Appendix A.1. Mean Forecast and Confidence Intervals for αi,t, i = 1,…,3 Forecasts

:

alpha1 y_lo80 y_hi80 y_lo95 y_hi95

13 0.7432724 0.6852024 0.8013425 0.6544620 0.8320829

14 0.7357374 0.6776673 0.7938074 0.6469269 0.8245478

15 0.7378042 0.6797342 0.7958742 0.6489938 0.8266147

16 0.7408417 0.6827717 0.7989118 0.6520313 0.8296522

17 0.7407904 0.6827204 0.7988604 0.6519800 0.8296009

18 0.7404501 0.6823801 0.7985201 0.6516396 0.8292605

19 0.7403603 0.6822903 0.7984303 0.6515498 0.8291707

20 0.7403981 0.6823281 0.7984681 0.6515876 0.8292085

21 0.7404788 0.6824087 0.7985488 0.6516683 0.8292892

22 0.7404786 0.6824086 0.7985487 0.6516682 0.8292891

23 0.7404791 0.6824091 0.7985491 0.6516686 0.8292895

24 0.7404758 0.6824058 0.7985458 0.6516654 0.8292863

:

alpha2 y_lo80 y_hi80 y_lo95 y_hi95

13 -1.250640 -1.351785 -1.149495 -1.405328 -1.095952

14 -1.243294 -1.344439 -1.142149 -1.397982 -1.088606

15 -1.241429 -1.342574 -1.140284 -1.396117 -1.086741

16 -1.243868 -1.345014 -1.142723 -1.398557 -1.089180

17 -1.244483 -1.345628 -1.143338 -1.399171 -1.089795

18 -1.241865 -1.343010 -1.140719 -1.396553 -1.087177

19 -1.240814 -1.341959 -1.139669 -1.395502 -1.086126

20 -1.240371 -1.341516 -1.139226 -1.395059 -1.085683

21 -1.240237 -1.341382 -1.139092 -1.394925 -1.085549

22 -1.240276 -1.341421 -1.139131 -1.394964 -1.085588

23 -1.240329 -1.341474 -1.139184 -1.395017 -1.085641

24 -1.240308 -1.341453 -1.139163 -1.394996 -1.085620

:

alpha3 y_lo80 y_hi80 y_lo95 y_hi95

13 4.584836 4.328843 4.757406 4.215410 4.870840

14 4.546167 4.307253 4.849862 4.163634 4.993482

15 4.527651 4.201991 4.803004 4.042913 4.962082

16 4.513810 4.216525 4.850160 4.048812 5.017874

17 4.517643 4.176214 4.828735 4.003502 5.001446

18 4.523109 4.203064 4.866713 4.027406 5.042371

19 4.522772 4.178489 4.848760 4.001079 5.026170

20 4.521846 4.191833 4.866066 4.013374 5.044524

21 4.521382 4.177560 4.854171 3.998472 5.033259

22 4.521451 4.186714 4.864755 4.007248 5.044222

23 4.521772 4.178995 4.857897 3.999300 5.037591

24 4.521862 4.184734 4.864155 4.004903 5.043987

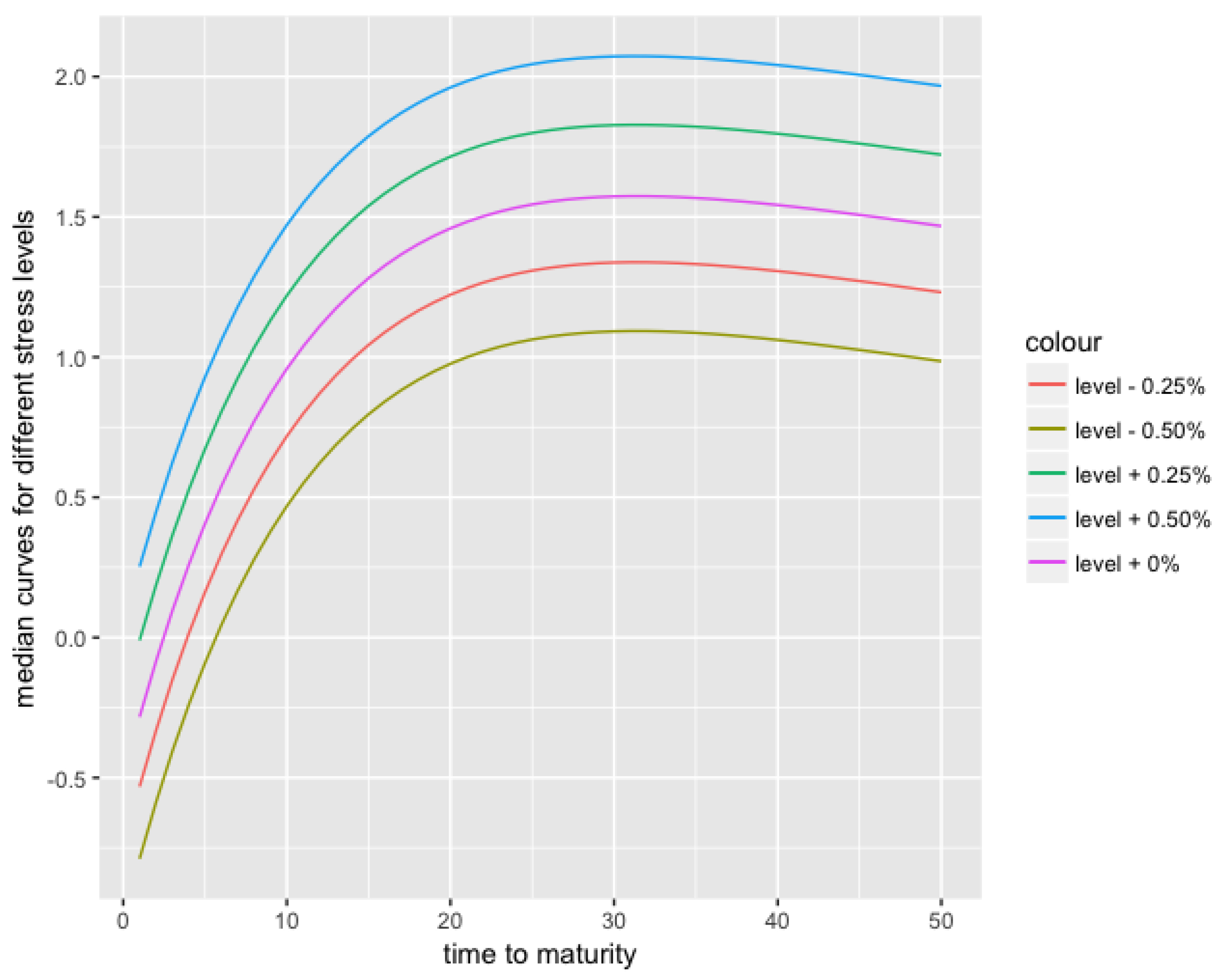

Appendix A.2. Stressed Forecast (α1,t + 0.5%) and Confidence Intervals for αi,t, i = 1,…,3 Forecasts

:

alpha1 y_lo80 y_hi80 y_lo95 y_hi95

13 1.25 1.19193 1.30807 1.16119 1.33881

14 1.25 1.19193 1.30807 1.16119 1.33881

15 1.25 1.19193 1.30807 1.16119 1.33881

16 1.25 1.19193 1.30807 1.16119 1.33881

17 1.25 1.19193 1.30807 1.16119 1.33881

18 1.25 1.19193 1.30807 1.16119 1.33881

19 1.25 1.19193 1.30807 1.16119 1.33881

20 1.25 1.19193 1.30807 1.16119 1.33881

21 1.25 1.19193 1.30807 1.16119 1.33881

22 1.25 1.19193 1.30807 1.16119 1.33881

23 1.25 1.19193 1.30807 1.16119 1.33881

24 1.25 1.19193 1.30807 1.16119 1.33881

:

alpha2 y_lo80 y_hi80 y_lo95 y_hi95

13 -1.222568 -1.323713 -1.121423 -1.377256 -1.067880

14 -1.219401 -1.320546 -1.118256 -1.374089 -1.064713

15 -1.211361 -1.312506 -1.110216 -1.366049 -1.056673

16 -1.216213 -1.317358 -1.115068 -1.370901 -1.061525

17 -1.215266 -1.316411 -1.114121 -1.369954 -1.060578

18 -1.211474 -1.312619 -1.110329 -1.366162 -1.056786

19 -1.210329 -1.311474 -1.109183 -1.365017 -1.055640

20 -1.209610 -1.310755 -1.108465 -1.364298 -1.054922

21 -1.209648 -1.310793 -1.108503 -1.364336 -1.054960

22 -1.209601 -1.310746 -1.108456 -1.364289 -1.054913

23 -1.209688 -1.310833 -1.108542 -1.364376 -1.055000

24 -1.209653 -1.310798 -1.108508 -1.364341 -1.054965

:

alpha3 y_lo80 y_hi80 y_lo95 y_hi95

13 4.500390 4.244398 4.672961 4.130964 4.786394

14 4.482948 4.244035 4.786643 4.100415 4.930263

15 4.441841 4.116182 4.717194 3.957103 4.876272

16 4.441744 4.144459 4.778094 3.976746 4.945808

17 4.439609 4.098181 4.750701 3.925469 4.923413

18 4.447151 4.127105 4.790755 3.951448 4.966412

19 4.446164 4.101881 4.772152 3.924471 4.949562

20 4.445421 4.115407 4.789641 3.936949 4.968099

21 4.445411 4.101589 4.778200 3.922501 4.957289

22 4.445491 4.110754 4.788795 3.931287 4.968262

23 4.445937 4.103160 4.782062 3.923465 4.961756

24 4.446012 4.108885 4.788306 3.929053 4.968137

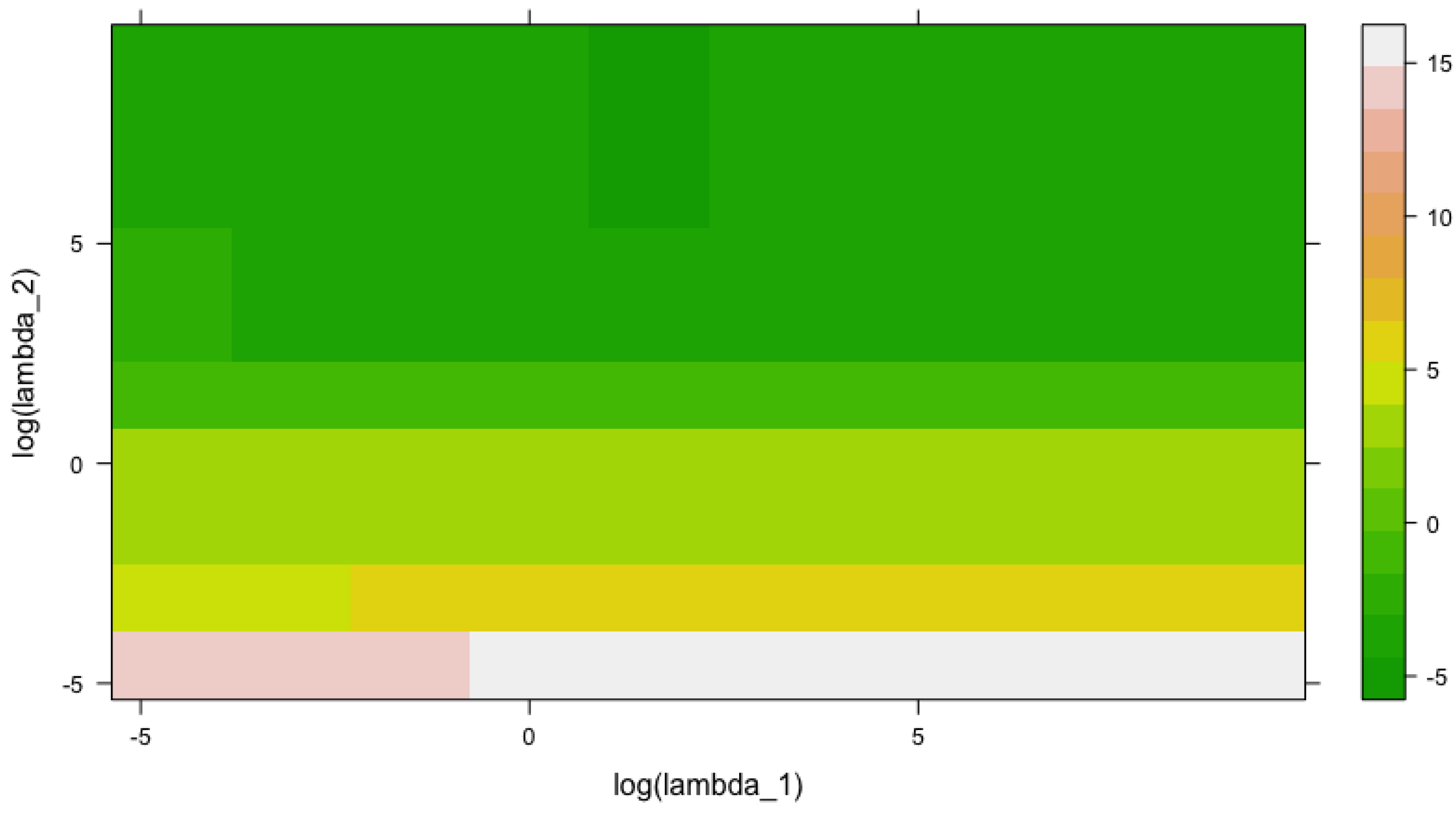

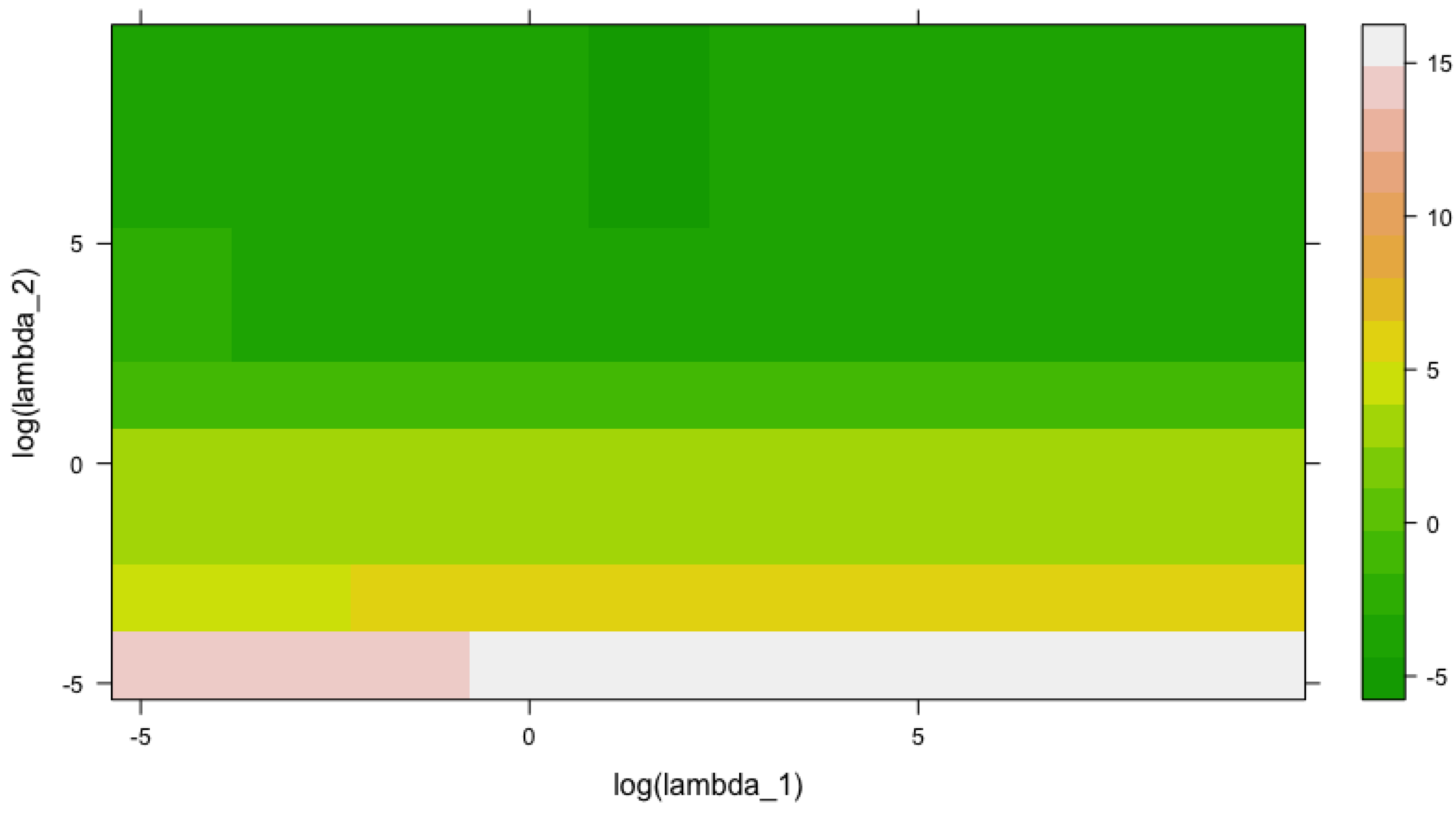

Appendix A.3. Out-of-Sample log(RMSE) as a Function of log(λ1) and log(λ2)

log_lambda1 log_lambda2 log_error

1 -4.605170 -4.605170 13.5039336

2 -3.070113 -4.605170 14.3538621

3 -1.535057 -4.605170 14.7912525

4 0.000000 -4.605170 14.8749375

5 1.535057 -4.605170 14.8928025

6 3.070113 -4.605170 14.8962203

7 4.605170 -4.605170 14.8975776

8 6.140227 -4.605170 14.8976494

9 7.675284 -4.605170 14.8976630

10 9.210340 -4.605170 14.8976715

11 -4.605170 -3.070113 3.9701229

12 -3.070113 -3.070113 4.9644144

13 -1.535057 -3.070113 5.2607788

14 0.000000 -3.070113 5.3208833

15 1.535057 -3.070113 5.3326856

16 3.070113 -3.070113 5.3351784

17 4.605170 -3.070113 5.3357136

18 6.140227 -3.070113 5.3358306

19 7.675284 -3.070113 5.3358557

20 9.210340 -3.070113 5.3358610

21 -4.605170 -1.535057 3.6692928

22 -3.070113 -1.535057 3.5643607

23 -1.535057 -1.535057 3.5063072

24 0.000000 -1.535057 3.4942438

25 1.535057 -1.535057 3.4904354

26 3.070113 -1.535057 3.4881352

27 4.605170 -1.535057 3.4888202

28 6.140227 -1.535057 3.4880668

29 7.675284 -1.535057 3.4886911

30 9.210340 -1.535057 3.4886383

31 -4.605170 0.000000 3.6224691

32 -3.070113 0.000000 3.8313407

33 -1.535057 0.000000 3.8518759

34 0.000000 0.000000 3.8163287

35 1.535057 0.000000 3.7993471

36 3.070113 0.000000 3.7948073

37 4.605170 0.000000 3.7937787

38 6.140227 0.000000 3.7935546

39 7.675284 0.000000 3.7935063

40 9.210340 0.000000 3.7934958

41 -4.605170 1.535057 -1.2115597

42 -3.070113 1.535057 -1.0130537

43 -1.535057 1.535057 -0.5841784

44 0.000000 1.535057 -0.3802817

45 1.535057 1.535057 -0.3109827

46 3.070113 1.535057 -0.2931830

47 4.605170 1.535057 -0.2891586

48 6.140227 1.535057 -0.2882824

49 7.675284 1.535057 -0.2880932

50 9.210340 1.535057 -0.2880524

51 -4.605170 3.070113 -2.0397856

52 -3.070113 3.070113 -3.1729003

53 -1.535057 3.070113 -3.8655596

54 0.000000 3.070113 -3.9279840

55 1.535057 3.070113 -3.9508440

56 3.070113 3.070113 -4.0270316

57 4.605170 3.070113 -4.0831569

58 6.140227 3.070113 -4.0953167

59 7.675284 3.070113 -4.0979447

60 9.210340 3.070113 -4.0985113

61 -4.605170 4.605170 -2.6779260

62 -3.070113 4.605170 -3.4704808

63 -1.535057 4.605170 -4.0404935

64 0.000000 4.605170 -4.2441836

65 1.535057 4.605170 -4.3657802

66 3.070113 4.605170 -4.3923094

67 4.605170 4.605170 -4.3862826

68 6.140227 4.605170 -4.3830293

69 7.675284 4.605170 -4.3820703

70 9.210340 4.605170 -4.3818486

71 -4.605170 6.140227 -3.5007058

72 -3.070113 6.140227 -3.8389274

73 -1.535057 6.140227 -4.1969545

74 0.000000 6.140227 -4.3400025

75 1.535057 6.140227 -4.4179718

76 3.070113 6.140227 -4.3797034

77 4.605170 6.140227 -4.3073100

78 6.140227 6.140227 -4.2866647

79 7.675284 6.140227 -4.2820357

80 9.210340 6.140227 -4.2810151

81 -4.605170 7.675284 -3.7236774

82 -3.070113 7.675284 -4.0057353

83 -1.535057 7.675284 -4.2699684

84 0.000000 7.675284 -4.3569254

85 1.535057 7.675284 -4.4156364

86 3.070113 7.675284 -4.3842360

87 4.605170 7.675284 -4.2759516

88 6.140227 7.675284 -4.2425876

89 7.675284 7.675284 -4.2346514

90 9.210340 7.675284 -4.2328863

91 -4.605170 9.210340 -3.7706268

92 -3.070113 9.210340 -4.0406387

93 -1.535057 9.210340 -4.2776907

94 0.000000 9.210340 -4.3498230

95 1.535057 9.210340 -4.4095778

96 3.070113 9.210340 -4.3860089

97 4.605170 9.210340 -4.2647179

98 6.140227 9.210340 -4.2273624

99 7.675284 9.210340 -4.2183911

100 9.210340 9.210340 -4.2163638

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}