Fractional Dynamics and Pseudo-Phase Space of Country Economic Processes

Abstract

1. Introduction

2. Fundamental Concepts

2.1. The Fractional Calculus

2.2. The Pseudo-Phase Space

3. The Description of the Time Series Dynamics

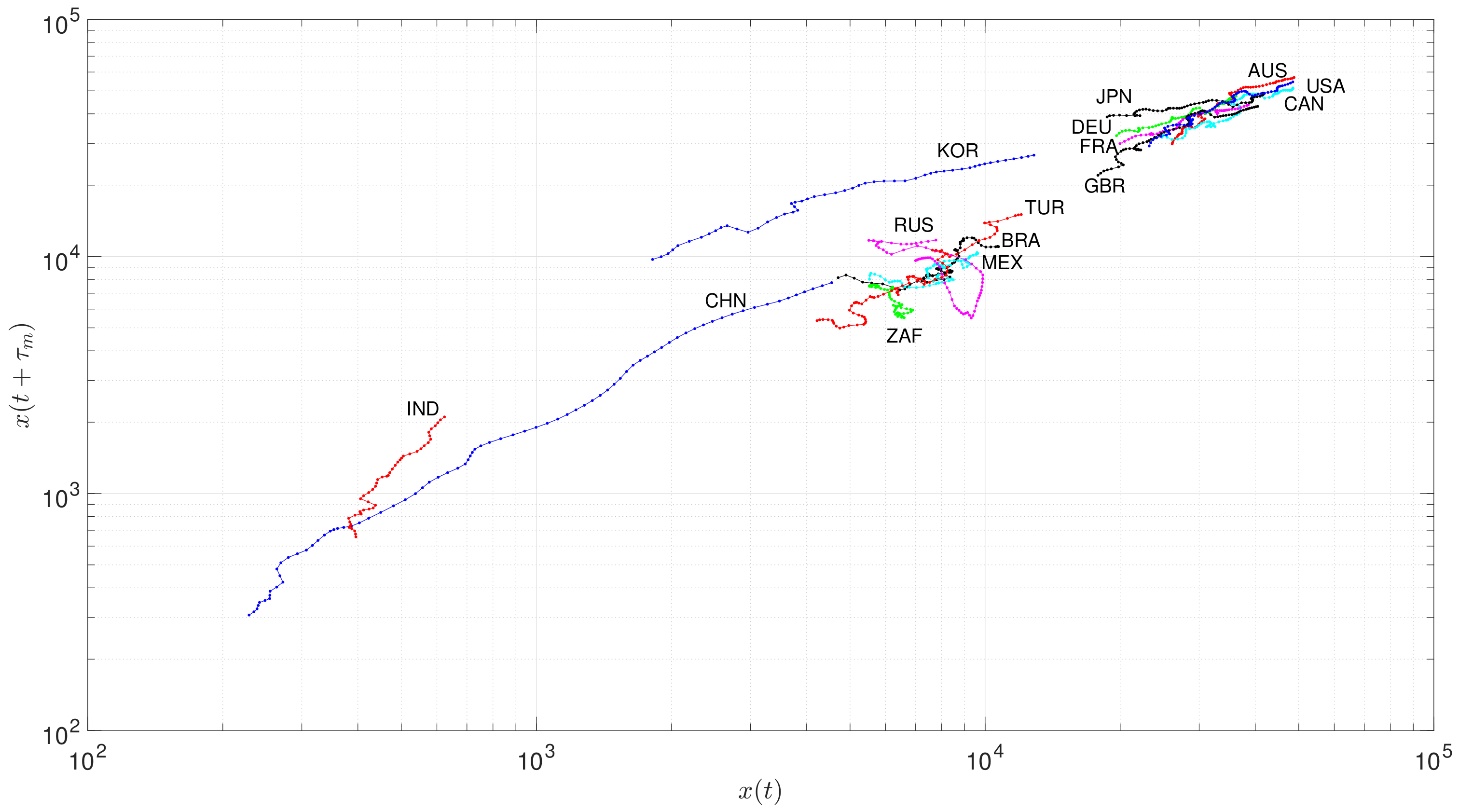

- The European partners and Japan could catch-up to the US and two other old European offshores (Australia and Canada). Before the late 1980s and the fall of the Berlin Wall, fighting communism may be considered to have been crucial to the national political strategies in most Western European countries and in East Asia. The anti-communist strategies clearly stimulated national policies in drawing them toward stock markets after the late 1980s. Many decision makers working at the World Bank and other international development agencies have even criticized codification of capital markets as meaning overregulation for the purpose of extending capitalism to communist-socialist areas.

- The heirs of old empires (Turkey and Russia), Korea, and three of the European offshores (Mexico, Brazil, and South Africa) also converged. In spite of cultural differences, genetic specificity, and climatic influences, they experimented consumption uniformization, with barriers that result from inequality in the distribution of revenue. Russia’s political change has made its transition to convergence with the most-developed economies difficult, and the country exhibits more erratic economic growth behavior, comprising periods of strong rates of growth separated by frequent and severe crises.

- The two Asian historical civilizations, China and India, have proceeded at fast and regular economic growth rates; China and India’s comparatively less-modern sectors have been catching up disproportionately faster to the world productivity frontier [44].

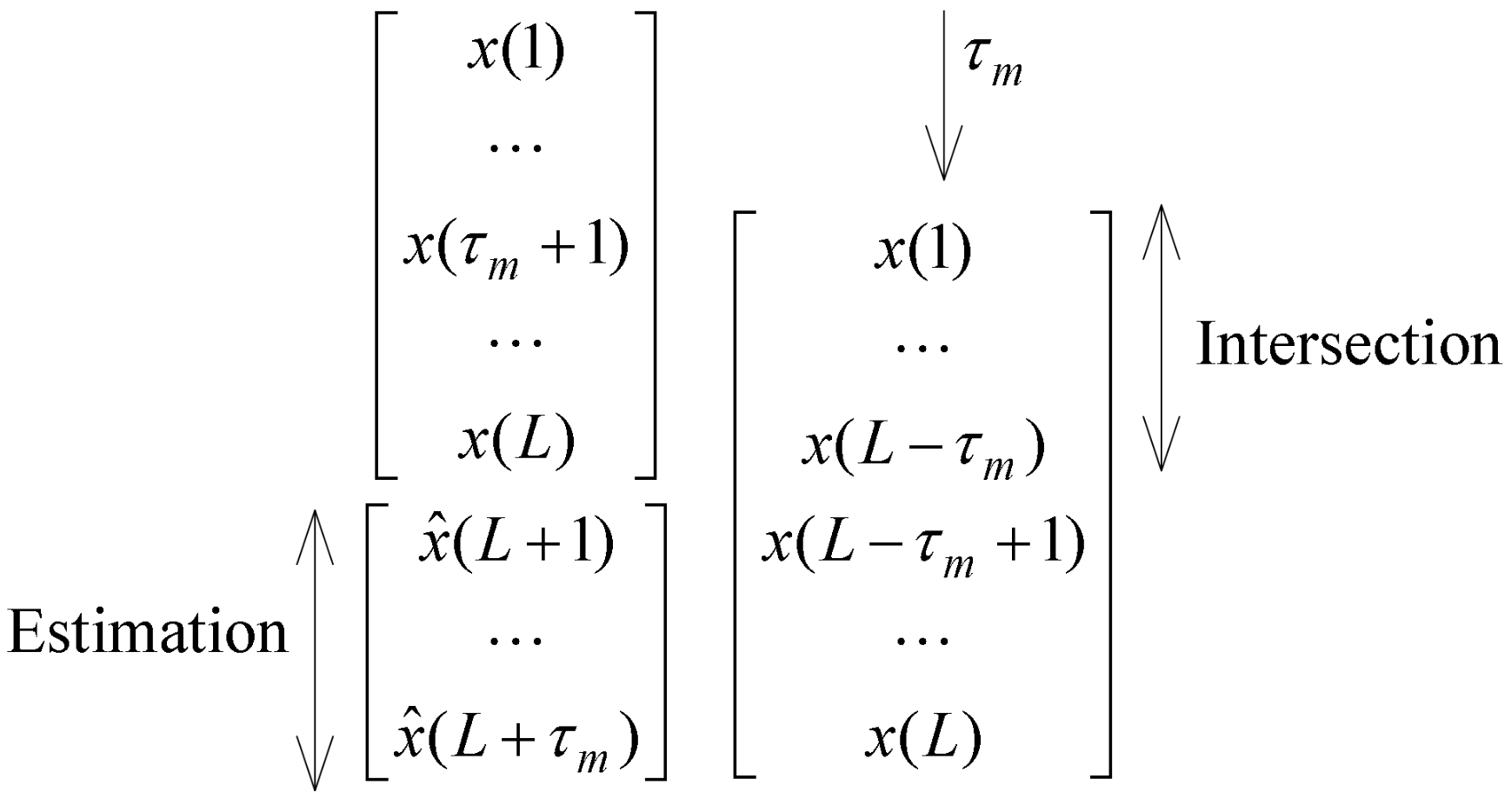

4. Estimation

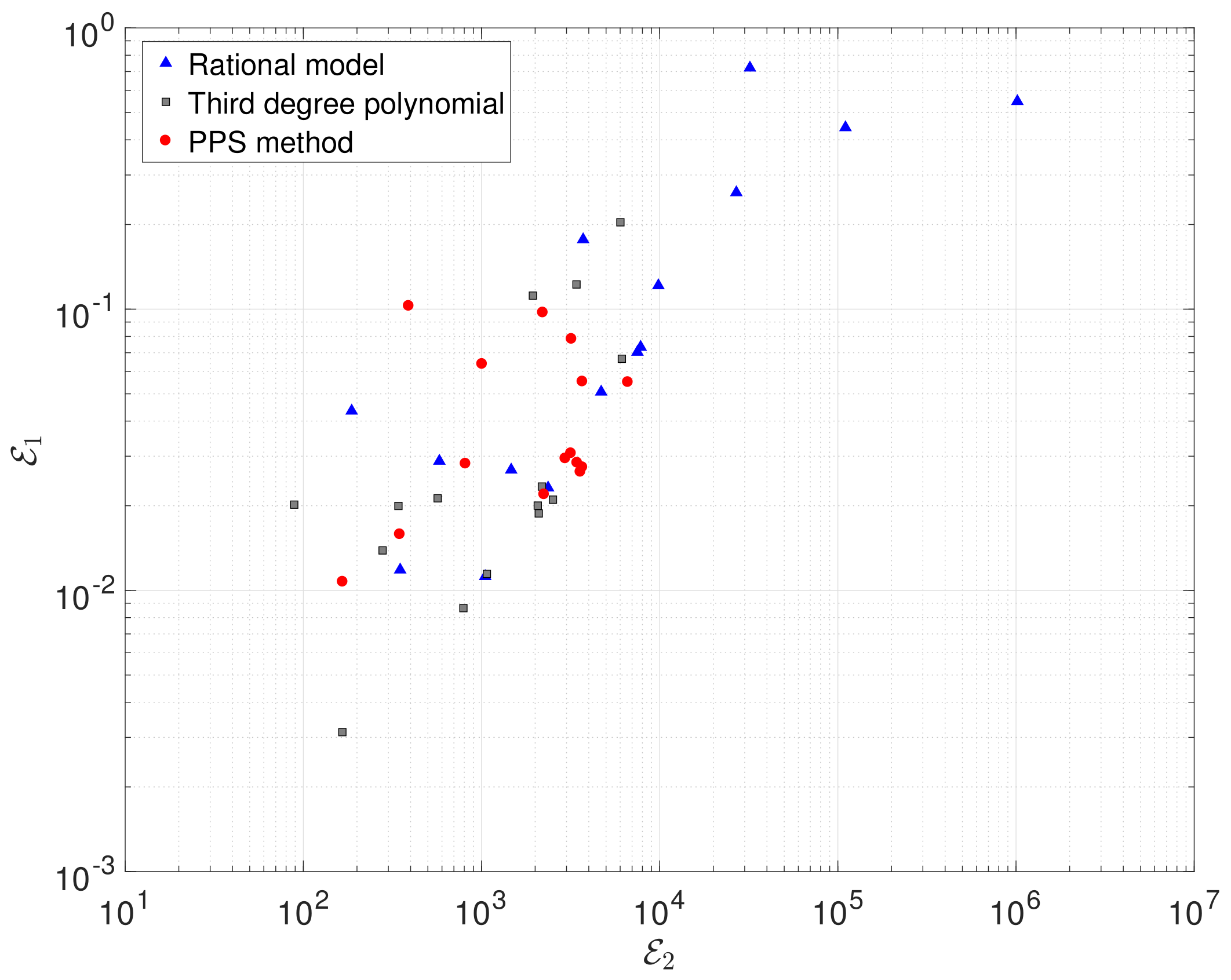

4.1. Assessing the Estimation Method

4.2. Complete Estimation of GDP per Capita

5. Discussion and Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Stiglitz, J.E.; Fitoussi, J.P.; Durand, M. Measuring What Counts: The Global Movement for Well-Being; The New Press: New York, NY, USA; London, UK, 2019. [Google Scholar]

- Stiglitz, J. It’s Time to Retire Metrics Like GDP. They Don’t Measure Everything that Matters. Available online: https://www.theguardian.com/commentisfree/2019/nov/24/metrics-gdp-economic-performance-social-progress?utm_campaign=todays_worldview&utm_medium=Email&utm_source=Newsletter&wpisrc=nl_todayworld&wpmm=1 (accessed on 26 November 2019).

- Fogel, R.W. Capitalism and Democracy in 2040: Forecasts and Speculations; NBER Working-Paper No. 13184; National Bureau of Economic Research: Cambridge, MA, USA, 2007. [Google Scholar]

- Bordo, M.; Eichengreen, B.; Klingebiel, D.; Martinez-Peria, M.S.; Rose, A.K. Is the Crisis Problem Growing More Severe? Econ. Policy 2001, 16, 53–82. [Google Scholar] [CrossRef]

- Schularick, M.; Taylor, A.M. Credit Booms Gone Bust: Monetary Policy, Leverage Cycles and Financial Crises, 1870–2008. Am. Econ. Rev. 2012, 102, 1029–1061. [Google Scholar] [CrossRef]

- Taylor, A.M. The Great Leveraging; NBER Working-Paper No. 18290; National Bureau of Economic Research: Cambridge, MA, USA, 2012. [Google Scholar]

- Maito, E.E. The Historical Transience of Capital: The Downward Trend in the Rate of Profit Since XIX Century; MPRA Paper No. 55894; National Bureau of Economic Research: Cambridge, MA, USA, 2014. [Google Scholar]

- Schumpeter, J.A. Business Cycles, a Theoretical, Historical and Statistical Analysys of the Capitalist Process; Martino Pub.: New York, NY, USA, 1939. [Google Scholar]

- Hayek, F.A. The Road to Serfdom: With the Intellectuals and Socialism; Routledge: London, UK, 1944. [Google Scholar]

- Rostow, W.W. Stages of Economic Growth, A Non-Communist Manifesto; Cambridge University Press: Cambridge, UK, 1960. [Google Scholar]

- Gerschenkron, A. Economic Backwardness in Historical Perspective: A Book of Essays; Belknap Press of Harvard University Press: Cambridge, MA, USA, 1962. [Google Scholar]

- Roe, M.J. Political Determinants of Corporate Governance: Political context, Corporate Impact; Oxford University Press on Demand: Oxford, UK, 2006. [Google Scholar]

- Maddison, A. Development Centre Studies the World Economy: A Millennial Perspective; OECD Pub.: Paris, France, 2001. [Google Scholar]

- Petráš, I.; Podlubny, I. State Space Description of National Economies: The V4 Countries. Comput. Stat. Data Anal. 2007, 52, 1223–1233. [Google Scholar] [CrossRef]

- Tenreiro Machado, J.; Mata, M.E. Europe at the Crossroads of Economic Integration: Multidimensional Scaling Analysis of the Period 1970–2010. Écon. Soc. 2012, 45, 1553–1577. [Google Scholar]

- Tenreiro Machado, J.; Mata, M.E. Multidimensional Scaling Analysis of the Dynamics of a Country Economy. Sci. World J. 2013, 2013, 594587. [Google Scholar] [CrossRef] [PubMed]

- Škovránek, T.; Podlubny, I.; Petráš, I. Modeling of the National Economies in State-space: A Fractional Calculus Approach. Econ. Model. 2012, 29, 1322–1327. [Google Scholar] [CrossRef]

- Machado, J.A.T.; Mata, M.E. A Fractional Perspective to the Bond Graph Modelling of World Economies. Nonlinear Dyn. 2014, 80, 1839–1852. [Google Scholar] [CrossRef]

- Machado, J.; Mata, M.; Lopes, A. Fractional State Space Analysis of Economic Systems. Entropy 2015, 17, 5402–5421. [Google Scholar] [CrossRef]

- Machado, J.T.; Mata, M.E. Pseudo-phase Plane and Fractional Calculus Modeling of Western Global Economic Downturn. Commun. Nonlinear Sci. Numer. Simul. 2015, 22, 396–406. [Google Scholar] [CrossRef]

- Tarasova, V.V.; Tarasov, V.E. Logistic Map with Memory from Economic Model. Chaos Solitons Fractals 2017, 95, 84–91. [Google Scholar] [CrossRef]

- Tarasov, V.E.; Tarasova, V.V. Dynamic Keynesian Model of Economic Growth with Memory and Lag. Mathematics 2019, 7, 178. [Google Scholar] [CrossRef]

- Tejado, I.; Pérez, E.; Valério, D. Fractional Calculus in Economic Growth Modelling of the Group of Seven. Fract. Calc. Appl. Anal. 2019, 22, 139–157. [Google Scholar] [CrossRef]

- Ming, H.; Wang, J.; Fečkan, M. The Application of Fractional Calculus in Chinese Economic Growth Models. Mathematics 2019, 7, 665. [Google Scholar] [CrossRef]

- Skovranek, T. The Mittag-Leffler Fitting of the Phillips Curve. Mathematics 2019, 7, 589. [Google Scholar] [CrossRef]

- Tarasov, V.E. On History of Mathematical Economics: Application of Fractional Calculus. Mathematics 2019, 7, 509. [Google Scholar] [CrossRef]

- Samko, S.; Kilbas, A.; Marichev, O. Fractional Integrals and Derivatives: Theory and Applications; Gordon and Breach Science Publishers: Amsterdam, The Netherlands, 1993. [Google Scholar]

- Kilbas, A.; Srivastava, H.; Trujillo, J. Theory and Applications of Fractional Differential Equations; North-Holland Mathematics Studies; Elsevier: Amsterdam, The Netherlands, 2006; Volume 204. [Google Scholar]

- Tarasov, V. Fractional Dynamics: Applications of Fractional Calculus to Dynamics of Particles, Fields and Media; Springer: New York, NY, USA, 2010. [Google Scholar]

- Baleanu, D.; Diethelm, K.; Scalas, E.; Trujillo, J.J. Fractional Calculus: Models and Numerical Methods; Series on Complexity, Nonlinearity and Chaos; World Scientific Publishing Company: Singapore, 2012. [Google Scholar]

- Machado, J.T.; Lopes, A.M. Analysis of Natural and Artificial Phenomena Using Signal Processing and Fractional Calculus. Fract. Calc. Appl. Anal. 2015, 18, 459–478. [Google Scholar] [CrossRef]

- Scalas, E.; Gorenflo, R.; Mainardi, F. Waiting-times and Returns in High-frequency Financial Data: An Empirical Study. Phys. A Stat. Mech. Its Appl. 2002, 314, 749–755. [Google Scholar]

- Machado, J.T.; Lopes, A.M. Relative Fractional Dynamics of Stock Markets. Nonlinear Dyn. 2016, 86, 1613–1619. [Google Scholar] [CrossRef]

- Lopes, A.M.; Machado, J.T.; Huffstot, J.S.; Mata, M.E. Dynamical Analysis of the Global Business-cycle Synchronization. PLoS ONE 2018, 13, e0191491. [Google Scholar] [CrossRef]

- Tarasov, V.E.; Tarasova, V.V. Macroeconomic Models with Long Dynamic Memory: Fractional Calculus Approach. Appl. Math. Comput. 2018, 338, 466–486. [Google Scholar] [CrossRef]

- Valério, D.; Trujillo, J.J.; Rivero, M.; Machado, J.T.; Baleanu, D. Fractional Calculus: A Survey of Useful Formulas. Eur. Phys. J. Spec. Top. 2013, 222, 1827–1846. [Google Scholar] [CrossRef]

- Lopes, A.M.; Machado, J.T. Discrete-time Generalized Mean Fractional Order Controllers. IFAC-PapersOnLine 2018, 51, 43–47. [Google Scholar] [CrossRef]

- Takens, F. Detecting Strange Attractors in Turbulence. In Dynamical Systems and Turbulence, Proceedings of a Symposium Held at the University of Warwick 1979/80; Rand, D., Young, L.S., Eds.; Lecture Notes in Mathematics; Springer: Berlin, Germany, 1981; Volume 898, pp. 366–381. [Google Scholar]

- Ali Shah, S.A.; Aziz, W.; Nadeem, A.; Sajjad, M.; Almaraashi, M.; Shim, S.O.; Habeebullah, T.M. A Novel Phase Space Reconstruction-(PSR-) Based Predictive Algorithm to Forecast Atmospheric Particulate Matter Concentration. Sci. Program. 2019, 2019, 6780379. [Google Scholar] [CrossRef]

- Holoborodko, P. Smooth Noise Robust Differentiators. 2008. Available online: http://www.holoborodko.com/pavel/numerical-methods/numerical-derivative/smooth-low-noise-differentiators/ (accessed on 26 November 2019).

- Clark, H.; Pinkovskiy, M.; Sala-i Martin, X. China’s GDP Growth May Be Understated; Technical Report; National Bureau of Economic Research: Cambridge, MA, USA, 2017. [Google Scholar]

- Haltmaier, J. Challenges for the Future of Chinese Economic Growth. In FRB International Finance Discussion Paper; Board of Governors of the Federal Reserve System: Washington, DC, USA, 2013. [Google Scholar]

- Deza, M.M.; Deza, E. Encyclopedia of Distances; Springer: Berlin/Heidelberg, Germany, 2009. [Google Scholar]

- Di Giovanni, J.; Levchenko, A.A.; Zhang, J. The Global Welfare Impact of China: Trade Integration and Technological Change; CEPR Discussion Paper; Centre for Economic Policy Research: London, UK, 2013. [Google Scholar]

- Clements, M.P.; Hendry, D.F. Forecasting Non-Stationary Economic Time Series; MIT Press: Cambridge, MA, USA, 2000. [Google Scholar]

- Granger, C.W.J.; Newbold, P. Forecasting Economic Time Series; Academic Press: Cambridge, MA, USA, 2014. [Google Scholar]

- Abeysinghe, T.; Rajaguru, G. Quarterly Real GDP Estimates for China and ASEAN4 with a Forecast Evaluation. J. Forecast. 2004, 23, 431–447. [Google Scholar] [CrossRef]

- Maity, B.; Chatterjee, B. Forecasting GDP Growth Rates of India: An Empirical Study. Int. J. Econ. Manag. Sci. 2012, 1, 52–58. [Google Scholar]

- Kaastra, I.; Boyd, M. Designing a Neural Network for Forecasting Financial and Economic Time Series. Neurocomputing 1996, 10, 215–236. [Google Scholar] [CrossRef]

- Claveria, O.; Monte, E.; Torra, S. Evolutionary Computation for Macroeconomic Forecasting. Comput. Econ. 2019, 53, 833–849. [Google Scholar] [CrossRef]

- Gupta, M.; Minai, M.H. An Empirical Analysis of Forecast Performance of the GDP Growth in India. Glob. Bus. Rev. 2019, 20, 368–386. [Google Scholar] [CrossRef]

- Moiseev, N.A. Forecasting Time Series of Economic Processes by Model Averaging Across Data Frames of Various Lengths. J. Stat. Comput. Simul. 2017, 87, 3111–3131. [Google Scholar] [CrossRef]

- Bencivelli, L.; Marcellino, M.; Moretti, G. Forecasting Economic Activity by Bayesian Bridge Model Averaging. Empir. Econ. 2017, 53, 21–40. [Google Scholar] [CrossRef]

- Deza, E.; Deza, M.M. Dictionary of Distances; Elsevier: Amsterdam, The Netherlands, 2006. [Google Scholar]

- Xavier, S.I.M. I Just Ran Two Million Regressions. Am. Econ. Rev. 1997, 87, 178-83. [Google Scholar]

- Stovsky, R.; Esch, K. Trendsetter Barometer: Business Outlook; Technical Report; Pricewaterhousecoopers LLP: London, UK, 2014. [Google Scholar]

- Guriev, S.; Vakulenko, E. Breaking out of Poverty Traps: Internal Migration and Interregional Convergence in Russia; DP9675; Center for Economic Policy Research: Washington, DC, USA, 2013. [Google Scholar]

- Battisti, M.; di Vaio, G.; Zeira, J. Global Divergence in Growth Regressions; DP 96872013; Center for Economic Policy Research: Washington, DC, USA, 2013. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

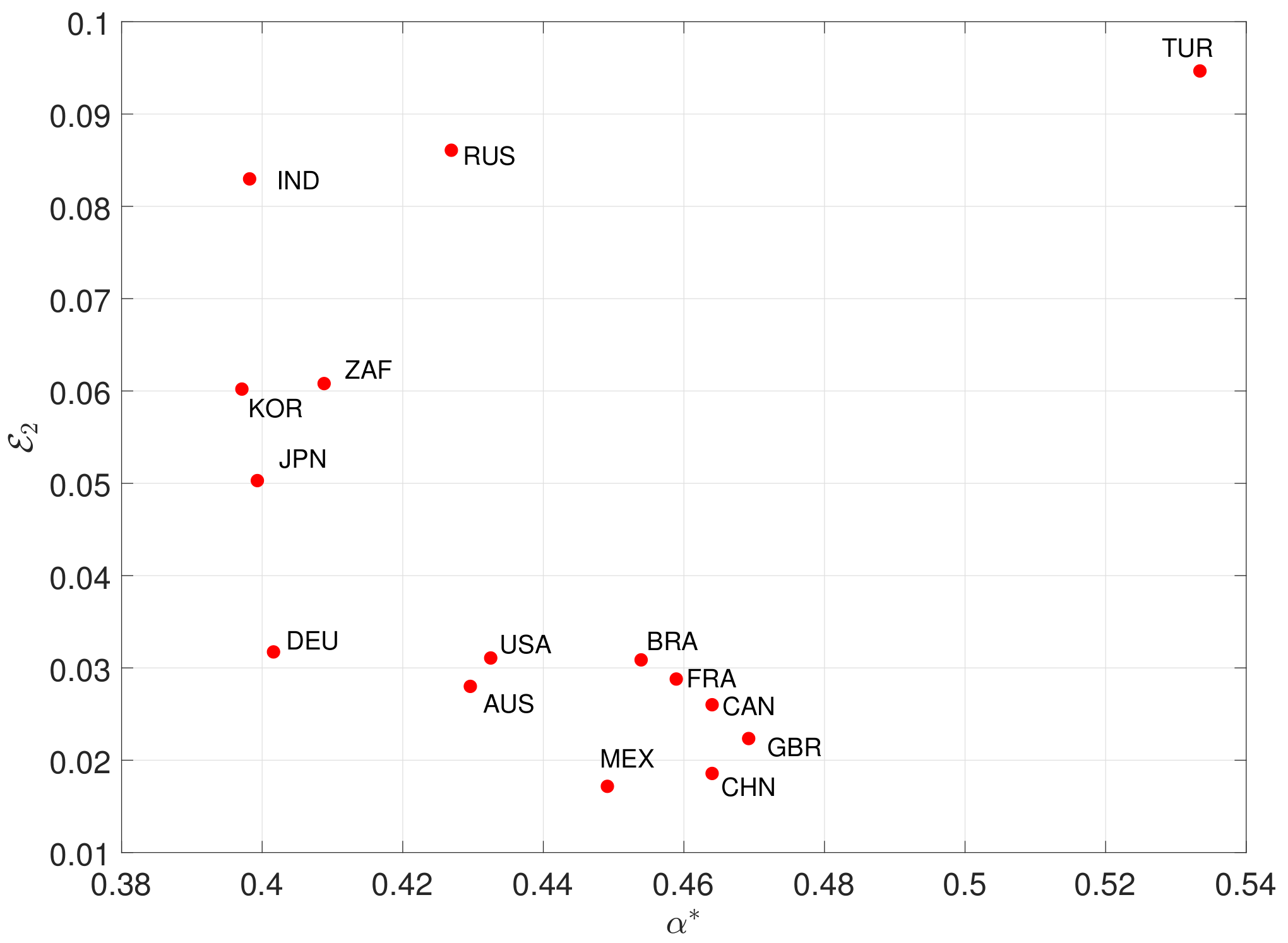

| AUS | BRA | CAN | CHN | FRA | DEU | IND | JPN | KOR | MEX | RUS | ZAF | TUR | GBR | USA | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (years) | 13 | 9.5 | 10 | 8 | 17.5 | 20 | 24.5 | 20.5 | 22 | 10 | 15 | 19 | 6 | 12 | 13 |

| 0.430 | 0.454 | 0.450 | 0.470 | 0.406 | 0.400 | 0.390 | 0.398 | 0.395 | 0.449 | 0.419 | 0.402 | 0.492 | 0.435 | 0.430 |

| AUS | BRA | CAN | CHN | FRA | DEU | IND | JPN | KOR | MEX | RUS | ZAF | TUR | GBR | USA | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (years) | 13 | 9.5 | 8.5 | 8.5 | 9 | 19 | 20.5 | 20 | 21 | 10 | 13.5 | 17 | 5 | 8 | 12.5 |

| 0.430 | 0.454 | 0.464 | 0.464 | 0.459 | 0.402 | 0.398 | 0.399 | 0.397 | 0.449 | 0.427 | 0.409 | 0.534 | 0.469 | 0.433 | |

| 3759.3 | 848.4 | 3170.7 | 315.3 | 2879.7 | 3278.0 | 325.0 | 6031.7 | 3995.9 | 374.3 | 1950.5 | 947.6 | 3764.0 | 2216.6 | 4089.5 | |

| 0.028 | 0.031 | 0.026 | 0.019 | 0.029 | 0.032 | 0.083 | 0.050 | 0.060 | 0.017 | 0.086 | 0.061 | 0.095 | 0.022 | 0.031 |

| AUS | BRA | CAN | CHN | FRA | DEU | IND | JPN | KOR | MEX | RUS | ZAF | TUR | GBR | USA | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.430 | 0.454 | 0.450 | 0.469 | 0.406 | 0.400 | 0.390 | 0.398 | 0.395 | 0.449 | 0.419 | 0.402 | 0.492 | 0.435 | 0.430 | |

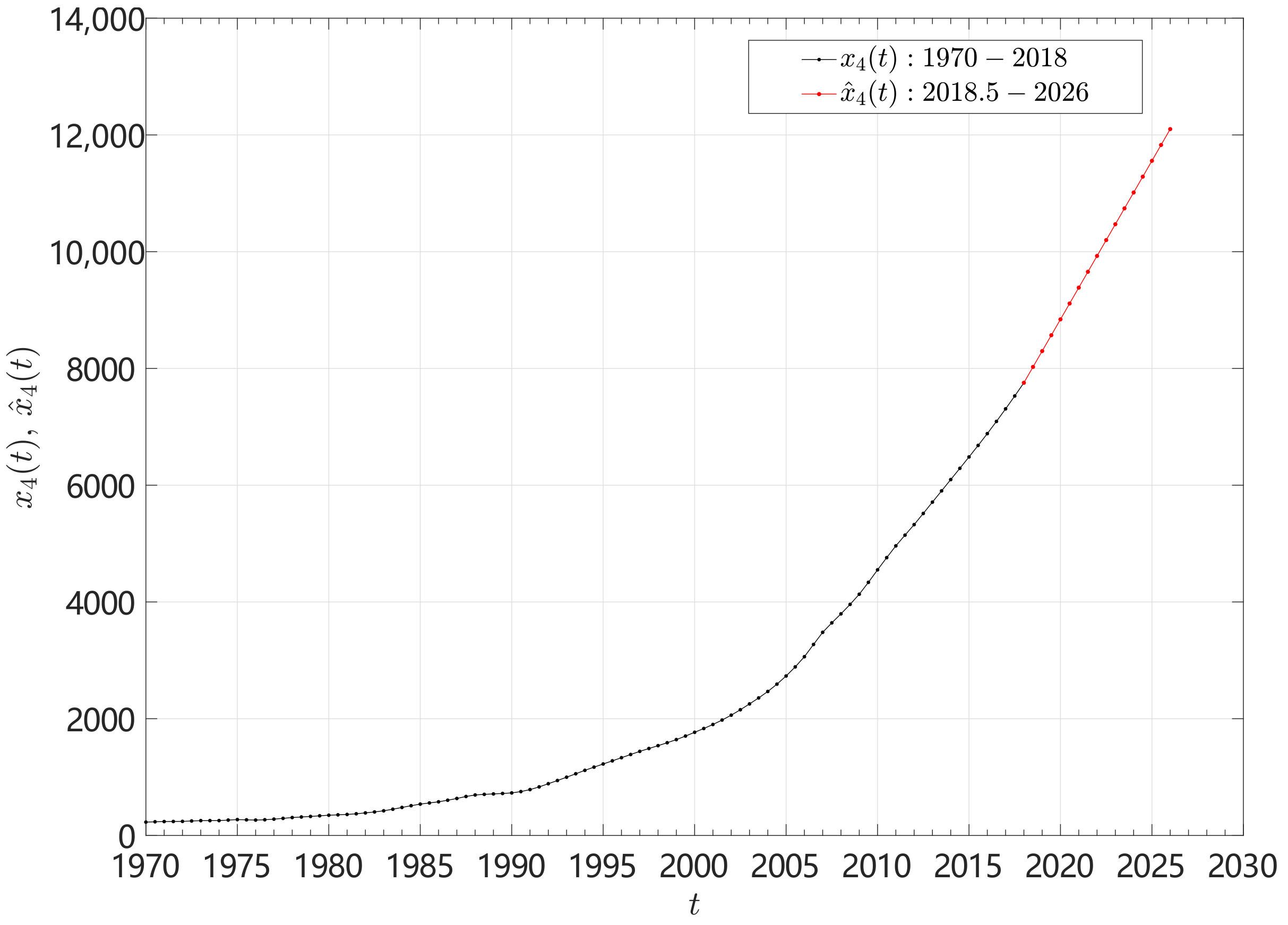

| 2018.5 | 57,908.8 | 11,509.6 | 52,625.9 | 8026.6 | 44,457.5 | 49,163.0 | 2084.8 | 50,188.3 | 27,743.1 | 10,273.7 | 10,915.1 | 7221.4 | 14,975.7 | 43,929.1 | 55,651.7 |

| 2019 | 58,898.2 | 11,992.9 | 53,387.6 | 8298.1 | 45,251.4 | 50,824.2 | 2065.3 | 51,457.0 | 28,724.3 | 9928.3 | 10,385.6 | 7002.8 | 15,469.5 | 44,872.2 | 56,761.7 |

| 2019.5 | 59,887.6 | 12,476.2 | 53,769.9 | 8569.7 | 46,045.3 | 52,449.0 | 2045.9 | 52,725.7 | 29,705.5 | 10,071.7 | 10,728.3 | 6784.3 | 15,741.7 | 45,815.3 | 57,871.6 |

| 2020 | 60,877.1 | 12,959.6 | 54,424.7 | 8841.3 | 46,839.2 | 53,163.3 | 2026.5 | 53,994.4 | 30,686.7 | 10,286.1 | 11,092.5 | 6565.7 | 15,993.1 | 46,758.4 | 58,981.6 |

| 2020.5 | 61,866.5 | 13,362.1 | 55,079.4 | 9112.9 | 47,633.1 | 53,701.7 | 2007.1 | 55,263.2 | 31,667.9 | 10,406.9 | 11,545.3 | 6629.8 | 16,368.9 | 47,701.5 | 60,091.6 |

| 2021 | 62,855.9 | 13,431.3 | 55,593.1 | 9384.5 | 48,427.0 | 53,973.0 | 1992.4 | 56,531.9 | 32,649.1 | 10,515.7 | 12,041.0 | 6710.8 | 16,686.6 | 47,397.5 | 61,000 |

| 2021.5 | 63,845.3 | 13,497.0 | 55,785.7 | 9656.1 | 49,220.9 | 53,947.0 | 2012.9 | 57,800.6 | 33,630.3 | 10,662.1 | 12,566.2 | 6765.2 | 16,809.6 | 47,562.3 | 59,875.8 |

| 2022 | 64,834.7 | 13,662.4 | 55,963.7 | 9927.7 | 50,014.8 | 53,884.5 | 2049.3 | 58,994.7 | 34,611.5 | 10,752.8 | 13,086.0 | 6824.4 | 16,938.8 | 47,831.8 | 58,935 |

| 2022.5 | 65,058.1 | 13,781.4 | 56,268.1 | 10,199.3 | 50,808.7 | 53,658.1 | 2098.5 | 58,961.4 | 35,592.7 | 10,754.4 | 13,533.4 | 6924.8 | 17,436.8 | 48,037.5 | 59,360 |

| 2023 | 65,271.7 | 13,768.1 | 56,665.0 | 10,470.9 | 51,602.6 | 53,474.2 | 2172.2 | 59,226.3 | 36,573.9 | 10,756.0 | 13,774.1 | 7049.4 | 17,912.0 | 48,238.8 | 59,946.1 |

| 2023.5 | 65,553.7 | 13,732.4 | 57,290.6 | 10,742.5 | 52,169.3 | 53,727.3 | 2243.0 | 59,732.2 | 37,555.1 | 10,813.4 | 13,233.9 | 7183.7 | 18,045.4 | 48,408.1 | 60,196.4 |

| 2024 | 65,956.3 | 13,493.9 | 57,706.9 | 11,014.1 | 52,749.4 | 54,107.9 | 2267.5 | 60,358.5 | 38,536.3 | 10,916.1 | 12,696.3 | 7330.1 | 18,100.0 | 48,595.7 | 60,437.7 |

| 2024.5 | 66,662.2 | 13,135.1 | 57,690.3 | 11,285.7 | 53,105.6 | 54,294.2 | 2288.3 | 61,030.6 | 39,517.5 | 11,024.9 | 12,907.5 | 7485.4 | 48,883.4 | 60,871.6 | |

| 2025 | 67,345.2 | 12,795.3 | 57,673.7 | 11,557.2 | 53,060.8 | 54,523.1 | 2322.7 | 61,559.4 | 40,498.7 | 11,136.6 | 13,261.0 | 7643.9 | 49,262.1 | 61,345.8 | |

| 2025.5 | 67,656.5 | 12,596.3 | 57,661.9 | 11,828.8 | 52,942.5 | 55,401.3 | 2357.7 | 62,036.6 | 41,479.9 | 11,239.3 | 13,544.7 | 7810.5 | 49,786.5 | 61,685.6 | |

| 2026 | 67,925.5 | 12,608.7 | 57,655.0 | 12,100.4 | 52,069.1 | 56,601.2 | 2380.1 | 62,462.1 | 42,461.1 | 11,323.9 | 13,820.3 | 7949.7 | 50,333.6 | 62,043.4 | |

| 2026.5 | 68,282.5 | 12,628.1 | 58,110.3 | 51,195.6 | 57,679.8 | 2406.4 | 62,881.9 | 43,442.3 | 11,378.4 | 14,090.5 | 8046.8 | 50,753.3 | 62,526.5 | ||

| 2027 | 68,639.5 | 12,647.4 | 58,672.6 | 51,428.2 | 58,527.7 | 2469.8 | 63,473.8 | 44,423.5 | 11,425.2 | 14,307.1 | 8094.7 | 51,104.7 | 63,099.1 | ||

| 2027.5 | 68,931.3 | 12,670.1 | 58,855.4 | 51,901.3 | 59,035.7 | 2543.5 | 63,847.7 | 45,404.7 | 11,473.6 | 14,459.3 | 7977.9 | 51,387.8 | 63,819.6 | ||

| 2028 | 69,239.4 | 58,936.1 | 52,441.3 | 59,270.6 | 2617.1 | 63,630.8 | 46,385.9 | 11,522.0 | 14,533.6 | 7860.3 | 51,652.7 | 64,441.5 | |||

| 2028.5 | 69,687.7 | 52,780.7 | 57,903.2 | 2690.8 | 63,115.6 | 47,367.1 | 14,481.8 | 7905.0 | 51,949.5 | 64,718.7 | |||||

| 2029 | 70,106.7 | 52,736.0 | 56,535.8 | 2764.5 | 61,522.1 | 48,348.3 | 14,376.4 | 7982.0 | 52,223.6 | 64,977.9 | |||||

| 2029.5 | 70,330.0 | 52,691.2 | 56,940.7 | 2838.2 | 59,928.6 | 49,329.5 | 14,168.9 | 8058.1 | 52,438.4 | 65,425.2 | |||||

| 2030 | 70,550.1 | 52,699.9 | 58,474.4 | 2911.8 | 60,950.7 | 50,310.7 | 14,015.1 | 8119.8 | 52,612.4 | 65,993.4 | |||||

| 2030.5 | 70,923.4 | 52,721.9 | 60,135.6 | 2985.5 | 62,207.9 | 51,291.9 | 14,019.7 | 8145.9 | 66,664.6 | ||||||

| 2031 | 71,417.3 | 52,817.5 | 61,742.2 | 3059.2 | 62,231.9 | 52,273.1 | 14,035.0 | 8168.8 | 67,461.1 | ||||||

| 2031.5 | 52,973.2 | 61,861.7 | 3132.8 | 62,250.2 | 53,254.3 | 14,114.7 | 8207.0 | ||||||||

| 2032 | 53,145.6 | 61,932.8 | 3206.5 | 62,629.9 | 54,235.5 | 14,248.1 | 8238.7 | ||||||||

| 2032.5 | 53,338.1 | 61,991.7 | 3279.4 | 63,284.8 | 55,216.7 | 14,394.9 | 8252.7 | ||||||||

| 2033 | 53,500.4 | 62,068.8 | 3353.1 | 64,043.1 | 56,197.9 | 14,571.2 | 8258.6 | ||||||||

| 2033.5 | 53,709.6 | 62,546.4 | 3426.8 | 64,640.7 | 57,179.1 | 8250.0 | |||||||||

| 2034 | 54,259.6 | 63,151.6 | 3500.5 | 64,813.8 | 58,160.3 | 8230.9 | |||||||||

| 2034.5 | 54,916.5 | 63,429.0 | 3574.1 | 64,969.8 | 59,049.7 | 8185.2 | |||||||||

| 2035 | 55,383.0 | 63,700.3 | 3647.8 | 65,383.8 | 59,799.7 | 8149.9 | |||||||||

| 2035.5 | 55,762.5 | 64,111.2 | 3721.5 | 65,832.3 | 60,609.0 | 8150.2 | |||||||||

| 2036 | 64,601.0 | 3795.1 | 66,062.8 | 61,409.5 | 8149.6 | ||||||||||

| 2036.5 | 65,194.0 | 3868.8 | 66,310.5 | 62,106.2 | 8135.4 | ||||||||||

| 2037 | 65,750.6 | 3942.5 | 66,982.7 | 62,791.0 | 8103.3 | ||||||||||

| 2037.5 | 66,155.4 | 4016.2 | 67,700.8 | 63,547.0 | |||||||||||

| 2038 | 66,469.2 | 4089.8 | 68,114.8 | 64,341.5 | |||||||||||

| 2038.5 | 4163.5 | 68,374.0 | 65,183.4 | ||||||||||||

| 2039 | 4237.2 | 66,028.3 | |||||||||||||

| 2039.5 | 4310.8 | 66,813.9 | |||||||||||||

| 2040 | 4384.5 | 67,566.9 | |||||||||||||

| 2040.5 | 4458.2 | ||||||||||||||

| 2041 | 4531.9 | ||||||||||||||

| 2041.5 | 4605.5 | ||||||||||||||

| 2042 | 4679.2 | ||||||||||||||

| 2042.5 | 4752.9 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tenreiro Machado, J.A.; Mata, M.E.; Lopes, A.M. Fractional Dynamics and Pseudo-Phase Space of Country Economic Processes. Mathematics 2020, 8, 81. https://doi.org/10.3390/math8010081

Tenreiro Machado JA, Mata ME, Lopes AM. Fractional Dynamics and Pseudo-Phase Space of Country Economic Processes. Mathematics. 2020; 8(1):81. https://doi.org/10.3390/math8010081

Chicago/Turabian StyleTenreiro Machado, José A., Maria Eugénia Mata, and António M. Lopes. 2020. "Fractional Dynamics and Pseudo-Phase Space of Country Economic Processes" Mathematics 8, no. 1: 81. https://doi.org/10.3390/math8010081

APA StyleTenreiro Machado, J. A., Mata, M. E., & Lopes, A. M. (2020). Fractional Dynamics and Pseudo-Phase Space of Country Economic Processes. Mathematics, 8(1), 81. https://doi.org/10.3390/math8010081