1. Introduction

The beer industry in the United States has experienced rapid growth in the “craft” beer segment in recent years, and declining sales in more mainstream segments. By 2016, for example, the craft segment had grown to 21.9% of U.S. beer sales by dollar value [

1], while domestic sales were down by 2.8% [

2]. It is no surprise then, that the definitions of these categories are contested [

3], and that big breweries (those producing over 6 million barrels per year) have increasingly moved into the “craft” space. They have done so by introducing craft-like brands and/or by acquiring formerly independent craft breweries. Critics have called these actions “craftwashing” [

4,

5], drawing from term greenwashing, which describes deceptive marketing practices for environmental issues.

Previous scholarly studies of the craft beer industry have identified a number of regulatory barriers that hinder the growth of this segment, such as excise taxes, zoning laws and distribution restrictions [

6,

7,

8,

9,

10]. Other researchers have explored consumer perceptions of “authenticity,” and found that craft beer drinkers have negative perceptions of beer produced by big brewers [

11] (or even breweries that offer beer styles associated with big brewers [

12]). There has been little research, however, on how these opaque patterns of ownership are reflected in “craft” beer selections at retailers.

How effective are craftwashing strategies in the craft beer segment? More specifically, (1) how many formerly independent craft beers are actually owned by big brewers; and (2) how is this represented on the shelves of typical retailers when ownership ties are obscured? To begin to answer these questions, I conducted an analysis of ownership of leading big brewer and craft beer brands, and visualized this in a cluster diagram. I then applied these results in an exploratory case study of the craft beer sections of 16 retailers in the Lansing, Michigan metropolitan area.

The results indicate that nearly all big brewers engage in craftwashing strategies, and that they have been effective in taking up 30% of “craft” shelf space in the case study area, as measured by all 4- and 6-pack facings recorded. In addition, retailers that were locally-owned were more likely to offer both larger craft sections, and fewer brands with ownership ties to big brewers. Below I provide additional background and my theoretical perspective/hypotheses, followed by more detail on the methods, results, and a discussion of their implications.

1.1. Background

An initial craftwashing strategy was launching “faux craft” or “crafty” beers, with the production of these products by big brewers kept relatively hidden [

13,

14,

15]. The packaging, placement, and even the price of these beers leads typical consumers to believe that they are purchasing an independently owned craft beer. One example is Anheuser-Busch InBev’s (Leuven, Belgium) brand Shock Top: an internal document in 2014 touted data indicating 75% of consumers thought it was from a small brewer, and highlighted the line, “Shock Top is (AB InBev subsidiary) Labatt’s big bet in the battle against Micro Craft” [

16].

The “crafty” strategy, however, encountered slower sales in recent years, such as an estimated 4% decline for Molson Coors’ (Denver, CO, USA) brand Blue Moon and 9% decline for Shock Top in 2016 [

17]. As a result, a more recent strategy is the acquisition of successful craft breweries by big brewers. AB InBev, for example, has acquired ten craft brewers in the U.S. in the last seven years, as shown in

Figure 1, and has partial stakes in five more. Ownership ties to the new parent corporations are also typically not disclosed, even as the big brewers’ resources enable the distribution and marketing of newly acquired brands to increase dramatically.

Craft brewers, particularly those organized in the Brewers Association (Boulder, CO, USA), have been increasingly vocal in their displeasure with these actions. They point out the numerous efforts big brewers have engaged in to keep independent craft brewers off the shelves of retailers and distributors, as well as to discourage consumers from buying their products. Just a few examples include:

One of the two leading beer firms is frequently designated by retail chains as the “category captain”, which gives them the power to design the placement and allotted shelf space for the entire beer section, including direct competitors’ products [

18].

After an investigation, the Department of Justice prohibited AB InBev from “continuing practices and programs that disincentive distributors from selling and promoting the beers of... rivals” [

19].

AB InBev ran advertisements during the 2015 and 2016 Super Bowls belittling craft beer drinkers [

20,

21].

Although the U.S. government has not yet intervened in craftwashing disputes, there have been several private lawsuits accusing big brewers of deceptive marketing for “import” brands that are actually brewed in the U.S. (one against AB InBev brand Beck’s was successful) [

22]. In Australia, however, the largest brewery was fined approximately US

$18,000 by a government agency, and agreed to stop distributing its “Byron Bay Pale Lager”. The regulators said the packaging on the Carlton & United (now a division of AB InBev) beer had deceived consumers into thinking it was made in a small facility, far from the industrial-scale brewery where it was actually produced [

4]. Jim Koch, the founder of Boston Beer Co., (Samuel Adams) (Boston, MA, USA) has said, “I think a beer drinker shouldn’t have to hire a private detective to figure out who actually makes the beer that they’re drinking” [

23]—although it should be pointed out that he engaged in a very similar practice with the “Oregon Beer and Brewing Co.” (Salem, OR, USA) in the 1990s [

24].

In response to craftwashing, the Brewers Association, which represents small and independent brewers in the U.S., released an “independent craft” seal in June 2017. Members and eligible non-members can place this seal on their beer labels, to help consumers identify which breweries do not have hidden ownership ties. To qualify, a brewery must produce 6 billion barrels or less annually, and have less than 25% ownership by a larger beer/wine/spirits firm [

25]. Under this definition, craft brewers that sell ownership stakes to private equity firms remain eligible for membership. The goals of private equity firms, however, are typically to achieve returns of 25–100% compounded annually, and a payout within three to seven years [

26], which increases the likelihood that these breweries will eventually be sold to larger firms. One of the largest members of the Brewers Association, Boston Beer, is publicly traded, and is therefore also susceptible to takeover attempts by larger firms.

1.2. Theoretical Perspective and Hypotheses

In this study I use Nitzan and Bichler’s theoretical framework of Capital as Power [

27] which posits that capitalists seek to improve their position relative to other dominant firms. Importantly, this means that they do not attempt to maximize profits, nor necessarily to achieve growth in production or sales, as long as they obtain a bigger share of the total, such as by beating average returns [

28,

29]. A key means of achieving this goal is “strategic sabotage”, which may involve numerous strategies for increasing firms’ “earnings and capitalization

relative to—and often

by undermining—those of others” [

29] (p. 7). Maintaining regulatory barriers that disproportionately affect smaller firms is one example, but controlling shelf space is another—dominant beer firms have been effective in increasing the visibility of their offerings, while also limiting or even removing visibility for competitors. AB InBev and Molson Coors, for example, have allegedly used their power as category captains, mentioned above, to take up disproportionately more shelf space relative to their percentage of beer sales [

18], particularly for the most prominent locations, such as at eye level and the end of rows [

30,

31].

These strategies of strategic sabotage do not need to be logically consistent, and may result in ironies—an example is an AB InBev Super Bowl commercial mocking pumpkin peach ale, just one week after acquiring a craft brewery that makes an ale with pumpkin and peach flavors. Dick Cantwell, one of the founders of this craft brewery, Elysian, turned in his resignation notice soon after the ad was aired. He explained, “There’s a big difference between an independent craft brewery that makes its own decisions and an enormous company that has one arm devoted to what they consider to be craft beer. In the case of Anheuser-Busch, they are perfectly content to have the different arms of their company at war with each other” [

32]. Big brewers have frequently responded to criticisms from smaller craft brewers with variations on the theme “can’t we all just get along?” They emphasize their shared interest in growing beer sales, while also deflecting attention away from their actions that limit growth in the craft segment [

5,

33].

Based on a previous study of wine in this region, which reported more varieties of wine and more Michigan-produced wine at locally owned retailers [

34], I developed two preliminary hypotheses for this study. These were that when controlling for retailer format (which allot differing amounts of shelf space to beer):

Hypothesis 1. Locally-owned retailers offer more craft beer selections.

Hypothesis 2. Locally-owned retailers offer fewer brands with ownership ties to big brewers.

Additional support for these hypotheses come from the fact that locally-owned retailers are much less likely than national chains to select one firm as a “captain” for category management. Captains may increase the number of stock-keeping-units (SKUs) for their own firm, but also frequently reduce the total number of SKUs in the category [

35]. To differentiate themselves from chain stores, some locally-owned retailers emphasize their selection of beers from regional craft breweries, including signage to highlight local or regional offerings. Increasingly, however, nationally-owned retailers are imitating these strategies to capture growing consumer interest in local craft beer [

36].

2. Methods

For the first component of this study, the 25 largest brewers in the U.S. were selected based on data from Beer Marketer’s Insights [

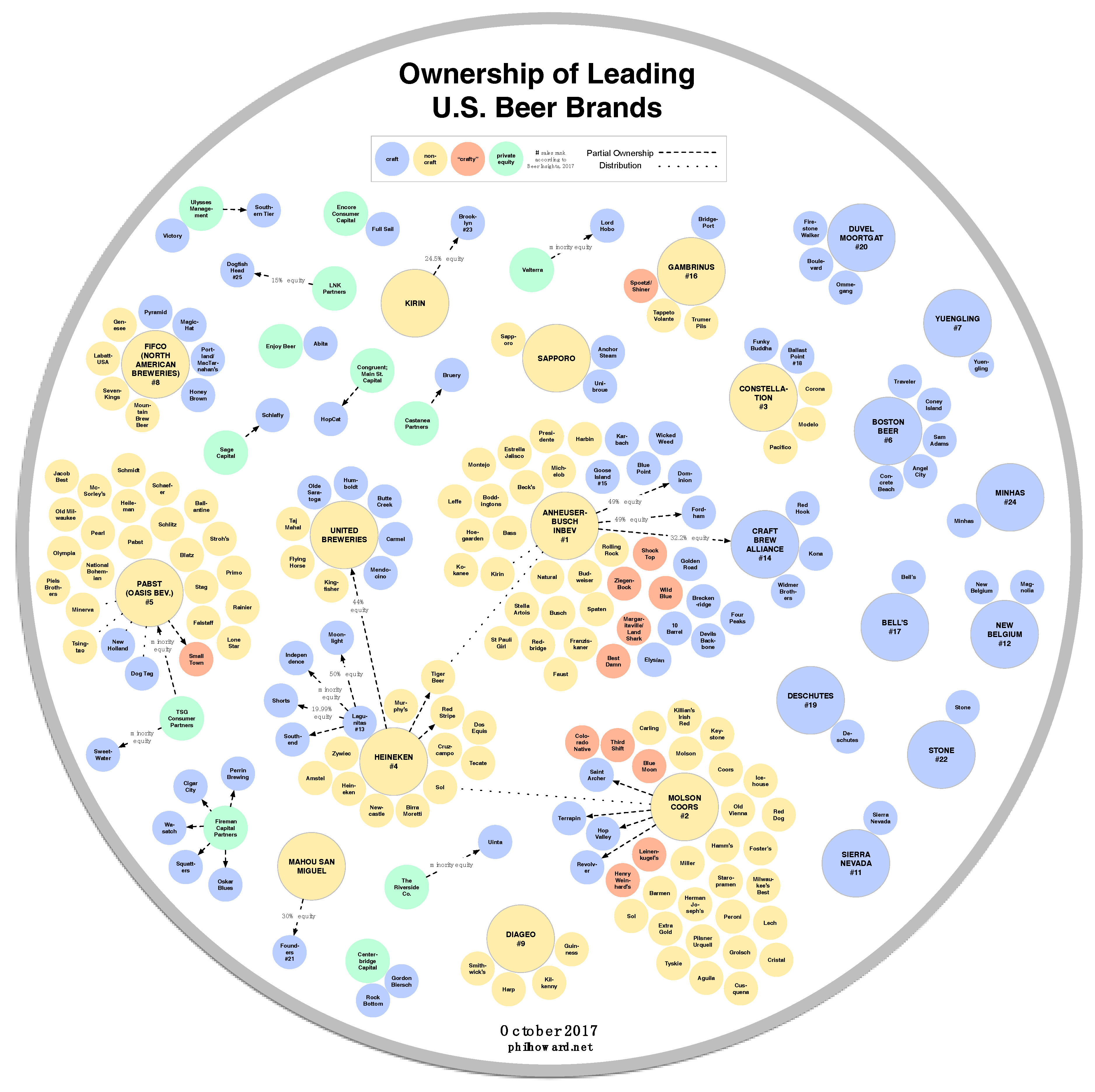

37], and the ownership relations of their subsidiary brands visualized in a cluster diagram. A cutoff of the top 25 was selected because no breweries below this ranking had ties to big breweries in the US, and therefore they would not have increased the complexity represented in in the visualization. Additional craft beer brands were added to the figure, however, if they had ownership connections with big brewers headquartered in other part of the world (e.g., Japan), or if they had ties to private equity firms.

This figure was developed using the diagramming software OmniGraffle (version 6.6.2, Seattle, WA, USA). The only brewer on the Beer Insights list that was omitted was tenth-ranked Mike’s Hard Lemonade Co., (Chicago, IL, USA) because the Brewers Association excludes flavored malt beverages from their definition of “beer”. Parent firms and their brands were coded as craft or non-craft brewers, based on Brewers Association definitions (prior to acquisitions). Brands that promote a “craft” image, but introduced by big brewers, were color coded in the visualization “crafty”. Partial equity was represented with dashed lines, and the percentage of minority stakes identified, if known. Distribution alliances were represented with dotted lines.

As mentioned previously, clear ownership data is rarely found on the product labels of brands owned by big brewers, and even websites may not reveal the full extent of subsidiary brands (Leinenkugel’s website, for example, lists the copyright as belonging to Jakob Leinenkugel Brewing Company—Chippewa Falls, WI, USA, with no mention of parent corporation Molson Coors). The data for this visualization therefore came from numerous sources, including press releases, newspaper articles, and industry trade journals or blogs. Key sources of data included Vinepair’s “Definitive Timeline of Craft Beer Acquisitions [

38] and a more narrowly focused cluster diagram I previously created based on 2010 data [

39], although all relationships were verified with additional sources to ensure they were accurate and up to date.

The second component of this research was an exploratory case study of craft beer selections at retailer shelves in the Lansing, Michigan metropolitan area in October 2017. It encompassed the city of Lansing, but focused primarily on retailers in the more affluent cities and suburbs to the north and east, which were expected to have larger craft beer selections (even compared to other outlets belonging to the same chain in this area).

Table 1 shows the demographics of the metropolitan area, which indicates a lower average income, higher poverty rates, and less ethnic diversity in comparison to national averages. Michigan ranks 6th among all states for the highest number of craft breweries [

40], and includes two of the top 25 breweries by sales in the U.S. (Bell’s and Founders). State-specific regulatory barriers [

6,

7,

9], and the fact that beer is heavy and expensive to transport [

41], both present challenges to national distribution for many craft beer firms. As a result, retail selections found in this area are unlikely to be representative of other regions of the country.

An inventory was conducted at 16 retailers, which were purposively selected to ensure representation along two dimensions: (1) retail format; and (2) store ownership.

Table 2 shows the number of retailers in three categories for each of these dimensions. Four of the format/ownership combinations were represented by just one retailer (e.g., a single nationally-owned natural foods retailer), because there were no other options to select from in this area, which reduced the power of the study to detect differences among these dimensions.

The inventory was limited to 4- and 6-pack facings in the refrigerator cases at most of these retailers. A facing is a package visible at the front of the shelf, with identical items stocked behind it, as shown in

Figure 2; these are periodically repositioned at the front of the shelf by employees as items are removed by customers. Most retailers also stocked single bottles/cans and larger packages (e.g., 12- and 15-packs) in their refrigerator cases, as well as various sizes on unrefrigerated shelves. However, these typically duplicated brands and varieties stocked as refrigerated 4- and 6-packs, and thus were not recorded. An exception was made for two of the natural foods format retailers—these had more limited refrigerator space, which contained primarily single bottles/cans, and 4- and 6-packs were displayed primarily on nearby unrefrigerated shelves. All 4- and 6-packs were recorded at these two stores, refrigerated or not.

Craft beer was shelved distinctly from other types of beer at all grocers and natural foods retailers in the study, and every facing in the craft section was recorded. Although the visualization of national ownership includes relationships for brands in the relatively new category of alcoholic root beers, nearly all Lansing-area retailers shelved these products in a separate section (usually with flavored malt beverages and hard ciders). Some convenience stores, due to their more limited shelf space, did not have distinct craft sections, and mixed craft brands with other types of beer. For these retailers, only the brands typically found in the craft section of larger retailers were recorded (e.g., omitting alcoholic root beers, mainstream beer brands and “import” beers).

These data were then coded for parent company ownership, and analyzed statistically. Based on my theoretical framework, I expected even small equity stakes from big brewers to provide them significant advantages over fully independent breweries—these could include greater access to distribution and retail channels, or even the ability to sabotage such access for close competitors. Therefore, I decided to place brands with any big brewer ownership stake in the category of having ties to big brewers, rather than the Brewers Association’s allowance of less than 25% equity. The analytic strategy included calculating the percentage of big brewer, private equity and craft beer ownership for all shelves, as well as for eye-level shelves. A stacked bar chart visualization was created to illustrate the big brewer and craft beer ownership percentages for each retailer. In addition, a treemap visualization of the shelf space allocated to big brewer brands across all retailers in the study was generated with RAWGraphs (app.rawgraphs.io).

The analytic strategy also included ordinary least squares regression analyses using the software PSPP (1.0.1,

https://www.gnu.org/). The dependent variables were the number of craft facings per retailer, and the percentage of craft beer with ownership ties to big brewers. The independent variables were the retailer characteristics of format and ownership, which were transformed into dummy variables. Grocery/supermarket format and local ownership were coded as the default categories, as these were expected to have the largest number of craft facings. Natural and convenience formats, and regional and national ownership were coded as the comparison categories.

3. Results

3.1. U.S. Beer Brand Ownership

Figure 3 illustrates the results of the analysis of ownership at the national level, as of October 2017. It shows that nearly all large, non-craft brewers (yellow) have made alliances with craft brewers (blue), either through an ownership stake or a distribution partnership. In addition, the two largest brewers (AB InBev and Molson Coors) both have five or more “crafty” (red) brands. Diageo (London, UK, and parent of Guinness and other import brands) is the only big brewer that has not yet allied with a craft brewer. Also notable is that at least a dozen craft brewers have been partially or fully acquired by private equity firms (green).

Among these brands, one of the few exceptions to obscuring ownership is Third Shift, which was introduced by Molson Coors nationally in 2013. The bottles are held in a craft-style uncoated cardboard carrier, with single-color printing. Although some initial packaging formats identified it as a product of “Band of Brewers”, and did not link it to the parent corporation [

43], eventually the smaller print on the front of the packaging stated, “crafted by Coors master brewers”. This brand was once highly visible in craft sections at a number of Lansing area retailers, and continues to be sold at retailers nationally, but was not found on any of the inventoried shelves in this study.

3.2. Case Study of Lansing, Michigan Retailers

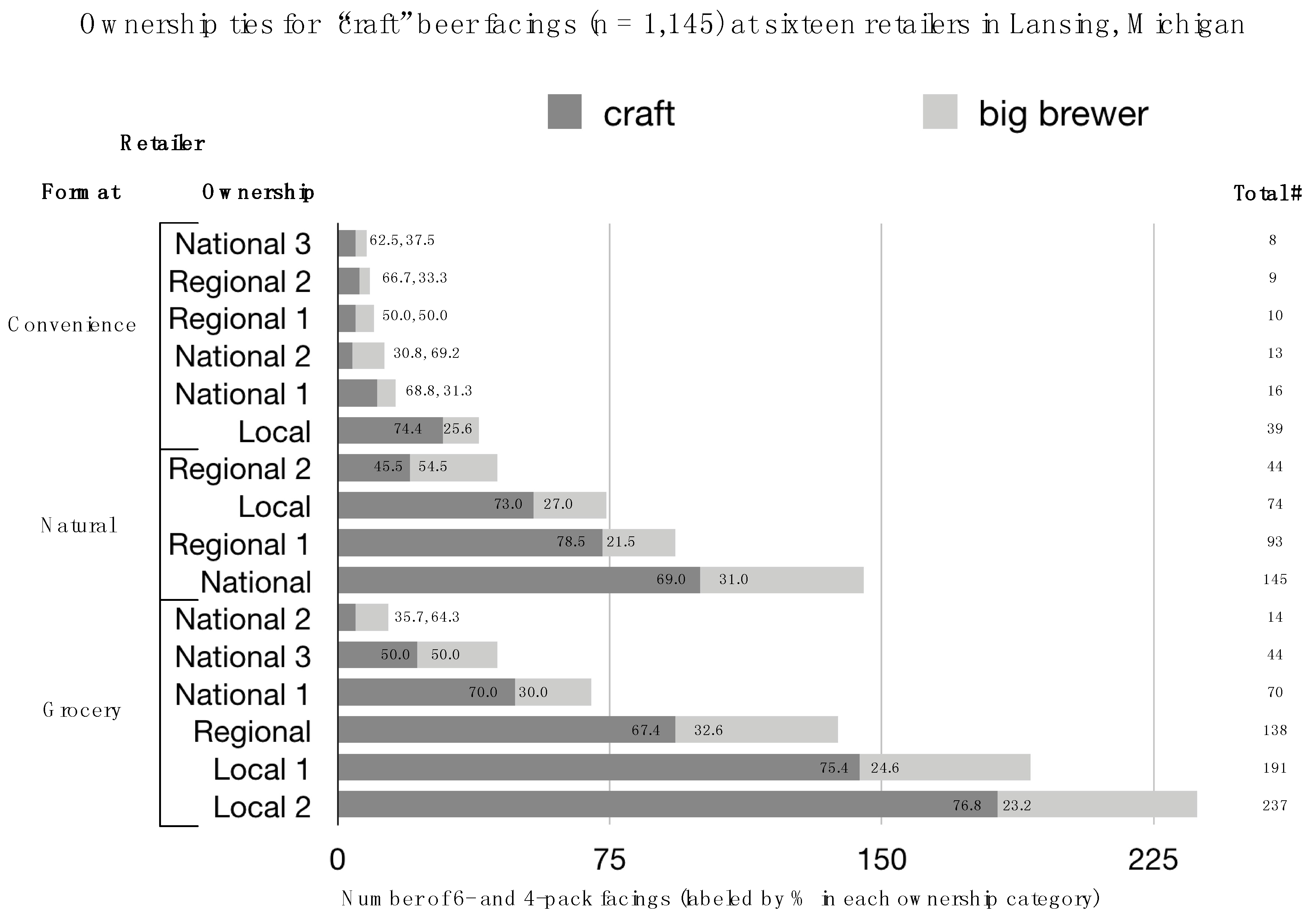

A total of 1145 facings, in a 4- and 6-pack format were recorded. For the sample as a whole, 64.1% were identified as having craft ownership, 5.9% had full or partial private equity ownership, and 30.0% were fully or partially owned by big brewers. A total of 275 of these facings were recorded at eye level, but analysis of this subsample indicated that the ownership percentages were quite similar—64.4% craft, 4.7% private equity ties, and 30.9% big brewer ties. Subsequent analyses therefore focused on all facings. In addition, due to the small percentages recorded, those with private equity ties were placed in the craft category.

If I had applied the more lenient Brewers Association definition of craft, 73 facings of Short’s (19.99% owned by Heineken) and 2 facings of Brooklyn (24.5% owned by Kirin) would have moved to the craft category, resulting in 70.7% craft, and 23.4% with larger stakes held by big brewers. The analysis does not include in the big brewer category those brands with distribution alliances, however. This would only have affected New Holland nationally, which has a distribution deal with Pabst, but this Michigan-based brewery accounted for 45 facings, or 3.9% of the study total.

Figure 4 shows the results for each retailer, organized as ascending from the smallest to largest number craft beer facings in each of the three retailer formats. As expected, these formats had strong differences in the number of craft facings, due to more limited shelf space at convenience stores, in comparison to natural food stores and mainstream grocers. Convenience stores offered 8 to 39 craft offerings, with the locally-owned store offering the most facings in this format. There was more variation in shelf space devoted to craft beer at natural and grocery formats: as low as 14 craft facings at one nationally-owned grocery retailer, and as high as 237 at one locally-owned grocery retailer. The average number of facings for all 16 retailers was 71.5.

The average number of craft facings with ownership ties to big brewers was 37.9% when calculated at the retailer level (i.e., not for the total number of facings in the study). Locally-owned retailers had percentages in a relatively narrow range, from 21.5% (natural) to 25.6% (convenience). Regionally and nationally-owned retailers all reported higher percentages, and their facings with big brewer ties ranged from 30.0% (grocery) to 69.2% (convenience).

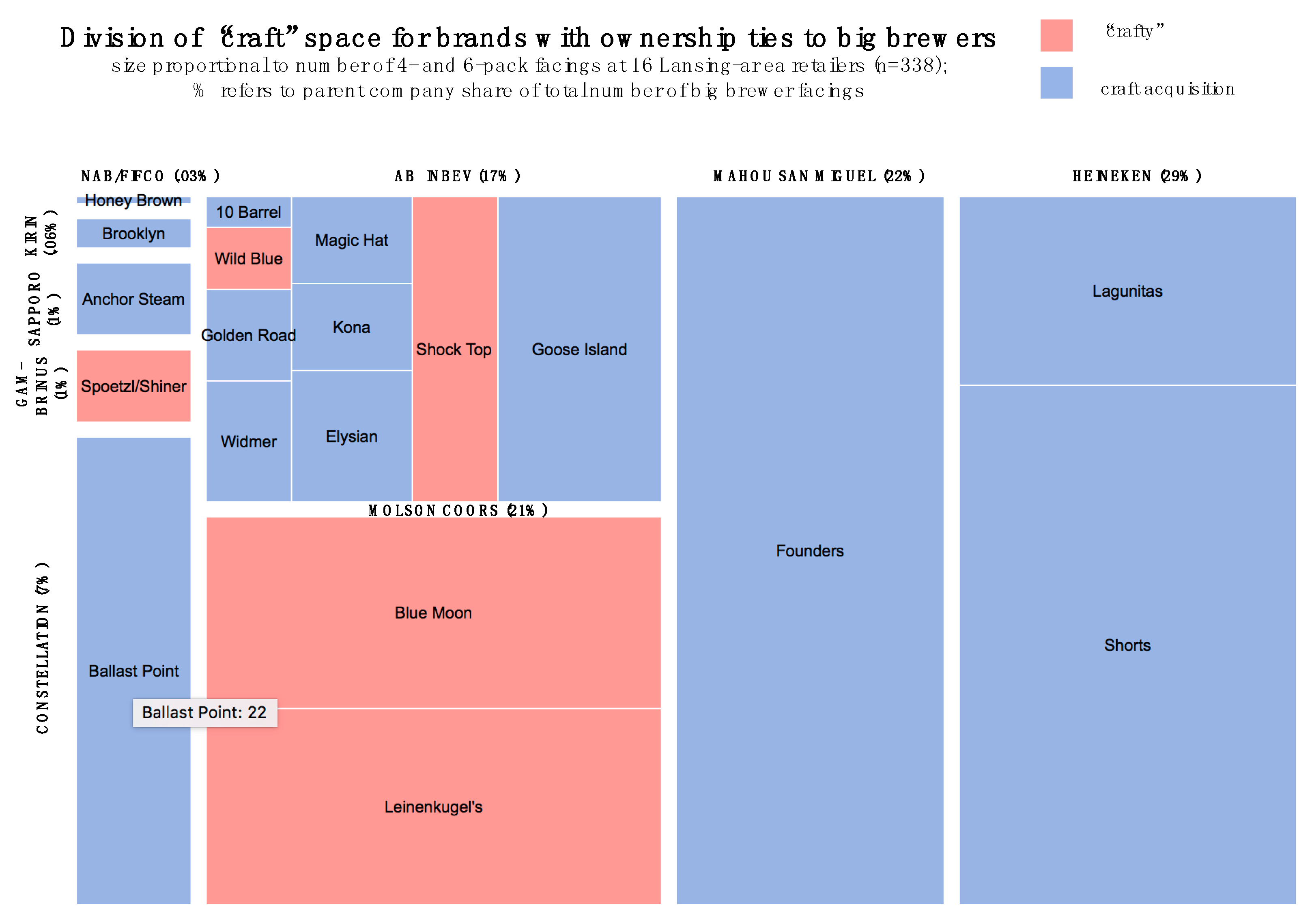

Figure 5 illustrates the facings with big brewer ownership ties by brand at all 16 retailers (338 facings). This treemap shows the breakdown of the 30% of study shelf space that was coded as “craftwashing”, divided by parent firm, and subdivided by their brands. The brands with the highest percentage of facings were Michigan-based breweries Founders and Shorts (approximately 22% each). However, Molson Coors’ “crafty” brands Blue Moon and Leinenkugel’s also take up a significant amount of space in the region’s craft beer sections (21%), although none of Molson Coors’ recently acquired brands were recorded in the study area. Conversely, AB InBev’s recent craft acquisitions took up substantially more shelf space than their “crafty” offerings (Shock Top, Wild Blue). Interestingly, another “crafty” brand owned by this firm Landshark, was previously found on area shelves, but not during this inventory period. Constellation has also been quite successful in placing a California-brewed acquisition on this area’s shelves (11%), after paying

$1 billion for Ballast Point’s craft brewing and distilling operations in November 2015.

Table 3 shows the results of the regression analyses. For Model 1 the dependent variable is the total number of craft facings. Not surprisingly, retailer format was associated with the number of craft facings, although the difference between grocers and convenience stores was much stronger than the difference between grocer and natural formats. The model predicts that compared to grocery retailers, a convenience store is expected to have 90 fewer craft facings, and a natural foods retailer 26 fewer craft facings, after controlling for ownership. The preliminary hypothesis that locally owned retailers would offer more craft beer selections also received some support from this model. It predicts a retailer with national ownership will have 78 fewer craft facings, and one with regional ownership will have 59 fewer craft facings in comparison to local ownership, after controlling for format.

For Model 2 the dependent variable is the percentage of craft facings with big brewer ownership ties. There were very weak differences between retailer formats and percentage of craft beer owned by big brewers, after controlling for ownership. Ownership, however, was associated with stronger differences. In comparison to local ownership, the model estimates 19% more craft facings from big brewers in a nationally-owned retailer, and 14% more in a regionally-owned retailer, after controlling for format. This provides some support for the preliminary hypothesis that locally owned retailers would offer fewer brands with ownership ties to big brewers, although this model explained much less variation (R2 = 0.06) in comparison to Model 1 (R2 = 0.48). Both models were very limited in the number of potentially confounding variables that were controlled, however, and the discussion below offers suggestions for what to include in models in future research.

4. Discussion

The results suggest that craftwashing in the U.S. beer industry is quite widespread, with only one big brewer (Diageo) so far resisting craft acquisitions. It is difficult for a typical consumer to identify ownership ties with big brewers, both for “crafty” brands and those with formerly independent craft heritage. The large numbers of acquisitions by private equity firms in recent years suggests that even more independent craft breweries will eventually be acquired by big brewers or other large corporations. As a result, those who want to support independent craft brewers must exert substantial effort to remain fully informed, and avoid unintentionally reinforcing these trends.

Locally-owned retailers in this study were more likely to have (1) larger craft sections; and (2) a lower percentage of brands with ties to big brewers, after controlling for retail format, which indicates some support for the preliminary hypotheses. Although the small sample size of the case study limits the power to make stronger generalizations, particularly outside Michigan, these hypotheses merit further research. This study was not able to disentangle if the low percentage of big brewer brands at locally-owned retailers was quite deliberate, or due primarily to offering larger selections. In other words, do these retailers offer a minimum number of brands with big brewer ties, and add an increasing number of independent brands with an expanded space dedicated to craft beer? Alternatively, do locally-owned retailers intentionally to seek to minimize the percentage of big brewer products they offer, regardless of the size of their craft beer shelf space?

Anecdotally, the answer to the last question is yes, at least for several craft beer-focused bars and packaged beer retailers that very publicly dropped Wicked Weed immediately after it was acquired by AB InBev [

45,

46]. This question has not been answered with more systematic research, however, such as through interviews and surveys of retail managers (particularly those that do not make use of category captains).

Future work could improve upon this study’s limited generalizability by expanding the sample size, and randomly sampling retailers, including a wider range of formats (e.g., liquor stores, bars, restaurants) and geographic locations. They could be further strengthened by including additional control variables at the retail-level, such as sales volumes for each brand, the size and composition of their entire beer shelf space (including domestic and import sections), and prices they charge relative to competing retailers. These studies could also potentially examine the demographics of regions surrounding retailers, or of the people who actually shop there, to explore additional hypotheses, such as fewer craft and independent craft offerings for less affluent customers.

Another suggestion for additional studies is to employ longitudinal designs, and analyze changes in craft offerings over time. In particular, these could explore the possibility that (1) the power of big brewers will enable them to further increase the amount of shelf space they take up in craft beer sections; and (2) they will replace declining space for “crafty” brands with their more recently acquired brands. An alternative potential outcome, however, is that the Brewers Association label raises awareness of independent craft brewery ownership, and reduces sales even for big brewers’ brands with craft heritage.

Craftwashing by big brewers has shifted from crafty introductions to acquiring brands with craft heritage. This change was influenced by the lack of effectiveness of their broader strategic sabotage strategies—the craft segment continues to grow, and at the expense of big brewers’ total sales. The situation is very dynamic, however, and the largest independent (or “mass craft”) breweries, such as Boston, Sierra Nevada, and New Belgium, have also experienced flat or declining sales in recent years. Much of the growth in the craft segment is now concentrated at the smaller-scale, such as neighborhood micro-breweries [

47]. This has coincided with the rise of consumer “neolocalism”, or loyalty to local place identities [

48]. A rapidly increasing number of craft brands are entering the U.S. market, but the amount of craft shelf space at retailers is remaining relatively static. As a result, retailers’ definitions of what is craft beer and what is not, will be a key factor in influencing how craftwashing strategies evolve in new directions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}