1. Introduction

It is worth noting that literature involving creative accounting does not explicitly specify if the auditor is obliged to reveal those creative accounting aspects that are permitted and legal (

Suer 2014). Herein, the audit committee plays a significant role in improving creative accounting practices and financial reporting quality. Based on this fact, the present study attempts to evaluate the creative accounting practices in Iraq and the subsequent impact on the banking sector and enhancement of financial reporting quality. In reality, auditing standards require that the processes formulated by the auditors must be able to ascertain whether the accounting practices followed by the business entities can record financial information appropriately (

Mutuc et al. 2019). Basically, creative accounting is the practice of influencing financial indicators through accounting knowledge without explicitly violating accounting policies, rules, and laws. Creative accounting is practiced to demonstrate the financial status desired by the company management wherein the stakeholders are informed what the management wants them to perceive (

Susmuş and Demirhan 2013). It facilitates the manipulation of financial information in its proper and accurate form in which the preparer uses the existing rules or in many cases ignores one or more rules (

Idris et al. 2012;

Mulford and Comiskey 2012).

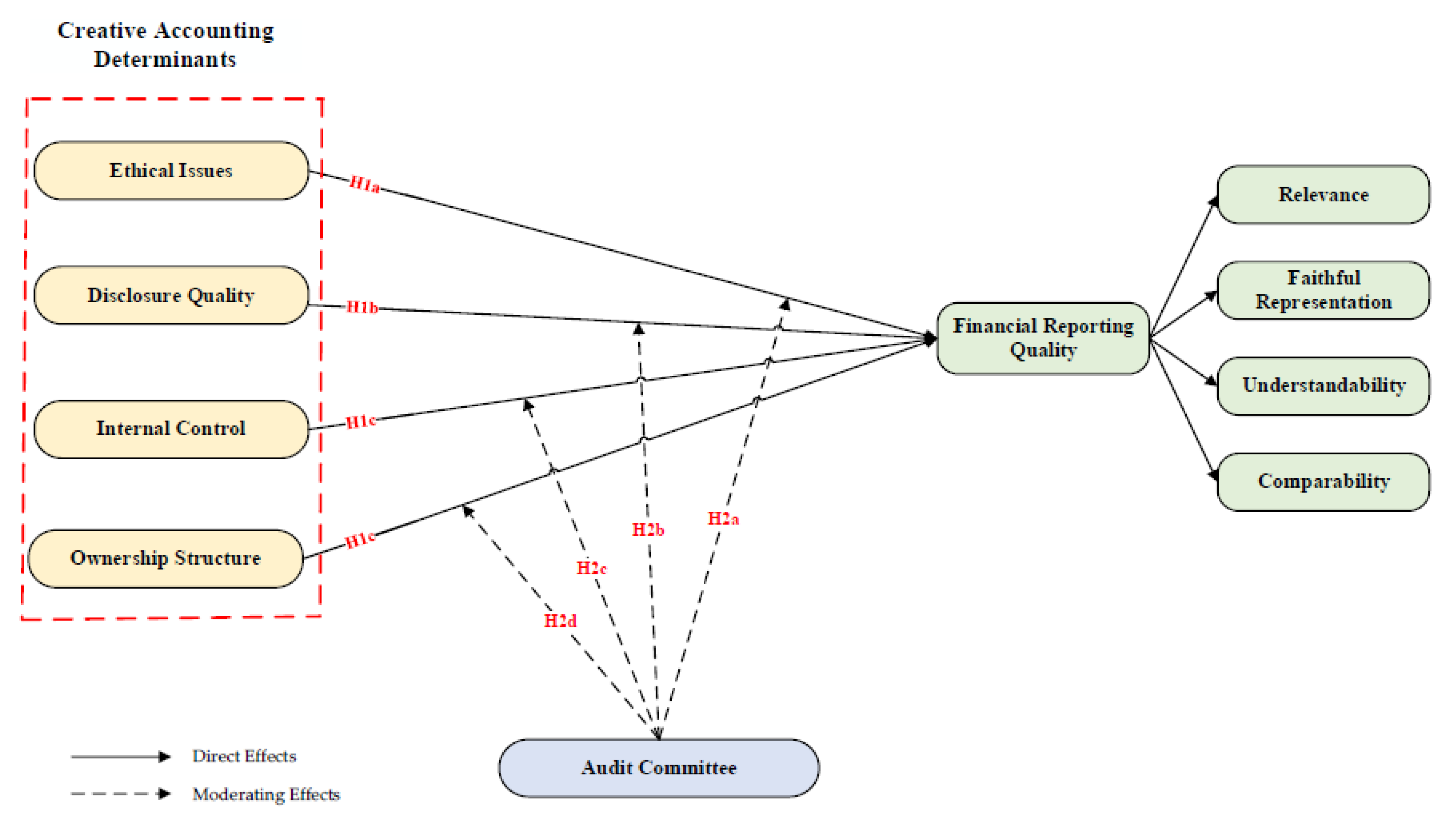

Previous research indicates that creative accounting has four fundamental determinants: ethical issues, disclosure quality, internal control and ownership structure (

Škoda et al. 2017). Thus, it is important to determine whether these determinants are properly practiced in the financial reporting of Iraq. In this regard, the current study intends to evaluate creative accounting practices influencing financial reporting in the banks of Iraq with regard to quality improvement. On top of this, this study determines the causative factors that motivate Iraqi banks to indulge in creative accounting practices for the betterment of overall performance (

Yaseen et al. 2019). To make decisions related to the efficient operations of banks, financial reports must provide reliable, timely and accurate data needed by the stakeholders (

Chang et al. 2019). Nevertheless, the main purpose of financial reporting by the banks is to present financial data to their users for better awareness and continuous updating of decisions. However, the current secretarial policy provides some choices regarding accounting practices and objective judgments to define the measurement strategies, recognition criteria and in some cases the characterization of the accounting bodies. The capacity to select varied accounting aspects enables administrators to deliberately manipulate the information or to practice concealment. Consequently, these manipulations can enhance the apparent attractiveness of the businesses, thereby projecting better profits and financial stability. In addition, such practices can sometimes mislead the users and investors, causing a significant hindrance to corporate growth and investment mobilization (

Campello et al. 2011;

Farhan Jedi and Nayan 2018;

Abed et al. 2020c). It has been asserted that the financial reports of the bank can provide a reliable direction to users for objective decision-making (

Mutuc et al. 2019). Essentially, the reports used for financial decision-making must be understandable, comparable, relevant, and realistic.

As aforementioned, a strong audit committee plays a paramount role in creative accounting practices and financial reporting quality. An inadequate governance structure provides an impetus to manipulative activities (

Tassadaq and Malik 2015;

Abed et al. 2020a). In fact, a poor audit committee displays a strong correlation to the manipulation of accounting (

Mudel 2015;

Trisanti 2016). Conversely, organizations with a strong audit committee framework have a low probability of exploiting creative accounting, and of misrepresentation of earnings and assets, as well as other deceptions (

Ababneh and Aga 2019). Researchers found that numerous stakeholders can adversely be affected due to creative accounting practices (

Brauweiler et al. 2019). These stakeholders include the customers, creditors, suppliers, equity investors, and regulators, among others. A comprehensive literature survey revealed that studies concerning creative accounting practices in Iraq and the Middle East remain deficient because these regions are less focused on this issue. In fact, the provisions for formulating effective systems to monitor and check creative accounting practices in Iraqi banks have been lacking. In contrast, intensive investigations have been conducted regarding creative accounting practices in developing nations. In this regard, (

Qian et al. 2015) focused on several developing nations and formed three groups to compare creative accounting practices used to protect investors. It was concluded that although one group had little investor protection, the creative accounting practices were numerous and aggressive.

Considering the impact of corporate governance on creative accounting practices and financial reporting quality improvement, this study aimed to achieve an in-depth understanding of both empirical and theoretical viewpoints in this domain in the context of Iraqi banks. A basic framework has been developed to provide hands-on support for the regulators and investors related to the banking sector in Iraq. It attained a new perspective regarding creative accounting practices in Iraqi banks, thus contributing significantly to the existing state-of-the-art knowledge. The primary goal was to enrich the literature related to creative accounting practices from four perspectives: first, to evaluate the primary determinants of creative accounting practices such as ethical issues, internal control, disclosure quality and ownership structure; second, to determine the effectiveness of a strong audit committee for eliminating creative accounting practices in the banking sector of Iraq; third, to utilize information regarding the commercial banks in Iraq to establish the extent to which the creative accounting practices are entrenched in the national banking system; finally, to assess the quality of financial reporting practiced by the Iraqi commercial banks from the perception of the regulatory agencies, audit committee and others. Based on this research background, the following problems need to be resolved.

However, there is limited evidence on how the impact of determinants of creative accounting on financial reporting quality is affected by the audit committee in the banking sector of Iraq. This study aims to examine the joint influence of determinants of creative accounting and the audit committee on financial reporting quality in Iraq. It concentrates on two questions:

What are the effects of creative accounting determinants on financial reporting quality in the banking sector?

To what extent does the audit committee impact the relationship between creative accounting determinants and financial reporting quality?

Finally, the findings of this study will be useful to policymakers, researchers, and managers. In particular, they provide current knowledge on the impact of the audit committee, creative accounting and financial reporting quality, contributing to the literature on performance from a bank-based view. Thus, the present research is designed to attain the following objectives that contribute to limit the practice of creative accounting and the increasing of the quality of financial reports in the banking sector.

To examine the effects of creative accounting determinants on financial reporting quality in the banking sector.

To examine the impacts of the audit committee on the relationship between creative accounting determinants and financial reporting quality.

4. Discussion and Conclusions

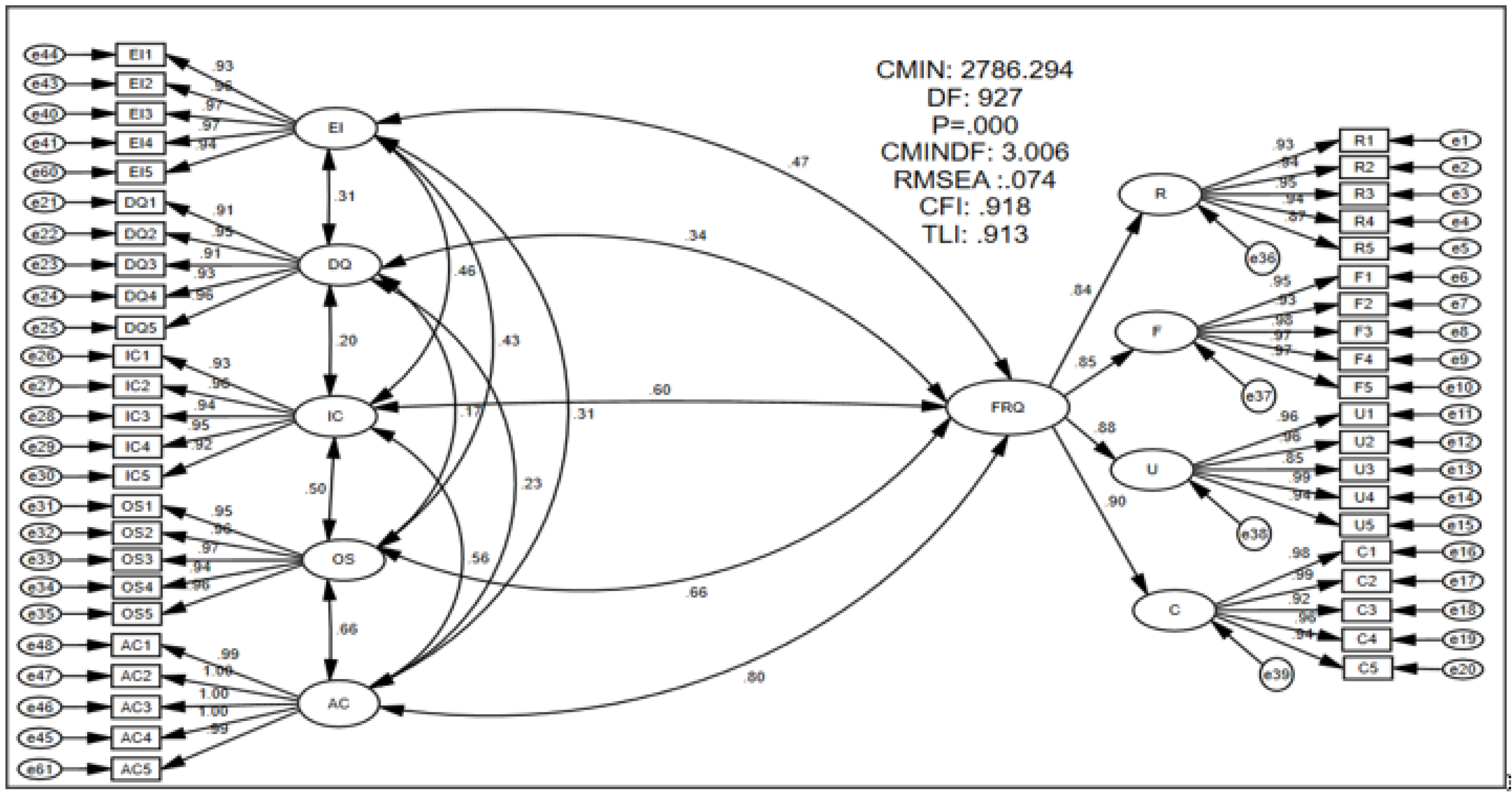

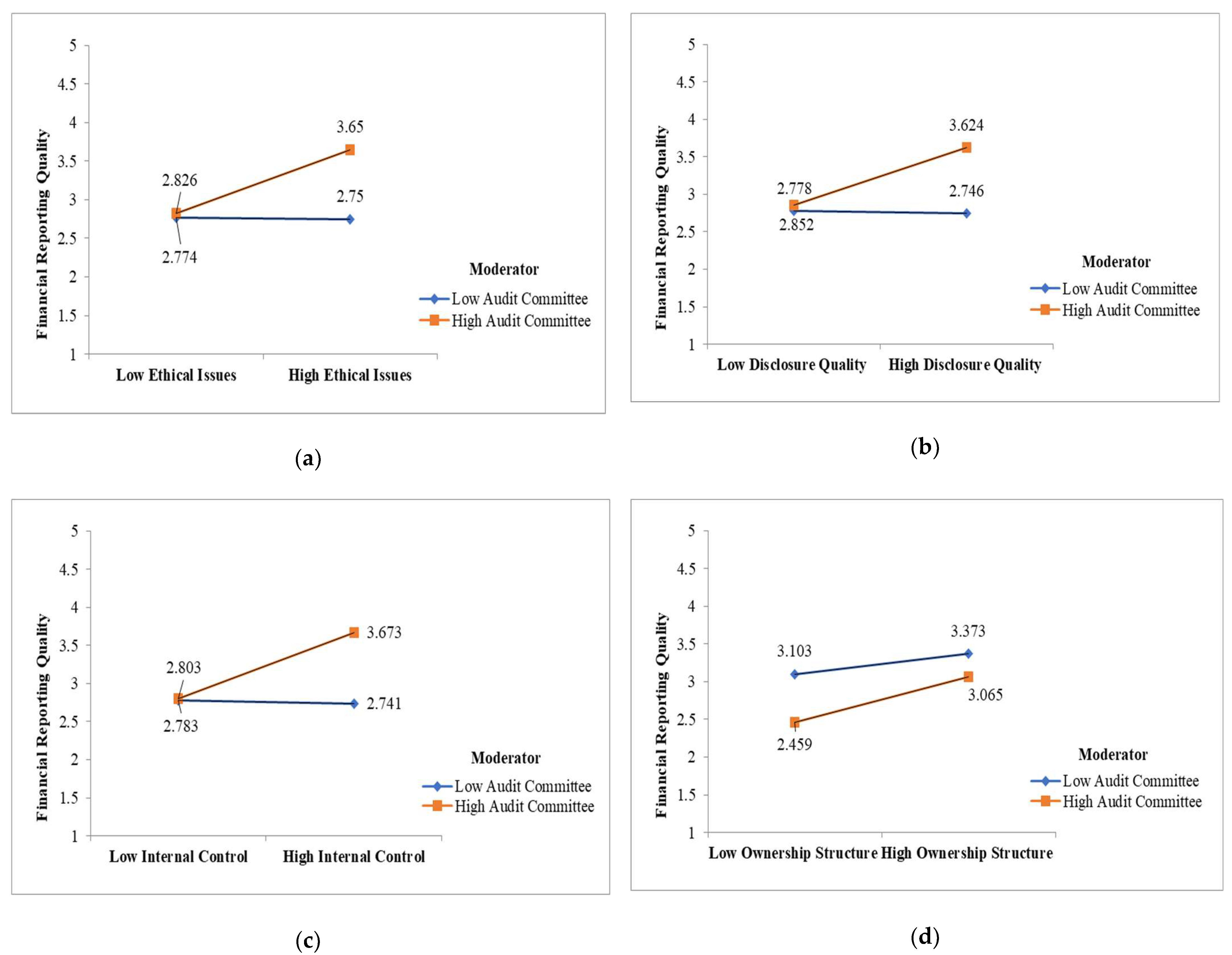

The present research findings confirmed the moderation impact of the audit committee on ethical issues, discourse quality, internal control and ownership structure together with financial reporting quality. This moderation relationship is proposed in three hypotheses that described the impact of the audit committee on each of the determinants of creative accounting practice. The obtained results showed that the role of creative accounting determinants in commercial banks can be enhanced and considered as a value-relevant property to acquire high reporting quality through the moderation of the corporate aspect of the audit committee. Accordingly, the result for hypotheses H1a was (t = 3.328) which aligned with the assumptions provided by the agency theory, whereas, the hypothesis indicated significant impacts of the maintenance of ethical issues on the quality of financial reporting. Furthermore, the results reaffirmed that ethical aspects lead to the establishment of higher quality of financial reporting practice as shown in the context of Iraqi commercial banks. Besides, the results acknowledged the findings in the previous studies presented by (

Tassadaq and Malik 2015;

Gras et al. 2016;

de Jesus et al. 2020;

Shafer et al. 2013) that demonstrate limited consideration of ethical issues on creative accounting practice in the context of commercial banks.

In addition, the result of H1b (t = 3.427) indicated a significant relationship between the constructs with the limited operation of disclosure procedures in the context of commercial banks. This determination designated the higher implications of creative accounting practice on the quality of financial reporting in the banking sector, which was found to be consistent with previous literature reviews (

Mutuc et al. 2019;

Qian et al. 2015;

Tri Wahyuni et al. 2020). The implementation of the new-institutional theory contributed to explaining the underlying preposition that limited disclosure practice in the context of commercial banks was due to the pressure exerted by the institutional setup that related to the ownership structure. These results are found to be in good agreement with numerous studies in the literature which display the significance of linkage between this determinant and accounting practice (

Mutuc et al. 2019;

Qian et al. 2015;

Mudel 2016;

Udin et al. 2017). However, the present research findings are contradicted by other studies that proposed a limited controlling role of disclosure quality in creative accounting practice (

Cooray et al. 2020;

Yasser et al. 2016;

Gerwanski et al. 2019). In brief, disclosure quality is found to be one of the essential determinants of institutional transparency that increase the trust of the public in the financial reporting quality of the bank. This finding is approved by its high consistency with previous claims cited in (

Zaman et al. 2018) on maintaining ethical concerns through disclosure quality.

The findings of the last two hypotheses related to the first research question are H1c (t = 3.640) and H1d (t = 3.912). As mentioned earlier, the present research findings showed a significant inter-correlated relationship between the determinants of creative accounting i.e., each of the determinants has an effect on others. The origin of this relationship is clearly identified in the previous literature, and is verified in the present research findings. Thus, the limited consideration of ethical issues and disclosure quality resulted in the limited implementation of internal control. These procedures enable the practice of creative accounting to take place in the commercial banking sector at various levels according to the ownership structure of the bank. Thus, the present findings are consistent with previous studies that indicated poor internal control which may lead to higher errors and inaccurate financial disclosure regarding the financial reporting quality in banks (

Lim et al. 2017;

Muraina and Dandago 2020).

It is worth declaring that the outcomes of this research supported the existing literature concerning the correlation between the determinants of creative accounting in detecting fraud practice, but these determinants fall to control this practice to safe levels (

Al-Hashemi 2020;

Ibrahim et al. 2017;

Ndebugri and Tweneboah Senzu 2017;

Cernusca et al. 2016). These findings are applied to the context of Iraqi commercial banks, although dedicated efforts are constantly made to retain, and establish healthy relations with the outside shareholders as one of the major resources, but additional enhancements re required to reduce Fraud practice within creative accounting in order to present high quality financial reports. This in turn implies that the internal banking system should maintain ethical issues, disclosure to the public, and implement qualified internal control for a faithful representation of the financial reporting practice in Iraqi commercial banks.

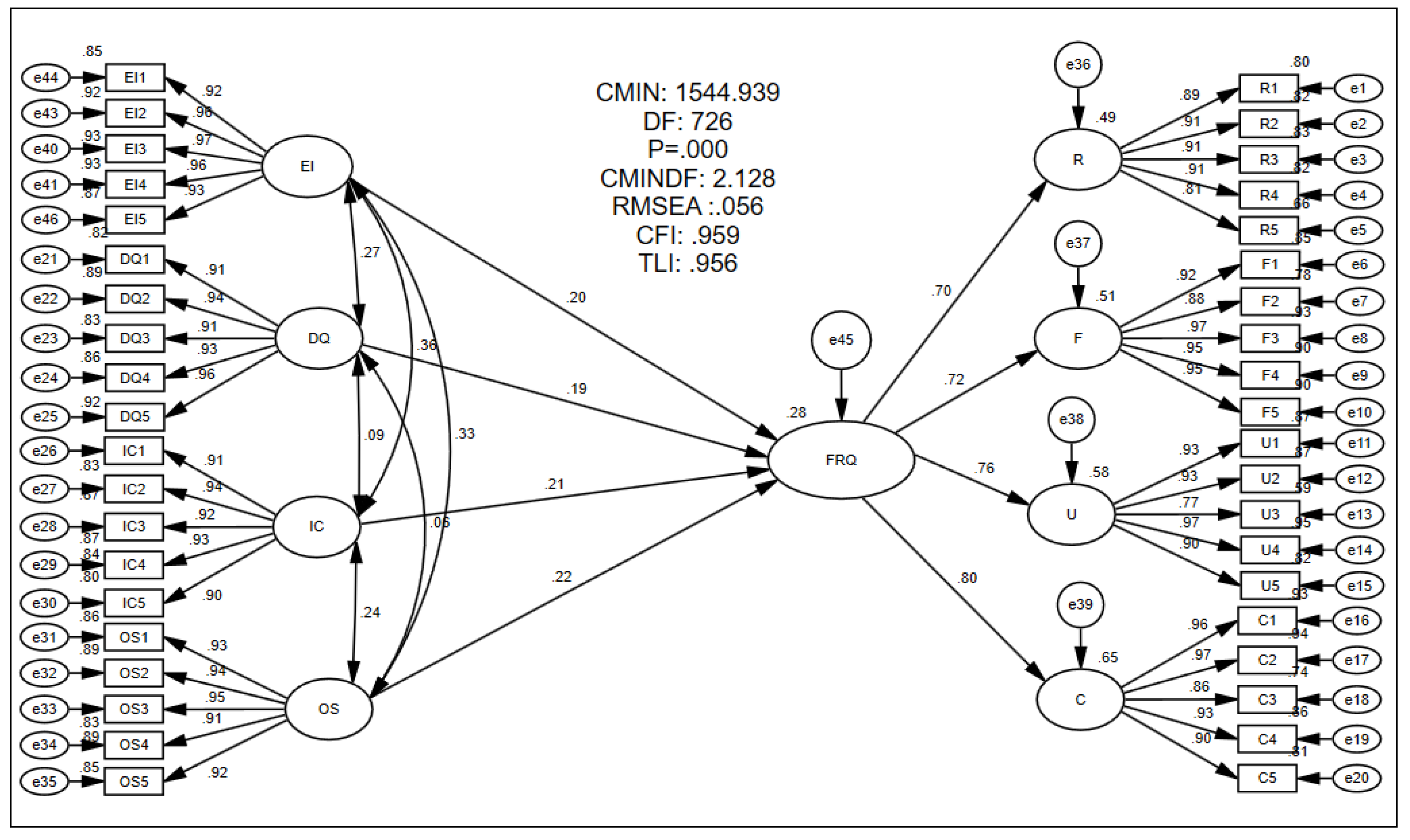

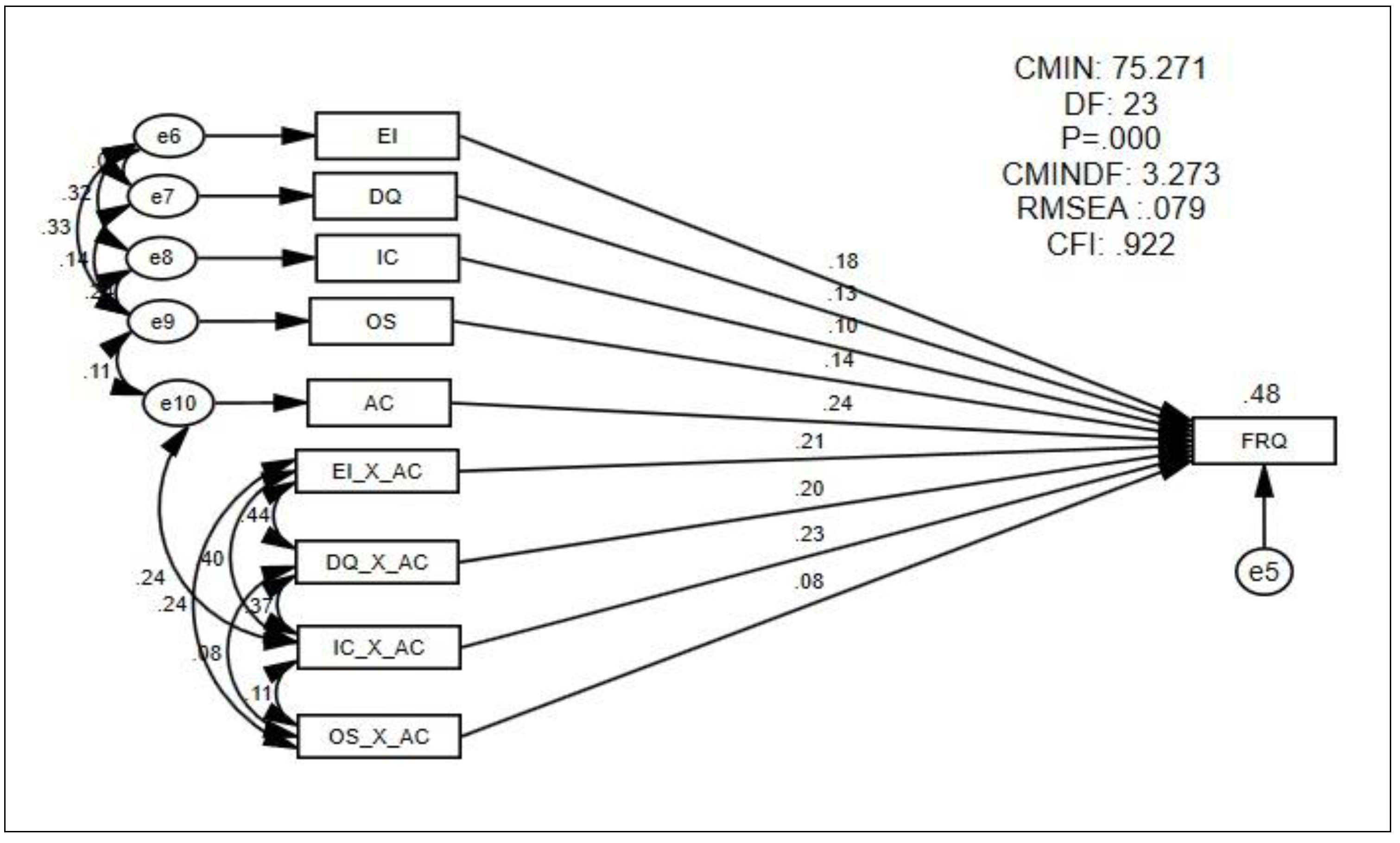

So far, the results obtained showed that the role of creative accounting determinants in commercial banks can be enhanced and considered as a valuerelevant property in acquiring high reporting practice through the moderation of the audit committee. Briefly, the findings regarding the audit committee supported the hypotheses H2a, H2b and H2c through the indicated value of t = 4.677, 4.622, and 5.094. In addition, the comprehensive analysis of the results illustrated some important correlations among the determinants of creative accounting and financial reporting quality moderated by the audit committee. In contrast, the findings did not support hypothesis H2d due to the absence of any significant value among the audit committee and ownership structure—t = 1.152. In this respect, the findings validated the previous research of (

Qian et al. 2015;

Mutuc et al. 2019;

Mudel 2016;

Suprianto et al. 2017) concerning the impacts of ownership structure on audit practice and financial reporting quality in the banking sector.

Furthermore, the present results contributed by examining the moderating role of the audit committee theoretically, whereas the agency and neoinstitutional theories could partially explain the present trends. In the content of commercial banks, the argument of neoinstitutional theories emphasizes exterior pressure as a significant driver of the audit committee structure at specific conditions, which make it independent from the ownership of the banks (

Trisanti 2016). Personal relationships can cause suspicious complications because they will result in cooperation or conflict of interest which highly impacts the maintenance of the independence of audit practice in the banks. The most interesting finding is that moderation of the audit committee monitors the quality and flow of information between shareholders, managers of banks and board members, which can identify any problem in the business, as addressed in the previous study of (

Brauweiler et al. 2019).

In addition, the present findings demonstrated that the audit committee highly moderates the determination of creative accounting on financial reporting quality in the commercial banking sector. Thus, it highlighted the intensive auditing practice embedded in the bank, posited to be directly related to financial reporting quality (

Rozidi et al. 2015;

Aifuwa et al. 2018;

Suprianto et al. 2017;

Salehi et al. 2018). In addition, the agency theory, or in other words information asymmetry between owners and managers, opportunistic behaviour of managers, and the failure of the principals to control the desired action of the agent. provides a theoretical framework to expand the present understanding of how such banks collapsed, a faithful representation of the findings in consistent view with previous works of (

Muraina and Dandago 2020;

Sharma et al. 2020;

Farhan et al. 2019).

As discussed in the previous sections, most of the earlier reports concluded that creative accounting determination generally depends on the framework, idiosyncrasies and interconnectivity (

Mahboub 2017;

Rozidi et al. 2015;

Lim et al. 2017;

Alzeban 2020). It was indicated that a perfect solution is impossible for all financial sectors, wherein creative accounting might be inappropriate and dependent on the contexts. Therefore, the level of creative practice may vary appreciably from one sector to another (

Goel 2014). The present findings contributed by presenting concurrent evidence on the flexibility of creative accounting determinants with a higher degree of implication of corporate aspects and financial reporting quality. The obtained findings also strongly emphasized the significant impacts of the moderator on the enhanced determination of creative practice, as well as the strength and the quality of financial reporting within Iraqi commercial banks.

The findings showed the importance of implementing an audit committee to moderate the relationships among the determinants and financial reporting quality in the banking sector of Iraq. Thus, entrepreneurial administration is needed connected to the identification of the scope and recognition of the problem, as well as trends in the commercial banks. This process enabled the management to contribute to the adjustment and upgrading of daily schedules, largely tactical acts for transforming the reporting systems of the banks into a higher level of qualified reporting practice (

Brauweiler et al. 2019;

Haji and Anifowose 2020). This identification has been shown in the findings of this study which supports required reform through the moderation of corporate aspects for financial reporting quality. In conclusion, this study showed harmony with the views demonstrated in most of the previous studies in the literature on the determination of creative practice that influences the preparation of financial reports as mentioned by (

Al-Olimat 2020;

Farhan Jedi and Nayan 2018;

Jadah 2016;

Kazem 2012).

5. Recommendation for Future Studies

Despite several notable contributions made by this study, some limitations have been encountered. Thereby, acknowledging these limitations contributes to the trustworthiness of the present research findings. This research is concerned with the variables defined in the conceptual design which aims to maintain a balanced view in the diagnostic and interactive use of the model in the Iraqi commercial banks. Such a design for different banking sectors, concerning factors like the determinants of creative accounting and audit committee changes, may vary, according to the contemporary environmental opportunities or threats, in investigating the profitability of the data in the specific banking sector that may not be completely applicable. Thus, the examination of these factors in different research contexts can offer a more inclusive perception of the mechanism and condition of the model and how it might fit in various banking sectors. Besides, new investigations can contribute to the generalization of the present research framework.

Therefore, the present study may serve as the platform on which further studies might be performed to enhance the field knowledge. As discussed in the previous sections, the present study conflicted with some previous studies and was consistent with others. However, the present study’s limitations can be avoided in future research. Besides, further research can be associated with the market valuation controversies. Further, to explain and address such a debate regarding banking markets, it may be essential to carry out further studies to understand how the deployment of the audit committee may affect determination of creative accounting practice in estimating market valuation of competitiveness. Therefore, the main area for future research is represented in adjusting the present conceptual model in multidimensional agreement with the International Accounting Standard Board 215 (IASB) in various research contexts. This must be observed by both internal control and the audit committee for a better presentation of financial reporting practice. Finally, it is recommended that future longitudinal studies must include the opinions of multiple sources of information from management and other auditing levels to confirm their impacts on developing the determination of creative accounting and financial reporting quality.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}