1. Introduction

Stochastic diffusion processes with linear drift and multiplicative noise are often considered both in theory and applications because they constitute a good compromise between adherence to reality and mathematical tractability when used as models of real phenomena. Among these processes, the Geometric Brownian Motion plays a prominent role in particular in the context of financial modeling. Much is known about this process, although a lack of results emerges when dealing with its version with non-zero asymptotic mean, namely the Inhomogeneous Geometric Brownian Motion (IGBM). The IGBM belongs to the class of Pearson diffusions [

1,

2] but goes under different names according to the field of study. In the interest rates field, it is called the Brennan-Schwartz model [

3,

4], denoted as the GARCH model when used for stochastic volatility and for energy markets [

5], as Lognormal diffusion process with exogenous factors when used for forecasting and analysis of growth [

6,

7], in real option literature, it goes under the names of Geometric Brownian motion with affine drift [

8,

9], Geometric Ornstein-Uhlenbeck [

10] or mean-reverting Geometric Brownian motion [

11].

Here we want to address the related first-passage-time (FPT) problem that arises in many applications in which the stochastic process evolves in the presence of a threshold [

12]. First-passage properties underlie a wide range of stochastic processes, spanning from diffusions with limited growth, to the dynamics of the spike generation in neurons or the triggering of stock options.

The mathematical study of the FPT problem rarely leads to a simple finding of the distribution of the random variable FPT, since it can be written in a closed-form expression only in a few cases [

13]. Most of the time it consists in the finding of integral equations involving the FPT density or in the calculation of its Laplace transform ( see [

14] for an extensive review). From these equations, information on the moments of the random variable or numerical evaluation of its density can be obtained.

Unlike its simpler version, the IGBM presents some difficulties when using these mathematical tools. The transition density of the IGBM does not have a practical closed-form expression [

8,

15] and this complicates the use of Volterra integral equations involving the FPT probability density function (pdf). Even the calculation of the moments of FPT is unpractical, despite the closed-form formula for the Laplace transform of the FPT pdf is available in the literature [

15]. In fact, the computation requires high order derivatives of a ratio of hypergeometric functions with respect to the first parameter, and to the best of our knowledge, only the expression of the first moment has been obtained with this strategy so far.

Moreover, an exact simulation scheme is not available. The classical Euler-Maruyama and Milstein methods exhibit non-zero probability to cross the entrance or exit boundaries even for arbitrary small time steps, that is the nature of the boundary is not preserved [

16]. For this reason, analytical expressions are of primary importance, but a different strategy must be undertaken.

Recently an approach that uses cumulants to obtain FPT pdf and related statistics has been proposed [

17,

18]. In particular in [

18], we propose an approximation of the FPT pdf of a square-root stochastic process by using cumulants and a Laguerre-Gamma polynomial approximation. The method is based on the closed-form expressions for cumulants recovered from the Laplace transform

of the FPT random variable

thanks to the use of the algebra of formal power series of

Cumulants encode many of the statistical properties of a pdf. For example, the third-order cumulant accounts for the skewness of the FPT pdf while the fourth-order cumulant involves the weight of tails in causing dispersion, that is the kurtosis. Moreover, from cumulants, moments of any order can be recovered.

To apply this method, the starting point is the availability of a closed-form expression of

in terms of power series. Unfortunately, this is not the case for the IGBM, but we exploit a property of the Tricomi function involving an asymptotic expansion. This expansion allows us to write

as a formal series in powers of

z which results to be particularly suited when transformed via the logarithm function. Thus in the case of a strong positive drift, we are able to get an approximation of the cumulants of

T of any order. In

Section 4.2 we stress that a good approximation of the first cumulant is better achieved when the starting point of the dynamics is close to the threshold suggesting that, in this case, the approximated cumulants could be used to approximate the FPT pdf even for small times

t.

We check the goodness of the approximation using realistic sets of parameters coming from two fields of application of the IGBM: neuronal modeling with reversal potential and mean reversion models of financial markets.

The IGBM has been used to model the changes in the membrane depolarization between two consecutive neuronal spikes in models in which the changes in depolarization are state-dependent and an inhibitory reversal potential is present [

19,

20,

21,

22,

23]. Further, by solving the related FPT problem, the dynamics of the spike generation have been described especially through the instantaneous firing rate that is the reciprocal of the first FPT cumulant [

24]. However, it is still undisclosed how the input statistics affect the moments of order higher than one of the neuronal output [

25,

26,

27].

The second application deals with models of financial markets with mean reversion where the study of extreme events, such as defaults, can be studied using the problems of first-passage time or exit time from a region. In this context the IGBM is better know as the GARCH diffusion process or Brennan–Schwartz model and it is characterized by the properties that the changes in the short rate are state-dependent and unlimited excursions of the process are not allowed (see for instance [

3,

4,

28]).

2. IGBM and the Related First-Passage-Time Problem

The inhomogeneous geometric Brownian motion (IGBM) is the diffusion process with infinitesimal mean and variance:

It is described by the stochastic differential equation

with

,

and

is a standard Wiener process. Equation (

2) is a linear SDE and admits a unique strong solution.

According to the Feller classification of boundaries if then v is an entrance boundary, i.e., it cannot be reached by in finite time, and there is no probability flow to the outside of the interval . We will always consider this case in the following.

We note that, for

, the solution of Equation (

2) corresponds to the well-known Geometric Brownian motion [

29]. Although for this last process a large literature is available, less is known about the IGBM. The transition density of the IGBM does not have a practical closed-form expression [

8,

30] and an exact simulation scheme is not available albeit very recently a splitting numerical method has been proposed [

16]. Explicit expressions of the IGBM solution of Equation (

2) can be found for instance in [

5] or [

31]. In particular in [

31] the IGBM moments are written in terms of a transformed Brownian motion, obtained using a change of time method.

We want to address the problem of the evolution of the IGBM process

in the presence of a constant threshold

S. In particular, we are interested in the random time

T the process

starting in

crosses

S for the first time. This random variable goes under the name of first-passage time (FPT) and is defined as

An analytical closed-form expression for the probability density function

of

T for the IGBM process is not available but its Laplace transform is known [

15]

where

and

is the confluent hypergeometric function of the second kind (or Tricomi’s function [

32]). When evaluated in

the Laplace transform (

4) returns the probability of crossing

In principle, moments of

T (or equivalently cumulants) of any orders can be computed using higher derivatives of

when they exist. For the IGBM process, only the first moment is known to have an explicit analytical expression, due to the cumbersome expression of

Indeed, from Equation (

4), in Ref. [

23] the mean FPT has been written using hypergeometric functions

as follows

with

and

. The previous formula holds for

; if

, Equation (

6) is intended as taking the following limit

Asymptotic expansions of the mean first passage time around the starting position

or around the boundary points are given in [

15].

To the best of our knowledge, explicit expressions for the variance of T or higher-order moments are not available in the literature for the IGBM process. The derivation from the Laplace transform is impractical, involving at least second derivatives of the Tricomi functions with respect to the first parameter.

Often, where analytical methods are impractical, numerical solutions are sought. In terms of complexity, difficulties apply as well in the numerical evaluation of moments of

T through the Siegert equation [

33],

although the stationary distribution

of

in the absence of a threshold is known to be a shifted inverse gamma distribution with the following shape, scale and location parameters [

23]

For all these reasons in the next section we propose a method based on the algebra of formal power series, to compute approximations of the cumulants of

T using an asymptotic expansion of the Laplace transform

Indeed an important asymptotic expansion of

is known when

namely [

34]

with

,

the rising factorial. As

for fixed

the rhs of (

9) returns the hypergeometric series

Note that the series is divergent unless a or are non-positive integers when it reduces to a polynomial. Nevertheless we might write by using the Borel summation of the series. In the following we deal with as it was an exponential formal power series in Indeed Lemma 1 in the subsequent section shows that with the ring of formal power series in the indeterminate a with coefficients in

3. Formal Cumulants

Given a sequence

of real numbers, with

the sequence of its formal cumulants

is such that

Note that in the ring

of formal power series in

the (exponential) formal power series

is well defined [

35] with

Then

are also said formal cumulants of

A polynomial expression of formal cumulants

in terms of

involves the logarithmic (partition) polynomials

where

are the partial exponential Bell polynomials [

36]

with the sum taken over all sequences

of non negative integers such that

In addition, the sequence

might be recovered from its formal cumulants

by using the complete Bell (exponential) polynomials

with

given in Equation (

14) and

replaced by

Remark 1. Both the k-th logarithmic polynomial (13) and the k-th complete Bell polynomial (15) are special cases of the k-th general partition polynomial [37] In particular, for we recover the k-th logarithmic polynomial as given in (13) whereas for we recover the the k-th complete Bell (exponential) polynomials as given in (15). Moreove if and are the coefficients of two exponential formal power series in let’s saythen the k-th general partition polynomial gives the k-th coefficient of the exponential formal power series composition [35]. When

is the Laplace transform of a pdf

then the logarithmic and the complete Bell polynomials allow us to deal with cumulants and moments related to

In particular, if

is the Laplace transform of the FPT pdf and the rhs of Equation (

12) is its Taylor expansion about

then

and there exist cumulants of any order

see for instance [

38]. In particular, from Equations (

11) and (

13), we have

Approximations of FPT Cumulants

Set

so that, according to the definitions (

5), we have

From (9) and (10), in the range of parameters such that the asymptotic expression (9) holds, the ratio

gives an approximation of the FPT Laplace transform

given in (

4). The aim of the subsequent Theorem 1 is to prove that

Thus its logarithm has the exponential formal power series representation (

11) whose coefficients

are the formal cumulants of

in (

19). From (

17), the sequence

will give an approximation of the cumulant sequence

for the range of parameters such that the asymptotic expression (

9) holds. In particular, an approximation of the mean of

T is given in Corollary 1.

To this aim, let us start by proving that with This result is given in Lemma 1 where denotes the unsigned Stirling numbers of first type and denotes the integer part of

Lemma 1. As exponential formal power series in the hypergeometric series has the following representationwhereandwith Proof of Lemma 1. To recover the expansion of

as formal power series in

we need to express both

and

in powers of

To this aim, recall that

where

are unsigned Stirling numbers of the first type. Similarly,

By expanding the binomial

and grouping with respect to the powers of

the rising factorial

can be rewritten as

Note that both

and

are polynomials of degree

n in

a and, after some algebra, their product gives the following polynomial of degree

in

a

with the coefficients

given in (

22). Note that

as

and

Therefore, plugging (

27) in (

23), an expansion of

in terms of powers of

a is

The expression of

given in (

20) follows after some algebra, exchanging the two summations in (

28). □

From Lemma 1, we have

since

in (

19) is the ratio of two formal power series in

In the following theorem, we first show that

then we expand

as given in (

11) in order to get a closed form formula of its formal cumulants

Theorem 1. The formal cumulants of in (19) are such thatwhere for we havewith the k-th logarithmic polynomial (13),with given in (20), the partial exponential Bell polynomials given in (14) and Proof of Theorem 1. From Lemma 1, we have

for

Since

let us first expand

a in (

19) as exponential formal power series in

Recalling that [

39]

from (

5) and (

18) we have

with

Thus

a has the following formal power series representation in

z, namely

By using (

36), the next step is to compute the coefficients of

as exponential formal power series in

This follows by observing that

as given in (20) results to be the composition of the two exponential formal power series

with coefficients given respectively in (

20) and (

36). Applying the Faà di Bruno’s formula (

16), we get

where

and

are the partial exponential Bell polynomials (

14). From (

11) we recover

where

are given in (

30). Thus the formal cumulants

in (

29) are obtained by observing that

using (

39) with

A replaced respectively by

and

and using the linearity property of formal power series. Finally,

given in (

38) can be further simplified as follows. Observe that from (

36)

and

given in (

32). By recalling a well-known property of Bell’s polynomials (see for instance [

40] page 146), we have

Thus, Equation (

31) follows from (

38) using (

41). □

As corollary, an approximation of the

k-th FPT cumulant

for

is

such that

with

the

k-th formal cumulant as given in Theorem 1.

Corollary 1. For the mean FPT of T is approximated by Proof of Corollary 1. The first formal cumulant of

in (

19)

where from (

31)

and from (

22)

Since

then

and the thesis follows.

Remark 2. The approximation of the mean FPT can be rewritten in terms of generalized hypergeometric functions as follows: Corollary 2. For the FPT variance is approximated bywherewith Proof of Corollary 2. The second formal cumulant of

in (

19) is

with

given in (

31) for

Thus (

50) follows from (

53) taking into account that

Recall that

has been given in (

45), from which (

51) follows with

as given in (

52). From (

31), we have

since

from (

32) and

As in the proof of Corollary 1, we have

Observe that

and

where

are the generalized harmonic numbers. Therefore from (

58) we have

Replacing (

58) and (

55) in (

54), after some algebra the result follows. □

4. Applications

In this section we consider two case studies coming from different areas of research to show how the problem of the FPT for the IGBM can arise in applied mathematical modeling and how the proposed methodology can be implemented. We limit to the case of the first moment of

T mainly for two reasons. The first one is that in this case, we can compare our results with the one existing in the literature. The second one is that this case is simpler from a numerical point of view and the main scope of the present paper is to propose a mathematical approach rather than perform a complete study of the computational properties of the numerical routine. However, we stress that cumulants of any order can be evaluated numerically by implementing a symbolic–numeric procedure using the

package

[

41]. Indeed the computation of the

k-th formal cumulant

in (

30) involves the computation of the

k-th logarithmic polynomial (

13), which is a special case of the general partition polynomial (

16). The routine

in the package

generates general partition polynomials. Thus the

k-th logarithmic polynomial as given in (

30) can be recovered by using the routine

in the package

with

where

and

are given in (

31) and (

18) respectively. The computation of

in (

59) can be traced back to general partition polynomials by setting

with

and

given in (

32) and (

21) respectively. As

is the sum of a numerical series, we have performed its computation by truncating the contribution of the remainder term when smaller of a fixed tolerance.

4.1. Stochastic Neuronal Model with Inhibitory Reversal Potential

Stochastic diffusion processes have been extensively used to model the evolution in time of the potential across the membrane of neuronal cells [

42]. They describe the changes in the membrane depolarization between two consecutive neuronal spikes. The reason why they are so important is that it is generally agreed that neurons transmit information about their synaptic inputs through these spikes. A spike occurs if the membrane voltage reaches a certain threshold value. From a mathematical point of view, this dynamics is studied by solving the related first-passage-time problem [

43]. The classical leaky integrate-and-fire model is described by a linear stochastic differential equation of Ornstein–Uhlenbeck type. However several modifications of the model were proposed to include more realistic features like the state-dependence of the the changes in depolarization and to avoid unrealistic properties like the unlimited state space of the process [

19,

20,

21,

22]. These alternative diffusion models maintain the linear drift while the additive noise is replaced by a multiplicative one. Among these diffusion processes, also the IGBM was proposed as a model of the neuronal activity to include the presence of an inhibitory reversal potential

[

23,

44].

The IGBM leaky integrate-and-fire model is described by an Itô stochastic differential equation of the following type

where

characterizes the synaptic input,

is called membrane time constant and takes into account the spontaneous voltage decay towards the resting potential (assumed equal to zero here) in the absence of input,

is a standard Wiener process and

is the starting depolarization. The diffusion coefficient

, where

represents the inhibitory reversal potential, determines the amplitude of the noise and guarantees at the same time that the changes in the membrane potential are smaller if

approaches

.

It is assumed that neurons express information about their input mainly by means of the average frequency of spikes described usually by the reciprocal value of the interval between consecutive spikes [

24,

45]. For this reason, the study of the first moment of the FPT is of primary importance.

The range of parameters such that the proposed asymptotic approximation (

43) holds can be interpreted in the neuronal modeling context as the presence of a strong excitatory input. This intuition is confirmed in the following figures where we plot the mean FPT for increasing values of

.

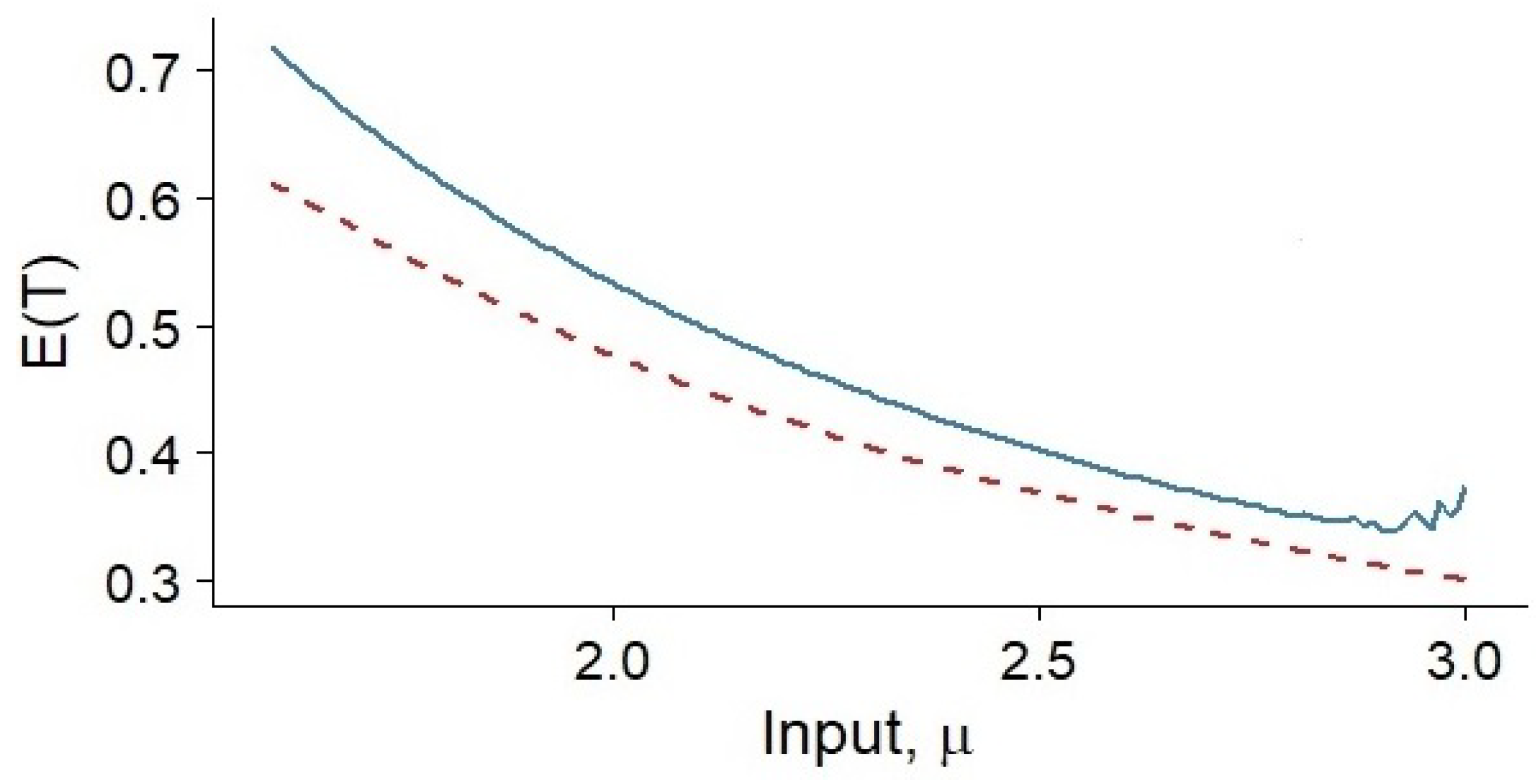

In

Figure 1 we compare the mean FPT of the IGBM process obtained with the asymptotic expression (

43) (red dashed line) and that given by the exact expression (

6) (blue solid line) for

,

,

,

,

.

We note that the proposed approximation slightly underestimates the value of

, but the agreement of the two curves improves for larger

. Moreover for values of

corresponding to strong external inputs the exact expression (

6) is unstable, while the approximation is not.

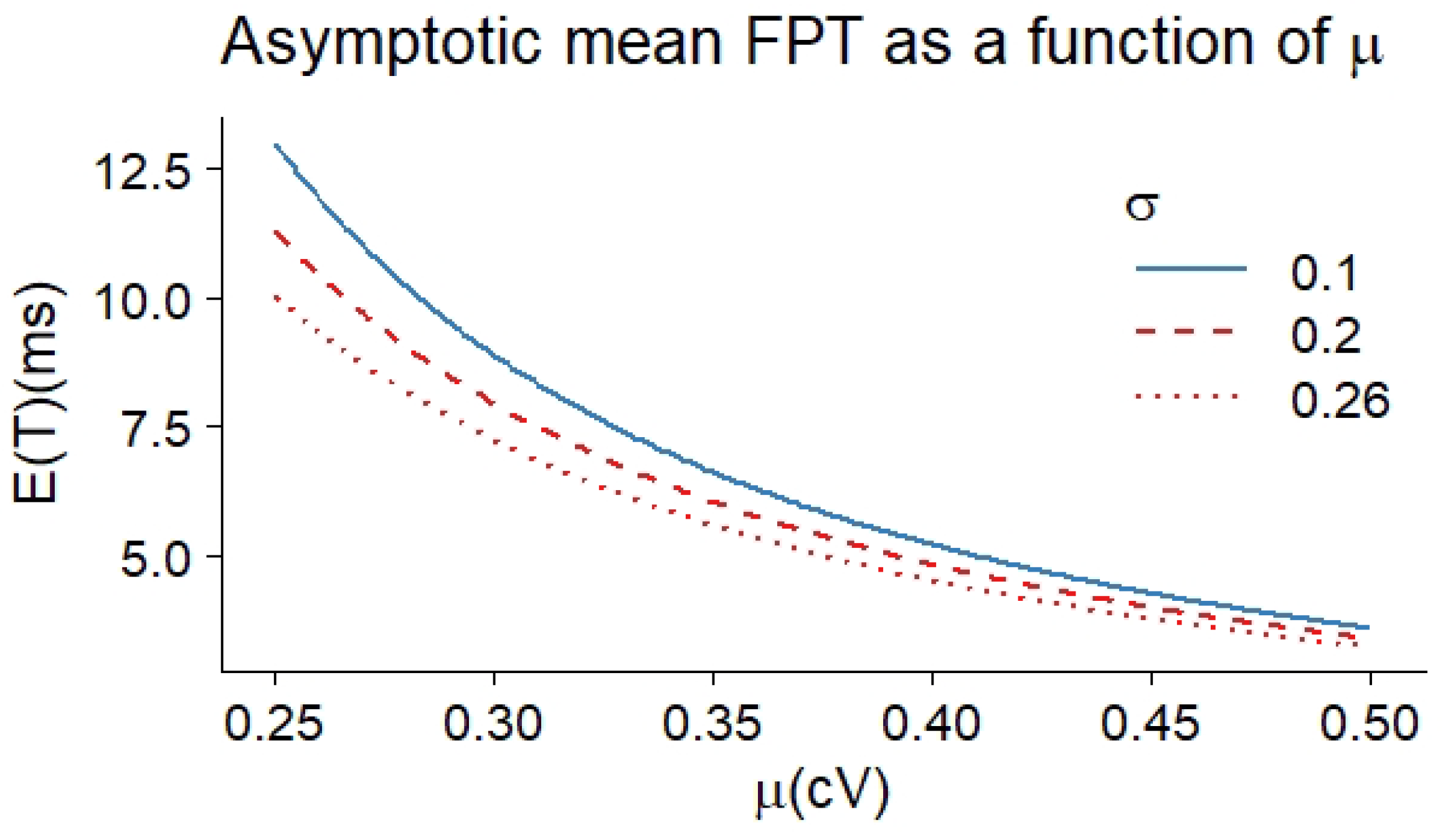

In the following, we consider physiologically realistic parameter values as suggested in [

19] and [

46], with their unit measures. The resetting potential is chosen equal to zero, i.e.,

mV, the inhibitory reversal potential is

mV, and the firing threshold

mV. The parameter of spontaneous decay towards the resting potential is chosen

ms.

To check how sensitive is the asymptotic expression (

43) to a change in

or

, we show the mean FPT as functions of the input for three different values of the noise amplitude in

Figure 2.

As expected the mean waiting time before the first spike decreases as increases. Moreover, for fixed , the mean FPT decreases for increasing (see the plot from the top downwards).

The measure units of the neuronal membrane potential are usually expressed in millivolt, while here we use centivolt. It is just a simple rescale of the SDE (

60) and does not affect the dynamics. The change of variable is used here as a numerical trick. In fact the series (

43) is more computationally stable for small parameter

.

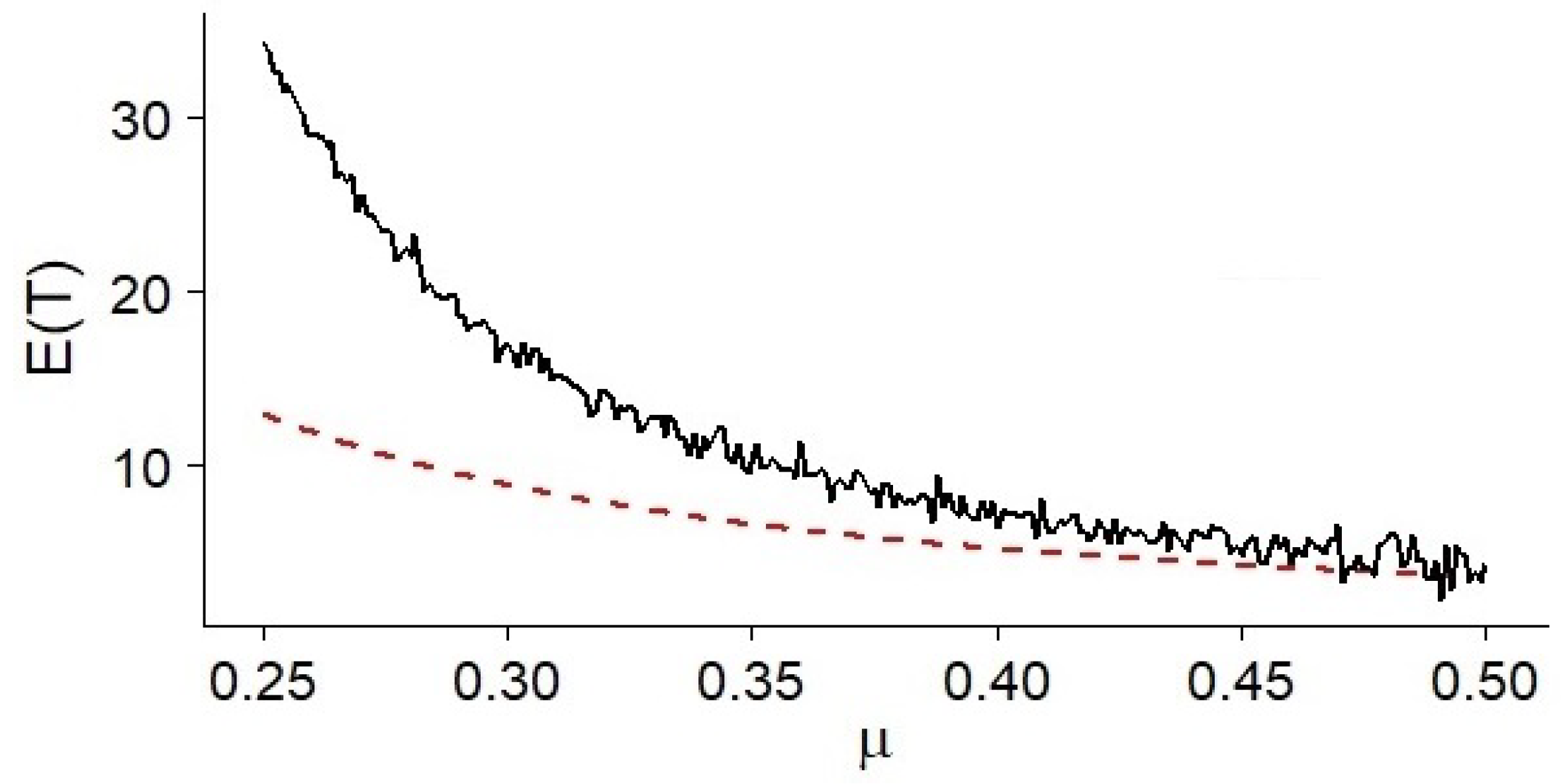

Finally, we observe that for the same computational accuracy, although non-optimal for small values of

, the approximated expression (

43) is way more stable than the exact expression (

6). For instance, in

Figure 3 we compare the mean FPT obtained via the two formulas for

ms

and other parameters as in

Figure 2.

Using the software environment R, for equal time and accuracy of the computation we observe that the asymptotic expression (

43), for

sufficiently large, is a more reliable tool for a numerical study of the firing rate.

4.2. Mean Reversion Models of Financial Markets

Mean reverting stochastic processes are often used in models of financial markets (see for instance [

3,

4,

5,

8,

10,

11,

15,

28]). The mean reversion property implies that the process tends to drive the short rate value towards the long term average level favoring upward (downward) movements if the short rate is too low (high). Among these processes the IGBM plays a relevant role: as GARCH diffusion process or Brennan and Schwartz model it is adopted to describe the value of real options, to study interest rates and to describe the underlying asset in the study of option prices in stochastic volatility models.

Here we want to investigate the sensitivity of the approximated mean FPT to a change in the threshold value S and in the instantaneous volatility . To avoid cumbersome calculations involving derivatives of hypergeometric functions with respect to the parameters, we display the main features of the approximated FPT through figures, using realistic parameters coming from the option-pricing literature.

We consider the model described by the following stochastic differential equation

where

represents the long-run mean,

is the instantaneous volatility,

is a standard Wiener process and

is related to the speed of reversion towards the mean level. If

is large, on average it takes less time for the process to move around the long-run mean and more time to move towards points far from it, i.e., more likely the process will not move far away from the long-run mean level.

In the following, we consider realistic parameters values as suggested in [

15] for Perpetual American Put Options:

,

,

,

.

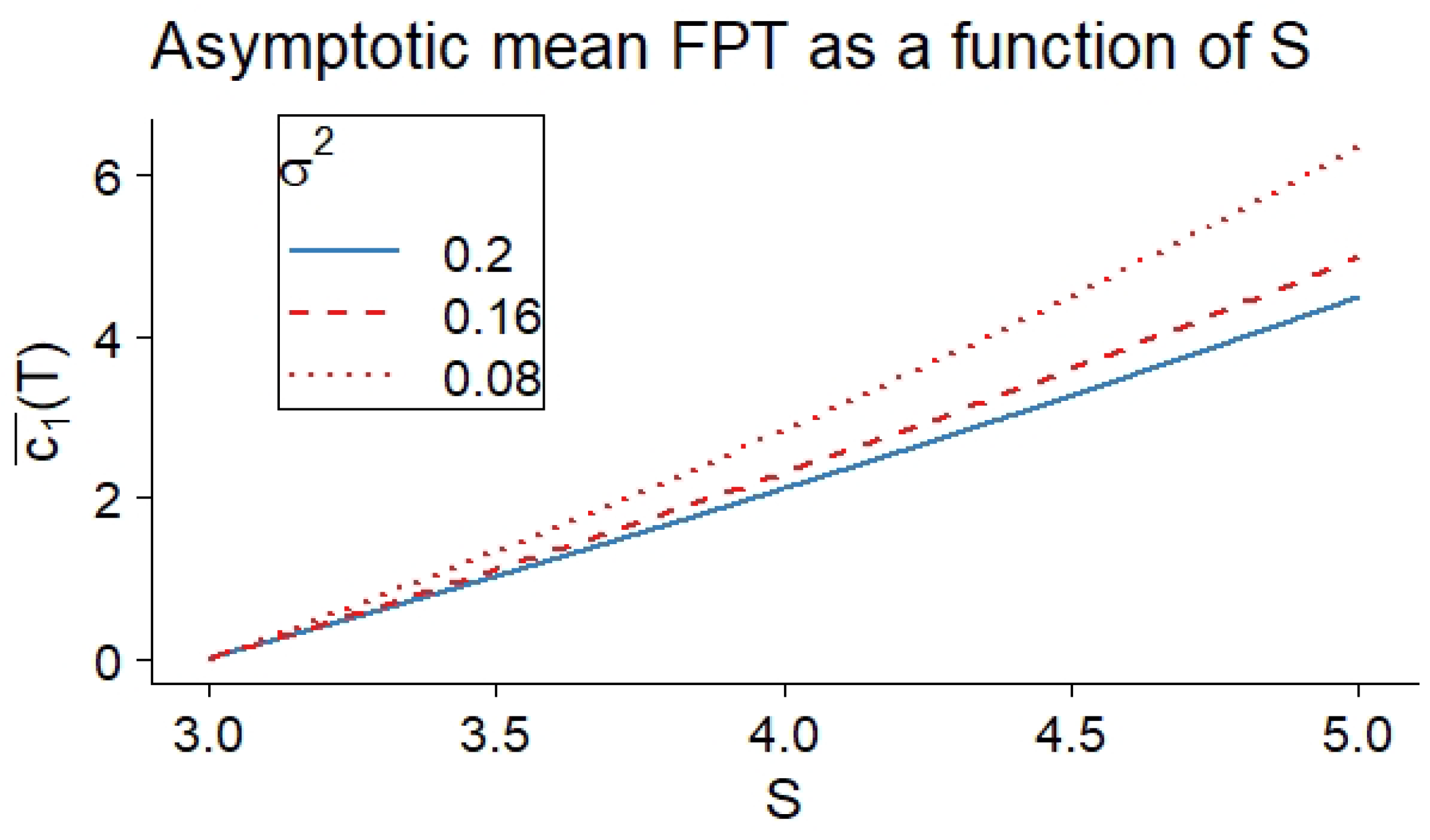

In

Figure 4 we show for

in Equation (

61) the asymptotic first FPT cumulant given by Equation (

43) as a function of

S. The mean FPT for

is equal to zero being, in this case,

, whereas, as expected, the mean time before the first crossing of

S increases if the threshold moves away from

. Moreover, we observe that the mean FPT decreases for increasing values of the instantaneous volatility

. In particular, if the long-run mean level is below

S and

is large,

is the main factor that can favor the threshold crossing.

In

Table 1 we show the relative error

between the asymptotic expression (43) and the mean FPT given by (

6) in the case

for five different choices of

S. We observe that the asymptotic approximation underestimates slightly the waiting time before the first crossing. The error increases with

S, although the relative error grows slowly. We note that the error is smaller for

S close to

. The reason is that our approximation performs better for

,

condition that, for fixed

, is better fulfilled if

.

4.3. Conclusions and Open Problems

We addressed the problem of the first passage time

T of the IGBM through a constant threshold, giving approximations of the cumulants of

T of any order obtained from an asymptotic expansion of the Laplace transform of

T using the algebra of formal power series. Moreover from the expression of the cumulants,

, moments of

T might be computed by using the recursion formula

We have shown that the approximations work better if the IGBM has a large positive drift or if the starting position of the dynamics is close to the threshold. Due to the lack of results in the literature about moments of

T of order higher than 1, even though they hold only in a certain parameters range the cumulants approximations constitute a novel result and a step forward in the comprehension of the FPT problem for this diffusion process. The first two approximated cumulants are given explicitly in Corollaries 1 and 2. The higher-order cumulants can be obtained from Theorem 1 analytically or by means of the

symbolic-numeric procedure sketched at the beginning of

Section 4 and based on the package

We stress that the computational cost of this procedure is lighter than the one for the classical approach with the integro-differential equations, although a more in-depth numerical analysis should be carried out.

These results can be used in many applications ranging from neuronal modeling with reversal potential to mean reversion models of financial markets both for understanding the underlying dynamics of extreme events and possibly for the simultaneous estimation of parameters involved in the model. The examples we have given show that this approximation works better when is large or is close to

These last observations suggest using the cumulants (

29) and the Laguerre-Gamma polynomial approximation proposed in [

18] to get an estimation of the FPT pdf

for the range of parameters for which expression (

9) holds. For large

the asymptotic results from [

47] can be applied to obtain information on

. Instead, for small-time

the approximation obtained through the expansion with Laguerre–Gamma polynomials and the cumulants (

29) should result to be competitive when compared with the Monte Carlo methods and when traced back to

large or

close to

Indeed, the classical simulation schemes like Euler–Maruyama or Milstein method often provide uncorrected values of

around zero and so the approximation of

for small

t turns out to be particularly relevant. This is on the agenda of our future research.

As the last remark, we stress that the methodology itself is not limited to the IGBM. As future work, we plan to extend this approach to other processes belonging to the class of Pearson’s diffusions, since the expression of the Laplace transform of the FPT pdf for these processes is often written as a ratio of two hypergeometric functions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}