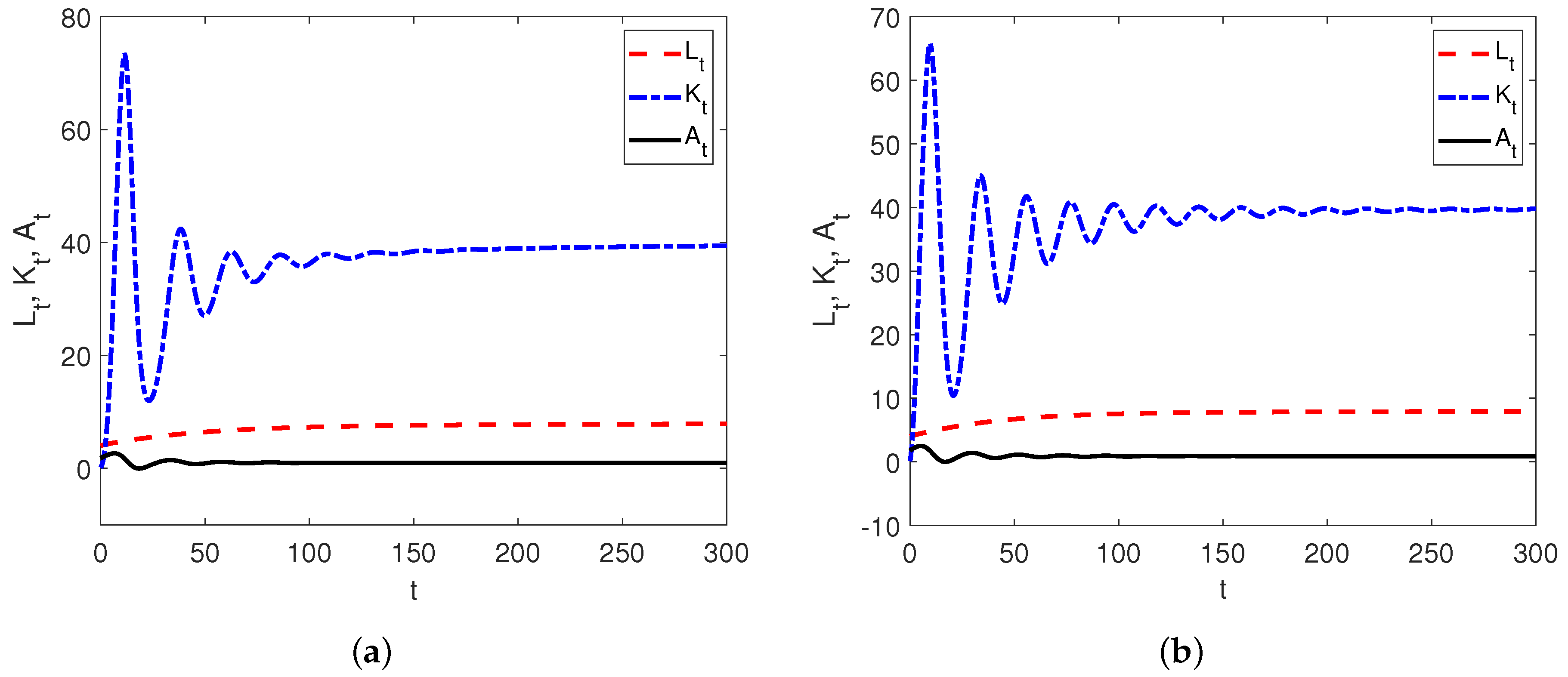

Case 2. To verify Theorem 2, we set The positive equilibrium point of system (

35) is calculated to be

. It can be verified that corresponding conditions in Theorem 2 are satisfied, so the equilibrium point

is Lyapunov asymptotically stable, and the convergence state of system (

35) is shown in

Figure 2a. Similarly, when

, the response curve of the memoryless model is shown in

Figure 2b.

Case 3. To verify Theorem 3, we set One of the positive equilibrium points calculated by numerical methods is

. It can be verified that corresponding conditions in Theorem 3 are satisfied, so the equilibrium point

is Lyapunov asymptotically stable, and the convergence state of system (

35) is shown in

Figure 3a. For

, the reponse curve is shown in

Figure 3b.

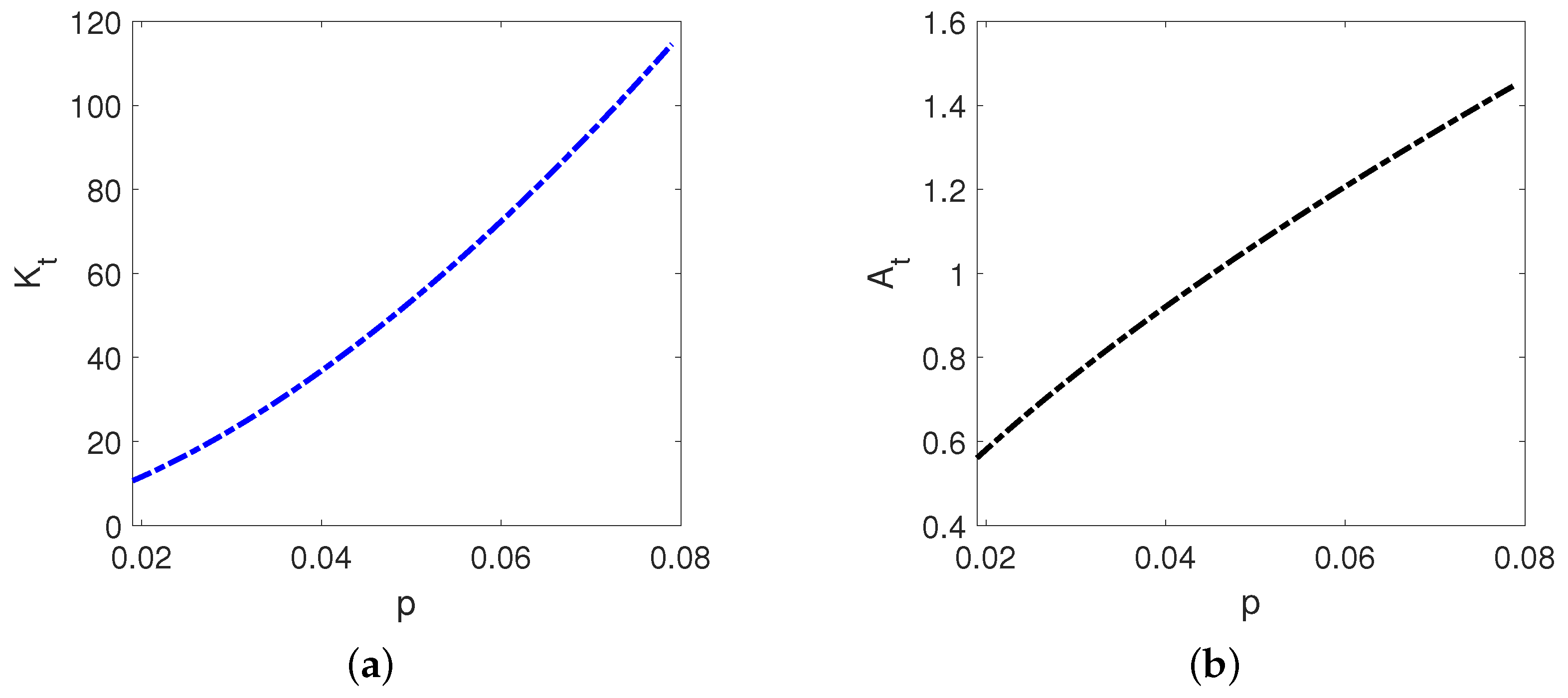

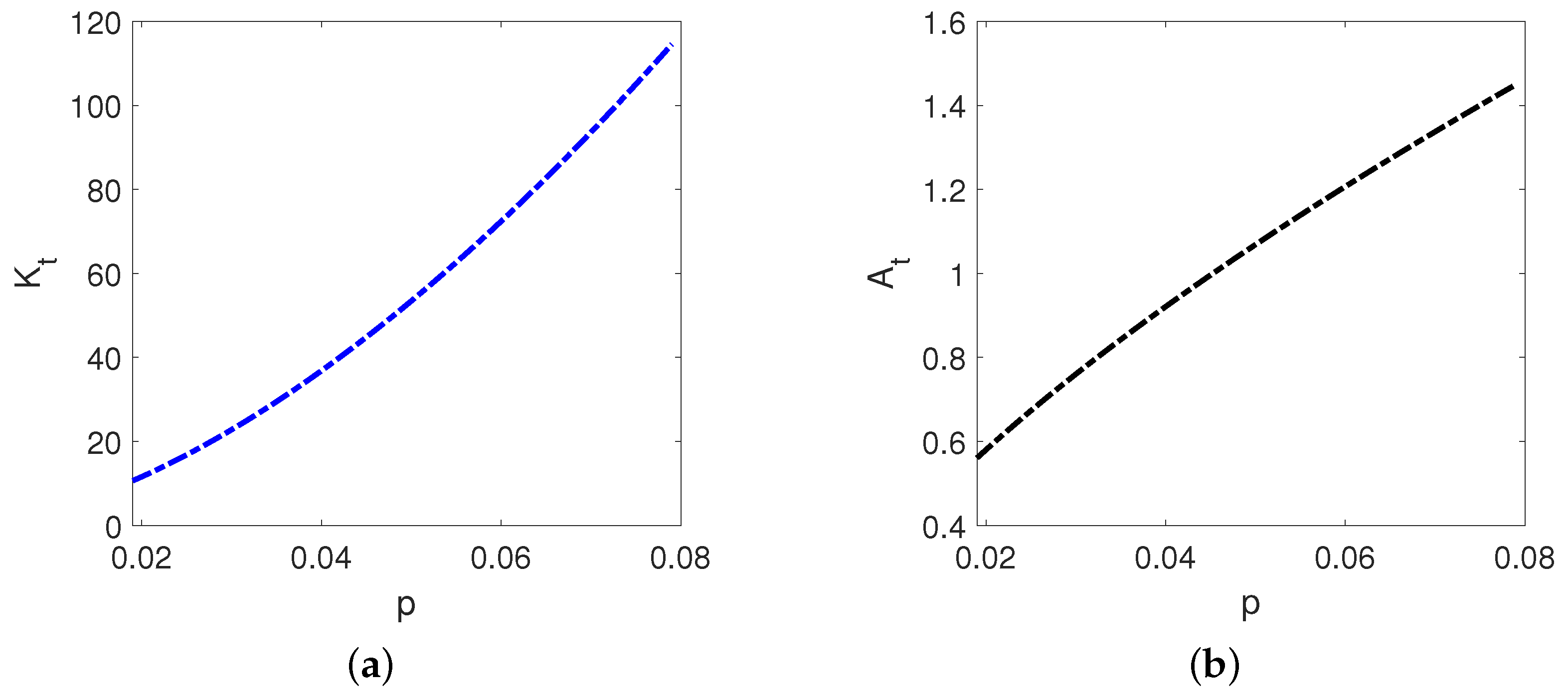

In order to analyze the influence of parameter variation on the equilibrium point and steady state, we perform parameter sensitivity analysis. Take Theorem 1 as an example. The following parameter values are chosen, and we only observe the influence of parameter

p on the system.

To obtain a stable equilibrium point, the suitable range of

p can be calculated through the stability condition displayed in Theorem 1, that is

. As

p changes within the interval, the equilibrium point keeps Lyapunov asymptotically stable, but the values of the equilibrium point gradually changes, as depicted in

Figure 4.

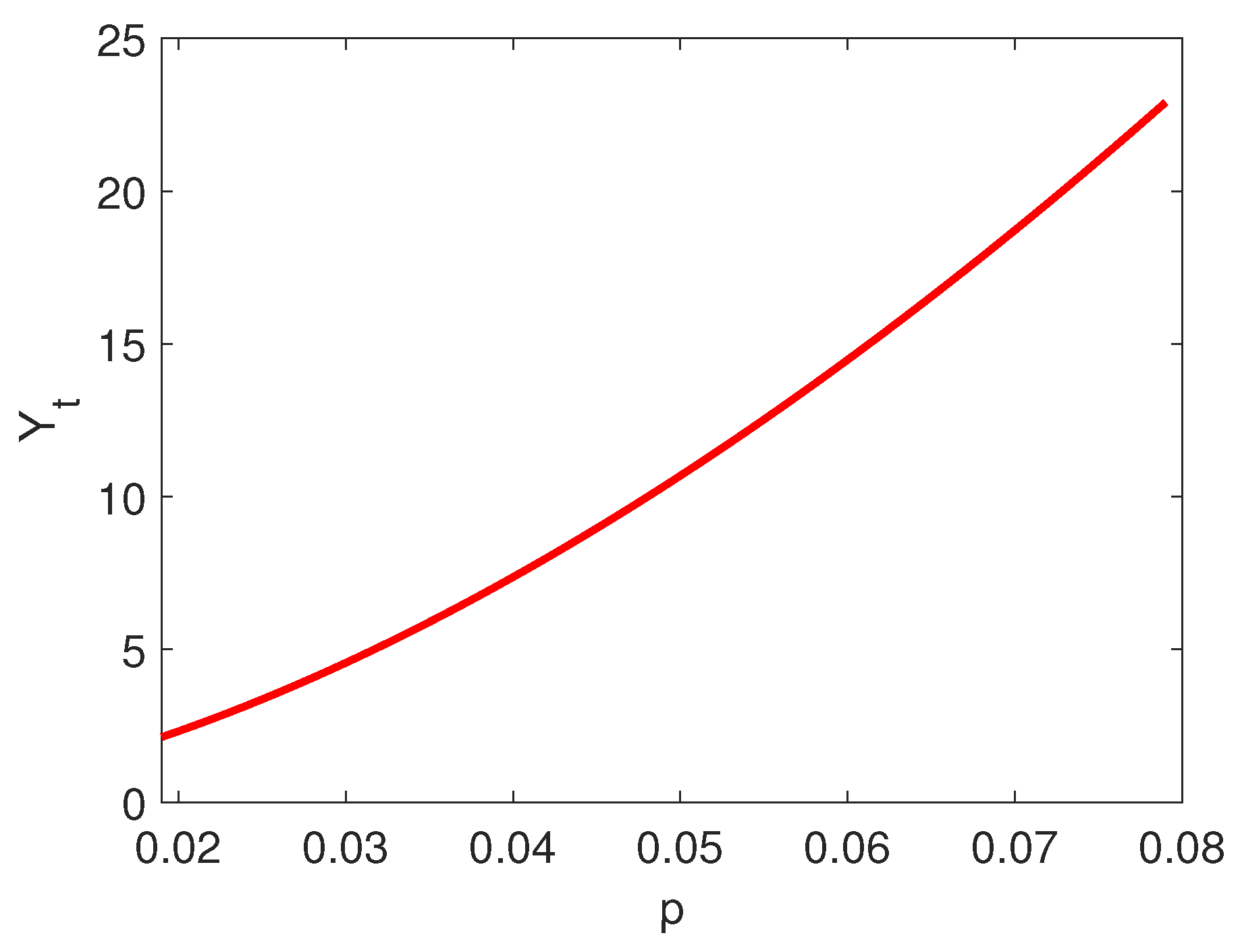

Furthermore, we use the Douglas production function

to calculate GDP value at the equilibrium point, which is shown in

Figure 5.

It can be seen that as

p increases, the equilibrium value of

and

are also gradually increasing, which drives GDP to a higher level, indicating economic growth. In system (

8),

p is TFP growth rate, reflecting the level of technological progress. On the one hand, when

p increases, the growth rate of TFP speeds up and stabilizes at a higher level. On the other hand, the acceleration of technological progress promotes capital accumulation, which further has a positive feedback effect on TFP due to endogenous growth. Therefore, under the dual influence of capital accumulation and TFP, the steady-state GDP will rise with the increase in

p. The analysis result of the parameter

p implies that increasing the TFP growth rate contributes to economic growth. It is consistent with the view that falls in TFP growth appear to explain past growth slowdowns of some middle-income countries [

40].

5. Economic Prediction

In this section, we predict China’s GDP in the next thirty years based on model (

8) and analyze its economic growth potential. To enhance the adaptability of the model, we allow the fractional orders

to change dynamically with time

t, denoted as

. For each period

t, we use the prediction error minimization principle and the grid search method to find the optimal fractional orders

. Then, we use curve fitting to predict the trend of

, and then predict the main variables (

) and GDP(

) in the next thirty years 2020–2050. Particularly, to clarify the impacts of different fractional derivatives and delay parameters on the predictions, we carefully choose a set of alternative

q and

to compare their prediction performance.

The data is taken from the “China Statistical Yearbook 2020”. It directly provides the working population (), total capital formation (), and GDP () from 1978 to 2020. Among them, the working population data appears an obvious gap around 1990 due to the different statistical method used. Therefore, we use the total population to regress and calibrate the working population by Ordinary Least Squares (OLS). For TFP, we use the Cobb Douglas function to calculate A as the true value of TFP, where the contribution ratio of capital to output is 0.6 as general.

Next, we set the parameters in system (

8) For working population

, we fit the integer-order population retardation growth model and get the growth rate

and the maximum population

million. Secondly, according to the final consumption rate data in 1978–2020, we set the average savings rate

. In addition, consulting relevant information, we take the contribution ratio of capital to output

, the depreciation rate

, the technological progress rate

, and the natural population growth rate

. For the sake of simplicity, we set

, that is, the third equation in system (

8) is simplified to

.

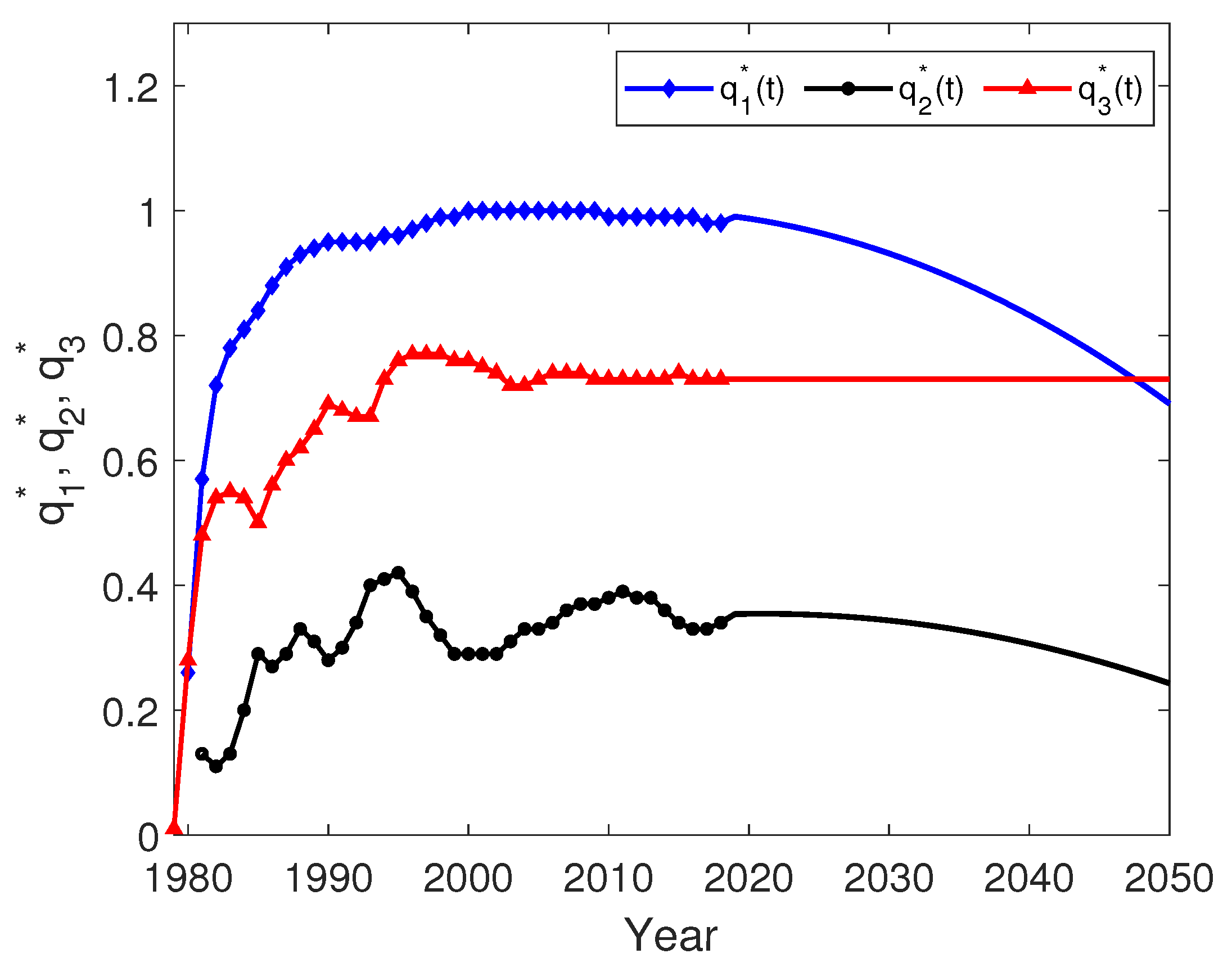

After the necessary data is ready, we start to make predictions. Above all, we show our approach to choose the suitable fractional derivative parameters

,

,

. To make the prediction more time-varying, we dynamically change the fractional derivative orders with time so that they turn into functions of

t, i.e.,

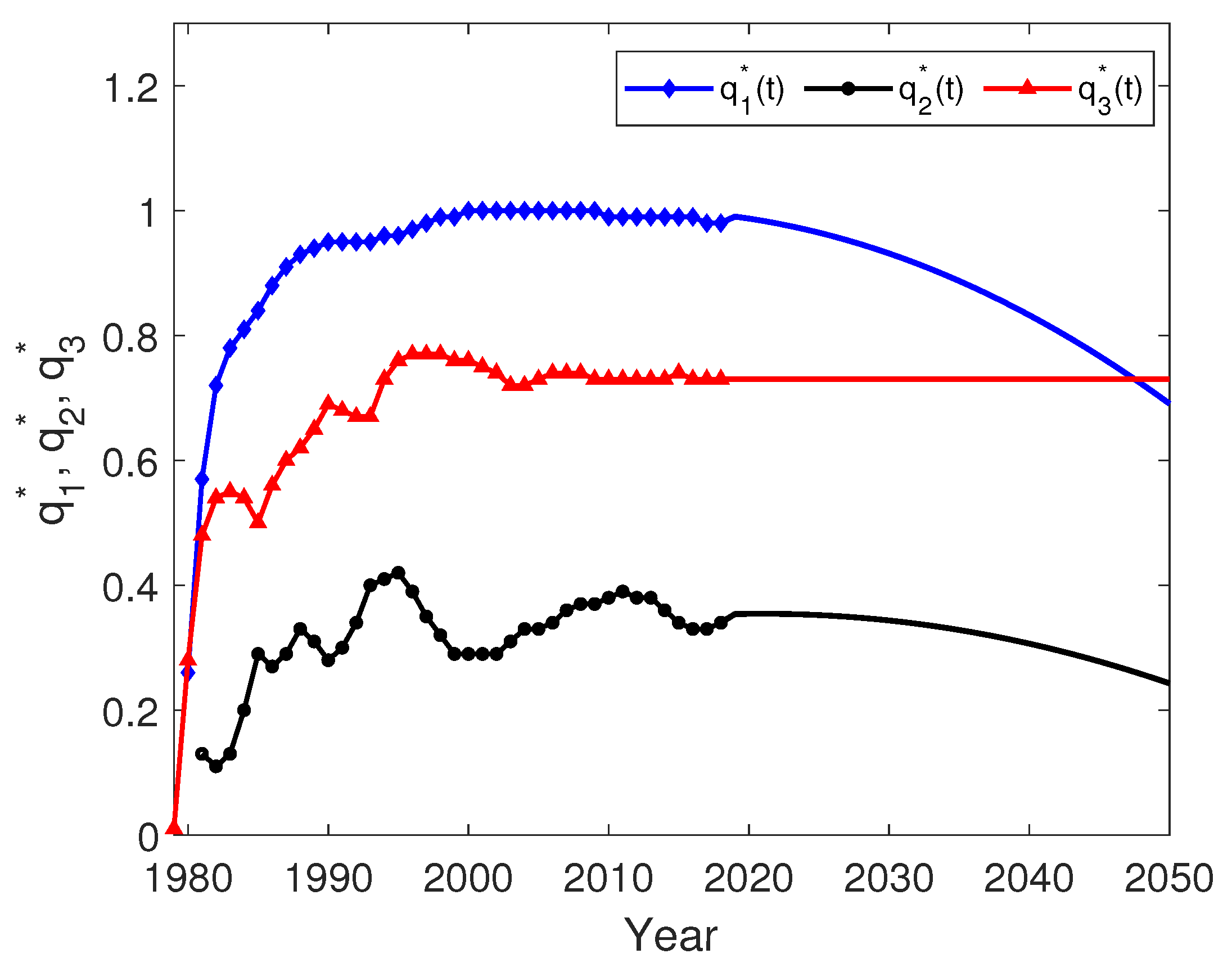

. We now use the existing data and model to solve them. Taking

as an example, we optimize it by minimizing the prediction error and obtain

where

is 2_norm. To solve (

36), for each period

t (

), we perform a grid search on

within the interval (0,1) by step length of

. In particular,

is figured out by the predictor–corrector method. For

, we fit

with a quadratic function and forecast its trend in the next thirty years as shown in

Figure 6 (the blue line). Using the same method, we can obtain the optimal

and

by minimizing the prediction error. As shown in

Figure 6,

(the red line) finally stabilizes at 0.73 around 2020, so we directly let

when

. As for

(the black line), we also perform a quadratic function fitting on

and predict its value in 2020–2050.

Based on

, we can calculate

according to Equation

using the predictor–corrector method. The fitted

and the predicted

are shown in

Figure 7.

The memory parameter

q plays a significant role in our framework. However, it is currently practically not studied in econometrics. Therefore, it is interesting and meaningful to explore its role in economic operations and its impact on economic predictions. We consider a wide range of

as well as the memoryless model

. Then, we take

as these fixed values and predict

in 1980–2050. As shown in

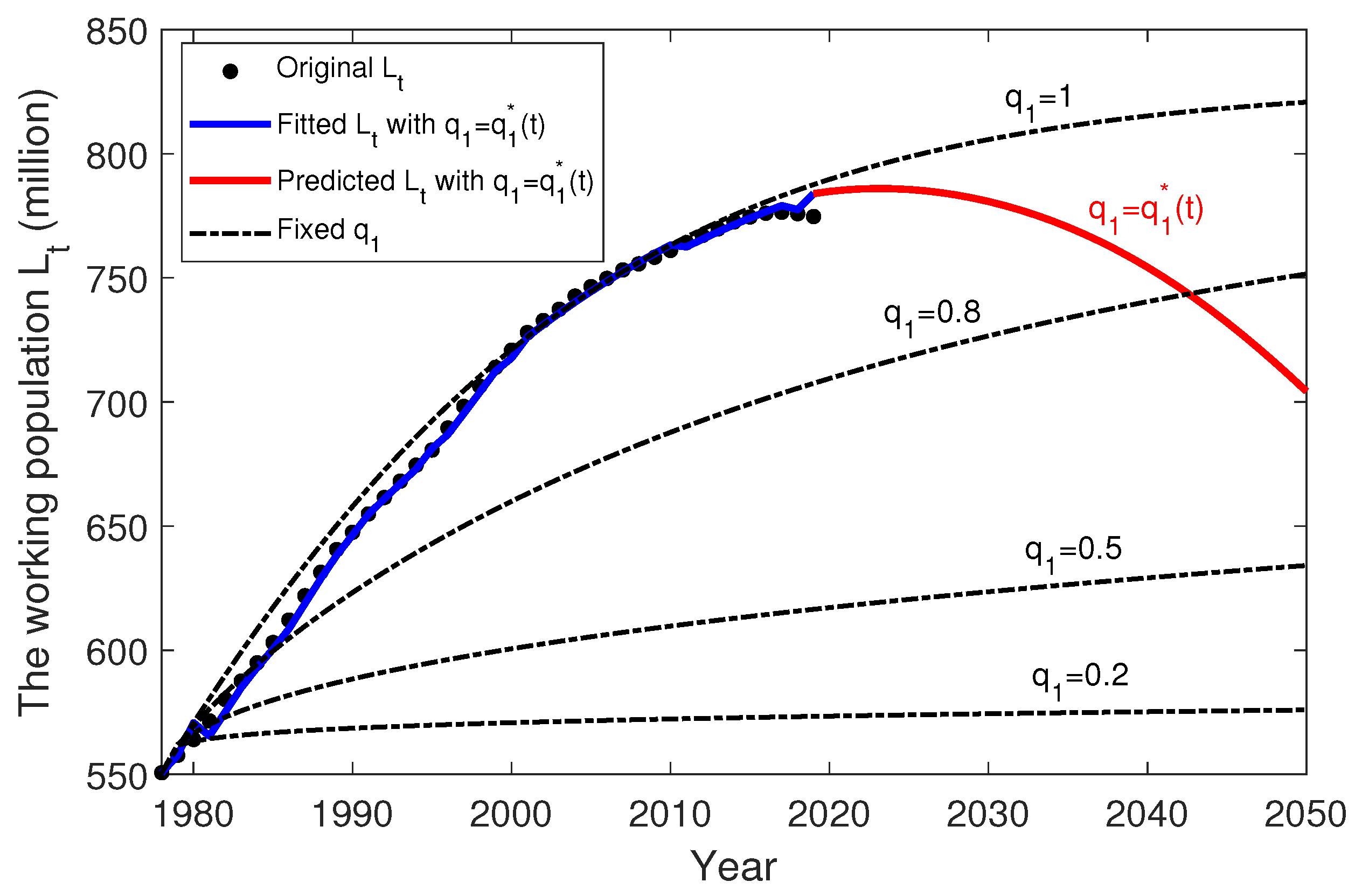

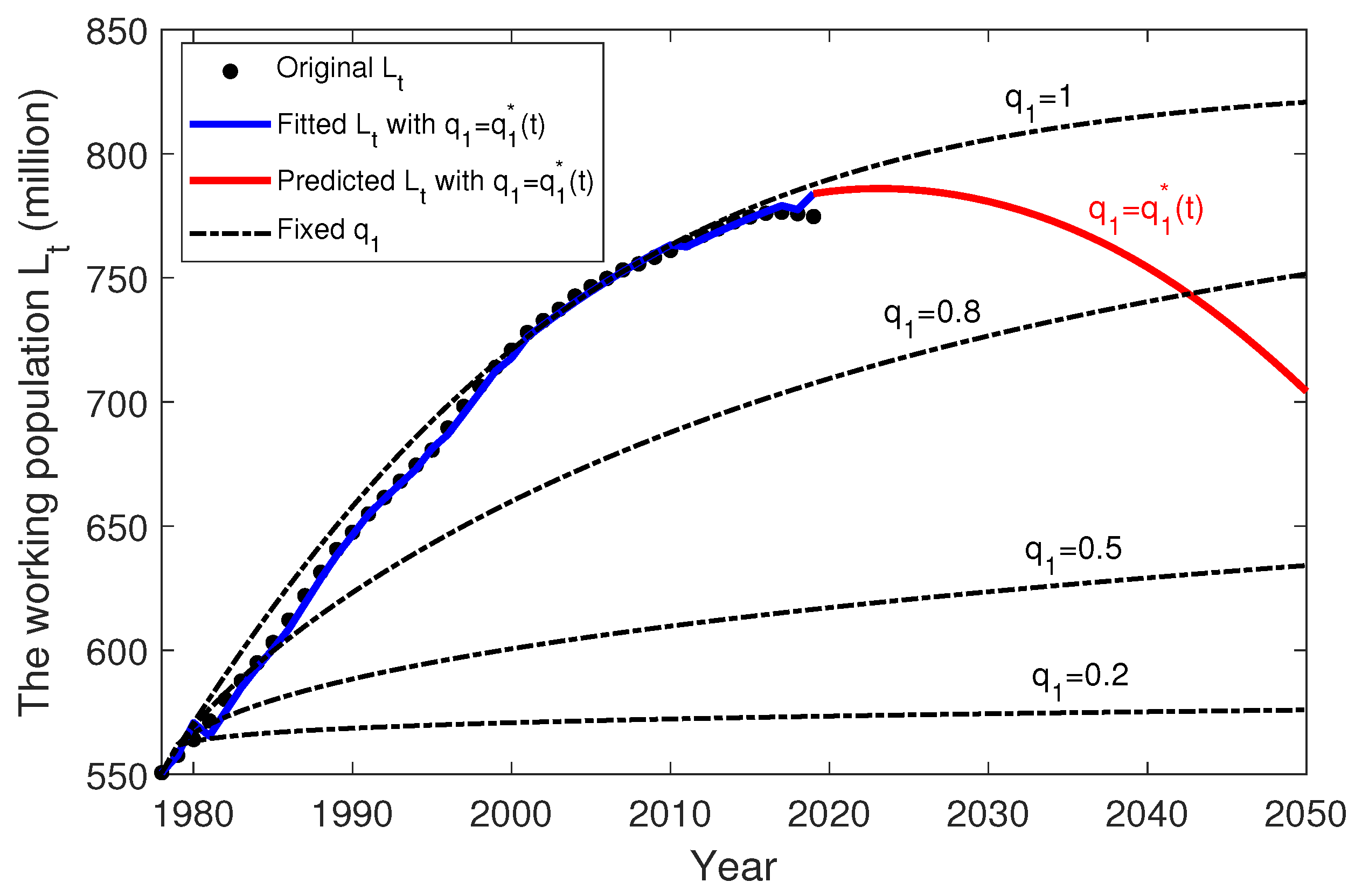

Figure 7, when

decreases, the predicted working population

declines, indicating that

describes the growth rate of population. In addition, compared with the optimal

, the memoryless

overestimates the working population, especially when

, while

greatly underestimates the working population.

The consideration of fractional derivatives does capture the memory and heredity feature in the population growth process, with its prediction more accurate. However, the fractional order parameters need to be carefully selected. Our method of minimizing the prediction error is proven to be an effective and precise approach to select the fractional derivative orders.

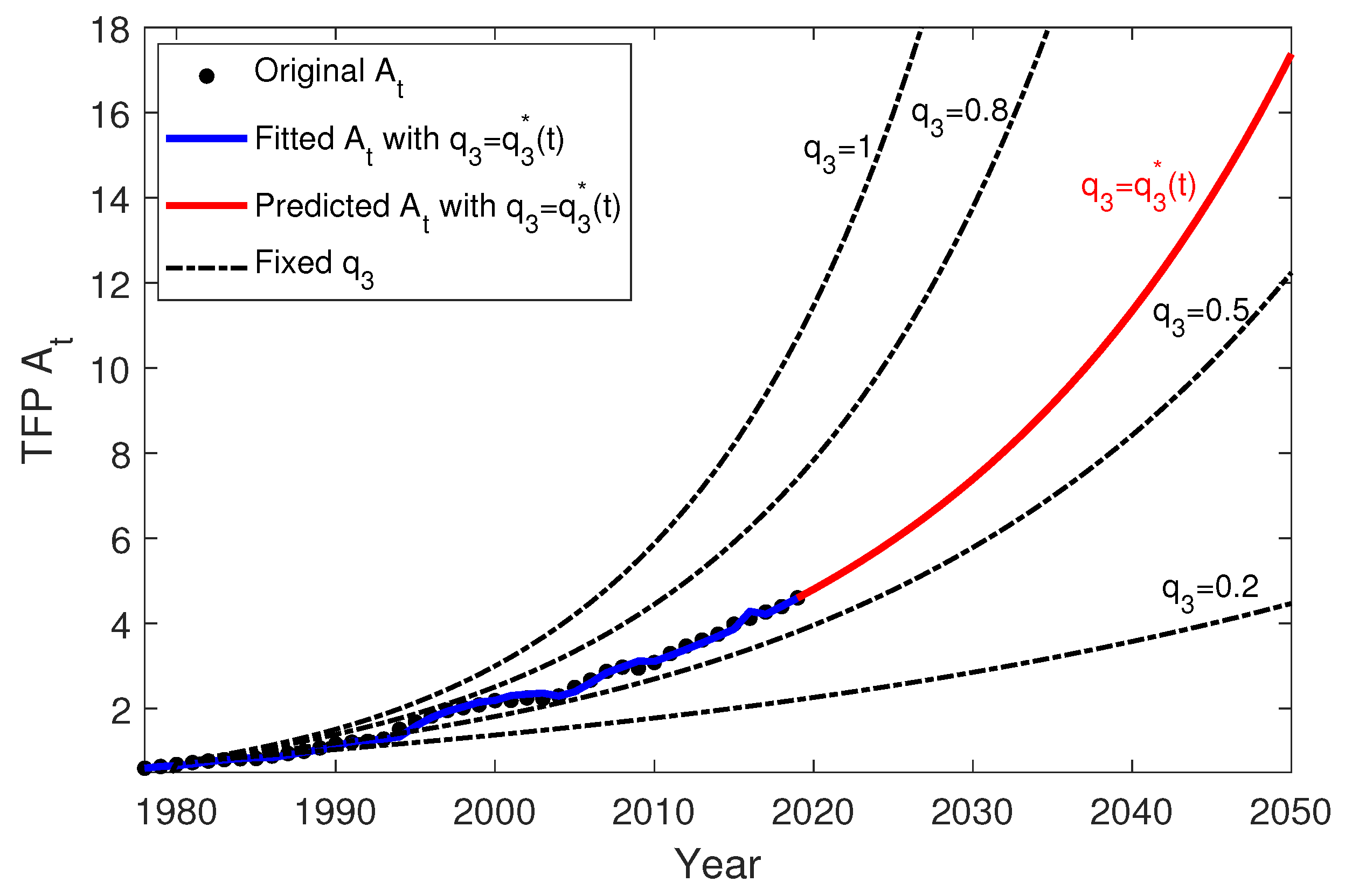

Similarly, based on the calculated

and the equation

, we can obtain the fitted and predicted

, as shown in

Figure 8. We also compare the prediction performance of

with a wide range of

and

. As reflected in

Figure 8, we conclude that the growth rate of TFP rises with the increase in

and

outperforms other fixed

.

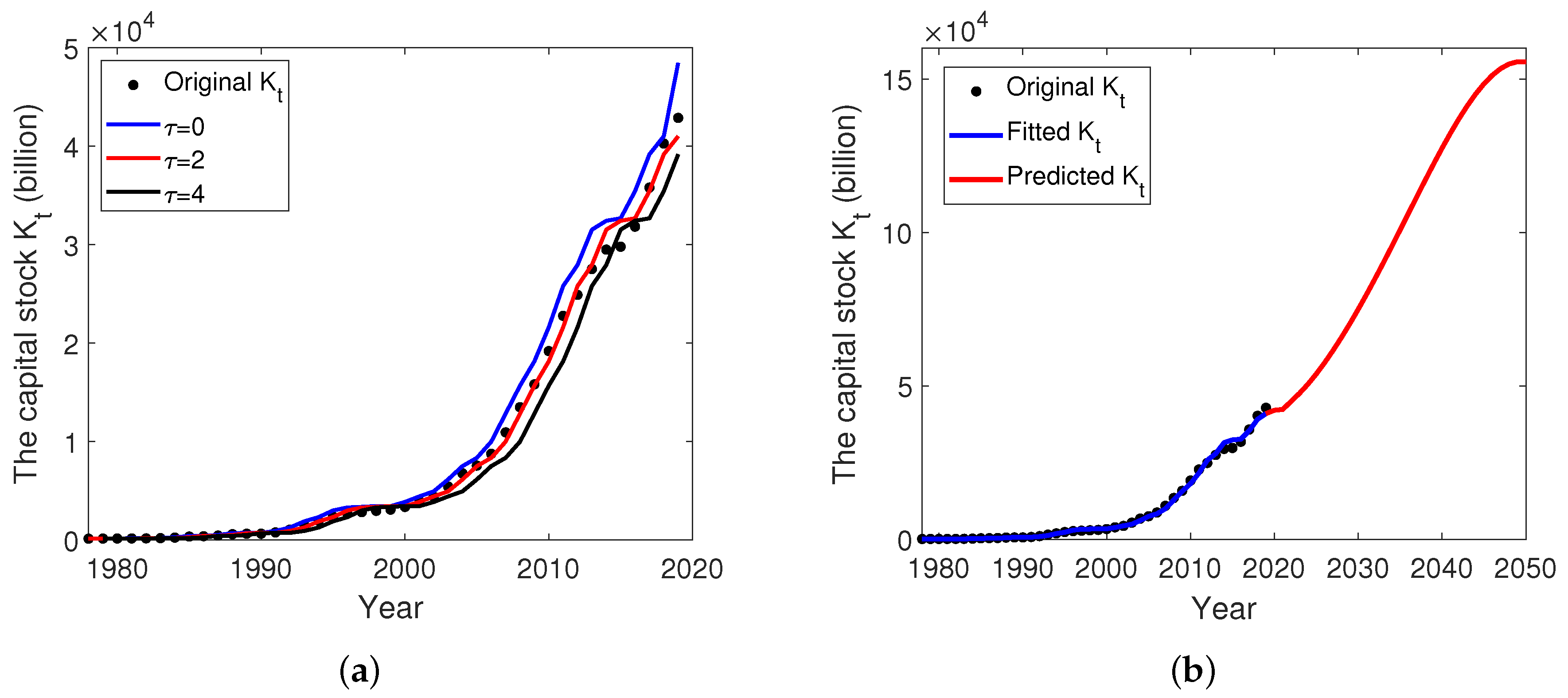

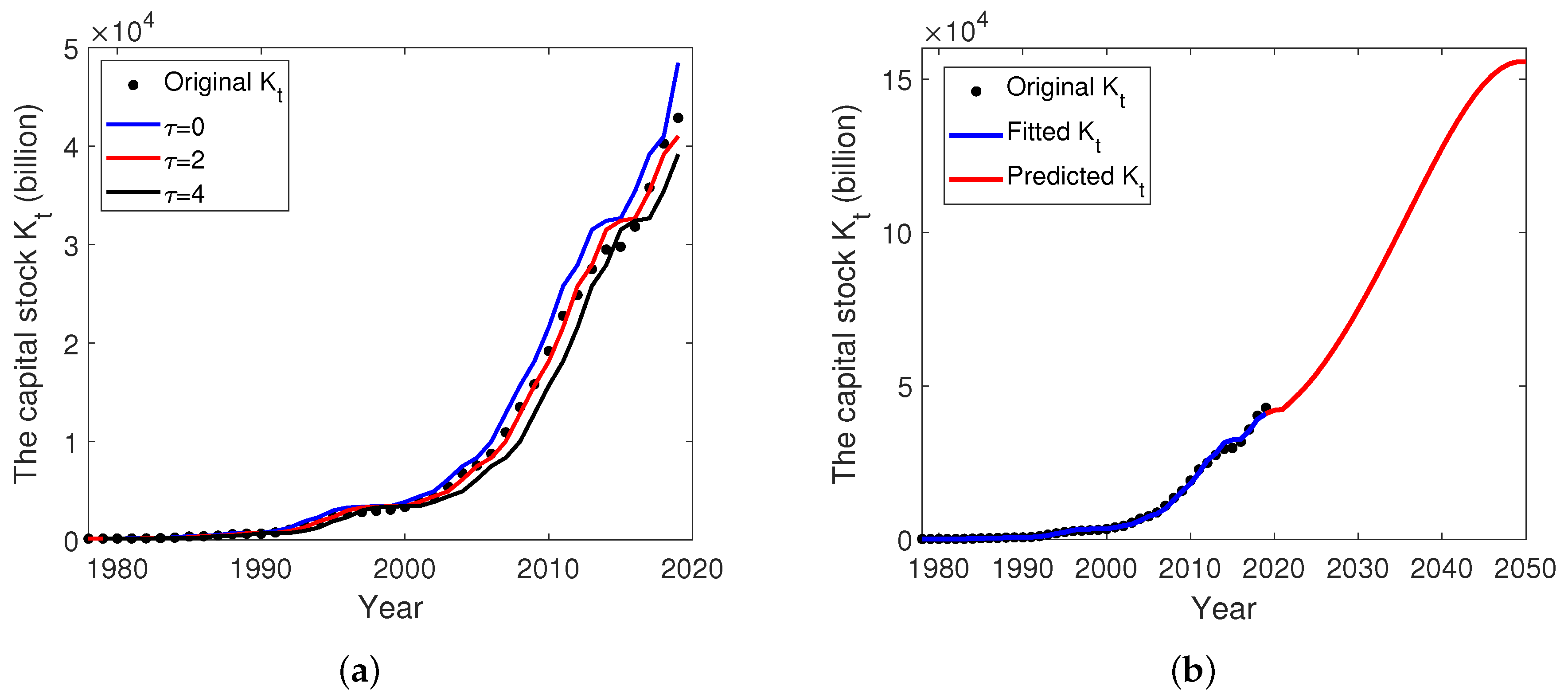

As for the capital stock

, we have the equation

, where

and

are replaced by the predicted values

and

, respectively. To select the suitable delay parameter

as well as examine the impacts of time lag on the predictions, we evaluate the prediction performance in three cases, namely no delay case

, medium delay case

and high delay case

. Similarly, the predictor-corrector scheme is used again to solve

. The fitting results of different delays are depicted in

Figure 9a.

As can be seen in

Figure 9a, the fitting result of the medium delay case

best matches with original

, so we choose it for our thirty-year prediction. It is worth noticing that

represents the no delay case, which slightly overestimates the capital stock. It is because

means that

is merely determined by

at time

t, while ignoring the historical state. In contrast, the time lag can take into consideration the previous values of economic variables in the capital accumulation process and emphasize the impact of historical data on the current

. It offsets the overestimation compared with the no delay case and largely improves the prediction performance. Therefore, we use

and

to predict

when

as shown in

Figure 9b.

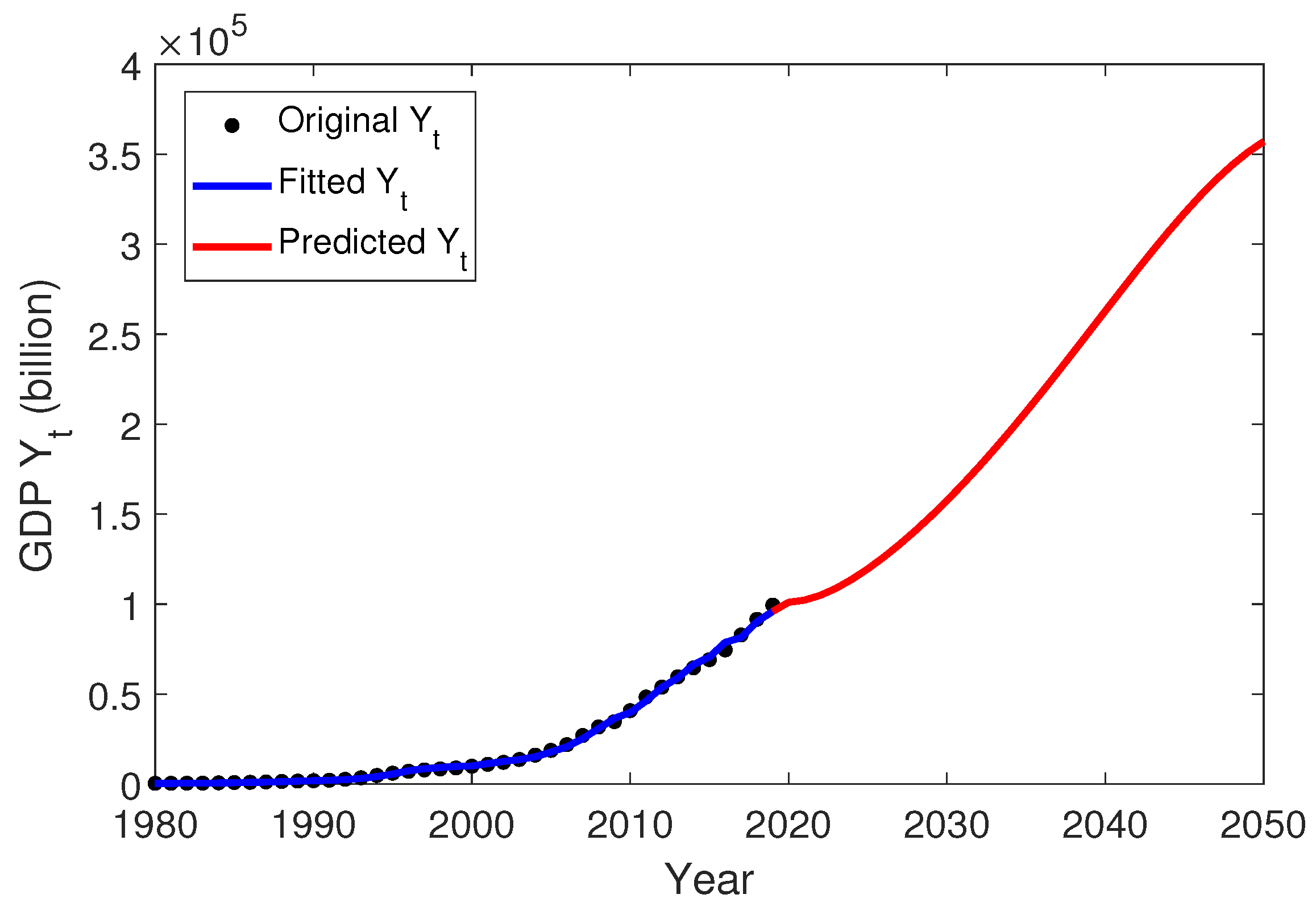

Finally, by using

and the predicted values of

,

, and

, we can easily get the predicted GDP (

) for each year, as shown in

Figure 10.

We now describe and analyze the prediction results from economic perspective. In

Figure 6, the fractional order

peaked around 2010 and then began to decline, leading to a downward trend in the working population (

) since 2020, as shown in

Figure 7. The decrease in the working population was attributed mainly to the government-sponsored family planning program and the so-called “one-child policy” introduced in the 1970s. The policy led to a sharp decline in total fertility rate and the acceleration of population aging [

41]. Consequently, the shrinking of the working population occurred and will probably continue in the approaching half a century [

42].

As for the prediction of TFP, since the fractional order

reached a plateau after 2000, fluctuating slightly around 0.73, TFP in 2020–2050 will probably continue to increase following the previous trend. In a developing country like China, the increase in TFP is largely caused by the “catch-up effect” which comes from the process of catching up from post-developed countries to developed countries. Evidence from multiple nations shows that if developing countries make full use of the advantages of chasers, they have the opportunity to accelerate development [

43].

Figure 9b indicates that the capital stock still holds an upward trend, but the growth rate will slightly slow down. The increase in capital stock makes it possible for developing countries to take advantage of advanced technology and accelerate productivity, which has a significant positive long-term impact on economic growth [

44]. Furthermore, the positive feedback is expected to continue in the short term according to the prediction.

Finally, as can be seen in

Figure 10, China’s GDP will continue to grow at a medium-to-high speed in the next five years, approaching about

billion in 2050. Despite a slight decrease in the working population, the increase in capital stock and the rise in TFP still provide persistent and vigorous impetus to economic growth.

However, in this paper, it is worth emphasizing that China will encounter multiple obstacles on the road to economic growth, and these impediments have already emerged in our forecasts. On the one hand, the decline in the working population is an inevitable trend, which indicates the disappearance of the demographic dividend. On the other hand, although the capital stock is still growing, the growth rate has shown signs of decelerating. We should have a clear understanding that the high-speed economic growth path derived by the accumulation of capital is unsustainable and will eventually come to an end in the long run. When capital is accumulated to a certain level, China will probably experience the development predicament like other developed countries such as Japan and South Korea. Therefore, in order to break through the dilemma, we should focus on TFP. According to the regularity of economic growth mode, the high contribution of TFP to economic growth usually appears when entering the mature period of growth deceleration [

45]. In other words, China needs to transform its economic growth into a trajectory dependent on TFP growth. In our forecasting model shown as

Figure 8, TFP is still growing along the trend in the short term, which, therefore, leads to sustainable economic growth. In conclusion, increasing the contribution rate of TFP in the future is the core goal and new engine of China’s economic growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}