On the Compound Binomial Risk Model with Delayed Claims and Randomized Dividends

Abstract

:1. Introduction

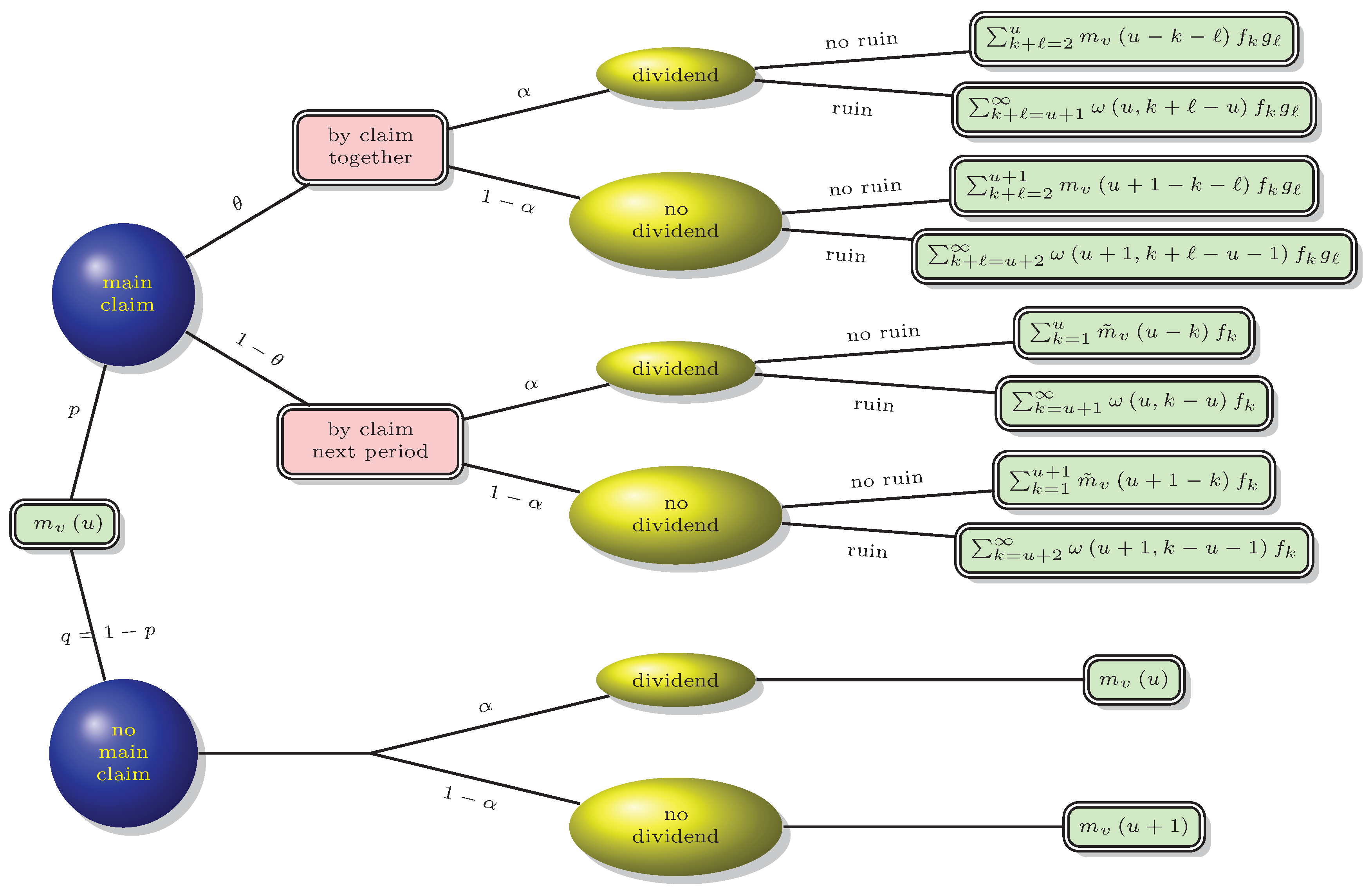

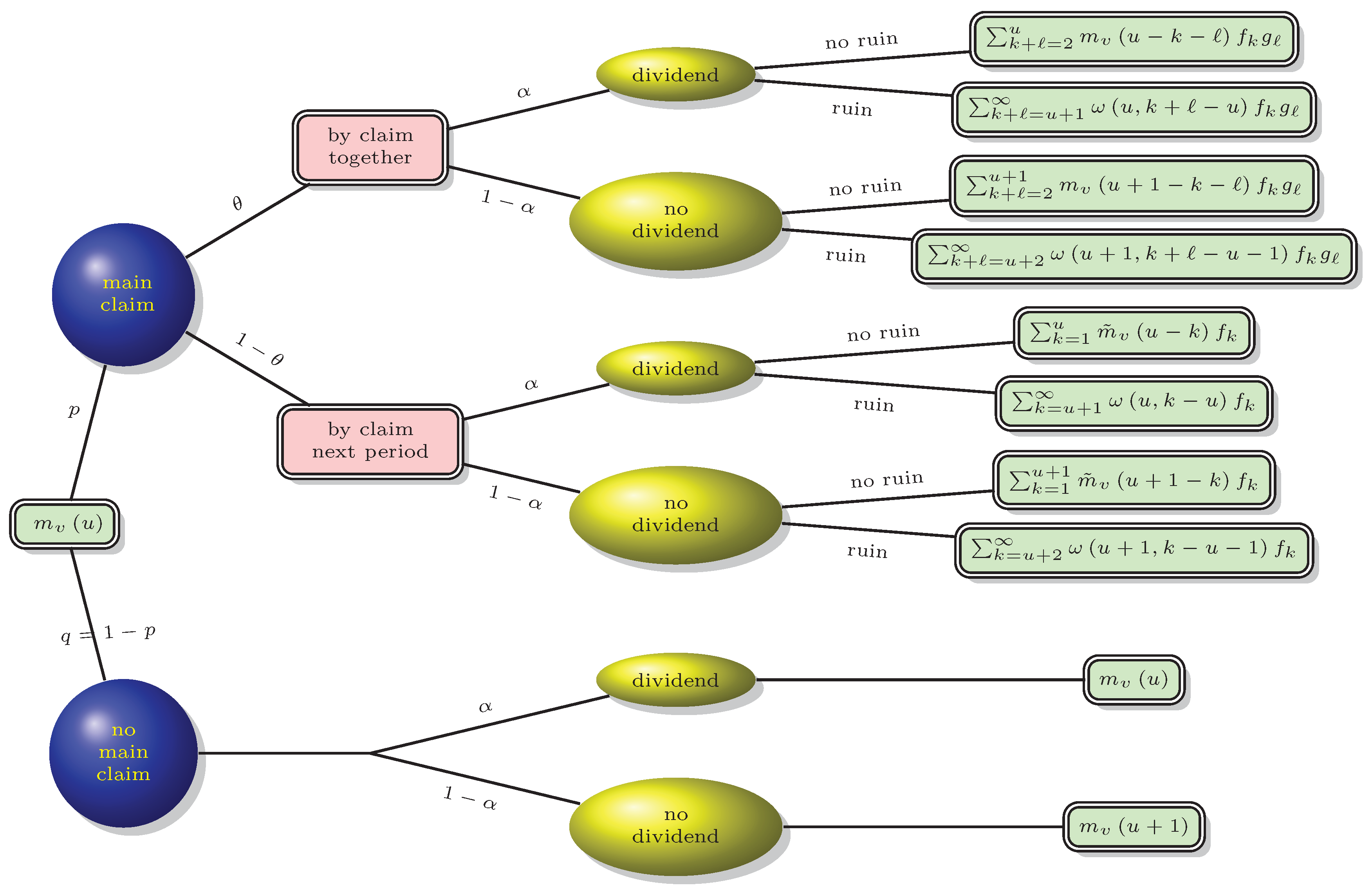

2. The Model

- is the surplus level after the claims and dividends payable at time t (at the end of period ) but before the premiums receivable at time t (at the beginning of period ).

- When both dividends and claims are payable at time t, dividends are paid before claims.

- It is worth noting that dividend payments at time i are triggered by two conditions, and . No dividend is payable if at least one condition is voided.

- If , that is, by-claims always occur simultaneously with their main claims, then it reduces to the model in Tan and Yang (2006).

- If , then it reduces to the compound binomial model with time-correlation only; see, for example, Yuen and Guo (2001).

- If both and , then the model becomes an original compound binomial model.

3. Main Results

3.1. The Case of .

- X: one main claim only with p.f. f;

- : one main claim plus its by-claim with p.f. ;

- Y: one by-claim only with p.f. g;

- : one main claim, its by-claim and a delayed by-claim with p.f. ;

- : one main claim and an undetermined by-claim with p.f. ;

- : one delayed by-claim with undetermined main and by-claims with p.f. .

- Firstly, we have and .

- Additionally,which gives , and for ,The last inequality follows from the positive safety loading condition assumed previously.

- Therefore, is a strictly increasing function on the interval that suffices to prove the existence of a unique solution to the equation .

3.2. The Case of .

- When , both surplus processes must not pay dividends in the first period.

- When , the first period may be subject to a dividend payment.

4. Final Remarks and Future Work

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Ahn, Soohan, Andrei L. Badescu, Eric C. K. Cheung, and Jeong-Rae Kim. 2018. An IBNR-RBNS insurance risk model with marked Poisson arrivals. Insurance: Mathematics and Economics 79: 26–42. [Google Scholar] [CrossRef]

- Avram, Florin, and Matija Vidmar. 2017. First passage problems for upwards skip-free random walks via the Φ, W, Z paradigm. arXiv, arXiv:1708.06080v1. [Google Scholar]

- Bao, Zhen-hua. 2007. A note on the compound binomial model with randomized dividend strategy. Applied Mathematics and Computation 194: 276–86. [Google Scholar] [CrossRef]

- Cheng, Shixue, Hans U. Gerber, and Elias S. W. Shiu. 2000. Discounted probabilities and ruin theory in the compound binomial model. Insurance: Mathematics and Economics 26: 239–50. [Google Scholar] [CrossRef]

- Cheung, Eric C. K., and David Landriault. 2010. A generalized penalty function with the maximum surplus prior to ruin in a MAP risk model. Insurance: Mathematics and Economics 46: 127–34. [Google Scholar] [CrossRef]

- Dassios, Angelos, and Hongbiao Zhao. 2013. A risk model with delayed claims. Journal of Applied Probability 50: 686–702. [Google Scholar] [CrossRef]

- Dickson, David C. M. 1994. Some comments on the compound binomial model. ASTIN Bulletin 24: 33–45. [Google Scholar] [CrossRef]

- Dos Reis, Alfredo D. Egídio. 2004. The compound binomial model revisited. Paper presented at the 35th International ASTIN Colloquium, Bergen, Norway, June 6–9; Available online: http://www.actuaries.org/ASTIN/Colloquia/Bergen/EgidiodosReis.pdf (accessed on 12 January 2018).

- Gerber, Hans U. 1988. Mathematical fun with the compound binomial process. ASTIN Bulletin 18: 161–68. [Google Scholar] [CrossRef]

- Gerber, Hans U., and Elias S. W. Shiu. 1998. On the time value of ruin. North American Actuarial Journal 2: 48–71. [Google Scholar] [CrossRef]

- He, Lei, and Xiangqun Yang. 2010. The compound binomial model with randomly paying dividends to shareholders and policyholders. Insurance: Mathematics and Economics 46: 443–49. [Google Scholar] [CrossRef]

- Landriault, David. 2008. Randomized dividends in the compound binomial model with a general premium rate. Scandinavian Actuarial Journal 2008: 1–15. [Google Scholar] [CrossRef]

- Lefèvre, Claude, and Stéphane Loisel. 2008. On finite-time ruin probabilities for classical risk models. Scandinavian Actuarial Journal 2008: 41–60. [Google Scholar] [CrossRef]

- Li, Jin-zhu, and Rong Wu. 2015. The Gerber-Shiu discounted penalty function for a compound binomial risk model with by-claims. Acta Mathematicae Applicatae Sinica, English Series 31: 181–90. [Google Scholar] [CrossRef]

- Li, Shuanming. 2008. The moments of the present value of total dividends in the compound binomial model under a constant dividend barrier and stochastic interest rates. Australian Actuarial Journal 14: 175–92. [Google Scholar]

- Liu, Guoxin, and Jinyan Zhao. 2007. Joint distributions of some actuarial random vectors in the compound binomial model. Insurance: Mathematics and Economics 40: 95–103. [Google Scholar] [CrossRef]

- Shiu, Elias S. W. 1989. The probability of eventual ruin in the compound binomial model. ASTIN Bulletin 19: 179–90. [Google Scholar] [CrossRef]

- Spitzer, Frank. 1964. Principles of Random Walk. New York: Springer. [Google Scholar]

- Tan, Jiyang, and Xiangqun Yang. 2006. The compound binomial model with randomized decisions on paying dividends. Insurance: Mathematics and Economics 39: 1–18. [Google Scholar] [CrossRef]

- Willmot, Gordan E. 1993. Ruin probabilities in the compound binomial model. Insurance: Mathematics and Economics 12: 133–42. [Google Scholar] [CrossRef]

- Willmot, Gordan E. 2007. On the discounted penalty function in the renewal risk model with general interclaim times. Insurance: Mathematics and Economics 41: 17–31. [Google Scholar] [CrossRef]

- Wu, Xueyuan, and Shuanming Li. 2012. On a discrete time risk model with time-delayed claims and a constant dividend barrier. Insurance Markets and Companies: Analysis and Actuarial Computations 3: 50–57. [Google Scholar]

- Wu, Xueyuan, and Kam Chuen Yuen. 2004. An interaction risk model with delayed claims. Paper presented at the 35th International ASTIN Colloquium, Bergen, Norway, June 6–9; Available online: http://www.actuaires.org/ASTIN/Colloquia/Bergen/Wu_Yuen.pdf (accessed on 8 September 2015).

- Wüthrich, Mario V., and Michael Merz. 2008. Stochastic Claims Reserving Methods in Insurance. Hoboken: Wiley. [Google Scholar]

- Xiao, Yuntao, and Junyi Guo. 2007. The compound binomial risk model with time-correlated claims. Insurance: Mathematics and Economics 41: 124–33. [Google Scholar] [CrossRef]

- Yuen, Kam Chuen, Mi Chen, and Kam Pui Wat. 2017. On the expected penalty functions in a discrete semi-Markov risk model with randomized dividends. Journal of Computational and Applied Mathematics 311: 239–51. [Google Scholar] [CrossRef]

- Yuen, Kam Chuen, Junyi Guo, and Kai Wang Ng. 2005. On ultimate ruin in a delayed-claims risk model. Journal of Applied Probability 42: 163–74. [Google Scholar] [CrossRef]

- Yuen, Kam Chuen, and Junyi Guo. 2001. Ruin probabilities for time-correlated claims in the compound binomial model. Insurance: Mathematics and Economics 29: 47–57. [Google Scholar] [CrossRef]

- Yuen, Kam Chuen, Jinzhu Li, and Rong Wu. 2013. On a discrete-time risk model with delayed claims and dividends. Risk and Decision Analysis 4: 3–16. [Google Scholar]

{kind=link}

| Probability | Current Period | Additional Impact on the Next Period | |

|---|---|---|---|

| Case 1 | No claim | Nil | |

| Case 2 | Main claim and by-claim | Nil | |

| Case 3 | Main claim | By-claim |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wat, K.P.; Yuen, K.C.; Li, W.K.; Wu, X. On the Compound Binomial Risk Model with Delayed Claims and Randomized Dividends. Risks 2018, 6, 6. https://doi.org/10.3390/risks6010006

Wat KP, Yuen KC, Li WK, Wu X. On the Compound Binomial Risk Model with Delayed Claims and Randomized Dividends. Risks. 2018; 6(1):6. https://doi.org/10.3390/risks6010006

Chicago/Turabian StyleWat, Kam Pui, Kam Chuen Yuen, Wai Keung Li, and Xueyuan Wu. 2018. "On the Compound Binomial Risk Model with Delayed Claims and Randomized Dividends" Risks 6, no. 1: 6. https://doi.org/10.3390/risks6010006

APA StyleWat, K. P., Yuen, K. C., Li, W. K., & Wu, X. (2018). On the Compound Binomial Risk Model with Delayed Claims and Randomized Dividends. Risks, 6(1), 6. https://doi.org/10.3390/risks6010006