A Model for Demand Planning in Supply Chains with Congestion Effects

Abstract

1. Introduction and Literature Review

2. Optimization Model for Demand Planning

2.1. Background

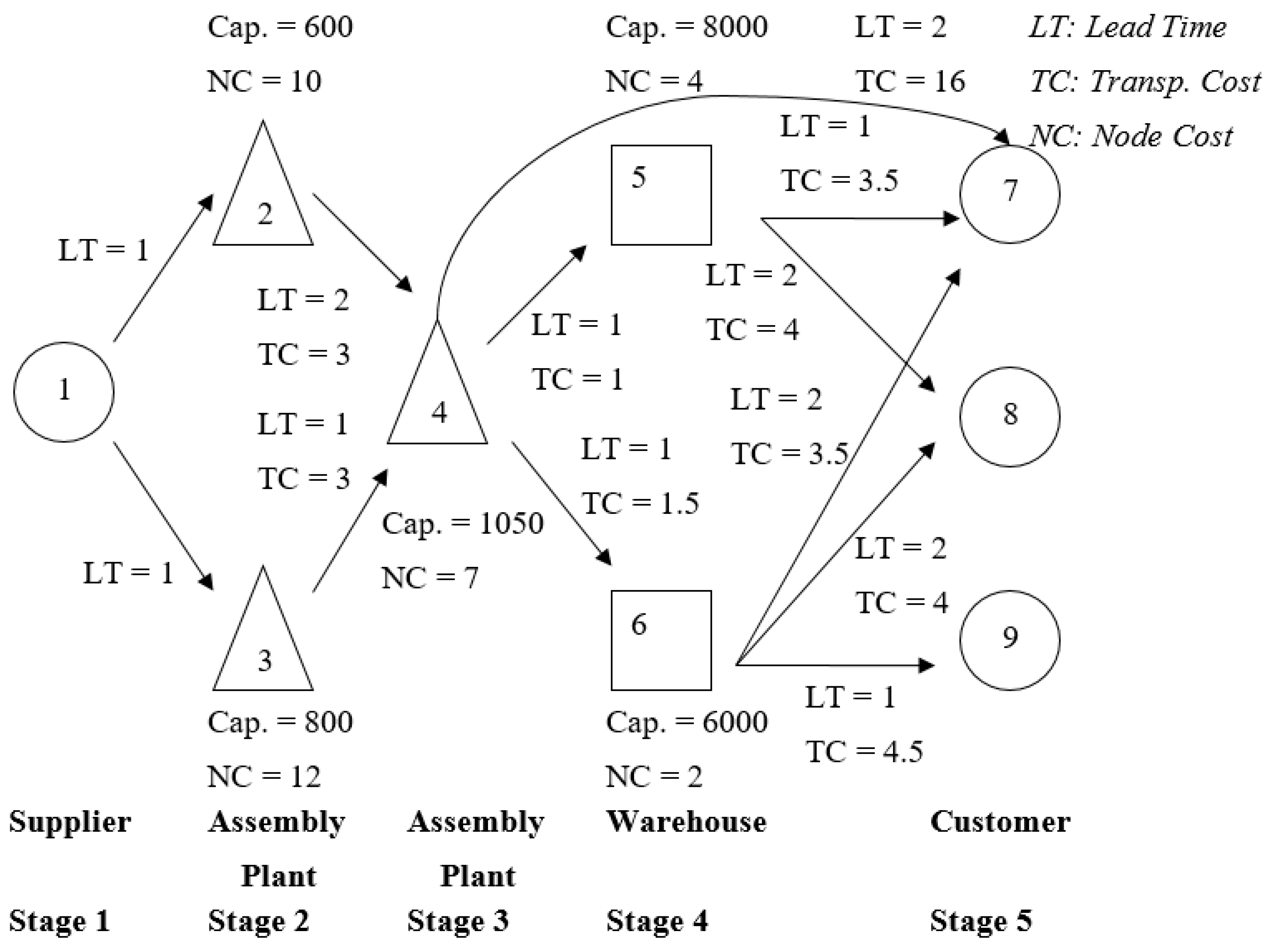

- Nodes in the network represent external nodes, such as suppliers or customers, and internal nodes, such as workstations, plants, and warehouses. Production nodes involve product transformation resulting from manufacturing, assembly, or blending based on recipes (see below).

- Arcs in the network represent transportation between nodes. In order to simplify the notation in our model, activities and capacity restrictions are imposed on nodes instead of arcs.

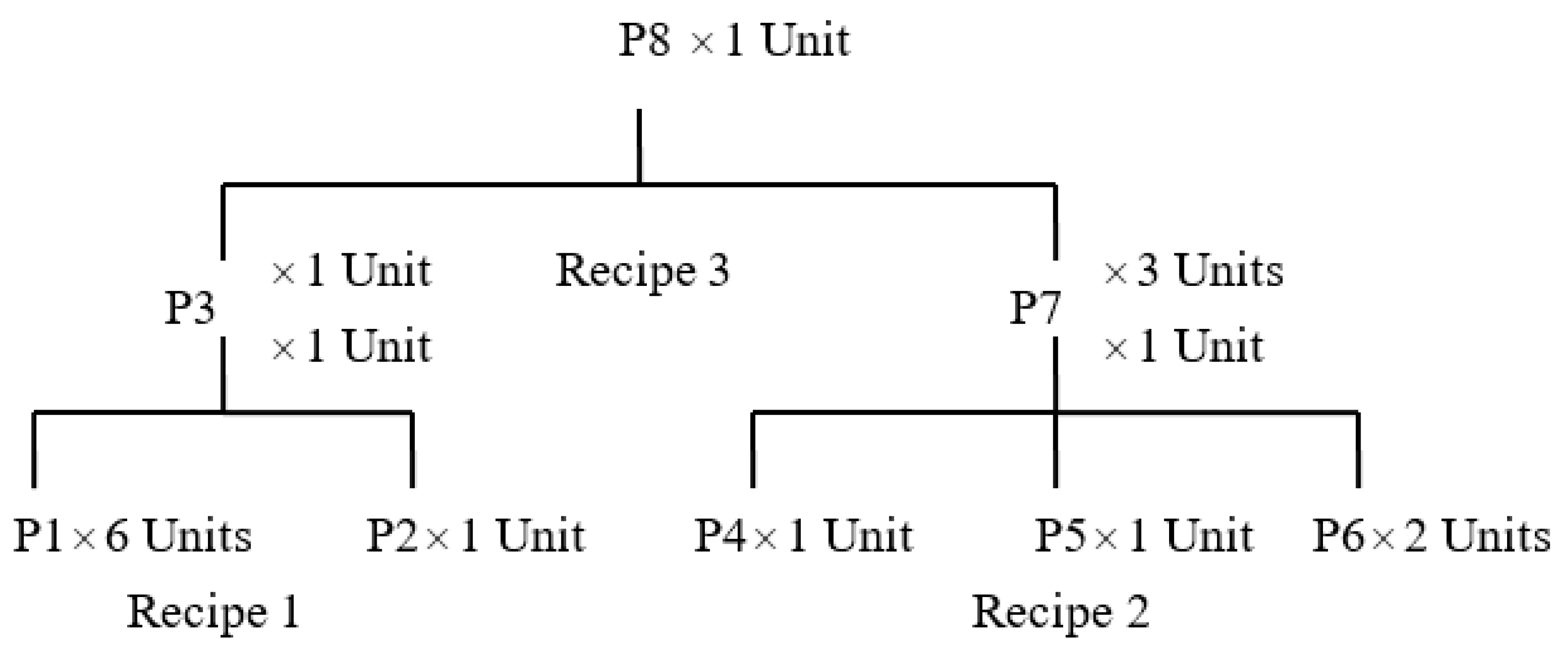

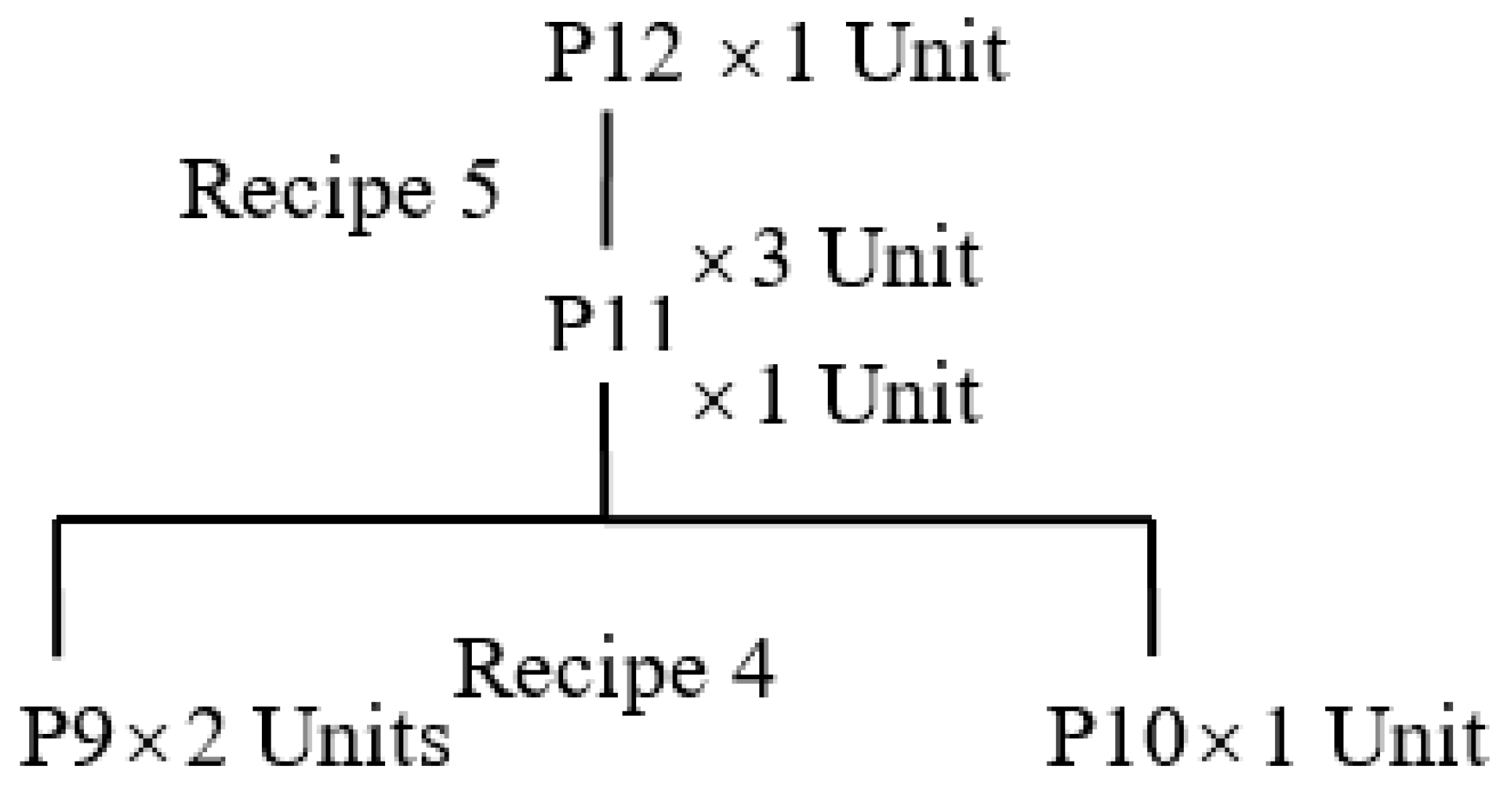

- A recipe is defined as a process step with input and output products. There is a subtle difference between the recipe concept and the bill-of-material concept; a recipe models inputs and outputs at the process level, while a bill of material is always defined at the product level. For example, a node could represent an assembly step. In this case, a step in an assembly bill of material could be regarded as a recipe with several discrete inputs and one output. However, if the node represents a plant, a recipe looks at inputs and outputs at the plant level. The intermediate steps in the bills of materials are collapsed to reflect that process level. A recipe could also represent blending with by-products and is general enough to model any discrete process.

- A new demand or RFQ is defined as a demand under negotiation. In this case, lateness is minimized through “artificial” penalties, which are penalties set by user discretion.

- As negotiation evolves, a new demand turns into a committed demand when a quotation (which is a response to an RFQ) is accepted by a customer.

- Flows arrive or leave at trans-shipment and demand nodes exactly midway through a time period. They stay for a minimum of one period at a node.

- At production nodes, it is assumed that flows arrive at the beginning of a time period; a fraction of flow may be used for production during the time period ().

2.2. Notation

| Items: | m |

| Time Periods: | t |

| Nodes: | j,k |

| Recipes: | r |

| Items: | M = {1, 2, …, m,} |

| Time Periods: | T = {1, 2, …, t,} |

| Production nodes: | IP = {1, 2, …, j,} |

| Trans-shipment nodes: | IT = {1, 2, …, j,}. |

| All intermediate nodes: | = IP ∪ IT |

| Suppliers: | S = {1, 2, …, j,} |

| Customers: | D = {1, 2, …, j,}. |

| All nodes: | N = {S ∪ I ∪ D}. |

| All Arcs: | Γ(t,j,t+l(j,k,m),k) |

| Amj: | Direct successors of resource j for item m |

| Bmj: | Direct predecessors of resource j for item m |

| fmt,j,t + l(j,k,m),k | flow of item m on arc (t,j,t + l(j,k,m),k) |

| xmt,j | initial inventory of item m at node j (ID) in time period t |

| Nt,j,r | actual number of production runs made using recipe r Rj at node j IP in time period t |

| δmt,j | quantity of item m of committed demand backlogged to customer j D in time period t |

| δm1t,j | quantity of item m backlogged in new demand to customer j D in time period t |

| sdmt,j | quantity of committed demand delayed from previous time periods that is satisfied in time period t for customer j D |

| snmt,j | quantity of new demand delayed from previous time periods that is satisfied in time period t for customer j D |

| umj | capacity utilized by one unit of item m flowing through trans-shipment node j IT |

| LXmj | lower bound on the level of stock of item m at node j I (safety stock) |

| UXmj | upper bound on the level of stocks of item m at node j I (space constraint) |

| l(j,k,m) | item m transportation lead time between nodes j and k |

| Lqmt,j | lower bound on the quantity of item m that can be ordered from node j S in time period t |

| Uqmt,j | upper bound on the quantity of item m to order from node j S in time period t |

| Ct,j | available capacity of node j I in time period t. In the case of trans-shipment nodes, Ct,j is in storage units because space availability is the primary concern in trans-shipment resources. |

| β | a value between 0 and 1 indicating the percentage of flow coming into an IP node during a time period that can be used for production |

| OPTj,r | output item set at node j IP, using recipe r Rj |

| IPTj,r | input item set at node j IP, using recipe r Rj |

| Pj | recipe set at node j IP |

| ROmj,r | number of units of output item m OPTj,r produced when recipe r Rj is run at node j |

| RImj,r | number of units of input item m IPTj,r consumed when recipe r Rj is run at node j |

| Vj,r | capacity utilized by one production run of recipe r Rj at node j IP. Vj,r and Ct,j in IP nodes are usually in available machine time. IPTj,r and OPTj,r come from the bill of materials and describe recipe r. |

| dmt,j | committed demand of item m for customer j D in time period t |

| dm1t,j | demand a firm may satisfy other than committed demand of item m for customer j D in time period t (RFQ) |

| lm | lateness order cost applicable to lateness for committed demand per time period |

| l1m | lateness order cost applicable to lateness for new demand per time period |

| Rmj | unit revenue realized when item m is delivered at node j D in response to committed demand |

| Rm1j | unit revenue realized when item m is delivered at node j D in response to new demand |

| smt,j,,k,t + l(j,k,m) | cost of ordering one unit of item m in time period t from node j S to node k (ID) with a lead time of l(j,k,m) |

| cj | item-independent unit cost at node j I per time period |

| cmj | item-dependent unit production cost at node j I for item m per time period |

| hmj | unit holding cost of item m at node j (ID) per time period |

| bmj,k | unit arc cost (sum of transportation and holding costs) between node j and k for item m per time period |

2.3. The Demand Planning Model

2.4. Using the Model

Bottleneck Elimination for Capacity Planning

3. Illustrative Example

3.1. Base-Case Scenario: Quoting Due Dates to Customers

3.2. Order Change: Increased Demand for Customer 8

3.3. New Recipe

3.4. Order Cancellation

3.5. Demand Planning and Capacity Bottleneck Alleviation

Bottleneck Alleviation Algorithm

4. Modelling Congestion Effects

4.1. Clearing Functions

4.2. The Nonlinear Clearing Function Model

| Zt,j,r | maximum number of production runs made using recipe r Rj at node j IP in time period t. |

4.2.1. Input/Output Clearing Function

4.2.2. M/D/1 Clearing Function

4.2.3. General Clearing Function

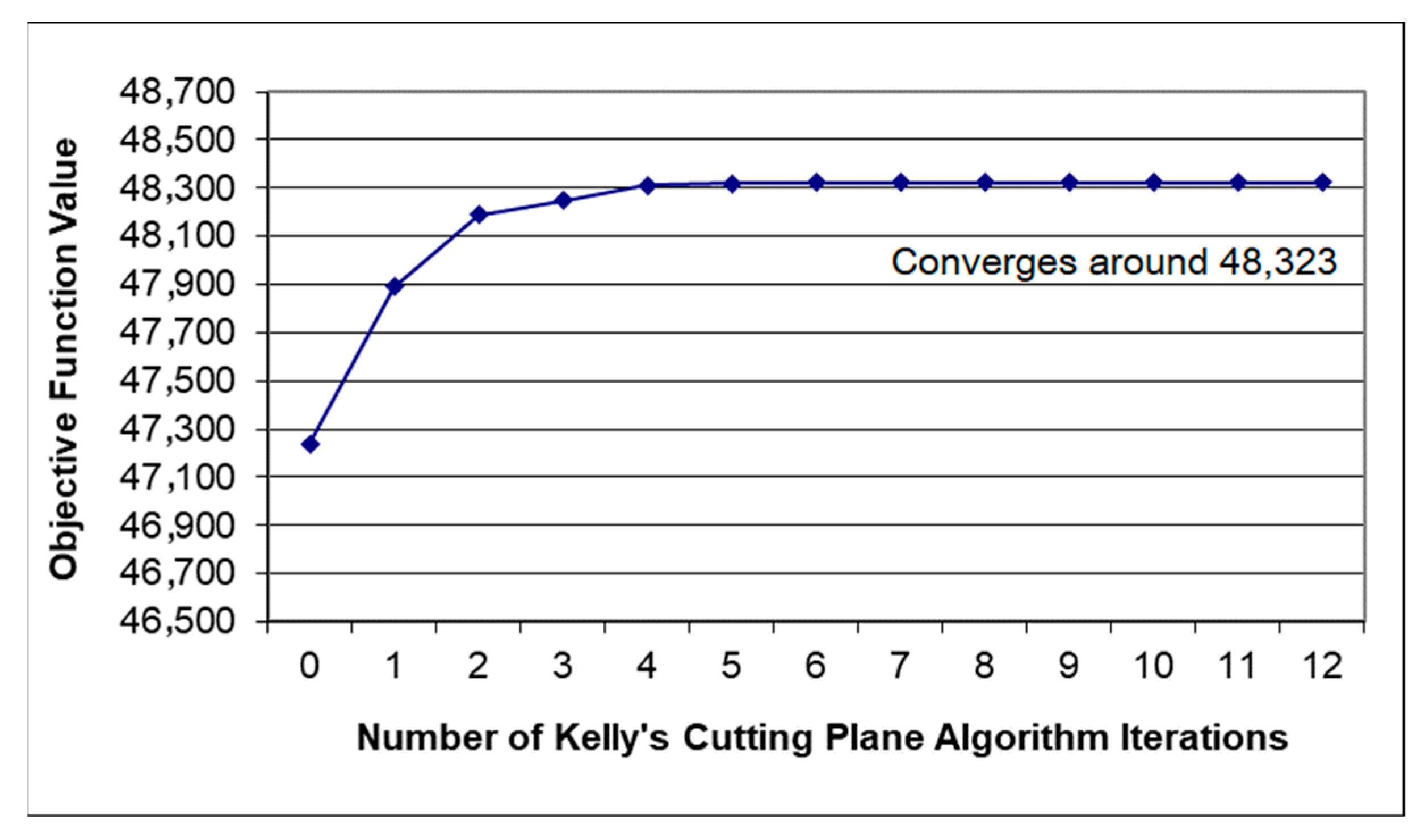

4.3. Algorithms for DPPNL

4.3.1. Inner Approximation

4.3.2. Outer Approximation

- (1)

- Set iteration counter i = 0, .

- (2)

- Drop Constraint (24) and define the following linear constraint:

- (1)

- Set .

- (2)

- Solve DPPNL.

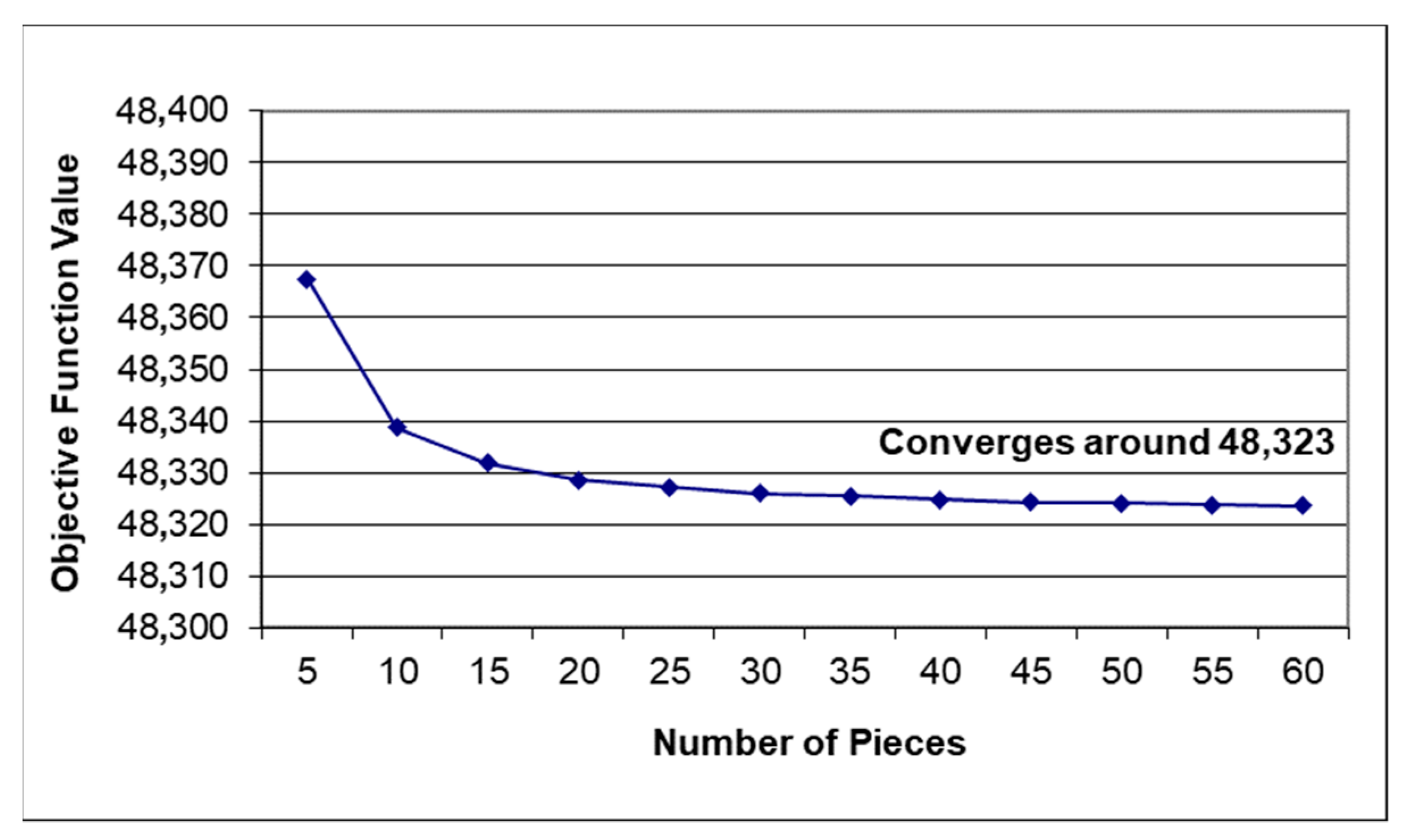

4.3.3. Computational Performance

Comparing Inner and Outer Approximation

Model Solution Time for Different Problem Sizes

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Beamon, B.M. Supply Chain Design and Analysis: Models and Methods. Int. J. Prod. Econ. 1998, 55, 281–294. [Google Scholar] [CrossRef]

- Keskinocak, P.; Tayur, S. Quantitative Analysis for Internet-Enabled Supply Chains. Interfaces 2001, 31, 70–89. [Google Scholar] [CrossRef]

- Askin, R.G.; Goldberg, J.B. Design and Analysis of Lean Poduction Systems; John Wiley and Sons: New York, NY, USA, 2002. [Google Scholar]

- Billington, P.J.; McClain, J.O.; Thomas, L.J. Mathematical Programming Approaches to Capacity-Constrained MRP Systems: Review, Formulation and Problem Reduction. Manag. Sci. 1983, 29, 1126–1141. [Google Scholar] [CrossRef]

- Baker, K.R. Requirement Planning. In Handbooks in Operations Research and Management Science. Logistics of Production and Inventory; Nemhauser, G.L., Rinnooy, K.A.H.G., Graves, S.C., Zipkin, P.H., Eds.; Elsevier Science Publishers B.V.: Amsterdam, The Netherlands, 1993; pp. 371–443. [Google Scholar]

- Rota, K.; Thierry, C.; Bel, G. Capacity Constrained MRP System: A Mathematical Programming Model Integrating Forecasts Firm Orders and Suppliers; Departement d’Automatique, Universite Toulouse II Le Mirail: Toulouse, France, 1997. [Google Scholar]

- Vidal, C.J.; Goetschaalckx, M. Strategic Production-distribution Models: A Critical Review with Emphasis on Global Supply Chain Models. Eur. J. Oper. Res. 1997, 98, 1–18. [Google Scholar] [CrossRef]

- Arntzen, B.C.; Brown, G.G.; Harrison, T.P.; Trafton, L.L. Global Supply Chain Management at Digital Equipment Corporation. Interfaces 1995, 25, 69–93. [Google Scholar] [CrossRef]

- Jang, Y.-J.; Jang, S.-Y.; Chang, B.-M.; Park, J. A combined model of network design and production/distribution planning for a supply network. Comput. Ind. Eng. 2002, 43, 263–281. [Google Scholar] [CrossRef]

- Shapiro, J.F. Bottom-up vs. Top-down Approaches to Supply Chain Modeling. In Quantitative Models for Supply Chain Management; Tayur, S., Ganeshan, R., Magazine, M., Eds.; Kluwer Academic Publishers: Dordrecht, The Netherlands, 1999; pp. 737–759. [Google Scholar]

- Rosenfield, D.B.; Shapiro, R.D.; Bohn, R.E. Implications of Cost-Service Trade-offs on Industry Logistics Structures. Interfaces 1985, 15, 47–59. [Google Scholar] [CrossRef]

- Moodie, D.R.; Bobrowski, P.M. Due Date Demand Management: Negotiating the Trade-off Between Price and Delivery. Int. J. Prod. Res. 1999, 37, 997–1021. [Google Scholar] [CrossRef]

- Venkatadri, U.; Srinivasan, A.; Montreuil, B. Demand and Price Planning in Supply Chain Networks. In Proceedings of the IERC 2003, Portland, OR, USA, 18–20 May 2003. [Google Scholar]

- Upasani, A.; Uzsoy, R. Incorporating Manufacturing Lead Times in Joint Production-Marketing Models: A Review and Further Directions. Ann. Oper. Res. 2008, 161, 171–188. [Google Scholar]

- Karmarkar, U.S.; Kekre, S.; Kekre, S. Lotsizing in Multi-Item Multi- Machine Job Shops. IIE Trans. 1985, 17, 290–298. [Google Scholar] [CrossRef]

- Cohen, M.A.; Lee, H.L. Strategic Analysis of Integrated Production-Distribution Systems: Models and Methods. Oper. Res. 1988, 36, 216–228. [Google Scholar] [CrossRef]

- Srinivasan, A.; Carey, M.; Morton, T.E. Resource Pricing and Aggregate Scheduling in Manufacturing Systems; Working paper; Purdue University: West Lafayette, IN, USA, 1989. [Google Scholar]

- Karmarkar, U.S. Capacity Loading and Release Planning with Work-in-progress (WIP) and Leadtimes. Manuf. Serv. Oper. Manag. 1989, 2, 105–123. [Google Scholar]

- Missbauer, H. Aggregate order release planning for time-varying demand. Int. J. Prod. Res. 2002, 40, 699–718. [Google Scholar] [CrossRef]

- Asmundsson, J.; Rardin, R.; Uzsoy, R. Tractable Nonlinear Production Planning Models for Semiconductor Wafer Fabrication Facilities. IEEE Trans. Semicond. Manuf. 2006, 19, 95–111. [Google Scholar] [CrossRef]

- Pahl, J.; Voß, S.; Woodruff, D.L. Production planning with load dependent lead times: An update of research. Ann. Oper. Res. 2007, 153, 297–345. [Google Scholar] [CrossRef]

- Selcuk, B.; Fransoo, J.C.; De Kok, A.G. Work-in-process clearing in supply chain operations planning. IIE Trans. 2008, 40, 206–220. [Google Scholar] [CrossRef]

- Asmundsson, J.; Rardin, R.L.; Turkseven, C.H.; Uzsoy, R. Production planning with resources subject to congestion. Nav. Res. Logist. 2009, 56, 142–157. [Google Scholar] [CrossRef]

- Missbauer, H.; Uzsoy, R. Optimization Models of Production Planning Problems. In An Introduction to Computational Science; Springer Science and Business Media LLC: New York, NY, USA, 2010; pp. 437–507. [Google Scholar]

- Kacar, N.B.; Monch, L.; Uzsoy, R. Planning Wafer Starts Using Nonlinear Clearing Functions: A Large-Scale Experiment. IEEE Trans. Semicond. Manuf. 2013, 26, 602–612. [Google Scholar] [CrossRef]

- Charnsirisakskul, K.; Griffin, P.M.; Keskinocak, P. Order selection and scheduling with leadtime flexibility. IIE Trans. 2004, 36, 697–707. [Google Scholar] [CrossRef]

- Kefeli, A.; Uzsoy, R. Identifying potential bottlenecks in production systems using dual prices from a mathematical programming model. Int. J. Prod. Res. 2015, 54, 2000–2018. [Google Scholar] [CrossRef]

- Wang, S. Supply Chain Planning using Network Flow Optimization. Unpublished. Master’s Thesis, Department of Industrial Engineering, Dalhousie University, Halifax, Nova Scotia, 2003. [Google Scholar]

- Chen, C.-Y.; Zhao, Z.-Y.; Ball, M.O. Quantity and Due Date Quoting Available to Promise. Inf. Syst. Front. 2001, 3, 477–488. [Google Scholar] [CrossRef]

- Chen, C.-Y.; Zhao, Z.-Y.; Ball, M.O. A Model for Batch Advanced Available-to-Promise. Prod. Oper. Manag. 2002, 11, 424–440. [Google Scholar] [CrossRef]

- Ball, M.O.; Chen, C.-Y.; Zhao, Z.-Y. Handbook of Supply Chain Analysis in the eBusiness Era; Simchi, L.D., David, W.S., Shen, M., Eds.; Kluwer Academic Publishers: Boston, MA, USA, 2004; pp. 447–484. [Google Scholar]

- Shapiro, J.F.; Singhal, V.M.; Wagner, S.N. Optimizing the Value Chain. Interfaces 1993, 23, 102–117. [Google Scholar] [CrossRef]

- Degbotse, A.; Denton, B.T.; Fordyce, K.; Milne, R.J.; Orzell, R.; Wang, C.-T. IBM Blends Heuristics and Optimization to Plan Its Semiconductor Supply Chain. Interfaces 2013, 43, 130–141. [Google Scholar] [CrossRef]

- Fordyce, K.; Wang, C.-T.; Chang, C.-H.; Degbotse, A.; Denton, B.; Lyon, P.; Milne, R.J.; Orzell, R.; Rice, R.; Waite, J. The Ongoing Challenge: Creating an Enterprise-Wide Detailed Supply Chain Plan for Semiconductor and Package Operations. Int. Ser. Oper. Res. Manag. Sci. 2011, 152, 313–387. [Google Scholar]

- Conway, R.; Maxwell, W.L.; McClain, J.O.; Thomas, L.J. The Role of Work-in-Process Inventory in Serial Production Lines. Oper. Res. 1988, 36, 229–241. [Google Scholar] [CrossRef]

- Bhatnagar, R.; Chandra, P. Variability in assembly and competing systems: Effect on performance and recovery. IIE Trans. 1994, 26, 18–31. [Google Scholar] [CrossRef]

- Hopp, W.J.; Spearman, M.L. Factory Physics: Foundations of Manufacturing Management, 2nd ed.; McGraw-Hill Irwin: New York, NY, USA, 2001. [Google Scholar]

- Robinson, S.M. A quadratically-convergent algorithm for general nonlinear programming problems. Math. Program. 1972, 3, 145–156. [Google Scholar] [CrossRef]

- Simmons, D.M. Nonlinear Programming for Operations Research. In International Series in Management; Prentice-Hall: Upper Saddle River, NJ, USA, 1975. [Google Scholar]

- Zangwill, W.I. Nonlinear Programming: A Unified Approach; Prentice-Hall: Englewood Cliffs, NJ, USA, 1969. [Google Scholar]

- Luenberger, D.G.; Ye, Y. Linear and Nonlinear Programming, 3rd ed.; International Series in Operations Research and Management Science ISOR 116; Hillier, F.S., Ed.; Springer: New York, NY, USA, 2008. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Item ID | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| Unit Cost | 4 | 10 | 18 | 5 | 3 | 2 | 15 | 200 |

| Unit Holding Cost | 0.016 | 0.04 | 0.072 | 0.02 | 0.012 | 0.08 | 0.06 | 0.8 |

| Node ID | Item ID | Capacity Consumed by Unit |

|---|---|---|

| 2 | 8 | 8 |

| 3 | 8 | 8 |

| Node ID | Recipe ID | Capacity Consumed by Production |

|---|---|---|

| 4 | 1 | 1 |

| 4 | 2 | 2 |

| 5 | 1 | 1 |

| 5 | 2 | 2 |

| 6 | 3 | 3 |

| Node ID | Item ID | Product Dependent Unit Cost |

|---|---|---|

| 2 | 8 | 2 |

| 3 | 8 | 2.2 |

| 4 | 1 | 0.645 |

| 4 | 2 | 0.8 |

| 4 | 3 | 0.965 |

| 4 | 4 | 1.025 |

| 4 | 5 | 1.14 |

| 4 | 6 | 1.26 |

| 4 | 7 | 1.45 |

| 5 | 1 | 0.77 |

| 5 | 2 | 0.925 |

| 5 | 3 | 1.09 |

| 5 | 4 | 1.15 |

| 5 | 5 | 1.265 |

| 5 | 6 | 1.385 |

| 5 | 7 | 1.575 |

| 6 | 3 | 1.215 |

| 6 | 7 | 1.7 |

| 6 | 8 | 2.75 |

| Node/Time Period/Demand | 6 | 7 | 8 | 9 | 10 | 11 | 12 |

|---|---|---|---|---|---|---|---|

| Node 7 | 80 | 75 | 120 | 135 | 170 | 140 | 100 |

| Node 8 | 30 | 45 | 50 | 45 | 55 | 40 | 35 |

| Node 9 | 50 | 150 | 20 | 100 | 20 | 25 | 60 |

| Total Demand | 160 | 270 | 190 | 280 | 255 | 205 | 195 |

| Scenario | Node ID | Time Period | Total Lateness |

|---|---|---|---|

| Scenario 1: Base Case | 7 | 10 | 123.34 |

| 8 | 10 | 25 | |

| 9 | 9 | 23.34 | |

| 9 | 10 | 20 | |

| Objective Function Value = 227,204.74 | |||

| Scenario 2: Increased Demand for Customer 8 | 7 | 10 | 193.34 |

| 8 | 10 | 25 | |

| 9 | 9 | 93.34 | |

| 9 | 10 | 20 | |

| Objective Function Value = 278,427.98 | |||

| Scenario 3: New Recipe | 7 | 10 | 131.9 |

| 7 | 11 | 17.17 | |

| 9 | 9 | 36.67 | |

| 9 | 10 | 31.67 | |

| Objective Function Value = 257,674.85 | |||

| Scenario 4: Order Cancellation | 7 | 11 | 6.67 |

| 9 | 11 | 6.67 | |

| Objective Function Value = 159,620.03 | |||

| Node ID | Time Period | Capacity Cost | RUN #1 | RUN #2 | ||||||

| Capacity | Dual Price | Improvement | Sensitivity Range (Upper Bound) | Capacity | Dual Price | Improvement | Sensitivity Range (Upper Bound) | |||

| 4 | 2 | 100 | 600 | 165.88 | 1025.09 | 615.56 | 600 | 165.9 | 1025.4 | 615.56 |

| 4 | 3 | 100 | 600 | 123.03 | 537.29 | 623.33 | 600 | 123.04 | 537.52 | 623.33 |

| 4 | 4 | 100 | 600 | 80.17 | −462.63 | 623.33 | 600 | 80.18 | −462.4 | 623.33 |

| 4 | 5 | 100 | 600 | 37.31 | −1462.6 | 623.33 | 600 | 37.32 | −1462.3 | 623.33 |

| 4 | 6 | 100 | 600 | 1 | −26,070 | 863.33 | 600 | 1 | −26,070 | 863.33 |

| 5 | 2 | 130 | 800 | 186.32 | 1313.95 | 823.33 | 823 | 186.33 | 18.5889 | 823.33 |

| 5 | 3 | 130 | 800 | 164.87 | 542.577 | 815.56 | 800 | 164.89 | 7.6758 | 800.22 |

| 3 | 4 | 130 | 800 | 121.98 | −187.11 | 823.33 | 800 | 121.98 | −2.6466 | 800.33 |

| 5 | 5 | 130 | 800 | 79.16 | −1186.1 | 823.33 | 800 | 79.17 | −16.774 | 800.33 |

| 5 | 6 | 130 | 800 | 36.26 | −2187 | 823.33 | 800 | 36.27 | −30.931 | 800.33 |

| Node ID | Time Period | Capacity Cost | RUN #3 | RUN #4 | ||||||

| Capacity | Dual Price | Improvement | Sensitivity Range (Upper Bound) | Capacity | Dual Price | Improvement | Sensitivity Range (Upper Bound) | |||

| 4 | 2 | 100 | 615 | 165.9 | 6172.85 | 708.67 | 690 | 165.9 | 1230.35 | 708.67 |

| 4 | 3 | 100 | 600 | 123 | 1400.47 | 660.89 | 600 | 123 | 429.41 | 618.67 |

| 4 | 4 | 100 | 600 | 80.18 | −1856.5 | 693.67 | 600 | 80.18 | −370.04 | 618.67 |

| 4 | 5 | 100 | 600 | 37.33 | −5870.3 | 693.67 | 600 | 37.33 | −1170 | 618.67 |

| 4 | 6 | 100 | 600 | 1 | −18546 | 787.33 | 600 | 1 | −3695.7 | 637.33 |

| 5 | 2 | 130 | 823 | 186.33 | 2057.17 | 859.52 | 823 | 186.33 | 1051.68 | 841.67 |

| 5 | 3 | 130 | 800 | 164.89 | 3268.15 | 893.67 | 800 | 164.89 | 651.396 | 818.67 |

| 3 | 4 | 130 | 800 | 121.98 | −751.23 | 893.67 | 800 | 121.98 | −149.73 | 818.67 |

| 5 | 5 | 130 | 800 | 79.17 | −4761.2 | 893.67 | 800 | 79.17 | −949 | 818.67 |

| 5 | 6 | 130 | 800 | 36.27 | −8779.7 | 893.67 | 800 | 36.27 | −1166 | 812.44 |

| Node/Time Period/Demand | 6 | 7 | 8 | 9 | 10 | RFQ in Periods 11–18 |

|---|---|---|---|---|---|---|

| Node 7 | 80 | 75 | 120 | 135 | 170 | 175 |

| Node 8 | 30 | 45 | 50 | 45 | 55 | 44 |

| Node 9 | 50 | 150 | 20 | 100 | 20 | 87 |

| Total Demand | 160 | 270 | 190 | 280 | 255 | 306 |

| Nodes | Time Periods | Total Number of Nodes | CPU Time (Seconds) for Outer Approximation ** | CPU Time (Seconds) for Inner Approximation * | Percentage Increase (Inner Approximation Over Outer Approximation) |

|---|---|---|---|---|---|

| 9 | 10 | 90 | 10.77 | 7.94 | −26.40% |

| 9 | 15 | 135 | 29.52 | 41.89 | 41.93% |

| 12 | 10 | 120 | 23.51 | 27.69 | 17.76% |

| 12 | 15 | 180 | 63.88 | 118.31 | 85.20% |

| 15 | 10 | 150 | 32.68 | 38.34 | 17.33% |

| 15 | 15 | 225 | 107.93 | 246.01 | 127.94% |

| 18 | 10 | 180 | 71.96 | 132.3 | 83.86% |

| 18 | 15 | 270 | 250.57 | 608.85 | 142.99% |

| Nodes | Time Periods | Augmented Lagrangian Optimal Obj. Fun. Value | Inner Approximation | Outer Approximation | ||

|---|---|---|---|---|---|---|

| Optimal Obj. Fun. Value * | Gap (%) | Optimal Obj. Fun. Value ** | Gap (%) | |||

| 9 | 10 | 15,979.45 | 16,276.77 | 1.86 | 15,974.56 | −0.031 |

| 9 | 15 | 13,861.32 | 13,903.68 | 0.31 | 13,855.34 | −0.043 |

| 12 | 10 | 22,575.77 | 23,098.55 | 2.32 | 22,119.49 | −2.02 |

| 12 | 15 | 18,867.84 | 18,918.27 | 0.27 | 18,843 | −0.13 |

| 15 | 10 | 27,174.84 | 27,855.08 | 2.5 | 26,982.46 | −0.71 |

| 15 | 15 | 23,914.94 | 23,925.25 | 0.04 | 23,833.54 | −0.34 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Venkatadri, U.; Wang, S.; Srinivasan, A. A Model for Demand Planning in Supply Chains with Congestion Effects. Logistics 2021, 5, 3. https://doi.org/10.3390/logistics5010003

Venkatadri U, Wang S, Srinivasan A. A Model for Demand Planning in Supply Chains with Congestion Effects. Logistics. 2021; 5(1):3. https://doi.org/10.3390/logistics5010003

Chicago/Turabian StyleVenkatadri, Uday, Shentao Wang, and Ashok Srinivasan. 2021. "A Model for Demand Planning in Supply Chains with Congestion Effects" Logistics 5, no. 1: 3. https://doi.org/10.3390/logistics5010003

APA StyleVenkatadri, U., Wang, S., & Srinivasan, A. (2021). A Model for Demand Planning in Supply Chains with Congestion Effects. Logistics, 5(1), 3. https://doi.org/10.3390/logistics5010003