Quantile Dependence between Crude Oil Returns and Implied Volatility: Evidence from Parametric and Nonparametric Tests

Abstract

1. Introduction

2. Literature Review

3. Methodology

3.1. Quantile Unit Root Test

3.2. Granger Causality in Quantiles

3.3. The Cross-Quantilogram

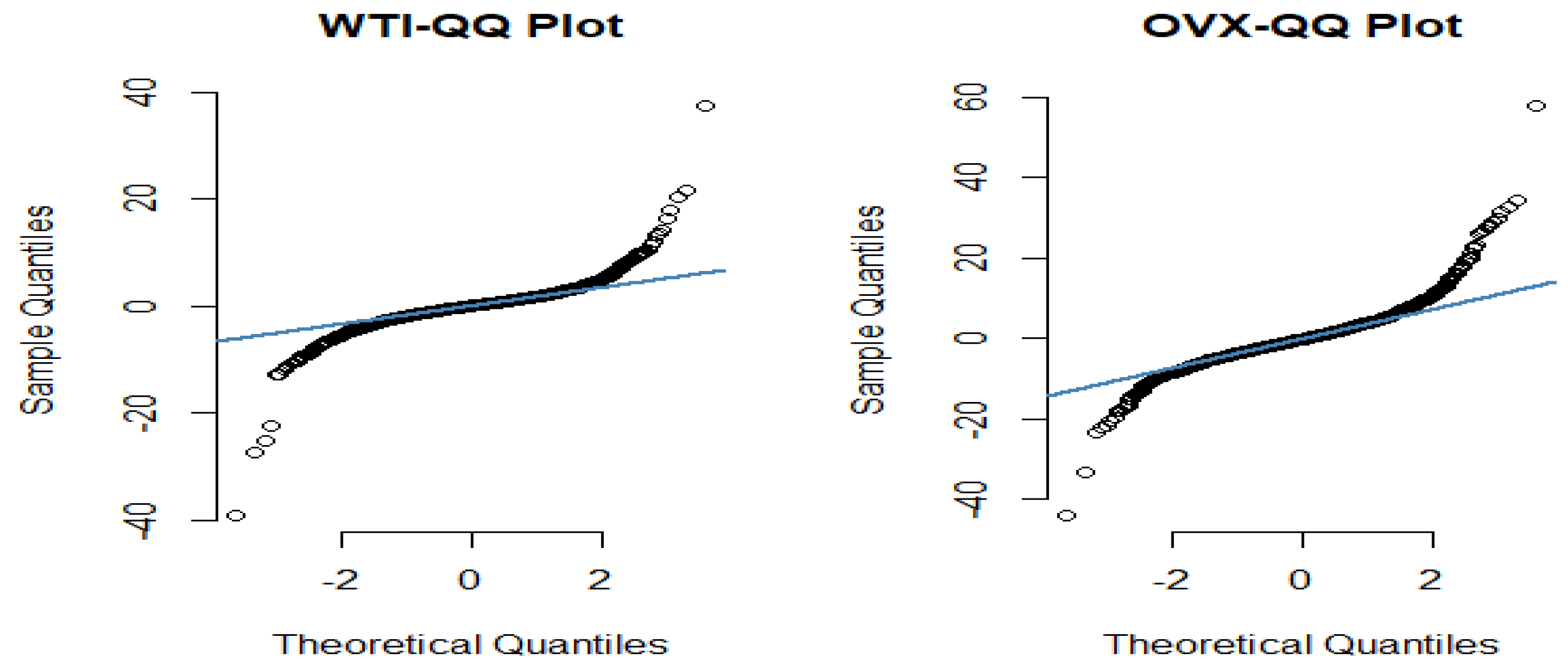

4. Data and Preliminary Analysis

4.1. Data Description

4.2. Unit Root Testing

4.3. Testing for Cointegration

5. Empirical Results

5.1. Granger Causality Test Results

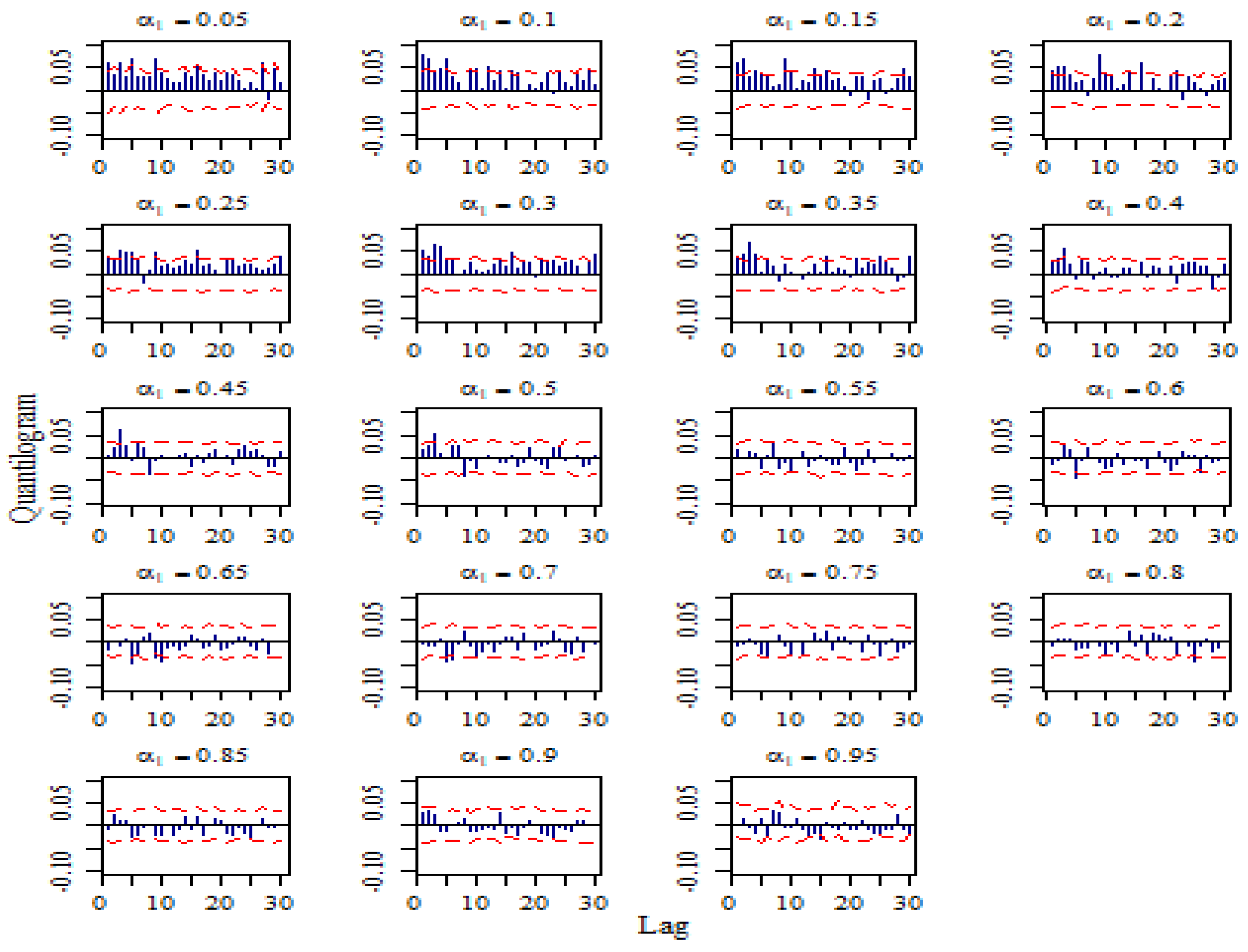

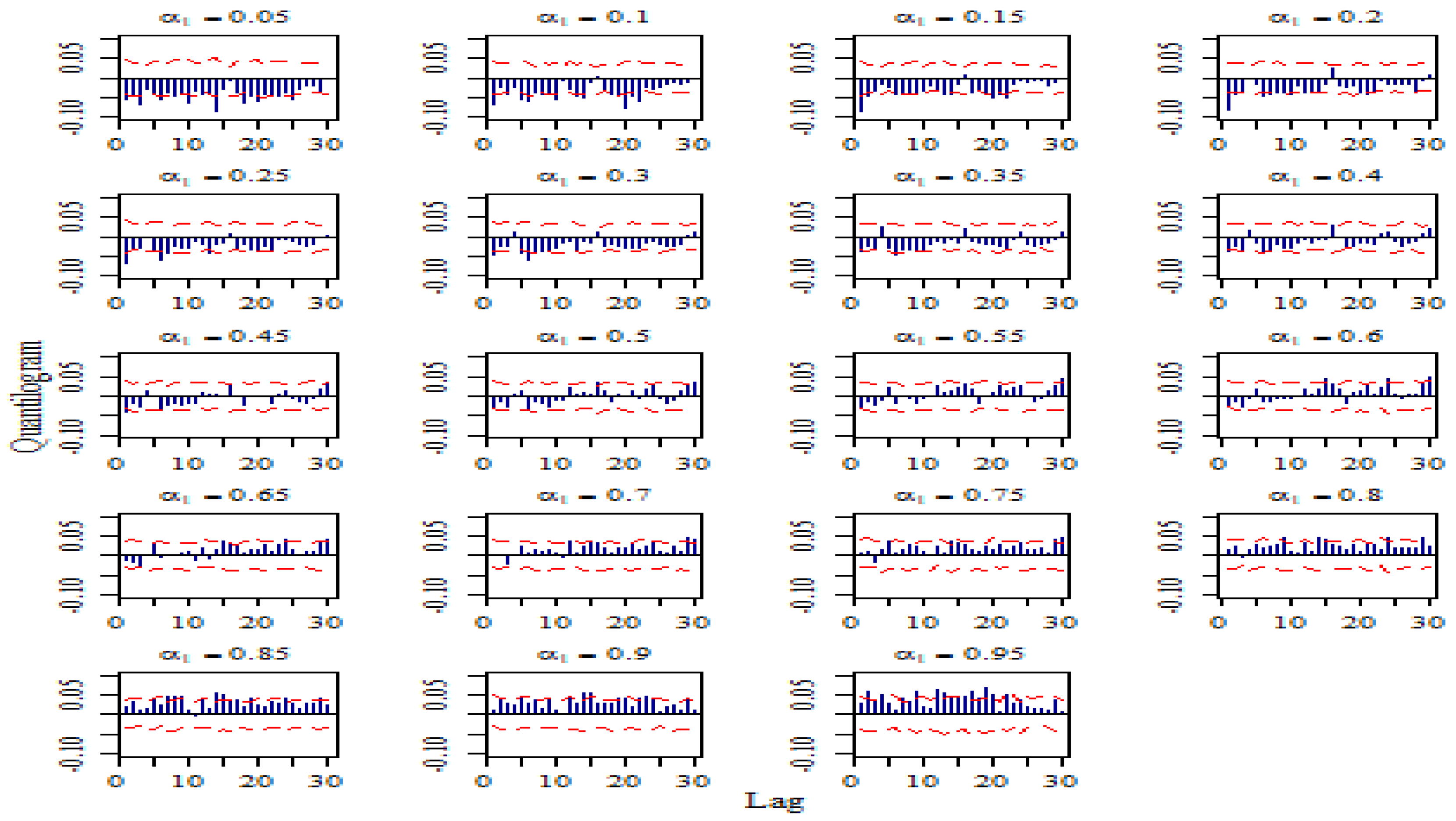

5.2. Cross-Quantilogram Analysis

5.2.1. Results When Both Return Series Are in the Same Quantiles

5.2.2. Results When the Return Series Are in Opposite Quantiles

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Aguilera, R.F.; Eggert, R.G.; CC, G.L.; Tilton, J.E. Depletion and the future availability of petroleum resources. Energy J. 2009, 30, 141–174. [Google Scholar] [CrossRef]

- Demirbas, A.; Omar Al-Sasi, B.; Nizami, A.S. Recent volatility in the price of crude oil. Energy Sources Part B Econ. Plan. Policy 2017, 12, 408–414. [Google Scholar] [CrossRef]

- Joo, Y.C.; Park, S.Y. Oil prices and stock markets: Does the effect of uncertainty change over time? Energy Econ. 2017, 61, 42–51. [Google Scholar] [CrossRef]

- Bouri, E.; Demirer, R.; Gupta, R.; Pierdzioch, C. Infectious diseases, market uncertainty and oil market volatility. Energies 2020, 13, 4090. [Google Scholar] [CrossRef]

- Dutta, A.; Bouri, E.; Noor, M.H. Climate bond, stock, gold, and oil markets: Dynamic correlations and hedging analyses during the COVID-19 outbreak. Resour. Policy 2021, 74, 102265. [Google Scholar] [CrossRef] [PubMed]

- Diaz, E.M.; Molero, J.C.; Perez de Gracia, F. Oil price volatility and stock returns in the G7 economies. Energy Econ. 2016, 54, 417–430. [Google Scholar] [CrossRef]

- Luo, X.; Qin, S. Oil price uncertainty and Chinese stock returns: New evidence from the oil volatility index. Finance Res. Lett. 2017, 20, 29–34. [Google Scholar] [CrossRef]

- Kinateder, H.; Wagner, N. Oil and Stock Market Returns: Direction, Volatility, or Liquidity? SSRN Electron. J. 2017. [Google Scholar] [CrossRef]

- Batten, J.A.; Kinateder, H.; Szilagyi, P.G.; Wagner, N.F. Liquidity, surprise volume and return premia in the oil market. Energy Econ. 2019, 77, 93–104. [Google Scholar] [CrossRef]

- Szakmary, A.; Ors, E.; Kyoung Kim, J.; Davidson, W.N. The predictive power of implied volatility: Evidence from 35 futures markets. J. Bank. Finance 2003, 27, 2151–2175. [Google Scholar] [CrossRef]

- Becker, R.; Clements, A.E.; White, S.I. Does implied volatility provide any information beyond that captured in model-based volatility forecasts? J. Bank. Finance 2007, 31, 2535–2549. [Google Scholar] [CrossRef]

- Mencía, J.; Sentana, E. Valuation of VIX derivatives. J. Finance Econ. 2013, 108, 367–391. [Google Scholar] [CrossRef]

- Liu, Z.; Tseng, H.K.; Wu, J.S.; Ding, Z. Implied volatility relationships between crude oil and the U.S. stock markets: Dynamic correlation and spillover effects. Resour. Policy 2020, 66, 101637. [Google Scholar] [CrossRef]

- Dutta, A.; Bouri, E.; Saeed, T. News-based equity market uncertainty and crude oil volatility. Energy 2021, 222, 119930. [Google Scholar] [CrossRef]

- Lanne, M.; Saikkonen, P. Modeling the U.S. Short-Term Interest Rate by Mixture Autoregressive Processes. SSRN Electron. J. 2005, 1, 96–125. [Google Scholar] [CrossRef]

- Ali, F.D.; Bin, L.; Leqin, W. Revisiting the risk-return relation in the South African stock market. Afr. J. Bus. Manag. 2012, 6, 11411–11415. [Google Scholar] [CrossRef]

- Chang, K.L. Does the return-state-varying relationship between risk and return matter in modeling the time series process of stock return? Int. Rev. Econ. Finance 2016, 42, 72–87. [Google Scholar] [CrossRef]

- Aslanidis, N.; Christiansen, C.; Savva, C.S. Risk-return trade-off for European stock markets. Int. Rev. Finance Anal. 2016, 46, 84–103. [Google Scholar] [CrossRef]

- Abakah, E.J.A.; Tiwari, A.K.; Alagidede, I.P.; Gil-Alana, L.A. Re-examination of risk-return dynamics in international equity markets and the role of policy uncertainty, geopolitical risk and VIX: Evidence using Markov-switching copulas. Finance Res. Lett. 2022, 47, 102535. [Google Scholar] [CrossRef]

- Lundblad, C. The risk return tradeoff in the long run: 1836–2003. J. Finance Econ. 2007, 85, 123–150. [Google Scholar] [CrossRef]

- Liu, B.; Ji, Q.; Fan, Y. Dynamic return-volatility dependence and risk measure of CoVaR in the oil market: A time-varying mixed copula model. Energy Econ. 2017, 68, 53–65. [Google Scholar] [CrossRef]

- Wu, S.-J.; Lee, W.-M. Intertemporal risk–return relationships in bull and bear markets. Int. Rev. Econ. Finance 2015, 38, 308–325. [Google Scholar] [CrossRef]

- Glosten, L.R.; Jagannathan, R.; Runkle, D.E.; Breen, W.; Hansen, L.; Hess, P.; Hsieh, D.; Judson, R.; Kocher-Lakota, N.; Mcdonald, R.; et al. On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks. J. Finance 1993, 48, 1779–1801. [Google Scholar] [CrossRef]

- Bollerslev, T.; Osterrieder, D.; Sizova, N.; Tauchen, G. Risk and return: Long-run relations, fractional cointegration, and return predictability. J. Finance Econ. 2013, 108, 409–424. [Google Scholar] [CrossRef]

- Chen, M. Risk-return tradeoff in Chinese stock markets: Some recent evidence. Int. J. Emerg. Mark. 2015, 10, 448–473. [Google Scholar] [CrossRef]

- Basher, S.A.; Sadorsky, P. Hedging emerging market stock prices with oil, gold, VIX, and bonds: A comparison between DCC, ADCC and GO-GARCH. Energy Econ. 2016, 54, 235–247. [Google Scholar] [CrossRef]

- Ji, Q.; Fan, Y. Modelling the joint dynamics of oil prices and investor fear gauge. Res. Int. Bus. Finance 2016, 37, 242–251. [Google Scholar] [CrossRef]

- Haugom, E.; Langeland, H.; Molnár, P.; Westgaard, S. Forecasting volatility of the U.S. oil market. J. Bank. Finance 2014, 47, 1–14. [Google Scholar] [CrossRef]

- Lux, T.; Segnon, M.; Gupta, R. Forecasting crude oil price volatility and value-at-risk: Evidence from historical and recent data. Energy Econ. 2016, 56, 117–133. [Google Scholar] [CrossRef]

- Dutta, A. Modeling and forecasting oil price risk: The role of implied volatility index. J. Econ. Stud. 2017, 44, 1003–1016. [Google Scholar] [CrossRef]

- Lv, W. Does the OVX matter for volatility forecasting? Evidence from the crude oil market. Phys. A Stat. Mech. Its Appl. 2018, 492, 916–922. [Google Scholar] [CrossRef]

- Chen, H.; Liu, L.; Li, X. The predictive content of CBOE crude oil volatility index. Phys. A Stat. Mech. Its Appl. 2018, 492, 837–850. [Google Scholar] [CrossRef]

- Benedetto, F.; Mastroeni, L.; Quaresima, G.; Vellucci, P. Does OVX affect WTI and Brent oil spot variance? Evidence from an entropy analysis. Energy Econ. 2020, 89, 104815. [Google Scholar] [CrossRef]

- Maghyereh, A.I.; Awartani, B.; Bouri, E. The directional volatility connectedness between crude oil and equity markets: New evidence from implied volatility indexes. Energy Econ. 2016, 57, 78–93. [Google Scholar] [CrossRef]

- Bouri, E.; Jain, A.; Biswal, P.C.; Roubaud, D. Cointegration and nonlinear causality amongst gold, oil, and the Indian stock market: Evidence from implied volatility indices. Resour. Policy 2017, 52, 201–206. [Google Scholar] [CrossRef]

- Choi, S.Y.; Hong, C. Relationship between uncertainty in the oil and stock markets before and after the shale gas revolution: Evidence from the OVX, VIX, and VKOSPI volatility indices. PLoS ONE 2020, 15, e0232508. [Google Scholar] [CrossRef] [PubMed]

- Naeem, M.A.; Hasan, M.; Agyemang, A.; Chowdhury, M.I.H.; Balli, F. Time-frequency dynamics between fear connectedness of stocks and alternative assets. Int. J. Finance Econ. 2021, 1–14. [Google Scholar] [CrossRef]

- Aboura, S.; Chevallier, J. Leverage vs. feedback: Which effect drives the oil market? Finance Res. Lett. 2013, 10, 131–141. [Google Scholar] [CrossRef]

- Chen, Y.; He, K.; Yu, L. The Information Content of OVX for Crude Oil Returns Analysis and Risk Measurement: Evidence from the Kalman Filter Model. Ann. Data Sci. 2015, 2, 471–487. [Google Scholar] [CrossRef]

- Lin, J.B.; Tsai, W. The relations of oil price change with fear gauges in global political and economic environment. Energies 2019, 12, 2982. [Google Scholar] [CrossRef]

- Agbeyegbe, T.D. An inverted U-shaped crude oil price return-implied volatility relationship. Rev. Finance Econ. 2015, 27, 28–45. [Google Scholar] [CrossRef]

- Echaust, K.; Just, M. Tail dependence between crude oil volatility index and WTI oil price movements during the COVID-19 pandemic. Energies 2021, 14, 4147. [Google Scholar] [CrossRef]

- Li, S.; Li, J.; Lu, X.; Sun, Y. Exploring the dynamic nonlinear relationship between crude oil price and implied volatility indices: A new perspective from MMV-MFDFA. Phys. A Stat. Mech. Its Appl. 2022, 603, 127684. [Google Scholar] [CrossRef]

- Shaikh, I. The relation between implied volatility index and crude oil prices. Eng. Econ. 2019, 30, 556–566. [Google Scholar] [CrossRef]

- Silva, J.C.A., Jr. An S-Shaped Crude Oil Price Return-Implied Volatility Relation: Parametric and Nonparametric Estimations. Int. J. Econ. Finance 2017, 9, 54. [Google Scholar] [CrossRef]

- Fousekis, P. Crude oil price and implied volatility: Insights from non-parametric quantile regressions. Stud. Econ. Finance 2019, 36, 168–182. [Google Scholar] [CrossRef]

- Galvao, A.F. Unit root quantile autoregression testing using covariates. J. Econom. 2009, 152, 165–178. [Google Scholar] [CrossRef]

- Troster, V. Testing for Granger-causality in quantiles. Econom. Rev. 2018, 37, 850–866. [Google Scholar] [CrossRef]

- Han, H.; Linton, O.; Oka, T.; Whang, Y. The Cross-Quantilogram: Measuring Quantile Dependence and Testing Directional Predictability between Time Series. J. Econom. 2016, 193, 251–270. [Google Scholar] [CrossRef]

- Yang, M. Journal of Economic Dynamics & Control The risk return relationship: Evidence from index returns and realised variances. J. Econ. Dyn. Control 2019, 107, 103732. [Google Scholar] [CrossRef]

- Agnolucci, P. Volatility in crude oil futures: A comparison of the predictive ability of GARCH and implied volatility models. Energy Econ. 2009, 31, 316–321. [Google Scholar] [CrossRef]

- Herrera, A.M.; Karaki, M.B. The effects of oil price shocks on job reallocation. J. Econ. Dyn. Control. 2015, 61, 95–113. [Google Scholar] [CrossRef]

- Herrera, A.M.; Karaki, M.B.; Rangaraju, S.K. Where do jobs go when oil prices drop? Energy Econ. 2017, 64, 469–482. [Google Scholar] [CrossRef]

- Karaki, M.B. Nonlinearities in the response of real GDP to oil price shocks. Econ. Lett. 2017, 161, 146–148. [Google Scholar] [CrossRef]

- Bahel, E.; Marrouch, W.; Gaudet, G. The economics of oil, biofuel and food commodities. Resour. Energy Econ. 2013, 35, 599–617. [Google Scholar] [CrossRef]

- Ma, F.; Wahab, M.I.M.; Huang, D.; Xu, W. Forecasting the realized volatility of the oil futures market: A regime switching approach. Energy Econ. 2017, 67, 136–145. [Google Scholar] [CrossRef]

- Chen, Y.; Zou, Y. Examination on the Relationship between OVX and Crude Oil Price with Kalman Filter. Procedia Comput. Sci. 2015, 55, 1359–1365. [Google Scholar] [CrossRef]

- Raggad, B. Can implied volatility predict returns on oil market? Evidence from Cross-Quantilogram Approach. Resour. Policy 2023, 80, 103277. [Google Scholar] [CrossRef]

- Koenker, R.; Xiao, Z. Unit root quantile autoregression inference. J. Am. Stat. Assoc. 2004, 99, 775–787. [Google Scholar] [CrossRef]

- Troster, V.; Shahbaz, M.; Uddin, G.S. Renewable energy, oil prices, and economic activity: A Granger-causality in quantiles analysis. Energy Econ. 2018, 70, 440–452. [Google Scholar] [CrossRef]

- Ye, C.; Chen, Y.; Inglesi-Lotz, R.; Chang, T. CO2 emissions converge in China and G7 countries? Further evidence from Fourier quantile unit root test. Energy Environ. 2020, 31, 348–363. [Google Scholar] [CrossRef]

- Sakov, A.; Bickel, P.J. An Edgeworth expansion for the m out of n bootstrapped median. Stat. Probab. Lett. 2000, 49, 217–223. [Google Scholar] [CrossRef]

- Broock, W.A.; Scheinkman, J.A.; Dechert, W.D.; LeBaron, B. A test for independence based on the correlation dimension. Econom. Rev. 1996, 15, 197–235. [Google Scholar] [CrossRef]

- Bai, J.; Perron, P. Computation and analysis of multiple structural change models. J. Appl. Econom. 2003, 18, 1–22. [Google Scholar] [CrossRef]

- Dickey, D.A.; Fuller, W.A. Distribution of the Estimators for Autoregressive Time Series with a Unit Root. J. Am. Stat. Assoc. 1979, 74, 427–431. [Google Scholar] [CrossRef]

- Phillips, P.C.B.; Perron, P. Testing for a unit root in time series regression. Biometrika 1988, 75, 335–346. [Google Scholar] [CrossRef]

- Zivot, E.; Andrews, D.W.K. Further evidence on the Great Crash, the oil-price shock, and the and Unit-Root hypothesis. J. Bus. Econ. Stat. 1992, 10, 251–270. [Google Scholar]

- Johansen, S. Estimation and Hypothesis Testing of Cointegration Vectors in Gaussian Vector Autoregressive Models. Econometrica 1991, 59, 1551–1580. [Google Scholar] [CrossRef]

- Johansen, S. Likelihood-Based Inference in Cointegrated Vector Autoregressive Models; Oxford University Press: Oxford, UK, 1995. [Google Scholar]

- Xiao, Z. Quantile cointegrating regression. J. Econom. 2009, 150, 248–260. [Google Scholar] [CrossRef]

- Lin, J.B.; Liang, C.C.; Tsai, W. Nonlinear relationships between oil prices and implied volatilities: Providing more valuable information. Sustainability 2019, 11, 3906. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| WTI | OVX | |

|---|---|---|

| Mean | −0.036 | 0.037 |

| Median | 0.053 | −0.27 |

| Maximum | 37.474 | 57.821 |

| Minimum | −39.087 | −43.991 |

| Std. Dev. | 2.747 | 4.938 |

| Skewness | -0.402 | 1.057 |

| Kurtosis | 35.974 | 16.026 |

| Jarque-Bera | 153,031.3 *** | 24,497.87 *** |

| Ljung–Box | 85.20 *** | 51.134 *** |

| Observations | 3376 | 3376 |

| Correlation | −0.325 *** | |

| m | WTI | OVX |

|---|---|---|

| 2 | 0.029 *** | 0.018 *** |

| 3 | 0.056 *** | 0.033 *** |

| 4 | 0.074 *** | 0.04 *** |

| 5 | 0.083 *** | 0.045 *** |

| 6 | 0.087 *** | 0.046 *** |

| 2 | 0.029 *** | 0.018 *** |

| OVX | WTI | |

|---|---|---|

| ADF Test | −59.922 *** | −62.137 *** |

| PP Test | −60.180 *** | −62.107 *** |

| ZA Test | −36.084 *** | −29.688 *** |

| WTI | OVX | |||||

|---|---|---|---|---|---|---|

| T-Stat | CV | T-Stat | CV | |||

| 0.05 | 0.047 | −10.595 | −3.37 | −0.154 | −23.545 | −2.31 |

| 0.1 | 0.031 | −19.564 | −3.35 | −0.111 | −42.006 | −2.31 |

| 0.15 | 0.049 | −25.391 | −3.293 | −0.092 | −48.172 | −2.31 |

| 0.2 | 0.075 | −29.558 | −3.236 | −0.055 | −55.28 | −2.313 |

| 0.25 | 0.065 | −34.652 | −3.236 | −0.047 | −60.029 | −2.385 |

| 0.3 | 0.038 | −38.02 | −3.208 | −0.039 | −62.469 | −2.53 |

| 0.35 | 0.023 | −43.397 | −3.195 | −0.041 | −63.142 | −2.588 |

| 0.4 | 0.015 | −47.051 | −3.136 | −0.03 | −65.601 | −2.65 |

| 0.45 | 0.011 | −48.649 | −3.073 | −0.029 | −67.283 | −2.644 |

| 0.5 | −0.002 | −51.437 | −3.07 | −0.024 | −65.054 | −2.704 |

| 0.55 | −0.012 | −53.711 | −3.066 | −0.02 | −62.884 | −2.742 |

| 0.6 | −0.01 | −52.972 | −3.01 | 0.007 | −59.946 | −2.854 |

| 0.65 | −0.023 | −51.49 | −2.964 | 0.016 | −54.166 | −2.895 |

| 0.7 | −0.044 | −49.292 | −2.884 | 0.018 | −49.539 | −2.888 |

| 0.75 | −0.067 | −45.158 | −2.764 | 0.038 | −45.41 | −2.902 |

| 0.8 | −0.092 | −39.279 | −2.575 | 0.067 | −41.718 | −2.901 |

| 0.85 | −0.121 | −34.714 | −2.491 | 0.052 | −38.062 | −2.914 |

| 0.9 | −0.168 | −28.373 | −2.31 | 0.088 | −22.758 | −3.036 |

| 0.95 | −0.149 | −13.036 | −2.31 | 0.075 | −7.644 | −3.154 |

| Panel A: Johansen Linear Cointegration Test | |||||

| Trace statistic H0: rank = 0 (15.41) | Max. eigenvalue statistic H0: rank = 0 (14.07) | ||||

| WTI-OVX | 20.202 (**) | 18.992 (**) | |||

| Panel B: Quantile Cointegration Test | |||||

| model | coefficient | critical values | |||

| 1% | 5% | 10% | |||

| WTI versus OVX | beta | 7406.825 (***) | 250.470 | 141.558 | 115.485 |

| gamma | 935.6308 (***) | 20.814 | 13.542 | 9.543 | |

| Number of Lags | |||

|---|---|---|---|

| 1 | 2 | 3 | |

| : WTI does not Granger-cause OVX | 0.341 | 0.35 | 0.441 |

| : OVX does not Granger-cause WTI | 0.00 ** | 0.001 ** | 0.002 ** |

| WTI to OVX | OVX to WTI | |||||

|---|---|---|---|---|---|---|

| Number of Lags | Number of Lags | |||||

| Quantiles | 1 | 2 | 3 | 1 | 2 | 3 |

| 0.05 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.1 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.15 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.2 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.25 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.3 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.35 | 0.0003 | 0.0003 | 0.0003 | 0.0151 | 0.0031 | 0.0031 |

| 0.4 | 0.1624 | 0.1445 | 0.3552 | 0.3417 | 0.7967 | 0.7699 |

| 0.45 | 0.2597 | 0.3121 | 0.1673 | 0.0034 | 0.0111 | 0.0089 |

| 0.5 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.55 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.6 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.65 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.7 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.75 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.8 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.85 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.9 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 | 0.0003 |

| 0.95 | 0.0086 | 0.0062 | 0.0123 | 0.9356 | 1 | 1 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Raggad, B.; Bouri, E. Quantile Dependence between Crude Oil Returns and Implied Volatility: Evidence from Parametric and Nonparametric Tests. Mathematics 2023, 11, 528. https://doi.org/10.3390/math11030528

Raggad B, Bouri E. Quantile Dependence between Crude Oil Returns and Implied Volatility: Evidence from Parametric and Nonparametric Tests. Mathematics. 2023; 11(3):528. https://doi.org/10.3390/math11030528

Chicago/Turabian StyleRaggad, Bechir, and Elie Bouri. 2023. "Quantile Dependence between Crude Oil Returns and Implied Volatility: Evidence from Parametric and Nonparametric Tests" Mathematics 11, no. 3: 528. https://doi.org/10.3390/math11030528

APA StyleRaggad, B., & Bouri, E. (2023). Quantile Dependence between Crude Oil Returns and Implied Volatility: Evidence from Parametric and Nonparametric Tests. Mathematics, 11(3), 528. https://doi.org/10.3390/math11030528