The Macroeconomic Effects of an Interest-Bearing CBDC: A DSGE Model

Abstract

:1. Introduction

2. Related Works: Modeling CBDC

2.1. Non-DSGE Models

2.2. DSGE Models

2.3. Open Economy Models

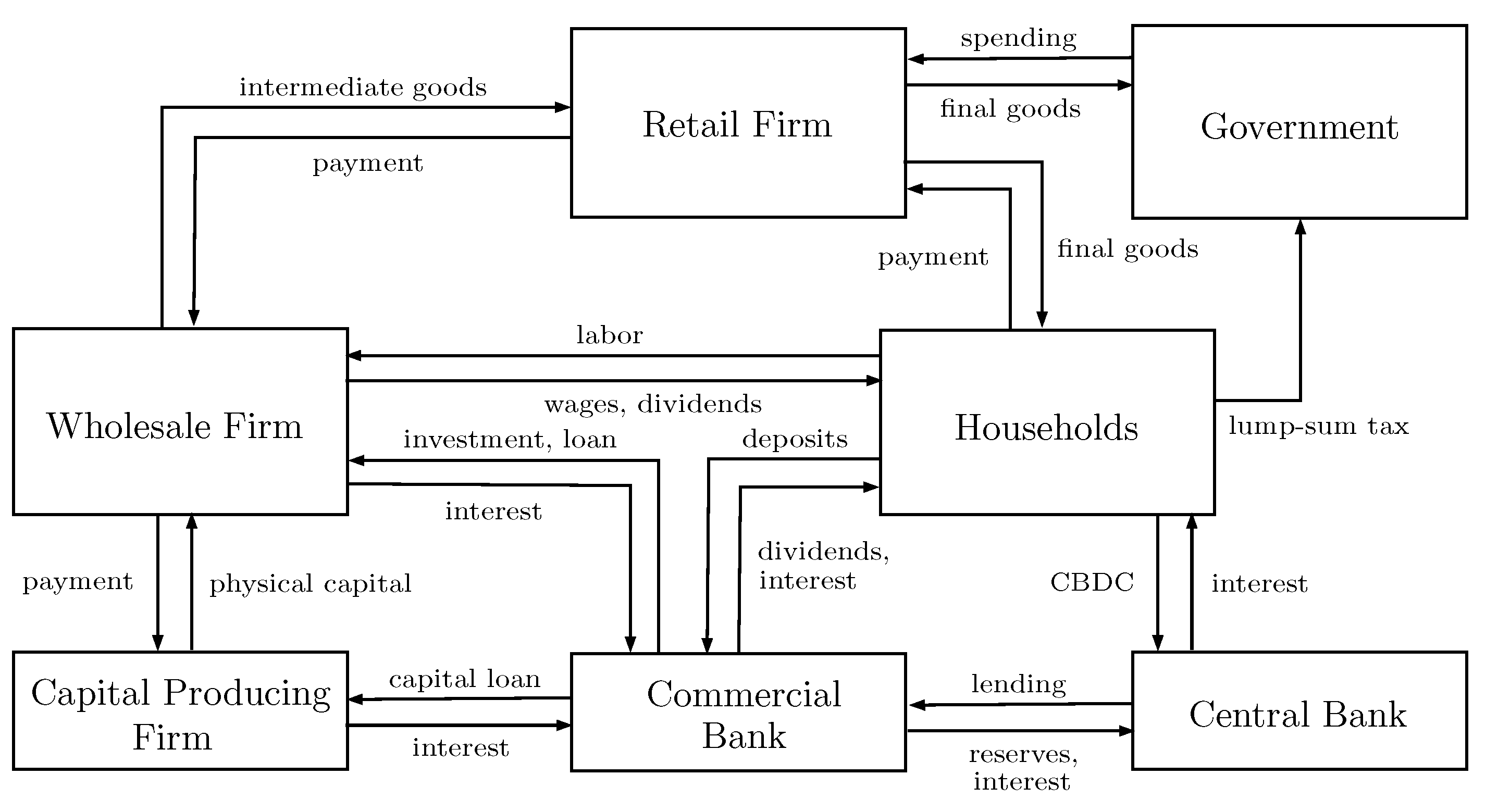

3. The Model Economy

3.1. Assumptions

- 1.

- 2.

- In the profit maximization of wholesale firms, we adopt the so-called Calvo price setting mechanism, where firms have a certain probability of either keeping the price fixed in the next period or optimally determining the price [12].

- 3.

- 4.

- Government bonds are held by banks and the central bank.

- 5.

- To quantify the effect of disruptions by economic shocks, our model is equipped with three shock generators, namely productivity shock, liquidity demand shock, and the monetary policy shock.

3.2. Households

3.3. Retail Firms

3.4. Wholesale Firms

3.4.1. The Cost Minimization Problem

3.4.2. The Profit Maximization Problem

3.5. Capital Producing Firms

3.6. Banks

3.7. The Central Bank

3.8. The Government

4. Log-Linearization

5. Calibration

6. Policy Analysis

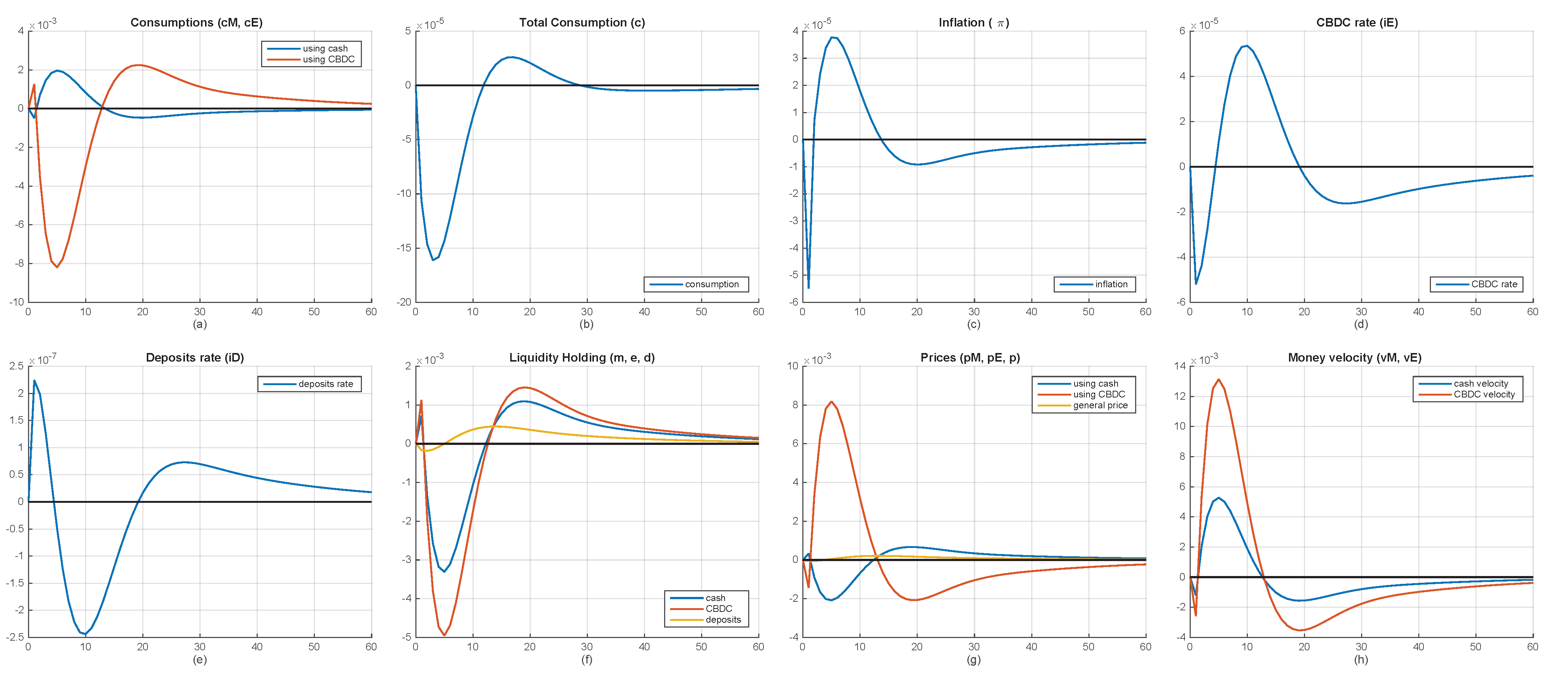

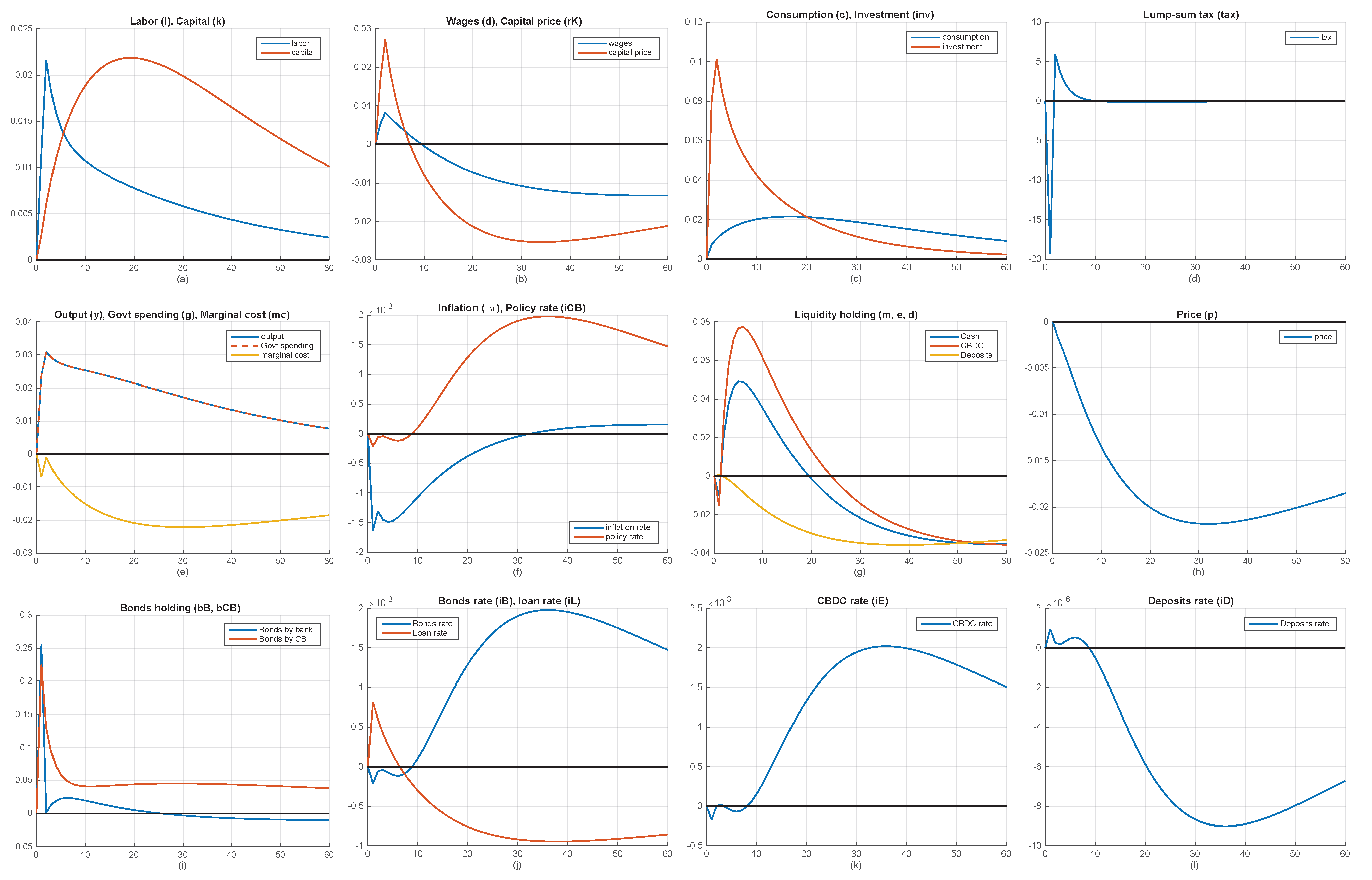

6.1. Effects of Liquidity Demand Shock

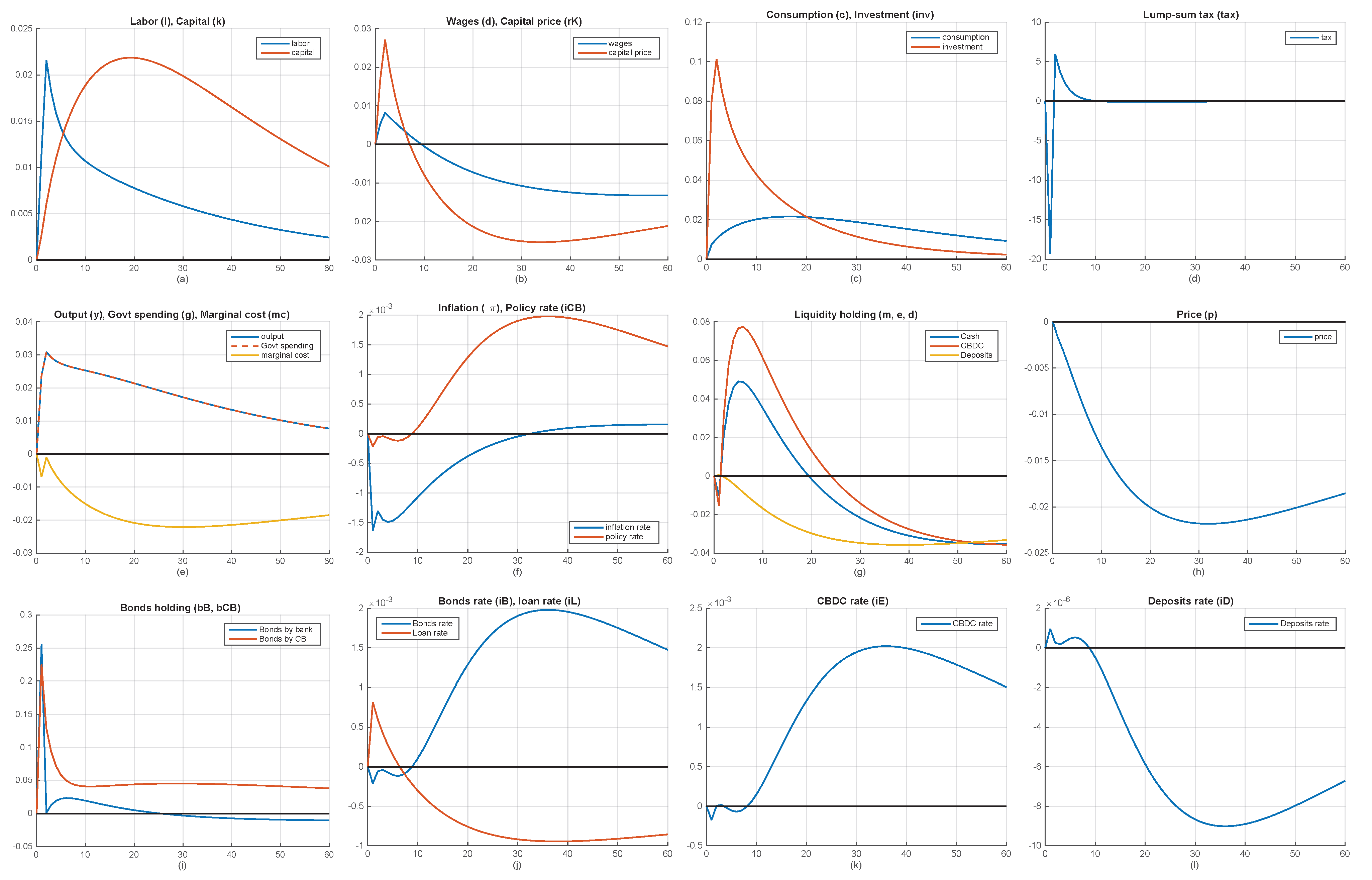

6.2. Effects of Productivity Shock

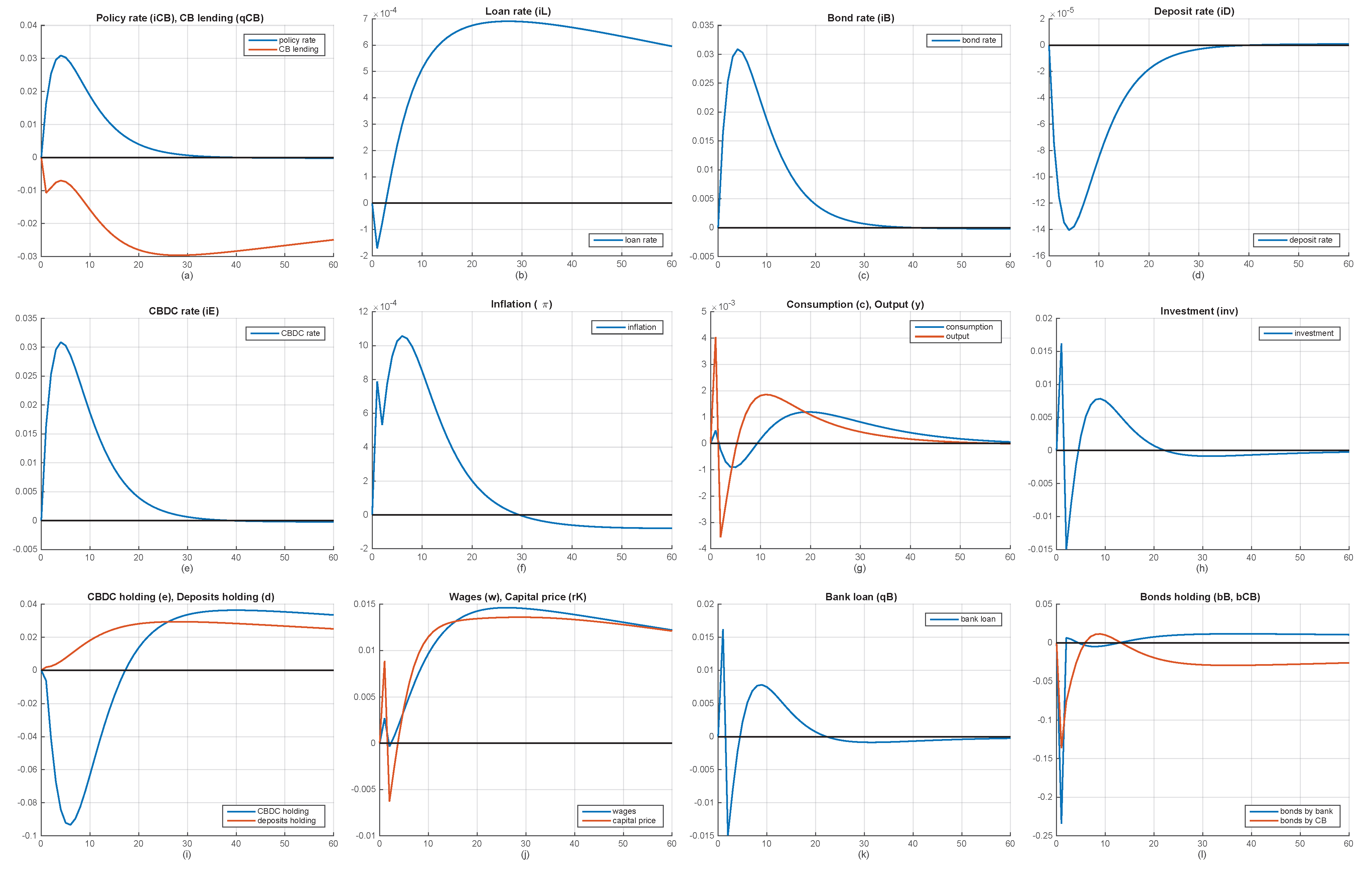

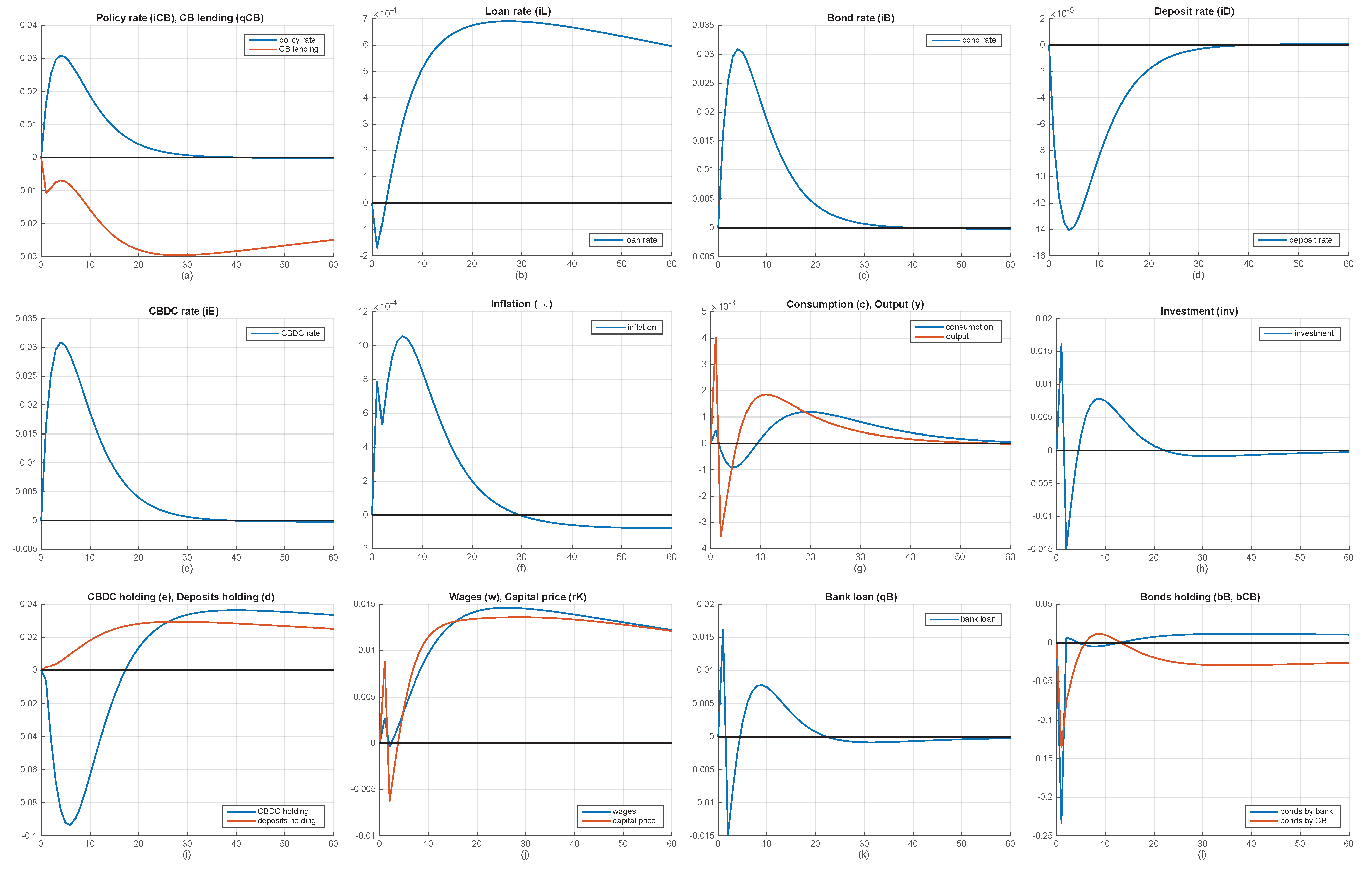

6.3. Effects of Monetary Policy Shock

6.4. Implementation of the Analytical Model

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Log-Linearized Equations

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| No. | Variable | Description |

|---|---|---|

| 1 | Productivity shock | |

| 2 | Government bonds | |

| 3 | Government bonds held by commercial bank | |

| 4 | Government bonds held by central bank | |

| 5 | Consumption by households | |

| 6 | Consumption by households using cash | |

| 7 | Consumption by households using CBDC | |

| 8 | Bank deposits holding by households | |

| 9 | CBDCs holding by households | |

| 10 | Government spending | |

| 11 | Nominal interest rate of government bonds | |

| 12 | Nominal interest rate by central bank (policy rate) | |

| 13 | Nominal interest rate of bank deposits | |

| 14 | Nominal interest rate of CBDC | |

| 15 | Nominal interest rate of loans | |

| 16 | Investment level | |

| 17 | Capital stocks | |

| 18 | Labor supply by households | |

| 19 | Cash holding by households | |

| 20 | Marginal cost | |

| 21 | Bank’s equity | |

| 22 | Price | |

| 23 | Price in cash | |

| 24 | Price in CBDC | |

| 25 | Inflation rate | |

| 26 | Loans given to commercial banks by central bank | |

| 27 | Price of capital | |

| 28 | Transaction cost for cash | |

| 29 | Transaction cost for CBDC | |

| 30 | Lump sum tax or transfer | |

| 31 | Reserves | |

| 32 | Monetary policy shock | |

| 33 | Wages | |

| 34 | Output | |

| 35 | Cash demand shock | |

| 36 | CBDC demand shock |

- 1.

- Labor supply:

- 2.

- CBDC demand:

- 3.

- Cash demand:

- 4.

- Deposits demand:

- 5.

- Euler equation:

- 6

- Consumptions using cash and CBDC:

- 7.

- Total consumption with transaction costs:

- 8.

- Transaction costs:

- 9.

- General price level:

- 10.

- Capital stocks:

- 11.

- Cobb–Douglas production function:

- 12.

- Optimal levels of labor and capital:

- 13.

- Marginal cost:

- 14.

- 15.

- Capital producing firm:

- 16.

- Bank’s balance sheet:

- 17.

- Bank’s equity:

- 18.

- Loan interest rate:

- 19.

- Deposits interest rate:

- 20.

- Bonds and CBDC interest rates are already given in linear forms:

- 21.

- Taylor rule is also given in linear form:

- 22.

- Central bank’s balance sheet:

- 23.

- Government’s budget constraint:

- 24.

- Economy-wide budget constraint:

- 25.

- Government expenditure:

- 26.

- Shock generators:where , , , and are exogenous shock variables.

Appendix B. Proof of Households Utility Maximization

Appendix C. Proof of Consumption and Price Indices

Appendix D. Derivation of Phillips Curve

References

- Pasuthip, P.; Yang, S. Central Bank Digital Currency: Promises and Risks; Academic Press: Cambridge, MA, USA, 2020. [Google Scholar]

- Bank for International Settlements (BIS). COVID-19 Accelerated the Digitalisation of Payments; Committee on Payments and Market Infrastructures: Basel, Switzerland, 2021. [Google Scholar]

- Balz, B. COVID-19 and cashless payments—Has coronavirus changed Europeans’ love of cash? In Proceedings of the Small and Medium Entrepreneurs Europe (SME Europe), Virtual Event, 21 October 2020. [Google Scholar]

- Kotkowski, R.; Polasik, M. COVID-19 pandemic increases the divide between cash and cashless payment users in Europe. Econ. Lett. 2021, 209, 110139. [Google Scholar] [CrossRef] [PubMed]

- Boar, C.; Holden, H.; Wadsworth, A. Impending Arrival—A Sequel to the Survey on Central Bank Digital Currency; BIS: Basel, Switzerland, 2020. [Google Scholar]

- Klein, M.; Gross, J.; Sandner, P. The Digital Euro and the Role of DLT for Central Bank Digital Currencies; FSBC Working Paper; Frankfurt School Blockchain Center: Frankfurt, Germany, 2020. [Google Scholar]

- Alonso, S.L.N.; Jorge-Vazquez, J.; Forradellas, R.F.R. Central banks digital currency: Detection of optimal countries for the implementation of a CBDC and the implication for payment industry open innovation. J. Open Innov. Technol. Mark. Complex. 2021, 7, 72. [Google Scholar] [CrossRef]

- Gross, J.; Schiller, J. A model for central bank digital currencies: Implications for bank funding and monetary policy. SSRN Pap. 2021, 3721965, 1–46. [Google Scholar] [CrossRef]

- Carapella, F.; Flemming, J. Central Bank Digital Currency: A Literature Review; FEDS Notes; Board of Governors of the Federal Reserve System: Washington, DC, USA, 2020. [Google Scholar]

- Sidrauski, M. Rational choice and patterns of growth in a monetary economy. Am. Econ. Rev. 1967, 57, 534–544. [Google Scholar]

- Blanchard, O.; Fischer, S. Lectures on Macroeconomics; MIT Press: Cambridge, MA, USA, 1989. [Google Scholar]

- Calvo, G.A. Staggered prices in a utility-maximizing framework. J. Monet. Econ. 1983, 1, 383–398. [Google Scholar] [CrossRef]

- Bindseil, U. Tiered CBDC and the Financial System; ECB Working Paper Series No. 2351; European Central Bank: Frankfurt, Germany, 2020. [Google Scholar]

- Christiano, L.J.; Eichenbaum, M.; Evans, C.L. Nominal rigidities and the dynamic effects of a shock to monetary policy. J. Political Econ. 2005, 113, 1–45. [Google Scholar] [CrossRef] [Green Version]

- Smets, F.; Wouters, R. Shocks and frictions in US business cycles: A bayesian DSGE approach. Am. Econ. Rev. 2007, 97, 586–606. [Google Scholar] [CrossRef] [Green Version]

- Ferrari, M.M.; Mehl, A.; Stracca, L. Central Bank Digital Currency in an Open Economy; Working Paper No. 2488; European Central Bank: Frankfurt, Germany, 2020. [Google Scholar]

- Agur, I.; Ari, A.; Dell’Ariccia, G. Designing central bank digital currencies. J. Monet. Econ. 2022, 125, 62–79. [Google Scholar] [CrossRef]

- Andolfatto, D. Assessing the Impact of Central Bank Digital Currency on Private Banks; Working Paper 2018-026; Federal Reserve Bank of St. Louis: St. Louis, MO, USA, 2018. [Google Scholar]

- Davoodalhosseini, S.M.R. Central Bank Digital Currency and Monetary Policy; Staff Working Paper 2018-36; Bank of Canada: Ottawa, ON, Canada, 2018. [Google Scholar]

- Williamson, S.D. Central bank digital currency and flight to safety. J. Econ. Dyn. Control 2021, 104146, in press. [Google Scholar] [CrossRef]

- Chiu, J.; Jiang, J.H.; Davoodalhosseini, S.M.R.; Zhu, Y. Central bank digital currency and banking. In Proceedings of the Society for Economic Dynamics: 2018 Annual Meeting of the Society for Economic Dynamics, Mexico City, Mexico, 28–30 June 2018. [Google Scholar]

- Chiu, J.; Jiang, J.H.; Davoodalhosseini, S.M.R.; Zhu, Y. Bank Market Power and Central Bank Digital Currency: Theory and Quantitative Assessment; Staff Working Paper No. 2019-20; Bank of Canada: Ottawa, ON, Canada, 2020. [Google Scholar]

- Keister, T.; Monnet, C. Central bank digital currency: Stability and information. In Proceedings of the 2018 Annual Research Conference of the Swiss National Bank and the Bank of Canada/Riksbank Conference on the Economics of Central Bank Digital Currencies, Ottawa, ON, Canada, 17–18 October 2019. [Google Scholar]

- Fernandez-Villaverde, J.; Sanches, D.; Schilling, L.; Uhlig, H. Central bank digital currency: Central banking for all? Rev. Econ. Dyn. 2021, 41, 225–242. [Google Scholar] [CrossRef]

- Kim, Y.S.; Kwon, O. Central Bank Digital Currency and Financial Stability; Working Paper; Bank of Korea: Seoul, Korea, 2019. [Google Scholar]

- Bitter, L. Banking crises under a central bank digital currency (CBDC). In Beitrage zur Jahrestagung des Vereins fur Socialpolitik 2020: Gender Economics; ZBW—Leibniz Information Centre for Economics: Kiel, Germany, 2020. [Google Scholar]

- Skeie, D.R. Digital Currency Runs; Chief Economists Workshop; Bank of England: London, UK, 2020. [Google Scholar]

- Christiano, L.J.; Eichenbaum, M.S.; Trabandt, M. On DSGE models. J. Econ. Perspect. 2018, 32, 113–140. [Google Scholar] [CrossRef] [Green Version]

- Stiglitz, J.E. Where modern macroeconomics went wrong. Oxf. Rev. Econ. Policy 2018, 24, 70–106. [Google Scholar] [CrossRef]

- Vines, D.; Wills, S. The rebuilding macroeconomic theory project: An analytical assessment. Oxf. Rev. Econ. Policy 2018, 34, 1–42. [Google Scholar] [CrossRef]

- Blanchard, O. PB 16-11 Do DSGE Models Have a Future? Peterson Institute for International Economics Policy Brief. August 2016, pp. 1–4. Available online: https://www.piie.com/system/files/documents/pb16-11.pdf (accessed on 28 April 2022).

- Hurtado, S. DSGE models and the Lucas critique. Econ. Model. 2014, 44, S12–S19. [Google Scholar] [CrossRef] [Green Version]

- Hoffmann, A. An overinvestment cycle in Central and Eastern Europe? Metroeconomica 2010, 61, 711–734. [Google Scholar] [CrossRef] [Green Version]

- Hoffmann, A.; Schnabl, G. A vicious cycle of manias, crises and asymmetric policy responses—An overinvestment view. World Econ. 2011, 34, 382–403. [Google Scholar] [CrossRef] [Green Version]

- Hoffmann, A.; Schnabl, G. National Monetary Policy, International Economic Instability and Feeback Effects—An Overinvestment View; Working Papers on Global Financial Markets No. 19; Universität Halle-Wittenberg: Halle, Germany, 2011. [Google Scholar]

- Ghironi, F. Macro needs micro. Oxf. Rev. Econ. Policy 2018, 34, 195–218. [Google Scholar] [CrossRef]

- Linde, J. DSGE models: Still useful in policy analysis? Oxf. Rev. Econ. Policy 2018, 34, 269–286. [Google Scholar] [CrossRef]

- Barrdear, J.; Kumhof, M. The macroeconomics of central bank digital currencies. J. Econ. Dyn. Control 2021, 104148, in press. [Google Scholar] [CrossRef]

- Luo, S.; Zhou, G.; Zhou, J. The impact of electronic money on monetary policy: Based on DSGE model simulations. Mathematics 2021, 9, 2614. [Google Scholar] [CrossRef]

- Lim, K.Y.; Liu, C.; Zhang, S. Optimal Central Banking Policies: Envisioning the Post-Digital Yuan Economy with Loan Prime Rate-Setting; Discussion Papers in Economics No. 2021/2; Nottingham Trent University: Nottingham, UK, 2021. [Google Scholar]

- George, A.; Xie, T.; Alba, J.D. Central Bank Digital Currency with Adjustable Interest Rate in Small Open Economies; Policy Research Paper No. 05-2020; Asia Competitiveness Institute, National University of Singapore: Singapore, 2020. [Google Scholar]

- Benigno, P.; Schilling, L.M.; Uhlig, H. Cryptocurrencies, Currency Competition, and the Impossible Trinity; NBER Working Papers 26214; National Bureau of Economic Research: Cambridge, MA, USA, 2019. [Google Scholar] [CrossRef]

- Gertler, M.; Karadi, P. A model of unconventional monetary policy. J. Monet. Econ. 2011, 58, 17–34. [Google Scholar] [CrossRef]

- Primus, K. Excess reserves, monetary policy and financial volatility. J. Bank. Financ. 2017, 74, 153–168. [Google Scholar] [CrossRef] [Green Version]

- Michaillat, P.; Saez, E. Resolving New Keynesian anomalies with wealth in the utility function. Rev. Econ. Stat. 2018, 103, 197–215. [Google Scholar] [CrossRef] [Green Version]

- Schmitt-Grohe, S.; Uribe, M. Foreign demand for domestic currency and the optimal rate of inflation. J. Money Credit. Bank. 2012, 44, 1207–1224. [Google Scholar] [CrossRef]

- Dixit, A.K.; Stiglitz, J.E. Monopolistic competition and optimum product diversity. Am. Econ. Rev. 1977, 67, 297–308. [Google Scholar]

- Agenor, P.-R.; Alper, K.; da Silva, L.P. Capital regulation, monetary policy, and financial stability. Int. J. Cent. Bank. 2013, 9, 198–243. [Google Scholar]

- Uhlig, H. A toolkit for analysing nonlinear dynamic stochastic models easily. In Computational Methods for the Study of Dynamic Economies; Marimon, R., Scott, A., Eds.; Oxford University Press: New York, NY, USA, 1999; pp. 30–61. [Google Scholar]

- Chawwa, T. Impact of reserve requirement and liquidity coverage ratio: A DSGE model for Indonesia. Econ. Anal. Policy 2021, 71, 321–341. [Google Scholar] [CrossRef]

- Piazzesi, M.; Rogers, C.; Schneider, M. Money and banking in a New Keynesian model. Bank of Canada Annual Conference—The Future of Money and Payments: Implications for Central Banking, Canada, ON, USA, 5–7 November 2020. [Google Scholar]

- Harmanta; Purwanto, N.M.A.; Rachmanto, A.; Oktiyanto, F. Monetary and macroprudential policy mix under financial frictions mechanism with DSGE model. In Proceedings of the International Economic Modeling Conference 2014 (EcoMod 2014), Bali, Indonesia, 16–18 July 2014; pp. 1–35. [Google Scholar]

- Angelini, P.; Neri, S.; Panetta, F. The interaction between capital requirements and monetary policy. J. Money Credit. Bank. 2014, 46, 1073–1112. [Google Scholar] [CrossRef]

- Syarifuddin, F. Optimal Central Bank Digital Currency (CBDC) Design for Emerging Economies; Working Paper; Bank Indonesia Institute: Jakarta, Indonesia, 2022. [Google Scholar]

- Bordo, M.; Levin, A. Central Bank Digital Currency and the Future of Monetary Policy; NBER Working Paper No. 23711; National Bureau of Economic Research: Cambridge, MA, USA, 2017. [Google Scholar]

- CPMI. Central Bank Digital Currencies; Markets Committee Paper No. 174; BIS: Basel, Switzerland, 2018; pp. 1–34. [Google Scholar]

- He, D.; Leckow, R.; Haksar, V.; Griffoli, T.; Jenkinson, N.; Kashima, M.; Khiaonarong, T.; Rochon, C.; Tourpe, H. Fintech and Financial Services: Initial Considerations; IMF Staff Discussion Notes No. 17/05; IMF: Washington, DC, USA, 2017. [Google Scholar]

- Agur, I.; Bernaga, M.; Bordo, M.; Engert, W.; Lis, S.; Fung, B.; Gnan, E.; Levin, A.; Niepelt, D.; Judson, R.; et al. Do we need central bank digital currency? In Proceedings of the SUERF—The European Money and Finance Forum and BAFFI CAREFIN Centre, Bocconi University, Milan, Italy, 7 June 2018. [Google Scholar]

- Nelson, B. The Benefits and Costs of a Central Bank Digital Currency for Monetary Policy; BPI Research Paper No. 202.589.2454; BSI: Basel, Switzerland, 2021. [Google Scholar]

- Mersch, Y. An ECB digital currency—A flight of fancy? In Proceedings of the Consensus 2020 Virtual Conference, New York, NY, USA, 11–13 May 2020. [Google Scholar]

- Wallis, J. Unlocking Financial Inclusion with CBDCs. Ripple Insight. 2021. Available online: https://ripple.com/insights/unlocking-financial-inclusion-with-cbdcs/ (accessed on 28 April 2022).

- Didenko, A.N.; Buckley, R.P. Central Bank Digital Currencies: A Potential Response to the Financial Inclusion Challenges of the Pacific; Issues in Pacicif Development No. 3; Asian Development Bank: Mandaluyong, Philippines, 2021; pp. 1–40. [Google Scholar]

- Nathan, A.; Galbraith, G.L.; Grimberg, J.; Bhushan, S.; Cahill, M.; Courvalin, D.; Pandl, Z.; Rosenberg, I.; Struyven, D.; Tilton, A.; et al. What’s in Store for the dollar. Goldman Sachs, 10 November 2020; 26p. [Google Scholar]

- Adam-Kalfon, P.; Arslanian, H.; Sok, K.; Sureau, B.; Jones, H.; Dou, Y. PwC CBDC Global Index, 1st ed.; PwC: London, UK, 2021. [Google Scholar]

- Mookerjee, A. What if central banks issued digital currency? Harvard Business Review, 15 October 2021; 1–11. [Google Scholar]

- Adrian, T. Stablecoins, central bank digital currencies, and cross-border payments: A new look at the international monetary system. In International Monetary Fund; 14 May 2019; pp. 1–5. [Google Scholar]

- An, Y.; Choi, P.; Huang, S. Blockchain, Cryptocurrency, and Artificial Intelligence in Finance; Springer: Singapore, 2021. [Google Scholar] [CrossRef]

- People’s Bank of China (PBoC). Progress of Research & Development of E-CNY in China. Working Group on E-CNY Research and Development; People’s Bank of China: Hong-Kong, China, 2021. [Google Scholar]

- Forner, G. Network Effects on Central Bank Digital Currencies and Blockchain Protocol Based Ledgers; Universita Ca’ Foscari Venezia: Venezia, Italy, 2020; Available online: http://hdl.handle.net/10579/17133 (accessed on 28 April 2022).

- Boar, C.; Wehrli, A. Ready, Steady, Go?—Results of the Third BIS Survey on Central Bank Digital Currency; BIS Papers No. 114; BIS: Basel, Switzerland, 2021; pp. 77–82. [Google Scholar]

- Gross, J.; Sedlmeir, J.; Babel, M.; Bechtel, A. Designing a Central Bank Digital Currency with Support for Cash-like Privacy; SSRN Papers No. 3891121; BIS: Basel, Switzerland, 2021. [Google Scholar]

- Vives, X. Digital disruption in banking. Annu. Rev. Financ. Econ. 2019, 11, 243–272. [Google Scholar] [CrossRef]

- Brugge, J.; Denecker, O.; Jawaid, H.; Kovacs, A.; Shami, I. Attacking the Cost of Cash; McKinsey & Company: Chicago, IL, USA, 2018; Available online: https://www.mckinsey.com/industries/financial-services/our-insights/attacking-the-cost-of-cash (accessed on 28 April 2022).

- ING Group. Central Bank Digital Currency in a European Context. ING, 2020 17 August 2020. [Google Scholar]

- Adrian, T.; Mancini-Griffoli, T. Central bank digital currencies: 4 questions and answers. IMF Blog, 12 December 2019. [Google Scholar]

- Borgonovo, E.; Caselli, S.; Cillo, A.; Masciandaro, D.; Rabitti, G. Central Bank Digital Currencies, Crypto Currencies, and Anonymity: Economics and Experiments; SUERF Policy Brief No. 222; SUERF: Wien, Austria, 2021. [Google Scholar]

- Jiang, J.; Lucero, K. Background and Implications of China’s Central Bank Digital Currency: E-CNY; SSRN Papers No. 3774479; Elservier: Amsterdam, The Netherlands, 2021. [Google Scholar]

- Shah, D.; Arora, R.; Du, H.; Darbha, S.; Miedema, J.; Minwalla, C. Technology Approach for a CBDC; Bank of Canada: Ottawa, ON, Canada, 25 February 2020. [Google Scholar] [CrossRef]

- Spivey, J. Technology Downtime: What’S Reasonable? (and What Isn’T?). WorkWingSwept Blog. 23 July 2021. Available online: https://www.wingswept.com/technology-downtime-whats-reasonable-and-what-isnt/ (accessed on 28 April 2022).

- Wadsworth, A. The pros and cons of issuing a central bank digital currency. Reserv. Bank N. Z. Bull. 2018, 8, 1–21. [Google Scholar]

- Auer, R.; Bohme, R. The technology of retail central bank digital currency. In BIS Quarterly Review; 1 March 2020; pp. 85–100. [Google Scholar]

- Minwalla, C. Security of a CBDC; Bank of Canada: Ottawa, ON, Canada, 24 June 2020. [Google Scholar] [CrossRef]

- Sveriges Riksbank. E-Krona Pilot Phase 1; Sveriges Riksbank Report; Sveriges Riksbank: Stockholm, Sweden, 2021; pp. 1–21. [Google Scholar]

- Agur, I. Central bank digital currencies: An overview of pros and cons. In Proceedings of the SUERF—The European Money and Finance Forum and BAFFI CAREFIN Centre Bocconi University, Milan, Italy, 7 June 2018; pp. 121–132. [Google Scholar]

- Goodell, G.; Aste, T. Can cryptocurrencies preserve privacy and comply with regulations? Front. Blockchain 2019, 2, 4. [Google Scholar] [CrossRef] [Green Version]

- Morales-Resendiz, R.; Ponce, J.; Picardo, P.; Velasco, A.; Chen, B.; Sanz, L.; Guiborg, G.; Segendorff, B.; Vasquez, J.L.; Arroyo, J.; et al. Implementing a retail CBDC: Lessons learned and key insights. Lat. Am. J. Cent. Bank. 2021, 2, 100022. [Google Scholar] [CrossRef]

| No. | Parameter | Description | Value |

|---|---|---|---|

| 1 | intertemporal discount factor | ||

| 2 | relative risk aversion coefficient | ||

| 3 | elasticity of having cash | ||

| 4 | elasticity of having CBDC | ||

| 5 | elasticity of having bank deposits | ||

| 6 | coefficient relates to Frisch elasticity of labor supply | ||

| 7 | relative utility weights or preference parameters of cash | ||

| 8 | relative utility weights or preference parameters of CBDC | ||

| 9 | relative utility weights or preference parameters of bank deposits | ||

| 10 | relative utility weights or preference parameters of labor time | ||

| 11 | degree of persistence in cash demand shock | ||

| 12 | degree of persistence in CBDC demand shock | ||

| 13 | depreciation rate of physical capital | ||

| 14 | elasticity of substitution between intermediate goods | 10 | |

| 15 | elasticity of output with respect to capital | ||

| 16 | degree of persistence in the supply shock | ||

| 17 | the portion of total wages borrowed from bank (strength of the cost channel) | ||

| 18 | probability of keeping the price fixed in the next period | ||

| 19 | probability of optimally determining the price | ||

| 20 | share of required reserves | ||

| 21 | constant interest elasticity of the supply of loan by the wholesale firm | ||

| 22 | constant interest elasticity of the supply of deposits by the household | ||

| 23 | fixed spread of bonds interest rate from central bank rate | ||

| 24 | fixed spread of CBDC interest rate from central bank rate | ||

| 25 | reaction intensity towards financial stress | ||

| 26 | interest rate smoothing parameter | ||

| 27 | steady state value of the policy interest rate | ||

| 28 | relative weights on inflation deviation | ||

| 29 | inflation target | ||

| 30 | relative weights on output gap | ||

| 31 | degree of persistence in the monetary policy shock | ||

| 32 | measure of nominal rigidity in the cash supply process | 1 | |

| 33 | measure of nominal rigidity in the CBDC supply process | 1 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Syarifuddin, F.; Bakhtiar, T. The Macroeconomic Effects of an Interest-Bearing CBDC: A DSGE Model. Mathematics 2022, 10, 1671. https://doi.org/10.3390/math10101671

Syarifuddin F, Bakhtiar T. The Macroeconomic Effects of an Interest-Bearing CBDC: A DSGE Model. Mathematics. 2022; 10(10):1671. https://doi.org/10.3390/math10101671

Chicago/Turabian StyleSyarifuddin, Ferry, and Toni Bakhtiar. 2022. "The Macroeconomic Effects of an Interest-Bearing CBDC: A DSGE Model" Mathematics 10, no. 10: 1671. https://doi.org/10.3390/math10101671

APA StyleSyarifuddin, F., & Bakhtiar, T. (2022). The Macroeconomic Effects of an Interest-Bearing CBDC: A DSGE Model. Mathematics, 10(10), 1671. https://doi.org/10.3390/math10101671