1. Introduction

There is no doubt about the achievements of China’s rapid economic development. The structure of China’s real economy has shifted from labor intensive to capital and technology intensive [

1]. If China wants to realize the sustainable development of the real economy, it is necessary to improve economic and allocation efficiency [

2]. The optimization and upgrading of the structure of China’s real economy is the only way to do this. Under certain conditions, financial development promotes economic growth. However, it cannot promote the upgrading of the structure of the real economy and realize the long-term development of the real economy if it only relies on the growth of the finance scale [

3]. Financial development is a broad concept. From the perspective of capital value and credit, the finance structure of a country reflects its economic structure. Therefore, the exploration of ways for financial development to promote the development of real economy must also start with the finance structure [

4]. Exploring how the finance structure affects the optimization of the structure of the real economy is the key to improving the development potential of the real economy [

5].

Finance can promote the development of the real economy and the upgrading of the structure of the real economy. This process raises several questions: What contribution does the transformation of the finance structure make to the real economy [

6]? How is the relationship between finance and real economy coordinated to promote the optimal growth of real economy [

7]? Does the effect of the expansion of finance scale and the change of finance structure on the real economy always promote its long-term development [

8]? What are the characteristics of the effects [

9,

10]? In order to explore these problems, this paper mainly refers to the research results of finance structure and economic structure; finance structure and economic growth; and then discusses the relationship between finance structure and real economy. There are a lot of academic results on finance and economic growth [

11], and finance and economic structure, but relatively few results on the relationship between finance structure and real economy.

The core goal of financial development is service economy, and the studies of finance structure ultimately follow this goal. In accordance with the optimal finance structure theory, scholars have carried out a multi-faceted exploration. A review of relevant literature shows that some scholars support the financial market-led finance structure [

12,

13,

14,

15], and some scholars support the bank-led finance structure [

16,

17,

18,

19]. Some scholars believe that a sound financial market environment and perfect laws and regulations are the premise for finance to play an effective role [

20,

21,

22,

23,

24,

25,

26]. Some scholars focus on the impact of digital finance on economic growth [

27,

28], some on the impact of financial intermediation on the real sector [

29], and some on the impact of different financial sectors on the economy [

30,

31]. Ergungor [

8] found that there is a nonlinear (contingent) relationship between growth and financial structure using a two-stage regression model, and countries that have an inflexible judicial system grow faster when they have a more bank-oriented financial system. Many scholars have also studied the interaction between financial models and the macro economy [

32].

Many scholars studied how the transformation and diversity of financial structure would affect the economy [

33]. Deidda and Fattouh [

3] suggest that both bank and stock market development have a positive effect on growth, and the change from a bank-based system to one in which market finance and bank finance coexist might have an adverse effect on economic growth. Milberg [

34] discusses the impact of finance on real economy from the perspective of financial crisis, and how the financialization of enterprises has changed the relation between stock prices and innovation, with adverse consequences for the growth of economies. Mazzucato [

4] argues for the return of finance to serve the real economy, and that it is fundamental to de-financialize companies in the real economy and think clearly how to structure finance. Polzin [

5] proposes that higher diversity and resilience in financial markets is complementary and perhaps even instrumental to engineer the transition of the real economy. Structural matching between finance and the real economy can promote economic growth [

6,

7,

35,

36]. Economic transformation is also inseparable from economic development. Many scholars have studied the relationship between economic structure and economic development. Saviotti [

37,

38] argues that structural change is not considered an epiphenomenon of economic development but one of its fundamental mechanisms. Freire [

39] concluded that economic diversification, such as structural transformation, is relevant for poorer developing countries to foster economic development. There are more complex potential links between sectoral production structure and sustainable development [

36,

40,

41].

Different countries have different financial systems, so the study of finance structure should be combined with the corresponding characteristics of a country, such as resource endowment and financial system [

42,

43,

44]. Tadesse [

45] examines the relation between the architecture of an economy’s financial system and economic performance in the real sector and finds that different types of economies behave differently, and that the proper financial system itself may be a source of value. Karwowski [

46] believes that market-based financial systems are more financialized, and financialization plays out differently across economic sectors and countries. A large number of studies have shown that there are national differences in the relationship between finance structure and economic growth [

12,

47,

48,

49], so it is necessary to conduct a special study on China’s situation. There are other scholars who examine the role of different financial systems at different economic stages. Some scholars contribute to the literature on financial system design by comparing markets and banks in a dynamic economy using a dynamic panel framework [

46,

47]. Some review the relationship between finance and growth considering its non-linear impact and discuss the impact on growth in mature financial systems [

50,

51]. There is also a view that literature has exaggerated the size of the finance growth effect in the past, and points to a positive but decreasing effect of financial development on growth and supports the hypothesis of financial supportive excess [

52].

At present, studies begin to describe the dynamic relationship between finance and economy, using the dynamic panel model [

10,

48], ARDL bounds testing approach [

53], cross-country growth regression [

47], CoVaR approach [

24], and TVPSS [

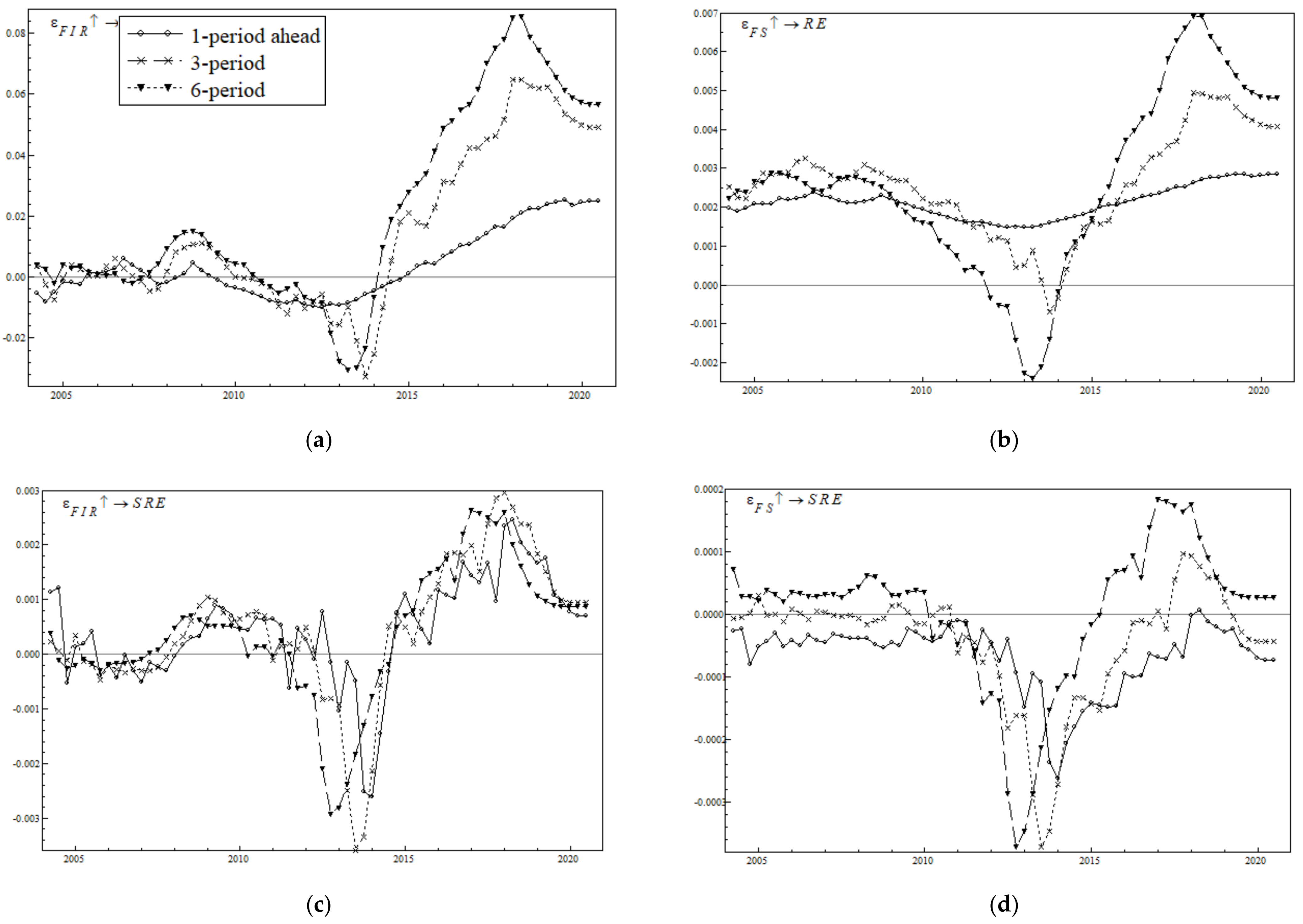

54], etc. In view of this, this paper summarizes the research results and methods used by scholars, and then further analyzes and characterizes the time-varying characteristics of the dynamic influence of finance structure on the scale and structure of real economy. The contribution of this paper is mainly embodied in: Firstly, the finance structure index is constructed to analyze and describe the evolution and characteristics of China’s finance structure in recent years. Then, the time-varying parameter-vector autoregression model (TVP-VAR) is constructed to describe the time-varying characteristics of the impact of finance structure on the scale and structure dynamics of the real economy. Because the impact of the finance scale on the real economy cannot be ignored, this paper also takes the finance scale as an influence variable into the model for empirical analysis. It is verified that the optimization of finance structure in China has different effects on the scale and structure of the real economy, and the dynamic impact presents significant time-varying characteristics, and the finance scale also has similar conclusions. The empirical results also show that the impact amplitude of the finance structure on the real economy is in a relatively unstable state. Accordingly, some suggestions are put forward for the current financial market [

24,

27], finance environment [

4], and financial regulatory system [

8] in China.

2. Theoretical Basis and Transmission Mechanism

In essence, the scale growth and structural upgrading of the real economy refer to the process of the optimized allocation of economic resources within the real economy, and the flow of production factors such as labor, capital and technology among different industries and departments within the real economy, resulting in changes in the output structure of the real economy [

55,

56]. This reallocation of resources is reflected in the transfer and flow of funds and personnel.

In the current financial economy, the financial sector can realize the dynamic allocation of capital among different industrial sectors. Optimizing capital allocation and improving the flow efficiency to serve the real economy are the functions and objectives of the multi-level financial market. The transmission mechanism of the financial sector to promote the development of the real economy and optimize the structure of the real economy is complex, and can be divided into the following two stages.

The first stage is when the real economy is in the factor-driven stage. The economy is just starting, and all sectors of the real economy are short of funds. Financial development can improve the efficiency of capital flows and accelerate the accumulation of capital. The expansion of the financial sector can offer more funds for the real economy, which promotes the expansion of various sectors of real economy [

57], attracting more inflows of production factors such as capital, labor and technology, which will further promote industrial upgrading and expansion, forming a virtuous circle.

The second stage is the efficiency-driven stage. With the development of the real economy, economy has gradually shifted from the factor-driven stage to the efficiency-driven stage, and even gradually to the innovation-driven stage [

13,

15]. At these stages, capital is no longer the core factor of production, and innovation and research play a more critical driving role. The driving factors of the development of the real economy have changed, and the development of each industrial sector needs to improve its capacity of technological research and development and innovation level, which inevitably requires a multi-level financial supply and higher efficiency of capital allocation. At this stage, if the financial sector pursues scale expansion without paying attention to the development of diversified financial products to improve the quality of financial services and improve the efficiency of capital allocation, it will worsen the pattern of capital allocation and hinder the flow of financial resources to innovative industries with high added value, thus slowing down the upgrading of structure and the benign expansion of the real economy [

58].

For second-stage economies, the real sector can be better served by a financial system that is appropriate to the stage of economy. First, the reasonably widespread scale of finance can provide the necessary financial resources, such as funds for the real economy, to ensure that the real economy can further pursue the improvement of its capacity of research, development and innovation levels [

59]. Second, the optimization of finance structure, for example, a variety of financial instruments, multi-channel financing sources, high coverage of branches of financial institutions, and financial services with high quality, can speed up financing and improve financing efficiency. The flexible and efficient operation of the financial system can increase the speed of capital flows and alleviate the shortage of funds for the rapid development of the real economy [

60]. Moreover, the optimization of finance structure can also attract more financial resources. The emergence of diversified new financial instruments or products can meet the investment needs of different investors, attractring more idle funds to flow into the real sector through the financial sector [

61]. Third, the upgrading of finance structure can influence the financing structure of different sectors and change the efficiency with which savings are converted into investments. Each sector of the real economy can choose the appropriate financing channels or methods based on its own needs, promoting the efficient allocation of capital from low to high value-added sectors to realize the restructuring and upgrading of the real economy. The financial system that does not match the real economy is mainly manifested as an insufficient scale of finance or an excessive structural transformation, which leads to financial restraint or financial bubbles. It’s not only detrimental to the deepening of financial sector, but also to the long-term development of the real economy and the optimization of its structure [

62,

63].

3. Construction of Finance Structure Index

This section describes the construction method of China’s financial structure index, data sources and processing, and analyzes the calculation results.

3.1. Index Setting

In recent years, there has been more research on the impact of finance structure on real economy or industry, and many scholars have constructed the finance structure index conforming to China’s financial system [

6,

9,

54,

63,

64]. This paper chooses the comprehensive index method [

65] to construct the finance structure index, which can choose the indicators highly related to the finance structure, so as to better describe the current structure of China’s financial system. The model is as follows:

where FS

t is the finance structure index at time t, Y

it is the ith index at time t, and

is the weight.

Based on the above analysis of the financial structure and the current situation of China’s financial system, this paper selects the basic indicators to measure the finance structure from three aspects. First, there is measuring the ability of operational efficiency of the financial sector, such as the loan-to-deposit ratio of financial institutions and the ratio of non-non-performing loans of commercial banks. The loan-to-deposit ratio of financial institutions refers to the lending capacity of Chinese financial institutions, as measured by the ratio of the outstanding loans of financial institutions to the outstanding deposits at that point in time [

62,

66]. The non-non-performing loan ratio of commercial banks evaluates the quality of loans issued by financial institutions on the whole and measures the current investment, financing and credit environment in China. The calculation method is the proportion of non-non-performing loans of financial institutions in the total loan balance [

67]. Second, there is the financing structure of the real economy, such as the structure of the financing tool, source and channel. The structure of the financing tool measures the ratio of stocks or bonds that an enterprise chooses to issue when financing directly from the financial market [

55]. The structure of the financing channel measures the choice of direct financing through the financial market or indirect financing through bank loans [

68]. The structure of the financing source refers to the source of funds, as measured by the ratio of the total market value of B-shares in foreign currency to A-shares in RMB [

62]. Third, there is the structure of each financial industry in the financial system, such as the dispersity of banking industry, structure of the securities market and the insurance market. The dispersity of banking industry measures the development of small- and medium-sized commercial banks in China and is calculated by the ratio of the total assets of non-large commercial banks to the total assets of the banking industry [

64]. The structure of the securities market measures the development of the Small and Medium Enterprise (SMEs) Board, Growth Enterprise Market (GEM) Board and New OTC (Over-the-Counter) Market in China by the ratio of their market value to the Main Board Market [

66]. The insurance structure measures the development of China’s insurance industry, calculated by the ratio of premium revenue to total financial assets [

66].

The basic indicators of finance structure in this paper are shown in

Table 1. The data period is from the first quarter of 2004 to the third quarter of 2020, mainly reflecting the structure of China’s financial system. Data were obtained from China Banking and Insurance Regulatory Commission, National Bureau of Statistics of China and Wind database.

In order to eliminate the influence brought on by dimension, this paper selects the averaging method to perform dimensionless processing of the original data of each index, that is, data standardization. It is assumed that the value of the ith basic index of the finance structure index system at time t is X

it, the data is averaged according to Equation (2), and Y

it is the standardized index data:

The weight of each index is calculated by the entropy evaluation method [

62]. The entropy method calculates the weight of each index by using the degree of difference within each index value and determines its weight according to the correlation degree and importance of each index, which can effectively avoid the deviation caused by subjective factors. The detailed steps for calculating index weight by using the entropy evaluation method are as follows.

First, change the specific gravity of the index:

where Y

it is value of the ith standardized index of the finance structure index system at time t, i = 1, 2, …, n, t = 1, 2, …, T.

Second, calculate the entropy of each index:

Third, calculate the difference coefficient of the entropy value of each index. For the ith index, the greater the difference of index value Y

it, the greater the effect on scheme evaluation, and the smaller the entropy value:

Fourth, determine the entropy weight of each indicator. The smaller the entropy value of ith index is, the more orderly the sample data of ith index will be, the greater the difference between the sample data will be, the greater the ability to distinguish the evaluation object will be, and the corresponding weight will be larger:

3.2. Descriptive Analysis of the Finance Structure Index

Using the entropy weighting method, the weight of each index can be obtained (see

Table 2). The structure of the financial sector has the highest weight in the finance structure index system, with a specific gravity of 0.49. This suggests that changes to various industries in the financial sector have the greatest impact on the finance structure, especially the weight of the structure of the securities market, which is 0.33, the highest weight of any secondary grade index. It shows that the structure of the securities market in China has the greatest influence on the finance structure. The establishment and development of Small and Medium Enterprise (SMEs) Board, Growth Enterprise Market (GEM) Board and the New OTC (Over-the-Counter) Market have had a significant impact on China’s finance structure and promoted the optimization and upgrading of China’s finance system.

Second, the importance of the financing structure of the real economy to obtain funds from the financial system is a middle value, reaching 0.39, among which the structure of financing tools accounts for a high proportion, mainly because China’s securities market is gradually maturing and more enterprises choose to issue stocks or bonds and other direct financing methods.

Third, the efficiency factor has the lowest importance in the finance structure index system, indicating that the efficiency of China’s financial system is low which is mainly due to the impact of the loan-to-deposit ratio of financial institutions. The non-non-performing loan ratio of commercial banks has the smallest weight among all the secondary indicators.

China’s finance structure index from the first quarter of 2004 to the third quarter of 2020 are shown in

Table 3. According to the principle of the entropy weighting method, the more orderly the sample data of the index is, the stronger the ability to distinguish the samples will be, so the corresponding weight will be larger. In a complete index system, the weight of each index can be any value in [0, 1], and the sum of the weights of all indicators is 1. The following main results can be obtained.

In general, China’s finance structure index shows an upward trend. It was at a low level in the early stage, ranging from 0 to 0.3, and began to rise in the later stage, fluctuating around 0.5, indicating that the financial system has constantly improved while the financial scale has expanded since 2004, and the finance structure has been continuously optimized and upgraded. The financial system is gradually transitioning from structurally poor to structurally sound. The realization of better coordination and the transmission of resources between the financial sector and the real economy are conducive to the realization of the financial sector’s function of serving the real economy and optimizing resource allocation.

From 2004 to 2020, the evolution trend of China’s finance structure index is shown in

Figure 1. The evolution process can be divided into three stages. One is the fluctuation adjustment stage.

From 2004 to 2008, the finance structure index fluctuated significantly in the range of [0, 0.3], and was generally in a low range, which was related to China’s financial environment at that time. China’s financial openness was not high, and the financial system was far from perfect, which required constant adjustment to adapt to economic development. Second, there is the stable recovery stage.

From 2009 to 2014, the finance structure index was in a relatively stable stage with small fluctuations, and mainly showed a slow rising trend. Around 2008, China’s financial system was greatly influenced by the 2008 international financial crisis, and China’s finance structure index fluctuated greatly, with an overall significant decline. The development of the financial system slowed down, followed by a slow recovery in which adjustments were made to restore proper order to the financial markets. Third, there is the rapid development stage. Since 2015, the overall level of China’s financial environment has been greatly improved, and the finance structure index has risen rapidly, mainly due to the adjustment of the structure of securities industry. With the conversion system of SEMs to receive listing applications from enterprises nationwide, the New OTC Market has been gradually improved. China’s multi-tiered capital market system, including the Main board, GEM board, OTC trading network and property rights market, has been further improved, and China’s finance structure index has been significantly improved and maintained at a high range of [0.5, 0.6].

{kind=link}

{kind=link}

{kind=link}

{kind=link}