The Italian Pension Gap: A Stochastic Optimal Control Approach

Abstract

1. Introduction

2. The Italian Pension Provision

- The workers with at least eighteen years of contributions on 31 December 1995 remained under the salary-related system and therefore were not touched by the reform.

- The workers with less than eighteen years of contributions on 31 December 1995 were subject to a mixed method.

- The workers who were first employed after 31 December 1995 are subject to the contribution-based system.

- w is the mean real GDP (Gross Domestic Product) increase.

- T indicates the number of past working years (for instance ).

- c is the contribution percentage for the calculation of the pension rate (supposed to be constant during the whole working life and, for the employees, set by law to 33%).

- is the conversion coefficient between a lump sum and the annuity rate, and its choice should reflect actuarial fairness. If it does, then , where is the single premium of a lifetime annuity issued to a policyholder aged x, i.e.,where is the extreme age, is the annual discount factor, and is the survival probability from age x to age .

3. The Optimization Problem

4. Solution

4.1 Solution to the Problem with Two Different Salary Evolutions

5. Simulations

5.1. Base Case: Assumptions

- the initial fund ;

- the public pension contribution ;

- the mean GDP growth rate ;

- the riskless interest rate ;

- the drift of the risky asset ;

- the diffusion of the risky asset ;

- the intertemporal discount factor ;

- the annuity value is calculated with the Italian projected mortality table IP55 (for males born between 1948 and 1960); ; therefore, the conversion factor from lump sum to annuity is as follows: ;

- the age when the member joins the scheme ;

- the time horizon , meaning that the retirement age ;

- the initial salary .

5.2. Base Case: Results

- Table 1 reports, for both cases of exponential and linear growths, the old pension , the new pension , the old net replacement ratio , the new replacement ratio , the rate of growth of the targets , and the last salary ;

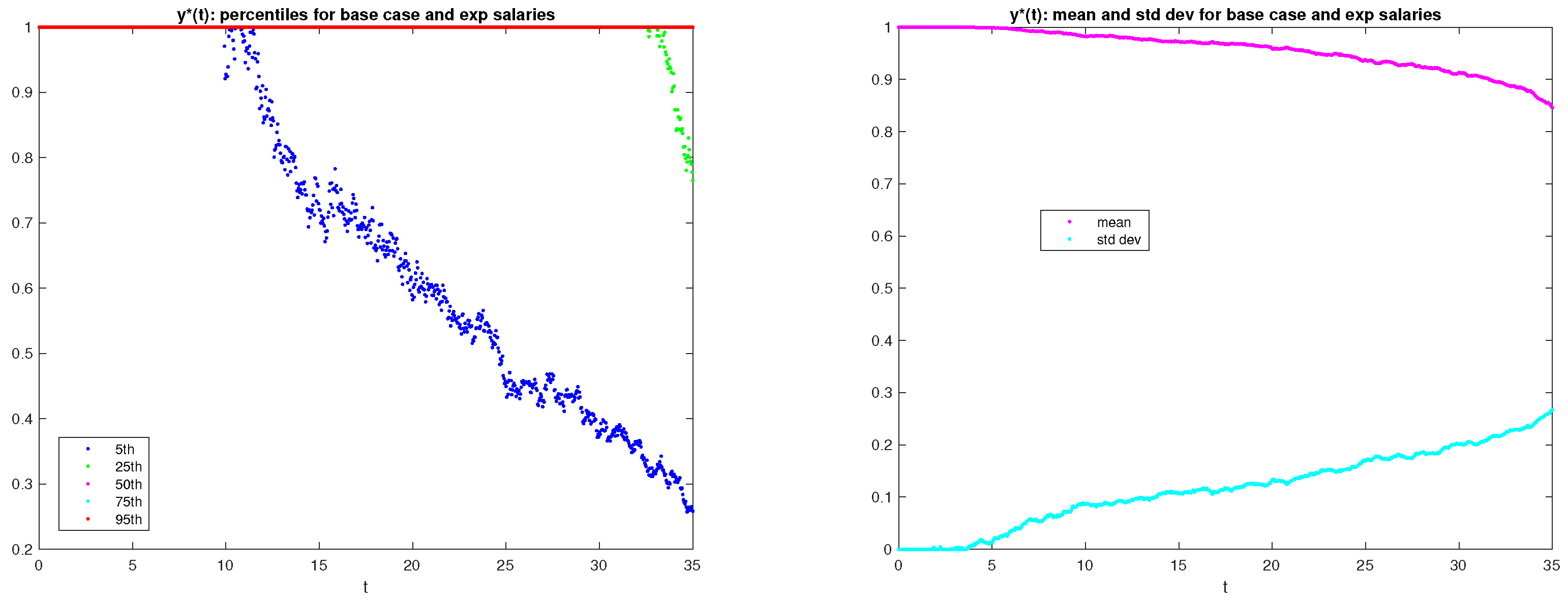

- the two graphs in Figure 1 report percentiles (graph on the left) as well as the mean and standard deviation (graph on the right) of the distribution, over the 1000 scenarios, of the investment strategy for , for exponential salary growth;

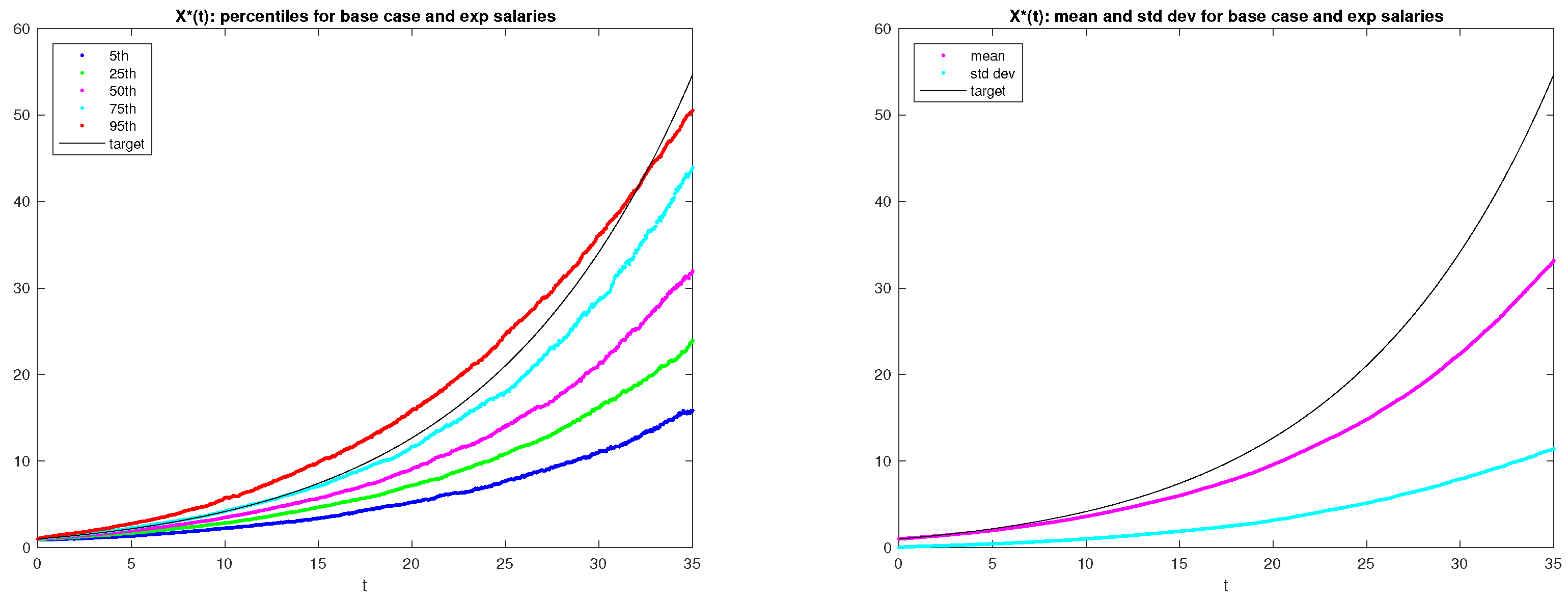

- the two graphs in Figure 2 report percentiles (graph on the left) as well as the mean and standard deviation (graph on the right) of the distribution, over the 1000 scenarios, of the fund for , for exponential salary growth;

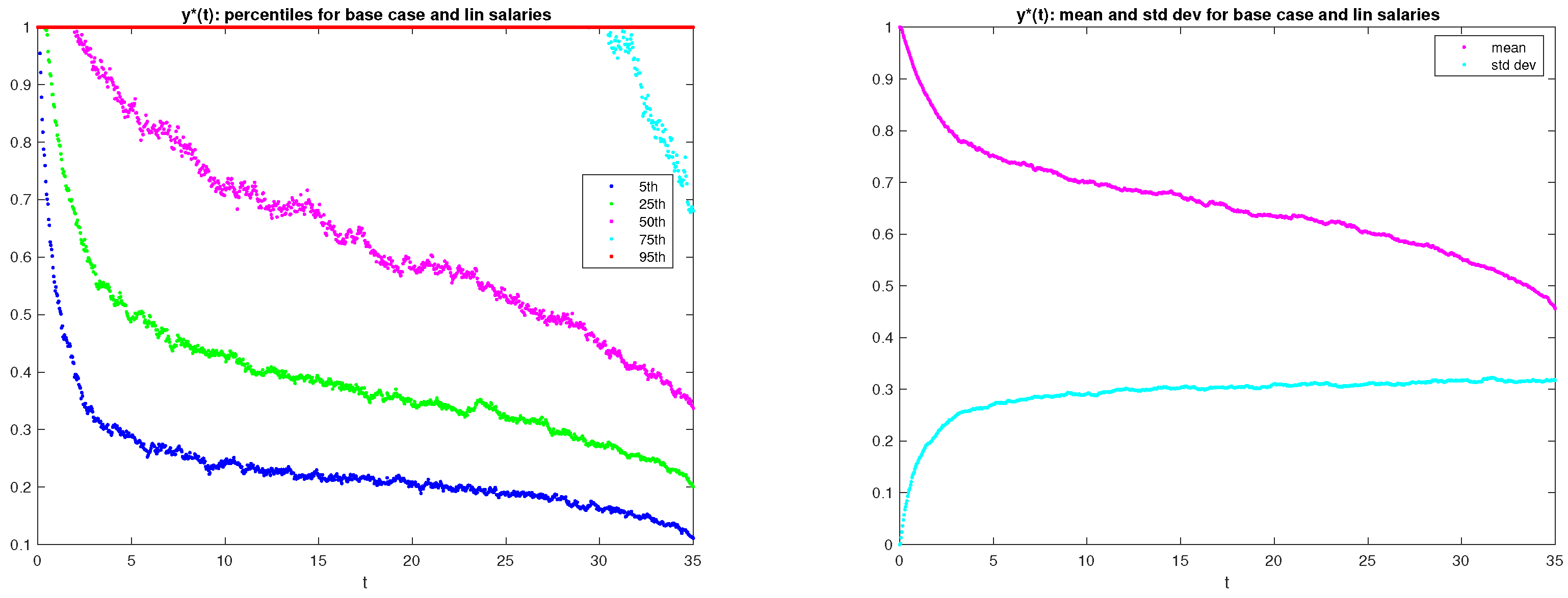

- the two graphs in Figure 3 report percentiles (graph on the left) as well as the mean and standard deviation (graph on the right) of the distribution, over the 1000 scenarios, of the investment strategy for , for linear salary growth;

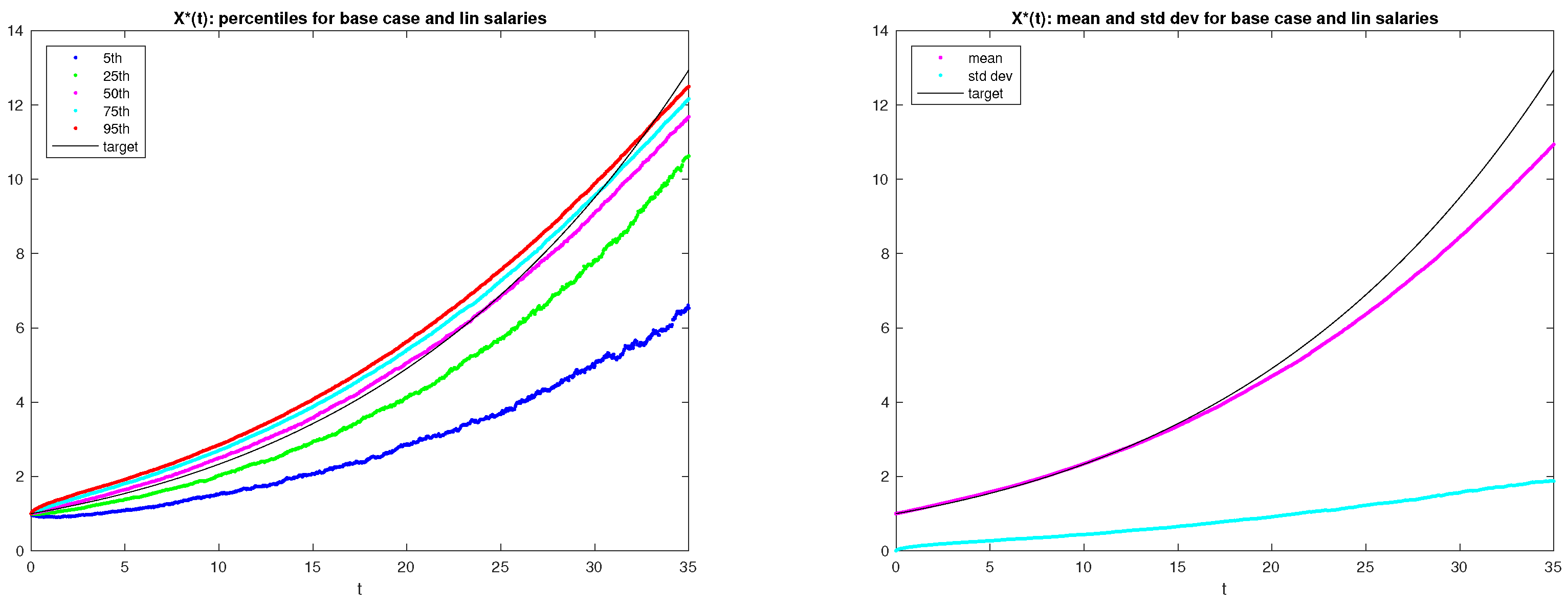

- the two graphs in Figure 4 report percentiles (graph on the left) as well as the mean and standard deviation (graph on the right) of the distribution, over the 1000 scenarios, of the fund for , for linear salary growth.

- As expected, with exponential salary growth, the final salary is significantly larger (more than double) than that with linear salary growth; therefore, though the old replacement ratio (that does not depend on the salary growth) is the same (), the old pension is much larger with a dynamic career than with a stagnant one.

- The investment strategy for the exponential growth is remarkably riskier than that for the linear growth: for the exponential growth in almost of cases, the portfolio is entirely invested in the risky asset for all t, while for the linear growth all percentiles of (apart from the 95th one) decrease gradually from 1 to 0 over time. The larger riskiness of the strategy for the exponential growth is due to the larger gap between the old and the new pension, see next point.

- With exponential salary growth the gap between the old and the new pension is larger than that with linear salary growth: the old replacement ratio is in both cases, but the new replacement ratio (that does depend on the salary growth) is for the exponential growth and for the linear growth; the larger gap to fill in for the exponential increase entails riskier strategies, and the smaller gap to fill in for the linear increase entails less risky strategies; these results seem to suggest that the new reform affects to a larger extent workers with a dynamic career than workers with a stagnant career.

- With both salary increases, on average the investment in the risky asset decreases over time and approaches 0 when retirement approaches; this result is in line with previous results on optimal investment strategies for DC pension schemes (see, e.g., Haberman and Vigna (2002)) and is consistent with the lifestyle strategy (see Cairns (2000)), which is an investment strategy largely adopted in DC pension funds in the UK.

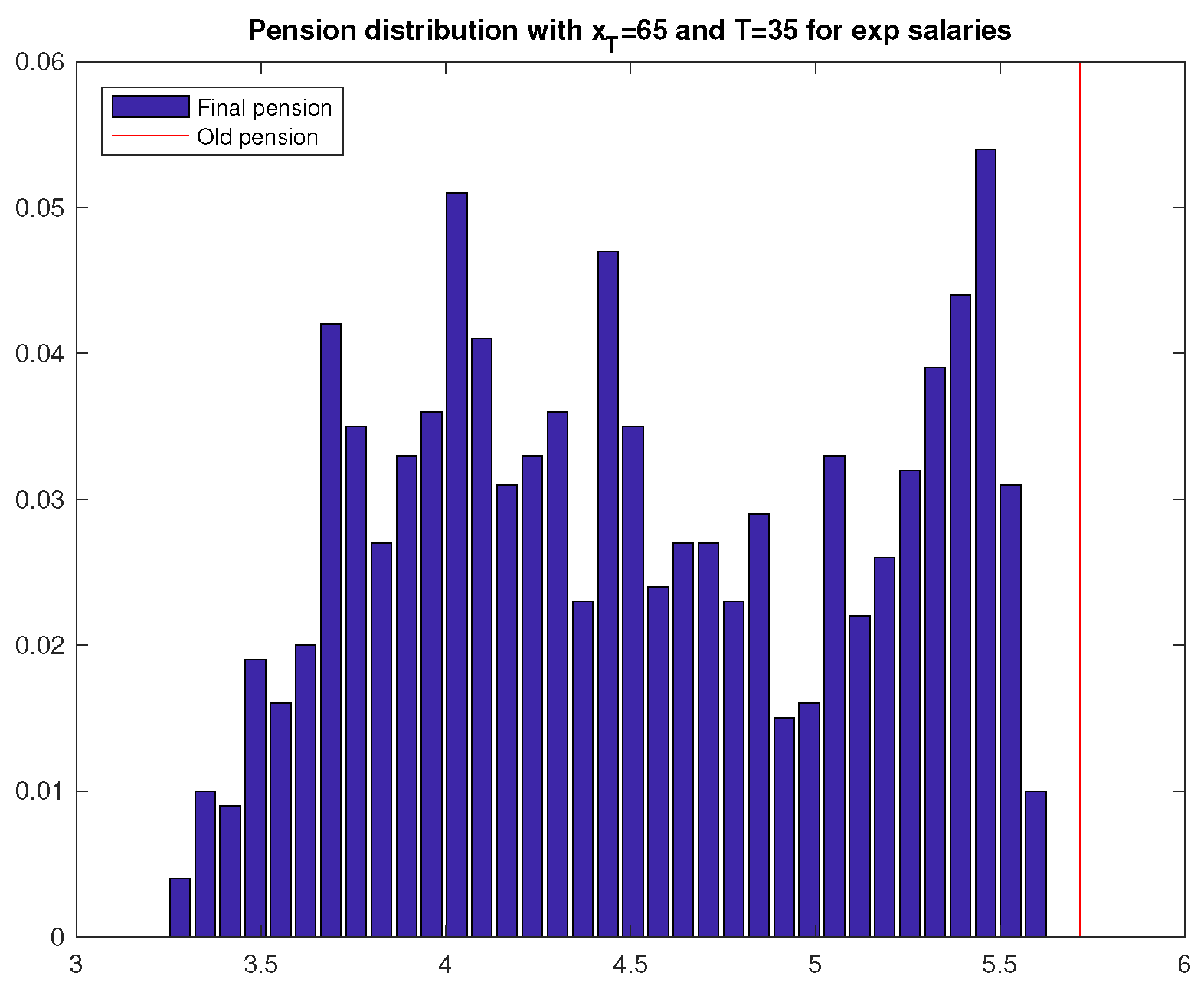

- Figure 5 reports, in the case of exponential salary growth, the distribution, over the 1000 scenarios, of the final pension that the retiree will receive; the old pension is also indicated, as a benchmark.

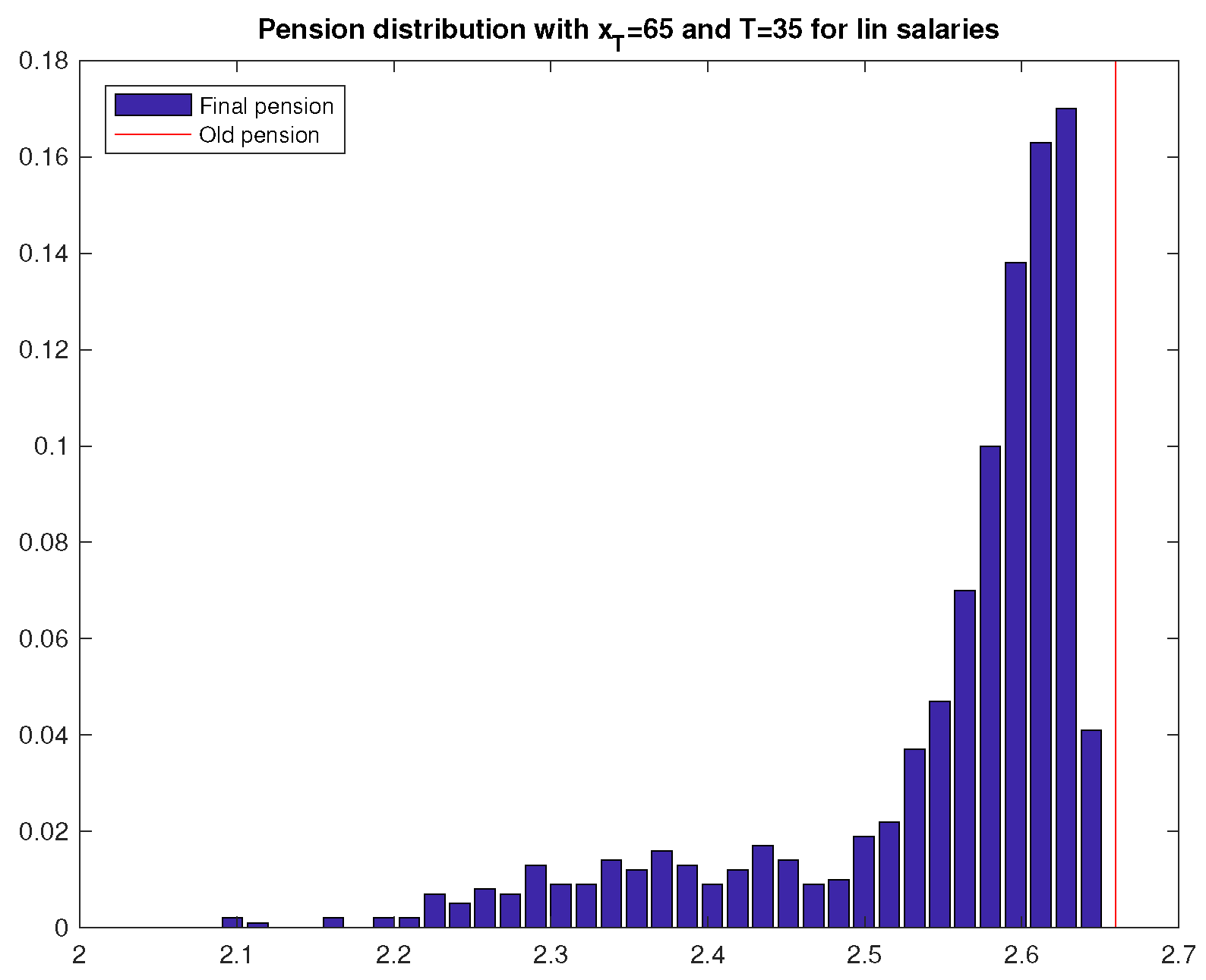

- Figure 6 reports, in the case of linear salary growth, the distribution, over the 1000 scenarios, of the final pension that the retiree will receive; the old pension is also indicated, as a benchmark.

- In the case of exponential salary growth, the final pension is distributed more uniformly between 3.3 and 5.6 (the old pension being 5.7), while for the linear salary growth, there is a large concentration of final pension on the immediate left of the target, between 2.5 and the target, 2.66.

- That observed above is due to the fact that it is easier to reach the target in the case of a linear increase than in the case of an exponential increase, because (as observed in Point 3 above) the gap between old and new pensions is larger with the exponential increase than with the linear increase.

- The fact that it is relatively easy to approach the target with the linear increase is consistent with the rate of increase of the annual targets (see Table 1). This rate lies between the return on the riskless asset () and the expected return on the risky asset (); oppositely, with an exponential salary increase, the rate of increase of annual targets is , which is larger than the expected return on the risky asset.

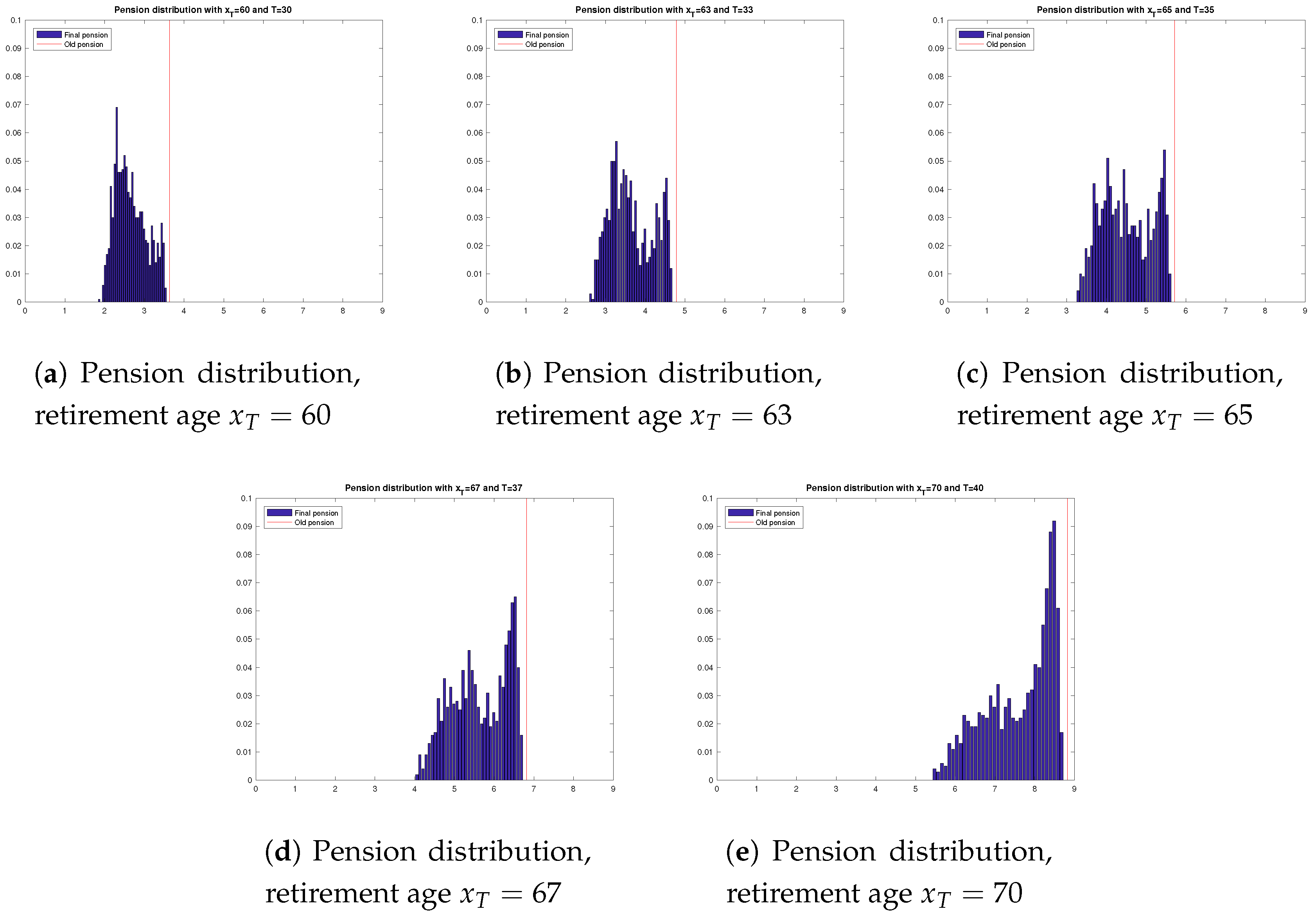

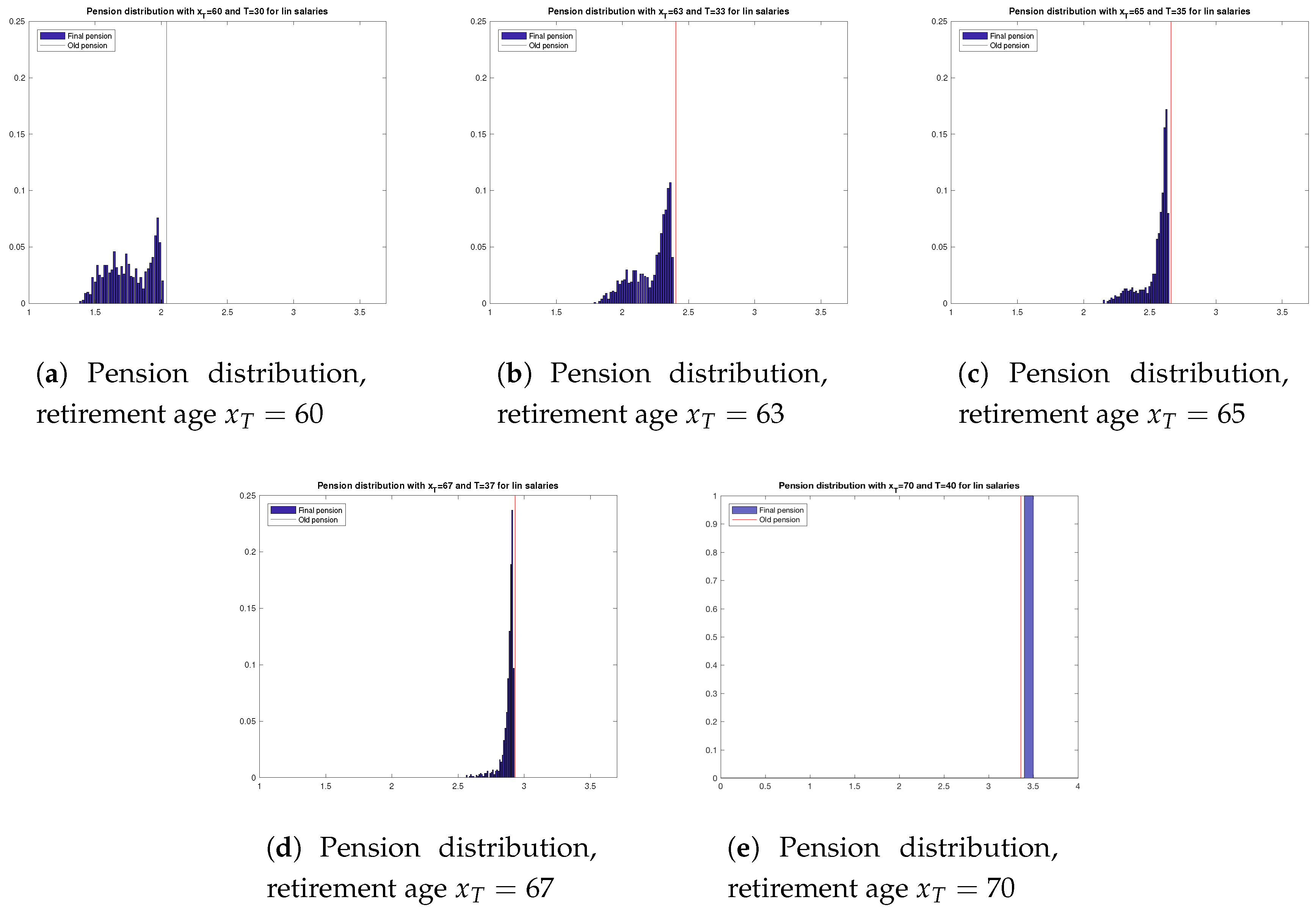

6. Changing the Retirement Age

- The comparison between exponential and linear salary increases confirms what was already observed in Section 5.2 at all ages: the distribution of the final pension is more spread out in the area on the left of the old pension in the case of an exponential salary increase, while it is more peaked immediately on the left of the old pension in the case of the linear target, showing a greater chance of approaching the target in the case of a linear increase.

- With both salary increases, we observe that it is easier to reach the target with an older retirement age: a higher retirement age means a lower gap between the old and the total pension. This is intuitive and expected, and is due to different reasons: (i) because of actuarial fairness principles, as retirement age increases, the price of lifetime annuity decreases; (ii) a higher retirement age also means that the fund grows for a longer period of time, which means that a higher lump sum is converted into pension. These two factors imply that, as retirement age increases, final pension increases, ceteris paribus.

- In the extreme case of linear salary increase and retirement age equal to 70, the difference between the old and the new pension is so small that investing in the riskless asset for the entire working life (40 years) is sufficient to cover the gap, and the final pension turns out to be higher than the old pension in of cases.

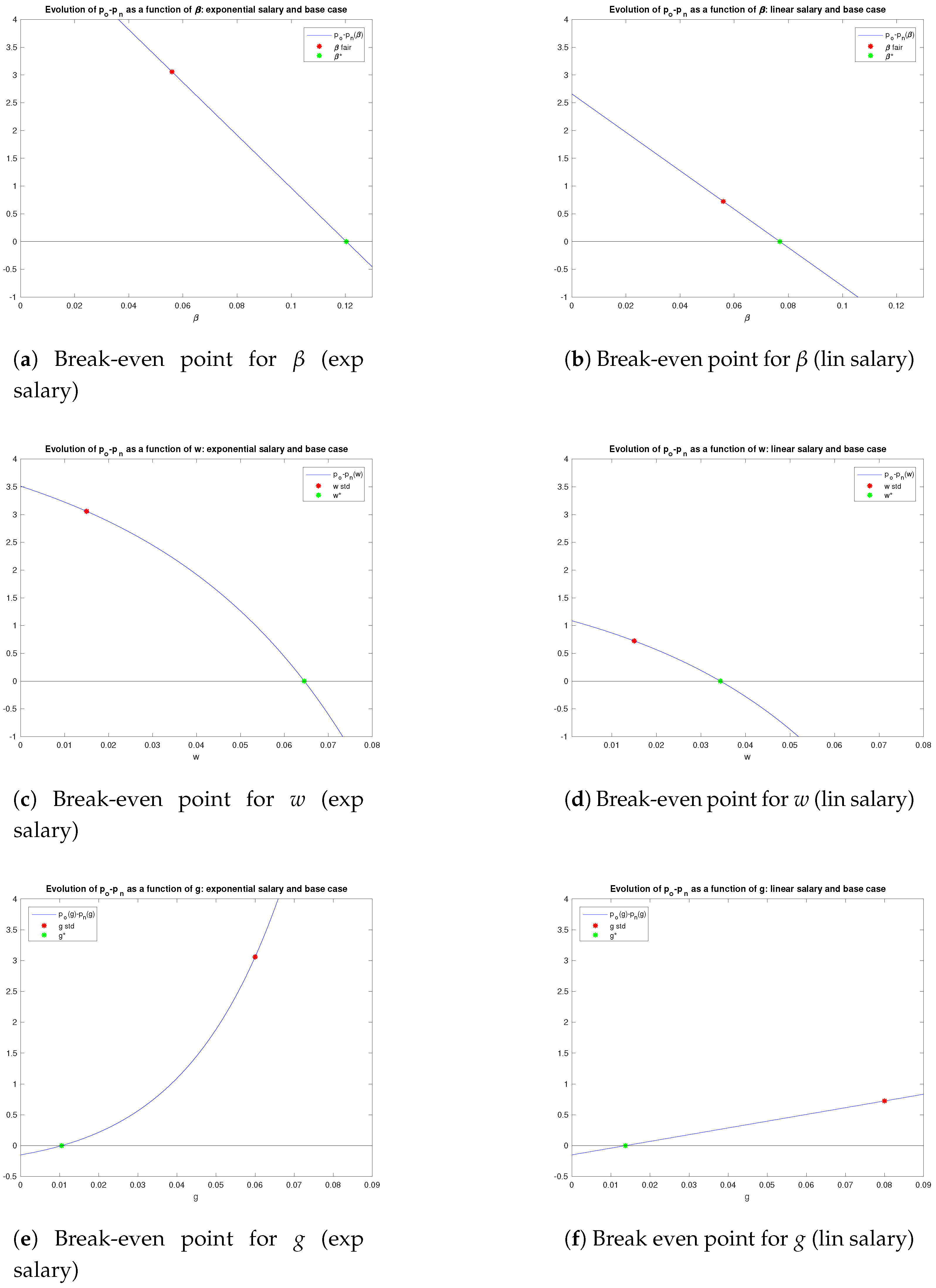

7. Break Even Points

- The difference between the old and new pensions decreases with , i.e., it increases with the price of the annuity . This is obvious, because the old pension is not affected by the price of the annuity, while the new pension is affected by and increases with it; therefore, as increases, increases, and decreases. With exponential increase, the old and new pensions are equal when , which corresponds to the price of the unitary annuity equal to approximately 8.33, against the base value of 17.785; with a linear increase, the old and new pensions are equal when approximately , which corresponds to the price of the unitary annuity equal to 12.82, against the base value of 17.785.

- The difference between the old and new pensions decreases with w. This is again obvious, because the old pension is not affected by the mean GDP growth rate w, while the new pension is affected by w and increases with it; therefore, as w increases, the new pension increases, and the gap between the old and new pensions decreases. With an exponential increase, the old and the new pensions are equal with a mean GDP of approximately . With a linear increase, the old and new pensions are equal with a mean GDP of approximately .

- The difference between the old and new pensions increases with g. This result is interesting, because both the old and new pensions are positively correlated with salary growth g, but to different extents: the old pension is affected by it only via the final salary that is used to calculate the pension income, whereas the new pension is affected by it via the yearly contributions that are paid into the fund and that accumulate until retirement. Figure 9e,f suggest that the impact of g on the old pension is larger than that on the new pension, leading to a larger gap in the case where g increases.

- The break-even point for the salary increase rate is about for the exponential salary increase, about for a linear increase. This result indicates that, with a sufficiently small salary increase, the old and new pensions coincide. In the presence of salary increase rates that are smaller than the break-even point, the new pension is larger than the old one. This is consistent with what was mentioned in Point 3 in Section 5.2: the effect of the pension reform is more significant for workers with dynamic careers than for workers with stagnant careers.

8. Conclusions

Author Contributions

Acknowledgments

Conflicts of Interest

References

- Battocchio, Paolo, and Menoncin Francesco. 2004. Optimal pension management in a stochastic framework. Insurance: Mathematics and Economics 34: 79–95. [Google Scholar] [CrossRef]

- Bordley, Robert, and Marco LiCalzi. 2000. Decision analysis using targets instead of utility functions. Decisions in Economics and Finance 23: 53–74. [Google Scholar] [CrossRef]

- Borella, Margherita, and Flavia Coda Moscarola. 2006. Distributive properties of pension systems: A simulation of the italian transition from defined benefit to notional defined contribution. Giornale Degli Economisti e Annali di Economia 65: 95–126. [Google Scholar]

- Borella, Margherita, and Flavia Coda Moscarola. 2010. Microsimulation of pension reforms: Behavioural versus nonbehavioural approach. Journal of Pension Economics and Finance 9: 583–607. [Google Scholar] [CrossRef]

- Borella, Margherita, and Flavia Coda Moscarola. 2015. The 2011 pension reform in italy and its effects on current and future retirees. 151/15. Turin, TO, Italy: CeRP (Center for Research on Pensions and Welware Policies), pp. 1–54. [Google Scholar]

- Börsch-Supan, Axel. 2005. From traditional db to notional dc systems: the pension reform process in sweden, italy, and germany. Journal of the European Economic Association 3: 458–465. [Google Scholar]

- Boulier, Jean-Franç, Shao Juan Huang, and Grégory Taillard. 2001. Optimal management under stochastic interest rates: the case of a protected defined contribution pension fund. Insurance: Mathematics and Economics 28: 173–189. [Google Scholar] [CrossRef]

- Boulier, Jean-Franç, Stéphane Michel, and Vanessa Wisnia. 1996. Optimizing investment and contribution policies of a defined benefit pension fund. Paper presented at the 6th AFIR Colloquium, Niirnberg, Germany, October 1–3; pp. 593–607. [Google Scholar]

- Boulier, Jean-Franç, Etienne Trussant, and Daniele Florens. 1995. A dynamic model for pension funds management. Paper presented at the 5th AFIR International Colloquium, Brussels, Belgium; pp. 361–384. Available online: http://www.actuaries.org/AFIR/colloquia/Brussels/Boulier-Florens-Trussant.pdf (accessed on 30 March 2018).

- Bucciol, Alessandro, Laura Cavalli, Igor Fedotenkov, Paolo Pertile, Veronica Polin, Nicole Sartor, and Alessandro Sommacal. 2017. A large scale olg model for the analysis of the redistributive effects of policy reforms. European Journal of Political Economy 48: 104–127. [Google Scholar] [CrossRef]

- Cairns, Andrew. 2000. Some notes on the dynamics and optimal control of stochastic pension fund models in continuous time. ASTIN Bulletin 30: 19–55. [Google Scholar] [CrossRef]

- Cairns, Andrew, David Blake, and Kevin Dowd. 2006. Stochastic lifestyling: Optimal dynamic asset allocation for defined-contribution pension plans. Journal of Economic Dynamic and Control 30: 843–877. [Google Scholar] [CrossRef]

- Deelstra, Griselda, Martino Grasselli, and Pierre-François Koehl. 2003. Optimal investment strategies in the presence of a minimum guarantee. Insurance: Mathematics and Economics 33: 189–207. [Google Scholar] [CrossRef]

- Di Giacinto, Marina, Salvatore Federico, and Fausto Gozzi. 2011. Pension funds with a minimum guarantee: A stochastic control approach. Finance and Stochastic 15: 297–342. [Google Scholar] [CrossRef]

- Di Giacinto, Marina, Salvatore Federico, Fausto Gozzi, and Elena Vigna. 2014. Income drawdown option with minimum guarantee. European Journal of Operational Research 234: 610–24. [Google Scholar] [CrossRef]

- Gerrard, Russell, Steven Haberman, and Elena Vigna. 2004. Optimal investment choices post retirement in a defined contribution pension scheme. Insurance: Mathematics and Economics 35: 321–42. [Google Scholar] [CrossRef]

- Gerrard, Russell, Steven Haberman, and Elena Vigna. 2006. The management of de-cumulation risks in a defined contribution pension scheme. North American Actuarial Journal 10: 84–110. [Google Scholar] [CrossRef]

- Gerrard, Russell, Bjarne Højgaard, and Elena Vigna. 2012. Choosing the optimal annuitization time post retirement. Quantitative Finance 12: 1143–59. [Google Scholar] [CrossRef]

- Haberman, Steven, and Elena Vigna. 2002. Optimal investment strategies and risk measures in defined contribution pension schemes. Insurance: Mathematics and Economics 31: 35–69. [Google Scholar] [CrossRef]

- Jessen, Robin, Davud Rostam-Afschar, and Sebastian Schmitz. 2018. How important is precautionary labour supply? Oxford Economic Papers, 1–24. [Google Scholar] [CrossRef]

- Kahneman, Daniel, and Amos Tversky. 1979. Prospect theory: An analysis of decision under risk. Econometrica 47: 263–91. [Google Scholar] [CrossRef]

- Li, Duan, and Wan-Lung Ng. 2000. Optimal dynamic portfolio selection: Multiperiod mean-variance formulation. Mathematical Finance 10: 387–406. [Google Scholar] [CrossRef]

- Menoncin, Francesco, and Elena Vigna. 2017. Mean-variance target-based optimisation for defined contribution pension schemes in a stochastic framework. Insurance: Mathematics and Economics 76: 172–84. [Google Scholar] [CrossRef]

- Vigna, Elena. 2014. On efficiency of mean-variance based portfolio selection in DC pension schemes. Quantitative Finance 14: 237–58. [Google Scholar] [CrossRef]

- Zhou, Xun Yu, and Duan Li. 2000. Continuous-time mean-variance portfolio selection: A stochastic LQ framework. Applied Mathematics and Optimization 42: 19–33. [Google Scholar] [CrossRef]

| 1. | In a NDC pension system pension benefits are paid out from current contributions, as in a PAYG system, but the link between benefits and contributions is defined via a defined-contribution formula. For this reason, a NDC pension system is not funded, it is a PAYG system. For a critical review of the pension reform strategy that turns defined benefit (DB) public PAYG systems into NDC systems see Börsch-Supan (2005). |

| 2. | We will approximate the value with the Newton–Raphson algorithm. |

| 3. | For a more accurate and realistic model for the salary growth in the Italian context, we refer to the micro-simulation model developed by Borella and Coda Moscarola (2006, 2010). |

| 4. | In the following figures, we have denoted the “sub-optimal” constrained investment strategy by and the “sub-optimal” constrained fund growth by for the sake of simplicity. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 5.716 | 2.657 | 0.7 | 0.325 | 0.078 | 8.166 | |

| 2.66 | 1.936 | 0.7 | 0.509 | 0.049 | 3.8 |

| T | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 60 | 30 | 20.95 | 0.048 | 3.63 | 1.57 | 0.6 | 0.26 | 2.04 | 1.26 | 0.6 | 0.37 |

| 63 | 33 | 19.11 | 0.052 | 4.78 | 2.15 | 0.66 | 0.3 | 2.4 | 1.63 | 0.66 | 0.45 |

| 65 | 35 | 17.88 | 0.056 | 5.72 | 2.66 | 0.7 | 0.33 | 2.66 | 1.94 | 0.7 | 0.51 |

| 67 | 37 | 16.64 | 0.06 | 6.81 | 3.29 | 0.74 | 0.36 | 2.93 | 2.3 | 0.74 | 0.58 |

| 70 | 40 | 14.81 | 0.068 | 8.82 | 4.56 | 0.8 | 0.41 | 3.36 | 2.98 | 0.8 | 0.71 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Milazzo, A.; Vigna, E. The Italian Pension Gap: A Stochastic Optimal Control Approach. Risks 2018, 6, 48. https://doi.org/10.3390/risks6020048

Milazzo A, Vigna E. The Italian Pension Gap: A Stochastic Optimal Control Approach. Risks. 2018; 6(2):48. https://doi.org/10.3390/risks6020048

Chicago/Turabian StyleMilazzo, Alessandro, and Elena Vigna. 2018. "The Italian Pension Gap: A Stochastic Optimal Control Approach" Risks 6, no. 2: 48. https://doi.org/10.3390/risks6020048

APA StyleMilazzo, A., & Vigna, E. (2018). The Italian Pension Gap: A Stochastic Optimal Control Approach. Risks, 6(2), 48. https://doi.org/10.3390/risks6020048