1. Introduction

The use of contracts to coordinate the supply chain is an important research field in the current supply chain management field. There are many types of supply chain contracts. A quantity discount contract is the most commonly used one, and it has many forms. The quantity discount contract in this paper refers to an agreement in which the unit wholesale price provided by the supplier is inversely proportional to the retailer’s order quantity. The contract is mainly used for small profits, but the quick turnover of industrial products or time-sensitive fresh agricultural and sideline products or seasonal clothing industries.

The initial research on the use of quantity discount contract to coordinate supply chains was mostly carried out on the premise of fixed market prices and a stable market external environment. Monahan [

1] took the lead in researching quantity discount contract. Cachon [

2] applied quantity discount contract to coordinate the simplest secondary supply chain. Huang et al. [

3] introduced quantity discount contracts to restrain retailers’ potential incentives to encourage returns. Sun et al. [

4] investigated the effectiveness of quantity discount contracts in slowing down the spread of bankruptcies among supply chain members. Ogier et al. [

5] proposed a batch model integrating quantity discounts for local planning problems. Kwong et al. [

6] used Stackelberg game theory to establish a joint optimization model of manufacturers and retailers considering quantity discount contracts.

The above studies are all about the benchmark quantity discount contract. Later scholars have conducted extensive research on the application of quantity discount contracts in practical problems. The research involves delayed payment, energy, trade credit, transportation, and so on. Yu et al. [

7] proposed a power supply chain coordination model based on quantity discount contracts. Sheen and Tsao [

8] considered the coordination of the quantity discount contract and delayed payment of the retailer’s transportation cost. Wang and Liu [

9] studied the role of trade credit and quantity discounts in supply chain coordination after considering the impact of sales efforts on market demand. Zhang et al. [

10] studied the use of quantity discount contracts to coordinate supply chains when there is a risk of trade credit default. Zhou and Kim [

11] proposed the optimal concession contract design method between the port authority and two container terminal operators under different quantity discount revenue sharing schemes. Zhang et al. [

12] discussed the issue of the multi-period newsvendor problem with stable demand and quantity discounts.

With gradual deepening of research, the scope of study gradually involves supply chain coordination issues under the circumstances of market demand fluctuations and changes in production costs. Peng et al. [

13] explored the quantity discount contract model of the fashion supply chain under uncertain income and random demand. Zhao et al. [

14] investigated the supply chain coordination problem of demand interruption in the fashion supply chain with revenue-sharing contract and linear quantity discount contract. Lee [

15] studied the quantity discount contract between the manufacturer and the retailer under a stochastic two-period inventory model. Most of the research mentioned above objects are the most straightforward secondary supply chains, and some scholars have studied more complex supply chains. Nie and Du [

16] discussed the quantity discount contract coordination mechanism in a binary supply chain composed of one supplier and two retailers. Huang et al. [

17] studied the quantity discount contract to coordinate a supply chain composed of a retailer and multiple suppliers. Zhang et al. [

18] considered the fixed life of the product and explored the coordination problem of a production-inventory integrated system with a quantity discount under the condition of limited productivity and deterministic demand. Zheng et al. [

19] considered the quantity discount contract of the new product supply chain composed of one supplier and multiple retailers under the two independent procurement and joint procurement cases.

After the 2008 financial crisis, scholars and business managers recognized the importance of supply chain risk management. Scholars have begun to study the problem of diversifying risks when participants are averse to risks due to emergencies under the premise of stable market prices. Agrawal and Seshadri [

20] proposed using quantity discount contracts to diversify the losses caused by risk-averse retailers. The research mentioned above mainly studies the methods of diversifying risks without quantitative estimation of risks. Later, many scholars introduced quantitative risk management methods in financial management into supply chain risk management. Liang et al. [

21] studied a supply chain system with a risk-neutral manufacturer as the leader and a risk-averse retailer as the follower based on the VaR (value-at-risk) method. Bai and Liu [

22] proposed a robust optimization method to solve the supply chain network design problem using the variable probability distribution through the fuzzy VaR modelling method. Rockfellar and Uryasev [

23,

24] proposed to use conditional value-at-risk (CVaR) as a risk measurement criterion for the limitations of VaR theory. As a result, CVaR has become a popular method for studying supply chain risk management. Tao et al. [

25] proposed a CVaR way to measure overdue penalties to incorporate decision-makers risk aversion. Chen et al. [

26] established an improved newsboy model with random default probability to reduce the default loss using CVaR as the measurement criterion.

Analyzing the literature shows that some consider the random changes in market prices caused by emergencies, but the supply chain participants remain risk-neutral. Some thought participants’ risk aversion caused by emergencies but did not consider the random fluctuations of market prices. The literature that considers multi-factor disturbances such as random changes in market prices and risk aversion among participants is still relatively rare. Therefore, this paper considers whether the supply chain can be effectively coordinated using quantity discount contracts under the simultaneous disturbance of multiple factors such as random market demand, random market prices, and supplier risk aversion.

In summary, the main contributions of this paper are as follows: (1) Analyze and revise the existing ‘profit-CVaR’ risk measure criteria. (2) Introduce stochastic price into the field of supply chain risk management and construct an emergency quantity discount contract model under multi-factor disturbance. (3) The phenomenon of bifurcation and mutation in supply chain coordination is discovered and analyzed.

The rest of the paper is structured as follows:

Section 2 constructs the benchmark quantity discount contract model, the emergency quantity discount contract model under the condition of price stability, and the emergency quantity discount contract model under the stochastic price. In

Section 3, the limitations of the existing “profit-CVaR” risk measure criteria are analysed, and relevant proofs are given. On this basis, an emergency quantity discount contract model under the condition of stochastic price and supplier risk aversion is further constructed.

Section 4 provides a specific numerical example and analyzes the results of the example in detail. The conclusion is given in

Section 5.

4. Numerical Example

Assuming that a company sells certain emergency supplies, the various parameters of the goods under the stable market conditions are:

,

,

,

,

,

(see the preceding text for the meaning of the above parameters). Suppose that the market demand under emergencies obeys the distributions

,

,

, and

respectively. Discuss the influence of the change of the risk aversion factor

in the interval

and

with 0.1 and 0.01 as the steps respectively on the optimal order quantity. See

Table 1 and

Table 2 for details. The impact of the risk aversion factor

in interval

with 0.001 as the step size on various decision variables in the supply chain is shown in

Figure 1,

Figure 2,

Figure 3,

Figure 4 and

Figure 5.

As can be seen from the data in

Table 1, when

changes in the interval of

with a step size of 0.1, the optimal order quantity under the risk aversion of the supplier is equal to the optimal order quantity under the risk neutrality of the participants regardless of the variance change. It shows that in this case, both risk aversion and variance have no effect on the performance of the supply chain, and the supply chain can achieve coordination.

It can be seen from

Table 2 that in the case of random prices and supplier risk aversion, when

changes in the interval

with a step length of 0.01, the optimal order quantity under different variances begins to change. When

is equal to 1, it is the same as the optimal order quantity in the risk-neutral case.

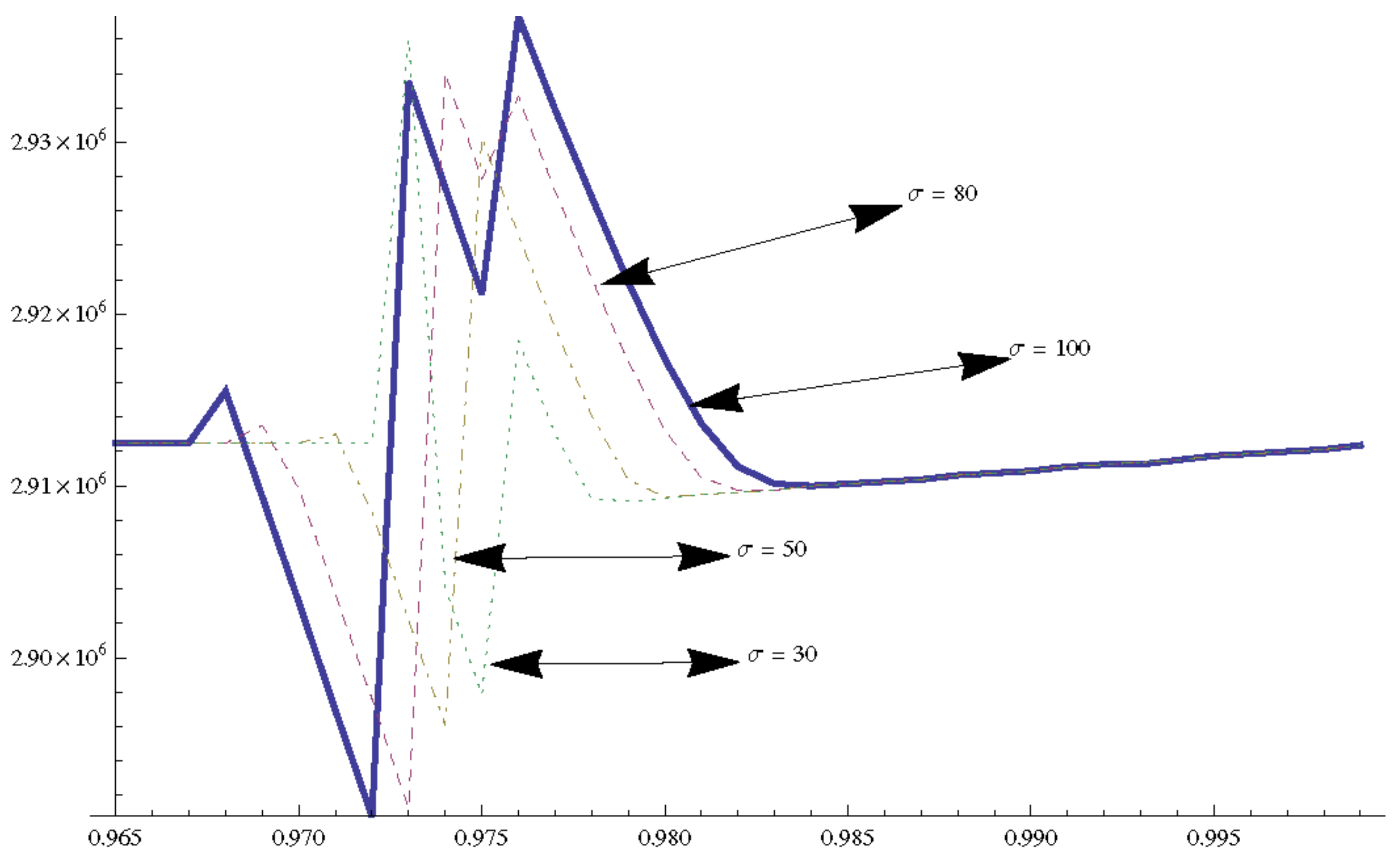

The

X-axis in

Figure 1,

Figure 2,

Figure 3,

Figure 4 and

Figure 5 represents the risk aversion factor, that is, the supplier’s risk aversion degree. The

Y-axis of

Figure 1,

Figure 2,

Figure 3,

Figure 4 and

Figure 5 respectively represent the optimal order quantity, retailer’s expected revenue, supplier’s expected revenue, supply chain’s expected revenue, and the value of “

”.

Figure 1 shows that when

and the risk aversion factor

, the retailer’s optimal order quantity begins to change and is no longer equal to 48,750. When

the optimal order quantity starts to change when

. When

and

, the optimal order quantity begins to change. When

, the optimal order quantity starts to change at

. From the above changes, it can be seen that the optimal order quantity under the coordination of the quantity discount contract will vary with the evolution of the risk aversion factor. However, when the risk aversion factor tends to 1, the optimal order quantity under different market demand distributions will gradually align with the optimal order quantity under risk-neutral conditions.

In addition, when , the optimal order quantity begins to show bifurcation mutation from , and the change interval of is . The value of is the smallest when and the largest when . When , the optimal order quantity begins to show a bifurcating mutation from , and the change interval of is , and the value of is the smallest when and the largest when . When , the optimal order quantity begins to show bifurcation mutation from , and the change interval of is , and the value of is the smallest when and the largest when . When , the optimal order quantity begins to show bifurcation mutation from , and the change interval of is , and the value of is the smallest when and the largest when .

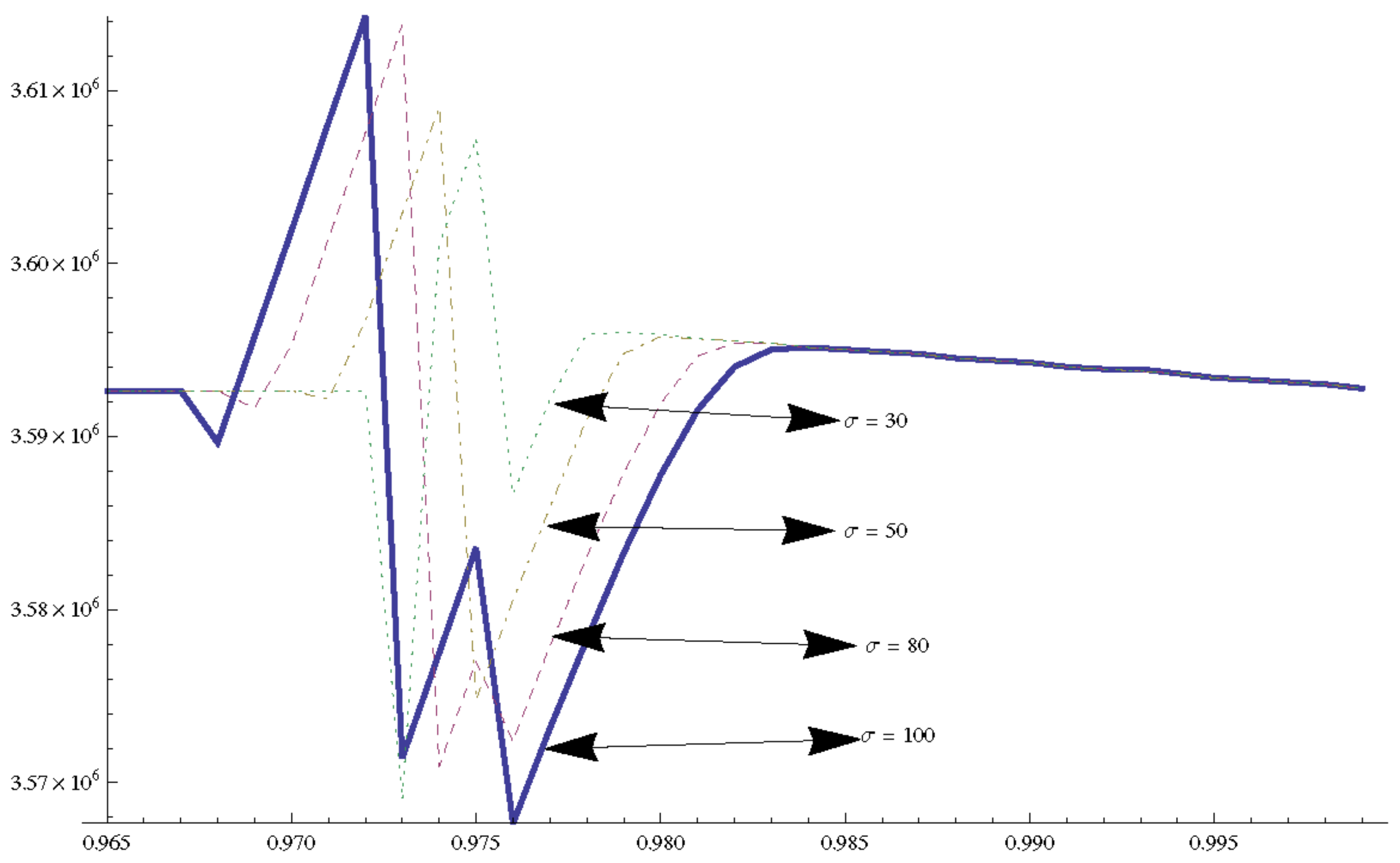

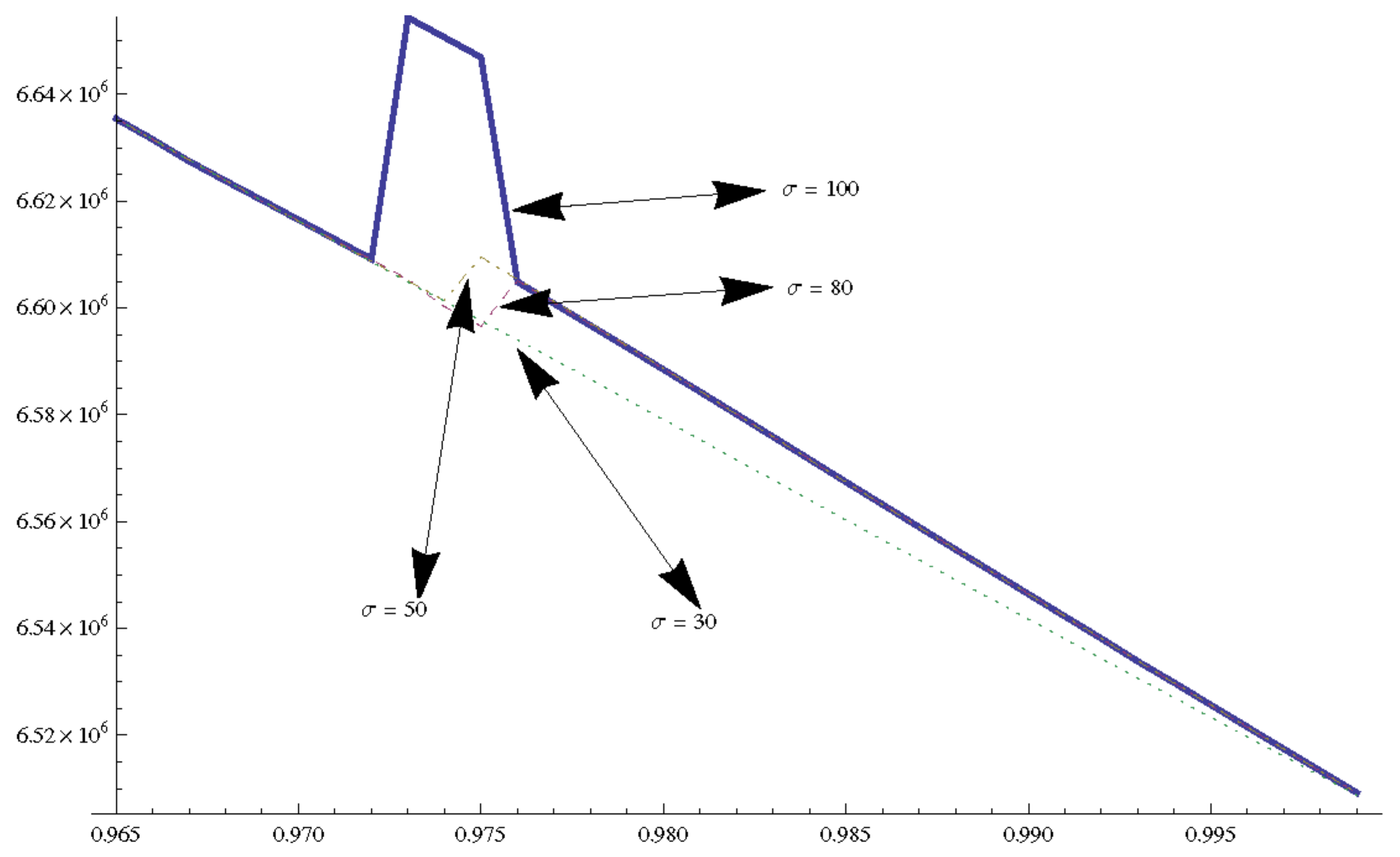

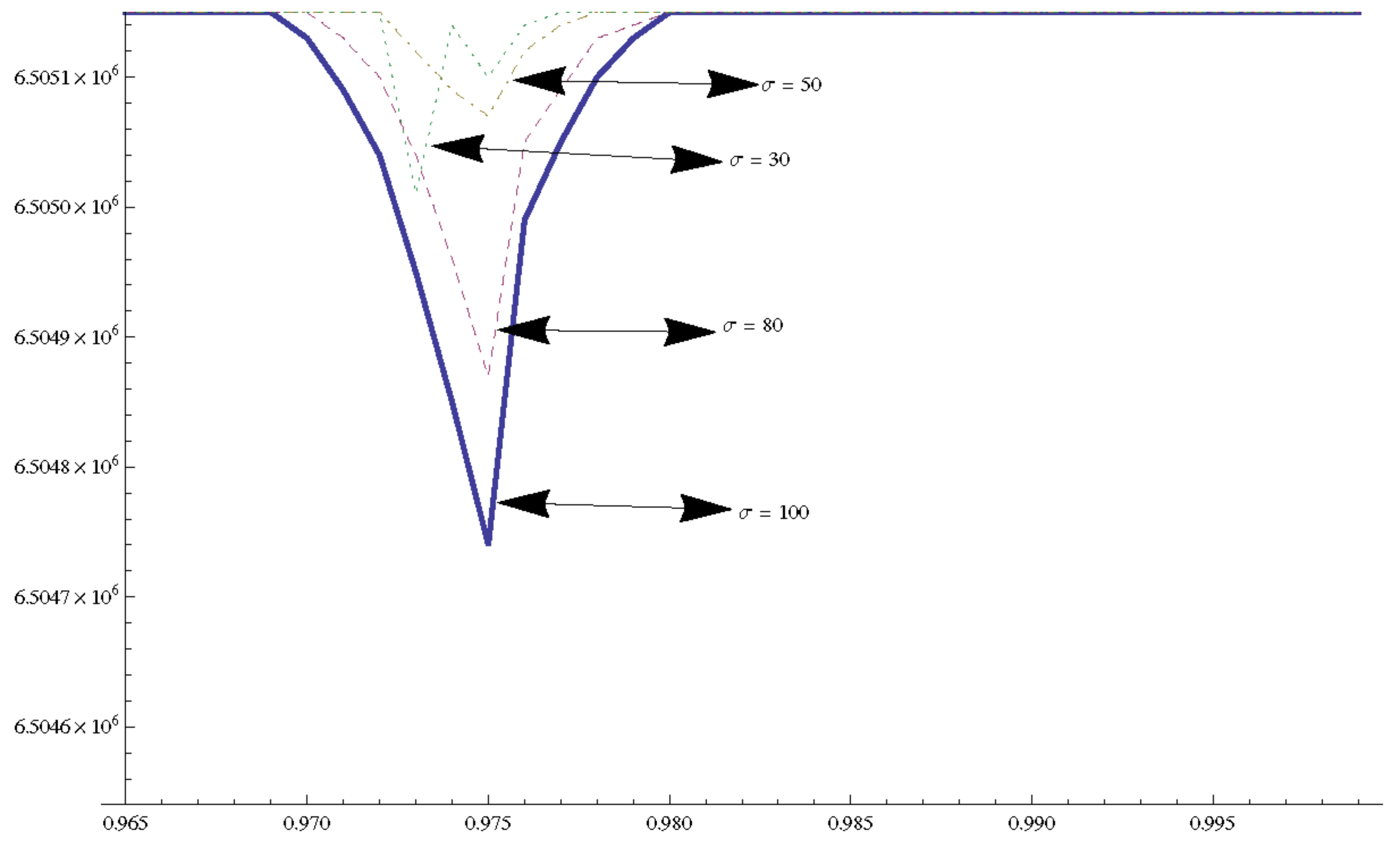

Similarly, the expected revenue of the retailer in

Figure 2, the expected revenue of the supplier in

Figure 3, and the expected revenue of the supply chain in

Figure 4 all have corresponding changes in the corresponding intervals.

Figure 1,

Figure 2,

Figure 3 and

Figure 4 show that in the bifurcation mutation interval when

is larger, the optimal order quantity, retailer’s expected revenue, supplier’s expected revenue, and the entire supply chain’s expected revenue will oscillate in a wider area, and the above-mentioned factors will oscillate up and down. On the other hand,

Figure 5 shows that the revised ‘Profit-CVaR’ chart shows no significant oscillations, indicating that the revised ‘Profit-CVaR’ is more stable as a risk measure criterion.

5. Conclusions

Under the premise of random market prices, an emergency quantity discount contract model of retailer’s risk neutrality and supplier’s risk aversion is constructed. This paper revises the existing risk measurement criteria, studies the coordination problem of the supply chain under the new risk measurement, and analyzes a numerical example. The following conclusions can be drawn after the analysis.

In the case of market price randomness and supplier risk aversion, the bifurcation and mutation phenomenon appears when the quantity discount contract is used to coordinate the supply chain. Supply chain coordination cannot be achieved in the region of bifurcation mutation, while supply chain coordination can be achieved outside the region of bifurcation mutation. Therefore, it can be seen that when suppliers are averse to risk, the managers in the supply chain should try to avoid the phenomenon of bifurcation and mutation in the supply chain; in other words: avoid cooperation in the bifurcation and sudden change areas. Otherwise, the supply chain members will not be able to maximize their benefits at the same time.

When the decision-maker encounters a risk for the first time, the risk decision-maker may have an ‘allergic reaction’, that is, the decision-maker will be overly nervous and even at a loss when facing a small risk. When the risk is large to a certain extent, or the decision-maker realizes that the risk is very likely to occur, on the contrary, he will not be particularly sensitive to the risk. The above phenomenon is consistent with objective reality. For example, when the decision-maker has no experience in handling risks at the beginning of preventing risks, he is abnormally uncomfortable with the first coming of risks, and various decision-making errors will often occur. On the other hand, when the decision-makers have experienced risks, or when the risks must occur, they will calmly respond instead. This kind of irrational phenomenon at the beginning of the defence risk can be regarded as a normal objective phenomenon, and managers should treat it correctly.

When a quantity discount contract is used to coordinate a supply chain with random prices and supplier risk aversion, the relevant elements of the supply chain will undergo bifurcation and mutation. The larger the standard deviation of the market demand distribution function, the larger the bifurcation mutation area of each element in the supply chain. The upper and lower amplitude of each element will increase accordingly. However, the maximum order quantity that appears in the bifurcation region does not correspond to the maximum expected return of the supply chain. There is a phenomenon of diseconomies of scale. This shows that risk decision-makers should try to prevent the occurrence of bifurcation and mutation when making centralized decisions in management practice. When risks are about to arise, and the situation is unclear, do not decide to cooperate lightly and wait until the situation is clear before making a decision.

The research of this paper is based on the premise of complete information symmetrical. Therefore, it only considers the coordination problem of the secondary supply chain with supplier risk aversion and retailer risk-neutral under the condition of random price. On this basis, we can further study supply chain coordination in the case of information asymmetry and risk aversion at the same time between supply and sales parties.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}