Socially-Oriented Approach to Financial Risk Management as the Basis of Support for the SDGs in Entrepreneurship

Abstract

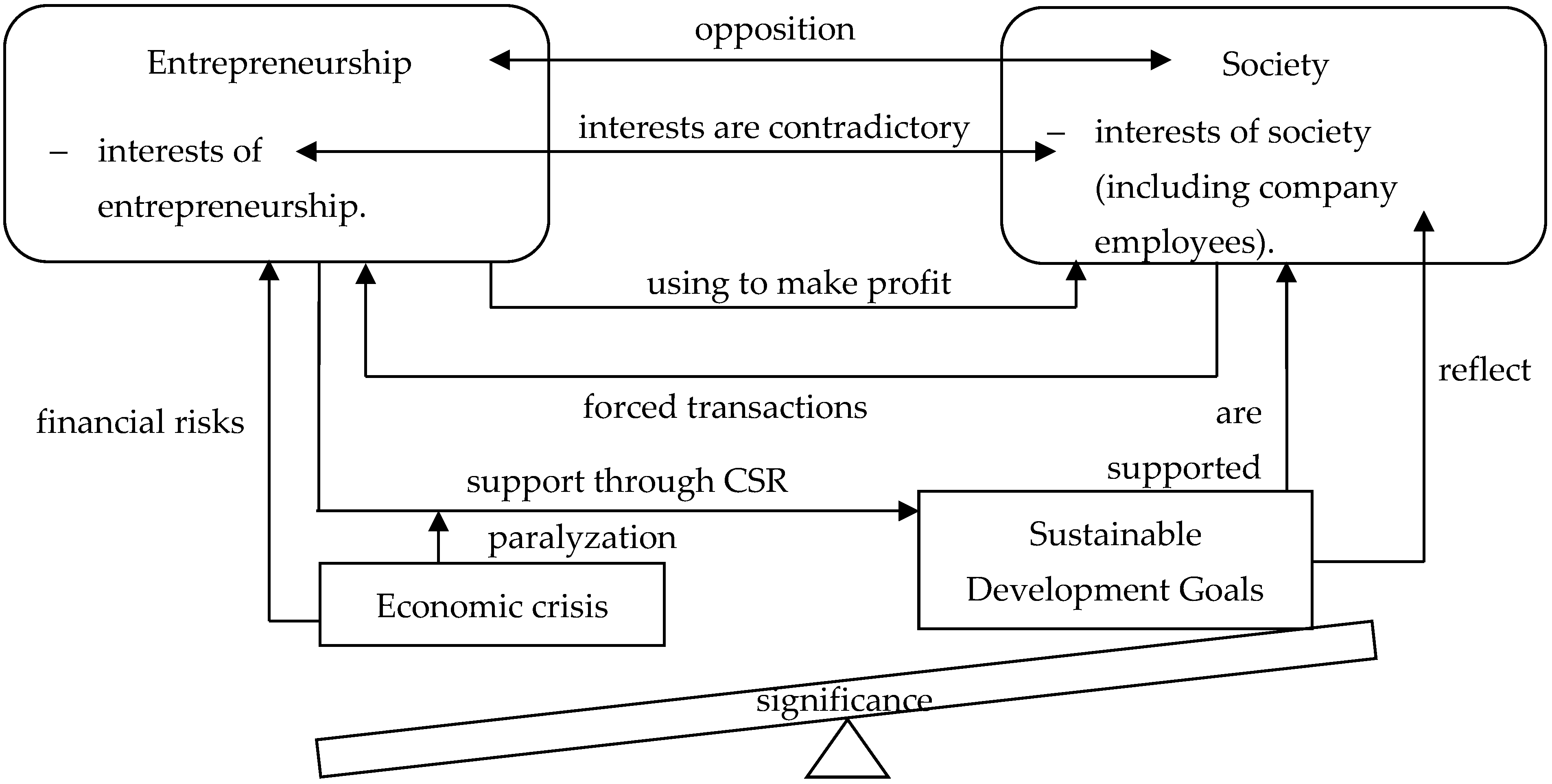

:1. Introduction

- -

- Determining the level of financial risks and the impact of the COVID-19 pandemic and crisis on them;

- -

- Proposing a socially-oriented approach to financial risk management in entrepreneurship and outlining its specifics and advantages (compared to the business-oriented approach);

- -

- Assessing the applicability of the socially-oriented approach to financial risk management in entrepreneurship under the conditions of crisis.

2. Literature Review

- -

- Whether long-term (strategic) advantages of the manifestation of corporate social responsibility during financial risk management could be obtained (first gap);

- -

- If they could be obtained, how is it possible (using which approach) to obtain them, since the existing business-oriented approach to financial risk management of entrepreneurship fully excludes the manifestation of corporate social responsibility in the process of this management (second gap);

- -

- If the appropriate approach is identified, whether it is possible to obtain long-term (strategic) advantages of the manifestation of corporate social responsibility during financial risk management in an economic crisis (third gap).

3. Materials and Methods

- -

- Zero (risk is absent), if there is no negative dynamics of the indicator’s change amid the pandemic;

- -

- Low, if negative dynamics of the indicator’s change amid the pandemic do not exceed 5% (in absolute value);

- -

- Moderate, if negative dynamics of the indicator’s change amid the pandemic are in the range of 5–10% (in absolute value);

- -

- High, if negative dynamics of the indicator’s change amid pandemic exceed 10% (in absolute value).

- -

- Caused by the COVID-19 pandemic and crisis, if the dynamics of the indicator’s change were positive before the pandemic, but became negative during the pandemic;

- -

- Increased by the COVID-19 pandemic and crisis, if the dynamics of the indicator’s change before the pandemic had been negative and further grew during the pandemic.

- -

- Underdeveloped countries (way behind developed and developing countries, with a slow rate of economic development);

- -

- Developing countries (slightly behind developed countries, with a fast rate of economic development);

- -

- Developed countries (OECD).

4. Results

- -

- Underdeveloped countries, where domestic credit to the private sector grew in 2019 (in comparison with 2018) by 1.12% (the risk was present before the pandemic, but it was low), and in 2020 (in comparison with 2019) by 53.52% (the risk grew manifold during the pandemic);

- -

- In developing countries, where domestic credit to the private sector grew in 2019 (in comparison with 2018) by 3.09% (the risk was present before the pandemic, but it was low), and in 2020 (in comparison with 2019) by 8.95% (the risk grew to the moderate level during the pandemic);

- -

- In developed countries, where domestic credit to the private sector in 2019 (in comparison with 2018) demonstrated positive dynamics (9.357%, i.e., there was no risk before the pandemic), and in 2020 (in comparison with 2019) grew by 10.51% (high risk emerged during the pandemic).

- -

- Underdeveloped countries, where market capitalization of listed domestic companies grew in 2019 (in comparison with 2018) by 7.30%, and in 2020 (in comparison with 2019) only by 1.82% (the pandemic significantly reduced the growth);

- -

- Developed countries, where market capitalization of listed domestic companies grew in 2019 (in comparison with 2018) by 28.39%, and in 2020 (in comparison with 2019) only by 3.27% (the pandemic significantly reduced the growth).

- -

- Developing countries, where total investment reduced in 2019 (in comparison with 2018) by 3.48% (the risk existed before the pandemic, but it was low) and in 2020 (in comparison with 2019 by 17.67% (during the pandemic, the risk grew to a high level;)

- -

- Developed countries, where total investment reduced in 2019 (in comparison with 2018) by 0.06% (the risk existed before the pandemic, but it was low) and in 2020 (in comparison with 2019) by 1.34% (during the pandemic, the risk grew but remained at a low level).

- -

- Increase in domestic credit to private sector by 0.58% of GDP. On the one hand, the support of the SDG increases business solvency, i.e., increases the accessibility of borrowed resources to the business. On the other hand, the financial leverage of business decreases (the share of borrowed assets in the structure of private entrepreneurial capital grows). Therefore, the influence of the Sustainable Development Index on this financial risk is contradictory. The regression model is sufficiently reliable—this is shown by the moderate value of the correlation coefficient (29.70%) and the significance F value of 0.12;

- -

- Decrease in lending interest rate by 0.05%. This could be explained by government support for the corporate social (and ecological) responsibility of business through the expansion of access and creation of favorable conditions for subsidized credit. The influence of the Sustainable Development Index on this financial risk is positive and moderate (correlation: 23.33%), but the regression model is insufficiently reliable—this is demonstrated by the significance F value of 0.25;

- -

- Increase in market capitalization of listed domestic companies by 0.22% of GDP. This is proof of the clear contribution that support of the SDGs has to the increase in market capitalization of the business. The influence of the Sustainable Development Index on this financial risk is positive and moderate (correlation: 17.52%), but the regression model is insufficiently reliable, which is shown by the significance F value of 0.25;

- -

- Decrease in inflation, consumer prices (annual) by 0.003%. Therefore, the systemic support of the SDGs at all stages of the added value chain reduced the risk of the growth of purchasing prices (costs). The influence of the Sustainable Development Index on this financial risk is positive and moderate (correlation: 3.38%), but the regression model is insufficiently reliable, which is shown by the significance F value of 0.83;

- -

- Decrease in total investment by 0.04% of GDP. This contradictory result should be treated with caution during the differentiation of regular (commercial) and responsible investments. There is no doubt that the support of the SDGs in business ensures an inflow of responsible investments, but regular (commercial) investments might reduce in this case. For this risk, moderate correlation (16.14%) combined with insufficient reliability of the regression model (significance F = 0.29) show the inexpedience of further consideration of this risk due to its contradictory character;

- -

- Increase in gross national savings by 0.30% of GDP. Therefore, the influence of the Sustainable Development Index on this financial risk is positive. The regression model is sufficiently reliable—this is shown by the high value of the correlation coefficient (53.92%) and significance F value of 0.0001.

- -

- ‘Shadowization’ of activities to reduce the tax burden, refusal of responsible innovations to manage the risks of the deficit of financial resources, forced increase in loan assets, an increase in credit interest rates, reduction of market capitalization of the business, and deficit of investments;

- -

- Increase in prices (transferring the increased expenditure to consumers) to manage the risk of purchasing power prices’ (prime cost) growth;

- -

- Reduction of product quality with unchanged or increased prices during the management of the risk of reduction of the effective demand volume.

- -

- Optimization of business processes to reduce expenditures and preservation of responsible innovations to manage the risks of the deficit of financial resources, as well as the forced increase in loan assets, an increase in credit interest rates, reduction of market capitalization of the business, and the deficit of investments;

- -

- Flexible pricing policy given the specifics of consumer categories to manage the risk of growth of purchasing prices (prime cost);

- -

- Preservation or equal reduction of quality and prices to manage the risk of reduction of the volume of effective demand.

- -

- Stability and consistency of corporate culture and its harmonious combination with the practice of crisis management of the responsible business;

- -

- Invariably high competitive advantages in loyalty: business possesses a substantial social capital; loyalty of employees (best personnel, increased efficiency, and unique corporate knowledge) and loyalty of consumers (stable and high demand, reduced price-demand elasticity).

5. Discussion

- -

- Quantitative measuring of this contribution. It has been established that an increase in the Sustainable Development Index by 1 point leads to an increase in market capitalization of listed domestic companies by 0.22% of GDP. The correlation between the indicators is moderate: the change of the market capitalization of business by 17.52% is due to the change in the Sustainable Development Index;

- -

- Specification of the condition for achieving this contribution. This condition is as follows: corporate social responsibility must completely thread the activity of business structures and be the core of their functioning, based on the socially-oriented approach to financial risk management. The use of the business-oriented approach with the secondary characteristics (small significance or small scale) of corporate social responsibility does not allow developing the potential contribution of corporate social responsibility to financial risk management. General sustainable development at the level of economy with insufficient support of the SDGs from business cannot ensure the reliable connection between the market capitalization of business and sustainable development. A solution here is corporate social responsibility with the focus on the support of SDGs in business, implemented with the help of the socially-oriented approach to financial risk management.

- -

- Provides long-term (strategic) advantages of the manifestation of corporate social responsibility during financial risk management: (1) stability and consistency of corporate culture, its harmonious combination with the practice of crisis management of responsible business; (2) invariable high competitive advantages in loyalty (thus filling the first gap);

- -

- Implies the manifestation of corporate social responsibility in the process of financial risk management of entrepreneurship, i.e., provides continuous support for the SDGs in the business environment (thus filling the second gap);

- -

- The described long-term (strategic) advantages of the manifestation of corporate social responsibility during the management of financial risks could be obtained during an economic crisis (thus filling the third gap).

6. Conclusions

- -

- High risk of a deficit of financial resources and forced increase in loan assets caused by the COVID-19 pandemic and crisis—this is most evident in underdeveloped countries.

- -

- Moderate risk of reduction of market capitalization of business, further increased by the COVID-19 pandemic and crisis—this is most evident in underdeveloped and developed countries.

- -

- High risk of growth of purchasing prices (prime cost), caused by the COVID-19 pandemic and crisis—this is most evident in developing countries.

- -

- The high risk of a deficit of investments, further increased by the COVID-19 pandemic and crisis—this is most evident in developing countries.

- -

- High risk of reduction of the volume of effective demand, caused by the COVID-19 pandemic and crisis—this is most evident in developing countries.

- -

- Establishing society’s interests as primary (key) interests, which ensure the achievement of the interests of both the economy and society;

- -

- Peripheral place of financial risks in the system of business risks;

- -

- The priority of financial risk management is the preservation of corporate knowledge and a positive image;

- -

- Prospective measures of financial risk management are recommended; they include optimization of business processes to reduce expenditures, preservation of responsible innovations, flexible pricing policy given the specifics of the categories of consumers, and preservation or equal reduction of quality and prices.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- Aloui, Mouna, Bassem Salhi, and Anis Jarboui. 2019. Market risk, corporate governance, and the regulation during the recent financial crisis: The French context. International Journal of Managerial Finance 15: 700–18. [Google Scholar] [CrossRef]

- Arslan-Ayaydin, Özgür, and James Thewissen. 2016. The financial reward for environmental performance in the energy sector. Energy & Environment 27: 389–413. [Google Scholar]

- Ayadi, Mohamed, Walid Ben Omrane, Jiayu Wang, and Robert Welch. 2022. Senior official speech attributes and foreign exchange risk around business cycles. International Review of Financial Analysis 80: 102011. [Google Scholar] [CrossRef]

- Bae, Kee-Hong, Sadok El Ghoul, Zhaoran Jason Gong, and Omrane Guedhami. 2021. Does CSR matter in times of crisis? Evidence from the COVID-19 pandemic. Journal of Corporate Finance 67: 101876. [Google Scholar] [CrossRef]

- Barontini, Roberto, and Jonathan Taglialatela. 2021. Patents and small business risk: Longitudinal evidence from the global financial crisis. Journal of Small Business and Enterprise Development. [Google Scholar] [CrossRef]

- Berkman, Henk, Michelle Li, and Helen Lu. 2021. Trust and the value of CSR during the global financial crisis. Accounting and Finance 61: 4955–65. [Google Scholar] [CrossRef]

- Bratis, Tteodoros, Nikiforos Laopodis, and Georgios Kouretas. 2020. Systemic risk and financial stability dynamics during the Eurozone debt crisis. Journal of Financial Stability 47: 100723. [Google Scholar] [CrossRef]

- Çağıl, Gulcan, and Sibel Yilmaz Turkmen. 2017. Renewable energy financing with a sustainable financial system following the 2008 financial crisis in developing countries. Contributions to Economics 2018: 259–74. [Google Scholar] [CrossRef]

- Chaivisuttangkun, Sirithida, and Pornsit Jiraporn. 2021. The effect of co-opted directors on firm risk during a stressful time: Evidence from the financial crisis. Finance Research Letters 39: 101538. [Google Scholar] [CrossRef]

- Galindo-Martín, Miguel-Ángel, Maria-Soledad Castaño-Martínez, and Maria-Teresa Méndez-Picazo. 2021. Effects of the pandemic crisis on entrepreneurship and sustainable development. Journal of Business Research 137: 345–53. [Google Scholar] [CrossRef]

- Harjoto, Maretno, and Indrarini Laksmana. 2018. The impact of corporate social responsibility on risk taking and firm value. Journal of Business Ethics 151: 353–73. [Google Scholar] [CrossRef]

- Havlinova, Aneta, and Jiri Kukacka. 2021. Corporate Social Responsibility and Stock Prices after the Financial Crisis: The Role of Strategic CSR Activities. Journal of Business Ethics. [Google Scholar] [CrossRef]

- He, Jie, Alastair Morrison, and Hao Zhang. 2021. Being sustainable: The three-way interactive effects of CSR, green human resource management, and responsible leadership on employee green behavior and task performance. Corporate Social Responsibility and Environmental Management 28: 1043–54. [Google Scholar] [CrossRef]

- Hu, Grace Xing. 2020. Rollover risk and credit spreads in the financial crisis of 2008. Journal of Finance and Data Science 6: 1–15. [Google Scholar] [CrossRef]

- International Monetary Fund. 2021. World Economic Outlook Database: October 2021. Available online: https://www.imf.org/en/Publications/WEO/weo-database/2021/October (accessed on 24 November 2021).

- Jiang, Jiaqi, and Yun Feng. 2021. The interaction of risk management tools: Financial hedging, corporate diversification and liquidity. International Journal of Finance and Economics 26: 2396–413. [Google Scholar] [CrossRef]

- Kabonga, Itai. 2020. Reflections on the ‘Zimbabwean crisis 2000–2008’ and the survival strategies: The sustainable livelihoods framework (SLF) analysis. Africa Review 12: 192–212. [Google Scholar] [CrossRef]

- Khan, Asif, Chih-Cheng Chen, Kwanrat Suanpong, Athapol Ruangkanjanases, Santhaya Kittikowit, and Shih-Chih Chen. 2021. The impact of CSR on sustainable innovation ambidexterity: The mediating role of sustainable supply chain management and second-order social capital. Sustainability 13: 12160. [Google Scholar] [CrossRef]

- Kharlanov, Alexey, Yuliya Bazhdanova, Teimuraz Kemkhashvili, and Natalia Sapozhnikova. 2022. The Case Experience of Integrating the SDGs into Corporate Strategies for Financial Risk Management Based on Social Responsibility (with the Example of Russian TNCs). Risks 10: 12. [Google Scholar] [CrossRef]

- Kruger, Chamay, Willem Daniel Schutte, and Tanja Verster. 2021. Using model performance to assess the representativeness of data for model development and calibration in financial institutions. Risks 9: 204. [Google Scholar] [CrossRef]

- Liang, Quanxi, Jiangshan Liao, and Leng Ling. 2022. Social interactions and mutual fund portfolios: The role of alumni networks in China. China Finance Review International. [Google Scholar] [CrossRef]

- Lippi, Andrea, and Simone Rossi. 2020. Run for the hills: Italian investors’ risk appetite before and during the financial crisis. International Journal of Bank Marketing 38: 1195–213. [Google Scholar] [CrossRef]

- Liu, Yipeng, and Fabian Jintae Froese. 2020. Crisis management, global challenges, and sustainable development from an Asian perspective. Asian Business and Management 19: 271–76. [Google Scholar] [CrossRef]

- Lopata, Ewelina, and Krzystof Rogatka. 2021. CSR&COVID19-How do they work together? Perceptions of Corporate Social Responsibility transformation during a pandemic crisis. Towards smart development. Bulletin of Geography. Socio-Economic Series 53: 87–103. [Google Scholar] [CrossRef]

- Ma, Yu-Luen, and Yayuan Ren. 2021. Insurer risk and performance before, during, and after the 2008 financial crisis: The role of monitoring institutional ownership. Journal of Risk and Insurance 88: 351–80. [Google Scholar] [CrossRef]

- Machokoto, Michael, Geofry Areneke, and Davis Nyangara. 2021. Financial conservatism, firm value and international business risk: Evidence from emerging economies around the global financial crisis. International Journal of Finance and Economics 26: 4590–608. [Google Scholar] [CrossRef]

- Magrizos, Solon, Eleni Apospori, Marylyn Carrigan, and Rosalind Jones. 2021. Is CSR the panacea for SMEs? A study of socially responsible SMEs during economic crisis. European Management Journal 39: 291–303. [Google Scholar] [CrossRef]

- Mori, Masaki, Seow Eng Ong, and Joseph Ooi. 2022. The Revival of Business Groups’ Risk Sharing: Evidence from Japanese Real Estate Investment Trust Market. Journal of Real Estate Finance and Economics, 1–35. [Google Scholar] [CrossRef]

- Pérez, Óscar Iván, Maria Claudia Romero, and Paola González Vargas. 2020. Interlinkages and synergies between sdg: An analysis from the perspective of social responsibility in Colombia. Desarrollo y Sociedad 2020: 191–244. [Google Scholar] [CrossRef]

- Popkova, Elena G., and Bruno S. Sergi. 2021. Dataset Modelling of the Financial Risk Management of Social Entrepreneurship in Emerging Economies. Risks 9: 211. [Google Scholar] [CrossRef]

- Rouleau, Linda, Markus Hällgren, and Mark de Rond. 2021. Covid-19 and Our Understanding of Risk, Emergencies, and Crises. Journal of Management Studies 58: 243–46. [Google Scholar] [CrossRef]

- Safta, Ioana Lavinia, Andrada-Ioanna Sabău (Popa), and Neli Muntean. 2021. Bibliometric analysis of the literature on measuring techniques for manipulating financial statements. Risks 9: 123. [Google Scholar] [CrossRef]

- Saha, Mallika, and Kumar Debasis Dutta. 2022. Does governance quality matter in the nexus of inclusive finance and stability? China Finance Review International. [Google Scholar] [CrossRef]

- Servaes, Henri, and Ane Tamayo. 2013. The impact of corporate social responsibility on firm value: The role of customer awareness. Management Science 59: 1045–61. [Google Scholar] [CrossRef] [Green Version]

- Shahzad, Akmal, Bushra Zulfiqar, Mumtaz Ali, Ayaz ul Haq, Maryam Sajjad, and Ahmad Raza. 2022. Mediating role of formalization of RM methods among the perceived business risk and organization performance. Cogent Business and Management 9: 2024116. [Google Scholar] [CrossRef]

- Shayan, Niloufar Fallah, Nasrin Mohabbati-Kalejahi, Sepideh Alavi, and Mohammad Ali Zahed. 2022. Sustainable Development Goals (SDGs) as a Framework for Corporate Social Responsibility (CSR). Sustainability 14: 1222. [Google Scholar] [CrossRef]

- Sinha, Avik, Sheklar Mishra, Arshian Sharif, and Larisa Yarovaya. 2021. Does green financing help to improve environmental & social responsibility? Designing SDG framework through advanced quantile modelling. Journal of Environmental Management 292: 112751. [Google Scholar] [CrossRef] [PubMed]

- Singh, Nitya. 2022. Developing Business Risk Resilience through Risk Management Infrastructure: The Moderating Role of Big Data Analytics. Information Systems Management 39: 34–52. [Google Scholar] [CrossRef]

- Sinkovics, Noemi, Rudolf Sinkovics, and Jason Archie-Acheampong. 2021. The business responsibility matrix: A diagnostic tool to aid the design of better interventions for achieving the SDGs. Multinational Business Review 29: 1–20. [Google Scholar] [CrossRef]

- Torrès, Olivier, Alexandre Benzari, Christian Fisch, Jinia Mukerjee, Abdelaziz Swalhi, and Roy Thurik. 2021. Risk of burnout in French entrepreneurs during the COVID-19 crisis. Small Business Economics 2021: 1–23. [Google Scholar] [CrossRef]

- UNDP. 2022. SDG Index and Dashboards 2018–2020. Available online: https://www.sdgindex.org/reports/sdg-index-and-dashboards-2018/ (accessed on 3 February 2022).

- Vagin, Sergei, Elena Kostyukova, Natalia Spiridonova, and Tatiana Vorozheykina. 2022. Financial Risk Management Based on Corporate Social Responsibility in the Interests of Sustainable Development. Risks 10: 35. [Google Scholar] [CrossRef]

- Waheed, Abdul, and Qingyu Zhang. 2022. Effect of CSR and Ethical Practices on Sustainable Competitive Performance: A Case of Emerging Markets from Stakeholder Theory Perspective. Journal of Business Ethics 175: 837–55. [Google Scholar] [CrossRef]

- Weber, Véronique, and Anke Müβig. 2022. The Effect of Business Strategy on Risk Disclosure. Accounting in Europe, 1–36. [Google Scholar] [CrossRef]

- Wentzel, Lance, Jullius Auodeji Fapohunda, and Rainer Haldenwang. 2022. The Relationship between the Integration of CSR and Sustainable Business Performance: Perceptions of SMEs in the South African Construction Industry. Sustainability 14: 1049. [Google Scholar] [CrossRef]

- World Bank. 2021. Indicators: Financial Sector. Available online: https://data.worldbank.org/indicator (accessed on 24 November 2021).

- Yankovskaya, Veronika, Vladimir Osipov, Aleksei Zeldner, Tatiana Panova, and Vitalii Mishchenko. 2021. Institutional matrix of social management in region’s economy: Stability and sustainability vs innovations and digitalization. International Journal of Sociology and Social Policy 41: 178–91. [Google Scholar] [CrossRef]

- Zhang, Yuming, Chao Xing, Quanli Zhang, and Xinyue Zhang. 2022. Crises and changes: The impacts of CSR expenditure on loan and subsidy allocation in China’s Pre- and Post-Pandemic periods. Finance Research Letters, 102697. [Google Scholar] [CrossRef]

- Zizi, Youssef, Amine Jamali-Alaoui, Badreddine El Goumi, Mohamed Oudgou, and Abdelsalam El Moudden. 2021. An optimal model of financial distress prediction: A comparative study between neural networks and logistic regression. Risks 9: 200. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Category of Countries | Country | GDP per Capita Growth in 2020 (Annual %) | Domestic Credit to the Private Sector (% of GDP) | Lending Interest Rate (%) | ||||

|---|---|---|---|---|---|---|---|---|

| 2018 | 2019 | 2020 | 2018 | 2019 | 2020 | |||

| Underdeveloped countries | Macao SAR, China | −56.9 | 113.39 | 119.51 | 280.34 | 5.29 | 5.36 | 5.26 |

| Maldives | −33.2 | 31.65 | 32.01 | 49.02 | 10.68 | 11.52 | 11.60 | |

| Fiji | −19.6 | 92.80 | 100.67 | 123.83 | 5.68 | 6.03 | 6,19 | |

| Panama | −19.2 | 87.04 | 87.06 | 107.97 | 6.88 | 7.09 | 7.01 | |

| Dominica | −16.9 | 47.49 | 43.01 | 57.14 | 7.81 | 7.54 | 6.94 | |

| Developing countries | Philippines | −10.8 | 47.56 | 47.97 | 51.89 | 6.12 | 7.10 | no data |

| Kyrgyzstan | −10.5 | 23.37 | 24.61 | 28.46 | 19.51 | 19.00 | 17.04 | |

| Mexico | −9.2 | 34.55 | 36.57 | 38.66 | 8.04 | 8.43 | 6.34 | |

| India | −8.9 | 50.37 | 50.13 | 55.25 | 9.45 | 9.47 | 9.15 | |

| Colombia | −7.8 | 49.57 | 51.50 | 54.08 | 12.11 | 11.77 | 9.85 | |

| Developed countries (OECD) | Spain | −11.2 | 99.57 | 94.68 | 108.52 | no data | no data | no data |

| UK | −10.3 | 134.63 | 133.53 | 146.45 | no data | no data | no data | |

| Italy | −8.6 | 76.71 | 74.28 | 83.58 | 2.68 | 2.60 | 2.33 | |

| Greece | −8.2 | 91.66 | 80.93 | 82.09 | no data | no data | no data | |

| France | −8.1 | 104.27 | 107.12 | 122.45 | no data | no data | no data | |

| Category of Countries | Country | Market Capitalization of Listed Domestic Companies (% of GDP) | Inflation, Consumer Prices (Annual %) | ||||

|---|---|---|---|---|---|---|---|

| 2018 | 2019 | 2020 | 2018 | 2019 | 2020 | ||

| Underdeveloped countries | Macao SAR, China | no data | no data | no data | 3.01 | no data | no data |

| Maldives | no data | no data | no data | −0.13 | 0.22 | −1.37 | |

| Fiji | no data | no data | no data | 4.08 | 1.77 | −2.60 | |

| Panama | 24.10 | 25.86 | 26.33 | 0.76 | −0.36 | −1.55 | |

| Dominica | no data | no data | no data | 0.99 | 1.50 | no data | |

| Developing countries | Philippines | 74.43 | 7.06 | 75.46 | 5.21 | 2.48 | 2.64 |

| Kyrgyzstan | no data | no data | no data | 1.54 | 1.13 | 6.33 | |

| Mexico | 31.50 | 32.60 | 37.13 | 4.90 | 3.64 | 3.40 | |

| India | 84.50 | 79.67 | 98.95 | 3.95 | 3.72 | 6.62 | |

| Colombia | 31.07 | 40.83 | 39.18 | 3.24 | 3.53 | 2.52 | |

| Developed countries (OECD) | Spain | 50.95 | 57.23 | 59.24 | 1.68 | 0.70 | −0.32 |

| UK | no data | no data | no data | 2.29 | 1.74 | 0.99 | |

| Italy | no data | no data | no data | 1.14 | 0.61 | −0.14 | |

| Greece | 18.09 | 26.13 | 26.92 | 0.63 | 0.25 | −1.25 | |

| France | 84.81 | no data | no data | 1.85 | 1.11 | 0.48 | |

| Category of Countries | Country | Total Investment (Percentage of GDP) | Gross National Savings (Percentage of GDP) | ||||

|---|---|---|---|---|---|---|---|

| 2018 | 2019 | 2020 | 2018 | 2019 | 2020 | ||

| Underdeveloped countries | Macao SAR, China | 17.213 | 14.120 | 27.605 | no data | no data | no data |

| Maldives | 20.000 | 20.000 | 20.000 | −8.386 | −6.451 | −9.925 | |

| Fiji | 20.358 | 19.942 | 18.358 | no data | no data | no data | |

| Panama | 41.453 | 39.292 | 28.547 | 33.803 | 34.302 | 30.876 | |

| Dominica | 32.031 | 23.373 | 20.998 | −10.344 | −14.499 | −3.498 | |

| Developing countries | Philippines | 27.151 | 26.402 | 17.383 | 24.591 | 25.593 | 20.973 |

| Kyrgyzstan | 27.734 | 26.370 | 18.648 | 15.682 | 14.270 | 23.155 | |

| Mexico | 22.711 | 21.166 | 19.307 | 20.658 | 20.856 | 21.739 | |

| India | 32.070 | 30.664 | 29.278 | 29.953 | 29.809 | 30.180 | |

| Colombia | 21.195 | 21.509 | 19.011 | 17.105 | 17.023 | 15.576 | |

| Developed countries (OECD) | Spain | 20.478 | 20.890 | 20.691 | 22.408 | 23.026 | 21.379 |

| UK | 17.765 | 18.340 | 17.221 | 14.084 | 15.246 | 13.508 | |

| Italy | 18.529 | 18.011 | 17.500 | 21.040 | 21.216 | 21.048 | |

| Greece | 13.337 | 12.689 | 13.450 | 9.766 | 10.456 | 6.029 | |

| France | 23.857 | 24.365 | 23.676 | 23.026 | 24.074 | 21.777 | |

| Category of Countries | Country | Sustainable Development Index, Score 0–100 | ||

|---|---|---|---|---|

| 2018 | 2019 | 2020 | ||

| Underdeveloped countries | Macao SAR, China | 70.1 | 73.2 | 73.89 |

| Maldives | 0 | 72.1 | 67.59 | |

| Fiji | 0 | 70.1 | 69.95 | |

| Panama | 64.9 | 66.3 | 69.19 | |

| Dominica | 0 | 0 | 0 | |

| Developing countries | Philippines | 65 | 64.9 | 65.5 |

| Kyrgyzstan | 70.3 | 71.6 | 73.01 | |

| Mexico | 65.2 | 68.5 | 70.44 | |

| India | 59.1 | 61.1 | 61.92 | |

| Colombia | 66.6 | 69.6 | 70.91 | |

| Developed countries (OECD) | Spain | 75.4 | 77.8 | 78.11 |

| UK | 78.7 | 79.4 | 79.79 | |

| Italy | 74.2 | 75.8 | 77.01 | |

| Greece | 70.6 | 71.4 | 74.33 | |

| France | 81.2 | 81.5 | 81.13 | |

| Financial Risk | Indicator of Financial Risk | Change of Indicator: 2019–2018, % | Change of Indicator: 2020–2019, % | Level of Risk during the COVID-19 Pandemic and Crisis |

|---|---|---|---|---|

| Deficit of financial resources and forced increase in loan assets | Domestic credit to private sector (% of GDP) | Underdeveloped countries | High risk, caused by the COVID-19 pandemic and crisis | |

| 1.12 | 53.52 | |||

| Developing countries | ||||

| 3.09 | 8.95 | |||

| Developed countries | ||||

| −3.57 | 10.51 | |||

| Growth of lending interest rate | Lending interest rate (%) | Positive changes | Risk is absent | |

| Decrease of market capitalization of business | Market capitalization of listed domestic companies (% of GDP) | Underdeveloped countries | Moderate risk, further increased by the COVID-19 pandemic and crisis | |

| 7.30 | 1.82 | |||

| Developed countries | ||||

| 28.39 | 3.27 | |||

| Growth of purchasing prices (prime cost) | Inflation, consumer prices (annual %) | Developing countries | High risk, caused by the COVID-19 pandemic and crisis | |

| −20.32 | 101.88 | |||

| Deficit of investments | Total investment (% of GDP) | Developing countries | High risk, further increased by the COVID-19 pandemic and crisis | |

| −3.48 | −17.67 | |||

| Developed countries | ||||

| −0.06 | −1.34 | |||

| Reduction of the volume of effective demand | Gross national savings (% of GDP) | Developing countries | High risk, caused by the COVID-19 pandemic and crisis | |

| −0.99 | 8.24 | |||

| Regression Statistics | Regression Models (Riskfin) | |||||

|---|---|---|---|---|---|---|

| Domestic Credit to Private Sector (% of GDP) | Lending Interest Rate (%) | Market Capitalization of Listed Domestic Companies (% of GDP) | Inflation, Consumer Prices (Annual %) | Total Investment (% of GDP) | Gross National Savings (% of GDP) | |

| Multiple R (correlation) | 0.2970 | 0.2333 | 0.1752 | 0.0338 | 0.1614 | 0.5392 |

| Significance F | 0.05 | 0.12 | 0.25 | 0.83 | 0.29 | 0.0001 |

| t-Stat | 2.04 | −1.57 | 1.17 | −0.22 | −1.07 | 4.20 |

| Constant (α) | 42.13 | 9.36 | 8.79 | 1.81 | 25.06 | −4.88 |

| Coefficient of regression (β) | 0.58 | −0.05 | 0.22 | −0.003 | −0.04 | 0.30 |

| Character of the impact of SDGs on financial risk | contradictory | positive | positive | positive | negative | positive |

| Characteristics of the Approach | Business-Oriented Approach | Socially-Oriented Approach | |

|---|---|---|---|

| Primary (key) interests | Interests of business are sought to the detriment of society’s interests | Society’s interests ensure the achievement of interests of business | |

| Role of financial risks in the system of business risks | Central | Peripheral | |

| Priority of financial risk management | Instantaneous and maximum reduction | Preservation of corporate knowledge and positive image | |

| Measures of financial risk management | Deficit of financial resources and forced increase in loan assets | ‘Shadowization’ of the activities to reduce the tax burden; refusal of responsible innovations | Optimization of business processes to reduce expenditures; preservation of responsible innovations |

| Increase in credit interest rates | |||

| Reduction of market capitalization of business | |||

| Deficit of investments | |||

| Growth of purchasing prices (prime cost) | Increase in prices (transferring increased expenditures on buyers) | Flexible pricing policy given the specifics of the categories of consumers | |

| Reduction of the volume of effective demand | Reduction of product quality with unchanged or increased prices | Preservation or equal reduction of quality and prices | |

| Strengths (S) | Weaknesses (W) |

|

|

| Opportunities (O) | Threats (T) |

|

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhilkina, A.N.; Karp, M.V.; Bodiako, A.V.; Smagulova, S.M.; Rogulenko, T.M.; Ponomareva, S.V. Socially-Oriented Approach to Financial Risk Management as the Basis of Support for the SDGs in Entrepreneurship. Risks 2022, 10, 42. https://doi.org/10.3390/risks10020042

Zhilkina AN, Karp MV, Bodiako AV, Smagulova SM, Rogulenko TM, Ponomareva SV. Socially-Oriented Approach to Financial Risk Management as the Basis of Support for the SDGs in Entrepreneurship. Risks. 2022; 10(2):42. https://doi.org/10.3390/risks10020042

Chicago/Turabian StyleZhilkina, Anna N., Marina V. Karp, Anna V. Bodiako, Samal M. Smagulova, Tatiana M. Rogulenko, and Svetlana V. Ponomareva. 2022. "Socially-Oriented Approach to Financial Risk Management as the Basis of Support for the SDGs in Entrepreneurship" Risks 10, no. 2: 42. https://doi.org/10.3390/risks10020042

APA StyleZhilkina, A. N., Karp, M. V., Bodiako, A. V., Smagulova, S. M., Rogulenko, T. M., & Ponomareva, S. V. (2022). Socially-Oriented Approach to Financial Risk Management as the Basis of Support for the SDGs in Entrepreneurship. Risks, 10(2), 42. https://doi.org/10.3390/risks10020042