1. Introduction

A number of recent events, including the COVID-19 outbreak in 2019, the Second Nagorno–Karabakh War in 2020, and the ongoing Russia–Ukraine conflict in 2022 have caused massive supply-side disruptions in the Asian thermal coal market. Due to the persistently strong demand and limited supply amidst the ongoing coal crises, the Newcastle coal benchmark index surged over 150% compared to the previous year, surpassing the USD 400 per tonne threshold in December 2022. Likewise, the price of the spot physical coal at Newcastle Port in Australia was USD

per ton, an all-time high in September 2022 [

1]. The crises, as mentioned earlier, can potentially jeopardize the cement industry, which is already engulfed in crisis, thus affecting the price and availability of cement in all local markets across the globe. Industry experts believe cement is a major component in infrastructural growth, like roads, bridges, dams, buildings, canals, and houses. Interestingly, the cement market globally is expected to grow at a CAGR of 5.1% between 2022 and 2029, from USD 340.61 billion in 2022 to USD 481.73 billion by 2029 [

2]. Moreover, the consumption of cement indicates how any nation marks its progress. Thus, any potential disruptions in the cement industry are troublesome for the entire economy of a nation.

Comparable to the current cement crisis, modern industrial history reports various other instances of the devastating impacts of supply-side disruptions that are caused by a lack of robustness and resiliency in existing organizational strategies [

3]. For example, Samsung, in 2017, had to stop the production lines of the highly popular Galaxy Note 7 because of the defectiveness of the batteries, which were delivered by its supplier [

4]. At that time, Hurricane Harvey unleashed its fury upon the Gulf Coast in August 2017, upending the lives of over 13 million individuals across Texas, Louisiana, Mississippi, Tennessee, and Kentucky. The aftermath of this catastrophe resulted in an astounding economic loss of approximately USD 180 billion. Similar events have reverberated across the globe, underscoring the vulnerability of our interconnected world. Think of Hurricane Maria’s devastating onslaught in 2017, the seismic upheaval, and tsunamis that rocked Indonesia in 2018, and more [

5]. These incidents not only exact a toll on lives and livelihoods but also spark an urgent demand for recovery efforts. One crucial resource that emerges as a linchpin in the recovery process is cement. This versatile building material is essential in rebuilding shattered communities and infrastructure. However, these dire circumstances frequently trigger disruptions in the supply chain. Earthquakes, floods, transportation hiccups, and even employee strikes also compound the challenges, leading to critical shortages.

In 2020, the BCI report found that a significant number of organizations lacked comprehensive business continuity plans. Among these, a staggering 73% had faced severe disruptions in their supply chains due to the impact of COVID-19, ultimately resulting in their financial collapse [

6]. Consequently, a current statistic reveals that 20% of these managers have opted to maintain higher inventory levels to mitigate potential future disruptions. Additionally, 27% are actively enhancing their supplier networks to guarantee the uninterrupted delivery of ordered goods [

7]. Very recently, amidst escalating global tensions such as Russia’s invasion of Ukraine and China’s persistent threat to take over Taiwan by force, Intel Corp. has strategically unveiled plans to invest over USD 50 billion in new semiconductor manufacturing facilities across Poland, Germany, and Israel. Recognizing the precarious geopolitical landscape, Intel is placing its bets on establishing manufacturing plants in multiple countries as a protective measure against potential disruptions [

8]. By expanding its operations across these diverse locations, Intel aims to fortify its supply chain resilience. Intel’s substantial investments and strategic maneuvering reflect its proactive stance in safeguarding its operations against external disruptions. Typically, these external disruptions are unpredictable yet occasional events that are caused by natural disasters, political instability, labour unrest, industrial accidents, the advent of pandemic diseases, etc. [

9]. This study focuses solely on the supply-side-disruption-related crises of cement retailers that result from shortages of input materials, machinery breakdowns, and soaring input costs and continue for a random duration.

On the other hand, the rapidly fluctuating demand rate is among the major concerns of cement retailers [

10]. For example, the demand for cement bags improves in the June quarter (i.e., before the rainy season) and slows down during the rainy season owing to sluggish construction activities during the latter. Moreover, several local factors, such as the use of cement in industries, the construction of large urban housing complexes, and elections, greatly affect the demand for cement bags at local retailers. In the case of selling-price-dependent demand, there has also been a significant role of deterioration [

11]. Together with fluctuating demand, cement retailers need to consider the probable number of sequential supply failures that lead to a rapid increase in the inventory lead time from zero (the normal business scenario) to multiplications of the review interval (during disruptions) [

12]. When supply-side disruptions are prolonged for various reasons, this causes shortages of cement bags at retailers. However, the construction activities of individual home builders and small builders, which account for 60–70% of rural sales and 40–50% of urban sales in India, come to a complete halt without cement. During supply-side disruptions, a segment of customers is unable to wait at a single cement retailer with a fixed cycle length and shifts to other retailers. This accounts for the partial back-ordering of shortages [

13]. Thus, cement retailers need to predict and meet real-time fluctuations in demand and influence them to achieve long-term business goals while ensuring operational agility and resilience to potential market adversities [

14]. Accordingly, many retailers employ some sort of artificial intelligence and forecasting-based semi-autonomous decision support (SADS) systems that can predict the demand for cement bags and communicate an upcoming order to cement manufacturers at the start of each review cycle.

Cement is a deteriorating item [

15]. Therefore, the leakage and entry of moisture into cement bags during inventory stock-in and/or storage at any retailer lead to an irreversible loss of cement quality, thus making some bags useless. Ghandehari and Dezhtaherian [

16] modeled a deteriorated inventory model with partial back-order. During the COVID-19 outbreak, nearly 26% of retailers holding 400+ bags offered major discounts to avoid spoilage. As with any periodic-review inventory system, cement retailers typically discard deteriorated cement bags at the end of each period, incurring some additional costs. These give the base-stock policy a capacity limit to bind the replenishment quantity in each period significant for the planned single-item long-run periodic-review inventory system of cement retailers [

17]. Existing sub-optimal base-stock levels lead to a loss of business opportunities for cement retailers with a fixed cycle length under stochastic supply disruptions.

Nevertheless, under probable supply-side disruptions, most existing EOQ models consider specific probability distributions based on exogenous review intervals that sometimes lead to sub-optimal replenishment decisions under longer intervals and increase the risk of inventory obsolescence [

18]. This way, to deal with probable supply-side disruptions under a varying demand rate and partial back-ordering of shortages for deteriorating items, the present study frames various cost components, such as expected long-run ordering, acquisition, holding, deterioration, and shortage costs, including back-ordering and lost sales costs, to obtain the retailer’s expected long-run net profit of one stochastic periodic-review base-stock inventory model.

Regarding the structure of the rest of this paper,

Section 2 deliberates on the background study in terms of two different aspects.

Section 3 discusses the notations, assumptions, and problem statements. Next, this study formulates the proposed inventory model of cement retailers in

Section 4, while

Section 5 analytically establishes the global optimality of the proposed model at the critically determined base-stock level. Later,

Section 6 numerically evaluates the proposed model. The 107 managerial insights are derived from the sensitivity analysis of several major parameters here, along 108 with comparisons to some well-established articles with comparisons to some well-established articles. Lastly,

Section 8 concludes the paper along with some scopes of future research.

4. Formulation of the Proposed Model

The present section designs an inventory control model to measure the optimal order up to the level that maximizes the total expected long-run net profit of the retailers. In practice, a number of retailers selling deteriorating items, like Nestlé S.A., BRF S.A., and Cargill, find the stock-out-related responsiveness to be more critical than the holding cost imposed on them, thereby keeping the competitive advantages through responsiveness at an ideal level. Accordingly, this study determines the different long-run expected cost components, namely the ordering cost, the acquisition cost, the holding cost, the deterioration cost, the shortage cost, and the ost sales cost, within both the regular span and the disruptive spans, as illustrated as follows:

4.1. Cost Components in the Regular Span

Expected long-run ordering cost

The retailer bears the one-time fixed ordering cost while placing the replenishment order at the beginning of any inventory cycle during the regular span. Thus, subject to unit ordering cost

, this study determines the expected long-run ordering cost of the retailer within the regular span as follows:

Expected long-run holding cost

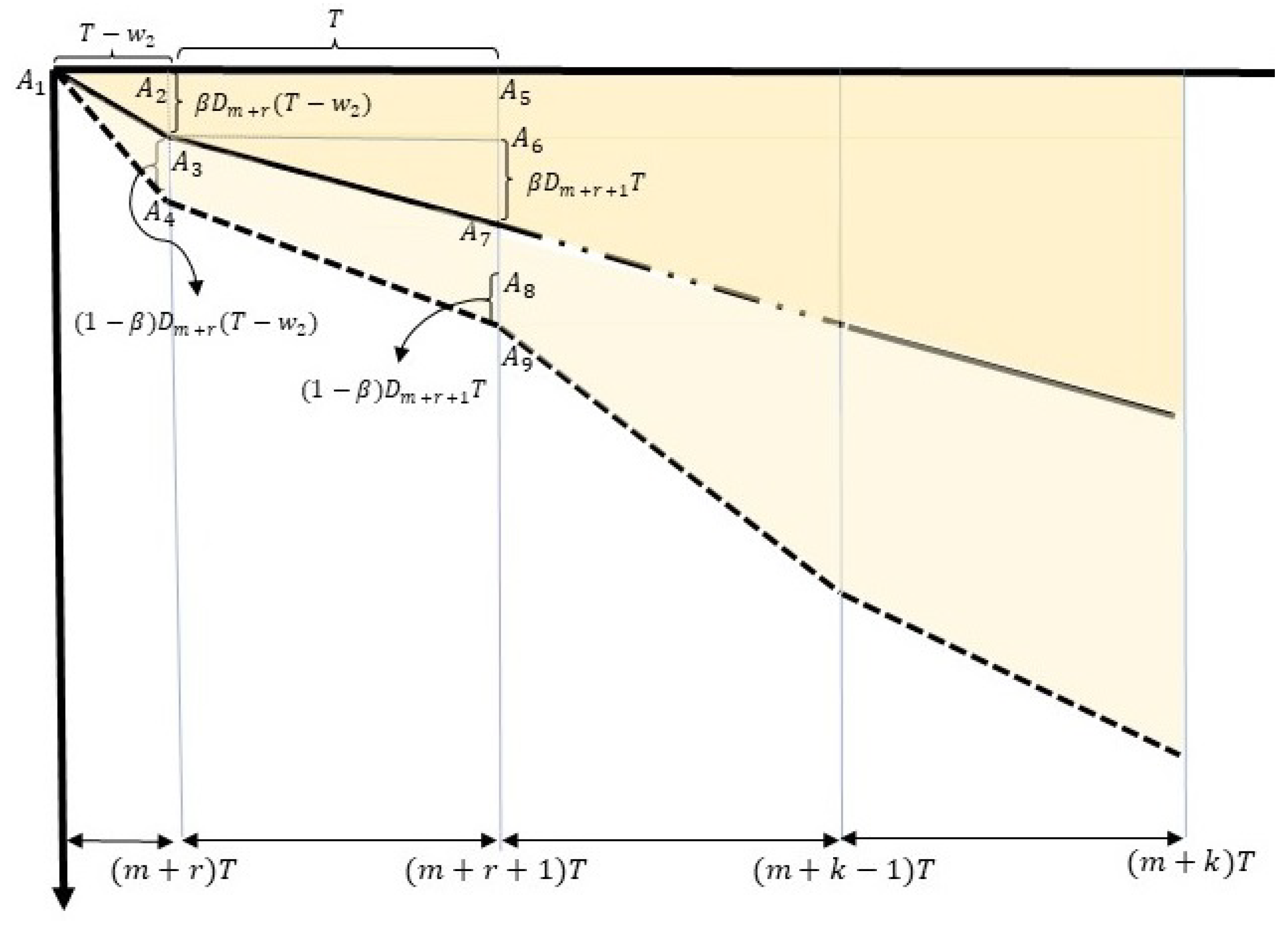

A suitable place, store, warehouse etc., is essential to store the saleable products. While the resulting holding cost includes the cost of insurance, numerous taxes, maintenance costs, electricity costs, and many others, researchers find this cost to be proportional to the number of products in the inventory within the holding period. Here, the area of the rectangle in any

inventory epoch (see, for details,

Figure 2) is

while the corresponding area of a triangle is

. This provides the total area under the inventory curve in any

inventory epoch within the regular span as follows:

Therefore, the expected long-run holding cost of the retailer within the regular span is as follows:

Expected long-run deterioration cost

The retailer discards the products that deteriorate over time from its inventory at the end of each on-hand inventory cycle. Thus, this study considers the expected long-run deterioration cost of the retailer within the regular span as follows:

Expected long-run shortage cost

Since this study assumes that the retailer stores enough stock to fulfill the demand of customers in any inventory cycle during the regular span, the scenario of shortages does not occur during the regular span. Thus, the resulting expected long-run shortage cost is nil.

Expected long-run acquisition cost

In any

regular inventory epoch, the retailer makes replenishment decisions for inventory up to the maximum stock level S by adding the number of sold items in the previous cycle and the number of deteriorated items to be discarded from inventory at the end of the current cycle. Thus, this study describes the order quantity

for which the SADS of the retailer autonomically places the order, as follows:

In this way, this study exemplifies the long-term expected acquisition cost of retailers within the regular span as follows:

In addition, this is to note that the random variables

X and

m are connected through the following relationship:

4.2. Cost Components in the Disruptive Span

With the aim to efficiently manage the sequential disruptions occurring randomly to the supplier in the inventory cycle and staying for the random duration Y (i.e., ), this study assumes the inventory state random variable to range from the to at most the on-hand inventory cycle under the disruptions. Whenever the successive disruptions continue to occur till the cycle or more, the retailer experiences shortages. Consequently, the supplier makes the replenishment afresh at the end of the inventory cycle.

Expected long-run ordering cost

The retailer does not place any request for the replenishment of stocks to the supplier during the disruptions but asks for the one-time replenishment only after the supply-side disruptions are over. Thus, this study obtains the expected long-run ordering cost of the retailer during supply-side disruption cycles as follows:

Expected long-run holding cost

This study measures the expected long-run holding cost and the associated deterioration cost by determining the areas of the various shaded regions displayed in

Figure 2. Here, the

inventory epoch follows the last replenishment before the sequential disruptions occur. Thus, the retailer’s

inventory cycle begins with

S units of items in its inventory during the disruptive span. Therefore, this study computes the area

of the trapezoidal region under the inventory curve at the

inventory epoch within the disruptive span as follows:

While the retailer discards the deteriorated items at the end of each on-hand inventory cycle during the disruptive span, this study determines the area of the trapezoidal region

under the inventory curve at the

on-hand inventory epoch within the disruptive span as follows:

Therefore, this study computes the area of the trapezoid representing the

cycle as follows:

All these yield the area of the trapezoid representing any

cycle as follows:

Whereas

Figure 2 suggests that the range of the on-hand inventory state random variable (

) extends from

m to

during the disruptive span, this study conceives that the retailer is capable of satisfying the demand of customers solely for the duration

in the

inventory epoch during the disruptive span. Accordingly, the area

of the triangle in the on-hand inventory at the

inventory epoch is as follows:

subject to the fraction

of the on-hand inventory period in the

inventory epoch, which is as follows:

see, for details,

Appendix C.

Thus, this study determines the area of the region of any

inventory epoch as follows:

The long-run average inventory of the retailer in the disruptive span is as follows:

In this way, subject to the per unit holding cost

this study measures the long-term expected holding cost of the retailer in the disruptive span as follows (see, for details,

Appendix D):

Expected long-run deterioration cost

Subject to the average on-hand inventory in the disruptive span as obtained in the relation (

13), the uniform deterioration rate

, and the unit scrap price

in any

inventory epoch, this study computes the long-term expected deterioration cost (

) of the retailer in the disruptive span as follows:

Negative Inventory Period

It is highly unpredictable to specify the period for which the sequential disruptions will keep going. Nevertheless, pessimistically, the shortages start to happen after the sequential disruptions reach the inventory cycle. By considering to be the fraction of the cycle length for which the demand is fulfilled from the inventory of the retailer, this study measures the expected long-run shortage cost consisting of the expected long-run back-ordering cost and the expected long-run lost sales cost as follows:

Expected long-run back-ordering cost

Here, the area of the right-angled triangular region

(see

Figure 3) representing the partially back-ordered inventory for the duration

in the

inventory cycle post disruption (i.e.,

inventory epoch) is as follows (see

Appendix B).

Here, the sides of the triangle

are expressed as

and

.

Likewise, this study measures the area of the trapezoidal region describing the partially back-ordered inventory within the inventory cycle as follows.

Here, the area of the trapezoidal region

is obtained as the sum of two regions, one rectangular region

with sides

and

, the triangular region with sides

, and

(see

Figure 3).

In this way, the present study measures the area of the trapezoidal region of the partially back-ordered inventory in any

inventory cycle as follows:

Analogous to the deliberation on the long-run average inventory of the retailer, this study computes the average back-ordering at the retailer as follows:

Thus, the expected average back-ordering at the retailer is as follows:

The following equations provide the expected long-run back-ordering cost of the retailer:

Expected long-run lost sales cost

This study measures the lost sales vertically by computing the difference between the actual inventory position and its position at

at the end of any negative inventory cycle (see

Figure 3), thereby deducing it as follows.

Here, the amount of lost sales for the

epoch is expressed as the length

. For the

epoch, the lost sales are represented by the segment

, which is the sum of the length

and

. Therefore,

. Likewise, the present study measures the amount of lost sales in any

cycles (see Equation (

26)).

Thus, this study finds the following:

In this way, this study computes the expected average lost sales cost of the retailer as follows:

Expected long-run acquisition cost

The base-stock level

S and the total amount of back-ordered portion in any

inventory epoch during disruption is described in

Figure 2 as

, which have to be ordered after the completion of the disruption. Thus, after the completion of the disruption, the SADS will place an order to the supplier. Consequently, the expected acquisition cost of the retailer within the disruptive span is as follows:

4.3. Retailer’s Expected Long-Run Net Profit per Unit Time

The amount of saleable items on cycle is expressed as , where the selling price is .

The total earnings before disruption are expressed as follows:

The total earnings after disruption are the sum of sellable items with a positive inventory level with the back-ordered portion, expressed as follows:

This study measures the retailer’s expected long-run aggregate earnings (by combining Equations (

30) and (

31)) per cycle as follows:

Again, on the basis of the various cost components of retailers in both the non-disrupted and disrupted cycles (see relation (

3) for

, relation (

5) for

, relation (

6) for

, relation (

8) for

, relation (

10) for

, relation (

18) for

, relation (

19) for

, relation (

25) for

, relation (

28) for

, and relation (

29) for

), this study expresses retailer’s expected long-run aggregate cost as follows:

Therefore, this study represents the expected long-run net profit per cycle of the retailer as follows (see, for the full expression,

Appendix E):

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}