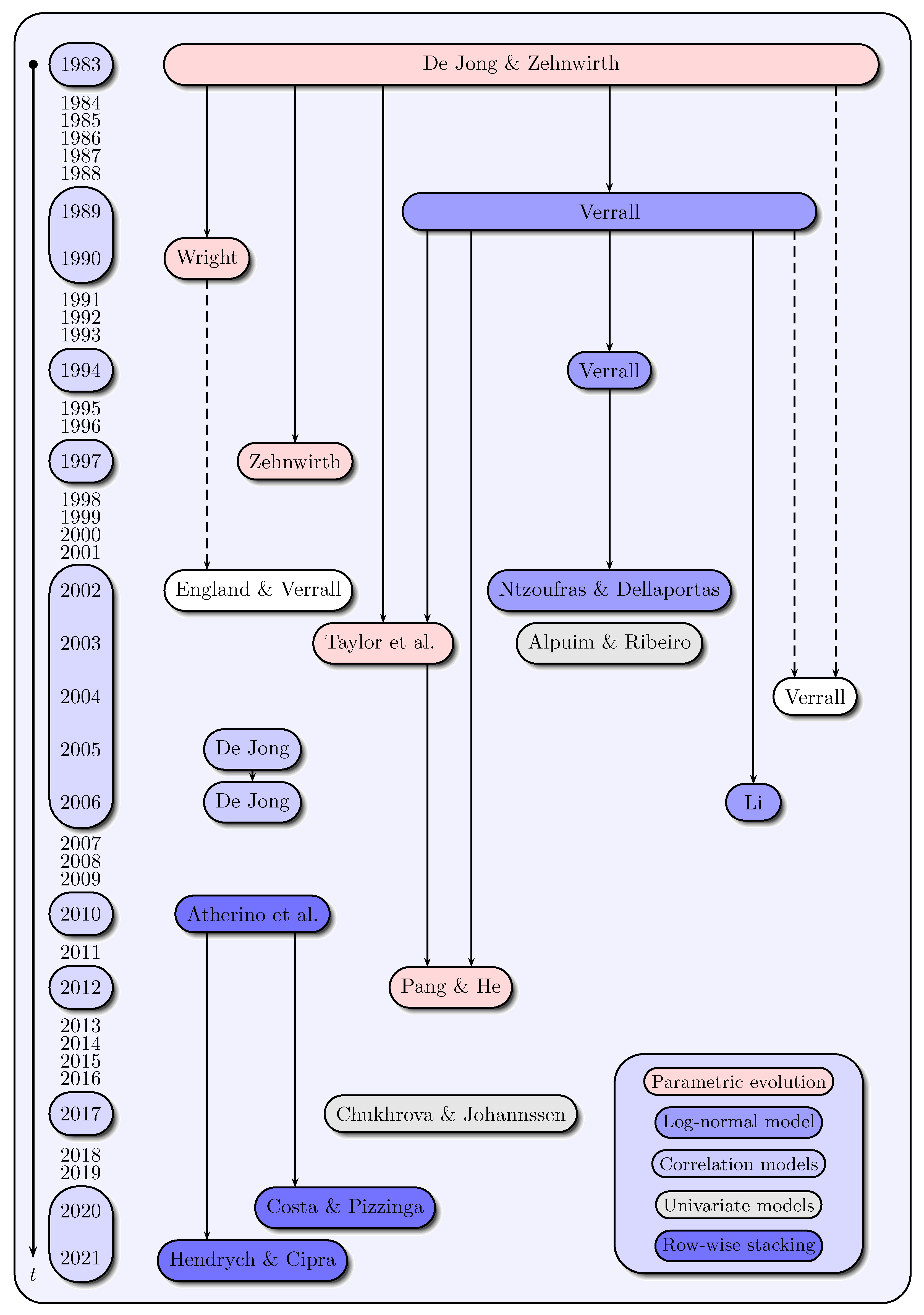

In this section, we present papers that are based on the assumption of a parametric evolution of the claims data across development years:

Three articles marked with ▸ are mainly based on the use of state space models and the Kalman filter learning theory, and thus are presented in detail, while the models of the other two articles marked with ⊳ are treated in a more brief form, as state space models are not the focus of their methodologies.

2.1. Claims Reserving, State Space Models and the Kalman Filter

De Jong and Zehnwirth (

1983) laid the foundation for the use of state space models and the Kalman filter in stochastic claims reserving with their article

“Claims Reserving, State-Space Models and the Kalman Filter”. The proposed state space model is constructed for the payment stream of the incremental payments and presumes known, time-varying system matrices.

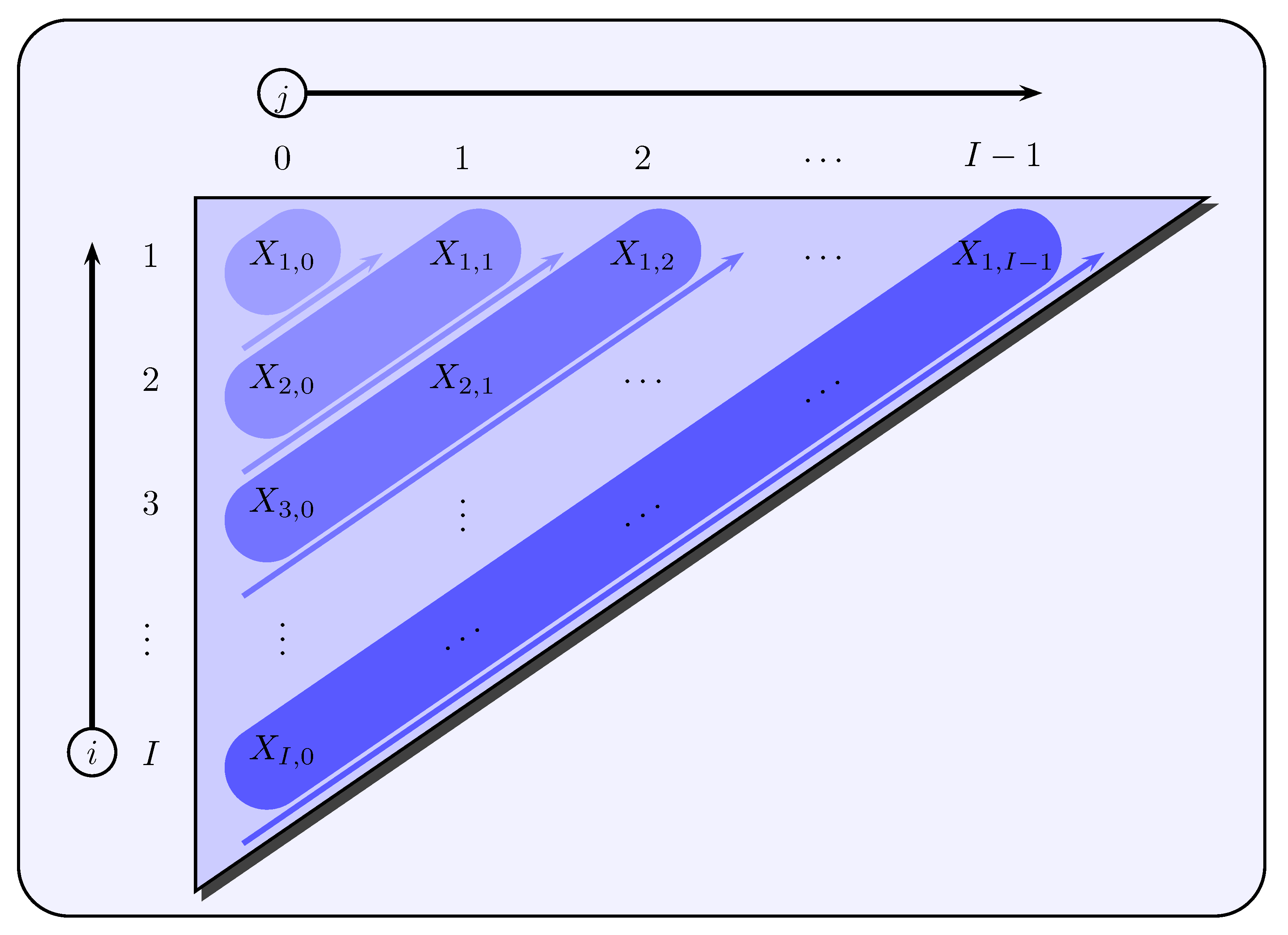

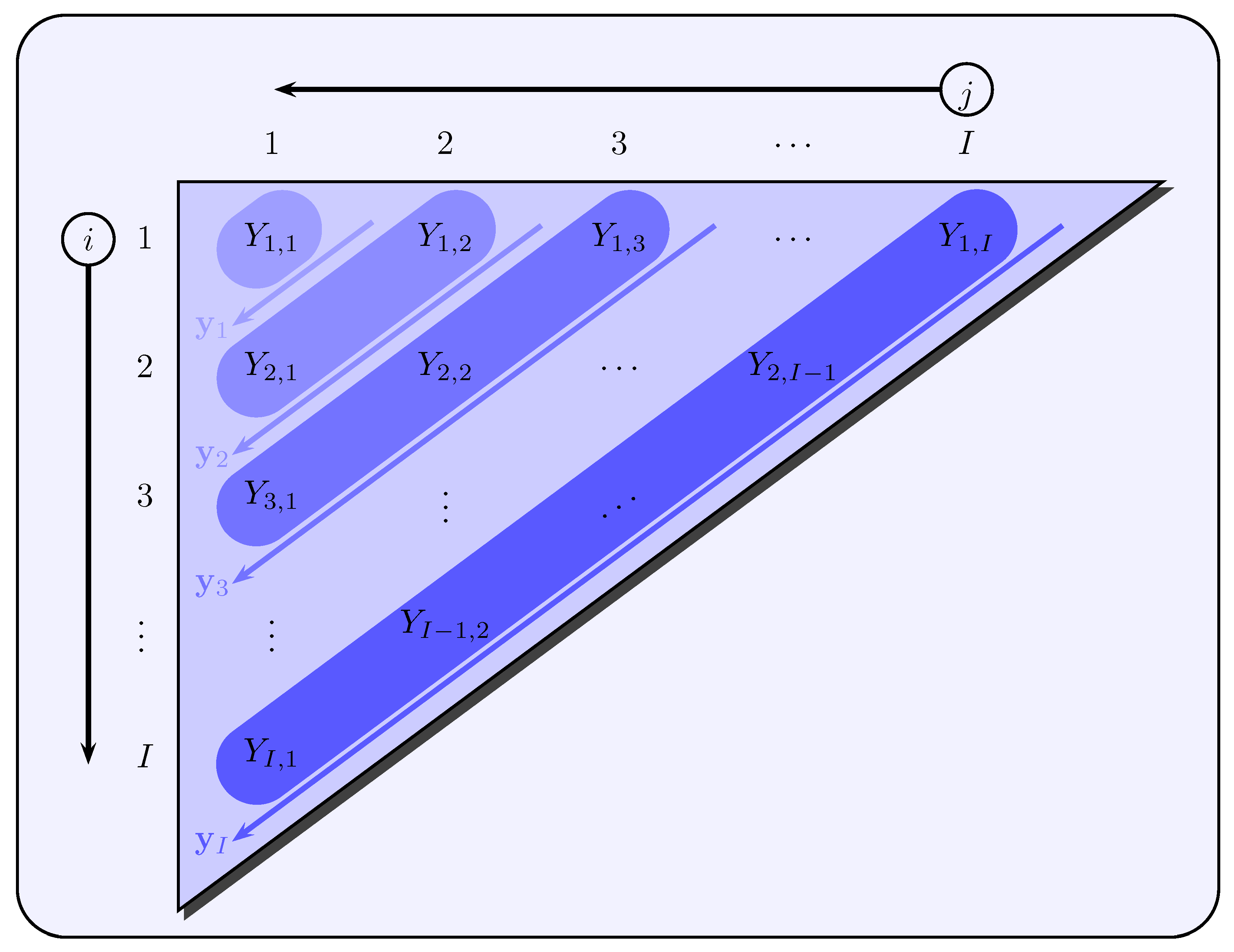

Modeling the payment stream of incremental payments

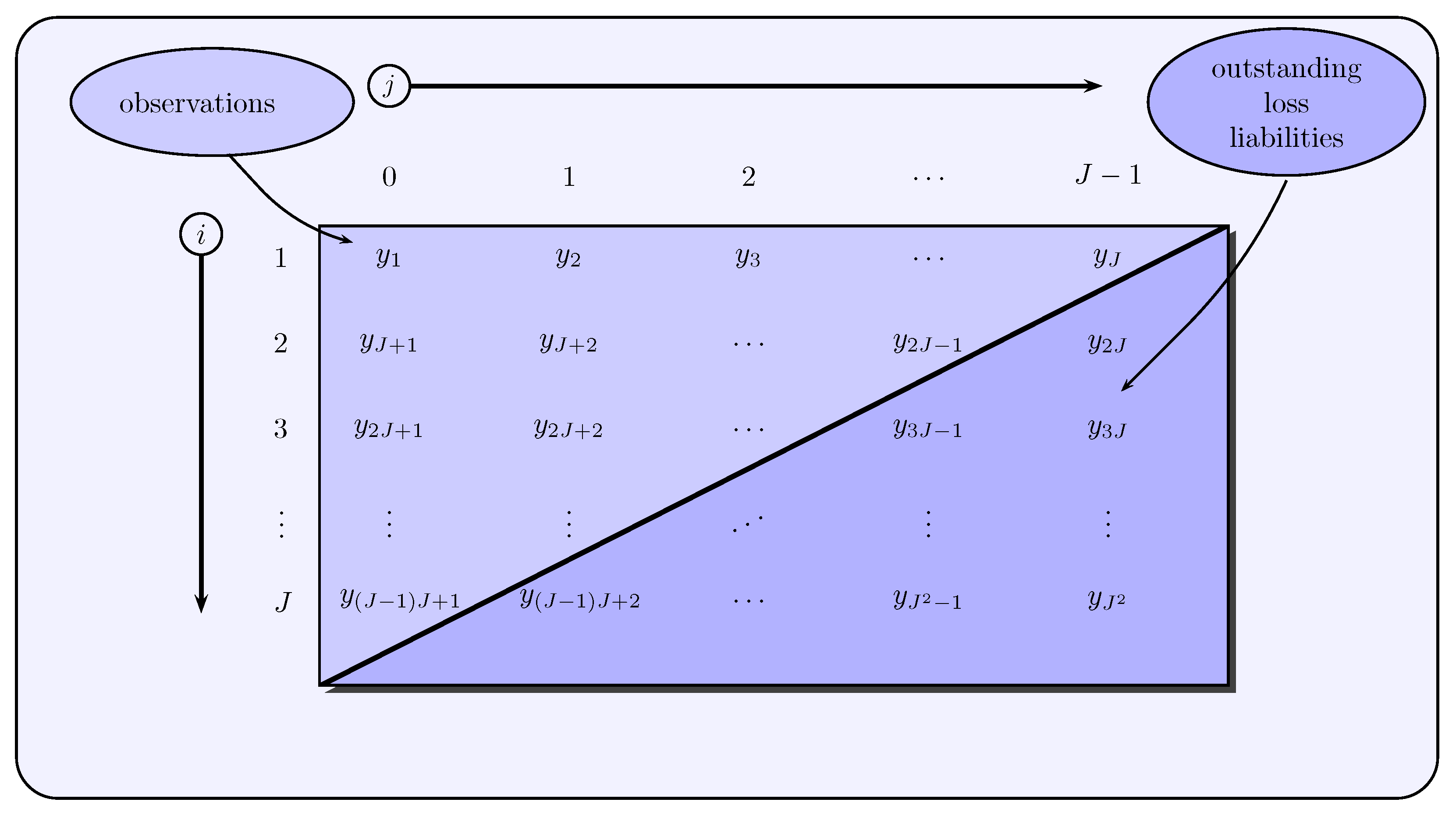

The modeling is based on claims development triangles in which incremental payments

are given for accident years

and development years

. The payment stream of incremental payments is modeled with increasing development year

and decreasing accident year

for a fixed calendar year

via

see also

Figure 2. Here, the quantity

is generally the expected claim payment to be made in accident year

i and development year

j of the

t-th calendar year, and

is a noise term with

.

De Jong and Zehnwirth (

1983) propose an optional modification of (

1) by including additional information such as the volume of business transacted in each accident year and the inflation factor for each calendar year. To this end, let

denote an appropriate index for the volume of business transacted in accident year

i and

denote an appropriate price index for payments in the

t-th calendar year. Using both these quantities, (

1) can be extended to

where

is the expected value of the inflation-adjusted and volume-weighted incremental payments in accident year

i and development year

j of calendar year

t.

Development of an appropriate state space representation

The modeling of the payment stream via (

1) and (

2) is promising with respect to the construction of an appropriate observation and state equation of a state space model, respectively. The following discussion in this regard is based on (

1), but can be applied to (

2) with minor modifications. In the first step of modeling the observation equation, (

1) is transferred into a vector representation in such a way that

represents the vector of observations

of the

t-th calendar year,

forms the vector of expected claims payments

, and

is the vector of noise terms

with

. Thus, the incremental payments made in calendar year

t can be specified via

or briefly as

. In the second step, the vector

is to be modeled in such a way that it is obtained by the product of a system matrix

and a state vector

. For this purpose,

De Jong and Zehnwirth (

1983) take

for a given accident year

i as a function depending on the development year

j and thus construct for each accident year a

distributed lag model of the form

where

are known functions in

j and

are unknown parameters depending on the respective accident year

i.

De Jong and Zehnwirth (

1983) justified the approach (

4) by an overall smooth evolution of

characterized by a firstly increasing and then decreasing behavior in

j for a given accident year

i. A variation of (

4) for

is the so-called

Hoerl curve

which

De Jong and Zehnwirth (

1983) use in their empirical application example. In addition, (

4) can be easily transferred into vector notation by using

as follows:

Substituting (

7) into (

3) then gives

or in a more compact form

with

and

for all

. Thus, given

,

, the system matrix

is a known time-varying diagonal matrix, and the state vector

contains unknown parameter vectors

for

. Assuming a Hoerl curve according to (

5), the observation Equation (

9) of the

t-th calendar year results in (due to

):

Subsequently,

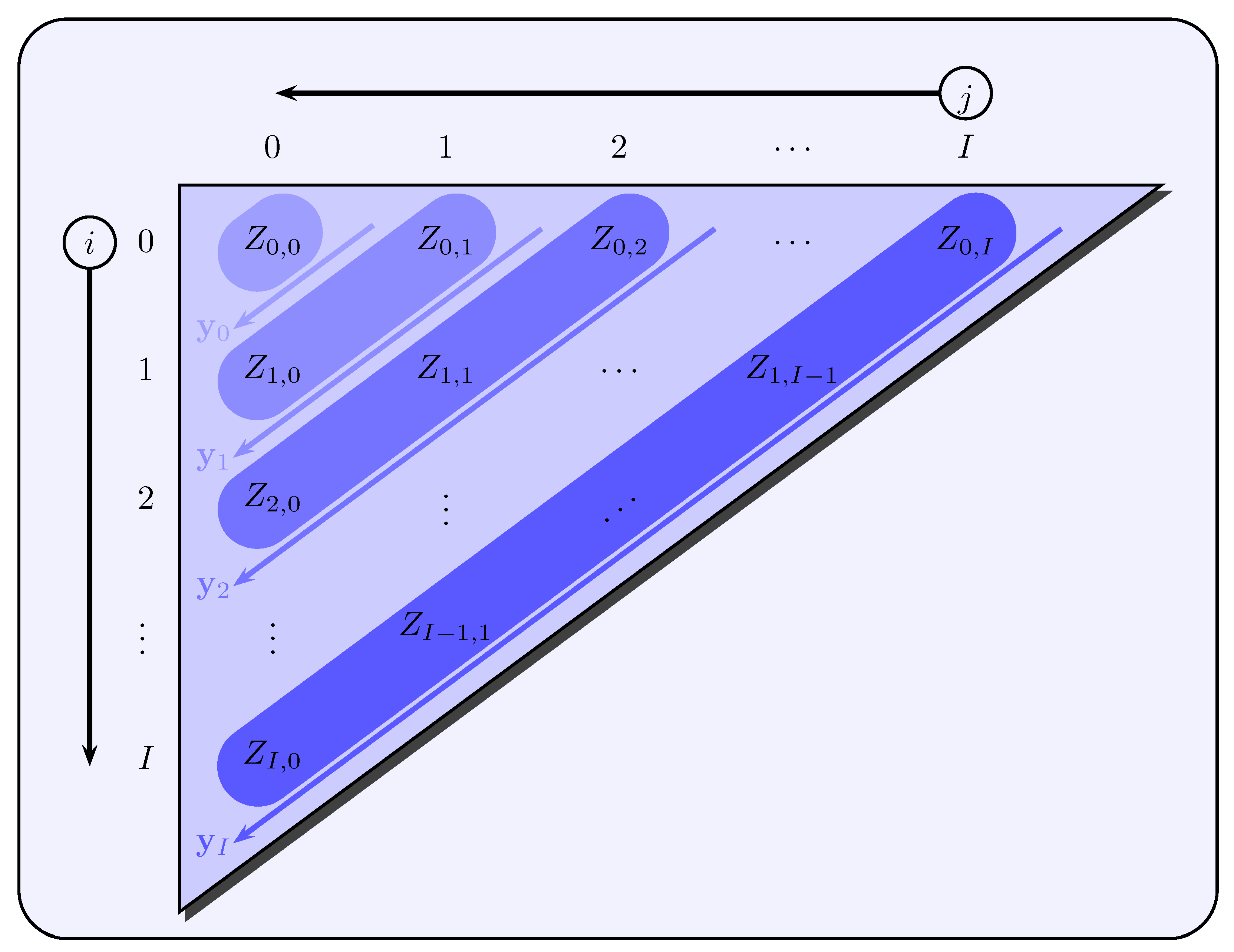

De Jong and Zehnwirth (

1983) specify an appropriate state equation, in which they establish a connection between the state vector

of the

t-th calendar year and the state vector

of the

-th calendar year. The basic idea is again to model a smooth evolution, but in a slightly different form than in (

4). The starting point is the sequence

, but with the difference that for a fixed development year

j the accident years

i are varied, whereas before for a fixed calendar year

t the development years

j varied (see

Figure 3).

For a given development year

j,

De Jong and Zehnwirth (

1983) propose modeling

via

with

, where

is a noise term with

. Thus, in contrast to (

4),

is not modeled in a deterministic way but as a random variable. Further, they assume that the conditional expected value on the right-hand side of (

10) is a polynomial in

i of degree

that passes through

. This leads to

with known

for

. Substituting (

7) on both sides into (

11) for

yields

where the (

)-dimensional matrix

and the

p-dimensional vector

are given by

respectively. If both sides of Equation (

12) are multiplied from the left by the inverse

of the matrix

(the existence of the inverse is ensured, see

De Jong and Zehnwirth 1983), one obtains

Transferring (

13) into matrix notation, we obtain

or in a more compact fom

with

and

as well as

for all

. The identity matrices

, zero matrices

and scalar matrices

with

in (

14) are each of dimension

. Note also that the system matrices

and

are known in the state Equation (

15).

A variation of the state Equation (

15) is given for

(i.e., assuming a Hoerl curve as in (

5)) and the parameters

of different accident years

are connected by a random walk

that is,

,

,

. Since we have

, the relation

holds. For this reason,

De Jong and Zehnwirth (

1983) aim to obtain

and thus a state equation in the form of the random walk (

16), i.e., they choose without loss of generality the fixed development year

.

With respect to (

10) and (

13), the use of (

16) implies

for all

. Accordingly, it follows for the system matrix

that it has the value one at positions

and zeros otherwise, while

corresponds to a

t-dimensional unit vector with the value one at position

. The state Equation (

15) thus simplifies to:

If one intends to model the observation and state equations by using (

2) instead of (

1), there are only changes in the observation Equation (

9), while the state Equation (

15) remains unchanged: each row

of the system matrix

has to be multiplied by a weighting factor consisting of volume and inflation indices, i.e., by

.

Forecasting the outstanding loss liabilities

As the system matrices

are assumed to be known for all

, the outstanding loss liabilities for individual and aggregated accident years can be predicted by using

and

in a straightforward way. To this end, all future incremental payments are collected in the vector

All these future observations belong to one of the accident years

, and therefore, they are based on the corresponding state

. Accordingly, the state vector

corresponds to the vector

of the current calendar year

I, which is why the state Equation (

15) is given by

(i.e.,

,

). The system matrix

of the observation equation is obtained on the basis of (

1) similar to that in (

8), i.e., it consists mostly of zero vectors, and the entries

with

are ordered such that they are multiplied by the states

from

of the corresponding accident year

of

from

. Thus, the future observations can be predicted via

(given by (

9)) and

respectively. The variance–covariance matrix of the prediction error

is given by:

Since

,

,

are known at time

, a prediction of the outstanding loss liabilities for individual and aggregated accident years is straightforward. With respect to the aggregated accident years, all components from

are to be added to the total loss reserve, while for individual accident years only those components from

related to the respective accident year

are to be added. An extraction of these components can be carried out via a diagonal matrix

, which has a value of one at the respective positions and otherwise zeros. The variance–covariance matrix belonging to

is thus

However, if the modified payment stream according to (

2) is used, additional uncertainty is induced via the inflation index

of future calendar years

, which is unknown at time

. This is due to the unknown entries

for

instead of the known entries

in the system matrix

.

2.2. A Stochastic Method for Claims Reserving in General Insurance

Wright (

1990) primarily establishes a model for incremental payments that includes a state space approach, where the variation of the parameters is modeled over different accident years. Thus, although the model of

Wright (

1990) is not mainly based on state space models and the Kalman filter theory, it embeds them in a model framework as one component. In the following, therefore, the model for incremental payments and the state space model are presented (for further details, see

Wright 1990).

Construction of the model for claims payments

The modeling is built on development triangles that include incremental payments

in accident years

and development years

. The proposed model is based on the assumption that incremental payments

are composed of the sum of

independent and identically distributed (i.i.d.) payments

(which are stochastically independent of

), that is,

. Thus,

Wright (

1990) uses the

collective risk model and

has a mixture distribution (see, e.g.,

Kaas et al. 2009). The lags

j of individual incremental payments

between the accident year of the claim and the actual payment are modeled as i.i.d. random variables, which is why

with

is defined as the probability of payments regarding claims of accident year

i in a given development year

j. Let the number

of payments for claims of accident year

i in development year

j be Poisson-distributed with parameter

, i.e.,

; then, the incremental payments

follow a mixture Poisson distribution. Following the convolution property of the Poisson distribution, the total number of claims payments

of an accident year

i also follows a Poisson distribution with parameter

where the

for different

j are assumed to be stochastically independent random variables and the parameter

serves as a measure for the

exposure of accident year

i. As for modeling of the probability

,

Wright (

1990) gives two alternatives, the stochastic CL and the Hoerl curve model. While in the first alternative it is assumed that the probabilities

are identical over all accident years

i, the second alternative (preferred by

Wright 1990) provides a modeling via a Hoerl curve of the form

with constants

,

and

to be estimated and

and

as functions depending on

j. Using (

17), the expected value and variance of

are as follows:

In addition to the number

of payments,

Wright (

1990) also models the amount of individual payments

for claims of an accident year

i in the

j-th development year, which, like the

, are also assumed to be stochastically independent for various

j. The first two moments of

are modeled distribution-free with help of

with proper (unknown) constants

,

,

and inflation parameter

. While such a modeling of the expected value with different

and

K provides a variety of possibilities, the modeling of the variance results from the assumption that the coefficient of variation

is time-invariant and corresponds to

. The optional term

in (

19) with

and

as the average annual inflation rate between calendar years

and

k, on the other hand, are used to account for inflation; i.e.,

reflects the inflation factor from the first calendar year to calendar year

. However,

Wright (

1990) proposes using

and therefore assumes a constant inflation rate

.

Considering (

18)–(

20), and using the moments of the mixture Poisson distribution, the expected value and variance of the incremental payments

in

are obtained via

and

where

are stochastically independent for different

j due to the assumptions regarding

and

. Moreover,

Wright (

1990) normalizes the incremental payments

with the help of

with exposure defined by

By using (

17), (

21), (

23), (

24), the expected value

of the normalized incremental payments

can be stated as follows:

with

Considering (

22), (

23), (

25), the variance of

is

with

Assuming that

and

are known, one obtains a

generalized linear model of the form

with the exponential response function

, linear predictor

consisting of

and noise term

with

where the parameter estimators

and variance–covariance matrices

can be determined for all

i using the Fisher scoring algorithm such that

is approximately satisfied. However, since

and

are usually unknown,

Wright (

1990) proposes an iterative approach using parameter initializations to determine initial values for

and

. Considering this approach, all accident years are run sequentially and the results of all accident years are subsequently used to obtain new estimates of the parameters for the next run.

Modeling the parameter variation via a state space model

To increase the reliability of the estimators

,

Wright (

1990) models the variation in the parameters

for different accident years

i via

with

By defining

with the help of

and by using (

26), (

27) can be written as

with

where

and

hold for all

. Thus, Equation (

28) forms the state equation of a state space model. Considering the estimators

as observations

, the associated observation equation can be obtained via

with

and

,

and

for all

. Accordingly, a complete state space model with

and

is specified via Equations (

28) and (

29).

2.4. Loss Reserving: Past, Present and Future

Taylor et al. (

2003) give a classification scheme for claims reserving methods whose higher-level criteria make a division between static and dynamic methods. In the framework of this taxonomic classification and especially with respect to the dynamic methods, they discuss a generalized Kalman filter, which allows for non-linearities in the observation equation and noise terms following a distribution of the Exponential Dispersion Family (EDF). They present two modeling approaches based on different types of claims data and state space representations constructed specifically for these data.

Accident year-based state space modeling

In the first modeling approach, an accident year-based state space representation is constructed, which is based on Payments Per Claim Incurred (PPCI) of a workers’ compensation insurance policy as claims data. The PPCI of an accident year in the development year are denoted by and belong to the ()-th calendar year with .

The state space model considered by

Taylor et al. (

2003) is based on a linear state equation of the form

with five-dimensional random vectors

, transition matrix

,

and

for

, while the observation equation

with (

)-dimensional random vectors

, system matrix

,

and

is based on a generalized linear model with link function

h (i.e., response function

) and linear predictor

for all

. Moreover,

holds for all

, the initial state

is uncorrelated with

and

for all

and

is assumed to be EDF-distributed for all

. Thus, any strictly monotonic and differentiable link function

h (such as a logarithm function) can be used to link the EDF-distributed observations

and the systematic component

. The resulting recursive equations

Taylor et al. (

2003) refer to as the EDF filter, which include the Kalman filter as a special case, namely for the identity function as link function and normally distributed noise terms

. The observation vector

in (

32) includes all PPCIs of an accident year

of the upper claims development triangle (see

Figure 4).

Taylor et al. (

2003) propose a logarithm function as a link function, the noise terms

are assumed to be gamma-distributed and the

-th row of the linear predictor

for an accident year

is given by

with respect to the development year

. Here,

denotes the

Kronecker delta,

which can be used to model the peak in development year

. Thus, the observation Equation (

32) of accident year

can be stated as follows:

On the other hand,

Taylor et al. (

2003) do not provide any information on the concrete form of the state Equation (

31).

Taylor et al. (

2003) model the evolution of the PPCI over the development years according to (

33) in a similar way to

De Jong and Zehnwirth (

1983),

Wright (

1990) and

Zehnwirth (

1997), who specify the evolution of incremental payments over the development years with the help of a Hoerl curve.

Taylor et al. (

2003) apply this approach to the PPCI, as their evolution over the development years is similar to that of incremental payments: They reach their peak in development year

and then drop relatively quickly to zero. This evolution of the PPCI is also the justification of

Taylor et al. (

2003) for the choice of the logarithm function as a link function and the assumption of a gamma distribution for the measurement noise.

Calendar year-based state space modeling

For the second modeling approach,

Taylor et al. (

2003) use a data set from

Taylor (

2000) that consists of motor vehicle bodily injury claim closure rates. Here, rather than collecting the observations from each accident year, they stack the observations from each calendar year into observation vectors. This is due to the fact that claim closure rates are relatively flat across development years, but are subject to calendar year effects.

The state space model proposed by

Taylor et al. (

2003) provides a linear state equation and an observation equation in the form of a generalized linear model, but differs from the first approach by the time index (calendar years

t instead of accident years

i) and by the matrix dimensions. They consider the following state space model consisting of the state equation

with (

)-dimensional random vectors

,

, a (

)-dimensional random vector

and transition matrix

for

, and the observation equation of the

t-th calendar year

with (

)-dimensional random vectors

,

, and

-dimensional system matrix

for

, where the assumptions concerning the noise terms correspond to those of the first approach (transferred to calendar years).

Taylor et al. (

2003) choose the identity function as a link function and the measurement noise is assumed to be normally distributed, which is why one obtains an ordinary linear observation equation and the usual linear Kalman filter can be used. This choice is motivated by the sufficiently high number of claims closures in the underlying claims data, and the assumption of an approximate normal distribution is justified by the central limit theorem, although the assumption of a discrete probability distribution such as the binomial distribution would be more appropriate. As for the development of the expected claim closure rate

with respect to the claims of an accident year

over the development years

,

Taylor et al. (

2003) assume

with

as effect of the

t-th calendar year and Kronecker Delta

. The observation vector

of the

t-th calendar year with

contains all

claim closure rates

of the respective calendar year

(see

Figure 5), which is why the

-dimensional state vector can be stated as

with

for

.

While the state vector

in the first modeling approach only contains the parameters of the

i-th accident year, the state vector

contains all parameters up to the

t-th accident year plus the corresponding calendar year effect. This is due to the fact that the observations of the

t-th calendar year pass through all accident years

. The observation Equation (

35) is thus given by

with

according to (

37) and

according to (

38) for all

as well as three-dimensional zero vectors

. The state Equation (

34) is then

where

and

in

are identity and zero matrices of dimensions

, respectively,

in

are three-dimensional zero vectors and

,

are given as follows:

Thus, the state equation involves a dynamic estimation of the parameters

and

via

for

. Finally,

Table 2 gives an overview of the dimensions of vectors and matrices in the state space models of

Taylor et al. (

2003).

2.5. The Application of State Space Model in Outstanding Claims Reserve

Pang and He (

2012) largely adopt the second modeling approach from

Taylor et al. (

2003), but without integrating calendar year effects. They extend the state equation by including a further lag of the state vector. Accordingly, the state space model they consider is given by

with

,

,

for all

.

Table 3 gives an overview of the dimensions of vectors and matrices in the state space model of

Pang and He (

2012).

The observation vector

contains all observations

of the

t-th calendar year, i.e., all

with

. However, the nature of the claims data is not obvious and the authors refer to it only as “times of compensation”. Therefore, in view of the magnitude of the observations and their modeling, claims data are assumed to be incremental payments. The expected incremental payments of an accident year

are assumed to have a parametric evolution over the development years

similar to (

33) via

with Kronecker Delta

. Thus, the observation Equation (

39) of the

t-th calendar year (

) results in a similar form as achieved within the second modeling approach of

Taylor et al. (

2003),

with

for all

.

Pang and He (

2012) do not give the general representation of the state equation according to (

40), but the reduced form

which solely contains the last four rows of (

40) that are of interest. For the remaining

-dimensional parameter matrices, they assume scalar matrices

and

for all

, which is why the state Equation (

42) is given by:

If, on the other hand, one intends to express the state equation in the form (

40), the upper

-dimensional part of

corresponds to an identity matrix, while the last four rows in the last four columns of

form the scalar matrix

and otherwise contain zeros. The parameter matrix

has only zeros in the

-dimensional upper part and also in the last four rows except for the last four columns, which correspond to the

-dimensional scalar matrix

. The noise vector

is equal to a zero vector in the first

rows and to the vector

in the remaining rows.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}