The Research Trend of Security and Privacy in Digital Payment

,

,

,

,  ,

,  and

and

Abstract

:1. Introduction

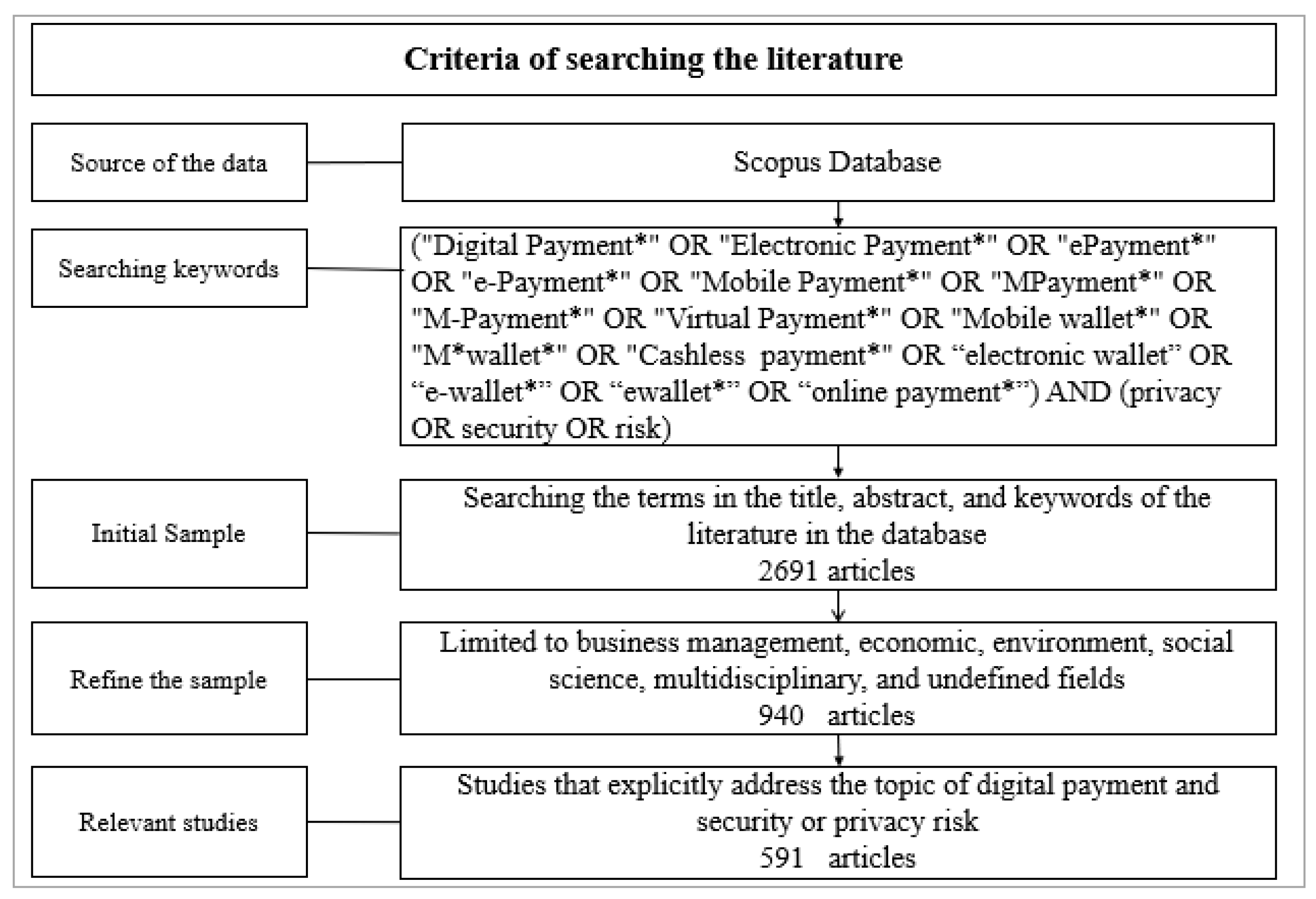

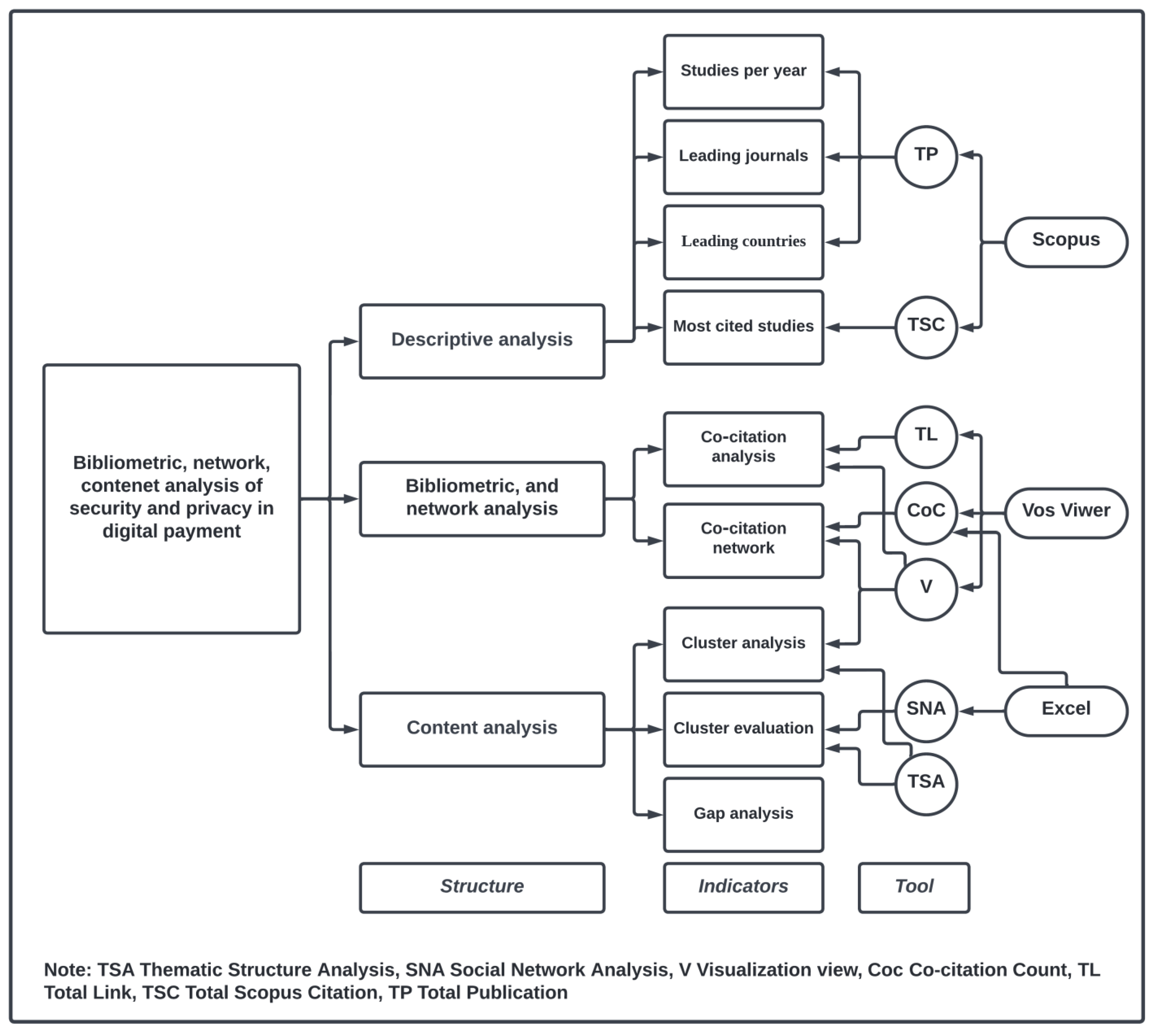

2. Materials and Methods

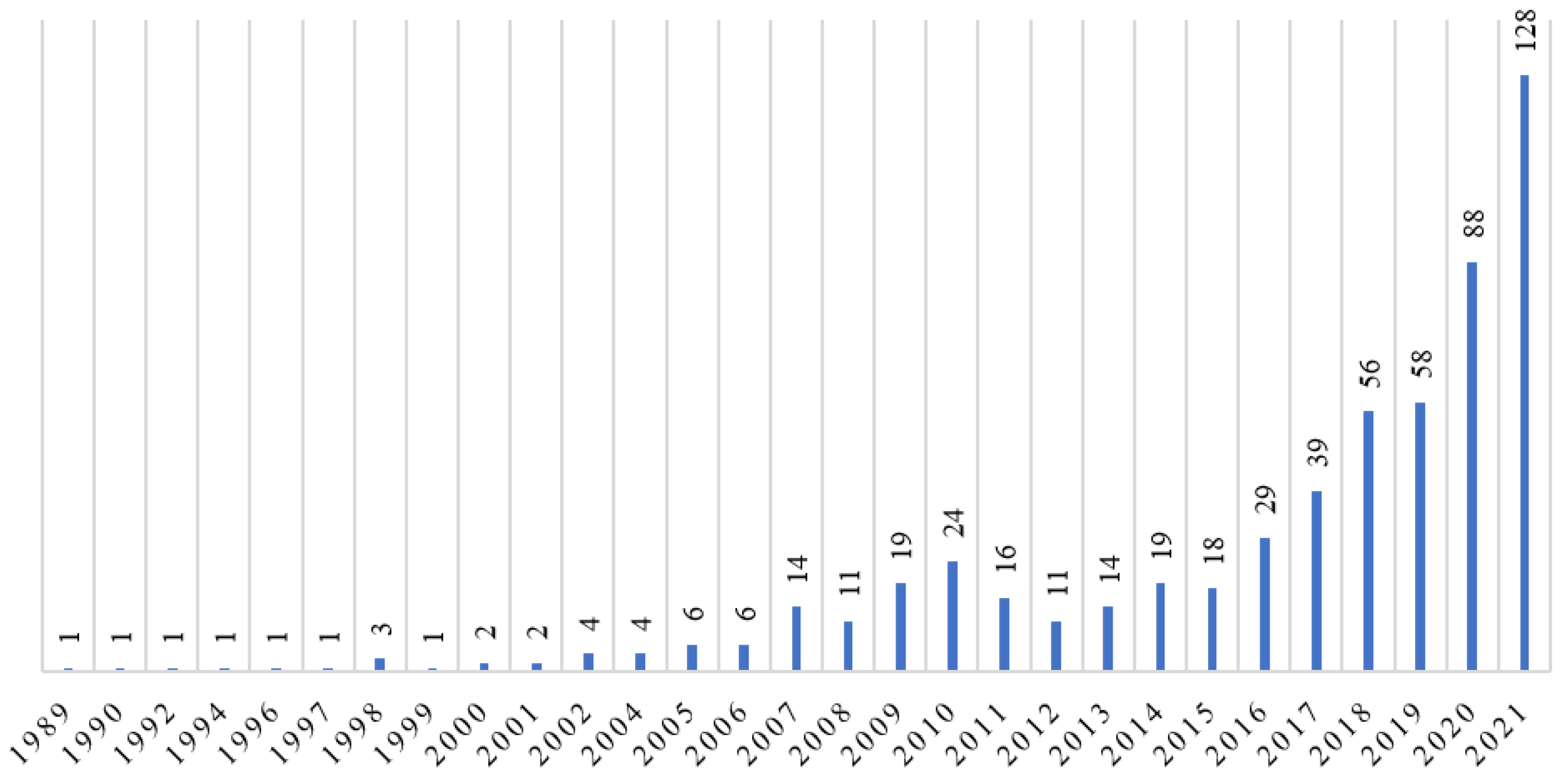

3. Results and Discussion

3.1. Leading Countries

3.2. Leading Journals

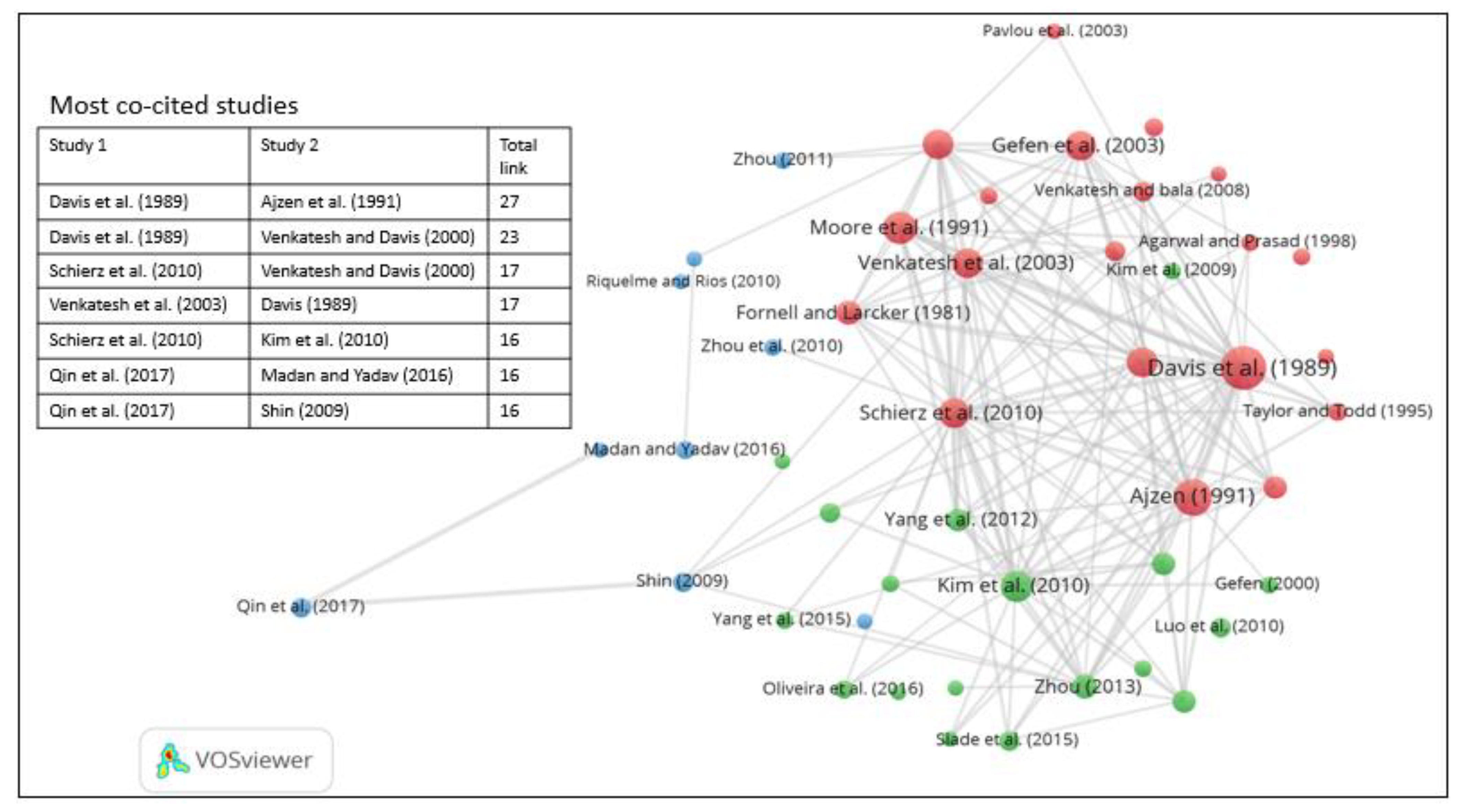

3.3. Most-Cited Studies

3.4. Co-Citation Analysis

4. Co-Citation Network

4.1. Cluster 1 (Red)

4.2. Cluster 2 (Green)

4.3. Cluster 3 (Blue)

5. Discussion and Future Research

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Teoh, W.M.Y.; Chong, S.C.; Lin, B.; Chua, J.W. Factors affecting consumers’ perception of electronic payment: An empirical analysis. Internet Res. 2013, 23, 465–485. [Google Scholar] [CrossRef]

- Sahi, A.M.; Khalid, H.; Abbas, A.F.; Khatib, S.F.A. The evolving research of customer adoption of digital payment: Learning from content and statistical analysis of the literature. J. Open Innov. Technol. Mark. Complex. 2021, 7, 230. [Google Scholar] [CrossRef]

- De Luna, I.R.; Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Mobile payment is not all the same: The adoption of mobile payment systems depending on the technology applied. Technol. Forecast. Soc. Chang. 2019, 146, 931–944. [Google Scholar] [CrossRef]

- Schierz, P.G.; Schilke, O.; Wirtz, B.W. Understanding consumer acceptance of mobile payment services: An empirical analysis. Electron. Commer. Res. Appl. 2010, 9, 209–216. [Google Scholar] [CrossRef]

- Aljawder, M.; Abdulrazzaq, A. The effect of awareness, trust, and privacy and security on students’ adoption of contactless payments: An empirical study. Int. J. Comput. Digit. Syst. 2019, 8, 669–676. [Google Scholar] [CrossRef]

- Duane, A.; O’Reilly, P.; Andreev, P. Realising M-Payments: Modelling consumers’ willingness to M-pay using Smart Phones. Behav. Inf. Technol. 2014, 33, 318–334. [Google Scholar] [CrossRef]

- Kumar, A.S.; Arun Palanisamy, Y. Examining the consumers’ preference towards adopting the mobile payment system. Int. J. Electron. Financ. 2019, 9, 268–286. [Google Scholar] [CrossRef]

- Sorkin, D.E. Payment methods for consumer to consumer online transactions. Akron Law Rev. 2001, 35, 1–30. [Google Scholar]

- Hwang, J.J.; Yeh, T.C.; Li, J. Bin Securing on-line credit card payments without disclosing privacy information. Comput. Stand. Interfaces 2003, 25, 119–129. [Google Scholar] [CrossRef]

- Qin, Z.; Sun, J.; Wahaballa, A.; Zheng, W.; Xiong, H.; Qin, Z. A secure and privacy-preserving mobile wallet with outsourced verification in cloud computing. Comput. Stand. Interfaces 2017, 54, 55–60. [Google Scholar] [CrossRef]

- Kartika, H.; Fatimah, Y.A.; Supangkat, S.H. Secure Cashless Payment Governance in Indonesia: A Systematic Literature Review. In Proceedings of the 2018 International Conference on ICT for Smart Society (ICISS), Semarang, Indonesia, 10–11 October 2018; pp. 1–4. [Google Scholar] [CrossRef]

- Yang, Y.; Liu, Y.; Li, H.; Yu, B. Understanding perceived risks in mobile payment acceptance. Ind. Manag. Data Syst. 2015, 115, 253–269. [Google Scholar] [CrossRef]

- El Haddad, G.; Aimeur, E.; Hage, H. Understanding Trust, Privacy and Financial Fears in Online Payment. In Proceedings of the 2018 17th IEEE International Conference On Trust, Security And Privacy In Computing And Communications/12th IEEE International Conference On Big Data Science And Engineering (TrustCom/BigDataSE), New York, NY, USA, 1–3 August 2018; pp. 28–36. [Google Scholar] [CrossRef]

- Bagla, R.K.; Sancheti, V. Gaps in customer satisfaction with digital wallets: Challenge for sustainability. J. Manag. Dev. 2018, 37, 442–451. [Google Scholar] [CrossRef]

- Kar, A.K. What Affects Usage Satisfaction in Mobile Payments? Modelling User Generated Content to Develop the “Digital Service Usage Satisfaction Model”. Inf. Syst. Front. 2021, 23, 1341–1361. [Google Scholar] [CrossRef] [PubMed]

- Grover, P.; Kar, A.K. User engagement for mobile payment service providers—introducing the social media engagement model. J. Retail. Consum. Serv. 2020, 53, 101718. [Google Scholar] [CrossRef]

- Rahi, S.; Abd.Ghani, M.; Hafaz Ngah, A. Integration of unified theory of acceptance and use of technology in internet banking adoption setting: Evidence from Pakistan. Technol. Soc. 2019, 58, 101120. [Google Scholar] [CrossRef]

- Luarn, P.; Lin, H.H. Toward an understanding of the behavioral intention to use mobile banking. Comput. Hum. Behav. 2005, 21, 873–891. [Google Scholar] [CrossRef]

- Apanasevic, T.; Markendahl, J.; Arvidsson, N. Stakeholders’ expectations of mobile payment in retail: Lessons from Sweden. Int. J. Bank Mark. 2016, 34, 37–61. [Google Scholar] [CrossRef]

- Liu, R.; Wu, J.; Yu-Buck, G.F. The influence of mobile QR code payment on payment pleasure: Evidence from China. Int. J. Bank Mark. 2021, 39, 337–356. [Google Scholar] [CrossRef]

- Singh, N.; Srivastava, S.; Sinha, N. Consumer preference and satisfaction of M-wallets: A study on North Indian consumers. Int. J. Bank Mark. 2017, 35, 944–965. [Google Scholar] [CrossRef]

- Uduji, J.I.; Okolo-Obasi, E.N. Young rural women’s participation in the e-wallet programme and usage intensity of modern agricultural inputs in Nigeria. Gend. Technol. Dev. 2018, 22, 59–81. [Google Scholar] [CrossRef] [Green Version]

- Zhou, T.; Lu, Y.; Wang, B. Integrating TTF and UTAUT to explain mobile banking user adoption. Comput. Hum. Behav. 2010, 26, 760–767. [Google Scholar] [CrossRef]

- Rahi, S.; Abd.Ghani, M. Investigating the role of UTAUT and e-service quality in internet banking adoption setting. TQM J. 2019, 31, 491–506. [Google Scholar] [CrossRef]

- Al-Okaily, M.; Lutfi, A.; Alsaad, A.; Taamneh, A.; Alsyouf, A. The Determinants of Digital Payment Systems’ Acceptance under Cultural Orientation Differences: The Case of Uncertainty Avoidance. Technol. Soc. 2020, 63, 101367. [Google Scholar] [CrossRef]

- Putri, M.F.; Purwandari, B.; Hidayanto, A.N. What do affect customers to use mobile payment continually? A systematic literature review. In Proceedings of the 2020 Fifth International Conference on Informatics and Computing (ICIC), Gorontalo, Indonesia, 3–4 November 2020. [Google Scholar] [CrossRef]

- Pramana, E. The Mobile Payment Adoption: A Systematic Literature Review. In Proceedings of the 2021 3rd East Indonesia Conference on Computer and Information Technology (EIConCIT), Surabaya, Indonesia, 9–11 April 2021; pp. 265–269. [Google Scholar] [CrossRef]

- Alkhowaiter, W.A. Digital payment and banking adoption research in Gulf countries: A systematic literature review. Int. J. Inf. Manag. 2020, 53, 102102. [Google Scholar] [CrossRef]

- Boateng, R.; Sarpong, M.Y.P. A Literature Review of Mobile Payments in Sub-Saharan Africa; Springer International Publishing: Berlin/Heidelberg, Germany, 2019; Volume 558, ISBN 9783030206703. [Google Scholar]

- Wonglimpiyarat, J. Competition and challenges of mobile banking: A systematic review of major bank models in the Thai banking industry. J. High Technol. Manag. Res. 2014, 25, 123–131. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Abdullah, D.F.; Hendrawaty, E.; Elamer, A.A. A bibliometric analysis of cash holdings literature: Current status, development, and agenda for future research. Manag. Rev. Q. 2021; 1–38, ahead of print. [Google Scholar] [CrossRef]

- Hazaea, S.A.; Zhu, J.; Al-Matari, E.M.; Senan, N.A.M.; Khatib, S.F.A.; Ullah, S. Mapping of internal audit research in China: A systematic literature review and future research agenda. Cogent Bus. Manag. 2021, 8, 1938351. [Google Scholar] [CrossRef]

- Zamil, I.A.; Ramakrishnan, S.; Jamal, N.M.; Hatif, M.A.; Khatib, S.F.A. Drivers of corporate voluntary disclosure: A systematic review. J. Financ. Report. Account. 2021; ahead of print. [Google Scholar] [CrossRef]

- Hazaea, S.A.; Zhu, J.; Khatib, S.F.A.; Bazhair, A.H.; Elamer, A.A. Sustainability assurance practices: A systematic review and future research agenda. Environ. Sci. Pollut. Res. 2022, 29, 4843–4864. [Google Scholar] [CrossRef]

- Block, J.H.; Fisch, C. Eight tips and questions for your bibliographic study in business and management research. Manag. Rev. Q. 2020, 70, 307–312. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Abdullah, D.F.; Elamer, A.A.; Abueid, R. Nudging toward diversity in the boardroom: A systematic literature review of board diversity of financial institutions. Bus. Strateg. Environ. 2021, 30, 985–1002. [Google Scholar] [CrossRef]

- Abbas, A.F.; Jusoh, A.B.; Masod, A.; Ali, J. Market Maven and Mavenism: A Bibliometrics Analysis using Scopus Database. Int. J. Manag. 2020, 11, 31–45. [Google Scholar] [CrossRef]

- Abbas, A.F.; Jusoh, A.; Mas’od, A.; Alsharif, A.H.; Ali, J. Bibliometrix analysis of information sharing in social media. Cogent Bus. Manag. 2022, 9, 2016556. [Google Scholar] [CrossRef]

- Khatib, S.; Abdullah, D.F.; Elamer, A.; Hazaea, S.A. The Development of Corporate Governance Literature in Malaysia: A Systematic Literature Review and Research Agenda. Corp. Gov. Int. J. Bus. Soc. 2022; ahead of print. [Google Scholar] [CrossRef]

- Taylor, E. Mobile payment technologies in retail: A review of potential benefits and risks. Int. J. Retail Distrib. Manag. 2016, 44, 159–177. [Google Scholar] [CrossRef]

- Massaro, M.; Dumay, J.; Guthrie, J. On the shoulders of giants: Undertaking a structured literature review in accounting. Account. Audit. Account. J. 2016, 29, 767–801. [Google Scholar] [CrossRef]

- Rasel, M.A.; Win, S. Microfinance governance: A systematic review and future research directions. J. Econ. Stud. 2020, 47, 1811–1847. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Abdullah, D.F.; Elamer, A.; Yahaya, I.S.; Owusu, A. Global trends in board diversity research: A bibliometric view. Meditari Account. Res. 2021; ahead of print. [Google Scholar] [CrossRef]

- Khatib, S.F.A.; Abdullah, D.F.; Al Amosh, H.; Bazhair, A.H.; Kabara, A.S. Shariah auditing: Analyzing the past to prepare for the future auditing. J. Islam. Account. Bus. Res. 2022; ahead of print. [Google Scholar] [CrossRef]

- Bürk, H.; Pfitzmann, A. Value exchange systems enabling security and unobservability. Comput. Secur. 1990, 9, 715–721. [Google Scholar] [CrossRef]

- Mallat, N. Exploring consumer adoption of mobile payments—A qualitative study. J. Strateg. Inf. Syst. 2007, 16, 413–432. [Google Scholar] [CrossRef]

- Dahlberg, T.; Mallat, N.; Ondrus, J.; Zmijewska, A. Past, present and future of mobile payments research: A literature review. Electron. Commer. Res. Appl. 2008, 7, 165–181. [Google Scholar] [CrossRef] [Green Version]

- Slade, E.L.; Dwivedi, Y.K.; Piercy, N.C.; Williams, M.D. Modeling Consumers’ Adoption Intentions of Remote Mobile Payments in the United Kingdom: Extending UTAUT with Innovativeness, Risk, and Trust. Psychol. Mark. 2015, 32, 860–873. [Google Scholar] [CrossRef]

- Kim, C.; Tao, W.; Shin, N.; Kim, K.S. An empirical study of customers’ perceptions of security and trust in e-payment systems. Electron. Commer. Res. Appl. 2010, 9, 84–95. [Google Scholar] [CrossRef]

- Thakur, R.; Srivastava, M. Adoption readiness, personal innovativeness, perceived risk and usage intention across customer groups for mobile payment services in India. Internet Res. 2014, 24, 369–392. [Google Scholar] [CrossRef]

- Au, Y.A.; Kauffman, R.J. The economics of mobile payments: Understanding stakeholder issues for an emerging financial technology application. Electron. Commer. Res. Appl. 2008, 7, 141–164. [Google Scholar] [CrossRef]

- Morosan, C.; DeFranco, A. It’s about time: Revisiting UTAUT2 to examine consumers’ intentions to use NFC mobile payments in hotels. Int. J. Hosp. Manag. 2016, 53, 17–29. [Google Scholar] [CrossRef]

- De Kerviler, G.; Demoulin, N.T.M.; Zidda, P. Adoption of in-store mobile payment: Are perceived risk and convenience the only drivers? J. Retail. Consum. Serv. 2016, 31, 334–344. [Google Scholar] [CrossRef]

- Von Solms, S.; Naccache, D. On blind signatures and perfect crimes. Comput. Secur. 1992, 11, 581–583. [Google Scholar] [CrossRef]

- Slade, E.; Williams, M.; Dwivedi, Y.; Piercy, N. Exploring consumer adoption of proximity mobile payments. J. Strateg. Mark. 2015, 23, 209–223. [Google Scholar] [CrossRef]

- Van Eck, N.J.; Waltman, L. Manual for VOSviewer version 1.6.8; Univeristeit Leiden: Leiden, The Netherlands, 2018; pp. 1–51. [Google Scholar]

- Ajzen, I. The theory of planned behavior. Organ. Behav. Hum. Decis. Process. 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Davis, F.D.; Bagozzi, R.P.; Warshaw, P.R. User Acceptance of Computer Technology: A Comparison of Two Theoretical Models. Manag. Sci. 1989, 35, 982–1003. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Davis, F.D.; College, S.M.W. A theoretical extension of the technology acceptance model: Four longitudinal field studies. Manag. Sci. 2000, 46, 186–204. [Google Scholar] [CrossRef] [Green Version]

- Phonthanukitithaworn, C.; Sellitto, C.; Fong, M. User intentions to adopt mobile payment services: A study of early adopters in Thailand. J. Internet Bank. Commer. 2015, 20, 1–29. [Google Scholar]

- Aslam, W.; Ham, M.; Arif, I. Consumer behavioral intentions towards mobile payment services: An empirical analysis in Pakistan. Market-Trziste 2017, 29, 161–176. [Google Scholar] [CrossRef] [Green Version]

- Liébana-Cabanillas, F.J.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Role of gender on acceptance of mobile payment. Ind. Manag. Data Syst. 2014, 114, 220–240. [Google Scholar] [CrossRef]

- Chawla, D.; Joshi, H. Consumer attitude and intention to adopt mobile wallet in India—An empirical study. Int. J. Bank Mark. 2019, 37, 1590–1618. [Google Scholar] [CrossRef]

- Shin, D.H. Towards an understanding of the consumer acceptance of mobile wallet. Comput. Hum. Behav. 2009, 25, 1343–1354. [Google Scholar] [CrossRef]

- Pham, T.T.T.; Ho, J.C. The effects of product-related, personal-related factors and attractiveness of alternatives on consumer adoption of NFC-based mobile payments. Technol. Soc. 2015, 43, 159–172. [Google Scholar] [CrossRef]

- Madan, K.; Yadav, R. Understanding and predicting antecedents of mobile shopping adoption: A developing country perspective. Asia Pacific J. Mark. Logist. 2018, 30, 139–162. [Google Scholar] [CrossRef]

- Zhang, J.; Luximon, Y. A quantitative diary study of perceptions of security in mobile payment transactions. Behav. Inf. Technol. 2021, 40, 1579–1602. [Google Scholar] [CrossRef]

- Venkatesh, V. Determinants of Perceived Ease of Use: Integrating Control, Intrinsic Motivation, and Emotion into the Technology Acceptance Model. Inf. Syst. Res. 2000, 11, 342–365. [Google Scholar] [CrossRef] [Green Version]

- Davis, F.D. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q. Manag. Inf. Syst. 1989, 13, 319–339. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Bala, H. Technology acceptance model 3 and a research agenda on interventions. Decis. Sci. 2008, 39, 273–315. [Google Scholar] [CrossRef] [Green Version]

- Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Anderson, J.C.; Gerbing, D.W. Structural Equation Modeling in Practice: A Review and Recommended Two-Step Approach. Psychol. Bull. 1988, 103, 411–423. [Google Scholar] [CrossRef]

- Bagozzi, R.P.; Yi, Y. On the evaluation of structural equation models. J. Acad. Mark. Sci. 1988, 16, 74–94. [Google Scholar] [CrossRef]

- Pavlou, P.A. Consumer Acceptance of Electronic Commerce: Integrating Trust and Risk with the Technology Acceptance Model. Int. J. Electron. Commer. 2003, 7, 101–134. [Google Scholar]

- Agarwal, R.; Prasad, J. A Conceptual and Operational Definition of Personal Innovativeness in the Domain of Information Technology. Inf. Syst. Res. 1998, 9, 204–215. [Google Scholar] [CrossRef]

- Gefen, D. E-commerce: The role of familiarity and trust. Omega 2000, 28, 725–737. [Google Scholar] [CrossRef] [Green Version]

- Featherman, M.S.; Pavlou, P.A. Predicting e-services adoption: A perceived risk facets perspective. Int. J. Hum. Comput. Stud. 2003, 59, 451–474. [Google Scholar] [CrossRef] [Green Version]

- Kim, G.; Shin, B.; Lee, H.G. Understanding dynamics between initial trust and usage intentions of mobile banking. Inf. Syst. J. 2009, 19, 283–311. [Google Scholar] [CrossRef]

- Moore, G.C.; Benbasat, I. Development of an instrument to measure the perceptions of adopting an information technology innovation. Inf. Syst. Res. 1991, 2, 192–222. [Google Scholar] [CrossRef] [Green Version]

- Taylor, S.; Todd, P.A. Understanding information technology usage: A test of competing models. Inf. Syst. Res. 1995, 6, 144–176. [Google Scholar] [CrossRef]

- Legris, P.; Ingham, J.; Collerette, P. Why do people use information technology? A critical review of the technology acceptance model. Inf. Manag. 2003, 40, 191–204. [Google Scholar] [CrossRef]

- Chuttur, M.Y. Overview of the technology acceptance model: Origins, developments and future directions. Work. Pap. Inf. Syst. 2009, 9, 9–37. [Google Scholar]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: Toward a unified view. MIS Q. Manag. Inf. Syst. 2003, 27, 425–478. [Google Scholar] [CrossRef] [Green Version]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Q. Manag. Inf. Syst. 2012, 36, 157–178. [Google Scholar] [CrossRef] [Green Version]

- Yang, S.; Lu, Y.; Gupta, S.; Cao, Y.; Zhang, R. Mobile payment services adoption across time: An empirical study of the effects of behavioral beliefs, social influences, and personal traits. Comput. Hum. Behav. 2012, 28, 129–142. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Kim, C.; Mirusmonov, M.; Lee, I. An empirical examination of factors influencing the intention to use mobile payment. Comput. Hum. Behav. 2010, 26, 310–322. [Google Scholar] [CrossRef]

- Shao, Z.; Zhang, L.; Li, X.; Guo, Y. Antecedents of trust and continuance intention in mobile payment platforms: The moderating effect of gender. Electron. Commer. Res. Appl. 2019, 33, 100823. [Google Scholar] [CrossRef]

- Qasim, H.; Abu-Shanab, E. Drivers of mobile payment acceptance: The impact of network externalities. Inf. Syst. Front. 2016, 18, 1021–1034. [Google Scholar] [CrossRef]

- Dahlberg, T.; Guo, J.; Ondrus, J. A critical review of mobile payment research. Electron. Commer. Res. Appl. 2015, 14, 265–284. [Google Scholar] [CrossRef]

- Alalwan, A.A.; Dwivedi, Y.K.; Rana, N.P. Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. Int. J. Inf. Manag. 2017, 37, 99–110. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. Antecedents of the adoption of the new mobile payment systems: The moderating effect of age. Comput. Hum. Behav. 2014, 35, 464–478. [Google Scholar] [CrossRef]

- Liébana-Cabanillas, F.; Sánchez-Fernández, J.; Muñoz-Leiva, F. The moderating effect of experience in the adoption of mobile payment tools in Virtual Social Networks: The m-Payment Acceptance Model in Virtual Social Networks (MPAM-VSN). Int. J. Inf. Manag. 2014, 34, 151–166. [Google Scholar] [CrossRef]

- Zhou, T. An empirical examination of continuance intention of mobile payment services. Decis. Support Syst. 2013, 54, 1085–1091. [Google Scholar] [CrossRef]

- Kumar, A.; Adlakaha, A.; Mukherjee, K. The effect of perceived security and grievance redressal on continuance intention to use M-wallets in a developing country. Int. J. Bank Mark. 2018, 36, 1170–1189. [Google Scholar] [CrossRef]

- Luo, X.; Li, H.; Zhang, J.; Shim, J.P. Examining multi-dimensional trust and multi-faceted risk in initial acceptance of emerging technologies: An empirical study of mobile banking services. Decis. Support Syst. 2010, 49, 222–234. [Google Scholar] [CrossRef]

- Martins, C.; Oliveira, T.; Popovič, A. Understanding the internet banking adoption: A unified theory of acceptance and use of technology and perceived risk application. Int. J. Inf. Manag. 2014, 34, 1–13. [Google Scholar] [CrossRef]

- Johnson, V.L.; Kiser, A.; Washington, R.; Torres, R. Limitations to the rapid adoption of M-payment services: Understanding the impact of privacy risk on M-Payment services. Comput. Hum. Behav. 2018, 79, 111–122. [Google Scholar] [CrossRef]

- Riquelme, H.E.; Rios, R.E. The moderating effect of gender in the adoption of mobile banking. Int. J. Bank Mark. 2010, 28, 328–341. [Google Scholar] [CrossRef]

- Khalilzadeh, J.; Ozturk, A.B.; Bilgihan, A. Security-related factors in extended UTAUT model for NFC based mobile payment in the restaurant industry. Comput. Hum. Behav. 2017, 70, 460–474. [Google Scholar] [CrossRef]

- Ghezzi, A.; Renga, F.; Balocco, R.; Pescetto, P. Mobile payment applications: Offer state of the art in the Italian market. Info 2010, 12, 3–22. [Google Scholar] [CrossRef]

- Liu, Z.; Ben, S.; Zhang, R. Factors affecting consumers’ mobile payment behavior: A meta-analysis. Electron. Commer. Res. 2019, 19, 575–601. [Google Scholar] [CrossRef]

- Lu, Y.; Yang, S.; Chau, P.Y.K.; Cao, Y. Dynamics between the trust transfer process and intention to use mobile payment services: A cross-environment perspective. Inf. Manag. 2011, 48, 393–403. [Google Scholar] [CrossRef]

- Madan, K.; Yadav, R. Behavioural intention to adopt mobile wallet: A developing country perspective. J. Indian Bus. Res. 2016, 8, 227–244. [Google Scholar] [CrossRef]

- Ondrus, J.; Pigneur, Y. Towards a holistic analysis of mobile payments: A multiple perspectives approach. Electron. Commer. Res. Appl. 2006, 5, 246–257. [Google Scholar] [CrossRef]

- Zhou, T. An empirical examination of initial trust in mobile banking. Internet Res. 2011, 21, 527–540. [Google Scholar] [CrossRef]

- Kalinic, Z.; Marinkovic, V.; Molinillo, S.; Liébana-Cabanillas, F. A multi-analytical approach to peer-to-peer mobile payment acceptance prediction. J. Retail. Consum. Serv. 2019, 49, 143–153. [Google Scholar] [CrossRef]

- Zhao, H.; Anong, S.T.; Zhang, L. Understanding the impact of financial incentives on NFC mobile payment adoption: An experimental analysis. Int. J. Bank Mark. 2019, 37, 1296–1312. [Google Scholar] [CrossRef]

- Francisco, L.C.; Francisco, M.L.; Juan, S.F. Payment systems in new electronic environments: Consumer behavior in payment systems via SMS. Int. J. Inf. Technol. Decis. Mak. 2015, 14, 421–449. [Google Scholar] [CrossRef]

- Gupta, S.; Xu, H. Examining the relative influence of risk and control on intention to adopt risky technologies. J. Technol. Manag. Innov. 2010, 5, 22–37. [Google Scholar] [CrossRef] [Green Version]

- Lim, S.H.; Kim, D.J.; Hur, Y.; Park, K. An Empirical Study of the Impacts of Perceived Security and Knowledge on Continuous Intention to Use Mobile Fintech Payment Services. Int. J. Hum. Comput. Interact. 2019, 35, 886–898. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | No. Studies | Time Cited | Avg. Citations | Avg. Pub. Year | Country | No. Studies | Time Cited | Avg. Citations | Avg. Pub. Year |

|---|---|---|---|---|---|---|---|---|---|

| China | 98 | 1262 | 12.88 | 2015.60 | South Africa | 11 | 359 | 32.64 | 2017.46 |

| India | 89 | 1364 | 15.33 | 2018.19 | Finland | 10 | 1231 | 123.10 | 2013.50 |

| USA | 69 | 2733 | 39.61 | 2015.15 | France | 10 | 623 | 62.30 | 2015.40 |

| Indonesia | 42 | 144 | 3.43 | 2019.48 | Thailand | 10 | 113 | 11.30 | 2017.40 |

| Malaysia | 37 | 432 | 11.68 | 2018.92 | Pakistan | 9 | 154 | 17.11 | 2017.11 |

| UK | 35 | 1082 | 30.91 | 2015.54 | Saudi Arabia | 9 | 140 | 15.56 | 2018.78 |

| Korea | 31 | 764 | 24.65 | 2016.94 | Singapore | 9 | 234 | 26.00 | 2017.78 |

| Germany | 21 | 953 | 45.38 | 2011.38 | Viet Nam | 9 | 72 | 8.00 | 2020.44 |

| Spain | 20 | 843 | 42.15 | 2017.00 | Belgium | 8 | 205 | 25.63 | 2011.63 |

| Taiwan | 20 | 273 | 13.65 | 2014.50 | Russia | 8 | 12 | 1.50 | 2018.00 |

| Hong Kong | 17 | 247 | 14.53 | 2016.29 | United Arab Emirates | 8 | 40 | 5.00 | 2019.87 |

| Australia | 13 | 676 | 52.00 | 2014.08 | Poland | 7 | 14 | 2.00 | 2020.43 |

| Canada | 12 | 124 | 10.33 | 2017.83 | Iraq | 6 | 2 | 0.33 | 2018.50 |

| Iran | 11 | 151 | 13.73 | 2013.91 | Turkey | 6 | 87 | 14.50 | 2015.50 |

| Jordan | 11 | 70 | 6.36 | 2017.91 |

| Journal Name | Documents | Citations | Avg. Citations | Avg. Pub. Year |

|---|---|---|---|---|

| Int. J. Bank Mark. | 16 | 471 | 29.44 | 2016.88 |

| Electron. Commer. Res. Appl. | 14 | 2070 | 147.86 | 2011.21 |

| IFIP Adv. Inf. Commun. Technol. | 12 | 22 | 1.83 | 2015.50 |

| Sustain. | 11 | 83 | 7.55 | 2019.91 |

| J. Electron. Commer. Res. | 9 | 170 | 18.89 | 2015.89 |

| Int. J. e-Bus. Res. | 8 | 48 | 6.00 | 2017.50 |

| J. Retail. Consum. Serv. | 8 | 324 | 40.50 | 2020.00 |

| Int. J. Inf. Manage. | 7 | 507 | 72.43 | 2016.29 |

| Int. J. Sci. Technol. Res. | 6 | 2 | 0.33 | 2019.17 |

| J. Paym. Strategy Syst. | 6 | 4 | 0.67 | 2020.17 |

| J. Theor. Appl. Electron. Commer. Res. | 6 | 68 | 11.33 | 2016.67 |

| Journal Grade of AJG 2021 | Documents | Citations | Avg. Citations | Avg. Pub. Year |

|---|---|---|---|---|

| Grade 4* | 2 | 7 | 3.5 | 2021.00 |

| Grade 4 | 3 | 528 | 176 | 2007.00 |

| Grade 3 | 29 | 1531 | 52.79 | 2016.51 |

| Grade 2 | 67 | 4233 | 64.14 | 2016.05 |

| Grade 1 | 89 | 1315 | 14.78 | 2019.38 |

| No Grade | 401 | 2549 | 6.36 | 2015.79 |

| Author/s Name | Year | Cited By | Summary of Findings | Source Title |

|---|---|---|---|---|

| Schierz et al. [4] | 2010 | 594 | The impacts of subjective norm, individual mobility, and compatibility are all strongly supported by the empirical findings. The impact of security is well-documented. | Elect. Commer. Res. Appl. |

| Mallat [46] | 2007 | 494 | The advantages of mobile payments differ from what adoption theories suggest and include time and location independence, availability, remote payment options, a lack of critical mass, and queue avoidance. Perceived risk, complexity, and premium pricing are among the main hurdles to adoption highlighted. | J. Strategic Inform Syst. |

| Dahlberg et al. [47] | 2008 | 442 | This study presents a framework consisting of four contingency and five competitive force variables and arranges mobile payment research around each. Contemporary studies best cover consumers’ perspectives on mobile payments as well as technical security and trust. The effects of social and cultural variables on mobile payments and comparisons between mobile and traditional payment services are all topics that have yet to be researched. | Elect. Commer. Res. Appl. |

| Slade et al. [48] | 2015 | 320 | The nonusers’ intentions to embrace remote mobile payments are highly influenced by performance expectancy, social influence, innovativeness, and perceived risk, but not by effort expectancy. | Psychol. Mark. |

| Kim, Tao, et al. [49] | 2010 | 273 | A conceptual model that identifies the factors that influence consumers’ perceptions of security and trust, as well as the impact of these factors on the adoption of e-payment systems, is proposed. | Elect. Commer. Res. Appl. |

| Thakur and Srivastava [50] | 2014 | 265 | Privacy risk and security risk are found to be significant subdimensions of perceived risk. | Internet Res. |

| Au and Kauffman [51] | 2008 | 257 | This study examines a new use of technology that is gaining traction globally in conjunction with the wireless revolution: mobile payments. Although this technology application is likely to have complexities and surprises, we urge the reader to keep in mind that many of the same economic dynamics will be at play as they have been in the past with other financial services and associated technology applications. | Electronic Commerce Research and Applications |

| Morosan and DeFranco [52] | 2016 | 228 | Performance expectancy was found to be the strongest predictor of intentions to use near-field communication mobile payments, followed by hedonic motives, habit, and social factors. There are a number of key consequences for academics and industrial decision-makers. | Int. J. Hosp. Manag. |

| De Kerviler et al. [53] | 2016 | 174 | Social benefits and hedonic, utilitarian, financial, and privacy threats are major drivers from the perspective of perceived value. The authors also look at the distinctions between the drivers of more common mobile buying behaviours and emphasize the importance of experience. | J. Retail. Consum. Serv. |

| Von Solms and Naccache [54] | 1992 | 169 | Blind signatures appear to be an ideal answer in light of the increased emphasis on protecting the privacy of user data and actions in electronic systems. This research, on the other hand, looks at a flaw in blind signatures, demonstrating how a perfect solution can lead to a perfect crime. | Comput. Secur. |

| Yang et al. [12] | 2015 | 160 | The main determinants of perceived risk are confirmed to be perceived service intangibility, perceived regulatory uncertainty, perceived technology uncertainty, and perceived information asymmetry, while perceived privacy risk, perceived financial risk, and perceived performance risk were found to have strong negative effects on acceptance intention and perceived value. | Ind. Manag. Data Sys. |

| Slade et al. [55] | 2015 | 158 | The extended model explains more variance in behavioural intention, but performance expectancy remains the best predictor across both models. | J. Strateg. Mark. |

| Author/s | # GS Citations | Focus of the Study | Summary of the Findings |

|---|---|---|---|

| [75] | 4030 | The antecedents of new information technologies adoption | Only compatibility implies a considerable modification in the work behaviour of a potential adopter. |

| [72] | 45,132 | Reviewing structural equation modelling in practice | It provides guidance to substantive scholars on the use of structural equation modelling for theory building and testing. |

| [73] | 28,578 | Structural equation models | The technique comprises a concerted effort to reconcile what are referred to as objective and subjective norms. |

| [71] | 84,340 | Structural equation models | This study builds and implements testing systems based on the measurement of shared variance within the structural model to determine the explanatory power of a model. |

| [76] | 9375 | TAM | Customer trust is just as critical to online commerce as the well-established TAM usage determinants of perceived utility and perceived ease of use. |

| [74] | 6918 | TAM | The suggested model incorporates both trust and perceived risk, which are necessary considerations in light of the implicit uncertainty inherent in the e-commerce context. |

| [51] | 699 | Mobile payments | This study stresses the roles of innovators and consumers of mobile payment services, sellers and network intermediaries, as well as government regulators and standards bodies, all of which are relevant to a range of issue areas. |

| [46] | 1245 | The adoption of mobile payment | Mobile payment acceptance is shown to be dynamic and dependent on contextual variables, such as a lack of other payment options or a sense of urgency. Factors such asperceived risk, lack of critical mass, complexity, and premium cost also have a significant effect. |

| [58] | 31,696 | Computer technology acceptance | Perceived utility significantly influences people’s intentions. Perceived ease of use shows a small but substantial influence on intentions. Subjective norms have little effect on intentions. Only a part of the influence of these beliefs on intentions is mediated by attitudes. |

| [69] | 63,961 | User acceptance of information technology | Correlations between usefulness and behaviour are much stronger than those between ease of use and behaviour. Perceived ease of use may be a causal antecedent of perceived usefulness. |

| [77] | 3185 | E-service adoption | Adoption of e-services is hurt mostly by performance-related risk perceptions, and perceived ease of use of the e-service reduced these risk worries. |

| [78] | 997 | The initial trust in mobile banking and intention to use | The firm’s overall reputation was insufficient to persuade customers to use mobile banking. The proportional benefits, trust proclivity, and structural guarantees have a significant impact on early trust in mobile banking. |

| [18] | 2516 | Factors determining users’ acceptance of mobile banking | The data demonstrate that the extended TAM is highly predictive in anticipating customers’ intentions to utilise mobile banking. |

| [79] | 11,821 | The adoption of information technology innovation | The study creates a tool for assessing an individual’s different viewpoints for accepting a breakthrough in information technology. |

| [4] | 1379 | Mobile payment acceptance | The findings corroborate previous research indicating that compatibility, individual mobility, and perceived standard all have an effect on mobile payment acceptance. |

| [80] | 11,470 | Information technology usage | By concentrating on the characteristics that are most likely to affect system usage via both design and implementation tactics, the deconstructed theory of planned behaviour gives a more comprehensive account of behavioural intention. |

| [70] | 6805 | Extending of technology acceptance model into TAM3 | The initiative built a comprehensive nomological network for information technology uptake and use of TAM3. |

| [59] | 23,706 | Extending the boundaries of the technology acceptance model into TAM2 | Both cognitive instrumental processes (reported ease of use, demonstrability of results, output quality, and work relevance) and social influence processes significantly affect user approval (image, voluntariness, and subjective norm). |

| Author/s | # GS Citations | Focus of the Study | Summary of the Findings |

|---|---|---|---|

| [57] | 97,385 | The planned behaviour theory | Subjective norms, perceived behavioural control, and attitudes are all tied to suitable sets of salient behavioural control and normative beliefs about the activity, but the exact form of these beliefs is uncertain. |

| [86] | 447 | Literature review | Scholars have continued to focus on specific themes (particularly customers’ acceptance and technology elements). |

| [83] | 36,128 | UTAUT | The authors develop the UTAUT as a complete model. |

| [87] | 891 | UTAUT2 | Performance expectation, effort expectancy, trust, price value, and hedonic motivation all have a large and beneficial effect on behavioural intention. Additionally, this study aims to provide Jordanian banks with suitable standards for adopting and developing mobile banking successfully. |

| [84] | 9793 | Introducing UTAUT2 | The extensions presented in UTAUT2 resulted in a significant increase in the variation explained by behavioural intention (from 56% to 74%) and technological usage (from 40% to 5%). |

| [88] | 1392 | The drivers of intention to use mobile payment | Compatibility with existing payment systems is not a significant factor in users’ choice to accept it. Perceived simplicity of use and perceived usefulness are significant predictors of intention to utilise m-payment. |

| [89] | 418 | To assess the relative significance of several elements in the adoption of a new system of mobile payment | The user’s age introduces significant changes in the proposed links between third-party effects and the payment system’s ease of use, between perceived trust in the system and its ease of use, and between perceived trust and a favourable attitude toward the payment system’s use. |

| [90] | 219 | The acceptance of mobile payment in virtual social networks | The suggested behavioural model was changed accordingly, demonstrating that prior experience improves the likelihood of use. |

| [91] | 828 | The determinants of customer adoption and intention to recommend mobile payment | Social influence, innovativeness, performance expectations, perceived technical security, and compatibility are all expected to have a major indirect and direct impact on mobile payment acceptance and the intention to suggest these technologies. |

| [55] | 294 | The possibility of a new customer technology adoption paradigm, as well as its extension with trust and risk frameworks | Although the extended model explains a greater proportion of the variance in behavioural intention, performance expectancy remains the greatest predictor in both models. |

| [50] | 467 | To investigate the functional link between mobile payment usage intention, perceived risk, and adoption readiness | When the proposed model was evaluated, five of the six hypotheses were found to be fully supported, while one was found to be moderately supported. The invariance test revealed significant variation between users and nonusers. |

| [84] | 9158 | UTAUT2 | In comparison to UTAUT, the extensions offered in UTAUT2 resulted in a significant increase in the variation explained by behavioural intention (from 56% to 74%) as well as technological use (40 percent to 52). |

| [85] | 703 | The drivers of mobile payment adoption | While personal characteristics, social influence, and behavioural beliefs all play a role in determining mobile payment service acceptance and use, their effects on behavioural intention vary throughout stages. |

| [12] | 341 | How diverse uncertainty leads to distinct perceived risk dimensions, which impede mobile payment adoption | Perceived service intangibility, perceived regulatory uncertainty, perceived information asymmetry, and perceived technological uncertainty have all been confirmed as significant predictors of perceived risks, whereas perceived privacy risk, perceived financial risk, and perceived performance risk have all been shown to have a significant negative impact on perceived value and acceptance intention. |

| [92] | 841 | Continue to use mobile payment | The primary factor determining trust is the quality of the service, but the primary factor affecting satisfaction is the quality of the system. The quality of information and services has an effect on flow. Trust, flow, and contentment all contribute to the intention of mobile payment users to continue using it. |

| [23] | 1592 | UTAUT and task technology fit model | Social influence, task technology fit, and performance expectations all have a substantial impact on user adoption. The match of task technology with performance expectations has a substantial effect. |

| Author/s | # GS Citations | Focus of the Study | Summary of the Findings |

|---|---|---|---|

| [47] | 1060 | Mobile payment | The paper provides a paradigm comprised of four unforeseen and five competing force elements. |

| [101] | 101 | The drivers of mobile payment applications | The case studies aided in the comprehension of the primary diffusion drivers: Despite the numerous benefits associated with these services, severe inhibitory factors and adoption barriers continue to limit user uptake. |

| [103] | 698 | The usage intention of mobile payment | Trust, in conjunction with positive and negative valence variables, has an effect on behavioural intention both directly and indirectly. These effects on employees and students have considerably varying magnitudes. |

| [104] | 209 | The usage intention of mobile wallets | Social influence, performance expectancy, enabling circumstances, perceived value, perceived risk, PRS, and PBS are recognized as significant predictors of behavioural intents to use mobile wallet systems, whereas effort expectancy is identified as a statistically insignificant predictor. |

| [91] | 828 | The adoption intention of mobile payment | Social influence, performance expectations, innovativeness, compatibility, and perceived technological security are all predicted to have a significant impact on mobile payments acceptance and the desire to suggest these technologies, both directly and indirectly. |

| [105] | 297 | Mobile payment compared to others | Factors have stymied technical and commercial development through the use of a decision support system based on the Electre I multicriteria decision making process. |

| [98] | 244 | The usage intention of mobile payment | Individuals’ intentions to utilise m-payment services are favourably influenced by perceived security, visibility, relative benefit, and ease of use. Additionally, trialability and ubiquity have a good effect on an individual’s impression of security, but concerns about privacy issues have a negative effect. |

| [100] | 373 | The usage intention of the mobile payment restaurants sector | Compared to the original model of UTAUT, the suggested model has roughly 20% predictive accuracy and higher explanatory powers. This provides compelling evidence for the impacts of trust, security, and risk on consumers’ willingness to adopt NFC-based MP technology in restaurant settings. |

| [95] | 110 | The use of m-wallets | Perceived utility and perceived simplicity of use have a substantial effect on user satisfaction and desire to use m-wallets in the future. Perceived security has a considerable influence on customer happiness, while grievance resolution mitigates the influence of perceived security on the desire to continue using m-wallets. |

| [97] | 1352 | The usage intention of internet banking | The findings corroborate several of UTAUT’s hypotheses, including performance expectation, social influence, and effort expectancy, as well as the importance of risk as a greater predictor of intention. |

| [10] | 53 | Mobile wallets | We then provide a novel approach to secure mobile wallets and protect the privacy of mobile users by incorporating digital signature and pseudoidentity techniques. |

| [99] | 791 | The usage intention of mobile banking | The factors that have the most influence on people’s willingness to use mobile banking services are social risk, social norms, and utility. When it comes to their sense of usefulness, female respondents were more impacted by ease of use than male, while male respondents were more influenced by relative advantage. |

| [21] | 138 | Satisfaction with mobile wallets | There is a strong correlation between mobile wallet users’ perceptions, preferences, and satisfaction. Additionally, the data demonstrate the effect of consumers’ perception, happiness, and preference on mobile wallets adoption in India. |

| [106] | 561 | The usage intention of mobile banking | Initial trust is mostly determined by structural assurance and information quality; however, perceived utility is greatly influenced by information quality and system quality. Initial trust has an effect on perceived usefulness, and both variables are associated with the desire to utilise mobile banking. |

| [96] | 1271 | Emerging IT artefacts | Risk perception, which is comprised of eight distinct dimensions, is a significant predictor of new technology uptake. Apart from previous research, the findings give empirical support for the use of personal characteristic variables in assessing the adoption of developing IT artefacts. |

| [64] | 748 | The validation of a complete consumer acceptance model of mobile payment | The model validates the conventional function of technology adoption factors. The users’ attitudes and intentions are impacted by perceived security and trust. Demographics have a significant moderating influence on the correlations between the variables, as demonstrated by the extended model. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sahi, A.M.; Khalid, H.; Abbas, A.F.; Zedan, K.; Khatib, S.F.A.; Al Amosh, H. The Research Trend of Security and Privacy in Digital Payment. Informatics 2022, 9, 32. https://doi.org/10.3390/informatics9020032

Sahi AM, Khalid H, Abbas AF, Zedan K, Khatib SFA, Al Amosh H. The Research Trend of Security and Privacy in Digital Payment. Informatics. 2022; 9(2):32. https://doi.org/10.3390/informatics9020032

Chicago/Turabian StyleSahi, Alaa Mahdi, Haliyana Khalid, Alhamzah F. Abbas, Khaled Zedan, Saleh F. A. Khatib, and Hamzeh Al Amosh. 2022. "The Research Trend of Security and Privacy in Digital Payment" Informatics 9, no. 2: 32. https://doi.org/10.3390/informatics9020032

APA StyleSahi, A. M., Khalid, H., Abbas, A. F., Zedan, K., Khatib, S. F. A., & Al Amosh, H. (2022). The Research Trend of Security and Privacy in Digital Payment. Informatics, 9(2), 32. https://doi.org/10.3390/informatics9020032