Volatility Modeling and Tail Risk Estimation of Financial Assets: Evidence from Gold, Oil, Bitcoin, and Stocks for Selected Markets

Abstract

1. Introduction

2. Literature Review

2.1. Risk Characteristics of Financial Assets

2.1.1. Risk Features and Performance of Non-Equity Assets

2.1.2. Risk Features and Performance of Equity Markets

2.2. Advances in Tail Risk Measurement Methodologies

2.3. Research Gap

3. Data and Methods

3.1. Data Sources and Variable Descriptions

3.2. GARCH Family Models

3.2.1. AR–GARCH Model

3.2.2. AR–EGARCH Model

3.3. VaR Model

3.3.1. Historical Simulation

3.3.2. Monte Carlo Simulation

3.3.3. GARCH Method

3.3.4. AR–EGARCH–EVT–VaR

3.4. VaR Backtesting Model

3.4.1. Kupiec Proportion of Failures Test

3.4.2. Christoffersen Conditional Coverage Test

4. Results

4.1. Statistical Feature Analysis

4.1.1. Descriptive Statistical Analysis

4.1.2. Stationarity Tests

4.1.3. Autocorrelation and ARCH Effects Tests

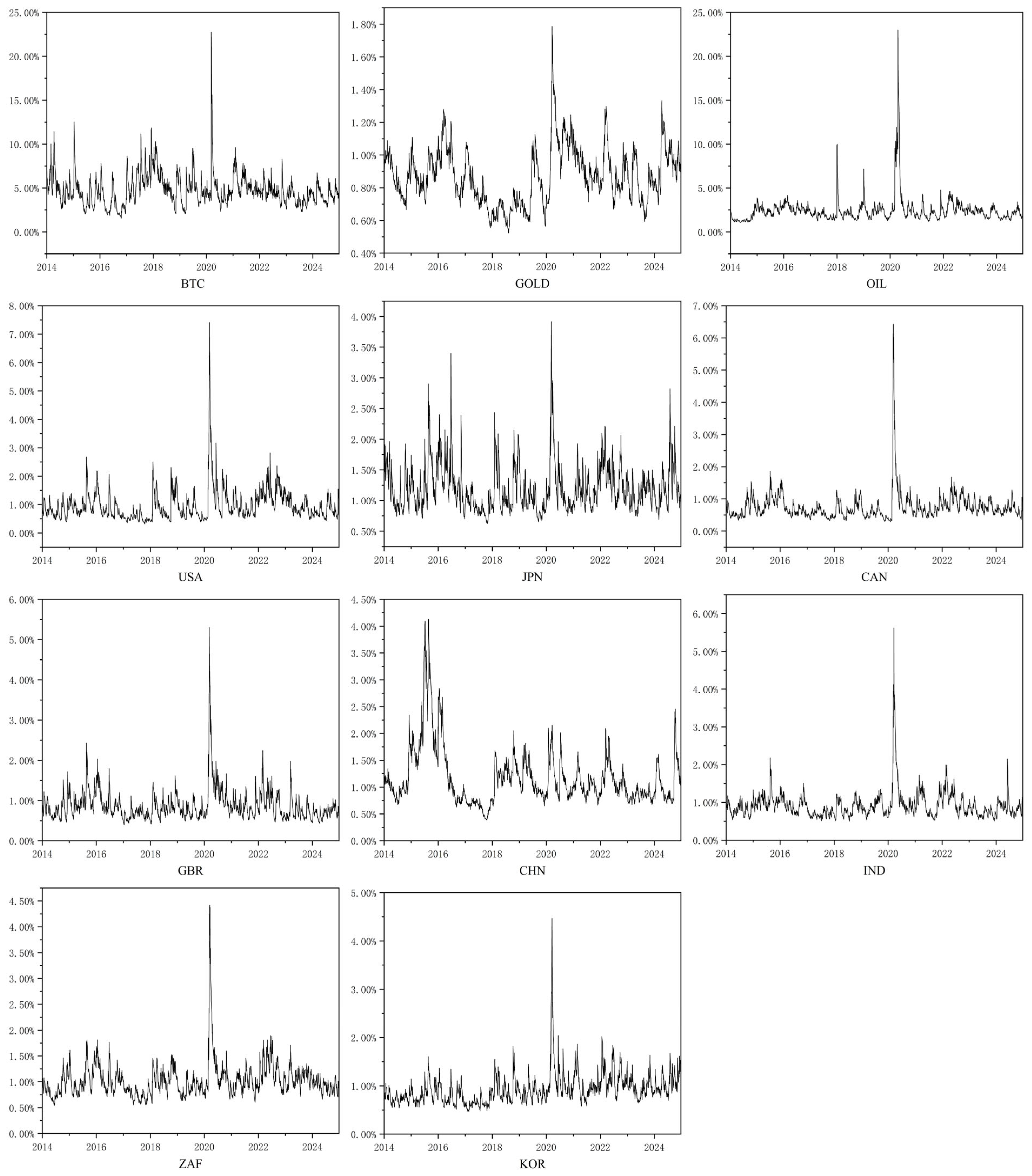

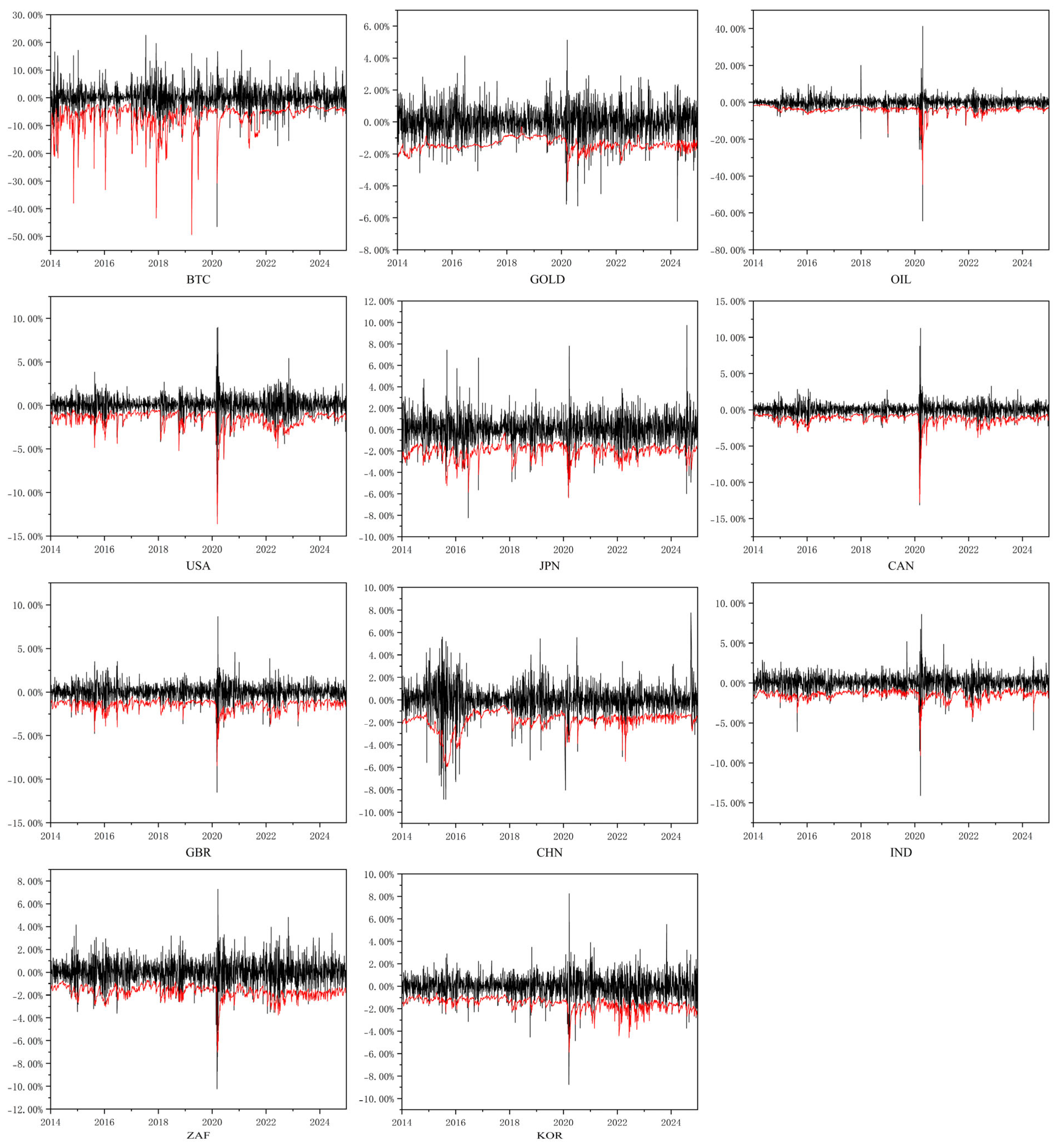

4.2. Volatility Analysis

4.2.1. Results of the EGARCH Model

4.2.2. Conditional Volatility Dynamics

4.3. Tail Risk Analysis

4.3.1. Model Accuracy Evaluation and Comparative Analysis

4.3.2. Comparative Analysis of Tail Risk

5. Discussion

5.1. Research Conclusions

5.2. Policy Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Abbreviations

| EGARCH | Exponential Generalized Autoregressive Conditional Heteroskedasticity |

| GARCH | Generalized Autoregressive Conditional Heteroskedasticity |

| VaR | Value at Risk |

| EVT | Extreme Value Theory |

| AR | Autoregressive |

| RCEP | Regional Comprehensive Economic Partnership |

| AIC | Akaike Information Criterion |

| POT | Peaks Over Threshold |

| GPD | Generalized Pareto Distribution |

| LR | Likelihood Ratio |

| JB | Jarque–Bera |

| ADF | Augmented Dickey–Fuller |

| ARCH–LM | Autoregressive Conditional Heteroskedasticity Lagrange Multiplier |

| PP | Phillips–Perron |

| LB | Ljung–Box |

| STD | Student’s T-Distribution |

| SSTD | Skewed Student’s T-Distribution |

| GED | Generalized Error Distribution |

| SGED | Skewed Generalized Error Distribution |

References

- Afzal, Fahim, Pan Haiying, Farman Afzal, Asif Mahmood, and Amir Ikram. 2021. Value-at-risk analysis for measuring stochastic volatility of stock returns: Using GARCH-based dynamic conditional correlation model. Sage Open 11: 21582440211005758. [Google Scholar] [CrossRef]

- Alexander, Carol, and Michael Dakos. 2023. Assessing the accuracy of exponentially weighted moving average models for Value-at-Risk and Expected Shortfall of crypto portfolios. Quantitative Finance 23: 393–427. [Google Scholar] [CrossRef]

- Bali, Turan G., Hengyong Mo, and Yi Tang. 2008. The role of autoregressive conditional skewness and kurtosis in the estimation of conditional VaR. Journal of Banking & Finance 32: 269–82. [Google Scholar] [CrossRef]

- Banihashemi, Shokoofeh, and Sarah Navidi. 2017. Portfolio performance evaluation in Mean-CVaR framework: A comparison with non-parametric methods value at risk in Mean-VaR analysis. Operations Research Perspectives 4: 21–28. [Google Scholar] [CrossRef]

- Batten, Jonathan A., Harald Kinateder, and Peter G. Szilagyi. 2024. Should you buy gold stocks or paper gold? Finance Research Letters 69: 106202. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Allan Trench. 2022. Not all gold shines in crisis times—Gold firms, gold bullion and the COVID-19 shock. Journal of Commodity Markets 28: 100260. [Google Scholar] [CrossRef]

- Baur, Dirk G., Lai T. Hoang, and Md Zakir Hossain. 2022. Is Bitcoin a hedge? How extreme volatility can destroy the hedge property. Finance Research Letters 47: 102655. [Google Scholar] [CrossRef]

- Bekaert, Geert, Campbell R. Harvey, and Tomas Mondino. 2023. Emerging equity markets in a globalized world. Emerging Markets Review 56: 101034. [Google Scholar] [CrossRef]

- Blau, Benjamin M., Todd G. Griffith, and Ryan J. Whitby. 2021. Inflation and Bitcoin: A descriptive time-series analysis. Economics Letters 203: 109848. [Google Scholar] [CrossRef]

- Bollerslev, Tim. 1986. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31: 307–27. [Google Scholar] [CrossRef]

- Boonman, Tjeerd M. 2023. Portfolio capital flows before and after the Global Financial Crisis. Economic Modelling 127: 106440. [Google Scholar] [CrossRef]

- Boubaker, Heni, Juncal Cunado, Luis A. Gil-Alana, and Rangan Gupta. 2020. Global crises and gold as a safe haven: Evidence from over seven and a half centuries of data. Physica A: Statistical Mechanics and Its Applications 540: 123093. [Google Scholar] [CrossRef]

- Chincarini, Ludwig B., and Fabio Moneta. 2021. The challenges of oil investing: Contango and the financialization of commodities. Energy Economics 102: 105443. [Google Scholar] [CrossRef]

- Christoffersen, Peter F. 1998. Evaluating interval forecasts. International Economic Review 39: 841–62. [Google Scholar] [CrossRef]

- Das, Nupur Moni, Bhabani Sankar Rout, and Yashmin Khatun. 2023. Does G7 engross the shock of COVID 19: An assessment with market volatility? Asia-Pacific Financial Markets 30: 795–816. [Google Scholar] [CrossRef]

- Deng, Xue, Wen Zhou, Fengting Geng, and Yuan Lu. 2024. A novel ARMA-GARCH-Sent-EVT-Copula Portfolio model with investor sentiment. Soft Computing 28: 13501–26. [Google Scholar] [CrossRef]

- Díaz, Antonio, Carlos Esparcia, and Raquel López. 2022. The diversifying role of socially responsible investments during the COVID-19 crisis: A risk management and portfolio performance analysis. Economic Analysis and Policy 75: 39–60. [Google Scholar] [CrossRef] [PubMed]

- Echaust, Krzysztof, and Małgorzata Just. 2020. Value at risk estimation using the GARCH-EVT approach with optimal tail selection. Mathematics 8: 114. [Google Scholar] [CrossRef]

- Fiszeder, Piotr, Marta Małecka, and Peter Molnár. 2024. Robust estimation of the range-based GARCH model: Forecasting volatility, value at risk and expected shortfall of cryptocurrencies. Economic Modelling 141: 106887. [Google Scholar] [CrossRef]

- Gomis-Porqueras, Pedro, Shuping Shi, and David Tan. 2022. Gold as a financial instrument. Journal of Commodity Markets 27: 100218. [Google Scholar] [CrossRef]

- Grout, Paul A., and Anna Zalewska. 2016. Stock market risk in the financial crisis. International Review of Financial Analysis 46: 326–45. [Google Scholar] [CrossRef]

- Halkos, George E., and Apostolos S. Tsirivis. 2019. Value-at-risk methodologies for effective energy portfolio risk management. Economic Analysis and Policy 62: 197–212. [Google Scholar] [CrossRef]

- Harjoto, Maretno Agus, and Fabrizio Rossi. 2023. Market reaction to the COVID-19 pandemic: Evidence from emerging markets. International Journal of Emerging Markets 18: 173–99. [Google Scholar] [CrossRef]

- He, Dong. 2021. Digitalization of cross-border payments. China Economic Journal 14: 26–38. [Google Scholar] [CrossRef]

- Hodoshima, Jiro, and Nana Otsuki. 2019. Evaluation by the Aumann and Serrano performance index and Sharpe ratio: Bitcoin performance. Applied Economics 51: 4282–98. [Google Scholar] [CrossRef]

- Hong, Hui, Zhicun Bian, and Chien-Chiang Lee. 2021. COVID-19 and instability of stock market performance: Evidence from the US. Financial Innovation 7: 1–18. [Google Scholar] [CrossRef] [PubMed]

- Huang, Yongrong, Huiqing Wang, Zhide Chen, Chen Feng, Kexin Zhu, Xu Yang, and Wencheng Yang. 2024. Evaluating cryptocurrency market risk on the blockchain: An empirical study using the ARMA-GARCH-VaR model. IEEE Open Journal of the Computer Society 5: 83–94. [Google Scholar] [CrossRef]

- Irfan, Muhammad, Mubeen Abdur Rehman, Sarah Nawazish, and Yu Hao. 2023. Performance analysis of gold-and fiat-backed cryptocurrencies: Risk-based choice for a portfolio. Journal of Risk and Financial Management 16: 99. [Google Scholar] [CrossRef]

- Izzeldin, Marwan, Yaz Gülnur Muradoğlu, Vasileios Pappas, and Sheeja Sivaprasad. 2021. The impact of COVID-19 on G7 stock markets volatility: Evidence from a ST-HAR model. International Review of Financial Analysis 74: 101671. [Google Scholar] [CrossRef] [PubMed]

- Kang, Wenjin, Ke Tang, and Ningli Wang. 2023. Financialization of commodity markets ten years later. Journal of Commodity Markets 30: 100313. [Google Scholar] [CrossRef]

- Kim, Jong-Min, Dong H. Kim, and Hojin Jung. 2021. Estimating yield spreads volatility using GARCH-type models. The North American Journal of Economics and Finance 57: 101396. [Google Scholar] [CrossRef]

- Koulis, Alexandros, and Constantinos Kyriakopoulos. 2023. On volatility transmission between gold and silver markets: Evidence from a long-term historical period. Computation 11: 25. [Google Scholar] [CrossRef]

- Krause, David. 2024. Mainstreaming Cryptocurrency: The State of Wisconsin Investment Board’s Pioneering Investment in Bitcoin ETFs. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4852566 (accessed on 10 July 2025).

- Kupabado, Moses Mananyi, and Juergen Kaehler. 2025. Price effects of commodity financialization: Review of the evidence. Journal of Economic Surveys 39: 352–74. [Google Scholar] [CrossRef]

- Kupiec, Paul H. 1995. Techniques for Verifying the Accuracy of Risk Measurement Models. Washington, DC: Division of Research and Statistics, Division of Monetary Affairs, Federal Reserve Board,, vol. 95. [Google Scholar]

- Li, Yang, and Qingfeng Du. 2024. Oil price volatility and gold prices volatility asymmetric links with natural resources via financial market fluctuations: Implications for green recovery. Resources Policy 88: 104279. [Google Scholar] [CrossRef]

- Likitratcharoen, Danai, and Lucksuda Suwannamalik. 2024. Assessing Financial Stability in Turbulent Times: A Study of Generalized Autoregressive Conditional Heteroskedasticity-Type Value-at-Risk Model Performance in Thailand’s Transportation Sector during COVID-19. Risks 12: 51. [Google Scholar] [CrossRef]

- Likitratcharoen, Danai, Pan Chudasring, Chakrin Pinmanee, and Karawan Wiwattanalamphong. 2023. The efficiency of value-at-risk models during extreme market stress in cryptocurrencies. Sustainability 15: 4395. [Google Scholar] [CrossRef]

- Lin, Zhe. 2018. Modelling and forecasting the stock market volatility of SSE Composite Index using GARCH models. Future Generation Computer Systems 79: 960–72. [Google Scholar] [CrossRef]

- Lyu, Yongjian, Siwei Tuo, Yu Wei, and Mo Yang. 2021. Time-varying effects of global economic policy uncertainty shocks on crude oil price volatility: New evidence. Resources Policy 70: 101943. [Google Scholar] [CrossRef]

- Mazur, Mieszko, Man Dang, and Miguel Vega. 2021. COVID-19 and the march 2020 stock market crash. Evidence from S&P1500. Finance Research Letters 38: 101690. [Google Scholar] [CrossRef] [PubMed]

- Mnif, Emna, and Anis Jarboui. 2021. COVID-19, bitcoin market efficiency, herd behaviour. Review of Behavioral Finance 13: 69–84. [Google Scholar] [CrossRef]

- Mrkvička, Tomáš, Martina Krásnická, Ludvík Friebel, Tomáš Volek, and Ladislav Rolínek. 2022. Backtesting the evaluation of Value-at-Risk methods for exchange rates. Studies in Economics and Finance 40: 175–91. [Google Scholar] [CrossRef]

- Nelson, Daniel B. 1991. Conditional heteroskedasticity in asset returns: A new approach. Econometrica: Journal of the Econometric Society 59: 347–70. [Google Scholar] [CrossRef]

- Nguyen, Quang Thi Thieu, Dao Le Trang Anh, and Christopher Gan. 2021. Epidemics and Chinese firms’ stock returns: Is COVID-19 different? China Finance Review International 11: 302–21. [Google Scholar] [CrossRef]

- Pan, Zhiyuan, Xiao Huang, Li Liu, and Juan Huang. 2023. Geopolitical uncertainty and crude oil volatility: Evidence from oil-importing and oil-exporting countries. Finance Research Letters 52: 103565. [Google Scholar] [CrossRef]

- Patra, Saswat. 2021. Revisiting value-at-risk and expected shortfall in oil markets under structural breaks: The role of fat-tailed distributions. Energy Economics 101: 105452. [Google Scholar] [CrossRef]

- Patra, Saswat, and Neha Gupta. 2023. Risk in the cryptocurrency markets: The role of structural breaks and fat-tailed distributions in estimating value-at-risk and expected shortfall. The European Journal of Finance, 1–21. [Google Scholar] [CrossRef]

- Raggad, Bechir, and Elie Bouri. 2023. Gold and crude oil: A time-varying causality across various market conditions. Resources Policy 86: 104273. [Google Scholar] [CrossRef]

- Rahman, Md Lutfur, Abu Amin, and Mohammed Abdullah Al Mamun. 2021. The COVID-19 outbreak and stock market reactions: Evidence from Australia. Finance Research Letters 38: 101832. [Google Scholar] [CrossRef] [PubMed]

- Ranković, Vladimir, Mikica Drenovak, Branko Urosevic, and Ranko Jelic. 2016. Mean-univariate GARCH VaR portfolio optimization: Actual portfolio approach. Computers & Operations Research 72: 83–92. [Google Scholar]

- Reese, Heather, A. Danielle Iuliano, Neha N. Patel, Shikha Garg, Lindsay Kim, Benjamin J. Silk, Aron J. Hall, Alicia Fry, and Carrie Reed. 2021. Estimated incidence of coronavirus disease 2019 (COVID-19) illness and hospitalization—United States, February–September 2020. Clinical Infectious Diseases 72: e1010–e1017. [Google Scholar] [CrossRef] [PubMed]

- Ren, Xiaohang, Ya Xiao, Feng He, and Giray Gozgor. 2024. The contagion of extreme risks between fossil and green energy markets: Evidence from China. Quantitative Finance 24: 627–42. [Google Scholar] [CrossRef]

- Rout, Bhabani Sankar, Nupur Moni Das, and Mohd Merajuddin Inamdar. 2021. COVID-19 and market risk: An assessment of the G-20 nations. Journal of Public Affairs 21: e2590. [Google Scholar] [CrossRef] [PubMed]

- Salisu, Afees A., Ibrahim D. Raheem, and Xuan Vinh Vo. 2021. Assessing the safe haven property of the gold market during COVID-19 pandemic. International Review of Financial Analysis 74: 101666. [Google Scholar] [CrossRef] [PubMed]

- Setiawan, Budi, Marwa Ben Abdallah, Maria Fekete-Farkas, Robert Jeyakumar Nathan, and Zoltan Zeman. 2021. GARCH (1, 1) models and analysis of stock market turmoil during COVID-19 outbreak in an emerging and developed economy. Journal of Risk and Financial Management 14: 576. [Google Scholar] [CrossRef]

- Soleymani, Fazlollah, Qiang Ma, and Tao Liu. 2025. Managing the risk via the Chi-squared distribution in VaR and CVaR with the use in generalized autoregressive conditional heteroskedasticity model. Mathematics 13: 1410. [Google Scholar] [CrossRef]

- Su, Chi-Wei, Lidong Pang, Muhammad Umar, and Oana-Ramona Lobonţ. 2022. Will gold always shine amid world uncertainty? Emerging Markets Finance and Trade 58: 3425–38. [Google Scholar] [CrossRef]

- Tanin, Tauhidul Islam, Ashutosh Sarker, Robert Brooks, and Hung Xuan Do. 2022. Does oil impact gold during COVID-19 and three other recent crises? Energy Economics 108: 105938. [Google Scholar] [CrossRef] [PubMed]

- Triki, Mohamed Bilel, and Abderrazek Ben Maatoug. 2021. The GOLD market as a safe haven against the stock market uncertainty: Evidence from geopolitical risk. Resources Policy 70: 101872. [Google Scholar] [CrossRef]

- Uddin, Moshfique, Anup Chowdhury, Keith Anderson, and Kausik Chaudhuri. 2021. The effect of COVID–19 pandemic on global stock market volatility: Can economic strength help to manage the uncertainty? Journal of Business Research 128: 31. [Google Scholar] [CrossRef] [PubMed]

- Usman, Abdullahi Ubale, Sunusi Bala Abdullahi, Yu Liping, Bayan Alghofaily, Ahmed S. Almasoud, and Amjad Rehman. 2024. Financial Fraud Detection Using Value-at-Risk with Machine Learning in Skewed Data. IEEE Access 12: 64285–99. [Google Scholar] [CrossRef]

- Wang, Weibin, and Yao Wu. 2023. Risk analysis of the Chinese financial market with the application of a novel hybrid volatility prediction model. Mathematics 11: 3937. [Google Scholar] [CrossRef]

- Wang, Xinya, Brian Lucey, and Shupei Huang. 2022. Can gold hedge against oil price movements: Evidence from GARCH-EVT wavelet modeling. Journal of Commodity Markets 27: 100226. [Google Scholar] [CrossRef]

- Xu, Yingying, and Donald Lien. 2022. Forecasting volatilities of oil and gas assets: A comparison of GAS, GARCH, and EGARCH models. Journal of Forecasting 41: 259–78. [Google Scholar] [CrossRef]

- Yang, Jing Yu, Minyoung Kim, Jiatao Li, and Jane Wenzhen Lu. 2023. Information voids and cross-border bandwagons of foreign direct investment into an emerging economy. Strategic Management Journal 44: 2751–82. [Google Scholar] [CrossRef]

- Yen-Ku, Kuo, Apichit Maneengam, Phan The Cong, Nguyen Ngoc Quynh, Mohammed Moosa Ageli, and Worakamol Wisetsri. 2022. COVID-19 and oil and gold price volatilities: Evidence from China market. Resources Policy 79: 103024. [Google Scholar] [CrossRef] [PubMed]

- Yoshino, Naoyuki, and Farhad Taghizadeh-Hesary. 2016. Causes and remedies of the Japan’s long-lasting recession: Lessons for China. China & World Economy 24: 23–47. [Google Scholar]

- Yu, Xiang, and Na Li. 2021. Understanding the beginning of a pandemic: China’s response to the emergence of COVID-19. Journal of Infection and Public Health 14: 347–52. [Google Scholar] [CrossRef] [PubMed]

- Yu, Yang, SongLin Guo, and XiaoChen Chang. 2022. Oil prices volatility and economic performance during COVID-19 and financial crises of 2007–2008. Resources Policy 75: 102531. [Google Scholar] [CrossRef] [PubMed]

- Zhang, Chen, and Xinmiao Zhou. 2024. Forecasting value-at-risk of crude oil futures using a hybrid ARIMA-SVR-POT model. Heliyon 10: e23358. [Google Scholar] [CrossRef] [PubMed]

- Zhang, Chun-Xia, Jun Li, Xing-Fang Huang, Jiang-She Zhang, and Hua-Chuan Huang. 2022. Forecasting stock volatility and value-at-risk based on temporal convolutional networks. Expert Systems with Applications 207: 117951. [Google Scholar] [CrossRef]

- Zhang, Weiping, Xintian Zhuang, and Yang Lu. 2020. Spatial spillover effects and risk contagion around G20 stock markets based on volatility network. The North American Journal of Economics and Finance 51: 101064. [Google Scholar] [CrossRef]

- Zhang, Wenwen, Shuo Cao, Xuan Zhang, and Xuefeng Qu. 2023. COVID-19 and stock market performance: Evidence from the RCEP countries. International Review of Economics & Finance 83: 717–35. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Name | Abbreviation | Categorization | Price Indicator |

|---|---|---|---|

| Bitcoin | BTC | Cryptocurrency | Bitcoin Spot Price |

| Gold | GOLD | Commodity | LBMA Gold Price |

| Crude Oil | OIL | Commodity | Brent Crude Oil price |

| The United States | USA | Developed Market | Standard & Poor’s 500 Index |

| Japan | JPN | Developed Market | Nikkei Stock Average 225 Index |

| Canada | CAN | Developed Market | Toronto Stock Exchange Composite Index |

| The United Kingdom | GBR | Developed Market | Financial Times Stock Exchange 100 Index |

| China | CHN | Emerging Market | Shanghai Stock Exchange Composite Index |

| India | IND | Emerging Market | Bombay Stock Exchange Sensitive Index |

| South Africa | ZAF | Emerging Market | JSE All-Share Index |

| Korea | KOR | Emerging Market | Korea Composite Stock Price Index |

| Minimum | Maximum | Mean | Std.Dev | Skewness | Kurtosis | JB Test | |

|---|---|---|---|---|---|---|---|

| BTC | −46.4730% | 22.6409% | −0.0108% | 4.1492% | −0.8525 | 11.0799 | 11,279.1818 *** |

| GOLD | −6.2171% | 5.1334% | 0.0238% | 0.8937% | −0.4064 | 4.1549 | 1610.0101 *** |

| OIL | −64.3699% | 41.2023% | −0.0707% | 3.1405% | −3.8483 | 103.5542 | 967,350.4500 *** |

| USA | −12.7652% | 8.9683% | 0.0342% | 1.1127% | −1.0579 | 18.2575 | 30,313.5650 *** |

| JPN | −8.2529% | 9.7366% | 0.0322% | 1.2805% | 0.0176 | 5.4614 | 2678.6146 *** |

| CAN | −13.1202% | 11.2469% | 0.0134% | 0.9638% | −1.8525 | 43.8932 | 174,086.5313 *** |

| GBR | −11.5124% | 8.6668% | −0.0090% | 0.9815% | −1.0493 | 15.7081 | 22,537.8461 *** |

| CHN | −8.8729% | 7.7551% | 0.0017% | 1.2916% | −0.8176 | 8.2146 | 6297.3328 *** |

| IND | −14.1017% | 8.5947% | 0.0436% | 1.0553% | −1.5376 | 23.8081 | 51,708.9719 *** |

| ZAF | −10.2268% | 7.2615% | 0.0039% | 1.1029% | −0.7235 | 8.3376 | 6428.0683 *** |

| KOR | −8.7670% | 8.2513% | 0.0013% | 1.0088% | −0.3636 | 7.2291 | 4739.2225 *** |

| ADF Statistics | p-Value | PP Statistics | p-Value | |

|---|---|---|---|---|

| BTC | −13.0866 | 0.0000 | −2196.2640 | 0.0000 |

| GOLD | −13.4634 | 0.0000 | −2079.4810 | 0.0000 |

| OIL | −10.7594 | 0.0000 | −2309.6850 | 0.0000 |

| USA | −13.5872 | 0.0000 | −2393.0940 | 0.0000 |

| JPN | −13.6343 | 0.0000 | −2174.1880 | 0.0000 |

| CAN | −12.6709 | 0.0000 | −2522.7020 | 0.0000 |

| GBR | −13.1727 | 0.0000 | −2205.2520 | 0.0000 |

| CHN | −13.9445 | 0.0000 | −1964.9990 | 0.0000 |

| IND | −13.4416 | 0.0000 | −2272.1950 | 0.0000 |

| ZAF | −13.5760 | 0.0000 | −2155.9530 | 0.0000 |

| KOR | −12.8407 | 0.0000 | −2055.7980 | 0.0000 |

| LB Statistics | p-Value | ARCH Statistics | p-Value | |

|---|---|---|---|---|

| BTC | 11.9871 | 0.2859 | 48.5969 | 0.0000 |

| GOLD | 9.0480 | 0.5276 | 86.2922 | 0.0000 |

| OIL | 80.5268 | 0.0000 | 382.9079 | 0.0000 |

| USA | 187.6131 | 0.0000 | 950.1055 | 0.0000 |

| JPN | 12.5436 | 0.2503 | 240.7091 | 0.0000 |

| CAN | 287.9943 | 0.0000 | 1052.1677 | 0.0000 |

| GBR | 33.7097 | 0.0002 | 616.2506 | 0.0000 |

| CHN | 20.9493 | 0.0215 | 292.0224 | 0.0000 |

| IND | 29.3374 | 0.0011 | 652.2125 | 0.0000 |

| ZAF | 22.5813 | 0.0124 | 866.7801 | 0.0000 |

| KOR | 17.1475 | 0.0712 | 665.7070 | 0.0000 |

| μ | θ | ω | α | β | γ | |

|---|---|---|---|---|---|---|

| BTC | 0.0009 | −0.0146 | −0.2428 *** | 0.3300 *** | 0.9602 *** | 0.0325 |

| GOLD | 0.0001 | 0.0151 | −0.1707 *** | 0.0979 *** | 0.9821 *** | 0.0293 ** |

| OIL | −0.0004 | 0.0170 | −0.3095 *** | 0.2285 *** | 0.9595 *** | −0.0767 *** |

| USA | 0.0004 ** | −0.0379 * | −0.3829 *** | 0.2442 *** | 0.9598 *** | −0.1593 *** |

| JPN | 0.0001 | −0.0115 | −0.5390 *** | 0.1907 *** | 0.9395 *** | −0.1365 *** |

| CAN | 0.0001 | 0.0546 *** | −0.3755 *** | 0.1660 *** | 0.9623 *** | −0.1555 *** |

| GBR | −0.0003 * | 0.0068 | −0.4167 *** | 0.1738 *** | 0.9564 *** | −0.1636 *** |

| CHN | −0.0001 | −0.0002 | −0.1383 *** | 0.1912 *** | 0.9846 *** | −0.0049 |

| IND | 0.0004 ** | 0.0534 *** | −0.3969 *** | 0.1462 *** | 0.9582 *** | −0.1238 *** |

| ZAF | −0.0001 | −0.0035 | −0.3499 *** | 0.1296 *** | 0.9620 *** | −0.1203 *** |

| KOR | −0.0001 | −0.0078 | −0.5064 *** | 0.2186 *** | 0.9461 *** | −0.0963 *** |

| Categorization | Maximum | Minimum | Std.Dev | Mean | Rank | |

|---|---|---|---|---|---|---|

| BTC | Cryptocurrency | 22.7453% | 1.5728% | 1.8097% | 4.7824% | 1 |

| GOLD | Commodity | 1.7861% | 0.5233% | 0.1702% | 0.8715% | 10 |

| OIL | Commodity | 23.0062% | 1.0559% | 1.3909% | 2.4076% | 2 |

| USA | Developed Market | 7.4119% | 0.3164% | 0.5561% | 0.9611% | 6 |

| JPN | Developed Market | 3.9159% | 0.6234% | 0.3809% | 1.2004% | 3 |

| CAN | Developed Market | 6.4226% | 0.2865% | 0.4514% | 0.7491% | 11 |

| GBR | Developed Market | 5.3045% | 0.3993% | 0.3894% | 0.8764% | 9 |

| CHN | Emerging Market | 4.1333% | 0.3899% | 0.5400% | 1.1765% | 4 |

| IND | Emerging Market | 5.6214% | 0.5020% | 0.3732% | 0.9191% | 8 |

| ZAF | Emerging Market | 4.4153% | 0.5431% | 0.3416% | 1.0230% | 5 |

| KOR | Emerging Market | 4.4674% | 0.4707% | 0.3288% | 0.9335% | 7 |

| NORM | STD | GED | SSTD | SGED | |

|---|---|---|---|---|---|

| BTC | −3.6264 | −3.9284 | −3.9241 | −3.9275 | −3.9233 |

| GOLD | −6.6672 | −6.7560 | −6.7573 | −6.7551 | −6.7564 |

| OIL | −4.7405 | −4.8858 | −4.8673 | −4.8909 | −4.8746 |

| USA | −6.6509 | −6.7486 | −6.7351 | −6.7588 | −6.7463 |

| JPN | −6.0782 | −6.1344 | −6.1351 | −6.1358 | −6.1378 |

| CAN | −7.1256 | −7.1652 | −7.1544 | −7.1920 | −7.1860 |

| GBR | −6.7799 | −6.8333 | −6.8252 | −6.8472 | −6.8421 |

| CHN | −6.2323 | −6.3379 | −6.3330 | −6.3385 | −6.3348 |

| IND | −6.6337 | −6.7040 | −6.6940 | −6.7068 | −6.6960 |

| ZAF | −6.4100 | −6.4371 | −6.4331 | −6.4427 | −6.4391 |

| KOR | −6.5994 | −6.6323 | −6.6333 | −6.6377 | −6.6394 |

| Historical Simulation | Monte Carlo Simulation | GARCH | ||||

| LR | p-Value | LR | p-Value | LR | p-Value | |

| BTC | 1.1044 | 0.2933 | 3.5330 | 0.0602 | 1.3300 | 0.2488 |

| GOLD | 0.1966 | 0.6575 | 1.5775 | 0.2091 | 1.1044 | 0.2933 |

| OIL | 3.2016 | 0.0736 | 0.4155 | 0.5192 | 1.2648 | 0.2608 |

| USA | 0.1222 | 0.7267 | 0.0030 | 0.9566 | 6.4250 | 0.0113 |

| JPN | 0.2002 | 0.6546 | 0.0020 | 0.9645 | 1.2648 | 0.2608 |

| CAN | 0.0632 | 0.8015 | 0.9003 | 0.3427 | 6.9007 | 0.0086 |

| GBR | 0.4155 | 0.5192 | 2.4530 | 0.1173 | 3.2016 | 0.0736 |

| CHN | 0.8694 | 0.3511 | 0.9003 | 0.3427 | 0.1966 | 0.6575 |

| IND | 1.5775 | 0.2091 | 8.0676 | 0.0045 | 0.6988 | 0.4032 |

| ZAF | 0.1222 | 0.7267 | 0.4155 | 0.5192 | 7.3923 | 0.0066 |

| KOR | 0.0632 | 0.8015 | 0.4124 | 0.5207 | 2.8733 | 0.0901 |

| AR–EGARCH– Norm | AR–EGARCH | AR–EGARCH– EVT | ||||

| LR | p-Value | LR | p-Value | LR | p-Value | |

| BTC | 2.1388 | 0.1436 | 0.4124 | 0.5207 | 9.3533 | 0.0022 |

| GOLD | 0.2958 | 0.5866 | 0.2002 | 0.6546 | 0.5465 | 0.4598 |

| OIL | 0.2002 | 0.6546 | 1.0581 | 0.3036 | 1.4892 | 0.2223 |

| USA | 4.2873 | 0.0384 | 0.2002 | 0.6546 | 0.1222 | 0.7267 |

| JPN | 0.6988 | 0.4032 | 0.0207 | 0.8856 | 0.2002 | 0.6546 |

| CAN | 6.4250 | 0.0113 | 1.7312 | 0.1883 | 1.2648 | 0.2608 |

| GBR | 3.2016 | 0.0736 | 0.2970 | 0.5858 | 0.0632 | 0.8015 |

| CHN | 0.4155 | 0.5192 | 0.1222 | 0.7267 | 0.1966 | 0.6575 |

| IND | 0.1222 | 0.7267 | 0.1222 | 0.7267 | 0.1222 | 0.7267 |

| ZAF | 2.2678 | 0.1321 | 0.0632 | 0.8015 | 0.0030 | 0.9566 |

| KOR | 4.2873 | 0.0384 | 0.2970 | 0.5858 | 0.5465 | 0.4598 |

| Historical Simulation | Monte Carlo Simulation | GARCH | ||||

| LR | p-Value | LR | p-Value | LR | p-Value | |

| BTC | 5.3064 | 0.0704 | 11.8385 | 0.0027 | 4.1909 | 0.1230 |

| GOLD | 0.4334 | 0.8052 | 1.9920 | 0.3694 | 1.1967 | 0.5497 |

| OIL | 8.6433 | 0.0133 | 3.8110 | 0.1487 | 1.5823 | 0.4533 |

| USA | 19.8173 | 0.0000 | 18.4488 | 0.0001 | 7.2984 | 0.0260 |

| JPN | 12.0518 | 0.0024 | 11.4603 | 0.0032 | 11.1644 | 0.0038 |

| CAN | 29.4825 | 0.0000 | 28.1917 | 0.0000 | 16.4627 | 0.0003 |

| GBR | 14.0667 | 0.0009 | 12.1080 | 0.0023 | 5.9891 | 0.0501 |

| CHN | 8.7583 | 0.0125 | 10.8119 | 0.0045 | 1.9890 | 0.3699 |

| IND | 6.2205 | 0.0446 | 14.5114 | 0.0007 | 0.7115 | 0.7007 |

| ZAF | 1.0178 | 0.6012 | 0.4299 | 0.8066 | 7.4121 | 0.0246 |

| KOR | 32.8371 | 0.0000 | 37.1521 | 0.0000 | 10.2014 | 0.0061 |

| AR–EGARCH– Norm | AR–EGARCH | AR–EGARCH– EVT | ||||

| LR | p-Value | LR | p-Value | LR | p-Value | |

| BTC | 4.1394 | 0.1262 | 1.0552 | 0.5900 | 14.1648 | 0.0008 |

| GOLD | 1.2373 | 0.5387 | 0.4429 | 0.8014 | 1.1147 | 0.5727 |

| OIL | 0.2050 | 0.9026 | 2.0473 | 0.3593 | 2.2951 | 0.3174 |

| USA | 4.2965 | 0.1167 | 0.4429 | 0.8014 | 0.1355 | 0.9345 |

| JPN | 2.9202 | 0.2322 | 1.5061 | 0.4709 | 1.0506 | 0.5914 |

| CAN | 7.2984 | 0.0260 | 2.4529 | 0.2933 | 4.0731 | 0.1305 |

| GBR | 10.2453 | 0.0060 | 4.2236 | 0.1210 | 3.1884 | 0.2031 |

| CHN | 3.8110 | 0.1487 | 4.4689 | 0.1071 | 4.1909 | 0.1230 |

| IND | 1.8502 | 0.3965 | 1.8502 | 0.3965 | 1.8502 | 0.3965 |

| ZAF | 3.5212 | 0.1719 | 1.9890 | 0.3699 | 2.2159 | 0.3302 |

| KOR | 7.7161 | 0.0211 | 1.8325 | 0.4000 | 1.8480 | 0.3969 |

| Categorization | Whole Period | Rank | During Crisis | Rank | |

|---|---|---|---|---|---|

| BTC | Cryptocurrency | −6.8829% | 1 | −6.7460% | 1 |

| GOLD | Commodity | −1.4310% | 10 | −1.6618% | 11 |

| OIL | Commodity | −3.8472% | 2 | −5.3084% | 2 |

| USA | Developed Market | −1.5682% | 6 | −2.2692% | 3 |

| JPN | Developed Market | −2.0273% | 3 | −2.0549% | 4 |

| CAN | Developed Market | −1.2630% | 11 | −1.7687% | 10 |

| GBR | Developed Market | −1.4998% | 8 | −2.0362% | 6 |

| CHN | Emerging Market | −1.8602% | 4 | −1.9867% | 7 |

| IND | Emerging Market | −1.4712% | 9 | −1.8876% | 9 |

| ZAF | Emerging Market | −1.7422% | 5 | −2.0577% | 5 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhu, Y.; Taasim, S.I.; Daud, A. Volatility Modeling and Tail Risk Estimation of Financial Assets: Evidence from Gold, Oil, Bitcoin, and Stocks for Selected Markets. Risks 2025, 13, 138. https://doi.org/10.3390/risks13070138

Zhu Y, Taasim SI, Daud A. Volatility Modeling and Tail Risk Estimation of Financial Assets: Evidence from Gold, Oil, Bitcoin, and Stocks for Selected Markets. Risks. 2025; 13(7):138. https://doi.org/10.3390/risks13070138

Chicago/Turabian StyleZhu, Yilin, Shairil Izwan Taasim, and Adrian Daud. 2025. "Volatility Modeling and Tail Risk Estimation of Financial Assets: Evidence from Gold, Oil, Bitcoin, and Stocks for Selected Markets" Risks 13, no. 7: 138. https://doi.org/10.3390/risks13070138

APA StyleZhu, Y., Taasim, S. I., & Daud, A. (2025). Volatility Modeling and Tail Risk Estimation of Financial Assets: Evidence from Gold, Oil, Bitcoin, and Stocks for Selected Markets. Risks, 13(7), 138. https://doi.org/10.3390/risks13070138