1. Introduction

Time series data usually arise in a wide variety of disciplines as machine learning, biology, geology, finance and medicine, among many other fields. Typically, most of the works on the analysis of these objects have focused on real-valued time series, while the study of time series with alternative ranges has been given limited attention. However, the latter type of time series naturally appear in several fields when attempting to analyze several phenomena. For instance, weekly counts of new infections with a specific disease in a particular place are often modeled through integer-valued time series [

1]. In some contexts, the time series under consideration do not even take numerical values (e.g., temporal records of EEG sleep states for an infant after birth [

2]). A comprehensive introduction to the topic of time series with alternative ranges including classical models, recent advances, key references, and specific application areas is provided by [

3].

Categorical time series (CTS) are characterized by taking values in a qualitative range consisting of a finite number of categories, which is called ordinal range (if the categories exhibit a natural ordering) or nominal range otherwise. In this paper, the specific case of an ordinal range is considered. Time series fulfilling this condition, frequently referred to as ordinal time series (OTS), pose several challenges to the statistical practitioner. Indeed, dealing with ordered qualitative outcomes implies that some classical analytic tools must be properly adapted. For instance, standard measures of location, dispersion and serial dependence cannot be defined in the same manner as in the real-valued case, but the underlying ordering existing in the series range still allows for a meaningful definition of the corresponding quantities in the ordinal setting. For instance, in [

4], a unified approach based on expected distances is proposed to obtain well-interpretable statistical measures for ordinal series. In addition, sample counterparts of the corresponding measures are introduced and their asymptotic properties are derived.

Ordinal series arise in multiple fields. Some interesting examples include credit ratings of different countries [

4] or degree of cloud coverage in different regions [

5]. In addition, OTS appear quite naturally in psychology, since temporal measurements in such discipline often originate from ordinal scales, such as Likert questionnaires. For instance, the so-called mood time series of the married couple [

6,

7] represents the daily mood of a married couple over a period of 144 days, which is recorded on Likert scales. Specifically, the mood measures arise from a questionnaire with 58 items such as “

Right now I feel good”, being the momentary intensity of emotions rated with answers 1 =

definitely not, 2 =

not, 3 =

not really, 4 =

a little, 5 =

very much, and 6 =

extremely. Such types of time series are naturally considered as ordinal. On the contrary, in many situations, the series under consideration are actually real-valued, but they are treated as ordinal ones because this provides several advantages. For instance, in [

8], the gross wage of different individuals is divided into six ordered categories according to the quintiles of the income distribution for each year. As stated by [

8], one of the advantages of considering wage categories relies on the fact that no inflation adjustment has to be made. Another illustrative example involves the well-known air quality index (AQI), which presents the status of daily air quality and shows the degree of air pollution in a particular place [

9]. The air quality is often classified into six different levels which are determined according to the concentrations of several air pollutants.

While the field of OTS data analysis is still in its early stages, there are already a few interesting works on the topic. In one of the first papers, ref. [

10] proposed robust methods of time series analysis which use only comparisons of values and not their actual size. As previously stated, ref. [

4] developed an interesting methodology for defining statistical features in the ordinal setting, which is based on expected distances. Later, ref. [

11] proposed a family of signed dependence measures for analyzing the behavior of a given OTS. There are also some recent works involving machine learning tasks in the context of ordinal series. For instance, ref. [

9] considered different models to forecast the air quality levels in 16 cities of Taiwan. Two novel distances between OTS were proposed in [

12] and used to construct effective clustering algorithms. The approaches were applied to datasets of financial time series and interesting conclusions were reached. Previous references highlight the remarkable growth that OTS analysis has recently undergone.

In accordance with previous comments, it is clear that the construction of software tools specifically designed to deal with OTS is crucial. However there exist no software packages in well-known programming languages (e.g., R version 4.1.2 [

13], Python version 3.11.1 [

14], etc.) aimed at dealing with ordinal series. Moreover, there are only a few libraries focusing on the analysis of ordinal data without a temporal nature, which are mostly written in the R language, but too often restricted to specific statistical procedures. For instance, the package

ordinal [

15] implements cumulative link models for coping with ordinal response variables. Specific functions for generating multivariate ordinal data are provided through package

MultiOrd [

16]. In a purely machine learning context, an innovative computing tool named

ocapis containing classification algorithms for ordinal data is described in [

17]. In addition, the library includes two preprocessing techniques: an instance selector and a feature selector. Note that, although their usefulness is beyond doubt, none of the previously mentioned packages is suitable to execute simple exploratory analyses, a task which should be usually performed before moving on to more sophisticated procedures. In sum, there are currently no software tools allowing to compute classical features for ordinal series.

The goal of this manuscript is to present the R package

otsfeatures, which includes several functions to compute well-known statistical features for ordinal series. As well as giving valuable information about the behavior of the time series, the corresponding features can be used as input for classical machine learning procedures, as clustering, classification, and outlier detection algorithms. In addition,

otsfeatures also includes some commands allowing to perform traditional inferential tasks. The two databases of financial time series described in [

12] are also available in the package, along with three synthetic datasets containing OTS which were generated from different underlying stochastic processes. These data collections allow the users to test the commands available in

otsfeatures. It is worth mentioning that some functions of the package can also be employed to analyze ordinal data without a temporal character.

In summary, the package

otsfeatures intends to integrate a set of simple but powerful functions for the statistical analysis of OTS into a single framework. The implementation of the package was performed by using the open-source R programming language due to the role of R as the most used programming language for statistical computing.

otsfeatures is available from the Comprehensive R Archive Network (CRAN) at

https://cran.r-project.org/web/packages/otsfeatures/index.html (accessed on 15 May 2023).

The rest of the paper is structured as follows. A summary of relevant features to analyze marginal properties and the serial dependence of ordinal series is presented in

Section 2. Furthermore, some novel features measuring cross-dependence between ordinal and numerical processes are also introduced. The main functions implemented in

otsfeatures and the available datasets are presented in

Section 3 after providing some background on ordinal series. In

Section 4, the functionality of the package is illustrated through several examples considering synthetic data and the financial databases included in

otsfeatures. In addition, the process of using the output of some functions to carry out traditional data mining tasks is described. Some conclusions are given in

Section 5.

2. Analyzing Marginal Properties and Serial Dependence of Ordinal Time Series

Let

,

, be a strictly stationary stochastic process having the ordered categorical range

with

. The process

is often referred to as an ordinal process, while the categories in

are frequently called the states. Let

be the count process with range

generating the ordinal process

, i.e.,

. It is well known that the distributional properties of

(e.g., stationarity) are properly inherited by

[

3]. In particular, the marginal probabilities can be expressed as

while the lagged joint probabilities (for a lag

) are given by

Note that both the marginal and the joint probabilities are still well defined in the general case of a stationary stochastic process with nominal range, i.e., when no underlying ordering exists in

. By contrast, in an ordinal process, one can also consider the corresponding cumulative probabilities, which are defined as

for the marginal and the joint case, respectively.

In practice, the quantities

,

,

, and

must be estimated from a

T-length realization of the ordinal process,

, usually referred to as

ordinal time series (OTS). Natural estimates of these probabilities are given by

where

denotes the indicator function.

Probabilities

,

,

, and

can be used to represent the process

in terms of marginal and serial dependence patterns. An alternative way of describing a given ordinal process is by means of features measuring classical statistical properties (e.g., centrality, dispersion, etc.) in the ordinal setting. A practical approach to define these quantities consists of considering expected values of some distances between ordinal categories [

4]. Specifically, a given distance measure

d defined in

gives rise to specific ordinal features. Three of the most commonly used distances are the so-called Hamming, block, and Euclidean, which are defined as

for a pair of states

and

, respectively, where

denotes the Kronecker delta. The first six quantities in

Table 1 describe the marginal behavior of the process

for a given distance

d. There, the notation DIVC stands for diversity coefficient, which is an approach for measuring dispersion proposed by [

18], and

and

refer to independent copies of

. In addition, the notation

was used to define a reflected copy of

, that is, a stochastic process independent of

such that

,

. Note that the considered location measures pertain to the ordinal set

. For the remaining marginal features, some assumptions are needed to obtain the ranges provided in

Table 1, where

. Particularly, for these four measures, we assume that

, a property which is usually referred to as maximization. In addition, for the asymmetry, we require that

is a positive semidefinite matrix, where

and

denote the identity and the counteridentity matrices of order

and

, where

is the corresponding pairwise distance matrix. Moreover, for both the asymmetry and the skewness to be reasonable measures, we assume that the distance

d is centrosymmetric, that is,

,

. Note that, for a symmetric process (that is, a process

such that

and

have the same marginal distribution), then both the asymmetry and the skewness are expected to be zero. It is worth highlighting that, under the required assumptions, the quantities

,

,

and

can be easily normalized to the interval

(or

in the case of the skewness) by dividing them by

.

Estimates of the marginal features in

Table 1, denoted by means of the notation

, where

stands for the corresponding measure (e.g.,

), can be obtained by considering estimates of

(

),

and

given by

respectively.

Table 1 also contains some features assessing the serial dependence in an ordinal process. In this context, one of the most common quantities is the so-called ordinal Cohen’s

, which measures the relative deviation of the dispersion for dependent and independent random variables at a given lag

. This quantity can take either positive or negative values, with its upper bound being 1 and its lower bound being dependent on the underlying distance

d. A sample version of

, denoted by

, is obtained by using

and the standard estimate of

defined as

A detailed analysis of the marginal quantities in

Table 1 plus the ordinal Cohen’s

is given in [

4]. In particular, the asymptotic properties of the corresponding estimates are derived and their behavior is analyzed in some simulation experiments.

The serial dependence of an ordinal process can be evaluated by means of alternative quantities which do not pertain to the approach based on expected distances. First, let us define the cumulative binarization of the process

as the multivariate process

such that

if

,

. By considering pairwise correlations in the cumulative binarization and fixing a lag

, we obtain the quantities

. The features in (

9) are very convenient because they play a similar role than the autocorrelation function of a numerical stochastic process. A measure of dependence at lag

l can be obtained by considering the sum of the squares of all features

. In this way, we define the total cumulative correlation (TCC) as

An estimate of the previous quantity can be obtained by considering

, where

is the natural estimate of

obtained by replacing

,

and

by

,

and

in (

9) computed from the realization

.

Another interesting phenomenon that can be analyzed when dealing with an ordinal process is to measure the degree of cross-dependence that the process displays with respect to a given real-valued process. To this aim, let

be a strictly stationary real-valued process with variance

and consider the correlation

, which evaluates the level of linear dependence between state

of process

and the process

at a given lag

. A more complete measure assessing general types of dependence can be constructed by defining the quantity

, where is a probability level, denotes the quantile function of process . Note that, by considering different values for , dependence at different levels at lag l can be evaluated between processes and .

The features of the form

can be combined in a proper way to obtain a suitable measure of the average linear correlation between an ordinal and a numerical process. In this way, we define the total mixed cumulative linear correlation (TMCLC) at lag

l as

Analogously, a measure of the average quantile correlation between both processes, so-called the total mixed cumulative quantile correlation (TMCQC) at lag

l, can be defined as

Note that both quantities

and

(see the lower part of

Table 1) are naturally defined in the range

, with the value 0 being reached in the case of null cross-dependence between

and

. On the contrary, larger values indicate a stronger degree of cross-dependence between both processes.

Natural estimates of

and

, denoted by

and

, respectively, can be obtained by considering standard estimates of

and

, denoted by

and

, respectively. To compute the latter estimates, a

T-length realization of the bivariate process

, that is

, is needed. In this way, estimates

and

take the form

where

denotes the standard estimate of the covariance between two random variables, and

is the standard estimate of the variance of process

computed from the realization

. Estimates in (

15) give rise to the quantities

and

.

4. Using the otsfeatures Package—AnIllustration

This section is devoted to illustrate the use of package otsfeatures. First we give some general considerations about the package and next, we provide some examples concerning the use of several functions for data analysis and feature extraction.

4.1. Some Generalities about otsfeatures

In otsfeatures, a T-length OTS with range , , is defined through a vector of length T whose possible values are the integer numbers from 0 to n. More precisely, the realization is represented by using the associated realization of the generating count process , that is, such that , . Note that the main advantage of this approach relies on the fact that only numerical vectors are needed for the representation of ordinal series.

The majority of functions in the package take as input a single OTS. For instance, functions in

Table 4 return by default the corresponding estimate. Some of these functions admit the argument

features = TRUE. In that case, the function returns a vector which contains the individual quantities which are considered to construct the corresponding estimate. For instance, the function

total_c_cor() computes by default the estimate

. However, if we employ the argument

features = TRUE, a matrix whose

entry contains the quantity

is returned. In fact, the extraction of the individual components of some estimates can be very useful for several purposes. Functions

ots_plot() and

plot_ordinal_cohens_kappa() with the default settings produce the corresponding time series plot and serial dependence graph, respectively. On the contrary, the remaining functions and function

plot_ordinal_cohens_kappa() with

plot = FALSE return the results of the corresponding hypothesis tests, namely the test statistic, the critical value for a given significance level used as input, and the

p-value. It is worth remarking that most commands in

otsfeatures require the corresponding states to be specified in a vector of the form

. This is done by means of the argument

states. In this way, several issues can be avoided. For instance, a particular realization may not include all the underlying ordinal values. Therefore, when analyzing such a series, one could ignore the existence of some states. This is properly solved by using the argument

states.

The databases included in

otsfeatures are defined by the means of a list named as indicated in the first column of

Table 2. In the case of the synthetic databases, each list contains two elements, which are described below.

On the other hand, the lists associated with datasets CreditRatings and AustrianWages only include the element data, as there are no underlying class labels for these data collections.

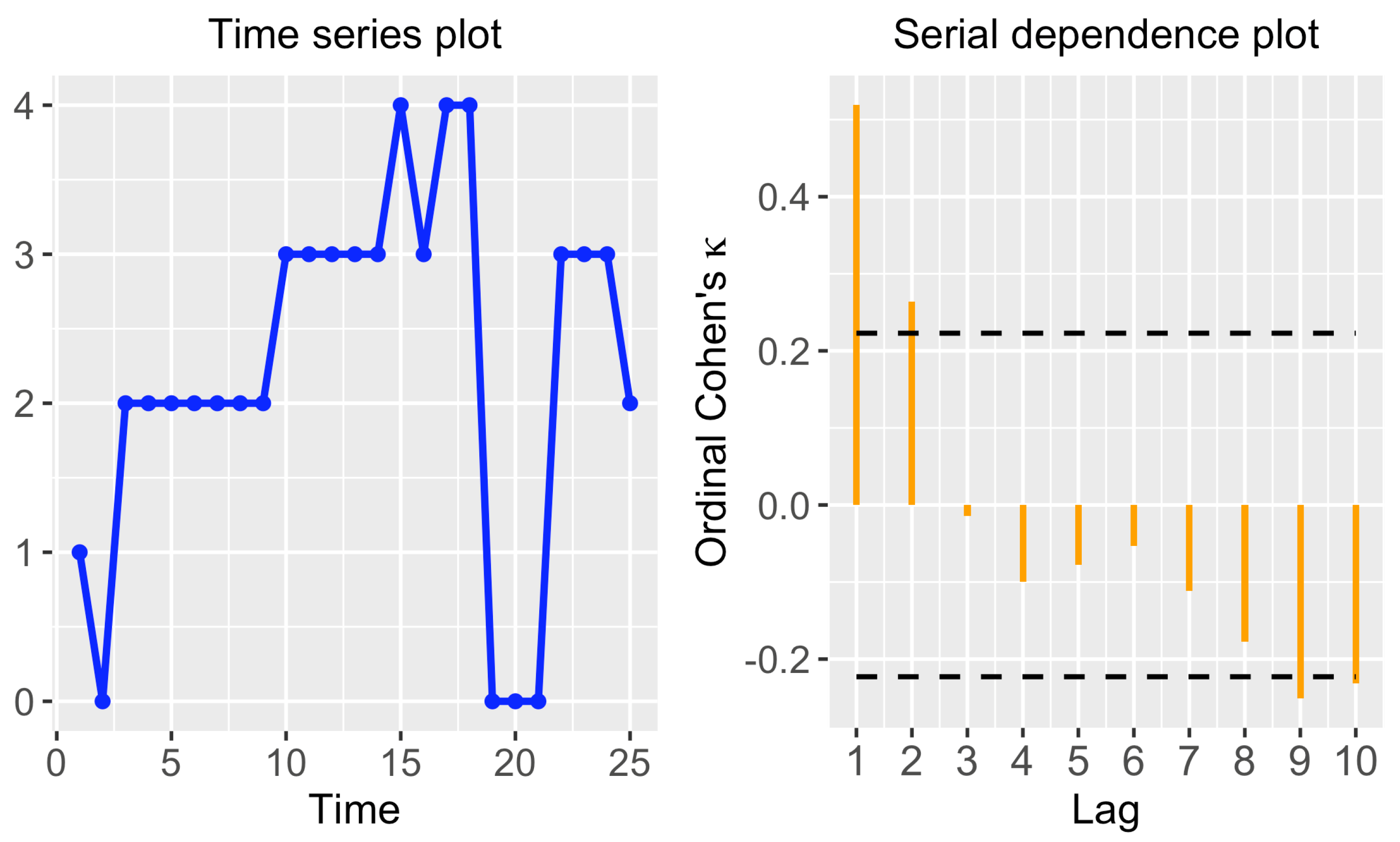

Let us take a look at one time series in dataset AustrianWages, which represents a specific employee of the Austrian labor market.

In this series, the corresponding wage categories are identified with the integers from 0 to 5 as explained in

Section 3.1 (category 0 represents the lowest incomes and category 5, the highest incomes). In this way, the previous sequence represents an individual who started with a moderate wage (category 3), then decreased his income level and finally ended up in the highest wage category. Note that this representation of the series by means of integer numbers provides a simple way of quickly examining the corresponding ordinal values.

4.2. Performing Inferential Tasks

The functions described in

Section 3.2 allow the user to obtain valuable information from a given ordinal series. Let us start by analyzing one of the time series in the dataset

AustrianWages. Before carrying out inferential tasks, we are going to visualize the corresponding time series as a preliminary step. To this aim, we can employ the function

ots_plot(), which takes as input the time series we want to represent and a vector containing the different states.

We also employed the argument

labels = 0:5 to indicate that the states

to

are labeled with the integers from 0 to 5, since this is the labeling used in the original dataset (see

Section 3.1). The corresponding graph is provided in the left panel of

Figure 1. This series corresponds to an individual who belonged to all income levels except for the highest one (5). It is worth highlighting that, as the different states are located in the

y-axis in increasing order, the plot is rather intuitive. In addition, note that, for the sake of simplicity, the different categories are treated as equidistant. Specifically, the graph is constructed by considering the block distance

between states, which is not always suitable, since the true underlying distance often depends on the specific context. Therefore, the graph produced by function

ots_plot() should not be treated as an accurate plot of the corresponding OTS, but as a rough representation thereof.

As stated in

Section 3.2.1, function

plot_ordinal_cohens_kappa() in

otsfeatures allows to construct a serial dependence plot based on the estimate

. Let us represent such plot for the series in the left panel of

Figure 1.

By default, the function considers lags from 1 to 10 (argument

max_lag) and a significance level

for the corresponding test (argument

). The resulting graph is given in the right panel of

Figure 1. As the standard autocorrelation plot, the corresponding estimates are displayed in a sequential order, with dashed lines indicating the critical values for the associated test. In this case, the serial dependence plot indicates significant dependence at lags 1 and 2. Moreover, dependence at lags 9 and 10 could also be considered significant, but this may be due to chance, since multiple tests are simultaneously carried out. In addition to the dependence plot, function

plot_ordinal_cohens_kappa() also produces numerical outputs. For instance, the corresponding

p-values can be obtained by using the argument

plot = FALSE.

> sd_plot <- plot_ordinal_cohens_kappa(series = AustrianWages$data[[100]],

states = 0 : 5, plot = FALSE)

> round(sd_plot$p_values, 2)

[1] 0.00 0.02 0.68 0.30 0.38 0.49 0.26 0.11 0.03 0.04

The p-values in the previous output corroborate that the quantity is significantly non-null, thus confirming the existence of serial dependence at the first lag. Note that the p-values associated with lags 2, 9 and 10 also indicate rejection of the null hypothesis at level . However, the set of p-values should be properly adjusted to handle random rejections of the null hypothesis that can arise in a multiple testing context. For instance, the well-known Holm’s method, which controls the family-wise error rate at a pre-specified -level, could be applied to the p-values by executing the following command.

> p.adjust(round(sd_plot$p_values, 2), method = ‘holm’)

[1] 0.00 0.18 1.00 1.00 1.00 1.00 1.00 0.66 0.24 0.28

According to the corrected p-values, significant serial dependence still exists at lag 1, but the null hypothesis of serial independence at lags 2, 9 and 10 cannot be now rejected.

In additon to analyzing serial dependence, hypothesis tests and confidence intervals for classical ordinal quantities can be constructed by using

otsfeatures (see

Section 3.2.2). To illustrate these tasks, we consider again the previous OTS and start by testing the null hypothesis stating that the quantity

is equal to 0. To this aim, we employ the function

test_ordinal_skewness(), whose main arguments are the corresponding ordinal series (argument

series) and the assumed value for

(argument

true_skewness), which is set to zero in this example.

> test_os <- test_ordinal_skewness(series = AustrianWages$data[[100]],

states = 0 : 5, true_skewness = 0)

> test_os$p_value

[1] 0.4239951

The p-value of the test resulted as 0.424. Therefore, the null hypothesis cannot be rejected at any reasonable significance level and we can assume that the series was generated from an ordinal process with 0 skewness. For illustrative purposes, let us repeat the previous test by setting true_skewness = 2.

> test_os <- test_ordinal_skewness(series = AustrianWages$data[[100]],

states = 0 : 5, true_skewness = 2)

> test_os$p_value

[1] 0.02287435

This time, the p-value indicates that the null hypothesis should be rejected at the standard significance level ; that is, we could assume that the true skewness is different from 2 at that level. However, this is no longer the case for stricter significance levels (e.g., ).

The construction of a confidence interval for the quantity can be easily performed by using the function ci_ordinal_skewness(). By default, a confidence level of 0.95 is considered (argument level).

The lower and upper bounds of the confidence interval are given by −0.75 and 1.79, respectively. It is worth remarking that, as we are dealing with a rather short time series (), the interval is quite broad. In addition, note that 0 is included in the interval, which is coherent with the results of the first hypothesis test for above. Let us now construct a confidence interval by considering a less strict confidence level, namely 0.90.

> ci_os <- ci_ordinal_skewness(series = AustrianWages$data[[100]],

states = 0 : 5, level = 0.90)

> ci_os

Lower bound Upper bound

1 -0.5498109 1.589811

As expected, the new interval has a shorter length than the previous one.

Inferential tasks for quantities

, and

can be carried out in an analogous way by using the corresponding functions (see

Table 3). Moreover, these commands can also be used when dealing with i.i.d. data by using the argument

temporal = FALSE.

4.3. Performing Data Mining Tasks

Jointly used with external functions, otsfeatures becomes a versatile and helpful tool to carry out different data-mining tasks involving ordinal series. In this section, for illustrative purposes, we focus our attention on three important problems, namely classification, clustering, and outlier detection.

4.3.1. Performing OTS Classification

Firstly, we show how the output of the functions in

Table 4 can be used to perform feature-based classification. We illustrate this approach by considering the data collection

SyntheticData1, which contains 80 series generated from 4 different stochastic processes, each one of them giving rise to 20 OTS. The underlying processes are given by two binomial AR(1) and two binomial AR(2) models. Thus, each series in the dataset

SyntheticData1 has an associated class label determined by the corresponding generating process. Using the necessary functions, each series is replaced by a feature vector given by the quantities

,

,

,

,

and

. In all cases, the argument

distance = ‘Block’ (default) is used to indicate that the block distance should be employed as the underlying block distance between states.

> features_1 <- unlist(lapply(SyntheticData1$data,

ordinal_location_1, states = 0 : 5, distance = ‘Block’))

> features_2 <- unlist(lapply(SyntheticData1$data,

ordinal_dispersion_2, states = 0 : 5, distance = ‘Block’))

> features_3 <- unlist(lapply(SyntheticData1$data,

ordinal_asymmetry, states = 0 : 5, distance = ‘Block’))

> features_4 <- unlist(lapply(SyntheticData1$data,

ordinal_skewness, states = 0 : 5, distance = ‘Block’))

> features_5 <- unlist(lapply(SyntheticData1$data,

ordinal_cohens_kappa, states = 0 : 5, distance = ‘Block’, lag = 1))

> features_6 <- unlist(lapply(SyntheticData1$data,

ordinal_cohens_kappa, states = 0 : 5, distance = ‘Block’, lag = 2))

> feature_dataset <- cbind(features_1, features_2, features_3,

features_4, features_5, features_6)

Note that the

ith row of the object

feature_dataset contains estimated values characterizing the marginal and serial behavior of the

ith OTS in the dataset. Therefore, several standard classification algorithms can be applied to these matrix by means of the R package

caret [

21]. Package

caret requires the dataset of features to be an object of class

data.frame whose last column must provide the class labels of the elements and be named

‘Class’. Thus, as a preliminary step, we create

df_feature_dataset, a version of

feature_dataset properly arranged to be used as input to

caret functions, by means of the following chunk of code.

> df_feature_dataset <- data.frame(cbind(feature_dataset,

SyntheticData1$classes))

> colnames(df_feature_dataset)[7] <- ‘Class’

> df_feature_dataset[,7] <- factor(df_feature_dataset[,7])

The function train() allows one to fit several classifiers to the corresponding dataset, while the selected algorithm can be evaluated, for instance, by leave-one-out cross-validation (LOOCV). A grid search in the hyperparameter space of the corresponding classifier is performed by default. First we consider a standard classifier based on k nearest neighbours (kNN) by using method = ‘knn’ as input parameter. By means of the command trControl(), we define LOOCV as evaluation protocol.

> library(caret)

> train_control <- trainControl(method = ‘LOOCV’)

> model_knn <- train(Class~., data = df_feature_dataset,

trControl = train_control, method = ‘knn’)

The object model_kNN contains the fitted model and the evaluation results, among others. The reached accuracy can be accessed as follows.

The kNN classifier achieves an accuracy of 0.95 in the dataset SyntheticData1. Specifically, it produces only 4 misclassifications. Next, we study the performance of the random forest and the linear discriminant analysis. To this aim, we need to set method = ‘rf’ and method = `lda’, respectively.

> model_rf <- train(Class~., data = df_feature_dataset,

trControl = train_control, method = ‘rf’)

> max(model_rf$results$Accuracy)

[1] 1

> model_lda <- train(Class~., data = df_feature_dataset,

trControl = train_control, method = ‘lda’)

> max(model_lda$results$Accuracy)

[1] 1

Both approaches reach a perfect accuracy of 1, thus improving the predictive effectiveness of the kNN classifier. For illustrative purposes, let us analyze the performance of the previous classifiers when the Hamming distance between ordinal categories is taken into account, which is indicated through the argument distance = ‘Hamming’.

> features_1 <- unlist(lapply(SyntheticData1$data,

ordinal_location_1, states = 0 : 5, distance = ‘Hamming’))

> features_2 <- unlist(lapply(SyntheticData1$data,

ordinal_dispersion_2, states = 0 : 5, distance = ‘Hamming’))

> features_3 <- unlist(lapply(SyntheticData1$data,

ordinal_asymmetry, states = 0 : 5, distance = ‘Hamming’))

> features_4 <- unlist(lapply(SyntheticData1$data,

ordinal_skewness, states = 0 : 5, distance = ‘Hamming’))

> features_5 <- unlist(lapply(SyntheticData1$data,

ordinal_cohens_kappa, states = 0 : 5, distance = ‘Hamming’, lag = 1))

> features_6 <- unlist(lapply(SyntheticData1$data,

ordinal_cohens_kappa, states = 0 : 5, distance = ‘Hamming’, lag = 2))

> feature_dataset <- cbind(features_1, features_2, features_3,

features_4, features_5, features_6)

> df_feature_dataset <- data.frame(cbind(feature_dataset,

SyntheticData1$classes))

> colnames(df_feature_dataset)[7] <- ‘Class’

> df_feature_dataset[,7] <- factor(df_feature_dataset[,7])

> model_knn <- train(Class~., data = df_feature_dataset,

trControl = train_control, method = ‘knn’)

> max(model_knn$results$Accuracy)

[1] 0.975

> model_rf <- train(Class~., data = df_feature_dataset,

trControl = train_control, method = ‘rf’)

> max(model_rf$results$Accuracy)

[1] 1

> model_lda <- train(Class~., data = df_feature_dataset,

trControl = train_control, method = ‘lda’)

> max(model_lda$results$Accuracy)

[1] 0.975

By considering the distance , the kNN classifier slightly improves its performance while the linear discriminant analysis shows a small decrease in predictive effectiveness. The random forest still reaches perfect results. The classification ability of alternative sets of features, as well as the behavior of any other classifier, can be examined in an analogous way as above.

4.3.2. Performing OTS Clustering

The package otsfeatures also provides an excellent framework to carry out clustering of ordinal sequences. Let us consider now the dataset SyntheticData2 and assume that the clustering structure is governed by the similarity between underlying models. In other terms, the ground truth is given by the 4 groups involving the 20 series from the same generating process (a specific binomial INARCH(p) process). We wish to perform clustering and, according to our criterion, the clustering effectiveness of each algorithm must be measured by comparing the experimental solution with the true partition defined by these four groups.

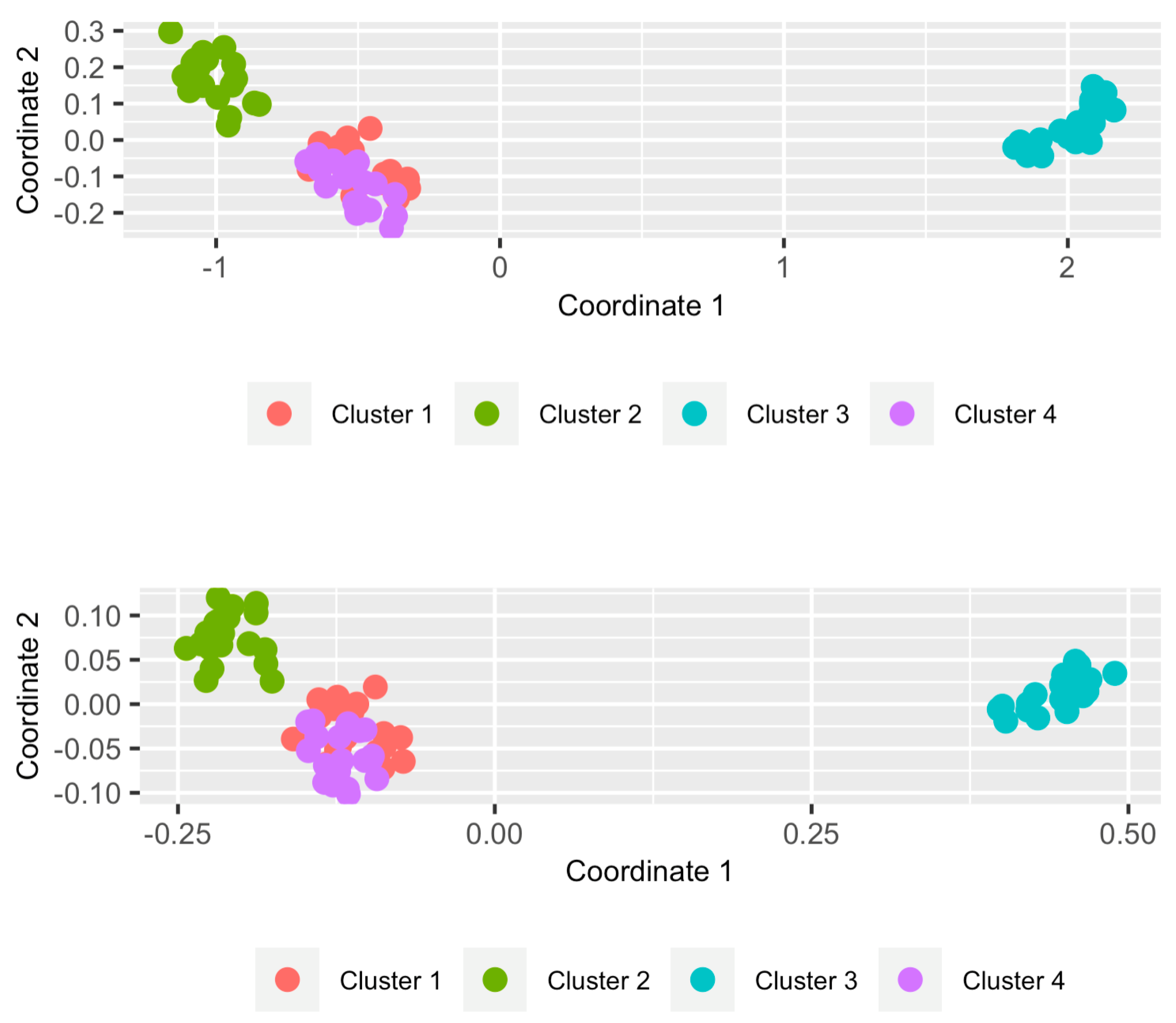

In cluster analysis, distances between data objects play an essential role. In our case, a suitable metric should take low values for pairs of series coming from the same stochastic process, and high values otherwise. A classical exploratory step to shed light on the quality of a particular metric consists of constructing a two-dimensional scaling (2DS) based on the corresponding pairwise distance matrix. In short, 2DS represents the pairwise distances in terms of Euclidean distances into a two-dimensional space preserving the original values as much as possible (by minimizing a loss function). For instance, we are going to construct the 2DS for dataset

SyntheticData2 by using two specific distances between CTS proposed by [

12] and denoted by

and

. More specifically, given two OTS

and

, the metrics

and

are defined as follows:

where

is a set of

L lags which must be determined in advance and the superscripts (1) and (2) indicate that the corresponding estimates are based on the realizations

and

, respectively. Both dissimilarities assess discrepancies between the marginal distributions (first terms) and the serial dependence structures (last terms) of both series. Therefore, they seem appropriate to group the CTS of a given collection in terms of underlying stochastic processes. However, note that the distance

is based on cumulative probabilities, thus taking into account the underlying ordering existing in the series range.

Let us first create the datasets dataset_1 and dataset_2 with the features required to compute and , respectively. As the series in SyntheticData2 were generated from binomial INARCH(1) and binomial INARCH(2) processes, we consider only the first two lags to construct the distance, i.e., we set . We have to use the argument features = TRUE in the corresponding functions.

> list_marginal_1 <- lapply(SyntheticData2$data,

c_marginal_probabilities, states = 0 : 5)

> list_serial_1_1 <- lapply(SyntheticData2$data,

c_joint_probabilities, states = 0 : 5, lag = 1)

> list_serial_1_2 <- lapply(SyntheticData2$data,

c_joint_probabilities, states = 0 : 5, lag = 2)

> dataset_marginal_1 <- matrix(unlist(list_marginal_1),

nrow = 80, byrow = T)

> dataset_serial_1_1 <- matrix(unlist(list_serial_1_1),

nrow = 80, byrow = T)

> dataset_serial_1_2 <- matrix(unlist(list_serial_1_2),

nrow = 80, byrow = T)

> dataset_1 <- cbind(dataset_marginal_1, dataset_serial_1_1,

dataset_serial_1_2)

> list_marginal_2 <- lapply(SyntheticData2$data,

marginal_probabilities, states = 0 : 5)

> list_serial_2_1 <- lapply(SyntheticData2$data,

joint_probabilities, states = 0 : 5, lag = 1)

> list_serial_2_2 <- lapply(SyntheticData2$data,

joint_probabilities, states = 0 : 5, lag = 2)

> dataset_marginal_2 <- matrix(unlist(list_marginal_2),

nrow = 80, byrow = T)

> dataset_serial_2_1 <- matrix(unlist(list_serial_2_1),

nrow = 80, byrow = T)

> dataset_serial_2_2 <- matrix(unlist(list_serial_2_2),

nrow = 80, byrow = T)

> dataset_2 <- cbind(dataset_marginal_2, dataset_serial_2_1,

dataset_serial_2_2)

The 2DS planes can be built using the function

plot_2d_scaling() of the R package

mlmts [

22], which takes as input a pairwise dissimilarity matrix.

> library(mlmts)

> distance_matrix_1 <- dist(dataset_1)

> plot_1 <- plot_2d_scaling(distance_matrix_1,

cluster_labels = otsfeatures::SyntheticData2$classes)$plot

> distance_matrix_2 <- dist(dataset_2)

> plot_2 <- plot_2d_scaling(distance_matrix_2,

cluster_labels = otsfeatures::SyntheticData2$classes)$plot

In the above code, the syntax

otsfeatures:: was employed because package

mlmts includes a data collection which is also called

SyntheticData2. The resulting plots are shown in

Figure 2. In both cases, the points were colored according to the true partition defined by the generating models. For this, we had to include the argument

cluster_labels in the function

plot_2d_scaling(). This option is indeed useful to examine whether a specific metric is appropriate when the true class labels are known. The 2DS planes reveal that both metrics are able to identify the underlying structure rather accurately. However, there are two specific groups of OTS (the ones represented by red and purple points) exhibiting a certain degree of overlap in both plots, which suggests a high level of similarity between the corresponding generating processes.

To evaluate the clustering accuracy of both metrics, we consider the popular partitioning around medoids (PAM) algorithm, which is implemented in R through the function

pam() of package

cluster [

23]. This function needs the pairwise distance matrix and the number of clusters. The latter argument is set to 4, since the series in dataset

SyntheticData2 were generated from 4 different stochastic processes.

> library(cluster)

> clustering_pam_1 <- pam(distance_matrix_1, k = 4)$clustering

> clustering_pam_2 <- pam(distance_matrix_2, k = 4)$clustering

The vectors

clustering_pam_1 and

clustering_pam_2 provide the respective clustering solutions based on both metrics. The evaluation of the quality of both partitions requires measuring their degree of agreement with the ground truth, which can be performed by using the Adjusted Rand Index (ARI) [

24]. This index can be easily computed by means of the function

external_validation() of package

ClusterR [

25].

> library(ClusterR)

> external_validation(clustering_pam_1,

otsfeatures::SyntheticData2$classes)

[1] 0.6545303

> external_validation(clustering_pam_2,

otsfeatures::SyntheticData2$classes)

[1] 0.6535088

The ARI index is bounded between −1 and 1 and admits a simple interpretation: the closer it is to 1, the better the agreement between the ground truth and the experimental solution is. Moreover, the value of 0 is associated with a clustering partition picked at random according to some simple hypotheses. Therefore, it can be concluded that both metrics

and

, respectively attain moderate scores in this dataset when used with the PAM algorithm. In particular, both partitions are substantially similar. Note that a nonperfect value of ARI index was already expected from the 2DS plots in

Figure 2 due to the overlapping character of Clusters 1 and 4.

The classical

K-means clustering algorithm can be also executed by using

otsfeatures utilities. In this case, we need to employ a dataset of features along with the

kmeans() function of package stats [

13].

set.seed(123)

clustering_kmeans_1 <- kmeans(dataset_1, c = 4)$cluster

external_validation(clustering_kmeans_1,

otsfeatures::SyntheticData2$classes)

[1] 0.6545303

> set.seed(123)

> clustering_kmeans_2 <- kmeans(dataset_2, c = 4)$cluster

> external_validation(clustering_kmeans_2,

otsfeatures::SyntheticData2$classes)

[1] 0.7237974

In the previous example, slightly better results are obtained when the is employed along with the K-means algorithm. Concerning , its clustering accuracy is exactly the same as the one associated with the PAM algorithm. The performance of alternative dissimilarities or collections of features regarding a proper identification of the underlying clustering structure could be determined by following the same steps than in the previous experiments.

4.3.3. Performing Outlier Detection in OTS Datasets

The topic of outlier detection has received a lot of attention in the literature, either in the nontemporal setting (see, e.g., [

26] for a review on outlier detection methods for univariate data) or in the context of time series data (see, e.g., [

27] for a review on anomaly detection in time series data). Concerning the latter subject, it is worth noting that different notions of outlier are considered in this context (additive outliers, innovative outliers, and others). Here, we consider the outlying elements to be whole OTS objects. More specifically, an anomalous OTS is assumed to be a series generated from a stochastic process different from those generating the majority of the series in the database.

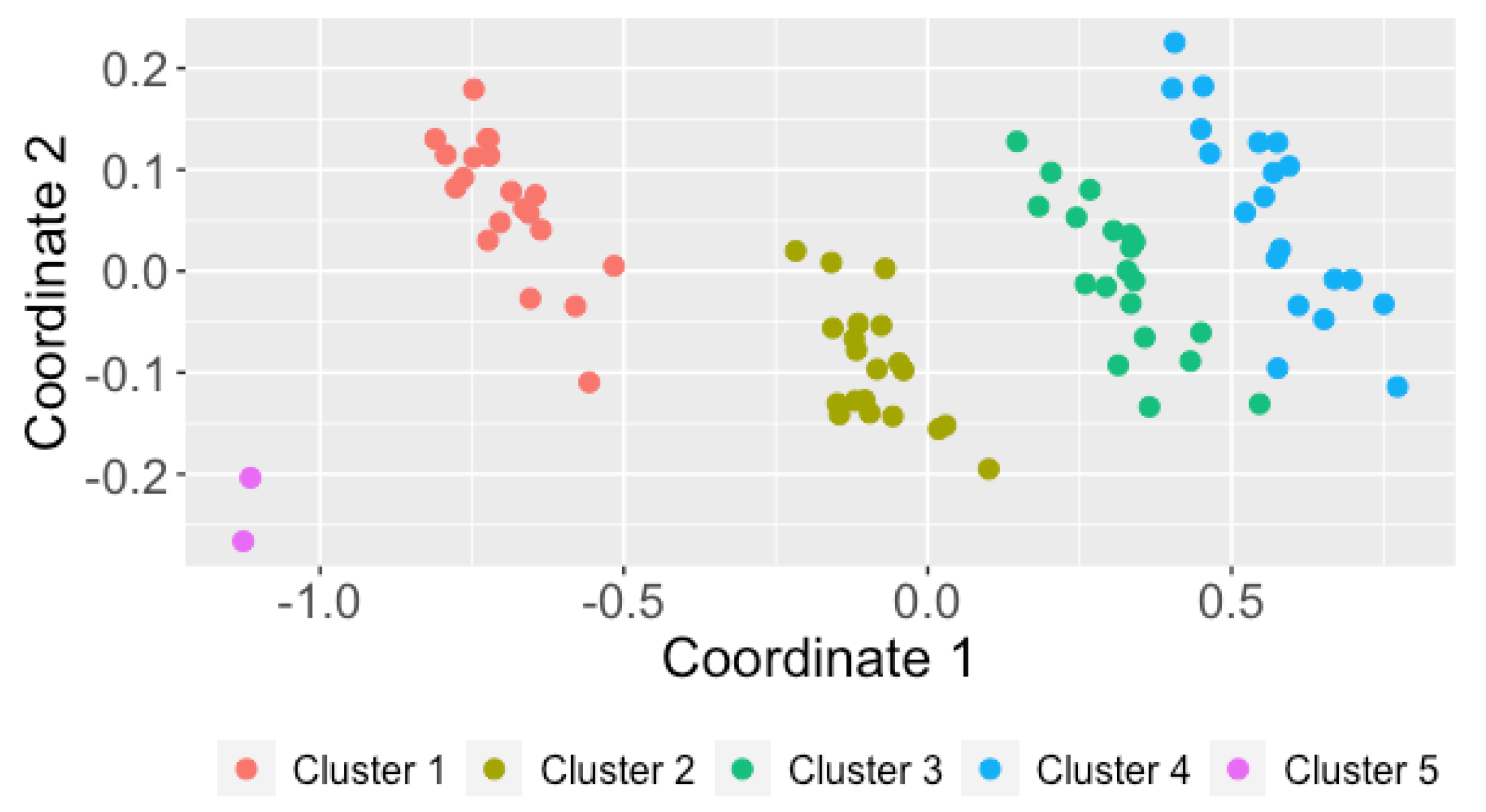

To illustrate how otsfeatures can be useful to carry out outlier identification, we create a dataset which includes two atypical elements. For it, we consider all the series in SyntheticData3 along with the first two series in dataset SyntheticData2.

The resulting data collection,

data_outliers, contains 82 OTS. The first 80 OTS can be split into four homogeneous groups of 20 series, but those located into positions 81 and 82 are actually anomalous elements in the collection because they come from an ordinal logit AR(1) model (see

Section 3.1).

A distance-based approach to perform anomaly detection consists of obtaining the pairwise distance matrix and proceeding in two steps as follows.

- Step 1.

For each element, compute the sum of its distances from the remaining objects in the dataset, which is expected to be large for anomalous elements.

- Step 2.

Sort the quantities computed in Step 1 in decreasing order and reorder the indexes according to this order. The first indexes in this new vector correspond to the most outlying elements, while the last ones to the least outlying elements.

We follow this approach to examine whether the outlying OTS in

data_outliers can be identified by using the distance

given in (

17). First, we construct the pairwise dissimilarity matrix based on this metric for the new dataset.

> list_outl_1 <- lapply(data_outliers, c_marginal_probabilities,

states = 0 : 5)

> list_outl_2 <- lapply(data_outliers, c_joint_probabilities,

states = 0 : 5, lag = 1)

> list_outl_3 <- lapply(data_outliers, c_joint_probabilities,

states = 0 : 5, lag = 2)

> dataset_outl_1 <- matrix(unlist(list_outl_1), nrow = 82, byrow = T)

> dataset_outl_2 <- matrix(unlist(list_outl_2), nrow = 82, byrow = T)

> dataset_outl_3 <- matrix(unlist(list_outl_3), nrow = 82, byrow = T)

> dataset_outl <- cbind(dataset_outl_1, dataset_outl_2, dataset_outl_3)

> distance_matrix_outl <- dist(dataset_outl)

Then, we apply the mentioned two-step procedure to matrix distance_matrix_outl by running

The previous output corroborates that is able to properly identify the two series generated from anamalous stochastic processes. As an illustrative exercise, let us represent the corresponding 2DS plot for the dataset containing the two outlying OTS by using a different color for these elements.

> library(mlmts)

> labels <- c(otsfeatures::SyntheticData2$classes, 5, 5)

> plot_2d_scaling(distance_matrix_outl, cluster_labels = labels)$plot

The corresponding graph is shown in

Figure 3. The 2DS configuration contains four groups of points which are rather well separated, plus two isolated elements representing the anomalous series appearing on the left part of the plot. Clearly, 2DS plots can be very useful for outlier identification purposes, since they provide a great deal of information on both the number of potential outliers and their location with respect to the remaining elements in the dataset.

In the previous example, the number of outliers was assumed to be known, which is not realistic in practice. In fact, when dealing with real OTS databases, one usually needs to determine whether the dataset at hand contains outliers. To that aim, it is often useful to define a measure indicating the outlying nature of each object (see, e.g., [

28,

29]), i.e., those elements with an extremely large scoring could be identified as outliers. In order to illustrate this approach, we consider the dataset

CreditRatings and compute the pairwise distance matrix according to distance

.

> list_cr_1 <- lapply(CreditRatings$data,

marginal_probabilities, states = 0 : 22)

> list_cr_2 <- lapply(CreditRatings$data,

joint_probabilities, states = 0 : 22, lag = 1)

> list_cr_3 <- lapply(CreditRatings$data,

joint_probabilities, states = 0 : 22, lag = 2)

> dataset_cr_1 <- matrix(unlist(list_cr_1),

nrow = 28, byrow = T)

> dataset_cr_2 <- matrix(unlist(list_cr_2),

nrow = 28, byrow = T)

> dataset_cr_3 <- matrix(unlist(list_cr_3),

nrow = 28, byrow = T)

> dataset_cr <- cbind(dataset_cr_1, dataset_cr_2,

dataset_cr_3)

> distance_matrix_cr <- dist(dataset_cr)

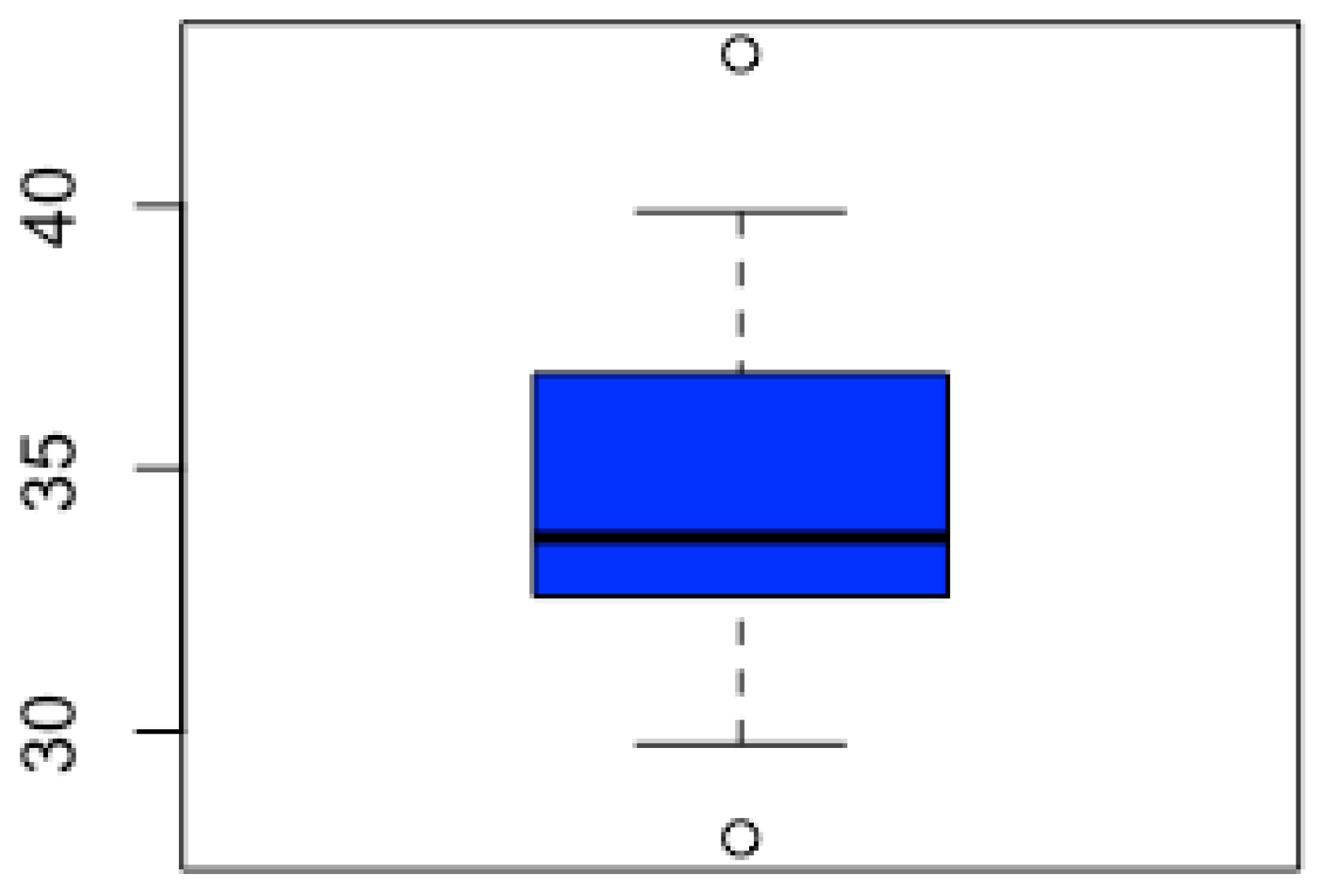

As before, the sum of the distances between each series and the remaining ones is computed.

The vector outlier_score contains the sum of the distances for each of the 28 countries. Since the ith element of this vector can be seen as a measure of the outlying character of the ith series, those countries associated with extremely large values in this vector are potential outliers. A simple way to detect these series consists of visualizing a boxplot based on the elements of outlier_score and checking whether there are points located into the upper part of the graph.

The resulting boxplot is shown in

Figure 4 and suggests the existence of one series with an abnormally high outlying score. Hence, this country could be considered to be anomalous and its individual properties be carefully investigated. Specifically, the uppermost point in

Figure 4 corresponds to Belgium. Note that the prior empirical approach provides an automatic method to determine the number of outliers. Similar analyses could be carried out by considering alternative dissimilarity measures.

5. Conclusions and Future Work

Statistical analysis of time series has experienced significant growth during the last 50 years. Although the majority of works focus on real-valued time series, ordinal time series have received a great deal of attention during the present century. The R package otsfeatures is fundamentally an attempt to provide different functions allowing the calculation of well-known statistical quantities for ordinal series. As well as providing an useful description about the behavior of the time series, the corresponding quantities can be used as input for traditional data mining procedures, as clustering, classification, and outlier detection algorithms. Additionally, otsfeatures includes some tools enabling the execution of classical inferential tasks, as hypothesis tests. It is worth highlighting that several functions of the package can also be used to analyze ordinal data without a temporal nature. The main motivation behind the package is that, to the best of our knowledge, no previous R packages are available for a general statistical analysis of ordinal datasets. In fact, the few software tools designed to deal with this class of databases focus on specific tasks (e.g., clustering or classification), application areas, or types of ordinal models. Package otsfeatures also incorporates two databases of financial time series and three synthetic datasets, which can be used for illustrative purposes. Although otsfeatures is rather simple, it provides the much-needed tools for the standard analyses which are usually performed before more complex tasks as modeling, inference, or forecasting.

A description of the functions available in otsfeatures is given in the first part of this manuscript to make clear the details behind the software and its scope. However, the readers particularly interested in specific tools are encouraged to check the corresponding key references, which are also provided in the paper. In the second part of the manuscript, the use of the package is illustrated by considering several examples involving synthetic and real data. This can be seen as a simple overview whose goal is to make the process of using otsfeatures as easy as possible for first-time users.

There are three main ways through which this work can be extended. First, as

otsfeatures is under continuous development, we expect to perform frequent updates by incorporating functions for the computation of additional statistical features which are introduced in the future. Second, note that the statistical quantities available in

otsfeatures are defined for univariate time series. However, multivariate time series [

29,

30] are becoming more and more common due to the advances in the storage capabilities of everyday devices. Thus, a software package allowing the computation of statistical features for multivariate ordinal series could be constructed in the future. Note that

otsfeatures assumes that all the values of a given time series are known. Although this assumption is entirely reasonable, it can become too restrictive in practice, since some OTS can include missing values. In this regard, it would be interesting to implement some functions aimed at properly correcting these values so that the computation of ordinal features is not negatively affected.

{kind=link}

{kind=link}

{kind=link}

{kind=link}