Public Funding, ESG Strategies, and the Risk of Greenwashing: Evidence from Greek Financial and Public Institutions

{kind=link}

{kind=link}

{kind=link}

Abstract

1. Introduction

2. Literature Review

3. Materials and Methods

4. Results

4.1. Quantitative Component: Data Envelopment Analysis (DEA)

- The amount of public or EU funding received for ESG purposes;

- Staff or resource allocation for ESG implementation;

- Administrative expenditures related to ESG programs.

- The number and scope of ESG-related actions (e.g., green investments, social programs);

- ESG scores (where applicable) from third-party agencies or internal assessments;

- Disclosure frequency and transparency index derived from published reports.

4.2. Qualitative Component: Content Analysis of ESG Disclosures

- The presence or absence of verifiable ESG metrics;

- Consistency between declared goals and actual performance indicators;

- The degree of specificity versus vagueness in ESG-related statements;

- The use of third-party certifications or audit references.

4.3. Sample and Data Collection

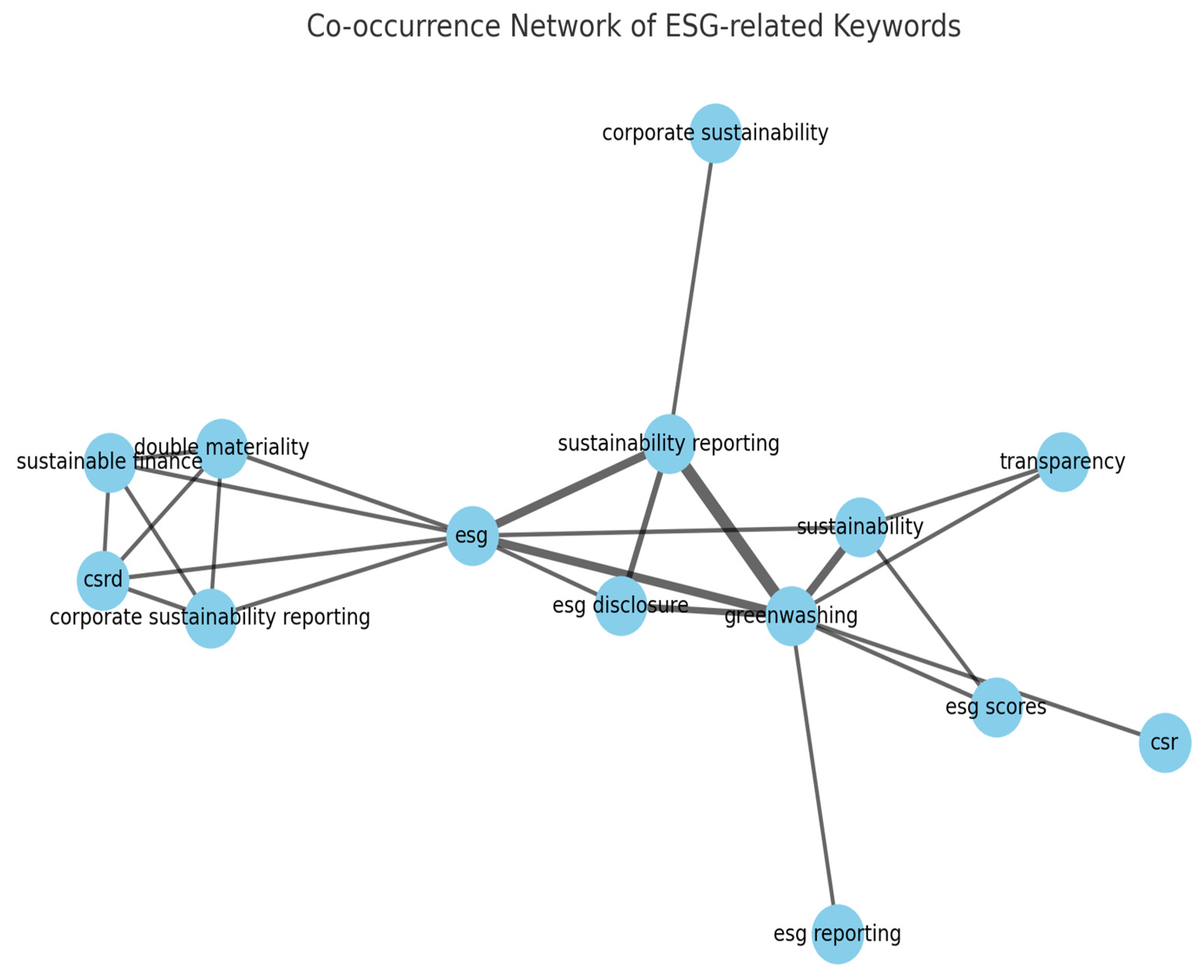

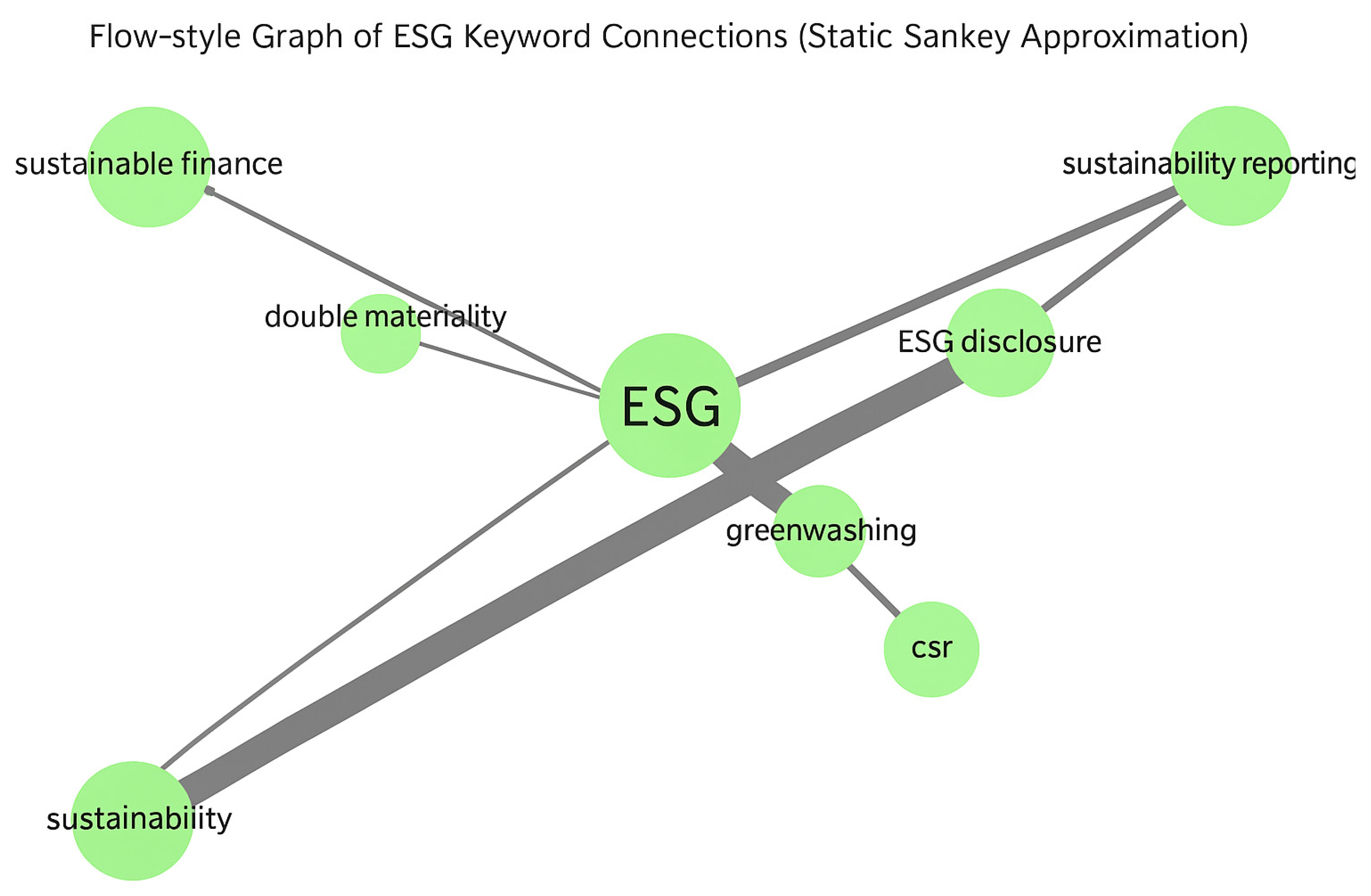

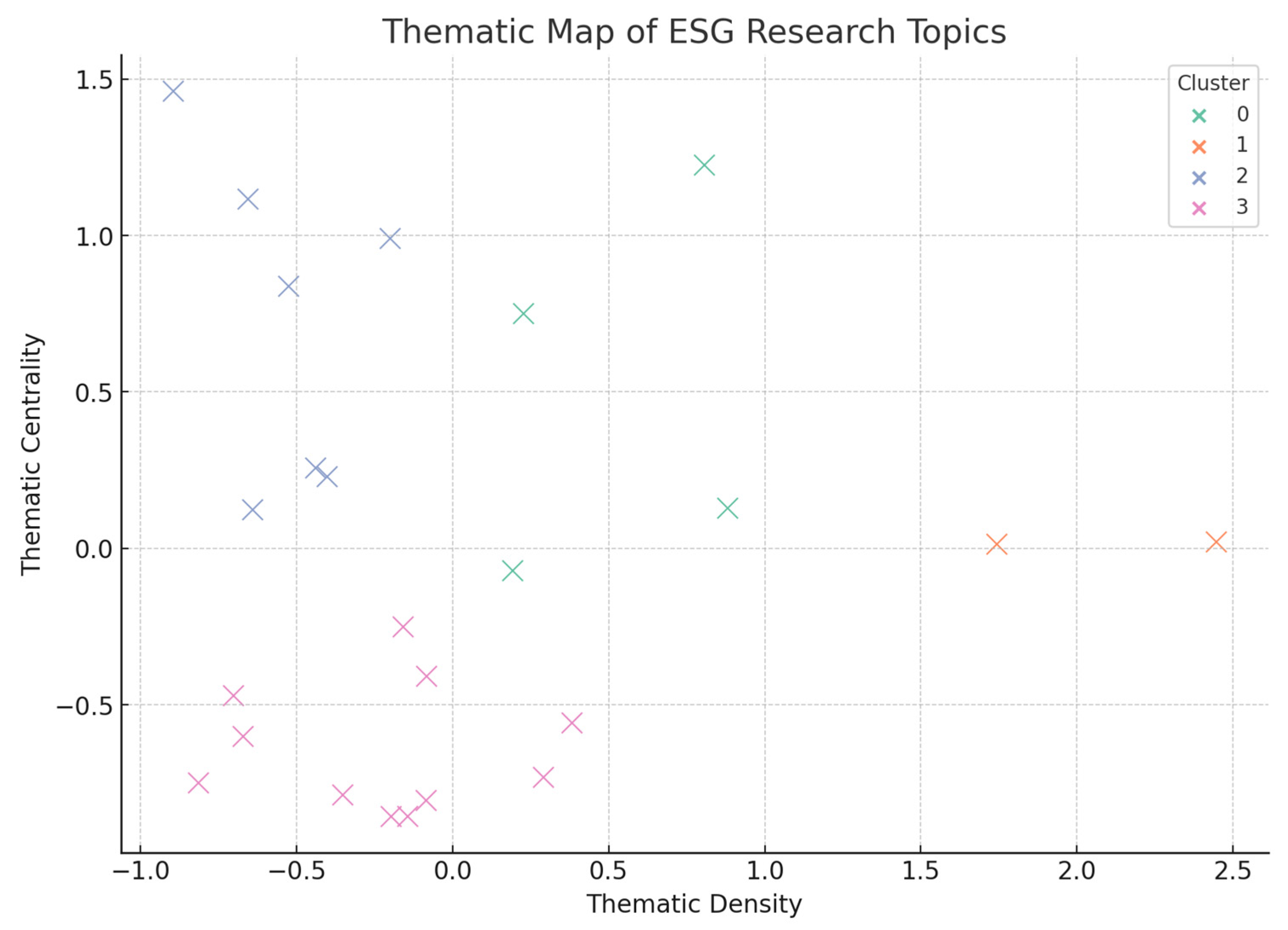

4.4. Bibliometric Analysis

- Co-occurrence network analysis, to identify commonly linked concepts and terminologies.

- Thematic mapping, to distinguish core research areas (e.g., ESG metrics, disclosure quality) from emerging ones (e.g., state funding and accountability).

- Sankey and trend topic visualizations, to track the evolution of research focus over time and the interconnection between ESG implementation and policy themes.

5. Discussion

5.1. DEA Efficiency Scores

5.2. ESG Disclosure Quality

5.3. Bibliometric Insights

6. Conclusions

7. Policy Implications

7.1. Strengthening ESG Monitoring and Accountability

7.2. Capacity Building in Public Institutions

7.3. Funding Eligibility and Performance Linkage

7.4. Enhancing Transparency in ESG Data

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Data Envelopment Analysis (DEA) Model Structure

Appendix A.1. Decision-Making Units (DMUs)

Appendix A.2. Input Variables

Appendix A.3. Output Variables

- The frequency of reports;

- The inclusion of verifiable ESG metrics;

- Consistency with sustainability frameworks (e.g., GRI, SASB).

Appendix A.4. DEA Model Type and Orientation

Appendix B. Content Analysis Coding Framework

Appendix B.1. Coding Dimensions

- Clarity: Are the ESG goals and results articulated clearly?

- Completeness: Are all relevant ESG dimensions (E, S, and G) addressed?

- Consistency: Is there alignment between reported goals and observed actions?

- Verifiability: Are performance indicators accompanied by supporting evidence?

- Third-party Assurance: Is there independent verification or audit of ESG data?

Appendix B.2. Rating Scale

Appendix C. List of Decision-Making Units (Anonymized)

| DMU Code | Type | Sector | Years Covered | Funding Source |

| DMU-01 | Public Agency | Environmental Policy | 2020–2023 | EU Structural Funds |

| DMU-02 | State-owned Bank | Financial Sector | 2021–2024 | National Recovery Plan |

| DMU-03 | Municipal Utility | Energy and Water | 2020–2022 | Mixed (EU/National) |

Appendix D. Bibliometric Data Collection Strategy

- Document types: Article, Review, Conference Paper;

- Language: English;

- Years: 2010–2024.

References

- Adams, Carol A. 2022. SDGs and ESG alignment in public finance. Sustainability Accounting, Management and Policy Journal. [Google Scholar] [CrossRef]

- Amel-Zadeh, Amir, and George Serafeim. 2018. Why and How Investors Use ESG Information: Evidence from a Global Survey. Financial Analysts Journal 74: 87–103. [Google Scholar] [CrossRef]

- Aria, Massimo, and Corrado Cuccurullo. 2017. bibliometrix: An R-tool for comprehensive science mapping analysis. Journal of Informetrics 11: 959–75. [Google Scholar] [CrossRef]

- Boiral, Olivier, Marie-Christine Brotherton, and David Talbot. 2024. What you see is what you get? Building confidence in ESG disclosures for sustainable finance through external assurance. Business Ethics, the Environment & Responsibility 33: 617–32. [Google Scholar]

- Bosi, Mathew Kevin, Nelson Lajuni, Avnner Chardles Wellfren, and Thien Sang Lim. 2022. Sustainability Reporting through Environmental, Social, and Governance: A Bibliometric Review. Sustainability 14: 12071. [Google Scholar] [CrossRef]

- Calabrese, Armando, Roberta Costa, Nathan Levialdi, and Tamara Menichini. 2016. A fuzzy Analytic Hierarchy Process method to support materiality assessment in sustainability reporting. Journal of Cleaner Production 121: 248–64. [Google Scholar] [CrossRef]

- Calabrese, Armando, Roberta Costa, Nathan Levialdi, and Tamara Menichini. 2019. Materiality analysis in sustainability reporting: A tool for directing corporate sustainability towards emerging economic, environmental and social opportunities. Technological and Economic Development of Economy 25: 1016–38. [Google Scholar] [CrossRef]

- Christensen, Dane M., Eric Floyd, Lisa Yao Liu, and Mark G. Maffett. 2021. The Real Effects of Mandatory ESG Disclosure. The Accounting Review 96: 261–87. [Google Scholar] [CrossRef]

- Cooper, William W., Lawrence M. Seiford, and Kaoru Tone. 2007. Data Envelopment Analysis: A Comprehensive Text with Models, Applications, References and DEA-Solver Software, 2nd ed. Berlin/Heidelberg: Springer. [Google Scholar]

- Delmas, Magali A., and Vanessa C. Burbano. 2011. The Drivers of Greenwashing. California Management Review 54: 64–87. [Google Scholar] [CrossRef]

- Donthu, Naveen, Satish Kumar, Dedidatta Mukherjee, Neharika Pandey, and Weng Mark Lim. 2021. How to conduct a bibliometric analysis: An overview and guidelines. Journal of Business Research 133: 285–96. [Google Scholar] [CrossRef]

- Eccles, Robert G., and Svetlana Klimenko. 2019. The Investor Revolution. Harvard Business Review 97: 106–16. [Google Scholar]

- EFRAG. 2023. ESRS Exposure Drafts. Available online: https://www.efrag.org/en/sustainability-reporting/esrs/sector-agnostic/first-set-of-draft-esrs (accessed on 10 May 2025).

- European Commission. 2021. Recovery and Resilience Facility: Regulation (EU) 2021/241 of the European Parliament and of the Council. Official Journal of the European Union. Available online: https://eur-lex.europa.eu/eli/reg/2021/241/2024-03-01/eng (accessed on 15 May 2025).

- European Commission. 2022. Sustainable Finance and EU Taxonomy Platform Reports. Available online: https://finance.ec.europa.eu/publications/platform-sustainable-finance-report-simplifying-eu-taxonomy-foster-sustainable-finance_en (accessed on 12 May 2025).

- Friede, Gunnar, Timo Busch, and Alexander Bassen. 2015. ESG and Financial Performance: Aggregated Evidence from More than 2000 Empirical Studies. Journal of Sustainable Finance & Investment 5: 210–33. [Google Scholar] [CrossRef]

- García-Sánchez, Isabel Maria, and Jennifer Martínez-Ferrero. 2022. ESG Performance, Cost of Capital, and Public Accountability. Journal of Public Economics 207: 104602. [Google Scholar] [CrossRef]

- Halkos, George E., Nickolaos G. Tzeremes, and Stavros A. Kourtzidis. 2016. Measuring sustainability efficiency using a two-stage data envelopment analysis approach. Journal of Industrial Ecology 20: 1159–75. [Google Scholar] [CrossRef]

- Heinrich, Carolyn J. 2019. Do government performance audits improve public accountability? Evidence from Green Budgeting in the EU. Public Administration Review 79: 610–22. [Google Scholar] [CrossRef]

- Knorren, P., and R. Munro. 2023. From disclosure to accountability: Institutional pressures and stakeholder expectations in ESG. Journal of Business Ethics 178: 845–62. [Google Scholar] [CrossRef]

- Korca, Blerita, Ericka Costa, and Lies Bouten. 2023. Disentangling the concept of comparability in sustainability reporting. Sustainability Accounting, Management and Policy Journal 14: 815–51. [Google Scholar] [CrossRef]

- Kossentini, Hager, Olfa Belhassine, and Amel Zenaidi. 2024. ESG index performance: European evidence. Journal of Asset Management 25: 653–65. [Google Scholar] [CrossRef]

- Liu, Yu, and Elling Tjønneland. 2024. ESG governance and funding misuse in public bodies: Regulatory lessons from Southern Europe. Environmental Policy and Governance 34: 27–41. [Google Scholar] [CrossRef]

- Lyon, Thomas P., and Aubrey W. Montgomery. 2015. The Means and End of Greenwash. Organization & Environment 28: 223–49. [Google Scholar] [CrossRef]

- Lyon, Thomas P., and John W. Maxwell. 2011. Greenwash: Corporate Environmental Disclosure under Threat of Audit. Journal of Economics & Management Strategy 20: 3–41. [Google Scholar] [CrossRef]

- Malan, Daniel, Alison Taylor, Anna Tunkel, and Birgit Kurtz. 2022. Why Business Integrity Can Be a Strategic Response to Ethical Challenges. MIT Sloan Management Review. Available online: https://sloanreview.mit.edu/article/why-business-integrity-can-be-a-strategic-response-to-ethical-challenges/ (accessed on 21 July 2025).

- Marquis, Christopher, and Michael W. Toffel. 2016. Scrutiny, Norms, and Selective Disclosure: A Global Study of Greenwashing. Organization Science 27: 483–504. [Google Scholar] [CrossRef]

- Michelon, Giovanna, Stefania Pilonato, and Federica Ricceri. 2015. CSR Reporting Practices and the Quality of Disclosure: An Empirical Analysis. Critical Perspectives on Accounting 33: 59–78. [Google Scholar] [CrossRef]

- OECD. 2022. Green Public Procurement and ESG Integration in the Public Sector. Available online: https://www.oecd.org/governance/green-public-procurement.html (accessed on 21 July 2025).

- Papadopoulos, Georgios, Ioannis Sotiropoulos, and Anastasios Kotsiras. 2025. ESG performance in the Greek public sector: An efficiency and transparency analysis. Cogent Business & Management 12: 2450092. [Google Scholar] [CrossRef]

- Paun, Adrian, Alex Sudmant, and Matthew Clark. 2023. ESG Resilience in Public Systems. Finance Research Letters 52: 103547. [Google Scholar] [CrossRef]

- Qi, Junmei, Edina Eberhardt-Toth, and Elisabeth Paulet. 2022. Determinants of Environmental Credit Risk Management: Empirical Evidence from European Banks. In New Approaches to CSR, Sustainability and Accountability, Volume III. Singapore: Springer Nature Singapore, pp. 17–36. [Google Scholar] [CrossRef]

- Schaltegger, Stefan, and Jacob Hörisch. 2017. In Search of the Meaning of Sustainability Accounting. Sustainability Accounting, Management and Policy Journal 8: 38–62. [Google Scholar] [CrossRef]

- Schramade, Willem. 2016. Integrating ESG into valuation models and investment decisions: The value-driver adjustment approach. Journal of Sustainable Finance & Investment 6: 95–111. [Google Scholar] [CrossRef]

- Stefanidis, Sotiris, Ioannis Kougkoulos, and Ioannis Deliyannis. 2022. Mapping ESG research in the European public domain: A bibliometric review. Frontiers in Environmental Science 10: 1087493. [Google Scholar] [CrossRef]

- Thanassoulis, Emmanuel, Maria Conceicao Silva Portela, and Ogan Despic. 2008. Data Envelopment Analysis: The Mathematical Programming Approach to Efficiency Analysis. In The Measurement of Productive Efficiency and Productivity Growth. Edited by Harold O. Fried, C. A. Knox Lovell and Shelton S. Schmidt. Oxford: Oxford University Press, pp. 251–420. [Google Scholar]

- Torelli, Roberto, Federica Balluchi, and Katia Furlotti. 2023. Greenwashing evolution: From symbolic management to strategic deception. Business Strategy and the Environment 32: 1890–907. [Google Scholar] [CrossRef]

- UNGC, GRI, and BCSD. 2021. SDG Compass: The Guide for Business Action on the SDGs. Available online: https://sdgs.un.org/partnerships (accessed on 12 May 2025).

- van Eck, Nees, and Ludo Waltman. 2010. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 84: 523–38. [Google Scholar] [CrossRef] [PubMed]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Efthalitsidou, K.; Kanavas, V.; Kagias, P.; Sariannidis, N. Public Funding, ESG Strategies, and the Risk of Greenwashing: Evidence from Greek Financial and Public Institutions. Risks 2025, 13, 143. https://doi.org/10.3390/risks13080143

Efthalitsidou K, Kanavas V, Kagias P, Sariannidis N. Public Funding, ESG Strategies, and the Risk of Greenwashing: Evidence from Greek Financial and Public Institutions. Risks. 2025; 13(8):143. https://doi.org/10.3390/risks13080143

Chicago/Turabian StyleEfthalitsidou, Kyriaki, Vasileios Kanavas, Paschalis Kagias, and Nikolaos Sariannidis. 2025. "Public Funding, ESG Strategies, and the Risk of Greenwashing: Evidence from Greek Financial and Public Institutions" Risks 13, no. 8: 143. https://doi.org/10.3390/risks13080143

APA StyleEfthalitsidou, K., Kanavas, V., Kagias, P., & Sariannidis, N. (2025). Public Funding, ESG Strategies, and the Risk of Greenwashing: Evidence from Greek Financial and Public Institutions. Risks, 13(8), 143. https://doi.org/10.3390/risks13080143