Dataset Modelling of the Financial Risk Management of Social Entrepreneurship in Emerging Economies

Abstract

:1. Introduction

2. Materials and Methods

2.1. Theoretical Basis, Literature Review and Gap Analysis

2.2. Methodology and Empirical Basis of the Research

3. Results

- −

- reduction in stimuli for using financial resources in long-term investments, which disrupts stability and decreases inclusion: an increase in msr1 of 1 point leads to an increase in the social entrepreneurship index of 0.1693 points;

- −

- joint public–private investments; reduction in investments in R&D: an increase in msr2 of 1 point leads to a decrease in the social entrepreneurship index of 0.3647 points;

- −

- decrease in investment in R&D: increase in msr3 of 1 point leads to an increase in the social entrepreneurship index of 0.3685 points;

- −

- expand investment in the skills needed for jobs and “markets of tomorrow”: increase in msr1 of 1 point leads to an increase in the social entrepreneurship index of 0.4548 points.

4. Discussion

- −

- reduction of stimuli for using financial resources in long-term investments, which disrupts the stability and decreases inclusion;

- −

- joint public–private investments; decrease in investments in R&D;

- −

- expand investment in the skills needed for jobs and the “markets of tomorrow”.

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Conflicts of Interest

References

- Alam, Shahriar Tanvir, Sayem Ahmed, Syed Mithun Ali, Sudipa Sarker, Golam Kabir, and Asif Ul-Islam. 2021. Challenges to COVID-19 vaccine supply chain: Implications for sustainable development goals. International Journal of Production Economics 239: 108193. [Google Scholar] [CrossRef] [PubMed]

- Al-Omoush, Khaled Saleh, VIrginia Simón-Moya, Mohammad Atwah Al-ma’aitah, and Javier Sendra-García. 2021. The determinants of social CRM entrepreneurship: An institutional perspective. Journal of Business Research 132: 21–31. [Google Scholar] [CrossRef]

- Azmat, Fara, Ameeta Jain, and Fabienne Michaux. 2021. Strengthening impact integrity in investment decision-making for sustainable development. Sustainability Accounting, Management and Policy Journal. [Google Scholar] [CrossRef]

- Bakos, Levente, and Danut Dumitrascu Dumitrașcu. 2021. Decentralized enterprise risk management issues under rapidly changing environments. Risks 9: 165. [Google Scholar] [CrossRef]

- Bouri, Elie, Riza Demirer, Rangan Gupta, and Jacobus Nel. 2021. Covid-19 pandemic and investor herding in international stock markets. Risks 9: 168. [Google Scholar] [CrossRef]

- Cardella, Giuseppina Maria, Brizeida Raquel Hernández-Sánchez, Alcides Almeida Monteiro, and Jose Carlos Sánchez-García. 2021. Social entrepreneurship research: Intellectual structures and future perspectives. Sustainability 13: 7532. [Google Scholar] [CrossRef]

- Chandra, Yanto, Fandy Tjiptono, and Andhy Setyawan. 2021. The promise of entrepreneurial passion to advance social entrepreneurship research. Journal of Business Venturing Insights 16: e00270. [Google Scholar] [CrossRef]

- Chen, Bingyao. 2021. Public-private partnership infrastructure investment and sustainable economic development: An empirical study based on efficiency evaluation and spatial spillover in china. Sustainability 13: 8146. [Google Scholar] [CrossRef]

- Dalwai, Tamanna, and Mahdi Salehi. 2021. A business strategy, intellectual capital, firm performance, and bankruptcy risk: Evidence from Oman’s non-financial sector companies. Asian Review of Accounting 29: 474–504. [Google Scholar] [CrossRef]

- Duygun, Meryem, Daniel Ladley, and Mohamed Shaban. 2020. Challenges to global financial stability: Interconnections, credit risk, business cycle and the role of market participants. Journal of Banking and Finance 112: 105735. [Google Scholar] [CrossRef]

- Elkhal, Khaled. 2019. Business uncertainty and financial leverage: Should the firm double up on risk? Managerial Finance 45: 536–44. [Google Scholar] [CrossRef]

- Fhiri, Nur Suriaty Daud, Shuhairimi Abdullah, Yasmin Ahmad, Noor Salwani Hussin, Jamsari Jamaluddin, and Abdul Jalil Ramli. 2021. Social entrepreneurship: Environmental sustainability. AIP Conference Proceedings 2339: 020237. [Google Scholar] [CrossRef]

- Fridhi, Bechir. 2021. Social entrepreneurship and social enterprise phenomenon: Toward a collective approach to social innovation in Tunisia. Journal of Innovation and Entrepreneurship 10: 14. [Google Scholar] [CrossRef]

- Galindo-Martín, Miguel-Ángel, Maria-Soledad Castaño-Martínez, and Maria-Teresa Méndez-Picazo. 2021. Effects of the pandemic crisis on entrepreneurship and sustainable development. Journal of Business Research 137: 345–53. [Google Scholar] [CrossRef] [PubMed]

- Graafland, Johan, and Thomas R. Wells. 2021. In Adam Smith’s Own Words: The Role of Virtues in the Relationship Between Free Market Economies and Societal Flourishing, A Semantic Network Data-Mining Approach. Journal of Business Ethics 172: 31–42. [Google Scholar] [CrossRef]

- Hassani, Hossein, Xu Huang, Steve MacFeely, and Mohammad Reza Entezarian. 2021. Big data and the united nations sustainable development goals (UN SDGs) at a glance. Big Data and Cognitive Computing 5: 28. [Google Scholar] [CrossRef]

- He, Chen, and Gujun Yan. 2020. Path selections for sustainable development of green finance in developed coastal areas of China. Journal of Coastal Research 104 (Suppl. 1): 77–81. [Google Scholar] [CrossRef]

- Institute of Scientific Communications. 2021. Dataset “Social Entrepreneurship in the Global Economy: From Virtual Scores to Big Data”. Available online: https://iscvolga.ru/dataset-social-predprinim (accessed on 9 August 2021).

- Kliestik, Tomas, Maria Misankova, Katarina Valaskova, and Lucia Svabova. 2018. Bankruptcy prevention: New effort to reflect on legal and social changes. Science and Engineering Ethics 24: 791–803. [Google Scholar] [CrossRef]

- Kovacova, Maria, Tomas Kliestik, Katarina Valaskova, Pavol Durana, and Zuzana Juhaszova. 2019. Systematic review of variables applied in bankruptcy prediction models of Visegrad group countries. Oeconomia Copernicana 10: 743–72. [Google Scholar] [CrossRef] [Green Version]

- Lasloom, Nasser Mohammed. 2021. The Inevitability of Financial Risks in Businesses and How to Overcome Them: Saudi Arabia in Focus. Smart Innovation, Systems and Technologies 227: 815–24. [Google Scholar] [CrossRef]

- Lee, Jung Wan. 2020. Green finance and sustainable development goals: The case of China. Journal of Asian Finance, Economics and Business 7: 577–86. [Google Scholar] [CrossRef]

- Locurcio, Marco, Francesco Tajani, Pierluigi Morano, Debora Anelli, and Benedetto Manganelli. 2021. Credit risk management of property investments through multi-criteria indicators. Risks 9: 106. [Google Scholar] [CrossRef]

- Méndez-Picazo, Maria-Teresa, Miguel-Angel Galindo-Martín, and Maria-Soledad Castaño-Martínez. 2021. Effects of sociocultural and economic factors on social entrepreneurship and sustainable development. Journal of Innovation and Knowledge 6: 69–77. [Google Scholar] [CrossRef]

- Moscow Exchange. 2021a. Sustainable Development Vector Index (MRSV). Available online: https://www.moex.com/ru/index/MRSV/archive/#/from=2019-10-01&till=2021-11-11&sort=TRADEDATE&order=desc (accessed on 9 August 2021).

- Moscow Exchange. 2021b. Moscow Exchange Index (IMOEX). Available online: https://www.moex.com/ru/index/IMOEX/archive/#/from=2020-09-21&till=2021-11-11&sort=TRADEDATE&order=desc (accessed on 9 August 2021).

- Popkova, Elena, Piper DeLo, and Bruno Sergi. 2020. Corporate Social Responsibility Amid Social Distancing During the COVID-19 Crisis: BRICS vs. OECD Countries. Research in International Business and Finance 55: 101315. [Google Scholar] [CrossRef] [PubMed]

- Sabău, Andrada-Ioanna, Codruta Mare, and Ioanna Lavinia Safta. 2021. A statistical model of fraud risk in financial statements. Case for Romania companies. Risks 9: 116. [Google Scholar] [CrossRef]

- Sahrakorpi, Tiia, and Venkata Bandi. 2021. Empowerment or employment? Uncovering the paradoxes of social entrepreneurship for women via Husk Power Systems in rural North India. Energy Research and Social Science 79: 102153. [Google Scholar] [CrossRef]

- Sebestyén, Viktor, and Janos Abonyi. 2021. Data-driven comparative analysis of national adaptation pathways for Sustainable Development Goals. Journal of Cleaner Production 319: 128657. [Google Scholar] [CrossRef]

- Setiawan, Hari Harjanto, Mu’man Nuryana, Badrun Susantyo, Agus Budi Purwanto, and Muhammad Belanawane Sulubere. 2021. Social entrepreneurship for beneficiaries of the Program Keluarga Harapan (PKH) toward sustainable development. IOP Conference Series: Earth and Environmental Science 739: 012053. [Google Scholar] [CrossRef]

- Shao, Jinhua, Brayan Tillaguango, Rafael Alvarado, Santiago Ochoa-moreno, and Johanna Alvarado-Espejo. 2021. Environmental impact of the shadow economy, globalisation, trade and market size: Evidence using linear and non-linear methods. Sustainability 13: 6539. [Google Scholar] [CrossRef]

- Staszkiewicz, Piotr, and Alaksander Werner. 2021. Reporting and disclosure of investments in sustainable development. Sustainability 13: 908. [Google Scholar] [CrossRef]

- Suseno, Yuliani, and Ling Abbott. 2021. Women entrepreneurs’ digital social innovation: Linking gender, entrepreneurship, social innovation and information systems. Information Systems Journal 31: 717–44. [Google Scholar] [CrossRef]

- Syed, Ali Murad, and Hana Saeed Bawazir. 2021. Recent trends in business financial risk—A bibliometric analysis. Cogent Economics and Finance 9: 1913877. [Google Scholar] [CrossRef]

- Tabares, Sabrina. 2021. Certified B corporations: An approach to tensions of sustainable-driven hybrid business models in an emerging economy. Journal of Cleaner Production 317: 128380. [Google Scholar] [CrossRef]

- Tang, Min, Peihan Liu, Xiangrui Chao, and Zhenglin Han. 2021. The performativity of city resilience for sustainable development of poor and disaster-prone regions: A case study from China. Technological Forecasting and Social Change 173: 121130. [Google Scholar] [CrossRef]

- Thörnqvist, Christer, and Jonna Kilstam. 2021. Aligning Corporate Social Responsibility with the United Nations’ Sustainability Goals: Trickier than it Seems? A Study of Social Entrepreneurship in Sweden. Economics 9: 161–77. [Google Scholar] [CrossRef]

- Ullah, Hafeez, Zhuquan Wang, Shahid Bashir, Abdul Razzaq Khan, Madiha Riaz, and Nausheen Syed. 2021. Nexus between IT capability and green intellectual capital on sustainable businesses: Evidence from emerging economies. Environmental Science and Pollution Research 28: 27825–43. [Google Scholar] [CrossRef] [PubMed]

- World Bank. 2021. Doing Business: Rating of Countries 2020. Available online: https://russian.doingbusiness.org/ru/rankings (accessed on 9 August 2021).

- World Economic Forum. 2021. Global Competitiveness Report Special Edition 2020: How Countries are performing on the Road to Recovery. Available online: https://www.weforum.org/reports/the-global-competitiveness-report-2020 (accessed on 9 August 2021).

- Wut, Tai-Ming, Wai-Tung Chan, and Stephanie W. Lee. 2021. Unconventional entrepreneurship: Women handicraft entrepreneurs in a market-driven economy. Sustainability 13: 7261. [Google Scholar] [CrossRef]

- Zhang, Bufan, and Yifeng Wang. 2021. The Effect of Green Finance on Energy Sustainable Development: A Case Study in China. Emerging Markets Finance and Trade 57: 3435–54. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country Category | Country | Receipt of Credits | Protection of Minority Investors | Taxation | Solution to Non-Solvency |

|---|---|---|---|---|---|

| Fr1 | Fr2 | Fr3 | Fr4 | ||

| Developing countries | Argentina | 104 | 61 | 170 | 111 |

| Brazil | 104 | 61 | 184 | 77 | |

| Chile | 94 | 51 | 86 | 53 | |

| China | 80 | 28 | 105 | 51 | |

| India | 25 | 13 | 115 | 52 | |

| Indonesia | 48 | 37 | 81 | 38 | |

| Mexico | 11 | 61 | 120 | 33 | |

| Russia | 25 | 72 | 58 | 57 | |

| Slovakia | 48 | 88 | 55 | 46 | |

| South Africa | 80 | 13 | 54 | 68 | |

| Turkey | 37 | 21 | 26 | 120 | |

| Developed countries | Finland | 132 | 72 | 95 | 65 |

| New Zealand | 1 | 3 | 9 | 36 | |

| Sweden | 80 | 28 | 31 | 17 | |

| Austria | 94 | 37 | 44 | 22 | |

| Japan | 94 | 57 | 51 | 3 | |

| Denmark | 48 | 28 | 8 | 6 | |

| France | 104 | 45 | 61 | 26 | |

| Ireland | 48 | 13 | 4 | 19 | |

| Israel | 48 | 18 | 13 | 29 | |

| Belgium | 67 | 45 | 63 | 9 | |

| Australia | 4 | 57 | 28 | 20 | |

| Estonia | 48 | 79 | 12 | 54 | |

| Netherlands | 119 | 79 | 22 | 7 | |

| Italy | 119 | 51 | 128 | 21 | |

| Germany | 48 | 61 | 46 | 4 | |

| Republic of Korea | 67 | 25 | 21 | 11 | |

| Canada | 15 | 7 | 19 | 13 | |

| UK | 37 | 7 | 27 | 14 | |

| Greece | 119 | 37 | 72 | 72 | |

| Portugal | 119 | 61 | 43 | 15 | |

| Poland | 37 | 51 | 77 | 25 | |

| Spain | 80 | 28 | 35 | 18 | |

| Switzerland | 67 | 105 | 20 | 49 | |

| Czech Republic | 48 | 61 | 53 | 16 | |

| Hungary | 37 | 97 | 56 | 66 | |

| USA | 4 | 36 | 25 | 2 |

| Country Category | Country | Increase Incentives to Direct Financial Resources towards Long-Term Investments, Strengthen Stability and Expand Inclusion | Facilitate the Creation of “Markets of Tomorrow”, Especially in Areas that Require Public-Private Collaboration | Incentivize and Expand Patient Investments in Research, Innovation and Invention That Can Create the New “Markets of Tomorrow” | Update Education Curricula and Expand Investment in the Skills Needed for Jobs and the “Markets of Tomorrow” |

|---|---|---|---|---|---|

| msr1 | msr2 | msr3 | msr4 | ||

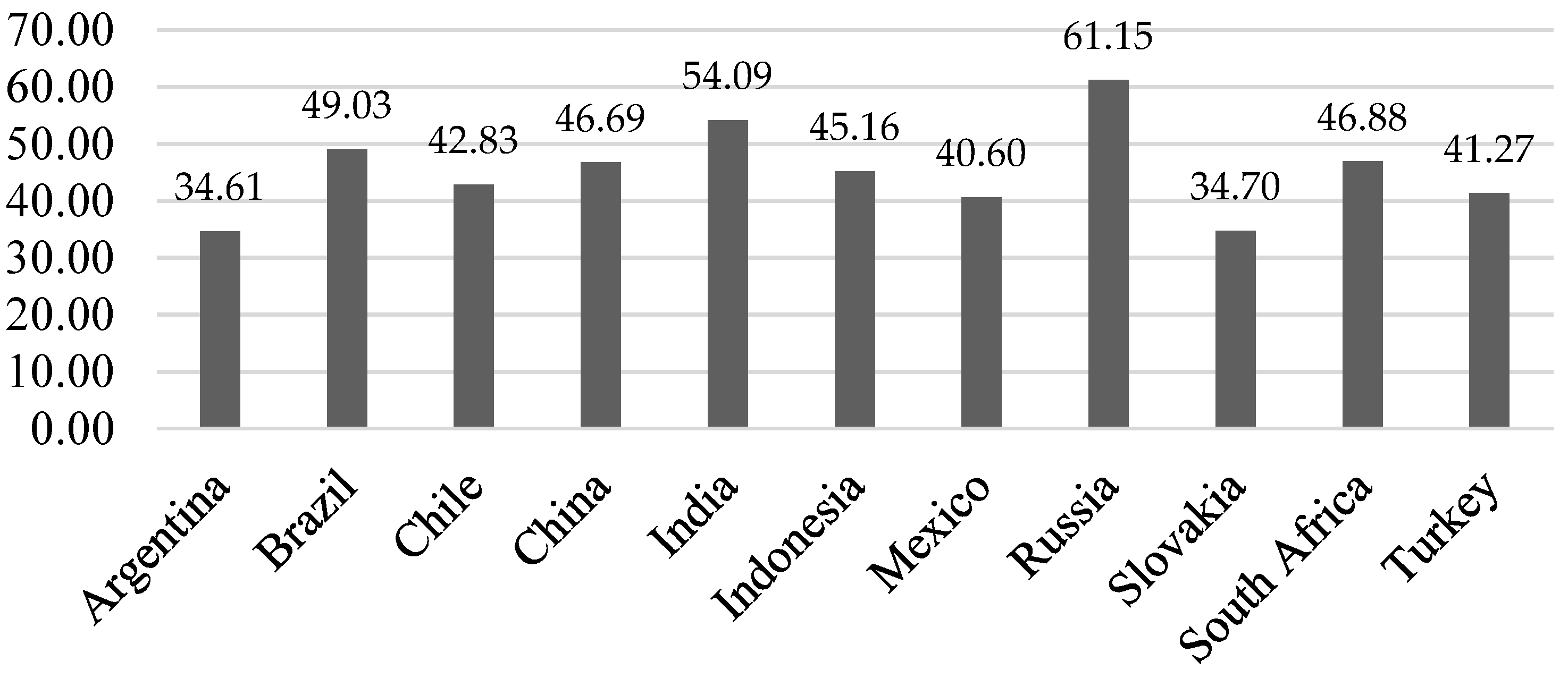

| Developing countries | Argentina | 32.8 | 34.3 | 31.9 | 46.9 |

| Brazil | 60.3 | 38.0 | 36.2 | 39.5 | |

| Chile | 57.5 | 39.7 | 31.7 | 52.1 | |

| China | 72.8 | 49.7 | 50.0 | 67.0 | |

| India | 54.5 | 40.2 | 32.5 | 43.5 | |

| Indonesia | 59.7 | 45.0 | 45.6 | 49.0 | |

| Mexico | 49.0 | 35.7 | 27.2 | 43.3 | |

| Russia | 55.3 | - | 35.6 | 44.9 | |

| Slovakia | 54.7 | 39.3 | 31.3 | 46.5 | |

| South Africa | 48.6 | 35.6 | 31.7 | 42.6 | |

| Turkey | 49.8 | 38.5 | 28.9 | 39.8 | |

| Developed countries | Finland | 95.4 | 59.5 | 53.4 | 75.3 |

| New Zealand | 93.2 | 45.0 | 45.2 | 63.4 | |

| Sweden | 89.0 | 52.2 | 50.8 | 69.4 | |

| Austria | 88.3 | 47.3 | 38.8 | 60.6 | |

| Japan | 84.7 | 53.5 | 54.7 | 51.3 | |

| Denmark | 84.6 | 46.7 | 41.7 | 71.5 | |

| France | 83.0 | 50.1 | 50.8 | 56.8 | |

| Ireland | 81.9 | 46.6 | 36.1 | 59.5 | |

| Israel | 81.77 | 51.2 | 53.1 | 66.6 | |

| Belgium | 81.2 | 49.3 | 47.8 | 65.8 | |

| Australia | 81.2 | 44.0 | 42.9 | 63.5 | |

| Estonia | 81.1 | 44.9 | 43.4 | 56.8 | |

| Netherlands | 79.9 | 50.4 | 48.3 | 71.8 | |

| Italy | 79.8 | 43.0 | 36.9 | 40.7 | |

| Germany | 79.3 | 48.1 | 49.2 | 61.4 | |

| Republic of Korea | 78.3 | 46.7 | 53.4 | 60.0 | |

| Canada | 75.1 | 49.5 | 42.8 | 65.3 | |

| UK | 72.4 | 46.1 | 40.9 | 59.7 | |

| Greece | 68.3 | 36.0 | 25.2 | 38.7 | |

| Portugal | 67.1 | 44.6 | 42.2 | 49.8 | |

| Poland | 62.7 | 37.5 | 32.1 | 41.9 | |

| Spain | 59.7 | 44.4 | 40.4 | 51.4 | |

| Switzerland | 59.2 | 50.8 | 51.6 | 70.8 | |

| Czech Republic | 58.2 | 41.9 | 40.2 | 48.5 | |

| Hungary | 52.0 | 39.4 | 36.7 | 40.8 | |

| USA | 47.8 | 57.7 | 57.3 | 68.2 |

| SEPR | Fr1 | Fr2 | Fr3 | Fr4 | msr1 | msr2 | msr3 | msr4 | |

|---|---|---|---|---|---|---|---|---|---|

| SEPR | 1 | - | - | - | - | - | - | - | - |

| Fr1 | −0.30 | 1 | - | - | - | - | - | - | - |

| Fr2 | −0.34 | 0.24 | 1 | - | - | - | - | - | - |

| Fr3 | −0.42 | 0.37 | 0.21 | 1 | - | - | - | - | - |

| Fr4 | −0.49 | 0.15 | 0.15 | 0.47 | 1 | - | - | - | - |

| msr1 | 0.47 | 0.18 | −0.20 | −0.41 | −0.53 | 1 | - | - | - |

| msr2 | 0.27 | 0.18 | −0.15 | −0.28 | −0.43 | 0.51 | 1 | - | - |

| msr3 | 0.51 | 0.05 | 0.00 | −0.39 | −0.51 | 0.54 | 0.67 | 1 | - |

| msr4 | 0.57 | −0.03 | −0.10 | −0.51 | −0.49 | 0.62 | 0.65 | 0.76 | 1 |

| Regression Statistics | ||||||

| Multiple R | 0.6029 | |||||

| R-square | 0.3635 | |||||

| Adjusted R-square | 0.2840 | |||||

| Standard error | 10.1788 | |||||

| Observations | 37 | |||||

| Dispersion analysis | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 4 | 1893.7802 | 473.4450 | 4.5696 | 0.0049 | |

| Residue | 32 | 3315.4357 | 103.6074 | |||

| Total | 36 | 5209.2159 | ||||

| Coefficients | Standard Error | t-Statistics | p-Value | Lower 95% | Upper 95% | |

| Constant | 67.9504 | 4.3443 | 15.6412 | 0.0000 | 59.1013 | 76.7996 |

| Coefficient at Fr1 | −0.0456 | 0.0499 | −0.9137 | 0.3677 | −0.1472 | 0.0560 |

| Coefficient at Fr2 | −0.1029 | 0.0675 | −1.5254 | 0.1370 | −0.2403 | 0.0345 |

| Coefficient at Fr3 | −0.0417 | 0.0467 | −0.8921 | 0.3790 | −0.1368 | 0.0535 |

| Coefficient at Fr4 | −0.1515 | 0.0663 | −2.2859 | 0.0290 | −0.2865 | −0.0165 |

| Regression Statistics | ||||||

| Multiple R | 0.6310 | |||||

| R-square | 0.3981 | |||||

| Adjusted R-square | 0.3229 | |||||

| Standard error | 9.8983 | |||||

| Observations | 37 | |||||

| Dispersion analysis | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 4 | 2073.9920 | 518.4980 | 5.2921 | 0.0022 | |

| Residue | 32 | 3135.2239 | 97.9757 | |||

| Total | 36 | 5209.2159 | ||||

| Coefficients | Standard Error | t-Statistics | p-Value | Lower 95% | Upper 95% | |

| Constant | 16.2665 | 9.3239 | 1.7446 | 0.0907 | −2.7258 | 35.2587 |

| Coefficient at msr1 | 0.1693 | 0.1398 | 1.2112 | 0.2347 | −0.1154 | 0.4540 |

| Coefficient at msr2 | −0.3647 | 0.2427 | −1.5031 | 0.1426 | −0.8590 | 0.1295 |

| Coefficient at msr3 | 0.3685 | 0.3192 | 1.1544 | 0.2569 | −0.2817 | 1.0187 |

| Coefficient at msr4 | 0.4548 | 0.2528 | 1.7990 | 0.0815 | −0.0602 | 0.9698 |

| Regression Statistics | ||||||

| Multiple R | 0.9944 | |||||

| R-square | 0.9888 | |||||

| Adjusted R-square | 0.9887 | |||||

| Standard error | 5.82 × 1011 | |||||

| Observations | 292 | |||||

| Dispersion analysis | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 1 | 8.64 × 1027 | 8.64 × 1027 | 25,506.1466 | 1.1 × 10−284 | |

| Residue | 290 | 9.83 × 1025 | 3.39 × 1023 | |||

| Total | 291 | 8.74 × 1027 | ||||

| Coefficients | Standard Error | t-Statistics | P-Value | Lower 95% | Upper 95% | |

| Constant | −9.6 × 1011 | 2.68 × 1011 | −3.58439 | 0.0004 | −1.5 × 1012 | −4.3 × 1011 |

| Coefficient at IMOEX | 2.3668 | 0.0148 | 159.7064 | 1.11 × 10−284 | 2.3377 | 2.3960 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Popkova, E.G.; Sergi, B.S. Dataset Modelling of the Financial Risk Management of Social Entrepreneurship in Emerging Economies. Risks 2021, 9, 211. https://doi.org/10.3390/risks9120211

Popkova EG, Sergi BS. Dataset Modelling of the Financial Risk Management of Social Entrepreneurship in Emerging Economies. Risks. 2021; 9(12):211. https://doi.org/10.3390/risks9120211

Chicago/Turabian StylePopkova, Elena G., and Bruno S. Sergi. 2021. "Dataset Modelling of the Financial Risk Management of Social Entrepreneurship in Emerging Economies" Risks 9, no. 12: 211. https://doi.org/10.3390/risks9120211

APA StylePopkova, E. G., & Sergi, B. S. (2021). Dataset Modelling of the Financial Risk Management of Social Entrepreneurship in Emerging Economies. Risks, 9(12), 211. https://doi.org/10.3390/risks9120211