Evaluating the Application of CSR in the High-Tech Industry during the COVID-19 Pandemic

Abstract

:1. Introduction

2. Literature Review

2.1. Related Literature on Corporate Social Responsibility (CSR)

2.2. Related Literature on the Elements Influencing CSR in High-Tech Industry

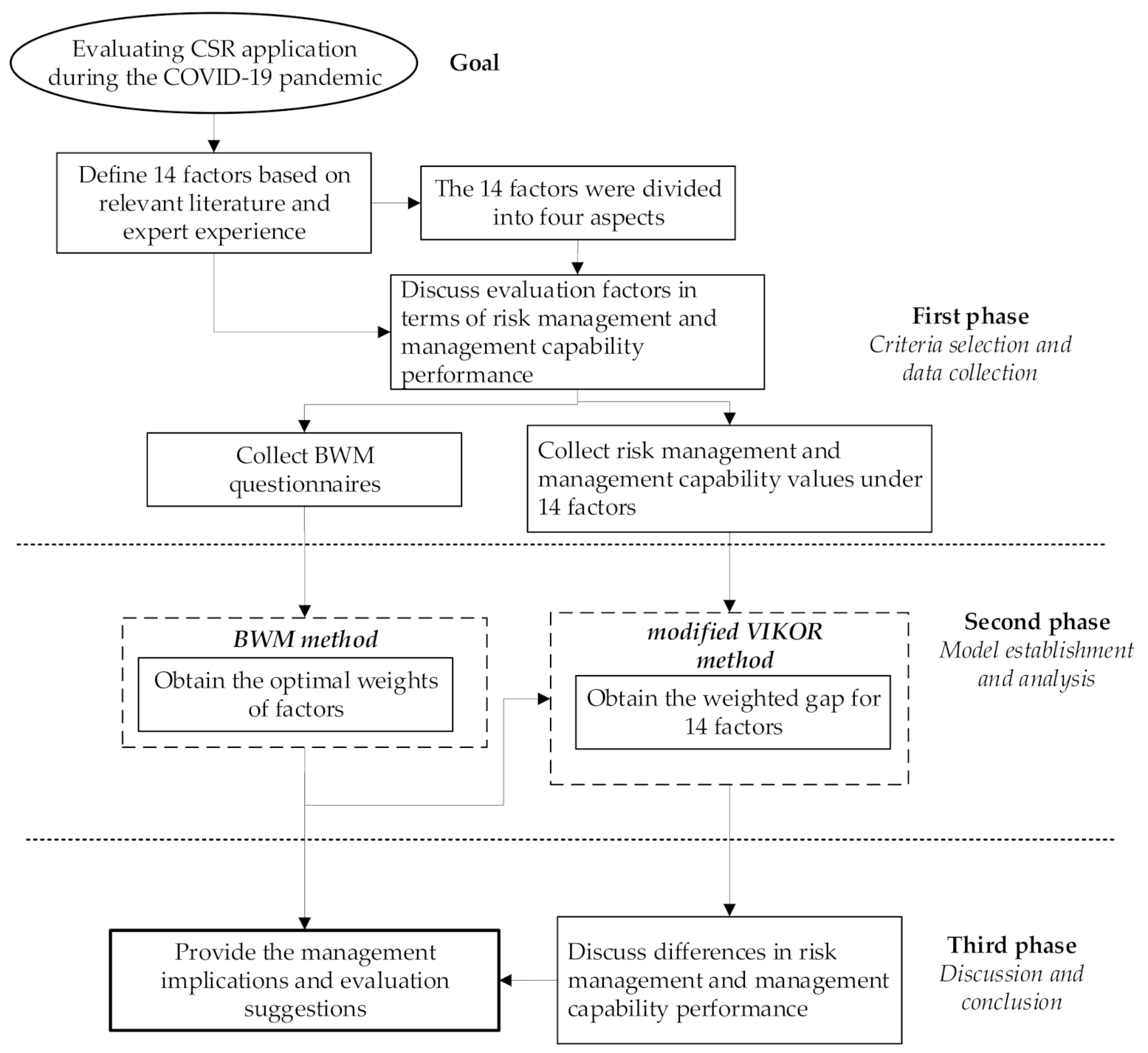

3. Establishing This CSR Application Based on an Integrated MCDM Model

3.1. Establishing the Ranking and Significant Weight with the BWM

3.2. Establishing the Weighted-Gap Levels by Modified VIKOR

4. Case Analysis

4.1. Data Collection

4.2. The Weight of Elements in CSR Application

4.3. Estimating and Mixing These Gaps in Performance with Modified VIKOR

4.4. Outcomes and Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- BBC. Coronavirus: Twitter Boss Pledges $1bn for Relief Effort. The BBC. Available online: https://www.bbc.co.uk/news/technology-52209690 (accessed on 18 April 2020).

- Seuring, S.; Müller, M. From a literature review to a conceptual framework for sustainable supply chain management. J. Clean. Prod. 2008, 16, 1699–1710. [Google Scholar] [CrossRef]

- Rajesh, R. Exploring the sustainability performances of firms using environmental, social, and governance scores. J. Clean. Prod. 2020, 247, 119600. [Google Scholar] [CrossRef]

- Rajeev, A.; Pati, R.K.; Padhi, S.S.; Govindan, K. Evolution of sustainability in supply chain management: A literature review. J. Clean. Prod. 2017, 162, 299–314. [Google Scholar] [CrossRef]

- Sarkis, J.; Zhu, Q. Environmental sustainability and production: Taking the road less travelled. Int. J. Prod. Res. 2018, 56, 743–759. [Google Scholar] [CrossRef]

- Bai, C.; Sarkis, J. Improving green flexibility through advanced manufacturing technology investment: Modeling the decision process. Int. J. Prod. Econ. 2017, 188, 86–104. [Google Scholar] [CrossRef]

- Brandenburg, M.; Govindan, K.; Sarkis, J.; Seuring, S. Quantitative models for sustainable supply chain management: Developments and directions. Eur. J. Oper. Res. 2014, 233, 299–312. [Google Scholar] [CrossRef]

- Dubey, R.; Gunasekaran, A.; Papadopoulos, T.; Childe, S.J.; Shibin, K.T.; Wamba, S.F. Sustainable supply chain management: Framework and further research directions. J. Clean. Prod. 2017, 142, 1119–1130. [Google Scholar] [CrossRef] [Green Version]

- Rajesh, R. Social and environmental risk management in resilient supply chains: A periodical study by the Grey-Verhulst model. Int. J. Prod. Res. 2019, 57, 3748–3765. [Google Scholar] [CrossRef]

- Fahimnia, B.; Tang, C.S.; Davarzani, H.; Sarkis, J. Quantitative models for managing supply chain risks: A review. Eur. J. Oper. Res. 2015, 247, 1–15. [Google Scholar] [CrossRef]

- Ikram, M.; Zhang, Q.; Sroufe, R.; Ferasso, M. The Social Dimensions of Corporate Sustainability: An Integrative Framework Including COVID-19 Insights. Sustainability 2020, 12, 8747. [Google Scholar] [CrossRef]

- Hakovirta, M.; Denuwara, N. How COVID-19 Redefines the Concept of Sustainability. Sustainability 2020, 12, 3727. [Google Scholar] [CrossRef]

- Chang, S.C.; Lu, M.T.; Pan, T.H.; Chen, C.S. Evaluating the E-Health Cloud Computing Systems Adoption in Taiwan’s Healthcare Industry. Life 2021, 11, 310. [Google Scholar] [CrossRef]

- Chen, H.L.; Hu, Y.C.; Lee, M.Y.; Yen, G.F. Importance of Employee Care in Corporate Social Responsibility: An AHP-Based Study from the Perspective of Corporate Commitment. Sustainability 2020, 12, 5885. [Google Scholar] [CrossRef]

- Li, Y.; Pinto, M.C.B.; Diabat, A. Analyzing the critical success factor of CSR for the Chinese textile industry. J. Clean. Prod. 2020, 260, 120878. [Google Scholar] [CrossRef]

- Tran, N. Applying 2-stage DEA model to evaluate the corporate social responsibility implementing efficiency of FDI firms. Manag. Sci. Lett. 2020, 10, 2491. [Google Scholar] [CrossRef]

- Lu, M.T.; Lin, S.W.; Tzeng, G.H. Improving RFID adoption in Taiwan’s healthcare industry based on a DEMATEL technique with a hybrid MCDM model. Decis. Support Syst. 2013, 56, 259–269. [Google Scholar] [CrossRef]

- Lu, M.T.; Tsai, J.F.; Shen, S.P.; Lin, M.H.; Hu, Y.C. Estimating sustainable development performance in the electrical wire and cable industry: Applying the integrated fuzzy MADM approach. J. Clean. Prod. 2020, 277, 122440. [Google Scholar] [CrossRef]

- Chang, S.C.; Chang, H.H.; Lu, M.T. Evaluating Industry 4.0 Technology Application in SMEs: Using a Hybrid MCDM Approach. Mathematics 2021, 9, 414. [Google Scholar] [CrossRef]

- Bae, K.H.; Ghoul, E.S.; Gong, Z.J.; Guedhami, O. Does CSR matter in times of crisis? Evidence from the COVID-19 pandemic. J. Corp. Financ. 2021, 67, 101876. [Google Scholar] [CrossRef]

- Gray, R.; Kouhy, R.; Lavers, S. Corporate social and environmental reporting. Account. Audit. Account. J. 1995, 8, 47–77. [Google Scholar] [CrossRef]

- Deegan, C. The legitimising effect of social and environmental disclosures—A theoretical foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Frynas, J.G.; Yamahaki, C. Corporate social responsibility: Review and roadmap of theoretical perspectives. Bus. Ethics Eur. Rev. 2016, 25, 258–285. [Google Scholar] [CrossRef]

- Huang, C.L.; Kung, F.H. Drivers of environmental disclosure and stakeholder expectation: Evidence from Taiwan. J. Bus. Ethics 2010, 96, 435–451. [Google Scholar] [CrossRef]

- Chen, F.; Tebourbi, I. The relationship between business performance, corporate social responsibility, and innovation capital: A case study of Taiwan. Manag. Decis. Econ. 2021, 42, 360–368. [Google Scholar] [CrossRef]

- Becker-Olsen, K.L.; Cudmore, B.A.; Hill, R.P. The impact of perceived corporate social responsibility on consumer behavior. J. Bus. Res. 2006, 59, 46–53. [Google Scholar] [CrossRef] [Green Version]

- Franco, S.; Caroli, M.G.; Cappa, F.; Del Chiappa, G. Are you good enough? CSR, quality management and corporate financial performance in the hospitality industry. Int. J. Hosp. Manag. 2020, 88, 102395. [Google Scholar] [CrossRef]

- Bocquet, R.; Le Bas, C.; Mothe, C.; Poussing, N. CSR, innovation, and firm performance in sluggish growth contexts: A firm-level empirical analysis. J. Bus. Ethics 2017, 146, 241–254. [Google Scholar] [CrossRef]

- Guerrero-Villegas, J.; Sierra-García, L.; Palacios-Florencio, B. The role of sustainable development and innovation on firm performance. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 1350–1362. [Google Scholar] [CrossRef]

- Mishra, D.R. Post-innovation CSR performance and firm value. J. Bus. Ethics 2017, 140, 285–306. [Google Scholar] [CrossRef]

- Garcia, A.S.; Mendes-Da-Silva, W.; Orsato, R.J. Sensitive Industries Produce Better ESG Performance: Evidence from Emerging Markets. J. Clean. Prod. 2017, 150, 135–147. [Google Scholar] [CrossRef]

- Escrig-Olmedo, E.; Rivera-Lirio, J.M.; Muñoz-Torres, M.J.; Fernández-Izquierdo, M.A. Integrating Multiple ESG Investors’ Preferences into Sustainable Investment: A Fuzzy Multicriteria Methodological Approach. J. Clean. Prod. 2017, 162, 1334–1345. [Google Scholar] [CrossRef]

- Martí-Ballester, C.P. Can Socially Responsible Investment for Cleaner Production Improve the Financial Performance of Spanish Pension Plans? J. Clean. Prod. 2015, 106, 466–477. [Google Scholar] [CrossRef]

- Tseng, M.L.; Tan, P.A.; Jeng, S.Y.; Negash, Y.T.; Darsono, S.N. Sustainable investment: Interrelated among corporate governance, economic performance and market risks using investor preference approach. Sustainability 2019, 11, 2108. [Google Scholar] [CrossRef] [Green Version]

- Karlsson, N.P.E. Business models and business cases for financial sustainability: Insights on corporate sustainability in the Swedish farm-based biogas industry. Sustain. Prod. Consum. 2019, 18, 115–129. [Google Scholar] [CrossRef]

- Guo, L.; Qu, Y.; Tseng, M.L. The interaction effects of environmental regulation and technological innovation on regional green growth performance. J. Clean. Prod. 2017, 162, 894–902. [Google Scholar] [CrossRef]

- Wu, W.-W.; Lee, Y.-T.; Tseng, M.-L.; Chiang, Y.-H. Data mining for exploring hidden patterns between KM and its performance. Knowl. Based Syst. 2010, 23, 397–401. [Google Scholar] [CrossRef]

- Nesticò, A.; He, S.; De Mare, G.; Benintendi, R.; Maselli, G. The ALARP Principle in the Cost-Benefit Analysis for the Acceptability of Investment Risk. Sustainability 2018, 10, 4668. [Google Scholar] [CrossRef] [Green Version]

- Prakash, C.; Barua, M.K. A combined MCDM approach for evaluation and selection of third-party reverse logistics partner for Indian electronics industry. Sustain. Prod. Consum. 2016, 7, 66–78. [Google Scholar] [CrossRef]

- Khedrigharibvand, H.; Azadi, H.; Teklemariam, D.; Houshyar, E.; De Maeyer, P.; Witlox, F. Livelihood alternatives model for sustainable rangeland management: A review of multi-criteria decision-making techniques. Environ. Dev. Sustain. 2017, 21, 11–36. [Google Scholar] [CrossRef]

- Garg, C.P.; Sharma, A. Sustainable outsourcing partner selection and evaluation using an integrated BWM–VIKOR framework. Environ. Dev. Sustain. 2020, 22, 1529–1557. [Google Scholar] [CrossRef]

- Rezaei, J. Best-worst multi-criteria decision-making method. Omega 2015, 53, 49–57. [Google Scholar] [CrossRef]

- Rezaei, J. Best-worst multi-criteria decision-making method: Some properties and a linear model. Omega 2016, 64, 126–130. [Google Scholar] [CrossRef]

- Gupta, H. Evaluating service quality of airline industry using hybrid best worst method and VIKOR. J. Air Transp. Manag. 2018, 68, 35–47. [Google Scholar] [CrossRef]

- Karaman, A.S.; Akman, E. Taking-off corporate social responsibility programs: An AHP application in airline industry. J. Air Transp. Manag. 2018, 68, 187–197. [Google Scholar] [CrossRef]

- Rezaei, J.; Nispeling, T.; Sarkis, J.; Tavasszy, L. A supplier selection life cycle approach integrating traditional and environmental criteria using the best worst method. J. Clean. Prod. 2016, 135, 577–588. [Google Scholar] [CrossRef]

- Rezaei, J.; Wang, J.; Tavasszy, L. Linking supplier development to supplier segmentation using Best Worst Method. Expert Syst. Appl. 2015, 42, 9152–9164. [Google Scholar] [CrossRef]

- Salimi, N.; Rezaei, J. Measuring efficiency of university-industry Ph.D. projects using best worst method. Scientometrics 2016, 109, 1911–1938. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Ren, J.; Liang, H.; Chan, F.T. Urban sewage sludge, sustainability, and transition for Eco-City: Multi-Criteria sustainability assessment of technologies based on best-worst method. Technol. Forecast. Soc. 2017, 116, 29–39. [Google Scholar] [CrossRef]

- Gupta, H.; Barua, M.K. Identifying enablers of technological innovation for Indian MSMEs using best–worst multi criteria decision making method. Technol. Forecast. Soc. 2016, 107, 69–79. [Google Scholar] [CrossRef]

- Ahmad, W.N.K.W.; Rezaei, J.; Sadaghiani, S.; Tavasszy, L.A. Evaluation of the external forces affecting the sustainability of oil and gas supply chain using Best Worst Method. J. Clean. Prod. 2017, 153, 242–252. [Google Scholar] [CrossRef]

- Pamučar, D.; Petrović, I.; Ćirović, G. Modification of the Best–Worst and MABAC methods: A novel approach based on interval-valued fuzzy-rough numbers. Expert Syst. Appl. 2018, 91, 89–106. [Google Scholar] [CrossRef]

- Kumar, A.; Aswin, A.; Gupta, H. Evaluating green performance of the airports using hybrid BWM and VIKOR methodology. Tour. Manag. 2020, 76, 103941. [Google Scholar] [CrossRef]

- Lu, M.T.; Tzeng, G.H.; Cheng, H.; Hsu, C.C. Exploring mobile banking services for user behavior in intention adoption: Using new hybrid MADM model. Serv. Bus. 2015, 9, 541–565. [Google Scholar] [CrossRef]

- Feng, Y.; Hong, Z.; Tian, G.; Li, Z.; Tan, J.; Hu, H. Environmentally friendly MCDM of reliability-based product optimisation combining DEMATEL-based ANP, interval uncertainty and Vlse Kriterijumska Optimizacija Kompromisno Resenje (VIKOR). Inf. Sci. 2018, 442, 128–144. [Google Scholar] [CrossRef]

- Wu, M.; Li, C.; Fan, J.; Wang, X.; Wu, Z. Assessing the global productive efficiency of Chinese banks using the cross-efficiency interval and VIKOR. Emerg. Mark. Rev. 2017, 34, 77–86. [Google Scholar] [CrossRef]

- Rajesh, R. Measuring the barriers to resilience in manufacturing supply chains using grey clustering and vikor approaches. Measurement 2018, 126, 259–273. [Google Scholar] [CrossRef]

- Wu, Y.; Zhang, B.; Xu, C.; Li, L. Site selection decision framework using fuzzy ANP-VIKOR for large commercial rooftop PV system based on sustainability perspective. Sustain. Cities Soc. 2018, 40, 454–470. [Google Scholar] [CrossRef]

- Opricovic, S.; Tzeng, G.H. Compromise solution by MCDM methods: A comparative analysis of VIKOR and TOPSIS. Eur. J. Oper. Res. 2004, 156, 445–455. [Google Scholar] [CrossRef]

- Lu, M.T.; Hsu, C.C.; Liou, J.J.; Lo, H.W. A hybrid MCDM and sustainability balanced scorecard model to establish sustainable performance evaluation for international airports. J. Air Transp. Manag. 2018, 71, 9–19. [Google Scholar] [CrossRef]

- Lu, M.T.; Tzeng, G.H.; Tang, L.L. Environmental strategic orientations for improving green innovation performance in fuzzy environment-Using new fuzzy Hybrid MCDM model. Int. J. Fuzzy Syst. 2013, 15, 297–316. [Google Scholar]

{kind=link}

| Aspect | Element | Description |

|---|---|---|

| Environment aspect (A1) | Resource reduction (RR) | Minimizing the resources used to produce a product |

| Product innovation (PI) | Firm innovation performance | |

| Emissions reduction (ER) | Emissions produced by a firm | |

| Social aspect (A2) | Product responsibility (PR) | Provide services and products by green concepts |

| Community (CO) | The role of the company in the community | |

| Human rights (HR) | The staff are qualified per the law | |

| Employment quality (EQ) | The quality of employment required for living standards is obtained through the company | |

| Corporate governance aspect (A3) | Compensation policy (CP) | The ratio to pay the compensation and executive strategy |

| Board functions (BF) | The functions of the trustee board in the company | |

| Vision and strategy (VS) | Vision and strategy in the company | |

| Shareholder rights (SR) | The rights of the shareholders in the firm | |

| Economic aspect (A4) | Shareholder loyalty (SL) | The loyalty of shareholders to CSR |

| Firm performance (FP) | The economic performance of the company each month | |

| Client loyalty (CL) | Clients’ loyalty to the investors |

| Aspects/Elements | Local Weight | Local Rank | Global Weight | Global Rank |

|---|---|---|---|---|

| Environment aspect (A1) | 0.147 | |||

| Resource reduction (RR) | 0.569 | 1 | 0.084 | 5 |

| Product innovation (PI) | 0.222 | 2 | 0.033 | 11 |

| Emissions reduction (ER) | 0.209 | 3 | 0.031 | 13 |

| Social aspect (A2) | 0.206 | |||

| Product responsibility (PR) | 0.182 | 2 | 0.037 | 10 |

| Community (CO) | 0.089 | 3 | 0.018 | 14 |

| Human rights (HR) | 0.291 | 2 | 0.060 | 7 |

| Employment quality (EQ) | 0.438 | 1 | 0.090 | 4 |

| Corporate governance aspect (A3) | 0.288 | |||

| Compensation policy (CP) | 0.204 | 2 | 0.059 | 8 |

| Board functions (BF) | 0.162 | 3 | 0.047 | 9 |

| Vision and strategy (VS) | 0.526 | 1 | 0.152 | 2 |

| Shareholder rights (SR) | 0.108 | 4 | 0.031 | 12 |

| Economic aspect (A4) | 0.359 | |||

| Shareholder loyalty (SL) | 0.354 | 2 | 0.127 | 3 |

| Firm performance (FP) | 0.427 | 1 | 0.153 | 1 |

| Client loyalty (CL) | 0.219 | 3 | 0.079 | 6 |

| Aspects/Elements | Local Weight | Global Weight | CSR Performance Gap | |

|---|---|---|---|---|

| Risk Management (S1) | Management Capability (S2) | |||

| Environment aspect (A1) | 0.147 | 0.304 | 0.253 | |

| Resource reduction (RR) | 0.569 | 0.084 | 0.370 | 0.290 |

| Product innovation (PI) | 0.222 | 0.033 | 0.120 | 0.150 |

| Emissions reduction (ER) | 0.209 | 0.031 | 0.320 | 0.260 |

| Social aspect (A2) | 0.206 | 0.328 | 0.321 | |

| Product responsibility (PR) | 0.182 | 0.037 | 0.360 | 0.290 |

| Community (CO) | 0.089 | 0.018 | 0.570 | 0.540 |

| Human rights (HR) | 0.291 | 0.060 | 0.290 | 0.260 |

| Employment quality (EQ) | 0.438 | 0.090 | 0.290 | 0.330 |

| Corporate governance aspect (A3) | 0.288 | 0.308 | 0.249 | |

| Compensation policy (CP) | 0.204 | 0.059 | 0.380 | 0.330 |

| Board functions (BF) | 0.162 | 0.047 | 0.340 | 0.300 |

| Vision and strategy (VS) | 0.526 | 0.152 | 0.230 | 0.170 |

| Shareholder rights (SR) | 0.108 | 0.031 | 0.500 | 0.400 |

| Economic aspect (A4) | 0.359 | 0.253 | 0.236 | |

| Shareholder loyalty (SL) | 0.354 | 0.127 | 0.240 | 0.220 |

| Firm performance (FP) | 0.427 | 0.153 | 0.210 | 0.200 |

| Client loyalty (CL) | 0.219 | 0.079 | 0.360 | 0.330 |

| SA | Total gaps | 0.279 | 0.242 | |

| Formula | Sequence of Improvement Priority | |

|---|---|---|

| F1: Sequence of aspects to reach target levels in two CSR performance areas (from high to low, via gap performances) | Risk management performance (S1) | (A2) > (A3) > (A1) > (A4) |

| Management capability performance (S2) | (A2) > (A1) > (A3) > (A4) | |

| F2: Sequence of elements to reach the target level within individual aspects (from high to low, via gap performances) | Risk management performance (S1) | |

| (A1): (RR) > (ER) > (PI) (A2): (CO) > (PR) > (EQ) > (HR) (A3): (SR) > (CP) > (BF) > (CS) (A2): (CL) > (SL) > (FP) | ||

| Management capability performance (S2) | ||

| (A1): (RR) > (ER) > (PI) (A2): (CO) > (EQ) > (PR) > (HR) (A3): (SR) > (CP) > (BF) > (CS) (A2): (CL) > (SL) > (FP) | ||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chang, S.-C.; Lu, M.-T.; Chen, M.-J.; Huang, L.-H. Evaluating the Application of CSR in the High-Tech Industry during the COVID-19 Pandemic. Mathematics 2021, 9, 1715. https://doi.org/10.3390/math9151715

Chang S-C, Lu M-T, Chen M-J, Huang L-H. Evaluating the Application of CSR in the High-Tech Industry during the COVID-19 Pandemic. Mathematics. 2021; 9(15):1715. https://doi.org/10.3390/math9151715

Chicago/Turabian StyleChang, Shih-Chia, Ming-Tsang Lu, Mei-Jen Chen, and Li-Hua Huang. 2021. "Evaluating the Application of CSR in the High-Tech Industry during the COVID-19 Pandemic" Mathematics 9, no. 15: 1715. https://doi.org/10.3390/math9151715

APA StyleChang, S.-C., Lu, M.-T., Chen, M.-J., & Huang, L.-H. (2021). Evaluating the Application of CSR in the High-Tech Industry during the COVID-19 Pandemic. Mathematics, 9(15), 1715. https://doi.org/10.3390/math9151715