1. Introduction to the Research

The combined economic impact of those involved in the beer industry across the U.S.A., that is to say the brewers, distributors, retailers, supply-chain partners and other related industries, totaled more than

$252.6 billion in 2014 (the Beer Institute, 2015 [

1]). At the end of 2015, the industry included more than 4100 brewers, a record high for the U.S.A. (the Brewers Association [

2]). According to the Beer Institute (2015) [

1] there were also more than 7000 beer distributors across the nation; generating more than

$48.5 billion in tax revenue. The beer industry’s economic impact goes beyond the obvious sources, to include agriculture, manufacturing, construction and transportation, alongside many other businesses. The industry employs more than 1.75 million Americans, providing nearly

$79 billion in wages and benefits, generating nearly

$50 billion in business, personal and consumption taxes (The Beer Institute, 2015 [

1]). These figures are derived from the total impact of beer brewed by brewers as it moves through the three-tier system (breweries, wholesalers and retailers), as well as all non-beer products such as food and merchandise, that brewpub restaurants and brewery taprooms sell (Watson, 2015 [

3]).

In Charlotte the majority of breweries are small, independent and traditional in nature, representative of the scene across the U.S.A. which has seen a change to the beer market since the mid-1980s; a change which is having huge economic impacts across the nation. In 1985 the number of craft breweries across the U.S.A., exceeded the number of national breweries and the growth continued exponentially during the 1980s and 1990s (Elzinga et al., 2015 [

4]). The volume share for craft brewers in 2015 was 12.2%, rising more than 12.8% per annum (The Beer Institute, 2015 [

1]). In an otherwise stagnant beer market, craft beer represents the only domestic beer growth arena (the Brewers Association [

2]). American tastes in beer are changing. Consumers want increased choice in beer styles, moving away from American light lager which has dominated the market for generations.

The small, independent craft brewers which have sprung up in Charlotte in recent years are recognized for their innovative, characterful beers. During the course of the craft beer renaissance in Charlotte, breweries have expanded into numerous locations, meaning that today the average Charlottean lives within a few miles of a local brewer. Whilst this development has largely been driven by consumer demand, it has been enabled by the legislative changes which have taken place in the last twenty years. Legislation has been introduced to: raise the alcohol by volume (ABV) limits on Charlotte beer, allow Charlotte breweries to produce and sell their own beer on-site, and allow Charlotte brewers’ limited self-distribution (Malone and Lusk, 2016 [

5]). N.C. has arguably loosened its regulations by the most in the southern region, changes which according to Tim Kent, executive director of the North Carolina Beer and Wine Wholesalers Association (NCBWWA) have made N.C. the “undisputed leader in craft beer from Virginia to Texas”, (Kloppot, 2015 [

6]).

This research seeks to explore the recent development of the craft beer industry, using Charlotte as a prism for development elsewhere in America. The research is conceptual in nature. A conceptual approach has been taken for three reasons, firstly, it allows engagement with the research in order to introduce new concepts. Secondly, engagement with the research through conceptual frameworks enables people to see issues in a way they had not previously, and thirdly, findings from such research can help broaden our understandings about the kinds of solutions that should be considered and are most appropriate to pursue to enhance development of the craft brewing industry.

2. The History and Development of Charlotte Craft Beer

It is not the intent of this paper to discuss in full detail the history of brewing in N.C. or in Charlotte, this has been widely documented elsewhere (Hartis, 2013 [

7]). In order to assess the impact of the legislative framework on the craft beer industry in Charlotte however, it is necessary to document how the Charlotte beer scene we see today came into being. Charlotte has been home to licensed commercial brewing since at least the C18th, which had developed into a thriving trade by the C19th. As elsewhere within the United States however, brewing was disrupted in Charlotte as a result of Prohibition. By the time that N.C. enacted Prohibition in 1908, Charlotte had been dry for three years, having enacted Prohibition in 1905 (MediaHub, 2016 [

8]). When national Prohibition ended in 1933, States were given the option to stay dry; and in N.C. this courtesy was extended to the counties. As a result, Prohibition in Charlotte lasted for more than 42 years, being repealed in 1947. Post-Prohibition the national breweries prospered, with regional breweries less able to compete. In Charlotte, only the Atlantic Brewing Company prospered after Prohibition before closing in 1956. After 1956 no beer would be commercially brewed in Charlotte for more than 33 years.

The repeal of Prohibition made no provision for home-brewing, a situation amended in 1978 by President Carter. Charlotte, in common with many U.S. cities, developed a thriving home-brewing scene in the 1980s. In Charlotte a local convenience store fostered the early craft beer scene, leading to the creation of Carolina BrewMasters, one of the oldest and most successful home brew clubs in the nation.

In 1989 Charlotte became home to a commercial craft brewery once more, when Dilworth Brewing Company began operations. The brewery was hugely successful; winning gold at the Great American Beer Festival in 1992, and was visited by beer writer Michael Jackson in 1994. In 1998, however the brewery closed down, largely as a result of distribution issues. The brewery had been joined by the Mill Bakery, Eatery and Brewery in 1990 and Johnson Beer Company in 1995; with the latter becoming one of the biggest in the South-East by the late 1990s (Hartis, 2013 [

7]). All three closed swiftly, due to distribution and debt servicing issues.

Craft brewing across the USA grew rapidly during the 1980s and 1990s, and this growth was seen in Charlotte. A number of breweries opened during the mid-1990’s including Southend Brewery and Smokehouse, Lake Norman Brewing Company and Carolina Beer Company. Whilst successful in the short term, a decade later they had all closed. The other breweries which developed during this period were corporate chains. Hops, the largest brewpub company in the U.S.A., opened five locations in and around Charlotte, but their popularity declined rapidly during the 2000s. Rock Bottom Restaurant and Brewery opened in Uptown in 1997 and is still going strong almost twenty years later; albeit after the company has undergone a number of ownership changes. These closures were typical of the scene across the USA as the early growth slowed towards the end of the 1990s. At this time the craft sector saw a shakeout, with the number of craft breweries across the country falling by more than 10% (Elzinga et al., 2015 [

4]). The reason for the decline was the same as it had been for the craft brewers in Charlotte, distribution and product quality issues (Tremblay and Tremblay, 2011 [

9]).

The closure of Southend Brewery in 2007 saw the end of the first wave of craft brewing in Charlotte, leaving a gap for a locally owned craft brewery which was filled with the opening of Olde Mecklenburg Brewery (OMB) in 2009. OMB paved the way for a second wave of craft brewing in Charlotte; quickly growing to be the largest of the Charlotte breweries. The success of OMB encouraged other breweries; Four Friends Brewing opened in 2010 (closing in 2014) and NoDa Brewing Company (NoDa) and Birdsong Brewing opened in 2011. These three breweries laid the foundations for the massive explosion of craft beer and breweries seen across the Charlotte region, between 2009 and 2016, as evidenced by

Appendix A.

3. Brewpubs and ‘Pop the Cap’

Although beer could be brewed in Charlotte post-Prohibition, the state set into place the Alcohol Boards of Control (ABC) structure, giving local jurisdictions control over the production, distribution and sale of alcohol across N.C. County ABC Boards are local independent political subdivisions of the State Boards, operating as separate entities, establishing their own policies and procedures. They retain authority to set policy and adopt rules in conformity with ABC laws and N.C. ABC commission rules. Mecklenburg County (Charlotte) ABC Board operates solely on the revenue derived from distilled spirit sales, and distributes funds to law enforcement services, substance abuse initiatives, Mecklenburg County and the City of Charlotte and the Charlotte Public Library System.

Post-Prohibition, each state was allowed to deliver alcohol legislation as they saw fit and it was enacted in various ways by states across the nation. In N.C. the state, through the ABC, enacted two pieces of legislation that impacted the beer industry across Charlotte. Firstly, it enacted legislation which made brewing beer and selling it on the same premises illegal; brewpubs could not legally exist. Secondly, a law was introduced which set a cap on the amount of alcohol in beer brewed and/or sold within the state, at 6% ABV (Myers, 2012 [

10]).

The first of these laws was successfully challenged and amended in 1986, following a lobbying campaign headed by a German immigrant who wanted to open a microbrewery (Weeping Radish Farm Brewery,

http://www.weepingradish.com). Further brewpubs also opened, albeit without success until in 1991, the Red Oak brewpub began operating, eventually becoming one of the most successful breweries in N.C. (Redoakbrewery.com). Many of these early craft breweries were unsuccessful in acquiring access to distribution networks, as under the ABC structure they were dominated by the large national brewers. As a result, they chose to operate as brewpubs, in order to both sell their beer on site and befit from the retail markups that would otherwise go to the distributors (Leland, 1988 [

11]).

The second post-Prohibition legacy, the 6% ABV cap, came under challenge in 2003 due to a group of beer enthusiasts lobbying for change, under the title ‘Pop the Cap’ (popthecap.org). The group grew a grassroots movement which at its height comprised thousands of North Carolinians. They hired a lobbyist, and finally overcame the resistance of distributors, neo-Prohibitionist interest groups, and politicians [

12]. Despite significant opposition, the bill was enacted into law in late 2005, raising the cap on beer to 15% ABV.

Pop the Cap was significant, not simply because it allowed the sale of higher ABV beers but because many believed N.C. lagged behind other states in developing a craft beer industry, because the ABV cap limited the styles with which creative brewers could experiment (Purvis, 2015 [

13]).

5. Beer Distribution and Retailing

The current pattern of beer distribution in Charlotte, as elsewhere in the U.S., has its roots in the Prohibition movement, which began in the late C19th. The first N.C. statewide Prohibition bill was introduced as early as 1881, and in 1909 N.C. enacted Prohibition, which lasted until 1937. In order to repeal Prohibition, Congress had to accept that states wishing to remain dry could do so, and allow them to enact local alcohol legislation of their choosing, short of total Prohibition. When it was repealed, N.C. along with most other states, introduced the three-tier system of distribution. Before Prohibition, brewers often had ownership ties to the taverns, the tied-house system, leading to tremendous pressure being exerted on retailers to maximize sales without regard to the well-being of customers or the general public. Under the tied-house system suppliers often owned retailers and required them to only sell the products of the supplier. The tied house system arguably led to overly aggressive marketing, in turn leading to intemperance, destabilizing of the market, criminal conduct and general moral decline (CSA, 2017 [

19]). The introduction of the three-tier system eliminated tied-house abuses. The three-tier system had positive intentions as it was introduced to avoid a return to the way alcohol was retailed before Prohibition. Within the N.C. three-tier system a company wishing to sell its products in N.C. must sell only to wholesalers, who in turn may sell only to retailers [

20]. The three tier system led to distributors having a monopoly in the distribution system, a position they have sought to protect ever since. In N.C., the three-tier system also prohibits any tier having a financial stake in another.

Post-Prohibition, across the U.S. states encouraged the development of beer wholesale associations, eventually leading to National Beer Wholesalers Associations (NBWA, nbwa.org [

21]). In N.C. the North Carolina Beer and Wine Wholesalers Association (NCBWWA,

www.ncbwwa.org [

22]) was founded in 1936 as a non-profit trade association to promote and protect the general business interests of beer and wine distributors in North Carolina. This organization’s members in effect control the distribution of beer throughout Charlotte. Since Mecklenburg County repealed Prohibition, the wholesalers have resisted any changes to the three-tier system, citing the promotion of consumer choice, value, temperance and the ensuring of a safe and orderly marketplace as reasons to maintain the status quo.

It is arguable whether these are truly the reasons for their views, which reflect the argument of their national body, the NBWA, and that perhaps a more economic rationale is in place. Across the U.S.A., the three-tier system guarantees wholesalers a significant percentage of the beer market and thus there is a clear economic incentive in preventing breweries circumventing the current system (Tamayo, 2010 [

23]). Gohmann (2016) [

24] argues that nationally, the wholesale distributors and national beer producers have an economic interest in limiting competition. In every state the new breweries are microbreweries and brewpubs, competing for shelf-space that distributors want to maintain for national accounts. Limiting the number of breweries in a state limits competition and increases the potential for greater profits.

Whilst in general the three-tier system is somewhat the same across the states, there are differences in the legislation concerning self-distribution of beer and the application of beer franchise laws. Many states allow for an element of self-distribution of beer, effectively permitting breweries to act as wholesalers of their own products. In N.C., since 2003 brewers are permitted to self-distribute no more than 25,000 barrels each year. When the breweries reach 25,000 barrels, however, they are required to contract distribution of all of their product to a wholesaler. The legislation applies to all of the beer produced, not simply that above the 25,000-barrel limit. This would be administered under the Beer Franchise laws. Both NoDa Brewing Company and OMB will be in a position to exceed 25,000 barrels by 2017 (Markovitch, 2016 [

25]).

5.1. Beer Franchise Laws and the Charlotte Craft Brewer

For many Charlotte brewers the issue with the franchise laws varies from the basic problem of limited access to the marketplace, to being contracted to a distributor that has little interest in, or knowledge of how to handle, specialty brands (Criston, 2014 [

26]). The franchise laws were developed in the 1970s and 1980s and reflect the market conditions of that time. Market power was consolidated in a decreasing number of breweries and a growing number of distributors. In many states, including N.C., these huge brands had significant bargaining advantages over small, family-owned, distributors. Consolidation meant breweries had more economic power and greater choice of distributors, which allowed them to influence the franchise negotiations and bargain for better terms. The intention behind beer franchise laws was to correct the imbalance between the breweries and distributors by creating statutorily mandated protections for distributors (Anhalt, 2016 [

27]).

In the contemporary U.S. marketplace however, the question has to be addressed, who do the franchise laws benefit? The wholesalers argue franchise laws are in place to limit the impact of the national brewers, who without such legislation would limit market access to craft breweries [

21]. As the NBWA website argues “franchise laws prohibit vertical integration of the brewing, distribution and retail tiers, preventing monopolies” [

21]. The evidence for such an argument however, is limited. A number of states, such as California, allow self-distribution, have no or weak franchise laws, and yet report some of the highest number of the breweries in the United States (the Brewers Association [

2]).

In N.C., a franchise agreement includes the right to offer and sell beer, but also extends into matters such as the use of trade names, trademarks, service marks or related symbols of the brewery; in other words, the wholesaler assumes full control of the brand. In addition, it is difficult for breweries to recover their distribution rights, as “N.C. law is favorable to the distributor and helps to protect distributor rights in a number of ways” (NC Beer Lawyer, 2014 [

28]). In order to terminate a franchise agreement, the brewery must show “the wholesaler fails to comply with provisions of the agreement which are reasonable, material, not unconscionable, and which are not discriminatory” (Whitman, 2003 [

29]). In reality, depending on the terms of the brewers’ contract with the distributor, this means a franchise agreement cannot be ended by the brewer and has no time limit.

This is what breweries such as OMB and NoDa Brewing Company are against. They believe that they are better able to ensure the quality of their products and to safeguard their brands if they are able to self-distribute their products without limits. As argued by John Marrino the owner of OMB “Craft freedom is critical to our business model,” and Todd Ford, owner of NoDa Brewing Company, “We can’t make business decisions,” (Purvis, 2015 [

13]). Many Charlotte brewers believe, what brewers across the U.S. believe, “These (franchise) laws reflected the market conditions at the time of their enactment. Subsequent to states enacting these protections, the dynamic of the beer industry changed, but the regulations remained the same.” (Anhalt, 2016 [

27])

The beer franchise laws impacting on Charlotte are representative of the situation across much of the U.S.A. While the distribution relationship is not a traditional franchise model, beer franchise laws regulate the brewer-wholesaler relationship, much like state laws govern more traditional franchises (Kurtz and Clements, 2014 [

30]). Beer franchise laws restrict under what conditions a brewer can terminate a contract with a wholesaler (NCleg, 2015 [

31]). In all but five states where this legislation has been enacted, beer franchise law requires the brewer to demonstrate ‘good cause’, as defined in the law, before a contract can be terminated. In most states, however, even when good cause is demonstrated, wholesalers are protected. Brewers are often required to give a period of grace in order to allow wholesalers to address the issues before termination can be enacted. Further restrictions granted under this legislation also allow wholesalers exclusive territories, ensuring no competing wholesaler can sell contracted brands to retailers. State approval of distributors is required for almost half of the states across the U.S., including N.C. Most states have some form of beer franchise laws, making it difficult for brewers to change wholesalers.

5.2. Changes to the 25000-Barrel Limit

Across the U.S., breweries have begun to put pressure on distribution legislation. In N.C. in 2015, two bills were introduced; the first aimed to increase the limit from 25,000 to 100,000 barrels, the second sought to clarify that beer sold at the brewery was not included in the limits. Neither bills were successful (McGrady, 2015 [

32]). The N.C. breweries do not intend to allow the current system to go unchallenged, however. Following the pattern established during ‘pop the cap’, a lobbying organization has been initiated known as Craftfreedom.org, with the intent of gaining public support for changes to the current legislation [

33]. At the end of 2016, this grassroots coalition encompassed more than 60 members, including most of the craft breweries in Charlotte, some of which are credited with initiating the campaign [

34].

Moderate voices argue that the relationship between distributors and brewers can be harmonious. The Executive Director of the N.C. Craft Brewers Guild is quoted as arguing that within Charlotte and across N.C. “Craft brewers have successful relationships with distributors … that’s been the case for 20 plus years. We commend them … in helping craft beer grow in N.C.” (Metzger, quoted in Daniel, 2015 [

35]). A similar moderate position is taken on the distributor side by the CEO of Caffey Distributing who, when asked if more progressive beer distribution laws could lead to growth responded, “some of my distributor peers would cringe at me saying this, but raising the cap? There’s not a strong argument against it as long as you maintain some of the integrity and ensure it maintains a competitive market” (Caffey, quoted in Daniel, 2015 [

35]).

Despite a few moderate voices, however, it is clear that going forward the two opposing sides of the self-distribution argument will become increasingly polarized. As Gohmann (2016) [

24] argues, “Distributors are small groups in terms of voting power. Their influence depends on their ability to persuade politicians to pass or maintain laws that make it more difficult for new breweries” (p. 1081). At both a national and state level the NBWA and the NCBWWA are well-funded and politically connected organizations. A recent report into the NCBWWA by the N.C. Centre for Public Policy Research identified four of its lobbyists as amongst the most influential in the state. Harold Brubaker (ranked #1), Tom Fetzer (#3), Lori Ann Harris (#11) and Tim Kent (#27) all represent the association’s interests before the N.C. General Assembly. The biographies of these individuals demonstrates the political power the NCBWWA has in its corner. Mr. Brubaker, identified as the most powerful lobbyist in N.C., is a Republican politician who served in the North Carolina General Assembly for 35 years. Brubaker was Speaker of the House for two terms (1995–1998), and in 2011 became chairman of the House Appropriations Committee. Tom Fetzer, another Republican, served three two-year terms as Mayor of Raleigh, North Carolina. He was elected the chairman of the North Carolina Republican Party in 2009, serving until 2011. The NCBWWA’s connections to the political process in N.C. are constantly reinforced, and results in “the association (being) consistently recognized as one of the state’s most influential associations with a long record of advocacy effectiveness at the N.C. General Assembly” [

36]. Across the country distributors will do what they can to ensure that the environment remains difficult for craft brewers. This includes providing campaign contributions to those lobbyists and politicians who share their perspective on the three-tier system and beer franchise laws (Gohmann, 2016 [

24]).

7. Taxation Applied to the Craft Beer Sector

Excise taxes, which are often thought of as a form of luxury tax, are paid when people purchase beer and are included in the price of the product. The federal tax code defines craft beer by the size of the production unit. Prior to 1978, the federal excise tax on beer was

$9.00 per barrel. In 1978, growth in the craft brewing sector was encouraged through federal tax credits offered to brewers which produce less than 2 million barrels, cutting their excise tax rate to

$7 per barrel on the first 60,000 barrels and allowing them a far lower overall effective tax rate on all barrels up to 2 million. This was a windfall for craft brewers. Federal excise taxes are currently set at a rate of

$18 per barrel for brewers of more than 2 million barrels and all beer importers. Despite these provisions, the craft brewing industry claims the existing tax burden is slowing its ability to grow. On average, more than 40 percent of what American beer drinkers pay for a beer goes toward federal, state and local taxes; from excise to consumption to sales to everyday business taxes. This makes taxes the most expensive ingredient in beer (Purdy, 2016 [

44]).

A number of bodies are seeking to amend the federal tax rates for breweries. The Craft Beverage Modernization and Tax Reform Act went before congress in 2016, supported by the house Small Brewers Caucus. This bill which has broad support from both political parties would cut excise tax to

$3.50 for the first 60,000 barrels,

$16 for every barrel past 60,000 up to 2 million, and

$18 for all barrels above 2 million. Any brewery that produces fewer than 6 million barrels of beer each year would be eligible for these rates. This bill is opposed by the distributors, who are seeking approval for alternative legislation, the Fair Beer act, which would provide tax relief for all brewers. Amongst other changes the Fair Beer act would reduce the federal excise tax to

$16 per barrel on the first 6 million barrels for all brewers and importers (Summers, 2015 [

45]). It is unclear whether either bill will be successful, outside of its inclusion in a wider tax restructuring.

In addition to federal excise tax, which is applied to all states in the same way, state excise tax is also imposed, however the rates vary widely by state. N.C., in line with many of the southern states, imposes a high rate of excise at the state level (Kazsuk, 2015 [

46]). Currently N.C. imposes a state tax rate of

$19.13 per barrel (

$0.6171 per gallon) on all beer sold. High excise taxes at the state level, when added to federal excise taxes, impact the breweries profits. If Charlotte brewers paid lower taxes, they could buy more equipment and do more marketing, creating sales that would come back to the state as sales taxes (Purvis, 2015 [

13]). In Charlotte a craft brewer is paying more than

$26 a barrel in taxes, while their compatriots in Wyoming, for example, pay a little over

$7.

8. Charlotte as a Case Study for Craft-Brewing in America

We can look at the city of Charlotte, along with the state of North Carolina, as representative of a change to the beer market in the U.S.A., which has been seen since the mid-1980s; a change which is having huge economic impacts across the nation. In Charlotte today, as in the whole of America, the majority of breweries are small, independent and traditional in nature. The volume share for craft brewers in the U.S.A. in 2015 was 12.2%, rising more than 12.8% per annum. This demonstrates a stark contrast to an otherwise stagnant U.S. beer market, where craft beer represents the only domestic beer growth arena (the Brewers Association [

2]). The growth in the craft beer market has taken place against a backdrop of decling beer sales across the U.S.A., both in volume and dollar amounts. The 2015 growth in craft beer sales was especially notable, as the total U.S. beer market reported a slight drop of 0.2% in volume during the same period. The spirits and wine industries have taken market share from beer in the total alcohol beverage category, resulting in stagnant sales for the overall beer category in recent years. Only beer imports are having a similar impact on American beer consumption. In 2015, craft brewers produced almost 25 million barrels of beer and saw a 16% rise in retail dollar value. Retail dollar value in 2015 was estimated at almost

$23 billion, which, for the first time ever, represented a more than 2% market share.

Additionally, at the beginning of 2015 the number of breweries operating in the U.S.A was growing by more than 15%, totaling a little over 4,100 breweries, which represents the highest number of breweries seen at any time in American history. The number of breweries in the U.S.A. in 2016 has finally outstripped the number pre-Prohibition. These breweries are almost all small, independent breweries, with the majority being microbreweries or brewpubs. In 2015 alone there were more than 600 new brewery openings, versus some sixty closings, a figure which shows a slight growth in closings against previous years. The growth seen in 2015 is in line with growth seen in the craft beer sector for many years now. Market share stood at only 5.7% in 2011; in 2015 that figure had more than doubled in just four years (the Brewers Association [

2]).

The South represents one of the fastest growing regions in the country, with states such as Virginia, North Carolina, Florida and Texas seeing net increases in the number of operating breweries with almost 100 new breweries between them. This growth establishes a strong base for future growth in the region.

For more than a decade craft brewers have expanded across the U.S. beer market, seeing double digit growth for eight of the last ten years (the Brewers Association [

2]). There is little sign that this growth is slowing, however there are some concerns nationally that the current exponential growth experienced by craft beer cannot continue indefinitely. A number of commentators have begun to argue that the market is saturated and heading for decline (Buckley, 2016 [

47]). Typical of these comments are those by Bucolo, “consumers are overwhelmed; the industry has been swamped. There’s too many brands, too many styles, not enough quality” (quoted in Buckley, 2016 [

47]); and Malandrakis quoted in the FT “we’re reaching peak craft in the U.S. … growth cannot be sustained forever” (Daneshkhu and Whipp, 2016 [

48]). Reports of stalwart craft brewers such as Stone Brewing and the Craft Brew Alliance, laying workers off has many people commenting (Buckley, 2016 [

47]). These concerns came to a head with a recent report which suggested that craft beer growth declined to 8% in early 2016 (Gribbens, 2016 [

49]). Whilst such figures are somewhat lower than have previously been achieved, they still represent significant growth in the market. In addition, it is argued by many that the figures are biased by the growth achieved by the largest of the craft brewers, brewers such as Sam Adams, Widmar Brothers and Deschutes. The combined volumes for the top twelve craft brewers grew only 1%–2% in early 2016. The slowdown in the craft beer market appears to be coming from the biggest craft brands (Gribbens, 2016 [

49]).

Most analysts believe there are still significant opportunities and areas for additional growth in the future (Morris, 2015 [

16]). American tastes in beer are changing, with consumers wanting increased choice in beer styles. The growth in the craft beer market across the U.S.A. has arisen because increasingly knowledgeable consumers are demanding an increasing variety of beer styles that craft brewers have popularized, including IPAs, session IPAs, pilsners and sour beers (Kell, 2016 [

50]). An important focus for these consumers will continue to be quality, as small and independent brewers continue to lead a movement for local, full-flavored beers. As Todd Ford of NoDa Brewing in Charlotte stated, “I think what is much more important than what the actual number of breweries is, is how many breweries are bringing something unique. If they focus on something that's unique I think that means our market's not mature yet” (quoted in, Wells, 2015 [

51], p. 1).

The U.S. beer industry is highly concentrated, particularly with regard to volume and dollar sales, a position caused by the mass consolidations which have taken place in recent years. The overwhelming percentage of the industry’s revenue is generated by only eight brewers (SBDCNet, 2012 [

52]). The number of national breweries declined during the period after 1950 due to marketing wars, technological improvements and the homogeneity of the product (Elzinga, et al., 2015 [

4], Tremblay and Tremblay, 2011 [

9]). The industry has been so consolidated that Porter (1980) [

53] used it as an example to demonstrate barriers to market entry, stating “in the brewing industry, product differentiation is coupled with economies of scale in production, marketing and distribution to create high barriers” (p. 9).

Beginning around 1980, however, the long decline in the number of breweries slowed and then was reversed. Based solely on the number of breweries across the U.S., it appeared that a significant change had occurred. During the 1980s the number of breweries began to increase, and by the late 1990s, hundreds of new breweries were operating in the U.S. In terms of a concentrated industry, however, the numbers are somewhat misleading. The overall industry has remained concentrated, with a very small number of brewers dominating the market, both in volume and dollar terms. (Beverage Industry, 2013 [

54]). There is an appearance of great diversity in the number of brands and varieties of beer sold in the United States. The beer industry, however, is dominated by a relatively small number of firms (Howard and Ogilvie, 2011 [

55]). As Hannaford (2007) [

56] argues, “The beer industry is not only dominated by two firms, it is dominated by a small number of varieties―just six account for more than half of all sales. The result is an ‘oligopoly within the oligopoly’” (p. 122).

Carroll and Swaminathan (2000) [

57] argue that the consolidation of the U.S. beer industry during the 1970s and 1980s left a peripheral product space, allowing for craft brewers to grow. They argue that as the national brewers produce identical American light lagers, this leaves a niche market for creative craft brewers producing more distinctive products. By comparison to the generally consolidated beer market, the craft beer competitive environment is primarily comprised of very small brewers who mostly compete on a local or regional basis. In craft beer, the top three brewers in 2016 were Boston Beer Company, Sierra Nevada Brewing Company and New Belgium Brewing Company; with the remaining market massively fragmented. One of the main reasons for the huge growth that has been seen in national craft beer markets is possibly that the barriers to entry into craft brewing, at the very small brewer level, are relatively low (Porter, 1980 [

53]). As long as breweries have entrepreneurs with a passion for brewing and a local customer base with semi-regional markets, they can succeed. As has been seen in Charlotte, however, the barriers significantly increase when craft brewers attempt to expand either in production volume or distribution. The competition among craft brewers occurs primarily in their method of distribution. The costs and barriers associated with expanding their distribution can prohibit outright expansion without secondary funding. As has been demonstrated for Charlotte, and is being experienced by craft brewers to a greater or lesser degree across the U.S.A., it’s exceptionally difficult for craft brewers to expand beyond local distribution simply through organic growth.

Distribution arrangements, in particular the Beer Franchise Laws which are prevalent in most states, undermine brewer autonomy as they force brewers across the U.S.A. to turn over their brands to independent companies for distribution to retailers. A small number of states, including; Arizona, Arkansas, Colorado, Louisiana, Massachusetts and North Carolina, have passed exceptions to these laws for small brewers that produce below a yearly limit. These limits are often low, for example the limit is under 6,000 barrels in Louisiana, creating a disincentive to growth (Burgdorf, 2016 [

58]). Craft brewers that have the potential to outgrow the small-brewer exception, but do not want to be forced to work with wholesalers, might intentionally avoid expanding their operations beyond the distribution limit.

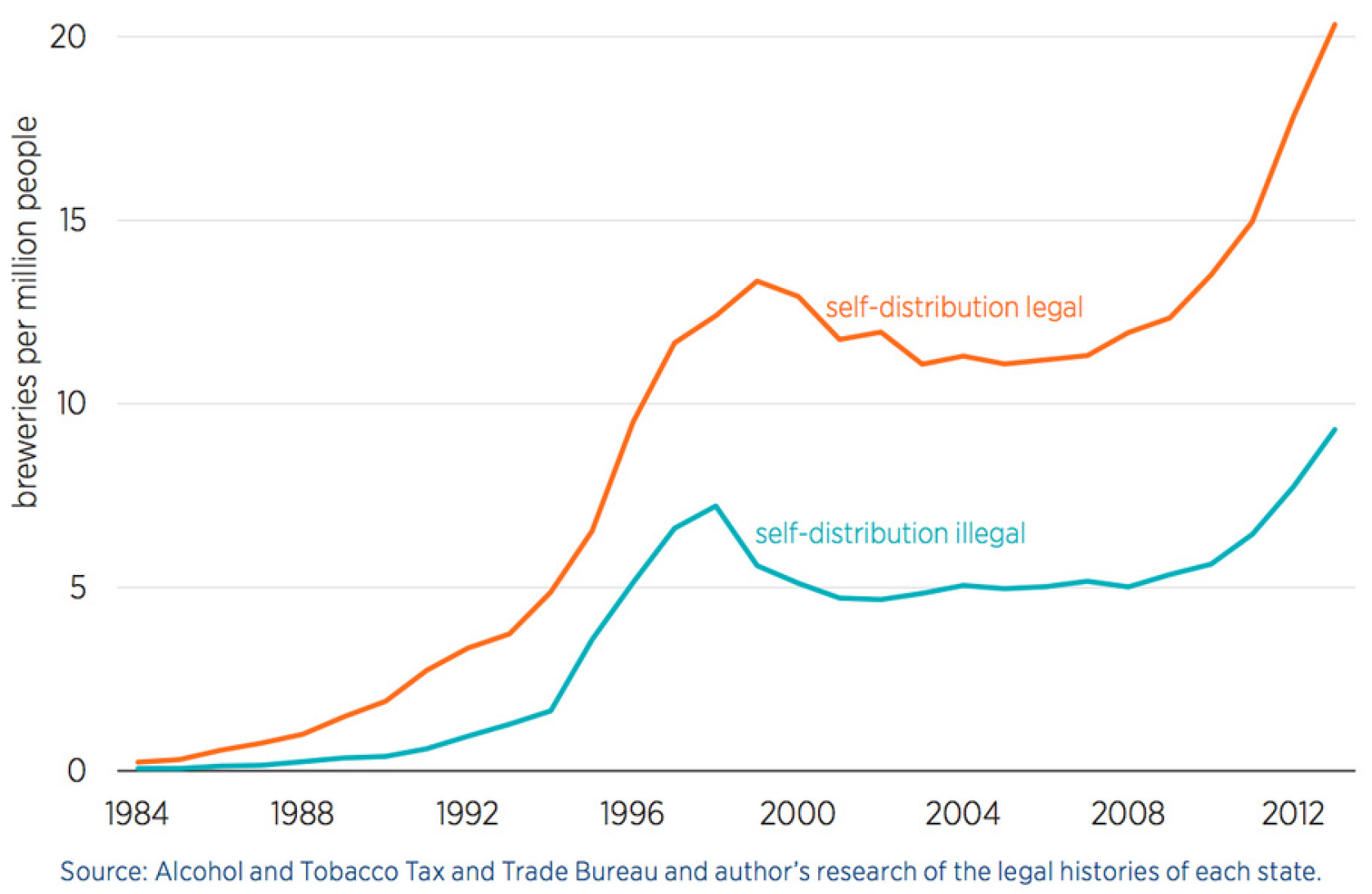

Research suggest that where states, such as North Carolina, restrict distribution it leads to fewer breweries being developed.

Figure A1 in

Appendix B, compares the number of breweries in states allowing self-distribution against those that do not. The research demonstrates that states allowing self-distribution on average had more than double the number of breweries than those that did not when adjusted for populations (Burgdorf, 2016 [

58]). These findings are supported by Gohmann, who argues that “states that allow self-distribution have 49% more breweries” (2016 [

24], p. 1080). It has been argued that somewhere between 60% to 75% of this difference is due to state legislation of self-distribution (Burgdorf, 2015 [

59]). The research also suggested that craft beer production was more than 150% higher in states which did not restrict self-distribution. Burgdorf (2016) [

58] also argues that in addition to restricting growth for existing breweries, beer franchise laws limit the potential for new breweries to enter a market.

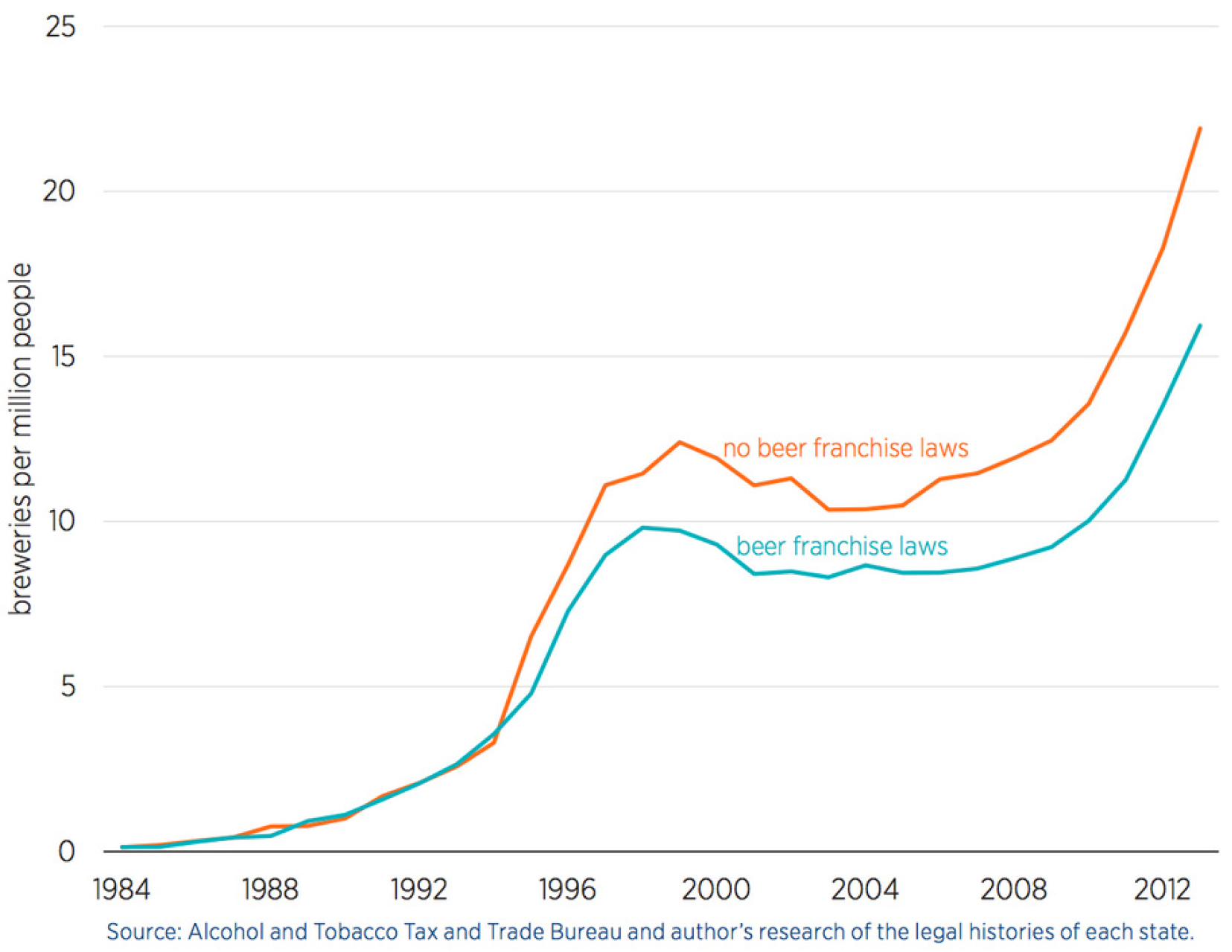

Figure A2 in

Appendix B demonstrates that in 2013, states without beer franchise laws averaged more than 20 breweries per million people, higher than the 15 breweries, achieved by states which have enacted franchise laws. Burgdorf argues that his research shows, the implementation of beer franchise laws affects a significant reduction in market entry and production of craft brewers.

State excise taxes also have to be taken into consideration when considering Charlotte as an exemplar of the craft beer industry nationally. State excise duty on beer varies widely, as does its application. Many states, such as Montana and Wisconsin, vary the rate based on volume, benefitting small brewers. Other states, such as Idaho, vary rates based on the ABV of the beer. Others, such as Georgia, by the way beer is packaged, differentiating between draft beer and bottled. As has been discussed, N.C. is one of a cluster of southern states that imposes high rates of excise duty on craft beer. N.C. applies its

$19.13 per barrel excise tax on all beer sold in the state, a level which places it in the top ten highest taxed beer states in the U.S. (Kazsuk, 2015 [

46]). The politics surrounding beer taxes and regulations at the state level are complicated. As Lester Jones (2015), chief economist at the Beer Institute, argues “it’s almost like selling beer in the United States is like selling it in 50 different countries” (quoted in Costa, 2015) [

60]. According to the Tax Foundation, state and local governments can also include volume taxes, wholesale taxes at a percentage of a product’s wholesale price, distributor taxes, and case or bottle fees, based on the size of the container (Costa, 2015 [

60]). In 2016, state excise duty varies from a low of

$0.58 per barrel in Wyoming, to a high of

$38.98 in Tennessee (the Brewers Association [

2]). The majority of states have excise rates in single digit dollar figures. States such as N.C., with their high levels of state excise duty, significantly impact the craft beer industry, where margins can be tight (Purdy, 2016 [

44]). Charlotte faces one of the highest state excise taxes on beer. In recent years, both Stone Brewing and New Belgium Brewing expanded by opening East coast facilities. Stone’s home state of California has an excise rate of

$6.2 per barrel, while Colorado, home of New Belgium Brewing, charges just

$2.48 per barrel. At the end of the day, Stone selected Virginia, with its excise rate of

$7.96, to build its expansion, while New Belgium opted for N.C. (Self, 2014 [

61]). Craft brewers argue that current excise rates at both national and state level are hampering growth. If N.C. excise taxes were at the level Stone pays in either California or Virginia, breweries could create more local jobs, and buy more equipment to meet demand. If all states applied excise duty in the same way, breweries would have the opportunity to grow across the board.

9. Conclusions

As can be seen, Charlotte has a long brewing tradition, one that is largely representative of the wider beer scene in America. Legislation has, and continues to, significantly impact the shape, size and structure of the craft beer industry. Despite this impact, however, it is clear that across the country; cities, counties and towns are battling to show they are the most craft-friendly, by passing new pro-craft brewing regulations (Crowell, 2013 [

39]).

Distribution laws continue to have significant impact, polarizing the industry. Many brewers argue raising the distribution cap is essential to their survival, whilst the distributors are adamant that the present system works to the benefit of competition, society and the consumer (McKenzie, 2015 [

62]. The imposition of a third tier between the brewer and the customer is hard to argue from an economic perspective. The wholesalers have to be paid which when combined with the taxes levied at both ends of the transaction, leads to increased costs for the consumer. The NBWA express the value of the current system as ensuring a safe, orderly marketplace. In N.C. the NCBWWA focusses on promoting their role in the responsible, legal consumption of alcohol, through the operation of a state-based regulatory system. Whilst there is some truth to these arguments, research demonstrates that the role of distributors as guardians of morality is over-played (Tamayo, 2010 [

23]). As Peck (2009) [

63] argues “The judiciary’s critical view of the three-tier system bolsters the General Assembly’s need to consider whether their laws truly promote temperance and reduce social costs, rather than regulating the alcohol industry on the basis of outdated social mores that viewed alcohol as an inherent evil” (p. 11). The current distribution system hampers the freedom necessary to grow the craft beer industry in Charlotte. The law hinders the brewers in a highly competitive market in which it is hard to stand out when you are one of hundreds of brands handled by a wholesaler (Pulscher, 2016 [

64]). To grow, change has to be made to self-distribution legislation (Anhalt, 2016 [

27]). It has been demonstrated that states which allow self-distribution and do not enact beer franchise laws consistently have more breweries, creating more choices for consumers (Burgdorf, 2016 [

58]).

Excise duties also have to be considered. Across the nation, craft brewers claim the existing federal and state tax burden is slowing their ability to grow. When more than 40% of the cost of a beer comprises some form of tax, this impacts on consumers. As has been discussed, taxes are the most expensive ingredient in beer, regardless of which state you are in (Purdy, 2016 [

44]). The problem is that, as with distribution rights and franchise laws, no consensus exists with regard to beer taxes. One group is advocating for federal excise tax relief only for small craft brewers, whilst another, for companies that in some cases are not making any beer in the United States. Clearly the current playing field is not level (Summers, 2015 [

45]).

The future will see a continuation of this conflict played out across the U.S. with both sides taking fixed positions. The wholesalers will seek to maintain the status-quo, through the judicious use of powerful lobbyists at the state level, paid through the huge profits generated by the three-tier system. They will be opposed by grass-roots organizations such as craft freedom. Previous changes to legislation in the craft beer industry have come about as a result of pressure from consumers. The growth of the U.S. craft beer industry is a valuable asset, one that the N.C. General Assembly has explicitly recognized as worth promoting and protecting (Tamayo, 2010 [

23]). The current campaigns which are taking place across the U.S.A., including those in N.C., continue this tradition as they seek to overturn legislation, much of which was put in place to manipulate the beer market post-Prohibition. It is a worthy discussion to have as to its continued relevance some 70 years later, and one which offers considerable scope for future research.

A cautionary factor which has to be taken into consideration, however, is the degree to which the current rapid growth seen in the craft beer market can be sustained, particularly under current distribution legislation. As Michael Brawley (quoted in Wells, 2015 [

51]) argues "I think we met the critical mass margin (for craft beer) a long time ago … you’re looking at market saturation … we are steadily approaching a time where the sheer number (of products) is going to make business difficult for everyone” (p. 1). Brawley argues that a crucial impediment to infinite brewery growth is distribution and retailing, citing the finite number of draft lines at bars and shelves at retailers. Competition for this space will increase as more breweries enter the market. The practice of tap rotation, the retailer’s preferred method in dealing with choice, provides little stability for beer producers. The degree to which current patterns of growth can continue under the current legislative frameworks offers a second potential arena for future research.

{kind=link}

{kind=link}