1. Introduction

Let

be a one-dimensional diffusion process defined by the stochastic differential Equation (see [

1])

where

is a standard Brownian motion. Assume that

and define the

first-hitting time (or

first-passage time)

where we assume that the boundaries at

and

are attainable in finite time. The moment-generating function

where

, of the random variable

satisfies the Kolmogorov backward equation

for

; see, for example, Cox and Miller [

2]. Moreover the boundary conditions are

. Similarly, the function

(if it exists) satisfies the ordinary differential Equation (ODE)

subject to

. Finally, the probability

is a solution of the ODE

and is such that

and

. First-hitting problems have applications in many fields, notably biology and financial mathematics.

In this paper, we consider the stochastic process

defined by

where

is a real function such that

,

,

is a standard Brownian motion process,

is a Poisson process with rate

(which is independent of

), and

are independent and identically distributed random variables. Moreover, we assume that

f is such that

is a jump-diffusion process.

We define the first-hitting time

and we let

where

. It can be shown (see [

3]) that the function

satisfies the integro-differential Equation (IDE) (writing

as

)

where

Y is distributed as the

’s. The boundary conditions are

.

Suppose that

Y has a uniform distribution on the interval

if

and a uniform distribution on the interval

if

. Then, by symmetry, we can write that

, so that we can consider the process in the interval

alone. Moreover, for

,

Hence, Equation (

9) becomes

for

.

Next, let

and

. To obtain these functions, we need to solve the following equations:

subject to the boundary conditions

, and

subject to

and

.

A possible application of the problem studied in this paper is as follows: Suppose that represents the position of an object (an aircraft, for example) at time t. The objective is to make the object in question follow a trajectory that corresponds to . To do this, we correct the trajectory according to a Poisson process, trying to bring the object back to the origin with thrusts that follow a uniform distribution whose mean is , with x being the current position of the object. Note that, by continuity, the probability of a jump from x to 0 is equal to 0. Moreover, because the jumps are instantaneous, if the process jumps from a positive to a negative value (or vice versa), it is assumed that it did not hit the origin.

We will consider the following particular cases for the function :

, so that is a Wiener process with zero drift and with jumps.

, where , so that is an Ornstein–Uhlenbeck process with jumps.

, where

, so that

is a (generalized) Bessel process with jumps. The condition

implies that the process can attain the origin; see [

4].

Remark 1. (i) We used the expression generalized Bessel process, because a Bessel process is non-negative by definition. Therefore, if it reaches the origin, we assume that there is a reflecting (or an absorbing) boundary at . However, a diffusion process that satisfies the stochastic differential equationcan be considered for negative values when . In particular, if , then is a standard Brownian motion, which is a Gaussian process. (ii) The Wiener process, or Brownian motion, is the basic and most important diffusion process. The Ornstein–Uhlenbeck process is also very important for the applications. It was proposed by Uhlenbeck and Ornstein in [5] as a model for the velocity of a particle that is undergoing Brownian motion. The Bessel process was studied extensively in the book by Revuz and Yor [6]. These three diffusion processes are treated in most textbooks on stochastic processes, for instance, in the works of Karlin and Taylor [4] and Lefebvre [7].

Obtaining exact and explicit solutions to boundary value problems for integro-differential equations is a difficult task. The first author has written a number of papers on such problems; see, in particular, refs. [

8,

9]. He also considered optimal control problems known as

homing problems for these processes.

A very important application of jump-diffusion processes is in financial mathematics; in his seminal paper, Merton [

10] used these processes to model the behaviour of stock prices. Other papers on jump-diffusion processes include the following: Abundo [

11,

12], Cai [

13], Peng and Liu [

14], Yin et al. [

15], Zhou and Wu [

16], and Ai et al. [

17].

In [

18], Abundo computed the first-passage area of one-dimensional jump-diffusion processes. Lefebvre [

19] also studied a first-passage-place problem for a one-dimensional jump-diffusion process and its integral.

Jump-diffusion processes are related to diffusion processes with

stochastic resetting, but they are fundamentally different. These processes were first studied by Evans and Majumdar [

20]; see also Abundo [

21] and the references therein. In the case of a diffusion process with resetting times, according to a Poisson process, at random times that follow an exponential distribution, the process is reset instantaneously to a fixed value

and then evolves from this position in accordance with the stochastic differential equation that defines the diffusion process. In contrast, when a jump occurs in a jump-diffusion process, the new position of the process is completely random and (when the jump size distribution is a continuous random variable) can never be the same.

In

Section 2, we will obtain exact analytical expressions for the probability

. We will first transform the IDE in Equation (

13) into a third-order linear ODE. After solving this ODE, subject to two boundary conditions, we will determine the third constant which is such that the solution to the ODE also satisfies the corresponding IDE.

Next, in

Section 3, numerical solutions for the mean

and the moment-generating function

will be presented. We will see the effect of the jumps on the solutions by comparing these functions with the corresponding ones when there are no jumps (that is, when

). Finally, we will end with a few remarks in

Section 4.

2. Ordinary Differential Equations

Differentiating both sides of the IDE in Equation (

11), we obtain (from Leibniz’s integral rule) that

Moreover, from Equation (

11),

Hence, we can state the following proposition.

Proposition 1. The moment-generating function (= ) satisfies, for , the third-order linear ODEfor . Moreover, we have the boundary conditions . Corollary 1. The mean of the random variable satisfies, for , the ODEfor , subject to the boundary conditions . Proof. Assuming that the moments of

exist, we can write that

Substituting the above expression for

into Equation (

17), we deduce from the terms in

that

is such that

which yields Equation (

18). □

Corollary 2. The probability satisfies, for , the ODEfor , and the boundary conditions are and . Remark 2. Equations (18) and (21) are actually second-order linear ODEs for and , respectively. In this section, we will obtain exact analytical solutions to Equation (

21) for the important special cases mentioned in the previous section. First, we take

and

so that the continuous part of the jump-diffusion process

is a Wiener process with zero drift and dispersion parameter equal to 1. Furthermore, for the sake of simplicity, we set

. Equation (

21) then reduces to

Making use of the software program

Maple (version 2020), we find that the solution to the above equation that satisfies the boundary conditions

and

can be written as follows:

where

is an arbitrary constant,

and

are Bessel functions, and StruveL

is the modified Struve function which solves the non-homogeneous Bessel equation

This is defined as follows in Abramowitz and Stegun [

22]:

Moreover, for

, we have (see also [

22])

where

(the Euler–Mascheroni constant

is approximately equal to 0.57721) and

Finally,

To determine the value of the constant

, we can substitute the above expression for the function

into the IDE (

13). The calculations are rather heavy. We find that we must take

. Hence, we have the following proposition.

Proposition 2. The probability when and is given byfor . When there are no jumps (that is,

), the function

satisfies the elementary ODE

The solution that satisfies the boundary conditions

and

is the straight line

. The functions

and

are shown in

Figure 1. We see the effect of the jumps on the probability of absorption at the origin as follows: jumps increase the value of this probability, which is logical since jumps bring the process from its current position

x to a random value whose mathematical expectation is equal to zero.

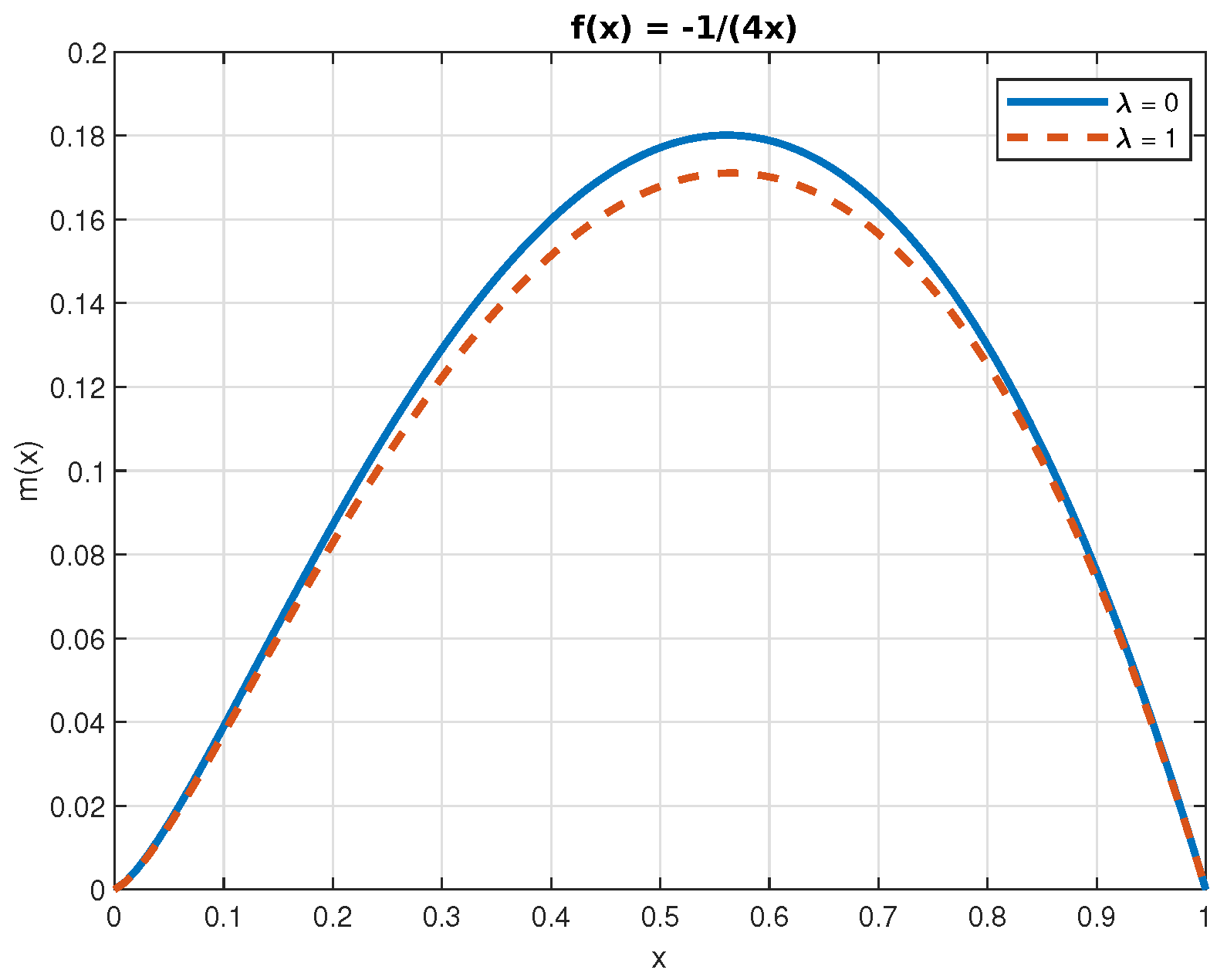

Next, we replace the function

by

, where

. This time, the continuous part of

is an Ornstein–Uhlenbeck process, which is a very important diffusion process for these applications. Equation (

21) becomes (with

)

The general solution of this ODE can be expressed in terms of the Meijer G function and a generalized hypergeometric function. In the special case when

, we find (with the help of

Maple) that

where

is a Bessel function which can be defined as follows for

:

The above function is such that

and

. Contrary to the previous case, we cannot set

equal to zero. We could substitute this expression into the IDE (

13) and try to determine the constant

for which the IDE is satisfied. We can also proceed as follows: The unique solution to Equation (

32) that satisfies the three conditions

,

and

is

Substituting this function into Equation (

13), we find that the constant

r is approximately equal to 0.676.

Proposition 3. The function when and is given byfor . Remark 3. Making use of Maple’s evalf function, we can rewrite the function as follows: With

, we must solve the ODE

We find that

where erf

is the error function defined by

Figure 2 presents the functions

and

in the interval

.

Finally, we consider the jump-diffusion process defined by

where

. As mentioned above, the continuous part of

is a Bessel process that can attain the origin. Since the origin is actually a

regular boundary for this process (see [

4]), we can consider it in the interval

. The Bessel process plays an important role in financial mathematics.

Let us take

and

. In the absence of jumps, the function

satisfies the ODE

With

and

, we find that

When

, we must solve the third-order linear ODE

The software program

Maple provides the following solution that is such that

,

and

:

where

and

hypergeom is the generalized hypergeometric function, which is defined in

Maple by

with

The generalized hypergeometric function is often denoted by

. Using this notation, we would write

etc.

When we substitute the function

defined in Equation (

45) into Equation (

13), we find that the IDE is satisfied if we take

.

Proposition 4. The probability when and is the function given in Equation (45) for , with . The functions

and

in the interval

are displayed in

Figure 3.

As we have seen in this section, the problem of calculating the probability , which is straightforward in the case of diffusion processes without jumps, becomes very difficult when jumps according to a Poisson process are added. In the next section, we will use numerical methods to obtain the mean of the random variable and its moment-generating function .

4. Discussion

To obtain more realistic models, many authors nowadays add jumps to diffusion processes according to a Poisson process such as a Brownian motion process. From a mathematical point of view, this entails that problems such as calculating the characteristics of random variables called first-hitting times become much more difficult.

Indeed, as we have seen in this paper, rather than solving linear ordinary differential equations, the introduction of jumps whose size is a continuous random variable implies that we now have to solve integro-differential equations.

In this paper, we considered such a problem in the case when the jump size is uniformly distributed on the interval (when ), where x is the current value of the process. We were able to obtain exact analytical expressions, in terms of special functions, for the probability that the jump-diffusion process will hit the origin before a barrier at . Three particular cases for the continuous part of were treated. These three cases are among the most important ones for applications.

In

Section 3, we presented numerical solutions to the integro-differential equations that must be solved, subject to the appropriate boundary conditions, to obtain the mean and the moment-generating function of the first-hitting time of interest.

There are still few papers with explicit results for this type of problem. Here, we were able to transform the integro-differential equations into third-order ordinary differential equations. These equations are linear, but with non-constant coefficients. Therefore, their solutions are often quite intricate. Moreover, even if we are able to solve them explicitly, we still have to substitute the solutions into the original integro-differential equations to determine the value of the third arbitrary constant in the general solutions.

The main difficulty in obtaining explicit and exact analytical results for the type of problems studied in this paper is thus solving the ODEs. We were able to do this for the function , but in the case of the functions and , we had to resort to numerical methods.

As a continuation of this work, we could consider jump-diffusion processes in two or more dimensions. Sometimes, by using symmetry, it is possible to reduce these problems to one-dimensional problems. Another possibility would be to consider jumps whose size is a discrete, rather than a continuous, random variable. In this case, instead of integro-differential equations, we would have to solve difference-differential equations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}