4.1. Correlation Analysis

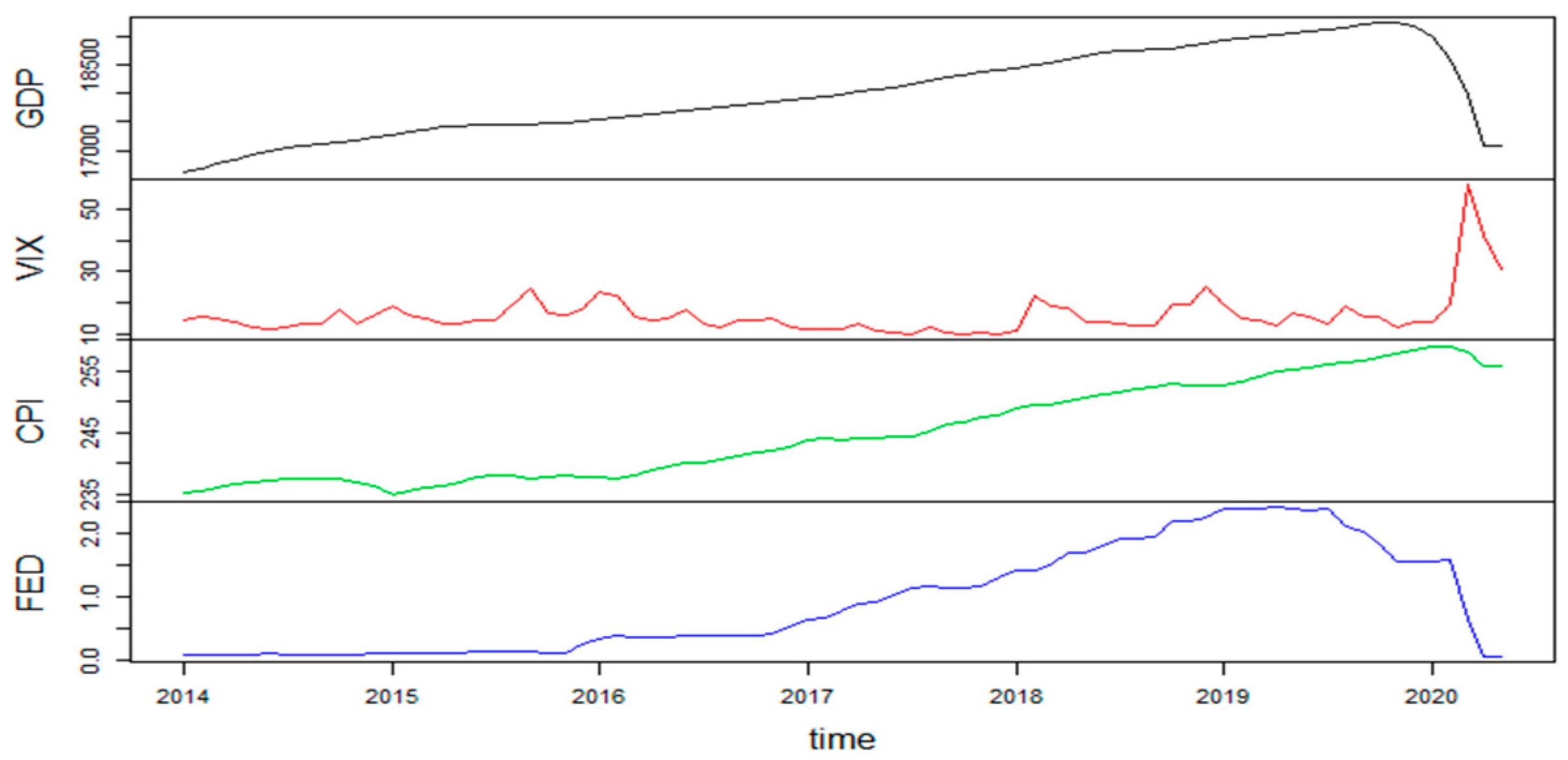

We start by motivating our choice of the macroeconomic variables GDP, CPI, and FED and the fear index VIX. To show that these four variables are able to capture the dynamics of the smart beta values, we use the following dynamic regression model:

Here, the error process,, in model (9) is described by the ARIMA(p, d, q) model in Equation (10), is a white noise series, and B is the backward shift operator (i.e., B = ). Specifically, p is the order of the autoregressive part, d is the order of the first differencing involved, and q is the order of the moving average part.

We apply model (9) and (10) to analyze the smart beta prices, , i = 1, 2, …, N, where N is the number of different smart betas considered. For any smart beta, the dependent variable, , is chosen in two different ways:

(a) the ratio between two consecutive prices of a smart beta (smart beta price ratio for short):

(b) the smart beta log-return:

We determine the best ARIMA process using the R function auto.arima() (see, Time Series Analysis with Auto.Arima in R|by Luis Losada|Towards Data Science for further details on the package).

Model (9) and (10) manages all spurious effects in the time series such as the presence of autocorrelation in the residuals. We consider the logarithm of the GDP to scale the value.

We have applied model (9) and (10) to the smart beta prices as a dependent variable and also investigated the dynamic regression of the smart beta price ratio as a dependent variable and macroeconomic variable. However, the results of these models provide weaker evidence of the link between smart beta and macroeconomics variables than the evidence of model (9) and (10) with dependent variables (a) and (b).

Table 3 shows the log-likelihood value (ML), AIC (Akaike) value, the standard error of the white noise (SE), and the coefficients associated with models (9) and (10).

The results displayed in

Table 3 show that the explanatory variables are closely related to the prices and log-prices of the smart betas.

Table A1 in

Appendix A shows the results related to the autocorrelation in the residuals according to the Ljung-Box test. The estimated model violates the assumption of no autocorrelation in the errors in the cases of Min. Vol. price ratio and log returns as dependent variables for the period January 2014–May 2014 (Panel A); the coefficients are significant due to the unit-root problem, while some information is missed in the model. In the same

Appendix A,

Table A3 and

Table A4 show the results of a lagged model to display the robustness of the results.

In general, COVID-19 leaves the relationship between smart beta and GDP or VIX more or less unchanged, but it reinforces the connection between the smart betas price ratio and the inflation/FED rate (see

Table 3 Panel B, top and middle panels). This situation can be explained by the fact that smart betas act as “defenders” with respect to market anomalies, allowing for extra returns during times of crisis.

To obtain further evidence of this finding, we investigate the linear relationship between smart beta returns and the macroeconomic variables and VIX using the Pearson correlation. The results are displayed in

Table 4.

The results show that there is a statistically significant correlation between the returns of all smart beta products and the VIX index, while the macroeconomic variables do not show significant correlations with smart betas except for the correlation between the FED rate and Quality ETF.

All significant coefficients are negative, which means that when market volatility increases, i.e., VIX increases, smart beta returns tend to fall and vice versa. Negative correlations are realistic due to the financial leverage of VIX and the US S&P 500 index. In particular, the negative correlation in the VIX/Size ETF pair may be due to the fact that small capitalization stocks are less liquid by nature. In the presence of a liquidity shortage that exacerbates spikes in the VIX index

4, investors are induced to sell for fear of not being able to sell if the returns continue to fall.

VIX is a purely financial index that highlights the behavior and expectations of financial operators. Therefore, a considerable linear dependence with this index suggests the existence of a strong link between factors and the financial market.

In contrast, there is no linear dependence with the series most representative of economic cycle trends. Periods of expansion or recession, characterized by positive or negative GDP growth, as well as expansive or restrictive monetary policy (decrease or increase of the FED rate) or periods of inflation or deflation (increase or decrease in CPI) do not directly impact the performance of smart betas.

This is interesting for asset allocation purposes since only the smart beta returns seem to lead to a portfolio closely related to the VIX index. Is this true? Indeed, we expect a connection between a portfolio of smart betas and macroeconomic variables when a suitable allocation strategy is implemented.

Our main finding is that this linkage is hidden in the portfolio weight dynamics when the asset allocation is managed through a suitable compromise of risk and return.

Therefore, in contrast to smart beta returns, investing the optimal weights of a self-financing portfolio only in smart beta products and managing them with a prudent strategy shows significant correlations with the macroeconomic variables considered.

This expectation is motivated by two facts. On the one hand, smart beta price ratios and log returns are closely related to the macroeconomic variables (see

Table 3 Panel A/B, top and middle panels). On the other hand, the macroeconomic variables cannot be assimilated into speculative assets so prudent strategies should reveal the connection.

As illustrated in

Section 2, the liquidation of the entire portfolio when the rehedging rule is satisfied is implemented to force the hidden link between portfolio strategy and macroeconomic variables to emerge. In fact, thanks to this liquidation, rehedging accounts for the dynamics of all smart betas, thus indirectly accounting for the economic dynamics captured by the factors underlying the smart betas.

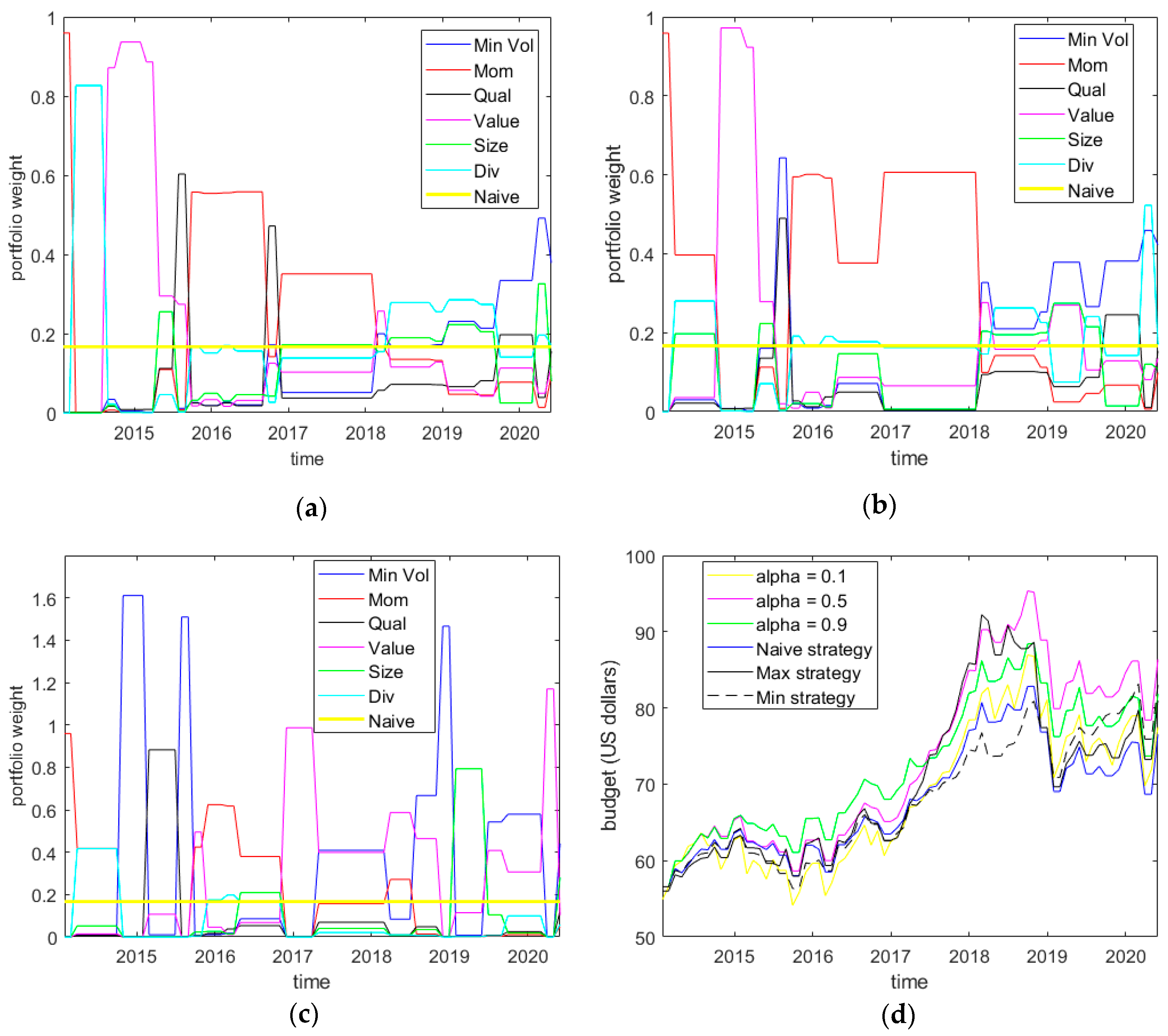

Hence, we first determine a strategy to reduce the correlation between VIX and portfolio weights and, then we analyze the portfolio weight dynamics as a function of the risk-aversion coefficient α. To pursue the first goal, we utilize three parameters: the largest admissible loss, γ, the largest admissible gain, ν, and the tail size, ψ, of the risk measure R; the risk-aversion coefficient α is used for the second objective.

As mentioned in the previous section, the largest loss and gain are fixed at 1% and 5%, respectively. These choices are prudent but rather realistic when no transaction costs are applied (see

Shelton 2017), while the parameter α is used to understand the relationship between macroeconomic variables and risk aversion after reducing/eliminating the correlation with VIX. Therefore, the tail size, ψ, is determined to minimize the correlation between portfolio weights and the VIX index. To this end, we select the highest level of risk aversion (i.e., α = 0) and we consider different risk scenarios, choosing ψ equal to 0.6, 0.7, 0.8, and 0.9. The results are reported in

Table 5.

Table 5 (Panel A and B) shows that when ψ moves from 0.60 to 0.90 and α = 0, the optimal weights of the smart beta portfolio are correlated with the VIX series up to ψ = 0.7, while this correlation disappears for larger values of ψ; that is, we do not find values statistically different from zero expect for those highlighted in gray.

This suggests that allowing for a higher probability of extreme losses not rewarded by higher returns because α is set to zero leads to a connection between weights and financial series that is volatile by nature. By adding the COVID period, the weights of Min. Vol. are correlated with VIX for higher values of ψ, while the link between the weights of Size and VIX remains unchanged suggesting that investors look for an extra return tied to less volatile assets.

We fix ψ = 0.8 and pursue the second objective; that is, we analyze the market timing portfolio as a function of the risk-aversion parameter α.

Table 6 shows correlations between smart beta weights and VIX for ψ = 0.8 and different values of α, specifically,

. This is done to determine the values of the risk-aversion parameter, α, that make the portfolio dynamics uncorrelated with the fear index. These portfolio dynamics are worth further investigation to show the connection with the macroeconomic variables.

These correlations show that in moving towards scenarios more focused on profit, i.e., α closer to 1, the optimal weights of smart beta Size and VIX become more correlated; for lower values of α, however, investors are prone to invest in less volatile assets, i.e., minimum volatility product.

With regard to

Table A7(a) and

Table A8(a) in the

Appendix B, note that the minimum volatility index is significantly and positively correlated with all the variables for more risk-averse investors (α = 0.1), i.e., an increase in GDP, CPI, FED, or VIX favors exposure to minimum volatility products, which allows higher market volatility to be contained in a crisis period characterized by the COVID-19 pandemic. Considering correlations of strategy size also leads to the same conclusion. The months of the COVID pandemic justify the negative correlation between the weights of the momentum strategy and macroeconomic/financial variables reflecting the tendency of investors to overreact to bad news regardless the value of alpha.

When we consider a portfolio entirely invested in financial ETFs

5, the analysis of correlations shows similar results. ETF returns are correlated only with the VIX series, as shown in

Table 7.

According to the correlation of optimal weights, ETFs are correlated with VIX only for ψ = 0.7, 0.9 when α = 0 as reported in

Table 8.

Nevertheless, for ψ = 0.8, the relationship between ETFs and VIX occurs for lower values of α if we consider the time period excluding the COVID-19 pandemic (

Table 9, Panel A).

Comparing Panels A and B in

Table 9, the COVID period causes a move toward global (IXG) rather than local (IYF) ETFs, increasing significant links between the weights of IXG and VIX.

In

Appendix B,

Table A7(b) and

Table A8(b) show correlations between the optimal weights and macroeconomic/financial time series considering α = 0.1, 0.9. The results show that for higher values of α, ETFs tend to be positively tied to the VIX variable; to obtain more remunerative portfolios, ETFs consider financial indices. On the contrary, the strategy of market timing on smart beta considers fluctuations of the economy as a whole.

We conclude by showing that the portfolio of the smart beta portfolio reveals the close link between these ETFs and the macroeconomic variables. To do so, we assess the link between the portfolio of smart betas and macroeconomic variables using the dynamic regression:

Here, as in the previous model, the error process,, in model (11) is described by ARIMA (p, d, q) model (i.e., Equation (12)), is a white noise series, B is the backward shift operator (i.e., B = ). Specifically, p is the order of the autoregressive part, d is the order of the first differencing involved and q the order of the moving average part. The dependent variable, is the portfolio ratio . We determine the best ARIMA process using the R function auto.arima().

Specifically, we test model (11)–(12) on portfolios of smart betas and financial ETFs for α = 0.1, 0.9 and ψ = 0.8. Model (11)–(12) is estimated by selecting the best ARIMA model that guarantees the error

to be white noise. In

Appendix A Table A2, we show the optimal choie of ARIMA model and the results of the Ljung-Box test. Moving from Panel A to Panel B in

Table 10, note that the portfolio of smart betas remains tied to the VIX index for any level of risk aversion considered, but reinforcing the link between all other macroeconomic variables considered in the analysis. In a crisis period, the smart beta strategy reduces the speculative aspect of the portfolio, increasing the relationship with macroeconomic variables especially for less risk-averse individuals, where GDP, CPI, and FED show significant coefficients (for α = 0.9 CPI is not significant).

Table A2 in the

Appendix A shows that in the case of financial ETF portfolios, the model violates the assumption of no autocorrelation in the residuals for α = 0.1, meaning that information is missed in the estimated model. The macroeconomic variables considered are not sufficient to explain the portfolio dynamics.

4.3. Forecasting via a Linear Discriminant Analysis

As mentioned in the previous sections, our proposed practical strategy permits to re-hedge portfolios only when it is possible to capitalize monthly gains (G) or losses (L), otherwise the portfolio is not updated (N). Thus, these three different occurrences are interpreted as a qualitative variable, named “tilting” variable, whose categories, G, L, N, depend on the smart beta dynamics.

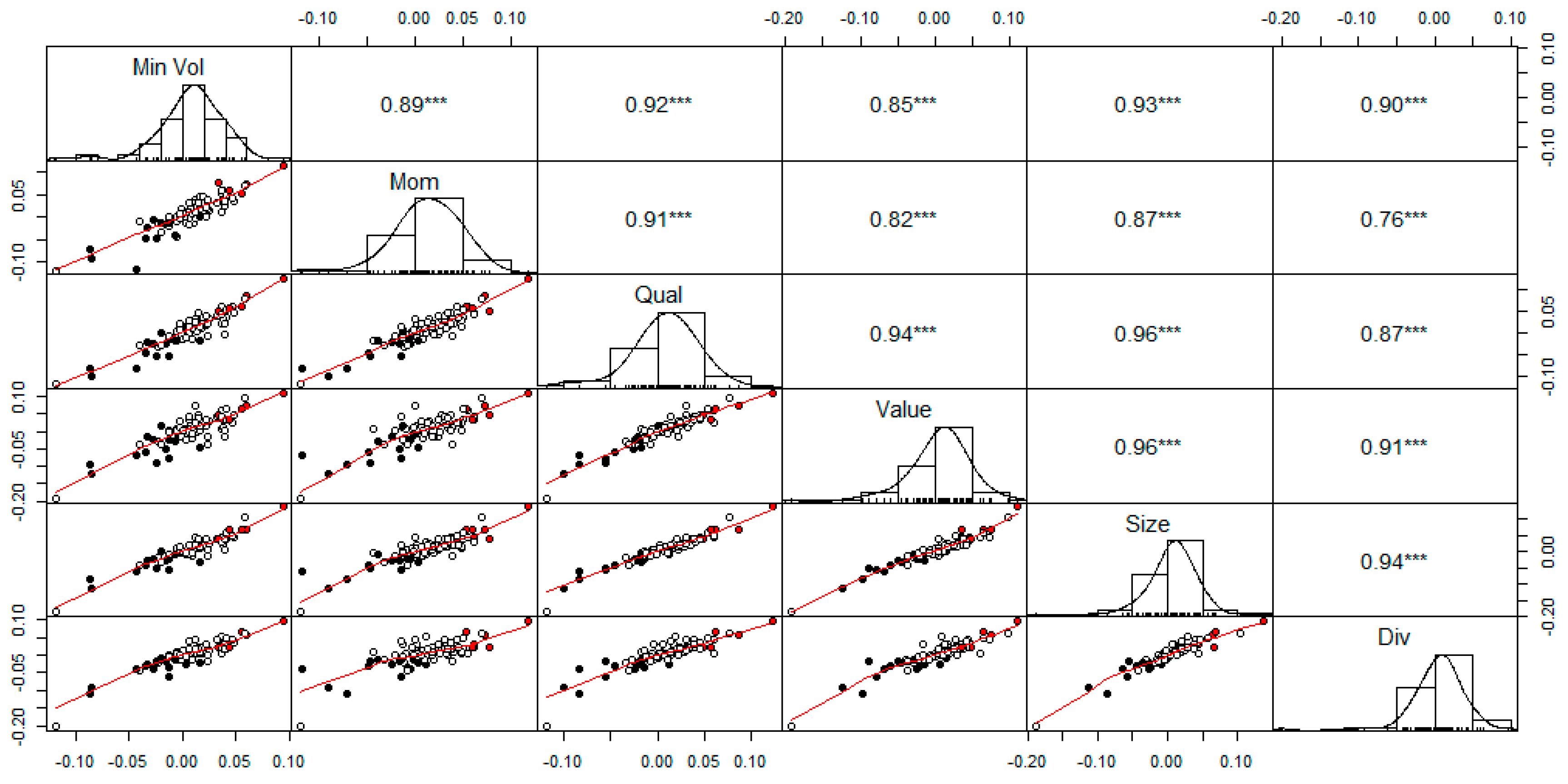

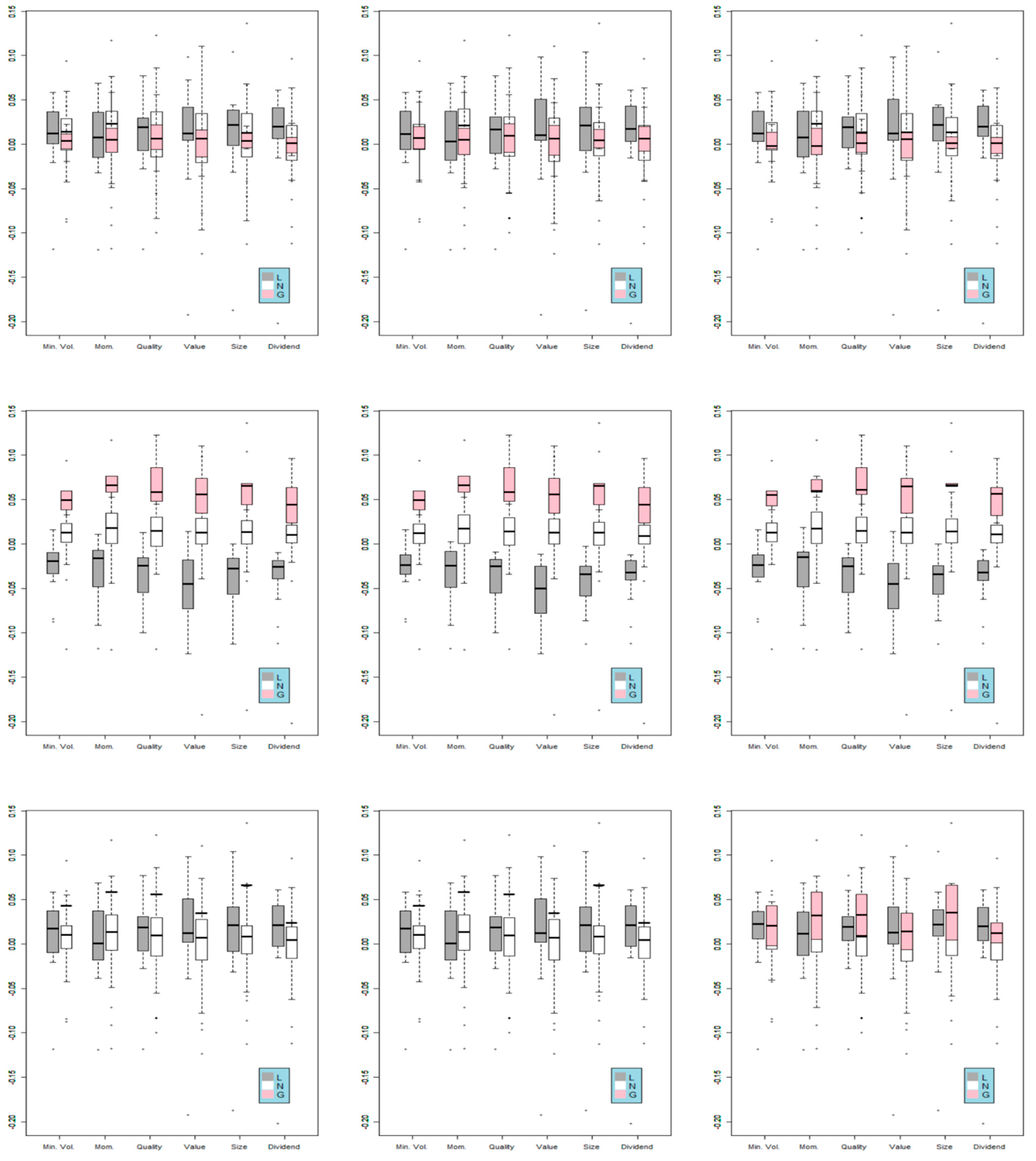

We investigate whether these three modes of the tilting variable can be distinguished through the observed smart beta returns. As shown in

Figure 4, we start analyzing the bivariate scatter plot to determine pairs of smart beta showing high performance in discriminating losses and gains. From

Figure 4, note that some smart betas better discriminate between gains and losses, or respectively from red to black circles, such as dividend and minimum volatility products regardless of other factor strategies coupled.

Since the tilting variable strongly depends on the threshold values, linear discriminant analysis (LDA) enables interesting results regarding these values in order to update portfolio weights and portfolio forecasting strategy.

Moreover,

Figure 5 shows an analysis of the returns according to tilting variable for different values of gain threshold, γ (2.5%, 5%, and 7.5%) and a fixed loss threshold, ν, of 1% to update portfolio weights.

The situation does not change if we consider different values of α (from left to right: 0.1, 0.5, 0.9) within each gain threshold. Differences can be seen between thresholds; indeed, when we consider a gain threshold value of 5% (middle panel), the average of smart beta products fluctuates around the loss and gain threshold values, 1% and 5%, respectively, or around 0 when the better strategy is represented by not rehedging.

Gain thresholds of 2.5% and 7% are not discriminant for the tilting variable: most of the time gains and losses are not distinguishable.

In addition, for each threshold, smart betas with small variances are more discriminant with respect to the tilting variable. For example, in the case of a gain threshold of 5%, Min. Vol., Mom, and Size products play an important role in gain capitalization, while Div products are important in the case of loss capitalization.

Table 11 confirms the fact that values set to 1% and 5% are reasonable and good discriminant thresholds to get portfolio dynamics “predictable and well-performing” for the values of α considered. This table shows scores associated with the first dimension of LDA according to different values of gain threshold.

Note that higher values of the first LDA coefficient are associated with the gain threshold of 5% regardless the value of α considered. This finding suggests that a gain threshold of 5% is the best choice to update portfolio weights according to Equation (2) and consequently, to detect a link between macroeconomic variables and smart betas.

The accuracy of the LDA described in

Table 12 shows that the results are robust when lagged returns are considered in the analysis.

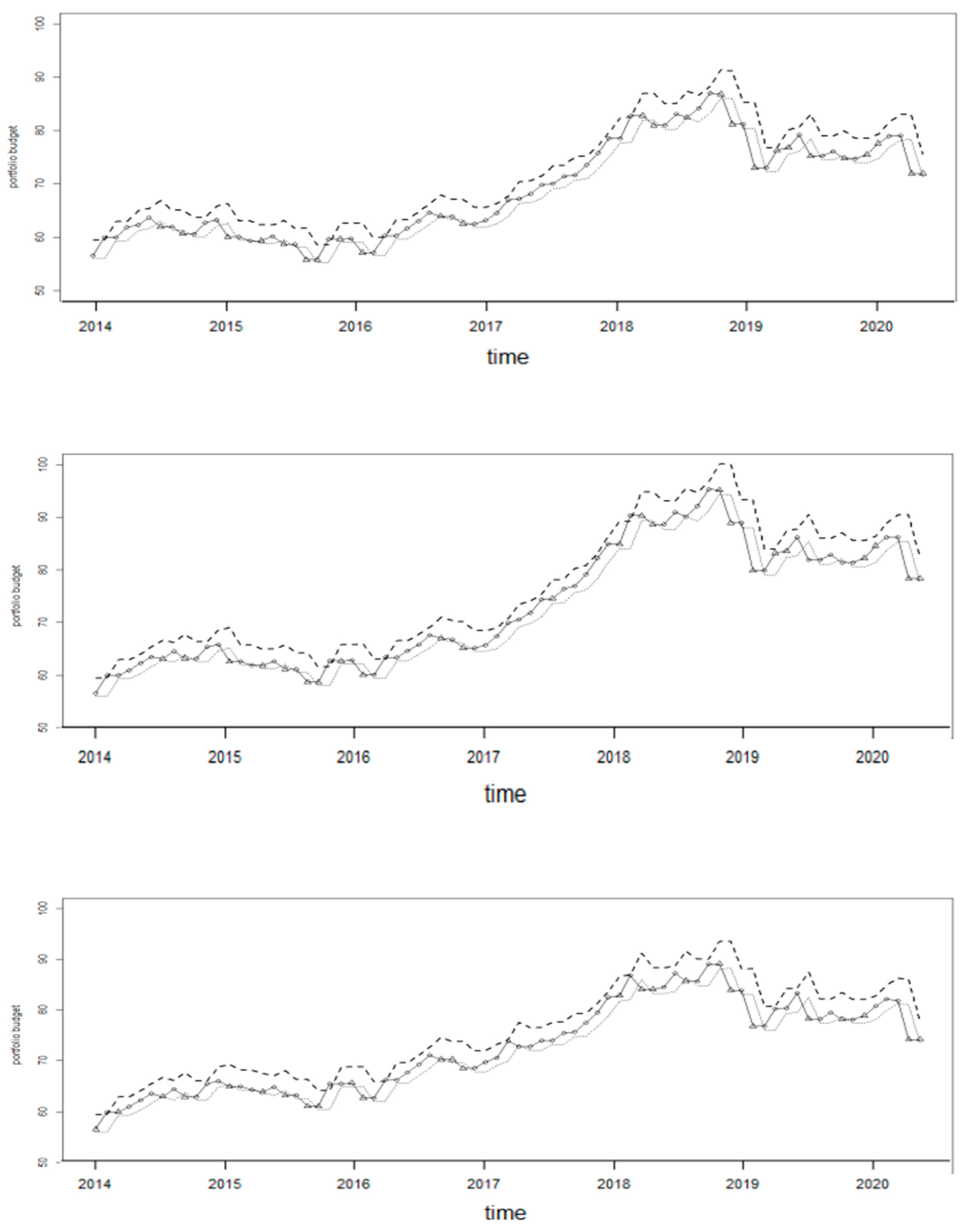

Moreover, we merge the two categories (gain and loss) of the tilting variable into the “rehedging” category in contrast to the “not rehedging” category to show results regarding the portfolio forecasting (see

Figure 6)

7.

The forecasting of portfolio rehedging is correct when triangles are out of the interval defined by lower and upper bounds, while the forecasting of the “not rehedging” is correct when the circle falls in the interval. Right prediction, i.e., triangles match budget out of bounds and circles budget within the bounds, occurs most of the time. Specifically, the accuracy of predictions is 79%, 72%, and 79% respectively for α = 0.1, 0.5 and 0.9.

The results of the LDA prediction based on the lagged smart beta returns allow us to detect the appropriate strategy represented by updating or not updating the portfolio weights one month in advance.

This fact emerges from

Figure 6, which shows that the prediction of the appropriate strategy of rehedging at time t effectively occurs when the true value of the portfolio budget is above or below the threshold bounds most of the time.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}